Sample Category Title

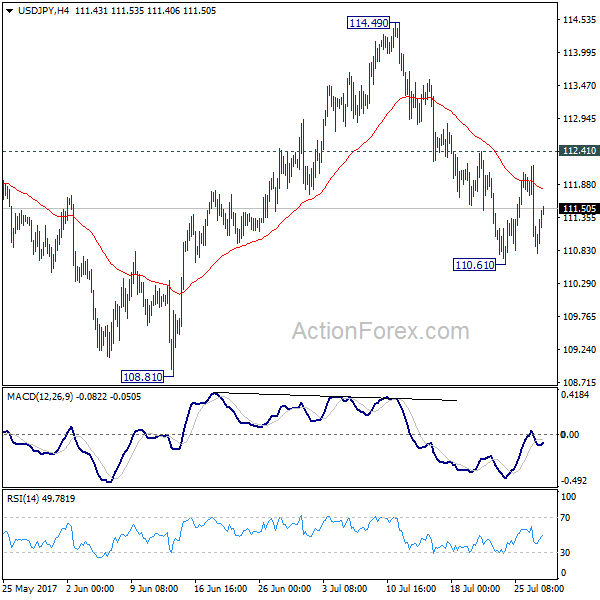

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.76; (P) 111.47; (R1) 111.89; More...

USD/JPY recovered ahead of 110.61 temporary low and stays in range below 112.41. Intraday bias remains neutral first. With 112.41 intact, further decline is expected. Below 110.61 will target 108.81. Break there will resume whole correction from 118.65 and target 61.8% retracement of 98.97 to 118.65 at 106.48. Nonetheless, break of 112.41 will dampen this bearish view and turn focus back to 114.49 resistance instead.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, down side should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

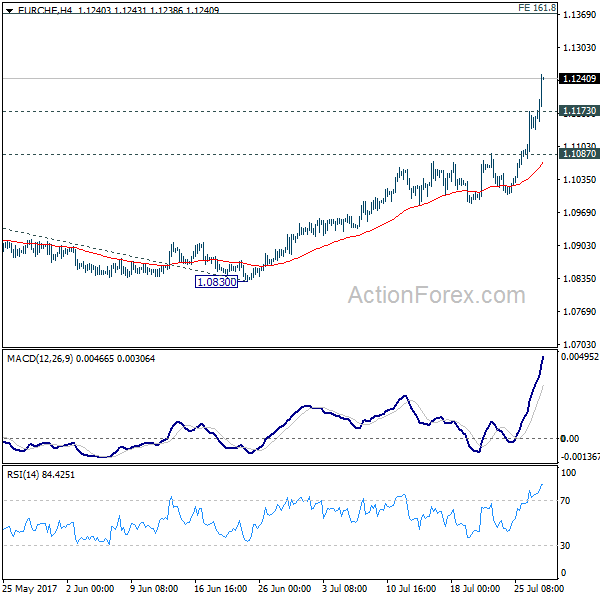

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.1099; (P) 1.1136; (R1) 1.1194; More...

EUR/CHF's rally accelerates further today and reaches as high as 1.1247 so far. 1.1198 key resistance level is seen as taken out decisively. And there is no sign of topping yet. Intraday bias remains on the upside for 161.8% projection of 1.0652 to 1.0986 from 1.0830 at 1.1370. On the downside, below 1.1173 minor support will turn intraday bias neutral and bring consolidations. But downside should be contained well by 1.1087 resistance turned support and bring rise resumption.

In the bigger picture, sustained break of 1.1198 key resistance will confirm resumption of the long term rise from SNB spike low back in 2015. In such case, EUR/CHF could eventually head back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.0986 resistance turned support holds.

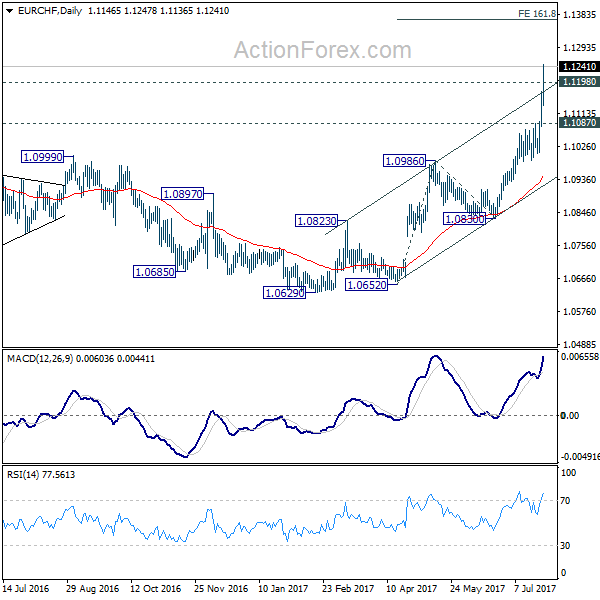

Spotlights Back on Swiss Franc as EUR/CHF Surges Past 1.12 Key Resistance

The spotlight moves back to the Swiss Franc today as EUR/CHF surges past 1.12 key resistance level. The cross is now setting up the momentum to regain 1.2 handle in medium term, which is the prior SNB imposed floor. Back in January 2015, SNB shocked the market by removing the floor and EUR/CHF dived to as low as 0.86, depending that what chart you read. With all the improvements in Eurozone, fundamentally, politically and system-wise, it now looks like there is no longer the need of safe haven parking in the Franc, with negative interest rates. The surge in commodity and energy prices would also help lift Eurozone inflation which keep ECB on course for stimulus exits.

Also regarding Swiss, the SNB's Libor will be discontinued in 2021, after being adopted as monetary policy target since 2000. An SNB spokesman said that the central bank will announce an alternative to franc Libor "in good time" And he emphasized that "The expected end of the franc Libor won't have an effect on the monetary policy orientation and monetary conditions." Some analysts pointed out that the Libor was mainly for the interbank market. SNB would need to rethink their approach. The secured Swiss Average Rate Overnight, SARON, could be an alternative.

Dollar paring back some post FOMC loss

Dollar is trying to recover today after the sharp post FOMC selloff. Some additional support is provided by solid economic data release. Meanwhile, it should be noted again that for the week as a whole, the Swiss Franc and Yen are indeed the weakest ones, not the greenback. Durable goods orders jumped 6.5% in June, well above expectation of 3.5%. But ex-transport orders rose only 0.2%, below expectation of 0.4%. Whole sale inventories rose 0.6% in June, above expectation of 0.3%. Initial jobless claims rose 10k to 244k in the week ended July 22, above expectation of 240k. It's nonetheless still the 125 straight week of sub 300k reading, the best streak since early 1970s. Continuing claims dropped 13k to 1.96m and stayed below 2m for 16 straight week, best since 1973.

Yesterday, Fed left its monetary policy unchanged, maintaining the federal funds rate target at 1-1.25%. The Fed made two tweak in the statement, though. First, it noted that balance sheet reduction would begin 'relatively soon', signaling that the official announcement would come in September. Second, policymakers revised lower the outlook on core inflation. US dollar plunged, with the weighted index falling to a 13-month low as the market interpreted the inflation assessment as dovish.

More on FOMC:

- FOMC Signaled To Begin Balance Sheet Normalization 'Relatively Soon', Downgraded Core Inflation Assessment

- Dollar Resumes The Unwind As Fed Fail To Impress

- FOMC Review: Smidgen Dovish But It Does Not Alter The Overall Picture

- FOMC: Steady As She Goes

- Little-Changed FOMC Statement Maintains Dovish Uncertainty, Weighs Further On Dollar

- Fed Stands Pat as Expected, Signals Coming Balance Sheet Normalization

- Fed Acknowledges the Inflation Miss, But Sticks to Balance Sheet Plans

EU officials warned of delay in Brexit negotiations

EU chief Brexit negotiator Michel Barnier briefed the 27 EU ambassadors yesterday regarding the July talks with UK. An EU official was quoted by Reuters saying that the chance of starting "future relationship talks" with UK in October "appeared to be decreasing". Progress on financial settlement, or the so called divorce-bill, was little to none. And EU officials believed that the problem lies in the lack of position of UK on many issues. The EU officials sounded a bit worried as the more time the first phrase drags on , the less time is left for the second phase, in particular on trade agreements.

UK Immigration Minister Brandon Lewis said today that "free movement of labor ends when we leave the European Union in the spring of 2019. I'll be very clear about that." While there is a period of negotiation with EU, Lewis emphasized that "we're very clear that free movement ends – it's part of the four key principles of the European Union – when we leave." That is seen as a response to recent reports that the UK government could allow a "transitional" period of three or four years regarding the issue.

Also released today, UK CBI realized sales rose to 22 in June. Eurozone M3 money supply rose 5.0% yoy in June. German Gfk consumer sentiment rose to 10.8 in August.

RBA Lowe warned of prolonged weak wage growth

In Australia, RBA governor Philip Lowe warned that prolonged weakness in wage growth could hurt the economy. He said that "if workers are getting no real wage increase year after year after year that's insidious." And, he emphasized that high wage growth "would help get inflation back to target and I think people would feel a bit better as well, and the fact that many of us have lowered our expectations of future income growth means we're less inclined to spend."

Regarding monetary policy, Lowe noted that "the main effect of lower interest rates is that more people have jobs". And "that's why I'm very comfortable with the current setting of monetary policy, it's helped people get jobs." Regarding the exchange rate, Lowe said that "it would be better if the exchange rate were a bit lower than it currently is. It would help generate more jobs, push inflation a bit closer to our target -- so that's the solution to a competitiveness problem."

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.1099; (P) 1.1136; (R1) 1.1194; More...

EUR/CHF's rally accelerates further today and reaches as high as 1.1247 so far. 1.1198 key resistance level is seen as taken out decisively. And there is no sign of topping yet. Intraday bias remains on the upside for 161.8% projection of 1.0652 to 1.0986 from 1.0830 at 1.1370. On the downside, below 1.1173 minor support will turn intraday bias neutral and bring consolidations. But downside should be contained well by 1.1087 resistance turned support and bring rise resumption.

In the bigger picture, sustained break of 1.1198 key resistance will confirm resumption of the long term rise from SNB spike low back in 2015. In such case, EUR/CHF could eventually head back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.0986 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Import Price Index Q/Q Q2 | -0.10% | 0.70% | 1.20% | |

| 06:00 | EUR | German GfK Consumer Confidence AUG | 10.8 | 10.6 | 10.6 | |

| 08:00 | EUR | Eurozone M3 Y/Y Jun | 5.00% | 5.00% | 5.00% | |

| 10:00 | GBP | CBI Realized Sales Jul | 22 | 10 | 12 | |

| 12:30 | USD | Initial Jobless Claims (Jul 22) | 244K | 240k | 233k | 234K |

| 12:30 | USD | Durable Goods Orders Jun P | 6.50% | 3.50% | -0.80% | |

| 12:30 | USD | Durables Ex Transportation Jun P | 0.20% | 0.40% | 0.30% | |

| 12:30 | USD | Advance Goods Trade Balance Jun | -63.9B | -65.0B | -65.9B | |

| 12:30 | USD | Wholesale Inventories Jun P | 0.60% | 0.30% | 0.40% | |

| 14:30 | USD | Natural Gas Storage | 28B |

US Futures Eye Core Durable Goods Data | Sterling And Euro Strong

- US core durable order should come strong and support the equity market

- Dovish FOMC ignites rally for euro and sterling

- European markets swing up and down due to earning results

US futures are trading higher ahead of the US core durable good order data. By looking at the US ISM's new order index and factory output, we expect the number to be strong today. The is the last set of important economic number before we get the US advance GDP q/q reading which is due tomorrow. The bar is set higher for the US core durable number as the forecast is for 0.4% while the previous reading was at 0.3%.

Investors in European markets are not that thrilled about today's earnings outcome and swinging between gains and losses. Both; Deutsche Bank and Royal Dutch Shell, surprised the markets with their numbers. It was refining and chemical business for Shell which really helped their top line number as the oil price itself is still not strong enough. Deutsche bank reported strong profits and the second quarter profit came well ahead of the Street estimate. However the CEO of the Bank brought attention to the fact that the revenue across the group still needs more work. Facebook also made a lot of noise last after the bell yesterday by beating the revenue and with a strong forecast.

Sterling and Euro are the most flashing currencies. The euro has smashed its two year resistance and Sterling is trading near the highest level since September. Before we dive into the common denominator which has produced this move, it is vital to mention that the fresh hawkish comments by Ewald Nowotny, the ECB committee member, who said it is time to slowly go off on gas, have also helped the currency. But the main catalyst behind these strong moves is the dovish statement by the Fed.

The statement was relatively dovish despite the fact that the Fed did mention that scaling down of the balance sheet would happen soon. The statement failed to produce any life in the volatility index and it touched another low. It is central banks around the world which pushed the volatility this low. The Fed fund rate is now pricing only a 45% chance for another rate hike for this year. The main reason is that the inflation is so low and markets do not believe that the Fed will increase the interest again this year. However, this could change rapidly because all it takes is just a couple of strong economic readings and these Fed fund rates will show a completely different percentage.

USD/CAD Dropping Significantly Without Any Substantial Retrace

The USD/CAD has been dropping significantly without any substantial retrace, finally hitting the 1.2400 zone support. On H4 chart the pair is showing the bullish divergence so there could be a push to the upside. Above 1.2450 we might see a bullish price action towards 1.2536. Sellers should be waiting at the POC and if the price gets there we might see a rejection. POC 1.2600-15 (W H3, 38.2, historical sellers). The POC zone is very close to W H4/M L4 so it adds additionally to its strength. Rejections might aim for sub 1.2400 levels, specifically 1.2360.

At this point it's important to notice the bullish divergence and possible upward move on the pair.

What Happened to the Dollar

The FOMC statement didn't offer much on Wednesday but it was enough to send the US dollar over the technical cliff. Several major levels broke as the dollar plunged in the aftermath. We look at what's ahead. The USDX charts below are an update from our May 19th analog USDX chart.

The US dollar moves in the aftermath of the FOMC statement look like the kind of thing you would see after a major dovish disappointment but they were more about positioning and technicals than anything from the Fed.

Tweaks to the statement included saying inflation was 'below' target rather than 'somewhat below'; and that the balance sheet runoff will start 'relatively soon' which could mean later than September. With regards to the inflation tweek, it remains to be seen whether the change was simply a mark-to-market reflection or a possible sign of the Fed's plan.

What's more important is what it didn't say. There were none of the hawkish or optimistic notes that many market participants were hoping for, and evidently positioning for. In a binary sense, this decision was either going to be neutral or more hawkish and traders piled into dollar longs in the hopes of a bounce.

It didn't come and the dollar fell by more than a cent. The move got a second wind on technicals as key levels broke. EUR/USD took out its August 2015 high of 1.1714, opening up a foray into the 2014/2015 the 1.20-1.27 zone.

The 1.2461 low in USD/CAD gave way and the pair touched a two-year low. AUD/USD also hit a fresh cycle high and cable is just a few pips away from doing the same.

The CFTC positioning data has repeatedly shown a bias to dollar longs but we're finally seeing cracks in the resolve.

Looking ahead, data comes back into focus. On Thursday, the volatile US durable goods orders are due, followed by Friday's first look at US Q2 GDP. The Fed may have been given an early look at GDP and that could explain the tepid statement. Beyond that the major numbers will be inflation, but July CPI isn't due until Aug 11, so there's plenty of time (scope) for the dollar to continue lower and the 200-week MA on USDX wilbe be the talk of the town.

Technical Outlook: US Oil – Bulls Eye Targets At $49.43 And 50.00

WTI Oil is holding high levels and pressuring $49.00 barrier on fresh extension of strong rally from $45.39 (24 July trough). Oil price maintains firm bullish sentiment which was strongly boosted on Tuesday, when oil price rallied strongly on announcement of Saudi Arabia about reducing exports in August and was reinforced by Wednesday's stronger than expected draw in US crude inventories.

Yesterday's close above daily cloud was a bullish signal, as the price is attempting to firmly break above weekly cloud (cloud top lies at $48.61).

Near-term focus turns towards targets at: $49.43 (200SMA), psychological $50.00 barrier and $50.27 (29 May high).

Bulls so far ignore strongly overbought conditions of slow stochastic, however corrective easing could be expected before the price clears 200SMA barrier.

Res: 49.00, 49.43, 49.63, 50.00

Sup: 48.51, 48.18, 47.89, 47.50

Market Update – European Session: German GFK Confidence Hits Fresh 16-Year High

Notes/Observations

USD weakness on view that Fed lowered its inflation bar thus inflation miss is no longer viewed as transitory

German GFK Confidence data at 16 year high

Overnight

Asia:

South Korea Q2 Preliminary GDP data still looks on course for a solid expansion this year, helped by government stimulus measures (Q/Q: 0.6% v 0.6%e; Y/Y: 2.7% v 2.7%e)

Moody's revised outlook on China banking system to stable from negative

Europe:

ECB's Nowotny (Austria): Confirms discussions have begun about tightening policy; agrees that time to slow take foot off the gas due to technical reason the QE ends at year end; Talks about reducing intensity of activity will be held in autumn

Americas:

Brazil Central Bank (BCB) cut Selic Target Rate by 100bps to 9.25% for its 7th straight cut in the current easing cycle

Economic Data

(DE) Aug GfK Consumer Confidence: 10.8 v 10.6e (highest since Oct 2001)

(FI) Finland July Business Confidence: 8 v 9 prior; Consumer Confidence Index: 22.8 v 23.9 prior

(NO) Norway May AKU Unemployment Rate: 4.3% v 4.5%e

(ES) Spain Q2 Unemployment Rate: 17.2% v 17.8%e (lowest level since financial crisis)

(SE) Sweden July Consumer Confidence: 102.2 v 103.1e v 102.5 prior; Manufacturing Confidence: 120.3 v 117.1e; Economic Tendency Survey: 112.4 v 111.5e

(HU) Hungary Jun Unemployment Rate: 4.2%e v 4.4% prior

(SE) Sweden Jun Unemployment Rate: 7.4% v 7.5%e; Unemployment Rate (Seasonally Adj): 6.4% v 6.6%e

(SE) Sweden Jun Household Lending Y/Y: 7.1% v 6.9%e

(EU) Euro Zone Jun M3 Money Supply Y/Y: 5.0% v 5.0%e

Fixed Income Issuance:

(IT) Italy Debt Agency (Tesoro) sold €6.5B vs. €6.5B indicated in 6-month Bills; Avg Yield: -0.362% v -0.372% prior; Bid-to-cover: 1.62x v 1.54x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.1% at 382.5, FTSE flat at 7449, DAX -0.5% at 12239, CAC-40 flat at 5191, IBEX-35 -0.1% at 10561, FTSE MIB +0.2% at 21613, SMI flat at 8994, S&P 500 Futures +0.2%].

Market Focal Points/Key Themes: European indices trade mixed this morning with volatility seen following a heavy day in terms of corporate earnings. The DAX under performs following weaker results from Bayer, BASF and Deutsche Bank, while in the UK Astrazeneca weighs following their results and their Mystic Lung cancer trial failed to meet primary endpoint. Drink makers Diageo and Anheuser Busch trade higher following strong results, while Telecom names Telefonica and Orange trade over 2% higher after beating views. Looking ahead to the US morning, expecting another heavy dose of earnings, namely from Verizon, Mastercard and P&G, as well as FIAT out of Europe.

Equities

Consumer discretionary [Diageo [DGE.UK] +6% (Earnings), Anheuser Busch InBev [ABI.BE] +5% (earnings), Nestle [NESN.CH] -1.3% (Earnings)]

Consumer Staples [Danone [BN.FR] +1.9% (Earnings)]

Industrials: [Volkswagen [VOW3.DE] -1% (earnings), BASF [BAS.DE] -1.6% (Earnings)]

Financials: [Lloyds [LLOY.UK] -2.2% (Earnings), Deutsche Bank [DBK.DE] -3.6% (Earnings), Allianz [ALV.DE] +1.4% (prelim results) ]

Technology: [Schneider Electric [SU.FR] +3.8% (Earnings, acquisition)]

Telecom: [Orange [ORA.FR] +2.8% (Earnings), Telefonica [TEF.ES] +2.9% (Earnings)]

Healthcare: [Bayer [BAYN.DE] -2.9% (Earnings, cuts outlook), Astrazeneca [AZN.UK] -15.7% (Earnings, Mystic trial misses primary endpoint), Roche [ROG.CH] +1.1% (Earnings)]

Real Estate: [Foxtons [FOXT.UK] -5% (Earnings)]

Speakers

EU might delay the next stage of Brexit talks until December

Financial Conduct Authority (FCA) stated that Libor to end in 2021; not enough transactions to give data

Japan Economic Adviser Takahashi: Economy does not need a stimulus package at this time; no reason for a supplementary budget

India Commerce Ministry official Manoj Dwivedi: Current-account deficit is comfortable now and there is a case for lowering import tax on gold

China Finance Leading Group's Yang Weimin: To curb risks in local govt debts in H2. China could have both deleveraging and stable growth and could not let leverage rise to boost economic growth. To keep liquidity ample in H2

Currencies

USD consolidated some of its recent weakness in the aftermath of Thursday's Fed rate decision and policy statement. The greenback was softer as dealers believed that the Fed lowered its inflation bar thus believing recent inflation miss was no longer viewed as transitory. The language on soft inflation was more explicitly than before.

EUR/USD tested a 2 1/2 year at 1.1778 before consolidating. European data continued to back up recent ECB speak as German GFK Confidence hot a fresh 16 year high. USD/JPY holding above the 111 level while the GBP/USD hovered around 1.3150 area

Fixed Income

Bund futures trade at 162.39 up 40 ticks and took out the key July 20th low of 161.55.. Resistance lies near the 162.75 level followed by 163.50. A break of the 160.00 support level could see lows target 159.25 followed by 157.50.

Gilt futures trade at 126.44 up 54 ticks, following the rally with Bunds and T-notes. Price finds key support at the 125.42 support level. An acceleration lower could test the 122.88 region. Resistance remains the noted 126.51 region, followed by 127.50.

Thursday's liquidity report showed use of the marginal lending facility rose to €1.2B from €496M prior.

Corporate issuance saw $1B come to market via 1issuer, Suntrust's senior unsecured note offering.

Looking Ahead

(CA) Canada July CFIB Business Barometer: No est v 60.9 prior

(BR) Brazil Jun Govt Budget Balance (BRL): -19.8Be v -29.4B prior

(ES) Spain Jun YTD Budget Balance: No est v -€16.2B prior

05:30 (ZA) South Africa Jun PPI M/M: 0.1%e v 0.5% prior; Y/Y: 4.4%e v 4.8% prior

05:30 (HU) Hungary Debt Agency (AKK) to sell 12-month Bills

05:30 (HU) Hungary Debt Agency (AKK) to sell Floating Bonds

06:00 (UK) July CBI Retailing Reported Sales: 10e v 12 prior; Total Distribution 15e v 17 prior

06:00 (IL) Israel Jun Unemployment Rate: No est v 4.5% prior

06:00 (RO) Romania to sell 3.4% 2022 Bonds

06:45 (US) Daily Libor Fixing

07:00 (TR) Turkey Central Bank (CBRT) Interest Rate Decision: Expected to keep key rates unchanged; Expected to leave Benchmark Repurchase unchanged at 8.00%; Expected to leave Overnight Lending Rate unchanged at 9.25%; Expected to leave Overnight Borrowing Rate unchanged at 7.25%; Expected to leave Late Liquidity Lending Rate unchanged at 12.25%

08:00 (BR) Brazil Jun PPI Manufacturing M/M: No est v 0.6% prior; Y/Y: No est v 2.1% prior

08:00 (UK) Baltic Dry Bulk Index

08:30 (US) Jun Preliminary Durable Goods Orders: +3.5%e v -0.8% prior; Durables Ex Transportation: 0.4%e v 0.3% prior; Capital Goods Orders (Non-defense/ex-aircraft): 0.3%e v 0.2% prior; Capital Goods Shipments (Non-defense/ex-aircraft): 0.3%e v 0.1% prior; Durables Ex-defense: No est v -0.5% prior

08:30 (US) Initial Jobless Claims: 240Ke v 233K prior; Continuing Claims: 1.96Me v 1.98M prior

08:30 (US) Jun Advance Goods Trade Balance: -$65.5Be v -66.3B prior (revised from -$65.9B)

08:30 (US) Jun Preliminary Wholesale Inventories M/M: 0.3%e v 0.4% prior; Retail Inventories M/M: No est v 0.6% prior

08:30 (US) Jun Chicago Fed National Activity Index: +0.35e v -0.26 prior

08:30 (US) Weekly USDA Net Export Sales

09:00 (RU) Russia Gold and Forex Reserve w/e July 21st: No est v $412.6B prior

09:00 (MX) Mexico Jun Trade Balance: -$0.3Be v -$1.1B prior

09:30 (BR) Brazil Jun Total Outstanding Loans (BRL): No est v 3.065B prior; M/M: No est v -0.2% prior; Personal Loan Default Rate: No est v 5.9% prior

10:30 (US) Weekly EIA Natural Gas Inventories

11:00 (US) July Kansas City Fed Manufacturing Activity Index: 11e v 11 prior

11:00 (BR) Brazil to sell 2023 LFT bills

11:00 (BR) Brazil to sell 2018, 2019 and 2022 LTN Bills

12:00 (CA) Canada to sell 10-Year Bonds

13:00 US) Treasuries to sell 7-Year Notes

15:00 (CO) Colombia Central Bank Interest Rate Decision: Expected to cut Overnight Lending Rate by 25bps to 5.50%

Technical Outlook: AUDUSD Eases From New Multi-Month High On Profit-Taking, Broken 0.8000 Handle Holds For Now

The Aussie dollar pulled back from fresh 26-month high at 0.8065 posted in Asia, but dips on profit-taking were so far contained at 0.8000 zone.

Daily close above former high at 0.7988 on Wednesday was bullish signal for continuation of broader uptrend which took a breather on 0.7988/0.7874 consolidation. Bulls need close above 0.8000 handle for confirmation and extension towards next target at 0.8161 (14 May 2015 high / 50% retracement of larger 0.9503/0.6825 downtrend).

However, downside remains vulnerable as overbought daily RSI and bearish divergence on slow stochastic warn of pullback. We look for today’s close, which would increase downside risk on close below 0.8000.

Res: 0.8065, 0.8100, 0.8161, 0.8200

Sup: 0.8000, 0.7988, 0.7956, 0.7923

EUR/USD Analysis: Reaches 1.1750 Mark

The common European currency was positioned to suffer losses against the US Dollar on Wednesday morning. However, that did not occur, as due to the US Federal Reserve the EUR/USD currency exchange rate jumped at 18:00 GMT on Wednesday. As a result of the move the currency pair traded just below the 1.1750 mark on Thursday morning. The rate was squeezed in between the weekly R1 at 1.1753 from the upside and the support of the upper trend line of the now broken ascending channel pattern. Most likely the resistance of the weekly R1 will be broken. As a result of such move the currency exchange rate would jump up to the 1.1842 mark. At that level the next notable resistance would be located at, as the weekly R2 is at that level.