Sample Category Title

Dollar Fresh Acceleration after Upbeat US Retail Sales

The dollar extends recovery against the basket of major currencies on fresh acceleration after upbeat US retail sales data. The greenback received fresh boost from July retail sales overshoot which comes as continuation of bullish signals from Fed Dudley's hawkish comments on Monday.

Both work in favor of Fed normalization scenario supporters, who turn focus towards economic data as inflation showed no signs of rebounding in the near future.

The dollar index broke above previous high at 93.75 and dented psychological 94.00 barrier after data. The price is riding on the third wave (from 92.82 trough) of five-wave cycle from 92.37 (02 Aug low) which eyes strong barriers at 94.16 (daily Kijun-sen) and 94.21 (FE 100%) break of which is needed to validate wave principles and open way for further upside.

Next target lies at 94.55 (FE 123.6%) ahead of more significant double-Fibonacci barrier at 94.75 (FE 161.8% and Fibo 61.8% retracement of 96.24/92.37 downleg).

Strong bullish momentum is building up and supports further advance.

Broken daily Tenkan-sen (93.28) now acts as solid support and underpins the action.

Res: 94.16; 94.21; 94.55; 94.75

Sup: 93.76; 93.42; 93.28; 92.82

Market Update – European Session: UK July CPI Misses Expectations (2nd Straight Month)

Notes/Observations

- Concerns over North Korea subside further; risk appetite back on; Kim Jong Un examined KPA Strategic Force's plan for "enveloping fire" at Guam; discussed it with his commanding officers but decided he will "watch US's conduct a little more

- Germany Q2 GDP data robust, but QoQ reading was somewhat weaker than expected

- UK July CPI misses expectations (2nd straight month), dents hawks bid for potential near-term hike

- Swedish July CPI moves above Riksbank 2% target for 1st time since late 2010

- German Federal Constitutional Court has reservations about ECB QE bond purchases; seeks guidance from European Court of Justice

- Assumption Day holiday keeps participation light in Europe (Italy, Greece and Poland closed)

Overnight

Asia:

- China Commerce Ministry (MOFCOM): Hoped US could be 'prudent' in review of China's intellectual property (IP) policy; Would take steps if US takes actions that hurt bilateral trade relations

- RBA Minutes: Judged steady policy consistent with growth and inflation targets. Growth likely picked up pace in Q2 and saw GDP around 3% for both 2018 and 2019. Confident of a pick-up in inflation and jobs

Europe:

- UK Govt document to propose setting up an post-Brexit interim customs agreement with the EU to allow the freest possible trade of goods and seek the right to negotiate other trade deals

Americas:

- President Trump directs the USTR to study China's actions on theft of US intellectual property. US will enforce fair, reciprocal trade rules

- Fed's Dudley (voter, dove): Would support another 2017 rate hike if economy evolves as expected

- US Defense Sec Mattis: if North Korean missiles were considered to be a threat to Guam "then it's game on"

Economic Calendar

- (DE) Germany Q2 Preliminary GDP Q/Q: 0.6% v 0.7%e; Y/Y: 2.1% v 1.9%e; GDP NSA Y/Y: 0.8% v 0.6%e

- (CH) Swiss July Producer & Import Prices M/M: 0.0% v 0.0%e; Y/Y: -0.1% v 0.0%e

- (SE) Sweden July CPI M/M: 0.5% v 0.3%e; Y/Y: 2.2% v 1.9%e

- (SE) Sweden July CPI CPIF M/M: 0.6% v 0.4%e; Y/Y: 2.4% v 2.1%e; CPI Level: 323.69 v 323.16e

- (CN) China July M2 Money Supply Y/Y: 9.2% v 9.5%e v 9.4% prior; M1 Money Supply Y/Y: 15.3% v 14.0%e; M0 Money Supply Y/Y: 6.1% v 6.5%e

- (CN) China July New Yuan Loans (CNY): 825.5B v 800Be v 1.54T prior

- (CN) China July Aggregate Financing (CNY): 1.22T v 1.00Te

- (UK) July CPI M/M: -0.1% v 0.0%e; Y/Y: 2.6% v 2.7%e; CPI Core Y/Y: 2.4% v 2.5%e; CPIH Y/Y: % v 2.7%e

- (UK) July RPI M/M: 0.2% v 0.1%e; Y/Y: 3.6% v 3.5%e; RPI-X (Ex-Mortgage Interest Payment) Y/Y: 3.9% v 3.7%e; Retail Price Index: 272.9 v 272.5e

- (UK) July PPI Input M/M: 0.0% v 0.4%e; Y/Y: 6.5% v 6.9%e

- (UK) July PPI Output M/M: 0.1% v 0.0%e; Y/Y: 3.2% v 3.1%e

- (UK) July PPI Output Core M/M: 0.1% v 0.1%e; Y/Y: 2.4% v 2.5%e

- (UK) Jun House Price Index Y/Y: 4.9% v 4.3%e

**Fixed Income Issuance:

- (ID) Indonesia sold total IDR5.71T in 2-year, 4-year, 7-year and 15-year Project-based Sukuk (PBS)

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

**Equities**

Indices [Stoxx50 +0.1% at 3,460, FTSE +0.3% at 7,379, DAX +0.2% at 12,189, CAC-40 +0.3% at 5,139, IBEX-35 flat at 10,461, FTSE MIB +1.7% at 21,722, SMI -0.3% at 9,004, S&P 500 Futures +0.1%]

Market Focal Points/Key Themes: European stocks open higher and maintain position though; move higher attributed to easing of geopolitical tensions around Korea; macro data out of Germany also helped support equities; materials stocks outperforming along with healthcare; oil was largely flat, with the energy sector higher on Songa; Songa Offshore jumps after receiving takeover offer from Transocean; upcoming earnings in the US session include Home Depot, Coach and TJX Companies

Equities

- Consumer discretionary: Schibsted SCH.NO -6.5% (competition from facebook), Danone BN.FR 1.6% (activist stake)

- Materials: K+S SDF.DE -5.0% (earnings)

- Financials: Orascom Development ODHN.CH +6.3% (results)

- Telecom: TKH Group TK.NL -9.0% (results) - Healthcare: Nicox COX.NO -11.8% (financing update)

- Energy: Songa Offshore SONG.NO +30.3% (receives bid)

Speakers

- Brexit Min Davis: Negotiations with EU were going fine. Probably would not have to pay customs union in interim period following Brexit but likely to be lots of turbulence during talks. There would NOT be a number on the Brexit divorce bill by Oct. Probably will not have to pay customs union in interim period following Brexit ( transition would last a year or two). European Court of Justice (ECJ) would not be the arbiter of the interim customs deal with EU; to set - out proposals for details of post Brexit-ECJ jurisdiction during week of Aug 21st

- EU Commission took note of UK request for Brexit implementation period; would only address after sufficient progress on terms of withdrawal. Working on position paper on customs issues related to the orderly withdrawal of the UK. Friction-less trade was not possible outside single market

- German Constitutional Court sent a lawsuit targeting ECB QE program to European Court of Justice. Believed ECB QE might violate EU treaties but sought EU colleagues for help on issue

- South Africa Court scraped the grafts Ombudsman bid to alter SARB's mandate (**Note: Ombudsman instructed Parliament to begin a process to amend the constitution to make the SARB focus on socioeconomic well-being of its citizens rather than inflation)

- Iran President Rouhani: Could abandon the nuclear agreement within hours should US continue to impose new sanctions upon the country

- IEA Atkinson: OPEC might have to 'dig in' for long haul to curb supplies; US shale presents a big challenge. difficult to see price going beyond mid-$50 range

Currencies

- GBP was on soft footing heading into the UK CPI reading. The annual inflation did come in-line with expectations as falling oil prices offset higher prices for clothing and food. Overall the July inflation data undershot market expectations thus dealing another blow to expectations of a rate increase in the coming months. GBP/USD hit a 5-week low of 1.2910 following the data release. The GBP did find some supports as BOE previously noted that they expected annual inflation to accelerate later this year and still believed interest rates would need to rise more rapidly than investors expect to keep price rises in check.

- Some easing of tensions on the Korean Peninsula saw USD/JPY climb another 0.7% to test 110.40.

- SEK currency (Krona) was firmer in the session after Sweden's inflation print for July came in higher than forecast. The annual p[ace of 2.25 was above Riksbank target for 1st time in six years and raised the possible of a rate hike in early 2018. Dealers noted that Riksbank, would likely to wait until the ECB showed signs of QE tapering to speak about its own policy stance. In the past the Riksbank had been s concerned about an overly strong krona hampering inflation.

Fixed Income

- Bund futures trades at 164.06 down 2 ticks, paring opening losses as risk assets partially reverse earlier moves with stocks trimming gains and credit spreads edging wider. Downside targets 163.75 followed by 162.56. To the upside the 165.00 to 165.20 remains key resistance.

- Gilt futures trades at 127.59 down 24 ticks as UK inflation holds steady in July as price pressures ease. A resumption to the upside could eye 128.25 then 128.75. A move back below 126.51 targets 125.97

- Tuesday's liquidity report showed Monday's use of the marginal lending facility rose to €428M from €189M prior.

- Corporate issuance saw $2.65B come to market via 3 issuers headlined by Philip Morris $1.25B 2 part offering, and Lear Corp $750M senior unsecured note offering.

Looking Ahead

- (PE) Peru July Unemployment Rate: 7.0%e v 6.9% prior

- (PE) Peru Jun Economic Activity Index (Monthly GDP) Y/Y: 3.5%e v 3.4 % prior

- 05:30 (UK) Weekly John Lewis LFL sales data

- 05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

- 06:00 (IE) Ireland Jun Trade Balance: No est v €4.3B prior

- 06:00 (TR) Turkey to sell Floating rate 2024 bond

- 06:45 (US) Daily Libor Fixing

- 07:45 Weekly Chain store sales

- 08:00 (IS) Iceland July Unemployment Rate: No est v 1.8% prior

- 08:00 (BR) Brazil Jun Retail Sales M/M: No +0.4%e v -0.1% prior; Y/Y: 2.1%e v 2.4% prior

- 08:00 (BR) Brazil Jun Broad Retail Sales M/M: +1.8%e v -0.7% prior; Y/Y: 3.2%e v 4.5% prior

- 08:00 (UK) Baltic Dry Bulk Index

- 08:30 (US) July Import Price Index M/M: +0.1%e v -0.2% prior; Y/Y: 1.5%e v 1.5% prior; Import Price Index ex Petroleum M/M: 0.1%e v 0.1% prior

- 08:30 (US) July Export Price Index M/M: +0.2%e v -0.2% prior; Y/Y: No est v 0.6% prior

- 08:30 (US) Aug Empire Manufacturing: 10.0e v 9.8 prior

- 08:30 (US) July Advance Retail Sales M/M: +0.3%e v -0.2% prior; Retail Sales Ex Auto M/M: +0.3%e v -0.2% prior; Retail Sales Ex Auto and Gas: +0.4%e v -0.1% prior; Retail Sales Control Group: +0.4%e v -0.1% prior

- 08:55 (US) Weekly Redbook Same Store Sales data

- 09:00 (CA) Canada July Existing Home Sales M/M: No est v -6.7% prior

- 09:00 (EU) Weekly ECB Forex Reserve data

- 09:00 (RU) Russia announces weekly OFZ bond auction

- 09:30 (NZ) Fonterra Dairy Auction

- 10:00 (US) Aug NAHB Housing Market Index: 64e v 64 prior

- 10:00 (US) Jun Business Inventories: 0.4%e v 0.3 % prior

- 10:00 (MX) Mexico weekly International Reserves

- 11:30 (IL) Israel July CPI M/M: +0.1%e v -0.7% prior; Y/Y: -0.5%e v -0.2% prior

- 11:00 (BR) Brazil to sell 2022, 2026, 2035 and 2055 I/L bonds

- 11:30 (US) Treasury to sell 4-Week and 52-week Bills

- 12:00 (CO) Colombia Q2 GDP Q/Q: +0.5%e v -0.2% prior; Y/Y: 1.2%e v 1.1% prior

- 15:00 (CO) Colombia Jun Economic Activity Index (Monthly GDP) Y/Y: 1.2%e v 1.2% prior

- 16:00 (US) Jun Total Net TIC Flows: No est v $91.9B prior; Net Long-term TIC Flows: No est v $57.3B prior

- 16:30 (US) Weekly API Oil Inventories

Trade Idea Update: EUR/USD – Sell at 1.1755

EUR/USD - 1.1700

Original strategy :

Sell at 1.1770, Target: 1.1670, Stop: 1.1805

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1755, Target: 1.1655, Stop: 1.1790

Position : -

Target : -

Stop : -

Current selloff adds credence to our view that the rebound from 1.1689 (last week’s low) has ended at 1.1847 and a firm break below said support would extend recent decline from 1.1910 top to 1.1640-50 (50% Fibonacci retracement of 1.1370-1.1910 and previous support), below there would encourage for subsequent fall towards 1.1600-10 which is likely to hold from here due to near term oversold condition.

In view of this, we are looking to sell euro on recovery as 1.1755-60 should limit upside and bring another decline later. Above 1.1790-95 would abort and risk a stronger rebound to 1.1820 but price should falter below said resistance at 1.1847.

USD Extends Gains on Retail Sales Data

A rebound in retail sales in the US in July has triggered further gains in the US dollar on Tuesday, sending the greenback to its highest level in almost three weeks.

Retail sales have been very underwhelming this year which has contributed to the view that the economy isn't ready for another rate hike this year. The dollar was already relatively well bid heading into the release on the back of some hawkish comments from William Dudley on Monday and today's release is doing that no harm. Not only did the July numbers comfortably beat expectations but the June numbers were also revised higher, providing an additional boost for dollar bulls.

While today's report will likely increase the chances of another rate hike this year, it is still far from being priced in by the markets. The general trend of retail sales still remains worrying, despite the improvement over the last couple of months and 2% inflation still looks a pipe dream. That said, the dollar has been so heavily sold over the course of the year that even a slight unwinding of these trades could provide a near-term boost to the greenback. The dollar index has recently been languishing at levels seen only half a dozen times or so since the start of 2015 but not yet breached. With that in mind, it may take relatively little at the moment to get such a reaction in the dollar.

Trade Idea Update: USD/JPY – Buy at 110.20

USD/JPY - 110.80

Original strategy :

Exit short entered at 110.10

Position : - Short at 110.10

Target : -

Stop : -

New strategy :

Buy at 110.20, Target: 111.20, Stop: 109.85

Position : -

Target : -

Stop : -

As the greenback has maintained a firm undertone after breaking above resistance at 110.18, suggesting the rebound from 108.73 low is still in progress and gain to previous resistance at 111.05 cannot be ruled out, however, break there is needed to retain bullishness and extend this rise for a stronger correction of early decline to 111.25-30, however, near term overbought condition should prevent sharp move beyond previous resistance at 111.71, risk from there is seen for a retreat later.

In view of this, would not chase this rise here and would be prudent to buy dollar on pullback as 110.20 should limit downside. Only below previous resistance at 109.80 would abort and signal top is formed instead, bring weakness towards support at 109.42.

US Retail Sales Kick off the Second Half of the Year with a Bang, Rising 0.6% in July

Retail sales were up a robust 0.6% m/m in July, well ahead of consensus expectations for a 0.3% gain. The tally in June was also revised up, from a previously reported decline of 0.2% to an increase of 0.3%.

Excluding autos and gas, sales were up 0.5% in the month, atop a revised 0.3% gain in June (previously reported at -0.2%).

The 'control group' (excluding gas, autos, building materials, and food services) was also up 0.6% the month, with June revised up to +0.1% (from -0.1% previously).

By category, the biggest gains were in miscellaneous (+1.8%), non-store retailers (+1.3%), building materials (+1.2%), and departments stores (+1.0%). There were declines in electronics (-0.5%), gasoline stations (-0.4%), and clothing (-0.2%).

Key Implications

Given the headline print and the positive revisions, this report is much better than expected and suggests that the consumer is in much better shape heading into the third quarter of the year. This strong showing should be enough to push economic growth to around 3% (annualized) in the third quarter and implies somewhat stronger growth in the second quarter as well.

With continued job growth and gradually accelerating wages, there is good reason to expect consumers to continue to lead the economic outlook in the months ahead.

For the Federal Reserve, continued strength in real activity is balanced by ongoing weakness in inflation. This suggests a cautious approach to normalizing policy. The fed funds rate target is likely to remain steady in September, even as the Fed announces its plans to normalize its balance sheet. Today's strong report raises the odds of at least one more rate hike this year, likely in December.

U.S Retailers Post their Strongest Sales Growth for 2017

- U.S Retail Sales Jumped +0.6% in July

- U.S Jul Retail Sales (ex Auto) +0.5% m/m

- U.S Jun Retail Sales and Ex-Autos Revised to +0.1%

U.S retailers posted their strongest sales growth all year in July. Sales at retailers and restaurants jumped +0.6% from a month earlier, the biggest increase in eight months.

Ex-autos, retail sales rose +0.5% m/m. The market had been expecting a +0.4% jump in both categories.

Today's report emphasizes financial stability and rising confidence of the U.S consumer, who are benefiting from a number of factors – a prosperous stock market, low inflation, strong job growth and slow-but-steady wage gains.

Digging deeper, Internet sales drove last month's increase, with spending at non-store retailers growing +1.3% (up +11.5% y/y) the most since last December.

Note: Amazon's Prime Day, a popular day of discounts at the site was a big supporter.

Car sales jumped +1.2%, as did spending on building materials and garden equipment. Sales at furniture outlets, grocery stores, restaurants and department stores all rose healthily.

In contrast, spending on gasoline, electronics and clothing all fell. Overall retail sales have climbed +4.2% over the past year.

Other U.S data showed that weak import prices point to persistently low inflation

The U.S inflation picture does not look much stronger after today's report on import prices.

Import prices climbed +0.1% in July m/m and it was entirely due to higher fuel prices.

Prices for non-fuel imports fell -0.1%, dropping for the first time in seven months and matching the biggest drop in 13-months.

Today's report is the latest to show that U.S inflation pressures remain subdued, having weakened from earlier in the year.

Don't expect the odds for a Fed Dec. hike to tighten that much after this morning's print – current odds heading into this morning's reports were +42% for a Dec. hike.

USD finds a bid against G7 pairs (€1.1704, £1.2855, ¥110.75 and C$1.2788). U.S treasuries extend todays losses, backing up a further +2 bps to +2.275%.

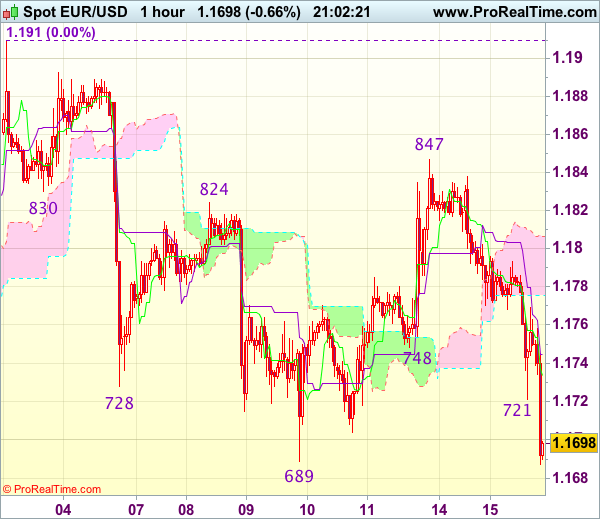

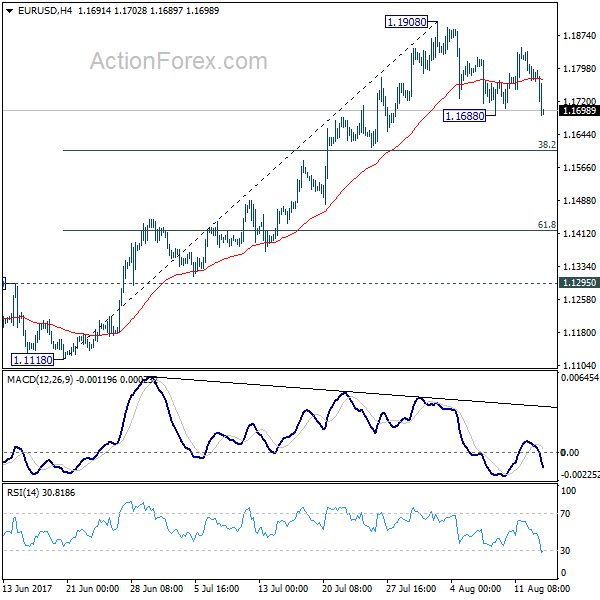

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1753; (P) 1.1796 (R1) 1.1822; More...

EUR/USD drops sharply in early US session but after all it's staying in consolidation from 1.1908. Break of 1.1688 will bring deeper pull back. But downside should be contained by 38.2% retracement of 1.1119 to 1.1908 at 1.1606 to bring rebound. On the upside, break of 1.1908 will extend recent up trend to 1.2042 long term support turned resistance next.

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained trading above 55 month EMA (now at 1.1768) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. But for now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

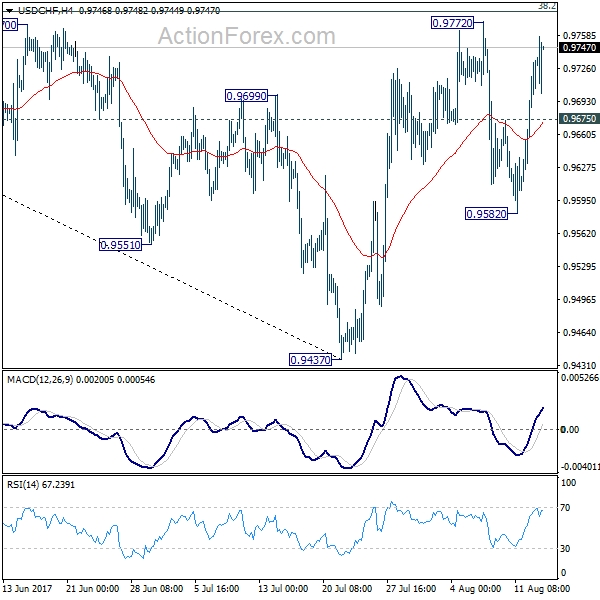

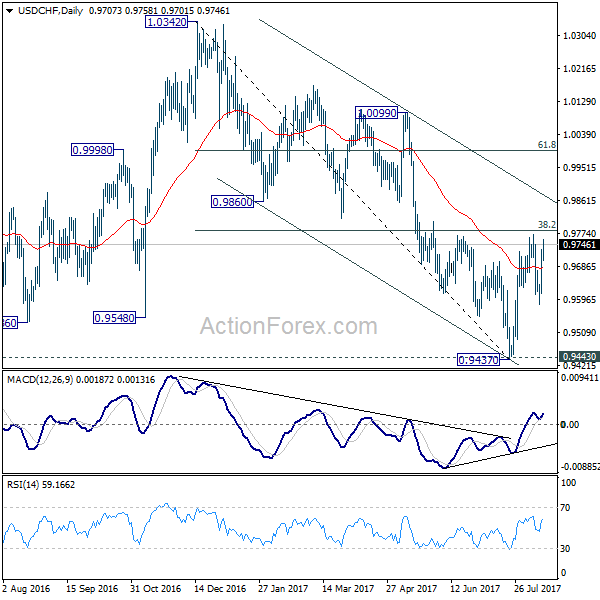

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9642; (P) 0.9687; (R1) 0.9765; More...

USD/CHF's rise from 0.9582 is still in progress and intraday bias remains on the upside for 0.9772 resistance. Decisive break there will revive the bullish case of reversal. That is, whole decline from 1.0342 has completed at 0.9437 after defending 0.9443 support. USD/CHF should then target channel resistance (now at 0.9880) next. On the downside, below 0.9675 minor support will turn intraday bias neutral first. Also, the pair is bounded inside medium term falling channel and limited below 38.2% retracement of 1.0342 to 0.9437 at 0.9783 for the moment. Break of 0.9582 will dampen our bullish view and turn bias back to the downside for 0.9437. This could also extend the fall from 1.0342 through 0.9437/43 key support level.

In the bigger picture, current development argues that USD/CHF has successfully defended 0.9443 key support level. And long term range trading in 0.9443/1.0342 is extending with another rise. At this point, there is no sign of an up trend yet. Hence, while further rise is expected in USD/CHF, we'll start to be cautious on loss of momentum above 61.8% retracement of 1.0342 to 0.9437 at 0.9996. However, firm break of 0.9443 will carry larger bearish implication and would target next key support at 0.9072.

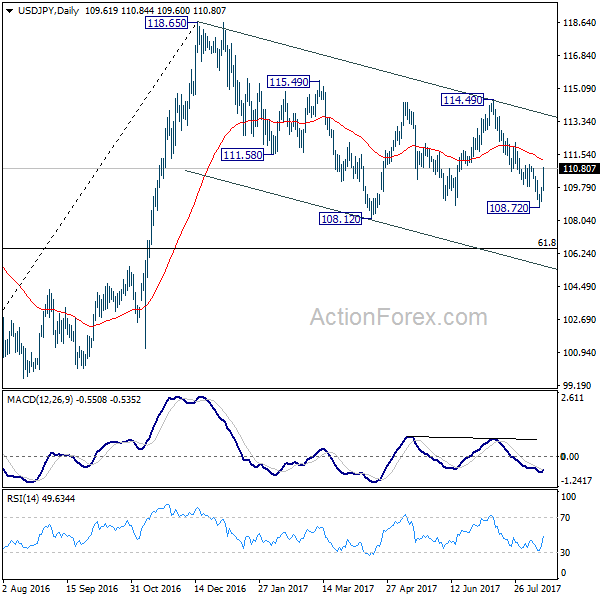

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.18; (P) 109.48; (R1) 109.95; More...

USD/JPY's rebound from 108.72 extends to as high as 110.78 so far. The break of 110.61 support turned resistance argues that decline form 114.49 is already completed at 108.72. Intraday bias is turned back to the upside for 112.18 resistance first. Break there will target 114.49 key near term resistance again. On the downside, break of 108.79 minor support will turn focus back to 108.72 instead.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, downside should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.