Sample Category Title

Will The Bank Of England Disappoint?

Key Points:

- Inflation and Retail Sales slowing.

- Market has largely priced in the risk of hawkishness.

- Current risk profile is slanted to the downside.

The Bank of England's monetary policy committee is set to meet in the coming day to provide a decision that could prove relatively explosive for the Cable. Presently, the Cable is trading at around the 1 year high which suggests that the many within the market have already partially priced in the risk of hawkishness from the central bank. However, the question remains if the central bank will simply disappoint the wider market with a less than robust decision.

To review the current facts, the BoE met last month and surprised the market with a 5-3 vote to not raise the official bank rate. The risk of additional dissenting votes had largely not been reflected in the positioning ahead of the decision and the Cable suddenly took a bullish direction. What was particularly illuminating was Carney's statements following the event which suggested that the central bank would considering the rising inflationary pressures over the next few months. Subsequently, speculation has been rampant that the BoE is preparing to take lay out a plan for monetary tightening at the coming meeting.

However, the market could be in for some disappointment as the UK retail spending, and inflation figures, have not been particularly robust over the past month coming in at 0.6%, and 0.0%, respectively (M/M). Whether this becomes a trend or is simply an anomaly within the data will remain to be seen but it certainly complicates the central bank's looming decision. Subsequently, there is currently a disconnect between what the market is largely pricing in and the underlying economic data that the central bank is likely to make their decision upon.

Ultimately, the most likely scenario for the coming meeting is that the official bank rate will remain on hold at 0.25% and that the central bank will take a “data dependent” view moving forward. In fact, I expect that the present vote divide of 5-3 is likely to remain in play. It's clear that the bank will need to normalise policy at some stage this year but the coming MPC isn't likely to be it. However, the impact on the Cable could be relatively negative given that the market is pricing in some fairly sharp hawkishness, if not a hike, from the decision. Subsequently, keep a close watch on the Cable because the downside could be beckoning in the wake of the decision.

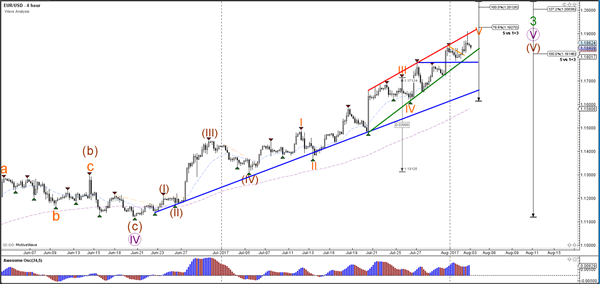

Daily Technical Analysis: EUR/USD Bullish Trend Reaches First Target At 1.1925

Currency pair EUR/USD

The EUR/USD has reached yesterday's first target at 1.1925. A continuation towards 1.20 is possible if price stays above the support trend lines (green/blue).

The EUR/USD completed an ending diagonal within the 5th wave (purple). The current bearish retracement could be part of a wave 4 (grey) if price manages to stay above the 50% Fibonacci level which is the invalidation spot for this wave structure.

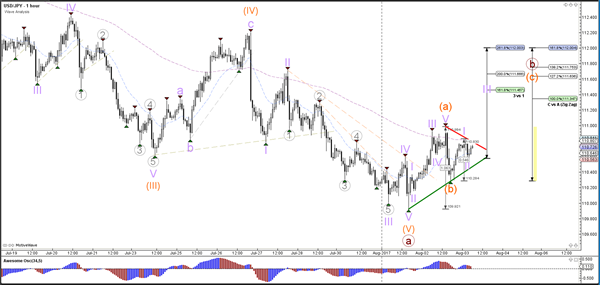

Currency pair USD/JPY

The USD/JPY failed to break the bottom and round level at 110, which was expected in yesterday's analysis due to the potential unfolding of an ABC zigzag pattern within wave B (brown). A bullish breakout above resistance (red) could signal the start of wave C (orange).

The USD/JPY potential breakout above resistance (red) could see a continuation towards the Fibonacci targets of wave 3 (purple) vs 1.

Currency pair GBP/USD

The GBP/USD did not manage as yet to break above the 1.3250 quarter level and is now building a correction. Whether the wave 3 (blue) will indeed be confirmed depends on how far the GBP/USD will move. A failure to break above the 100% Fibonacci target could indicate an ABC rather than a 123.

The GBP/USD could be building an extension of the wave 3 (green) with 5 internal waves (orange/purple). A pullback could be part of the wave 4 (purple) which means that the Fibonacci levels of wave 4 vs 3 could act as support.

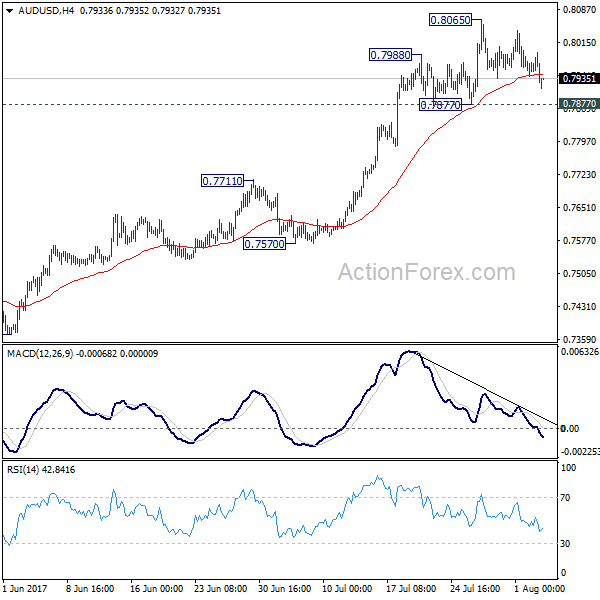

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7941; (P) 0.7967; (R1) 0.7992; More...

Intraday bias in AUD/USD remains neutral as consolidation from 0.8065 extends. Further rise is in favor with 0.7877 support intact. Break of 0.8065 will target 100% projection of 0.6826 to 0.7833 from 0.7328 at 0.8335. Nonetheless, break of 0.7877 will indicate short term topping, possibly with bearish divergence condition in 4 hour MACD. In such case, intraday bias will be turned back to the downside for 0.7711 resistance turned support.

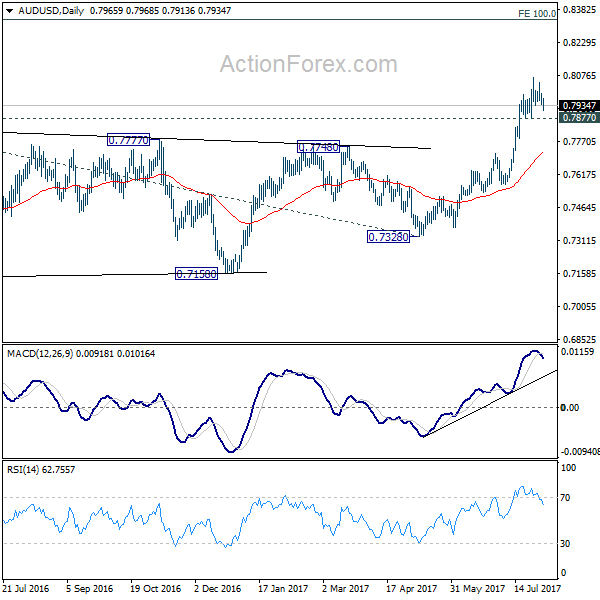

In the bigger picture, current development suggests that rebound from 0.6826 is developing into a medium term rise. There is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, further rise is now expected to 55 month EMA (now at 0.8100) or even further to 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now expected.

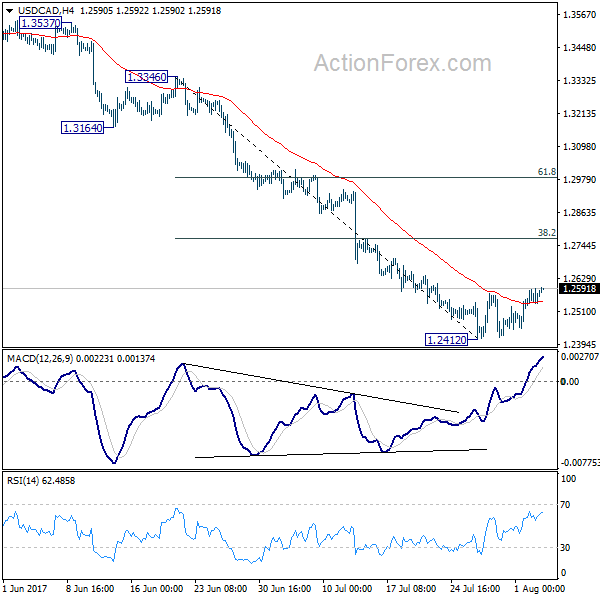

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2536; (P) 1.2564; (R1) 1.2597; More....

Intraday bias in USD/CAD remains mildly on the upside as correction from 1.2412 short term bottom continues. Further rise would be seen to 38.2% retracement of 1.3346 to 1.2412 at 1.2769. At this point, we'd expect upside to be limited there to bring fall resumption. On the downside, break of 1.2412 will extend recent fall from 1.3793 to next key fibonacci level at 1.2048.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. Fall from 1.3793 is seen as the third leg and should target 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. However, firm break there will target 100% projection of 1.4689 to 1.2460 from 1.3793 at 1.1564.

European Open Briefing: Risk Appetite Decreased Overnight

Global Markets:

- Asian stock markets: Nikkei and Hang Seng both down 0.20 %, Shanghai Composite lost 0.25 %, ASX 200 fell 0.40 %

- Commodities: Gold at $1261 (-0.85 %), Silver at $16.51 (-1.35 %), WTI Oil at $49.45 (-0.30 %), Brent Oil at $52.20 (-0.35 %)

- Rates: US 10-year yield at 2.26, UK 10-year yield at 1.23, German 10-year yield at 0.49

News & Data:

- China Caixin PMI Services Jul: 51.5 (Prev 51.6)

- China Caixin PMI Composite Jul: 51.9 (Prev 51.1)

- Australia Trade Balance (AUD) Jul: 856m (Est 1.8B Prev 2.47B)

- New Zealand ANZ Commodity Price Jul: -0.80% (Prev 2.10%)

- Japan Nikkei PMI Composite Jul: 51.8 (Prev 52.9)

- Japan Nikkei PMI Services Jul: 52 (Prev 53.3)

- Fed's Williams: Maybe 1 More Rate Hike In 2017, 3 More In 2018 Appropriate

- Fed's Williams: USD Decline Isn't a Big Factor in Inflation Outlook

- PBoC Fixes USDCNY Reference Rate At 6.7211(Prev 6.7205)

Markets Update:

Risk appetite decreased overnight following worse than expected Chinese economic data. Asian stock markets came under pressure, along with risk currencies such as the Aussie and New Zealand Dollar.

AUD/USD fell from 0.7970 to 0.7915 overnight. Support is now seen at 0.7880 and stronger at 0.7830. The outlook is still positive, and the Aussie is likely to run into decent demand below 0.79.

Meanwhile, NZD/USD fell below 0.74. The weak employment numbers from Tuesday have brought the currency under pressure. However, it should find good support around 0.7330.

USD/JPY is holding surprisingly well given the risk-off bias. The pair traded only briefly below 110 yesterday, and managed to bounce back to 110.90. While the outlook is still negative, USD/JPY is showing a lot of resilience given the broad Dollar weakness elsewhere. A break back above 111.30 resistance would signal that the recovery could extend to 112.

The Euro remains strong. While the charts suggest EUR/USD is heavily overbought in the short-term, it is not showing any signs of a reversal yet. There is little resistance until 1.20 now, and the pair is likely to test that level soon.

Upcoming Events:

- 08:45 BST – Italian Services PMI

- 08:50 BST – French Services PMI

- 08:55 BST – German Services PMI

- 09:00 BST – Euro Zone Services PMI

- 09:30 BST – UK Services PMI

- 10:00 BST – Euro Zone Retail Sales

- 12:00 BST – Bank of England Rate Decision

- 15:00 BST – US ISM Services PMI

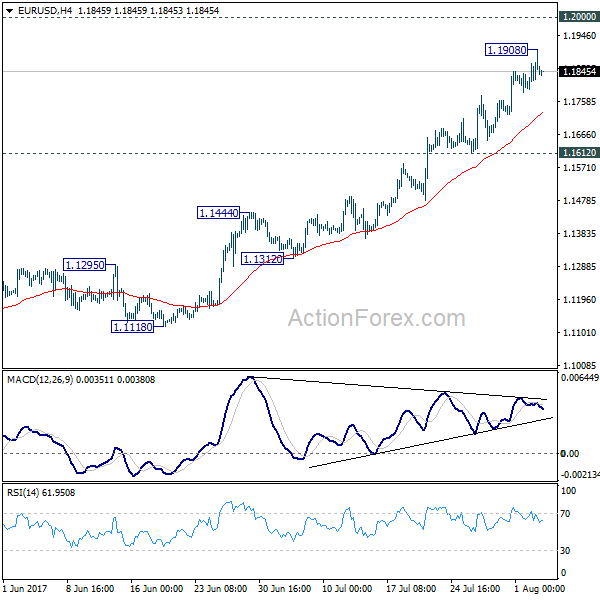

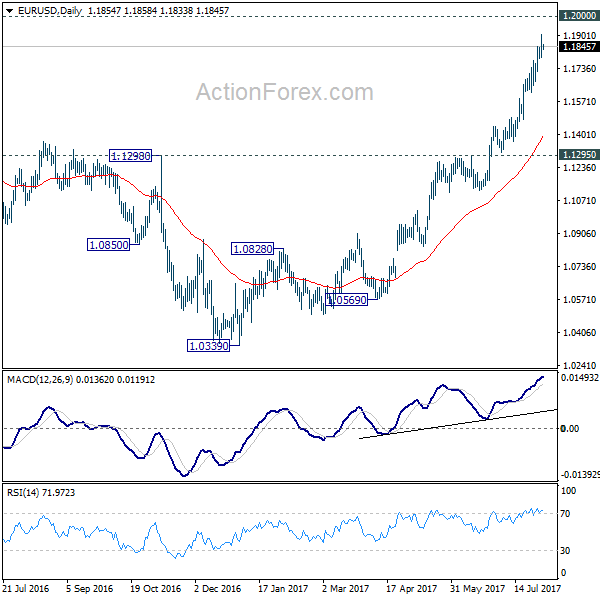

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1795; (P) 1.1853 (R1) 1.1912; More...

A temporary top is in place at 1.1908 in EUR/USD. Intraday bias is turned neutral first. Another rise is expected as long as 1.1612 support holds. Above 1.1908 will target 1.2 psychological level. Considering bearish divergence condition in 4 hour MACD, we'll be cautious on topping around there to bring correction. On the downside, break of 1.1612 will indicate short term topping and bring deeper pull back to 55 day EMA (now at 1.1379).

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained break of 55 month EMA (now at 1.1760) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. But for now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

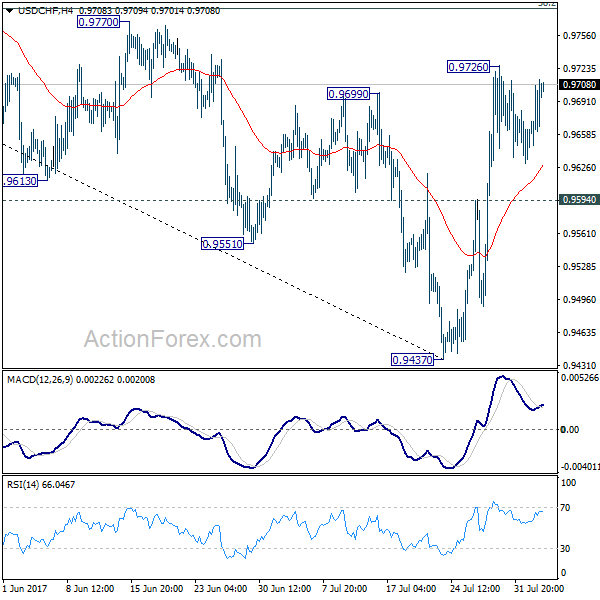

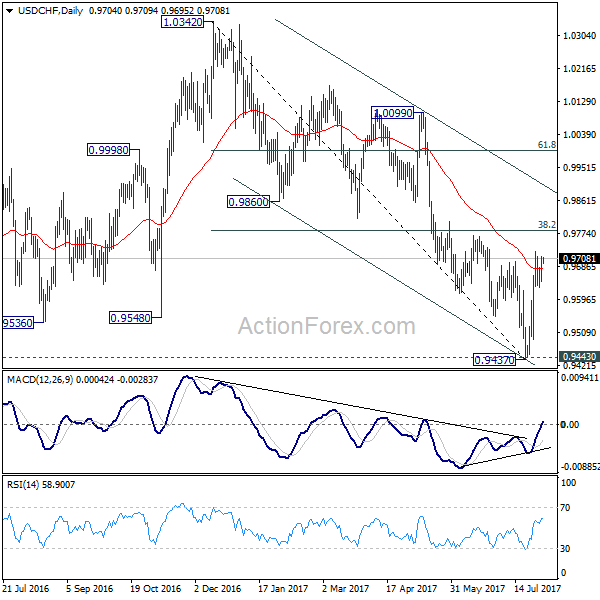

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9664; (P) 0.9689; (R1) 0.9735; More...

USD/CHF is still staying in consolidation below 0.9726. Intraday bias remains neutral at this point. Another rise is expected as long as 0.9594 support holds. Prior break of 0.9699 resistance suggests near term reversal after defending 0.9443 key support. Above 0.9726 will target 38.2% retracement of 1.0342 to 0.9437 at 0.9783 first. Break will target channel resistance (now at 0.9899). However, firm break of 0.9594 will dampen this bullish view and turn bias back to the downside for 0.9437.

In the bigger picture, current development argues that USD/CHF has successfully defended 0.9443 key support level. And long term range trading in 0.9443/1.0342 is extending with another rise. At this point, there is no sign of an up trend yet. Hence, while further rise is expected in USD/CHF, we'll start to be cautious on loss of momentum above 61.8% retracement of 1.0342 to 0.9437 at 0.9996.

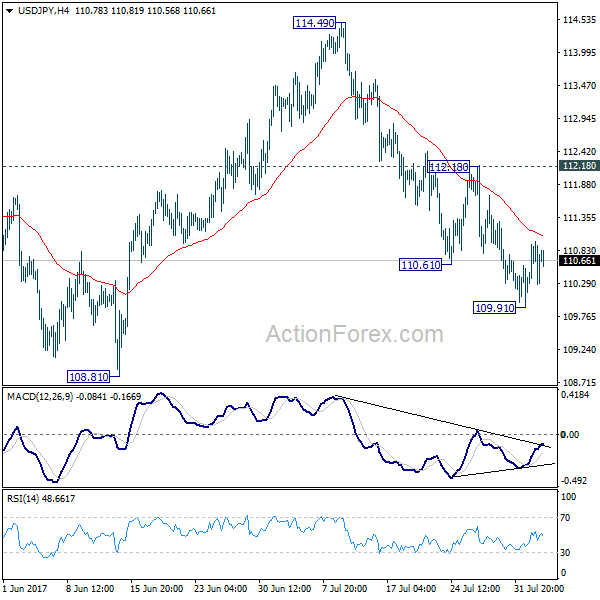

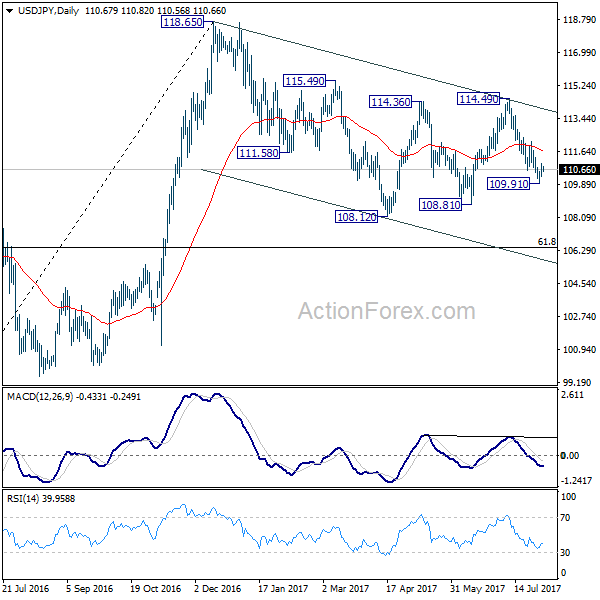

USD/JPY Daily Outlook

Daily Pivots: (S1) 110.33; (P) 110.66; (R1) 111.06; More....

USD/JPY is staying in consolidation above 109.91 and intraday bias remains neutral for the moment. As long as 112.18 remains intact, outlook stays bearish for deeper fall. Below 109.91 will target 108.81 support first. Break there will resume whole correction from 118.65 and target 61.8% retracement of 98.97 to 118.65 at 106.48. Nonetheless, break of 112.18 resistance will dampen our bearish view and turn focus back to 114.49 resistance instead.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, down side should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

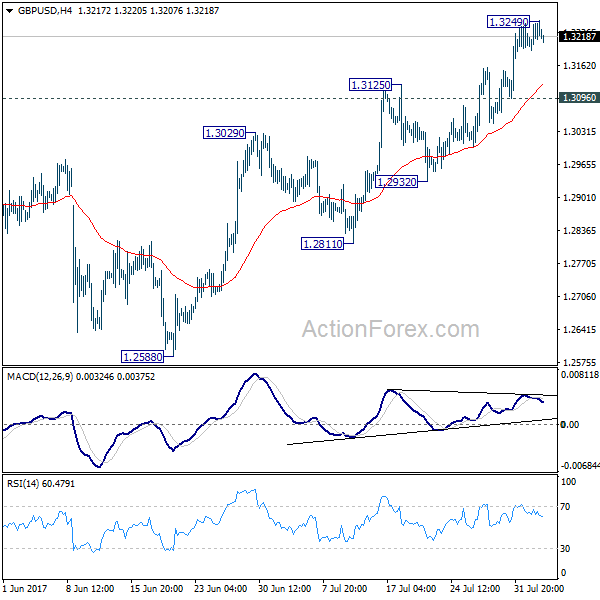

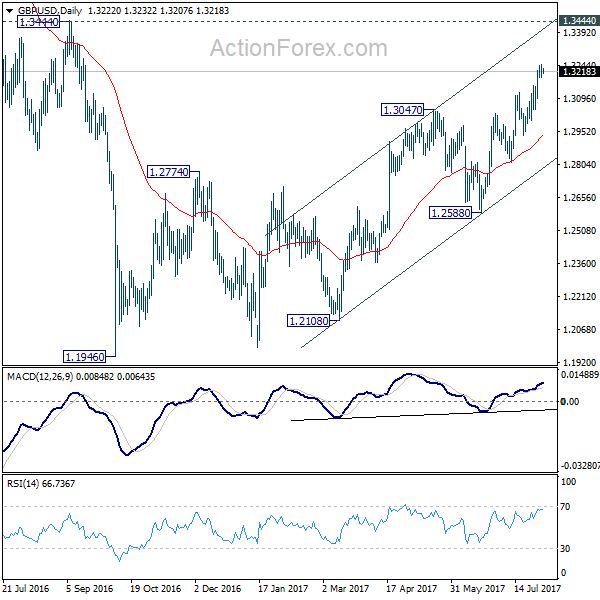

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3191; (P) 1.3221; (R1) 1.3252; More...

GBP/USD lost some momentum after hitting 1.3249. Intraday bias is turned neutral for some consolidations first. Further rally is expected as long as 1.3096 minor support holds. Above 1.3249 will target 1.3444 key resistance. But still, price actions from 1.1946 are viewed as a corrective pattern. Hence, we'll look for topping signal again around 1.3444. Meanwhile, break of 1.3096 will be the first sign of reversal. Intraday bias will be turned back to 1.2932 support first in that case.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is expected, larger outlook remains bearish as long as 1.3444 key resistance holds. Down trend from 1.7190 (2014 high) is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

Sterling Staying Firm ahead of BoE Super Thursday, Votes and Projections the Keys

Sterling is trading as the second strongest currency for the week so far, next to Euro, as markets await BoE Super Thursday. While monetary is widely expected to be unchanged, the vote split and inflation report will catch all attention from the markets. Meanwhile, commodity currencies are generally lower even though risk appetite remains firm in the stock markets. DOW extended its record run and closed up 0.24% at 2201.24, above 22k handle. US treasury yields were mixed with 10 year yield closed up 0.011 at 2.262. In other markets, Gold dipped notably and is trading below 1270. WTI crude oil recovered after a steep dip earlier this week to below 48.50. WTI is currently trading at 49.4 and struggles to regain 50 handle.

BoE vote split and projections watched

BoE is widely expected to keep monetary policy unchanged today. The Bank rate should be held at 0.25% with the asset purchase target kept at GBP 435B. The vote split and updated economic forecast from the quarterly inflation report will be the main focuses. Normally, there are nine voting members in the MPC but i was lowered to eight earlier this year after Charlotte Hogg resigned. Kristin Forbes was the most hawkish one and started voting for a hike since March. After two meetings, Michael Saunders and Ian McCafferty joined last month to make the the vote 5-3 to kept interest rate unchanged. That was at a time when inflation in UK was still accelerating. Chief economist Andy Haldane then expressed his hawkish comments on interest rate and BoE Governor Mark Carney then said that there will be rate hike debates soon.

However, the situation have changed since then. CPI slowed back sharply from 2.9% yoy to 2.6% yoy in June. Q2 growth was sluggish at 0.3% qoq. And speculations on a rate hike cooled. It's unlikely that Haldane with vote for a hike this time. The most hawkish one, Forbes, has left the MPC already in June. Her replacement Silvana Tenreyro is seen as generally on the dovish side. That makes a 6-2 vote split the base case for this meeting. And the outcome will be rather dovish should either Saunders or McCafferty change their mind.

IMF recently downgraded UK growth forecast after a weak Q1. IMF now expects UK economy to growth 1.7% this year, notably lower than 2.0% projection back in April. BoE's own projections might follow with a downgrade in the quarterly inflation report today. On the other hand, if inflation forecast could be kept unchanged, it will indicate that policymakers still believe that the spike in CPI earlier this year was temporary. And that will reduce the chance of a rush to rate hike in near term.

Fed officials support balance sheet reduction this fall

San Francisco Fed President John Williams said that the September FOMC meeting seems "an appropriate time" to start shrinking the USD 4.5T balance sheet. He noted that the economy has "fully recovered" from the financial crisis and inflation will reach 2% target "in the next year or two". Boston Fed President Eric Rosengren also said that "there's no reason to have that extraordinary accommodation coming from the balance sheet any longer." Cleveland Fed President Loretta Mester said that Fed should continue to gradual approach of stimulus removal even with fluctuation in economic data. She emphasized the "benefits to this consistency" and it "removes some ambiguity" and underscores that policy focuses on "medium-run outlook". On the other hand, St. Louis Fed President James Bullard said that inflation outlook "has deteriorated in 2017" and "I would not support further moves in the near term." And for now, Bullard believed that "we should remain on pause."

US-China relations turns sour

On the geopolitical front, US President Donald Trump has become less patient over China's actions, of lack of actions, towards North Korea, a hermit kingdom that has been growing provocative with it missile tests. Trump and China's President Xi Jinping agreed back in May that the latter would increase diplomatic and economic pressure over North Korea, in an attempt to denuclearize the country. However, little effect has been seen so far and North Korea even had two successful tests of ICBM missile over the past month. A CNN report revealed that revised military options for North Korea have been prepared by the US though diplomatic engagement is still preferred.

US-China trade relations have soured since July and it was reported that the US has been preparing broad trade case against China. We believe the triggering point is China's reluctance to confront North Korea over nuclear weapons. Indeed, Trump, since his inauguration in January, has linked US-China trade relations to the North Korean problem. Staying in Asia, China claims India pulled out most troops from Doklam in India and Donglang in China, the tri-junction border shared by China, India, and Bhutan. The standoff has entered its seventh week and neither side appears ready for a war or a compromise.

On the data front

Australia trade surplus narrowed to 0.86b in June. New Zealand ANZ commodity price dropped -0.8% in July. China Caixin PMI services dropped 0.1 to 51.5 in July. Looking ahead, BoE rate decision will be the main focus in European session. In addition, UK will release PMI services. ECB will also release monthly bulletin while Eurozone will release PMI services final. In US session, ISM services will be the main focus will jobless claims and factory orders will also be featured.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3191; (P) 1.3221; (R1) 1.3252; More...

GBP/USD lost some momentum after hitting 1.3249. Intraday bias is turned neutral for some consolidations first. Further rally is expected as long as 1.3096 minor support holds. Above 1.3249 will target 1.3444 key resistance. But still, price actions from 1.1946 are viewed as a corrective pattern. Hence, we'll look for topping signal again around 1.3444. Meanwhile, break of 1.3096 will be the first sign of reversal. Intraday bias will be turned back to 1.2932 support first in that case.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is expected, larger outlook remains bearish as long as 1.3444 key resistance holds. Down trend from 1.7190 (2014 high) is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:00 | NZD | ANZ Commodity Price Jul | -0.80% | 2.10% | ||

| 1:30 | AUD | Trade Balance (AUD) Jun | 0.86B | 1.77B | 2.47B | 2.02B |

| 1:45 | CNY | Caixin China PMI Services Jul | 51.5 | 51.9 | 51.6 | |

| 7:45 | EUR | Italy Services PMI Jul | 54.1 | 53.6 | ||

| 7:50 | EUR | France Services PMI Jul F | 55.9 | 55.9 | ||

| 7:55 | EUR | Germany Services PMI Jul F | 53.5 | 53.5 | ||

| 8:00 | EUR | ECB Economic Bulletin | ||||

| 8:00 | EUR | Eurozone Services PMI Jul F | 55.4 | 55.4 | ||

| 8:30 | GBP | Services PMI Jul | 53.6 | 53.4 | ||

| 9:00 | EUR | Eurozone Retail Sales M/M Jun | 0.00% | 0.40% | ||

| 9:00 | EUR | Eurozone Retail Sales Y/Y Jun | 2.50% | 2.60% | ||

| 11:00 | GBP | BoE Rate Decision | 0.25% | 0.25% | ||

| 11:00 | GBP | BoE Asset Purchase Target | 435B | 435B | ||

| 11:00 | GBP | MPC Official Bank Rate Votes | 2--0--6 | 3--0--5 | ||

| 11:00 | GBP | MPC Asset Purchase Facility Votes | 0--0--8 | 0--0--8 | ||

| 11:00 | GBP | BoE Inflation Report | ||||

| 11:30 | USD | Challenger Job Cuts Y/Y Jul | -19.30% | |||

| 12:30 | USD | Initial Jobless Claims (JUL 29) | 242K | 244K | ||

| 14:00 | USD | ISM Non-Manufacturing Composite Jul | 56.9 | 57.4 | ||

| 14:00 | USD | Factory Orders Jun | 2.80% | -0.80% | ||

| 14:30 | USD | Natural Gas Storage | 17B |