Sample Category Title

Japan’s nominal wage gains hit 3% in Nov, but inflation erodes real earnings

Japan’s real wages fell by -0.3% yoy in November, marking the fourth consecutive monthly decline as wage growth failed to outpace inflation again.

While nominal wages rose by a robust 3.0% yoy—beating expectations of 2.7% yoy and extending a 35-month streak of growth—consumer prices grew at an even faster pace of 3.4% yoy during the same period, up from 2.6% yoy in October.

A notable highlight in the data was the sharp rise in special cash earnings, including bonuses, which surged by 7.9% yoy. Excluding bonuses and nonscheduled payments, average wages increased by 2.7% yoy, the fastest rate in 32 years, suggesting some underlying improvement in base wages.

Markets Took Aim at UK Assets

Markets

Markets took aim at UK assets. Both gilts and sterling suffered steep losses. Yields soared another 4.5-11.3 bps. The 10-yr yield (+11.3 bps to 4.79%) surpassed the previous post-pandemic highs to hit the highest levels since ’08. The 30-yr yield already smashed Tuesday’s 27-yr high by adding another 10.9 bps to 5.35%. Such underperformance at the long end of the curve reveals fiscal and inflation risks are the driving force. This has been the case ever since UK Chancellor Reeves’ presented her extremely loose fiscal plans in October. Because of the material yield increase, the UK risks breaching its self-imposed fiscal rules when the OBR (UK’s budget watchdog) releases new forecasts March 26. If that were to be the case, Bloomberg reported citing people familiar that Reeves would resort to spending cuts rather than impose new taxes. The ones proposed in the October budget have already caused a corporate backlash and dented sentiment. Higher risk premia explain why the pound fails to profit from otherwise juicy rates. EUR/GBP shot up from 0.828 towards 0.835 and is extending gains in Asian trading this morning. Rates in Europe climbed higher as well. Germany added between 0.5 and 6.6 bps. Its 10-yr yield hit a 7-month high north of 2.5%. US rates were little changed on the day with moves varying between -0.8 bps and +1.8 bps. Lower than expected weekly jobless claims contrasted with the ADP job report undershooting consensus. The closely watched 30-yr auction went smooth. The minutes of the hawkish Fed’s December policy meeting carried a similar tone. They triggered little intraday volatility. The dollar appreciated against most majors. EUR/USD closed around 1.032, down from 1.034 but off intraday lows. USD/JPY isn’t planning to leave the 158 big figure anytime soon, despite the verbal warnings over the last couple of days from Japanese officials. USD/CNY (7.331) continues to grind higher with the 2023 multi-year high (7.35) ever coming closer. GBP/USD (cable) underperformed and is currently testing April 2024 support at 1.23. The general trend of a strong(er) USD and higher core bond yields is obvious. It could take a breather today though given the empty economic calendar, proximity of important resistance levels and the partial absence of US investors. US stock markets are closed and its bond markets leave early due to a national day of mourning for ex-president Carter.

News & Views

China December inflation data published this morning showed that deflationary tendencies remain in place despite multiple government efforts to revive domestic demand. CPI inflation was unchanged in November (0.0% m/m), lowering the y/y measure from 0.2% to 0.1%. Goods prices declined 0.2% Y/Y, services inflation rose slightly (0.4% from 0.5%). Core inflation (ex food and energy) also rose slightly from 0.3% Y/Y to 0.4%. Factory gate prices (PPI) remain negative for the 27th consecutive month at -2.3 Y/Y (from -2.5% in November). The ‘rise’ in core inflation and the slowdown in producer price deflation might be a first indication that support measures have some stabilization effect, but there is still a long way to go to restart a protracted reflation spiral. At 1.61%, China’s 10-yr government bond yields stabilizes near record low levels. Ongoing low inflation justifies a weak currency, but the PBOC continues to take action for this process to develop in an orderly fashion. At USD/CNY 7.331, the onshore yuan trades near its 2023 low against the dollar. The PBOC this morning announced the launch of a 60 bln yuan sale of 6-month bills in Hong Kong to increase demand for the offshore currency.

Permanent placements and vacancies fell at accelerated rates in December, the KPMG and REC UK report on jobs revealed. Firms were reported to be further considering the employment cost implications of the late October government Budget, and as such placements fell to the greatest degree since August 2023. Despite a drop in permanent placements, the report signals an acceleration in the rate of starting salary inflation as firms remained willing to raise pay for high quality staff. Even so, vacancies in December also declined at the fastest pace in well over 4 years. At the same time, the availability of staff increased at the steepest pace since June. The combination of a slowdown in labour demand on the one hand and at the same time ongoing wage rises is another illustration of the policy paradox for the Bank of England as it ponders the pace of further easing going into 2025.

Another Truss Moment?

The selloff in US treasuries continued yesterday over concerns that Donald Trump’s presidency would boost spending and inflation in the US, and make the Federal Reserve’s (Fed) job of bringing inflation back to the 2% target more difficult. The downside pressure slowed, however, after the ADP report showed that the US economy added slower-than-expected new private jobs last month.

But the minutes from the latest FOMC minutes clearly said – without explicitly mentioning a name – that the upcoming changes in immigration and trade policies may require a policy reaction from the Fed. And that reaction would be in the form of less interest rate cuts this year to contain inflation. Voila. The US 30-year yield flitted with the 5% mark for the first time since November 2023 before easing and the 10-year yield spiked above the 4.70% level for the first time since April and is set for a further advance to 5% - a level that will probably make it an interesting buy target for the US 10-year papers. Strong economic data could accelerate that journey, while a weak data – unless alarmingly weak – may not prevent it.

Another truss moment?

The 10-year gilt yield advanced to the highest level since 2008 yesterday (after the 30-year yield hit the highest since 1998 earlier this week) during an aggressive selloff and broke above the peak levels that were reached during Liz Truss’ historic mini budget crisis and again during the summer/autumn period of 2023 on tighter Bank of England (BoE) monetary policy and growing fiscal concerns.

Today, the UK’s demons are back, driven by heightened fiscal concerns – evoking memories of Liz Truss’s chaotic 'mini-budget days.' Back then, markets lost confidence in the government’s spending plans, triggering an aggressive selloff that forced the BoE to intervene. The fallout toppled Truss’s government, setting the stage for Labour’s strong electoral win.

But now, the newly elected Labour government, which promised to rescue the country, improve finances, and boost growth, faces its own reckoning. To deliver on its ambitions, it needs market support – a resource proving elusive. Without it, borrowing costs will spiral higher, forcing tougher choices: more taxes, less spending, and weaker growth. And none of that bodes well for the pound.

Sterling tanked to 1.2320 against a broadly stronger US dollar. But this time, it also aggressively sold off against the euro. It’s time to step out of long sterling positions and wait for the dust to settle.

On the equities front, the FTSE 100 recovered earlier losses, as a softer pound is supportive of the FTSE 100 companies that make most of their revenues outside the UK, while the smaller British stocks are more vulnerable to political uncertainty and rapidly rising yields. Happily, many investors rely on the BoE’s power to calm down the game if things get out of control – and that’s perhaps limiting a further selloff in British stocks, altogether.

Elsewhere

Across the Channel, the EUR/USD also dived and traded below the 1.03 on the back of a strong US dollar buying across the board. The pair is consolidating near this level this morning. Whether it will continue its journey toward parity or make a U-turn toward the 1.05 level depends on where the US dollar will be headed next. Right now, the US dollar remains bid on the back of a hawkish shift in the Fed policy outlook versus a no particular change to the European Central Bank’s (ECB) softer stance. But a soft-looking data could rapidly change that dynamic and slow the US dollar’s appreciation near the current levels.

On the data front, figures released yesterday showed that the German factory orders slumped by more than 5% in November, while the business climate and consumer confidence deteriorated in the Eurozone in December while producer prices jumped more than expected. The PPI rose to 1.6% in November from 0.4% printed a month earlier. A big part of it was already priced in – as the expectation was an advance to 1.5%. But the combination of weak sentiment and rising prices is never good for stock appetite. Still, for the contrarians, the German DAX index is expected to print the biggest EPS growth this year: earnings per share in Germany are expected to grow by 10%, followed by the Swiss SMI – expected to deliver a 9.5% EPS growth and France’s CAC 40 – expected to print an 8.8% EPS growth according to the data gathered by Bloomberg Intelligence. The British FTSE 100 is only at the 5th place from the top in this list with an expected EPS growth of only 5.9% this year. But a possibly U-turn in energy prices could change that expectation.

Crude oil made a great start to the year. The barrel of US crude remembered what it was like to sit above the $75pb level for a while, before returning to the $73-ish levels. From a technical perspective, crude oil is now in the medium-term bullish consolidation zone and should remain there above the $72.85pb support. But the growing concerns regarding China’s inability to boost growth could limit the upside potential into the 200-DMA – that currently stands just above $75.50pb.

And speaking of China, the trade tensions get tenser between the US and the latter. Earlier this week, China said it would curb exports of metals that are used in making batteries. And yesterday, Biden announced additional restrictions on AI chip exports – oh, after blacklisting Tencent and CATL, one of Tesla’s key battery suppliers. Nvidia dipped below $140 share after the bell, while quantum stocks tanked after Jensen Huang said that he doesn’t see quantum computers’ usefulness before 15 – or even 20 years. Note that the US stock markets will be closed today as day of mourning for Jimmy Carter, while the bond market will close at 2pm New York time.

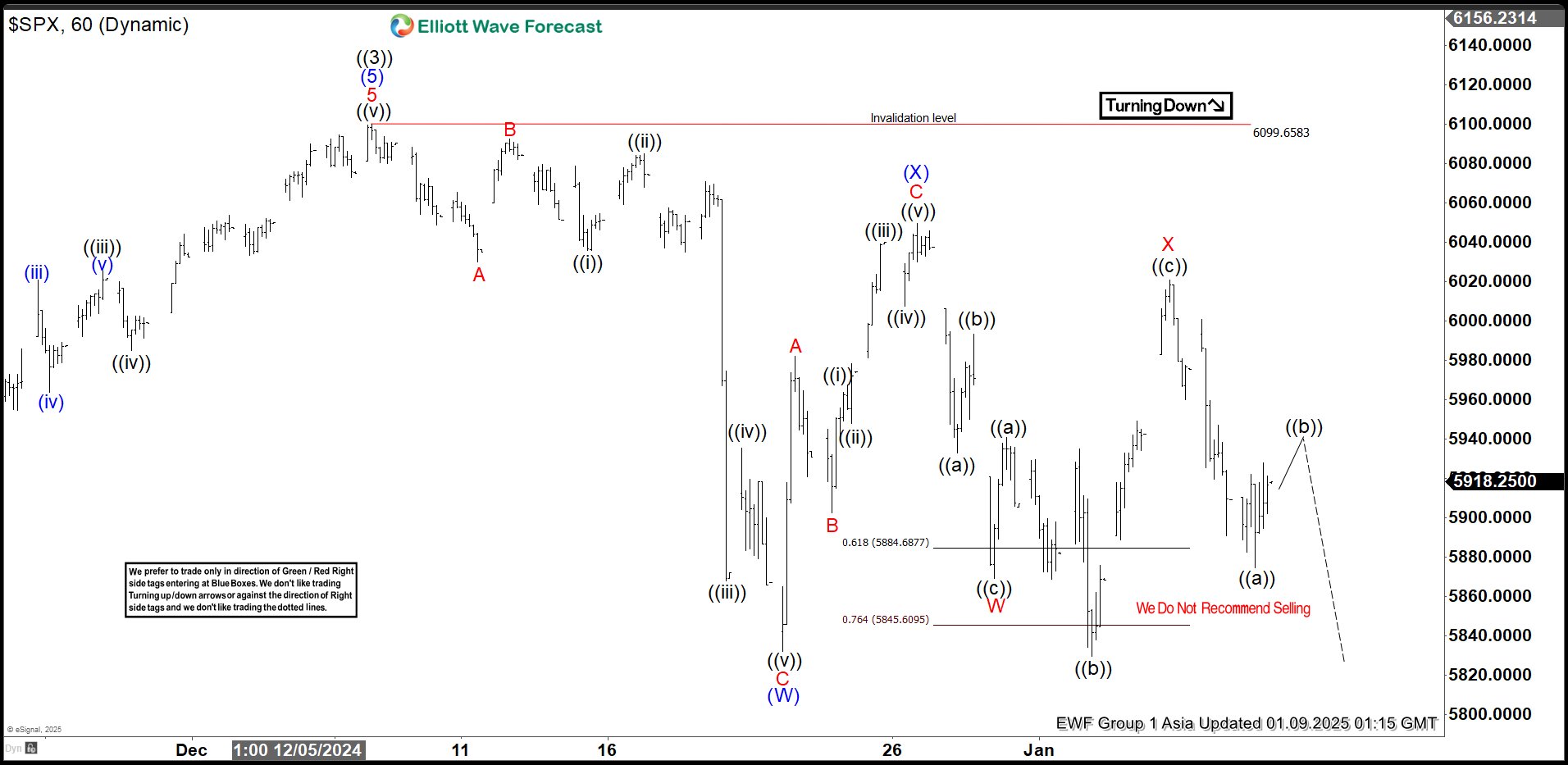

Elliott Wave View: S&P 500 (SPX) Looking for a Double Correction

Short Term Elliott Wave view in S&P 500 (SPX) suggests the rally to 6099.6 ended wave ((3)). Pullback in wave ((4)) is currently in progress to correct cycle from December 22, 2022 low. Internal subdivision of the pullback is unfolding as a double three Elliott Wave structure. Down from wave ((3)), wave A ended at 6029.89 and wave B rally ended at 6092.59. The Index then resumed lower in wave C towards 5832.3. This completed wave (W) in higher degree. From there, Index corrected in wave (X). Up from wave (W), wave A ended at 5982.06 and wave B ended at 5902.57. Wave C higher ended at 6049.75 which completed wave (X).

The Index has resumed lower in wave (Y). Down from wave (X), wave W ended at 5869.16. Wave X unfolded as an expanded flat structure. Up from wave W, wave ((a)) ended at 5940.79, and wave ((b)) pullback ended at 5829.53. Wave ((c)) higher ended at 6021.04 which completed wave X in higher degree. Index then resumed lower in wave Y. Down from wave X, wave ((a)) ended at 5874.78. Near term, as far as pivot at 6099.65 high stays intact, expect rally to fail in 3, 7, 11 swing for further downside. Potential target lower is 100% – 161.8% Fibonacci extension of wave (W). This area comes at 5616 -5782 where support can be seen.

S&P 500 (SPX) 60 Minutes Elliott Wave Chart

$SPX Elliott Wave Video

https://www.youtube.com/watch?v=AGIZcM4tVl0

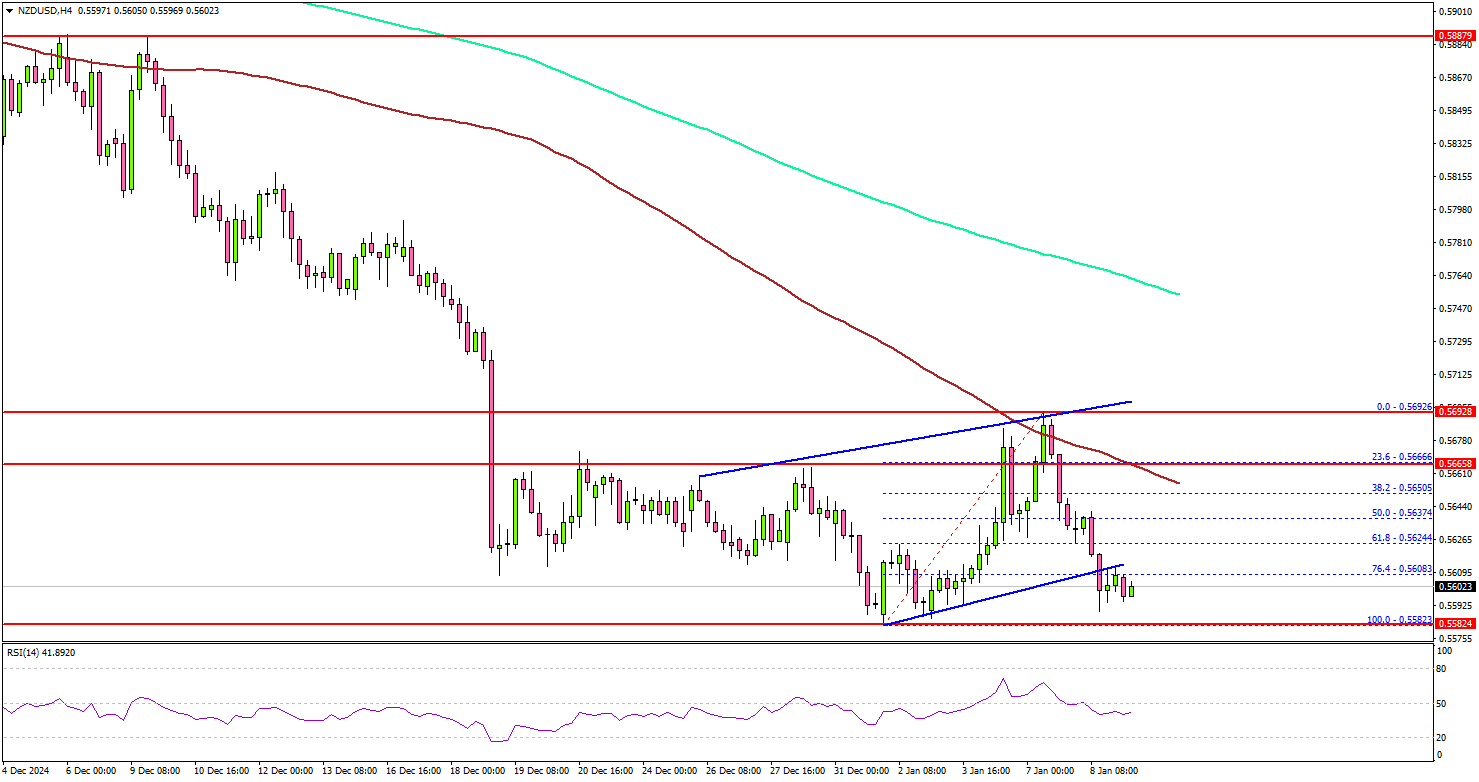

NZD/USD Decline Deepens: Bearish Pressure Escalates

Key Highlights

- NZD/USD started a fresh decline below the 0.5750 level.

- It traded below a short-term rising channel with support at 0.5610 on the 4-hour chart.

- EUR/USD is again under pressure and might revisit the 1.0225 level.

- Bitcoin is showing bearish signs below the $98,500 resistance level.

NZD/USD Technical Analysis

The New Zealand Dollar started a major decline from well above 0.5800 against the US Dollar. NZD/USD gained bearish momentum below 0.5750 and 0.5700.

Looking at the 4-hour chart, the pair settled below the 0.5660 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). The pair even declined below the 0.5620 support zone.

Recently, it traded below a short-term rising channel with support at 0.5610. It opened the doors for more downsides. On the downside, immediate support sits near the 0.5580 level.

The next key support sits near the 0.5550 level. Any more losses could send the pair toward the 0.5520 level. On the upside, the pair is facing hurdles near the 0.5630 level. The first major resistance is near the 0.5650 level.

The next major resistance is near the 0.5665 level. A close above the 0.5665 level could set the tone for another increase. In the stated case, the pair could rise toward the 0.5720 resistance.

Looking at EUR/USD, the pair is now under pressure, and the bears seem to be aiming for a drop below the 1.0225 level.

Upcoming Economic Events:

- Fed's Schmid speech.

- Fed's Bowman speech.

US100: Deeper Correction Targets December and November Lows

Fundamental Analysis

The Nasdaq 100 (US100) started the week with a sharp correction, dropping 1.9% on Tuesday, weighed down by weakness in tech stocks, particularly Nvidia, which fell more than 6% after reaching an all-time high the previous day. Mixed economic data, such as the increase in the ISM services PMI prices paid index (64.4 vs. 58.2 prior) and a rise in November job openings, heightened concerns about persistent inflation, reducing expectations for Federal Reserve rate cuts before June.

In this context, the 10-year Treasury yield climbed 7 basis points to hover near 4.7%, reflecting uncertainties about the direction of monetary policy. Investors remain cautious ahead of Friday’s labour market data, which could provide further clarity on the economic outlook. This environment of shifting monetary policy bets and movements in the tech sector continues to create a volatile scenario for the Nasdaq 100.

Technical Analysis

US100, H1

- Supply Zones (Sell):21244.30 and 21587.34

- Demand Zones (Buy): 21052.05

The recovery attempt was invalidated after breaking the key intraday support at 21295.17, leaving an uncovered POC* on Tuesday at 21587.34 and the daily POC near 21244.30. Both are acting as key supply zones, triggering selling orders.

From a volume perspective, price shows an accumulation of sell orders. Following a moderate bullish reaction to Friday’s POC at 21064, bears are expected to dominate, driving the price below 21000 toward December’s support at 20794.56 in the short term, with a target of December lows between 20630 and 20320.

Technical Summary

Bearish Scenario: Sell below 21244.30 with targets at 21000, 20795, and 20600 in extension.

Bullish Scenario: Buy above 21296 (after the formation and confirmation of a PAR*) with targets at 21300, 21400, and 21500 in extension.

Always wait for the formation and confirmation of a Reversal/Exhaustion Pattern (PAR) on M5, as shown here, before entering any trades in the key zones indicated.

*Uncovered POC: POC = Point of Control. This is the level or zone where the highest volume concentration occurred. If it preceded a bearish move, it is considered a sell zone and acts as resistance. Conversely, if it preceded a bullish move, it is considered a buy zone, usually located at lows, forming support zones.

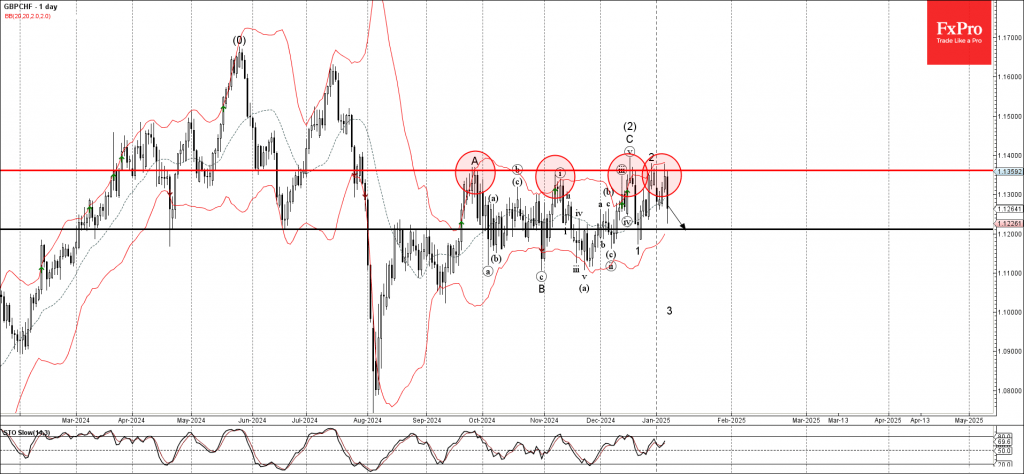

GBPCHF Wave Analysis

- GBPCHF reversed from resistance zone

- Likely to fall to support level 1.1200

GBPCHF currency pair recently reversed down from the resistance zone located between the strong multi-month resistance level 1.1360 (which has been reversing the price from September) and the upper daily Bollinger Band.

The downward reversal from this resistance zone is likely to form the daily Evening Star Japanese candlesticks reversal pattern.

Given the strength of the nearby resistance level 1.1360, GBPCHF currency pair can be expected to fall to the next support level 1.1200.

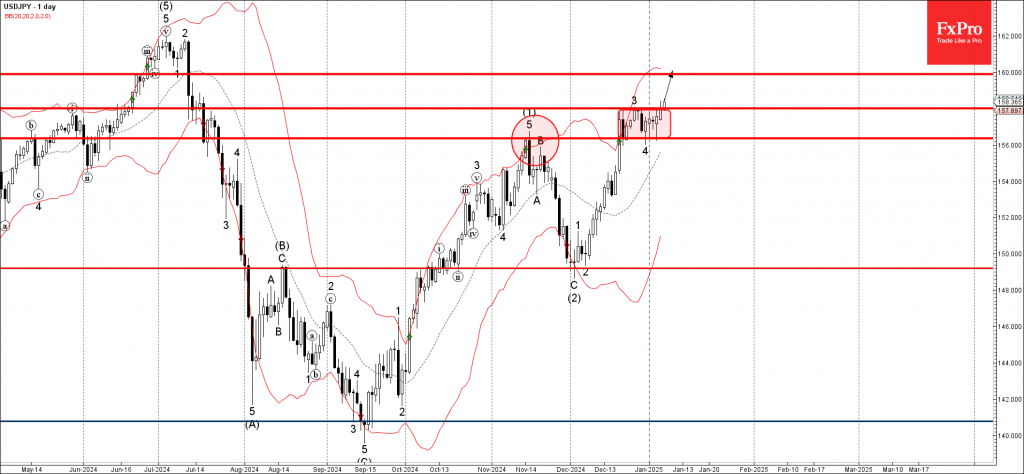

USDJPY Wave Analysis

- USDJPY broke resistance level 158.00

- Likely to rise to resistance level 160.00

USDJPY currency pair recently broke the resistance level 158.00, which is the upper border of the narrow sideways price range inside which the pair has been trading from December.

The breakout of the resistance level 158.00 should accelerate the active minor impulse wave 5 of the intermediate impulse wave (3) from the start of December.

Given the clear daily uptrend and the continued bullish US dollar sentiment, USDJPY currency pair can be expected to rise to the next resistance level 160.00.

FOMC minutes signal nearness to slow pace of rate cuts

The minutes from Fed's December meeting revealed divided sentiment among policymakers regarding the latest rate cut. While the decision to lower rates was ultimately made, it was described as “finely balanced,” with some participants emphasizing the "merits" of pausing rate reductions given persistent challenges in curbing inflation.

The minutes highlighted a growing sense within the FOMC that monetary easing might need to slow. After a cumulative 100 basis points of cuts in 2024, participants noted that the Committee is “at or near the point at which it would be appropriate to slow the pace of policy easing.” Most agreed that a more cautious approach would be prudent when considering additional rate adjustments.

The inflation outlook remained a key area of focus. While participants expected inflation to gradually align with the 2% target, recent higher-than-anticipated inflation readings and uncertainty stemming from potential changes in trade and immigration policy raised concerns.

These developments suggest that the disinflation process may "take longer than previously anticipated", with some participants observing signs that progress might have stalled temporarily.