Sample Category Title

USD/JPY Daily Outlook

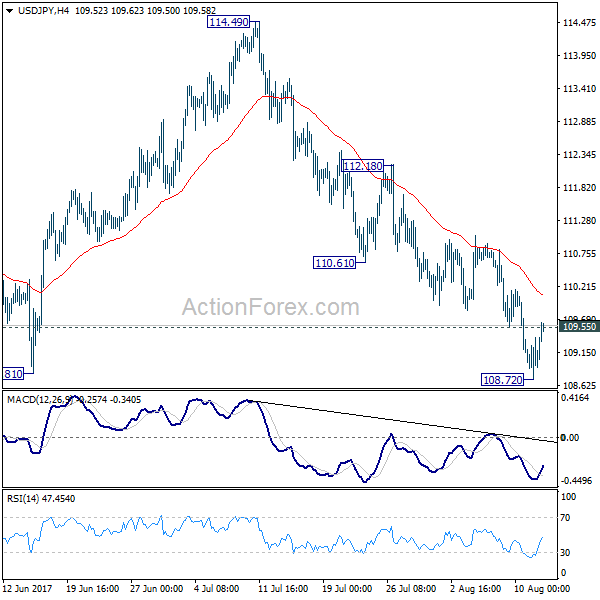

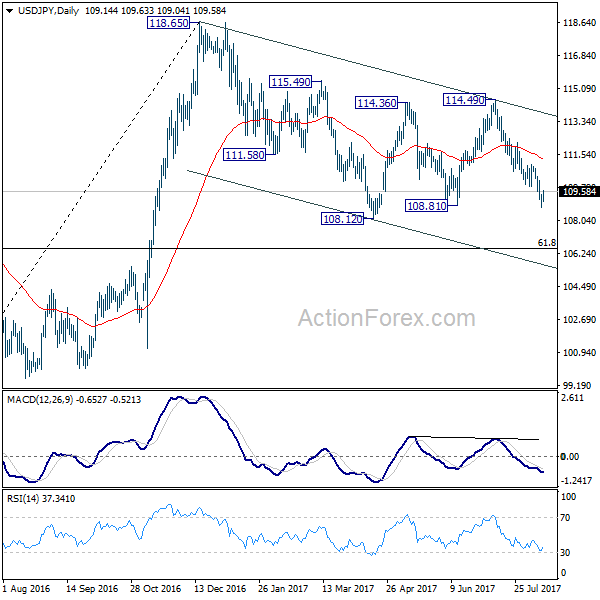

Daily Pivots: (S1) 108.78; (P) 109.09; (R1) 109.46; More...

USD/JPY's recovery and break of 109.55 minor resistance suggests temporary bottoming at 108.72. Intraday bias is turned neutral for consolidation first. Near term outlook remains bearish as long as 110.61 support turned resistance holds and deeper decline is expected. Firm break of 108.81 support will resume whole corrective fall from 118.65 and target 61.8% retracement of 98.97 to 118.65 at 106.48.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, downside should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

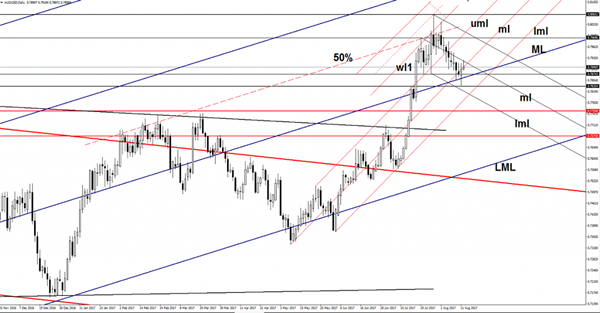

AUD/USD Struggling To Rebound

AUD/USD rebounded and tries to jump much higher after the false breakdown below the median line (ML) of the major ascending pitchfork. Could climb higher because has failed to close right on the ML, this scenario will happen only if the USDX will slide further on the short term.

Aussie increased even if the Chinese data have disappointed, the Industrial Production increased by 6.4%, less compared to the 7.1% estimate and versus the 7.6% growth in the former reading period, the Fixed Asset Investment increased only by 8.3% in July, less compared to the 8.6% estimate and versus the 8.6% in June. The Retail Sales rose by 10.4%, less compared to the 10.9% estimate and versus the 11.0% in the previous reading period.

AUD/USD found resistance at the median line of the minor descending pitchfork, now is pressuring the median line (ml) of the minor ascending pitchfork. A valid breakout above the mentioned levels will confirm a further increase.

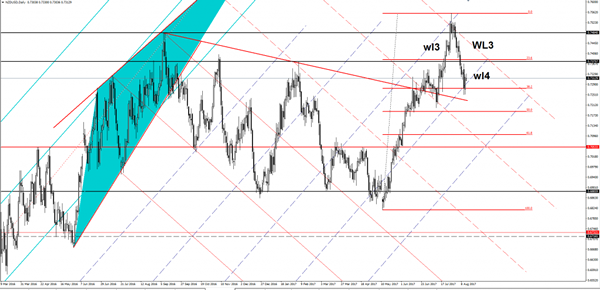

NZD/USD Throwback In Play

NZD/USD increased in the early morning and looks determined to climb much higher as the dollar index drops again. Price resumed the Friday’s bullish candle, will jump much higher in the upcoming days if the USDX will approach the 92.55 previous low.

USDX dropped again in the last three days and could move in range on the short term till will recapture more bullish energy to be able to start a broader rebound. Only an accumulation movement will signal a reversal, the greenback needs a bullish spark from the US economy these days, otherwise will drop further.

The increased on the positive economic data, the New Zealand Retail Sales rose by 2.0% in Q2, beating the 1.6% growth in Q1, while the Core Retail Sales by 2.1%, more compared to the 1.5% in the previous reporting period.

Price increased after the false breakdown below the confluence formed between the 38.2% retracement level with the fourth warning line (wl4) of the former ascending pitchfork. A retest of the wl4 will confirm a further increase towards the 23.6% retracement level.

Only a failure to climb above the mentioned static resistance will send the rate down again on the short term. I’ve said in the last weeks that the perspective will remain bullish as long as the rate is located above the warning line (wl4), so only a valid breakdown will confirm a larger drop in the upcoming weeks.

Market Update – Asian Session: Japan Registers Faster Than Expected GDP Growth In Prelim Q2

Asia Summary

Asian equity markets opened mixed before trending mostly higher. While regional focus over the weekend remained on North Korea and US trading threats, the Kospi traded higher the Won strengthened, ignoring the elephant in the room as usual. Japan reported stronger than expected Q2 preliminary GDP, with annualized GDP rising the fastest pace since Q1 2015. Notable subcomponent was private non-res investment (corporate CAPEX), 2.4% v 1.2%e. The yen continued to weaken in the session against the USD, A$ and Euro by 0.5-0.6%.

Focus then shifted to China July industrial production which came in lower than expected at 6.4% v 7.1E, coal, crude and power output all rose; while oil output fell. Retail sales were also a bit weaker at 10.4%. The PBOC again strengthened the yuan to the strongest setting since September 2016. While Trump had said he would delay investigation into China intellectual property theft as a sign of good faith on backing UN sanctions against North Korea, it is now expected he will launch the probe tomorrow.

Key economic data

(NZ) NEW ZEALAND Q2 RETAIL SALES (EX-INFLATION) Q/Q: 2.0% V 0.7%E; Y/Y: 5.4% V 4.2%E

(CN) CHINA JUL INDUSTRIAL PRODUCTION Y/Y: 6.4% V 7.1%E; YTD Y/Y: 6.8% V 6.9%E

(CN) CHINA JUL RETAIL SALES Y/Y: 10.4% V 10.8%E; YTD Y/Y: 10.4% V 10.5%E

(CN) CHINA JUL FIXED ASSETS EX RURAL YTD Y/Y: 8.3% V 8.6%E

(NZ) New Zealand Jul Performance Services Index: 56.0 v 58.6 prior

Speakers and Press

China/Hong Kong

(CN) China Stats Bureau (NBS): Overheated property market has cooled somewhat; China economy to continue steady operation in H2; Normal for H2 GDP to see a slow down

(CN) President Trump said to call on Trade Rep Lighthizer to announce a probe on China Monday, that will determine whether to investigate Chinese trade practices that force US firms operating in China to turn over intellectual property

(HK) Hong Kong Financial Services Chief Chan: No plan to ease anti-property cooling steps

Australia/New Zealand

(AU) RBA Assistant Gov Kent: Will be some time before RBA normalizes rates

Korea

(KR) White House: in teleconference President Trump and China President Xi Jinping reiterated mutual commitment to the denuclearization of the Korean peninsula

(KR) South Korea Finance Min Kim: Tensions with North Korea are impacting global market uncertainties; market sees current North Korea-US tension as more severe than in the past

Japan

(JP) Japan Econ Min Motegi: No change to view that Japan economy is in gradual recovery trend; not considering fresh stimulus steps

Asian Equity Indices/Futures (00:00ET)

Nikkei -0.7%, Hang Seng +1.2%, Shanghai Composite +0.4%, ASX200 +0.6%, Kospi +0.7%

Equity Futures: S&P500 +0.4%; Nasdaq100 +0.5%, Dax +0.5%, FTSE100 +0.4%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1835-1.1805; JPY 109.54-108.96; AUD 0.7919-0.7885; NZD 0.7331-0.7306

Dec Gold -0.1% at 1,293/oz; Sept Crude Oil +0.1% at $48.84/brl; Sept Copper -0.2% at $2.91/lb

(AU) Australia sells A$500M in 2028 bonds; avg yield 2.6464%; bid-to-cover 4.85x

USD/CNY *(CN) PBOC SETS YUAN REFERENCE RATE AT: 6.6601 V 6.6642 PRIOR (strongest setting since Sept 22, 2016)

(CN) China PBoC OMO injects CNY210B in v CNY130B prior in 7 and 14-day reverse repos

(KR) Bank of Korea (BOK) sells KRW1.06T v KRW1.1T offered in 1-yr monetary stabilization bonds; avg yield 1.52% v 1.47% prior

OLAM.SG Sees cocoa trading at $1,500-1,700/lb range; sees strong palm oil output recovery in Malaysia and Indonesia

Equities notable movers

Hong Kong/China

Yue Yuen Industrial, 551.HK Reports H1 Net profit $259M v $249M y/y, Rev $4.45B v $4.28B y/y; announces special dividend; +6.2%

Japan

Taikisha, 1979.JP Reports Q1 Net ¥265M v ¥791M y/y; Op ¥503M v ¥1.0B y/y; Rev ¥43.4B v ¥38.1B y/y; -10%

Cosmo Energy, 5021.JP Reports Q1 Net ¥4.7B v ¥4.8B y/y, Op ¥12.1B v ¥12.6B Rev ¥563.0B v ¥478.7B y/y; +13%

Nexon, 3659.JP Reports H1 Net ¥39.4B v ¥1.3B y/y, Op ¥56.0B v ¥17.1B Rev ¥121.9B v ¥95.6B y/y; +11%

Australia

Ansell, ANN.AU Reports FY17 Net profit $148M v $159M y/y; EBIT $217.8M v $230Me; Rev $1.60B v $1.57B y/y; -2.3%

JB Hi-Fi, JBH.AU Reports FY17 Net A$172.4M v A$191Me; Rev A$5.63B v A$5.6Be; -2.2%

South Korea

Korea Aerospace, 047810.KR Weakness attributed to North Korea tension; -5%

Will The Euro Remain Relatively Neutral In The Week Ahead?

Key Points:

- Euro rallies following weak U.S. CPI result.

- The EU GDP release is likely to be the key fundamental event for the coming week.

- Euro Dollar outlook remains neutral in the week ahead.

The Euro Dollar initially started the week under pressure as the U.S. JOLTS Job Openings came in above expectations but this sentiment quickly turned around in the face of increased risk from the North Korean crisis. Subsequently, the pair managed to find some support, as capital sought a safe haven away from the greenback, and rose to close the week higher at 1.1820 but it remains to be seen if the pair can remain buoyant in the week ahead.

The Euro Dollar initially started the week negatively following a relatively buoyant U.S. JOLTS Job Openings result of 6.16M as well as a slip in the German Industrial Production figures to -1.1%. However, the pair's prospects turned around rapidly in the face of increased geopolitical pressure from North Korea as the rhetoric ratcheted higher between Trump and Kym Jong Un. Subsequently, the markets largely took a risk-off approach and sentiment swung away from the greenback and into perceived safe havens. In addition, the broad bid was exacerbated by a range of disappointing U.S. economic data, including the Core CPI and PPI figures which fell to 0.1%, and -0.1%, respectively. Subsequently, the Euro benefitted from the change in sentiment and this saw the pair lift to close the week higher at 1.1820.

Looking ahead, the coming week is likely to contain some key fundamental events with the EU GDP and U.S. Philly Fed results due for release. In particular, the Annual EU GDP figures will be relatively illuminating given that the Eurozone economy has continued to firm of late and speculation is rampant over near term monetary policy changes. The GDP result is forecast at 2.1% y/y, but as always, this number could vary significantly. Additionally, the U.S. Philly Fed figures are due for release late in the week and, given the recent trend of poor economic data, could bring about some significant volatility for the pair if a miss is evident. Subsequently, keep a close watch over both events because they are likely to form the basis for the fundamental trend in the week ahead.

From a technical perspective, the pair's pullback from 1.1908 appears to have now largely ceased. However, with the key near term resistance point intact, our initial bias now turns to neutral until the 1.1908 high is broken. Any downside moves are likely to be contained by the 38.2% retracement level at 1.1606 and, subsequently, bring about a rebound but watch for sideways action in the week ahead. Support is currently in place for the pair at 1.1685, 1.1606, and 1.1478. Resistance exists on the upside at 1.1908, 1.1977, and 1.2179.

Ultimately, the Euro is likely to take its near term fundamental trend from the pending EU GDP figures and this will be a relatively critical event for the week. However, there is still plenty of geopolitical risk floating around with the ongoing North Korean crisis which could tip the scales at any stage.

Investors Looking For Havens On Escalating North Korea Tensions

The Dollar Index stays steady. The dollar index, which measures the greenback against a basket of six major currencies, held steady at 93.096, after slipping around 0.4 percent on Friday. Subdued U.S. inflation data released on Friday added to doubts as to whether the Fed would raise interest rates again this year, weighing on the dollar.

Investors Are Seeking For The Safe Haven Yen. The dollar edged higher against the yen on Monday, trading above last week's near 4-month low, with rising tensions between the United States and North Korea seen as the key to the near-term outlook. The dollar is now close to the bottom of a 108 yen to 115 yen range. If tensions escalate further, then there would be an increased risk of a drop to levels below 108 yen

Gold Is Totally Dependent On The North Korea Situation. Gold hovered near a two-month high, benefiting from the U.S.- North Korean tensions and Friday's weak U.S. inflation data. The dollar's recent weakness was also seen to be helping gold.

Geopolitical Risk Remains Despite Small Relief Rebound

- Traders relieved as weekend brings no further geopolitical risk;

- Yen slips despite very encouraging Q2 GDP data;

- Chinese data disappoints at the start of Q3.

Following the lead from Asia, European equity markets are poised to start the week on a positive note with sentiment buoyed by the absence of any escalation in the ongoing feud between the US and North Korea.

The war of words between the two countries weighed heavily on risk appetite for much of last week and despite today's bounce, it will continue to pose a threat in the days ahead. What we're seeing today is relief at the situation not deteriorating over the weekend, something traders were clearly wary of towards the end of last week.

Still, given the unpredictability of those involved, traders are likely to remain on edge and I don't think it will take much for the safe haven rush to resume. In the meantime, we're seeing a small unwinding of those risk aversion trades, with Gold trading slightly lower and the yen and Swiss franc off against the dollar, pound and euro.

The yen's losses come despite far better than expected second quarter GDP data being released overnight. A 1% quarter on quarter increase – 4% on an annualised basis – blew away expectations and was particularly encouraging as it was strongly driven by much better consumer spending and capital expenditure, both of which were double what was expected. If Japan can carry this momentum into the second half of the year, the Bank of Japan may be able to consider whether less accommodation is necessary, although as it stands, inflation still remain well below target.

The data out of China was far less encouraging, with retail sales, industrial production and fixed asset investment all falling well below expectations. The Chinese economy has expanded at a very good pace so far this year, spurred on by fiscal stimulus – which is expected to slow in the second half of the year – and external demand. These numbers are perhaps a reflection of what we can expect over the next couple of quarters, with infrastructure spending likely to cool. The most concerning aspect is probably retail sales for that reason, with this being seen as the area that's meant to fill the void.

Today is looking a little quiet on the data side which means traders will remain focused on geopolitical developments. There is a lot more data to come over the course of the rest of the week though so things will certainly pick up.

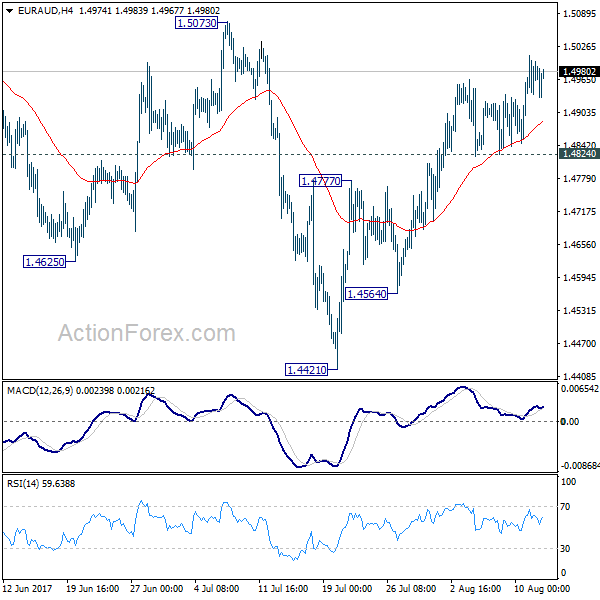

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4934; (P) 1.4972; (R1) 1.5007; More...

Intraday bias in EUR/AUD remains on the upside for 1.5073 resistance. Outlook is unchanged that correction from 1.5226 should have completed with three waves down to 1.4421 already. Firm break of 1.5073 will likely resume the rise from 1.3624 and target 61.8% projection of 1.3624 to 1.5226 from 1.4421 at 1.5411 next. On the downside, however, break of 1.4824 support will dampen our bullish view and turn bias back to the downside for 1.4564 support instead.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. The corrective structure of the fall from 1.5226 is affirming this view. Above 1.5226 will target a test on 1.6587 key resistance. However, another decline will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.9051; (P) 0.9084; (R1) 0.9118; More

Intraday bias in EUR/GBP remains on the upside for the moment. Current rise from 0.8312 is expected to target a test on 0.9304 high. At this point, there is no clear sign of up trend resumption yet. Hence, we'll be cautious on strong resistance from 0.9304 to limit upside and bring another fall. On the downside, considering bearish divergence condition in 4 hour MACD, break of 0.9007 support will indicate short term topping. Intraday bias will then be turned back to the downside for 0.8742/8948 support zone.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's uncertain whether it is finished yet. But in case of another fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes.

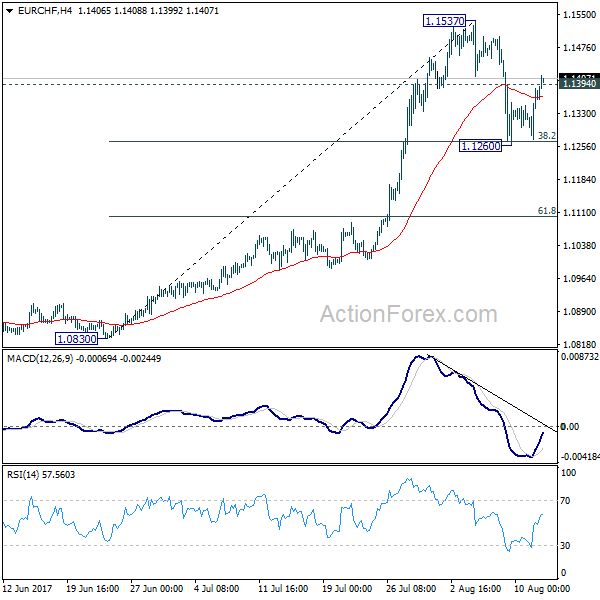

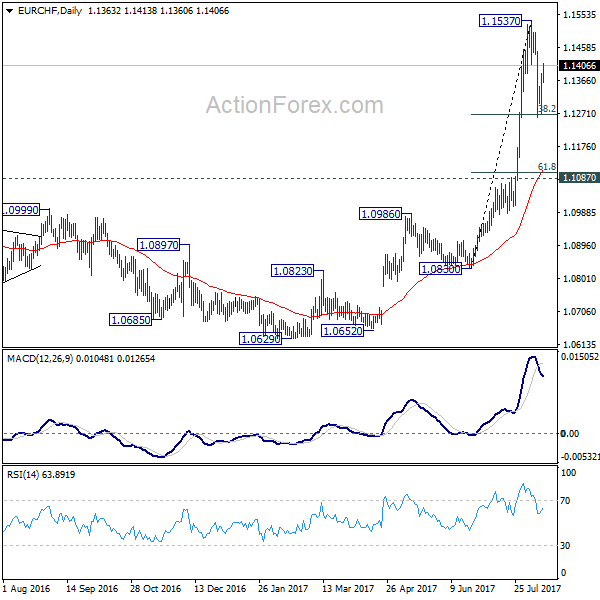

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1298; (P) 1.1342; (R1) 1.1411; More...

The break of 1.1394 minor resistance suggests that EUR/CHF's pull back from 1.1537 has completed at 1.1260. Strong support was seen as 38.2% retracement of 1.0830 to 1.1537 at 1.1267 as expected. Intraday bias is turned back to the upside for retesting 1.1537 high first. On the downside, however, firm break of 1.1267 will extend the fall and target 61.8% retracement at 1.1100.

In the bigger picture, firm break of 1.1198 key resistance confirms resumption of the long term rise from SNB spike low back in 2015. In this case, EUR/CHF would eventually head back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1087 resistance turned support holds.