Sample Category Title

Dollar Broadly Lower after Dovish Yellen, Loonie Outshone by Aussie

Dollar ended last week as the weakest currency as markets took Fed Chair Janet Yellen's testimony as a dovish one. Traders further pared back bet on a rate hike in September. And the development was accompanied by surge in stock indices to record highs. Canadian Dollar ended as the second strongest as lifted by BoC rate hike and rebound in oil prices. But it was outshone by Australian dollar which soared on iron ore prices. Sterling followed as markets continued to adjust their expectations on a near term BoE hike after central banker comments. Euro and Swiss Franc followed Dollar as the weakest ones ahead of ECB meeting this week. Meanwhile, Yen traded mixed as focus is turning to BoJ meeting.

Yellen indicated rate not far from neutral

Fed Chair Janet Yellen delivered mostly what the markets expected during her testimony to Congress last week. She reiterated that Fed is still on course for "gradual" rate hike. The unwinding of the USD 4T balance sheet will start later this year. Nonetheless, the biggest surprise was that in her view, federal funds rate "would not have to rise all that much further" to reach a neutral level. Markets perceived that as a dovish sign that there is not much room for Fed to hike even if the tightening cycle is going to continue. Further more, traders continued to pare bet on rate hike after disappointing CPI and retail sales data. Currently, Fed fund futures are only pricing in 8.4% chance of a September hike. That's less than half of 18% pricing a month ago.

DOW and S&P 500 hit record highs

Such sentiments and expectation is also clearly seen in surging equity, falling yields and Dollar. US equity indices staged a strong upside breakout on Friday and surged to new records highs. DOW rose 84.65 pts, or 0.39% to close at 21637.74. S&P 500 rose 11.44 pts, or 0.47%, to close at 2459.7. Both are new records. NASDAQ also tried to catch up and rose 38.03 pts, or 0.61% to close at 6312.47, just inches below record high at 6341.70. DOW's up trend is relatively healthy and is set to extend. The index stayed comfortably above rising 55 day despite recent consolidation. Daily MACD also turned up above signal line, indicating regaining of momentum. The key will now be on near term channel resistance. Break there will indicate further upside acceleration and would likely violate the bearish divergence condition in daily MACD. In that case, DOW would target 61.8% projection of 17883.66 to 21169.11 from 20379.55 at 22410.02 next.

10 year yield rejected from near term resistance

Treasury yield, on the other hand, was rather unconvincing. The deep pull back in 10 year yield last week raised the chance that it's rejected by 2.423 resistance. But this it isn't confirmed yet as for the moment, TNX is still supported by 55 day EMA. Break of 2.423 will confirm that the consolidation pattern from 2.621 has completed at 2.103 and should bring retest of this high. However, sustained trading below 55 day EMA (now at 2.276) will extend the consolidation with another fall through 2.103.

Dollar index extending long term correction

Dollar index's decline from 103.82 continued last week to close at 95.15. There is no change in the near term bearish outlook. Such fall from 103.82 is correcting the long term up trend from 2011 low at 72.96. Further fall is expected as long as 97.87 resistance holds. Deeper decline would be seen to 91.91 cluster level (38.2% retracement of 72.69 to 103.82 at 91.93) before having enough support for sustainable rebound.

Loonie jumped on BoC hike and oil rebound

Canadian Dollar was boosted by the neutral BoC rate hike last week, as well as rebound in oil price. As we noted before, there was a risk to Canadian Dollar if BoC signaled that the highly anticipated rate hike was a one-off. Instead, the central bank said in the statement that ""future adjustments to the target for the overnight rate will be guided by incoming data as they inform the Bank's inflation outlook". This was taken by the markets as an indication that BoC is now in a tightening cycle. Upcoming data, including this week's CPI and retail sales, could drive the Loonie further high.

At the same time, oil price will be another factor for Loonie traders to watch. Last week's rebound put 55 day EMA back into focus ( now at 46.64). Sustained break there will extend the rebound from 42.5 to trend line resistance, which is close to 50 handle. Nonetheless, rejection from 55 day EMA will bring another fall towards 50% retracement of 26.05 to 55.24 at 40.65 before completing the correction from 55.24.

Aussie surged on increasing Chinese demand on Iron Ore

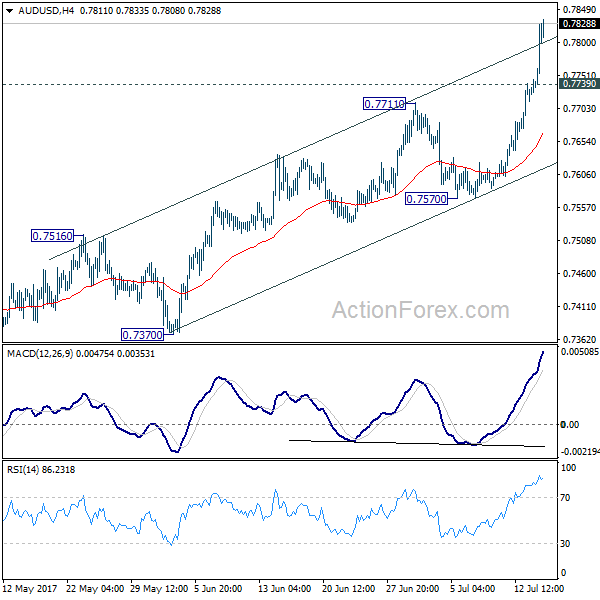

While Canadian Dollar was strong, it was indeed out-performed by Australian Dollar, which ended as the strongest currency last week. A key boost to Aussie was report that iron ore price jumped on pickup in Chinese demand. It's reported that China imported 94.7m tonnes of iron ore in June, up from 91.5m tonnes in May. A total of 539m tonnes was imported in the first half of the year. And, China is going to buy as much as 1b tonnes of iron ore from overseas producers this year. More importantly, if the pace in the first half continued, China iron ore import would top record of 1024b tonnes. Iron ore price was back to 65 level after tumbling to 53 back in June on concerns of slowing China import. AUD/USD jumped to close at 0.7828 and the upside acceleration could push for a strong breakout that indicate larger trend reversal.

Sterling saved by hawk McCafferty

Sterling was the third strongest currency as market looked past recent disappointing economic data. BoE Deputy Governor Ben Broadbent's comment that he's not ready to vote for a hike in August triggered brief setback in the Pound. But BoE hawks Ian McCafferty's talk of unwinding the GBP 435b assets revived speculations of tightening. This was indeed the first time a BoE official talked about unwinding in public. And McCafferty has made it very clear that he will still vote for a rate hike in the next meeting. Sterling staged a strong come back as markets were repositioning themselves ahead of this week's inflation data from UK.

Euro weakened as ECB likely to be outpaced by BoC and RBA

Euro was the third weakest currency, next to Dollar and Swiss Franc. It's still generally expected that ECB would announce tapering of some sort in September, or by latest in October. There were also talks that ECB President Mario Draghi would make use of the annual Jackson Hole conference in US to signal a policy shift. However, there were also media reports that ECB would prefer to maintain flexibility and not indicate a clear end to the asset purchase program. Markets will be eager to look into ECB rate decision and press conference this week for more guidance, but there is unlikely anything new. For now, judging from the steep decline in EUR/CAD and EUR/AUD, traders could be trading the fact that even if ECB is on course for stimulus exit would be far outpaced by BoC and RBA.

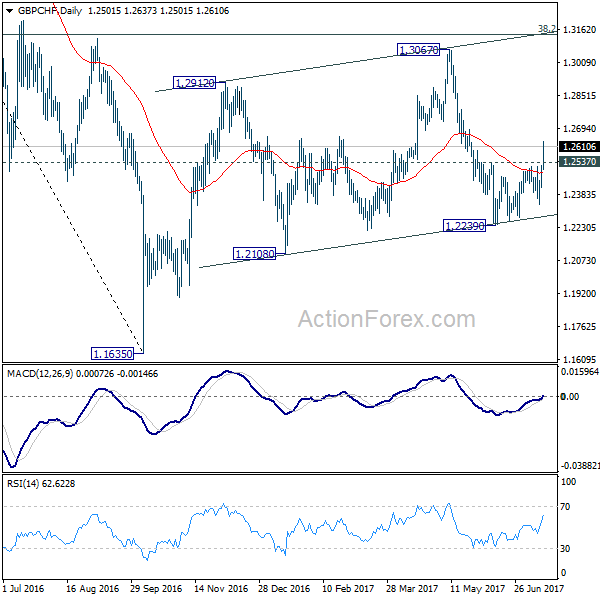

Trading strategy: Buy GBP/CHF

The overall theme in the markets is unchanged. That is, we're now entering into an era of monetary stimulus removal. Yen and Swiss Franc will continue to lag behind other major currencies. For the moment, we'd prefer not to chance rally in Loonie and Aussie, as well as Yen crosses. Instead, we'll try to buy GBP/CHF as the late rebound is taken as a sign of near term reversal. The strong break of 1.2537 resistance indicates that pull back from 1.3067 has completed at 1.2239 after drawing support from near term channel. We'll buy GBP/CHF at market this week for short term rally back to 1.3067. At this point, there is no sign of larger reversal yet with 38.2% retracement of 1.5570 to 1.1635 at 1.3138 intact. Hence, we'll get out at 1.3000, with a stop put at 1.2450.

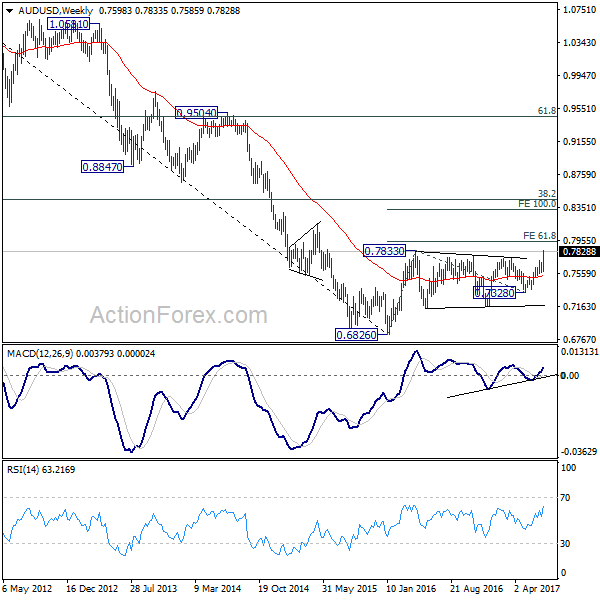

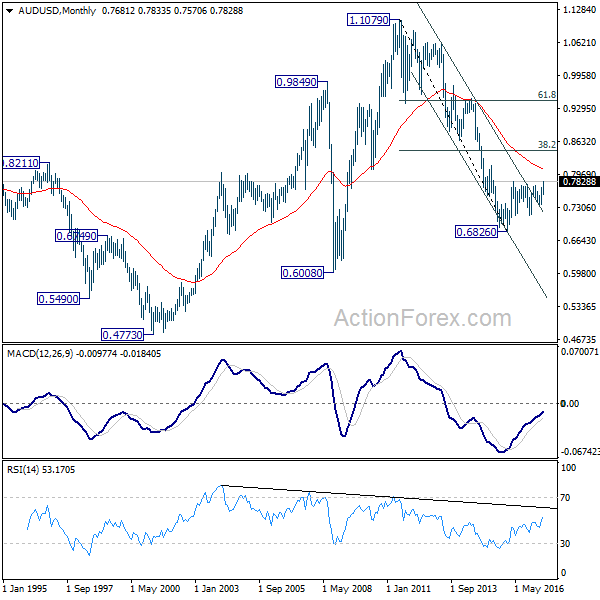

AUD/USD Weekly Outlook

AUD/USD surged to as high as 0.7833 last week as rise from 0.7328 extended. The upside acceleration argues that it's resuming larger rebound from 0.6826 bottom. Initial bias remains on the upside this week. Firm break of 0.7833 resistance will confirm this bullish case and target 61.8% projection of 0.6826 to 0.7833 from 0.7328 at 0.7950 next. On the downside, below 0.7739 minor support will turn intraday bias neutral first. But near term outlook will stay cautiously bullish as long as 0.7570 support holds.

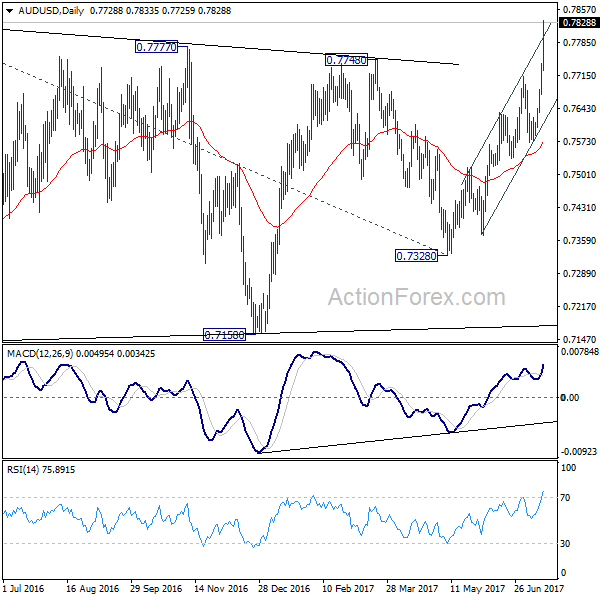

In the bigger picture, current development suggests that rebound from 0.6826 is developing into a medium term rise. There is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, further rise is now expected to 55 month EMA (now at 0.8100) or even further to 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now in favor.

In the longer term picture, 0.6826 is seen as a long term bottom. Rise from there could either reverse the down trend from 1.1079, or just develop into a corrective pattern. At this point, we're favoring the latter. And, as long as 38.2% retracement of 1.1079 to 0.6826 at 0.8451 holds, we'd anticipate another decline through 0.6826 at a later stage.

Summary 7/17 – 7/21

Monday, Jul 17, 2017

[php_everywhere] [/php_everywhere]

Tuesday, Jul 18, 2017

[php_everywhere] [/php_everywhere]

Wednesday, Jul 19, 2017

[php_everywhere] [/php_everywhere]

Thursday, Jul 20, 2017

[php_everywhere] [/php_everywhere]

Friday, Jul 21, 2017

[php_everywhere] [/php_everywhere].

Weekly Economic and Financial Commentary

U.S. Review

Key Economic Indicators Mixed in June

- All eyes were on Chair Janet Yellen this week as she gave testimony at the Semiannual Monetary Policy meeting to Congress. She reiterated components of the economy where the Fed is less certain about the path of growth, namely inflation.

- Retail sales and consumer prices came in below expectations in June, while industrial production posted a stronger than expected reading. Although retail sales were weaker than expected, the year-over-year rate still suggests the expansion in consumer spending has room to grow. Year-over-year core consumer prices were unchanged at 1.7 percent in June.

Revisiting the Four Big Uncertainties

"The quest for certainty blocks the search for meaning. Uncertainty is the very condition to impel man to unfold his powers." Erich Fromm (American psychoanalyst)

In mid-2016, Chair Janet Yellen highlighted four big uncertainties confronting the U.S. economy. At the time, she mused whether domestic spending would continue to be the main driver of real GDP growth, offsetting weak business fixed investment growth and the outlook for the global economy, productivity growth, and inflation dynamics.

About one year later, in the biannual Monetary Policy Report to the Congress, the theme of uncertainty was revisited and although the text is somewhat different, the list of unknowns looks vaguely familiar. Topics rekindled included inflation, in particular, how it will respond to low resource slack, fiscal policy, and an old favorite, global trade, especially as the Bank of Canada is among the first major central banks, other than the Fed, to begin tightening monetary policy. Indeed, indicators released during the week continued to shed light on some of these uncertainties.

Producer prices excluding, food, energy, and trade services, which is a measure of core wholesale prices, rose 2.0 percent in June relative to a year earlier, a tick softer than the gain in prices in the previous month. Core prices further back in the pipeline were mixed, with intermediate goods excluding food and energy down on the month, marking the first decline in 16 months. Unprocessed goods, nonfood excluding energy edged higher and are up 3.4 percent year over year. Although the increase in raw material prices appears to support the view that prices should climb higher in the coming months, the pass through to the consumer has been limited.

Headline consumer prices were flat in June, with weakness in commodities, wireless telephone services, lodging, airline fees, and apparel. Year over year, headline prices are up 1.6 percent, which is roughly in line with core prices. Core prices, which exclude food and energy, rose modestly in June, marking the third straight monthly gain. The shelter component, which is the largest core segment, grew more than 3 percent over the past year; roughly around the same pace registered since early-2016. The read on the trend in inflation after the June CPI report is largely unchanged.

Nominal retail sales came in below expectations in June, falling 0.2 percent, with the largest declines registered at gasoline stations, restaurants, and miscellaneous stores (e.g. bakeries, and flower shops.) However, nominal and real retail sales grew 3.0 percent on the year. Nonstore retailers and building material stores, consistent with our single-family housing outlook, continue to post the strongest year over year gains, with nearly all of the increase due to sheer volume rather than inflation. On the other hand, modest increases in electronics, health, clothing, and gasoline were mostly due to inflation.

Industrial production was also released during the week, increasing 0.4 percent in June, with gains in manufacturing and mining, while the utilities component was flat on the month.

U.S. Outlook

Import Price Index • Tuesday

Import prices softened in May, led lower by the third consecutive decline in imported petroleum prices. Ex-fuel, import prices were flat in May and up 0.8 percent over the year, a pullback from the five-year high reached in April. Export prices also slid amid broadly-based monthly deflation.

We expect another slide in energy prices to keep import prices flat for June. In the near-term, energy prices will likely continue to keep a lid on overall import price growth. Taking a longer-term view, our currency strategists' outlook for medium-term U.S. dollar weakness, if realized, would apply some modest upward pressure to nonfuel import prices, all else equal. With core inflation moving further away from the FOMC's two percent target, a reversal of the dollar's strength over the past few years could help halt this recent slide in core inflation.

Previous: -0.3% Wells Fargo: 0.0% Consensus: -0.2% (Month-over-Month)

Housing Starts • Wednesday

Housing starts once again disappointed in May, with single-family starts falling 3.9 percent and multifamily starts declining 9.7 percent. Permits also fell for both single- and multifamily, suggesting there is more at play than statistical noise. With builder confidence near cycle-highs, price gains steady and inventory historically low, the drop in single-family permits is perplexing.

Starts are still running 3.2 percent ahead of their year-ago pace through May, with single-family accounting for all of the gain. Worker shortages may be a growing issue, with the number of single-family homes authorized but not started rising 4.0 percent in May and surging 14.7 percent over the past year. Construction employment was up 3.1 percent year-over-year in June, down from a cycle-high of 6.1 percent in late 2014, and at 1.5 percent the threemonth annualized rate for construction hiring suggests limited near-term momentum.

Previous: 1.092M Wells Fargo: 1.173M Consensus: 1.160M (Annualized Rate)

Leading Economic Index • Thursday

The Leading Economic Index (LEI) rose for the ninth consecutive month in May. The interest rate spread, ISM new orders and consumer expectations all helped drive the index higher. Building permits were the lone drag on this indicator of future economic activity. Another solid monthly gain helped push the six-month annualized change to a two-year high.

The LEI is a key input into our preferred recession forecasting model, which produces the probability of a recession in the next six months. The recent run of solid readings from the LEI has pushed the probability of a recession in the next six months down to very low levels. We anticipate another gain in the LEI in June. If realized, this should produce a model result that suggests the probability of a recession in the second half of this year remains low.

Previous: 0.3% Wells Fargo: 0.4% Consensus: 0.4% (Month-over-Month)

Global Review

Global Economy Shows Further Signs of Improvement

- Eurozone industrial production was higher than the consensus estimate with an increase of 1.3 percent increase in May after an increase of 0.3 percent in the previous month.

- The central bank of Canada this week decided to increase its overnight interest rate by 25 basis points. The bank justified its move by recognizing the improvement in the global economic landscape as well as an improving Canadian economy.

- In Mexico, industrial production was up 0.1 percent in May, month on month, and by 1.0 percent on a year-earlier basis thanks to improvements in construction, public utilities and mining output while manufacturing output was down.

Eurozone Industrial Activity Gives Credence to Tightening Talk

As expected, Eurozone industrial production was higher than consensus estimates with an increase of 1.3 percent in May after a 0.3 percent rise in the previous month. This was the first time we had three consecutive positive prints for Eurozone industrial production since the second half of 2013 and speaks to the improving production environment in the region today. Furthermore, this strong increase means that it is not only Germany and France (which released strong industrial production prints last week, 1.2 percent and 1.9 percent, respectively) are doing better, but confirms that the rest of the region has also joined the club, which is positive for Eurozone economic growth as well as for global economic activity.

Canada's Central Bank Joins the Few

As expected, the Bank of Canada this week decided to increase its overnight interest rate by 25 basis points, the first change in interest rates since June 2015 when it lowered its rate to 0.50 percent. The bank justified its move by recognizing the improvement in the global economic landscape as well as an improving Canadian economy. Furthermore, the bank indicated that although inflationary pressures have abated somewhat they expect this to be temporary and see inflation returning to "close to 2 percent by the middle of 2018."

At the same time, the bank is expecting economic growth to actually slow-down from current rates with the economy's output gap closing by the end of this year. According to the central bank, the economy is expected to grow 2.8 percent in 2017 and only 1.6 percent in both 2018 and 2019.

Latin American Largest Economies

In Mexico, industrial production was up 0.1 percent in May, month on month, and by 1.0 percent on a year-earlier basis thanks to improvements in construction, public utilities and mining output while manufacturing output was down in the month. However, the good news was that the weakness in manufacturing output was not due to weakness in automobile production but in other sectors. We have also seen improvements in automobile exports to the United States market, which also points to improving automobile demand north of the border during the second quarter after a very weak first quarter. The bad news was that the weakest sectors are closely linked to domestic consumption, which has started to weaken in the second quarter of the year. In Brazil, political turmoil remains prevalent for a while longer with Judge Moro's decision to convict ex-president Lula da Silva to an almost 10 year prison term on corruption charges linked to the Lava Jato influence peddling case. Furthermore, the May economic activity index dropped 0.5 percent after increasing 0.2 percent in April, month over month, while increasing 1.4 percent on a year-earlier basis after a decline of 1.7 percent year-over-year in April. The Brazilian economy continues to be exposed to the whims of the political system.

Global Outlook

China GDP • Monday

China will release June data on retail spending, industrial production and fixed asset investment on Monday. But the highlight of the data barrage on Monday will be the GDP data for the second quarter, which will subsume the monthly data for June.

Economic growth in China has clearly downshifted since the beginning of the decade. That said, the year-over-year rate of real GDP growth has stabilized between 6.5 percent and 7.0 percent over the past few years. Chinese authorities have shown an adroit ability in recent years to tweak macroeconomic policies in an attempt to stabilize GDP growth. By and large, they have succeeded in this objective. We are in line with the consensus forecast, which expects that the year-over-year rate of real GDP growth in China ticked down to 6.8 percent in Q2-2017 from 6.9 percent in the first quarter.

Previous: 6.9% Wells Fargo: 6.8% Consensus: 6.8% (Year-over-Year)

U.K. Retail Sales • Thursday

Real GDP growth in the United Kingdom has been driven largely by consumer spending in recent years. However, growth in real retail spending has weakened recently, which has led to deceleration in the British economy this year. The culprit behind the slowdown in consumer spending appears to be higher inflation, spurred by depreciation of the British pound in the wake of last June's Brexit referendum, which has eroded growth in real disposable income. Data for retail spending in June are on the docket on Thursday.

Speaking of inflation, data on CPI inflation in June will print on Tuesday. The year-over-year rate of CPI inflation rose to a four-year high of 2.9 percent in June, well above the Bank of England's target of 2 percent. Although there are some members of the Monetary Policy Committee who would like to raise rates, most members believe that inflation will drift lower in coming months due to the sluggish pace of economic growth at present.

Previous: -1.6% Consensus: 0.5% (Month-on-Month)

Canada Retail Sales • Friday

After slipping into a mild recession in early 2015, real GDP growth in Canada has come roaring back. This rebound in the Canadian economy has been driven, at least in part, by strong growth in consumer spending. To wit, the value of retail sales in Canada was up 7.0 percent on a year-ago basis in April. Data on retail spending in May are slated for release on Friday.

The Bank of Canada conducts monetary policy in order to keep CPI inflation in a range of 1 percent to 3 percent. At only 1.3 percent, the current rate of CPI inflation is near the bottom of this range. As described on page 4, however, the Bank of Canada (BOC) decided this week to raise its main policy rates by 25 bps, its first rate hike in seven years. Policymakers argued that above-potential economic growth will eventually cause the inflation rate to move higher. CPI inflation data for June are also on the docket on Friday.

Previous: 0.8% Consensus: 0.3% (Month-over-Month)

Point of View

Interest Rate Watch

Closer to Neutral

Fed Chair Yellen's mid-year economic testimony was slightly more dovish than expected, helping drive bond yields lower and equity prices higher. One key takeaway is the federal funds rate is closer to neutral than earlier thought. Yellen cautioned the neutral rate would rise over time, as more of the recovery broadens. The process is proving slower than expected, as evidenced by the continued underperformance of retail sales and inflation.

June's disappointing retail sales are a real head scratcher, as employment, income and consumer confidence all should support increased spending. The data may simply reflect that government statistics often have difficulty incorporating massive structural shifts like we are currently seeing to online retailing. The slew of store closings has also likely depressed both prices and retail sales – which are reported in nominal terms. Merchandise is being liquidated throughout the supply chain and goods destined for retailers are undoubtedly finding their way to off-price brick-and-mortar and online merchants.

As the Fed is so fond of saying, the lack of inflationary pressures is in all likelihood transitory. The economy is almost certainly at or near full employment and even 2 percent real GDP growth will ultimately drive wages and prices higher. The process is taking much longer, however, and a growing number of Fed presidents and governors are now hinting the trajectory of future rate hikes may be more gradual.

Yellen's comments likely take a September rate hike off the table – which we had already done – and raise some doubts about a December move. There is an awful lot of time between now and December, however, and the economic and inflation environment are both likely to firm considerably by then.

There was little additional insight into the Fed's plans to reduce their balance sheet. While there are legitimate concerns about the Fed taking monetary policy to a place it has not gone before, the Fed plans to start slowly and proceed cautiously. We look for a September announcement and initial roll off in December.

Credit Market Insights

Large Consumer Credit Increase

Consumer credit rose by $18.4 billion in May, the largest increase of the year thus far. The increase represents a 5.8 percent increase at a seasonally adjusted annual rate. April's soft print was also upwardly revised. The May increase was led by a recovery in revolving credit, which rose by $7.4 billion. This marks the largest increase in revolving credit in 2017 and the second largest since June 2016. Nonrevolving credit continues to climb at a remarkable pace, while the level of revolving credit is close to its prerecession high.

Outstanding student loans continue its upward march, eclipsing $1.4 trillion dollars in the most recent reading. The level of outstanding motor vehicle loans has shown recent signs of stabilization, but remains elevated at $1.1 trillion.

This month's release also contained data on interest rates for various forms of consumer borrowing. On balance, interest rates ticked modestly higher; the interest rate on a 48-month new car loan, for instance, rose 15 bps from Q1 to 4.67 percent in May. Likewise, credit card rates continue to tick higher. Charge-off rates at commercial banks for all consumer loans, edged higher in May. But at 2.1 percent, charge-off rates are well below the rates seen leading up to the Great Recession. The Fed raising rates at its most recent meeting could create a headwind at the margin for consumers. A tight labor market and strong consumer confidence, however, should help offset the drag.

Topic of the Week

Dollar Outlook Shifts as Global Monetary Policy Starts to Converge

The U.S. dollar has had a challenging year, with losses of around 6 percent on a major trade-weighted basis yearto- date. Greenback weakness has primarily reflected shifting expectations for monetary policy both in the United States and in other key developed economies.

In the United States, key inflation measures have slowed, economic activity has been restrained and prospects for growth supportive fiscal stimulus have receded, all of which have brought into question the degree to which the Federal Reserve might raise interest rates going forward. This represents a marked shift from the dollar outlook at the beginning of the year, when U.S. data were more robust, supportive fiscal policy was widely expected and the Federal Reserve was signaling a faster pace of interest rate hikes.

Meanwhile, just as Fed rate expectations have been pared back, other key global central banks have moved toward a less accommodative policy bias. In particular, the Bank of Canada raised interest rates earlier this week, becoming the first major developed market central bank to do so after the Federal Reserve, while the European Central Bank and Bank of England have also hinted at the eventual reduction of policy accommodation. Accordingly, while we had expected monetary policy divergence (that is, wider U.S./global yield spreads) would be the key theme in 2017, the focus has instead shifted toward monetary policy convergence (narrower U.S./global yield spreads).

As a result of these shifting dynamics, we have gradually evolved our view over the course of this year from one of medium-term U.S. dollar strength to one of mediumterm U.S. dollar weakness. We now believe that the greenback's multi-year appreciation cycle—which began in mid-2011—peaked around the beginning of this year, and the greenback has now entered a multi-year depreciation cycle. Accordingly, our current view is for trend weakness in the U.S. dollar and trend strength in most foreign currencies over time.

The Weekly Bottom Line

U.S. Highlights

- Fedspeak took center stage this week. Fed Chair Yellen delivered prepared remarks to Congress, where among other things, she acknowledged the uncertainty as to when inflation would rise back toward its target.

- Taken together with Governor Brainard's comments, markets interpreted the tone as dovish, with long-term Treasury yields and U.S. dollar falling, while U.S. equities soared toward all-time highs.

- Both the CPI and retail sales reports came in below consensus, adding further downside risk to the pace of Fed hikes over the next year and a half.

Canadian Highlights

- The Canadian dollar gained more than a cent vis-à-vis its U.S. counterpart since mid-week as the Bank of Canada hiked interest rates for the first time since 2010 and indicated that more increases are likely in store.

- Hawkish statements and a solid economic outlook both suggest that another policy rate increase is coming soon – most likely in October. A more gradual pace of hikes is expected thereafter.

- Governor Poloz noted that the path forward will be 'data dependent', but with inflation forecast to remain soft through the remainder of this year, the pace of future hikes will likely hinge on the continued rotation of economic growth. Non-commodity investment and exports are the indicators to watch most closely.

U.S. - Soft Inflation Risks Delaying Fed Hike

Fedspeak took center stage this week with six members of the FOMC making public appearances. In what may be her last Congressional testimony as Fed Chair, Janet Yellen delivered prepared remarks and answered questions in both the House and Senate this week. She reiterated the Fed's narrative that the economy is healthy enough to withstand further rate increases and that the process of balance sheet reduction is expected to begin this year. That said, she did acknowledge the uncertainty as to when inflation would rise back toward its target, noting that a handful of past factors would pressure inflation down until they drop out of the annual calculation. Inflation numbers out this morning confirmed that price pressures remained subdued in June, with the softness casting some doubt as to the idiosyncratic nature of the recent loss in momentum (Chart 1).

The Chair elaborated on the neutral rate of interest, noting that it is currently low, necessitating patience as far as rate hikes. However, she suggested that the neutral rate would likely move higher towards the 3% mark as the temporary factors holding it down ease off, motivating additional rate hikes over the coming years. This marked a divergence from Governor Brainard, who suggested in her remarks this week that the neutral rate is "likely to remain close to zero in real terms over the medium term." Taken together, markets interpreted the comments as dovish, with long-term Treasury yields and U.S. dollar falling, while U.S. equities soared toward all-time highs. The latter were also buoyed by rising oil prices, on account of a bullish U.S. inventory report.

Yields and the dollar were further weighed down by a soft retail spending report with sales retreating in June, falling short of expectations for a modest gain (Chart 2). While the softer print leaves our second quarter consumption estimate still near 3%, the story is less upbeat as far as momentum heading into the third quarter with consumption on track to decelerate closer to the mid-2% mark. Together with the relatively broad-based weakness in discretionary spending categories, the poor spending performance leaves us somewhat puzzled – particularly given the continued strength in the labor market. On the whole, the combination of the weak CPI and retail sales reports adds some downside risk to the pace of Fed hikes over the rest of the next year and a half.

Still, we expect inflation pressures will begin to build through the remainder of the year, helped by an increasingly tight labor market. The labor market strength was reaffirmed by secondary data releases this week, with the JOLTS report indicating improved hiring and quit levels – the latter reflecting worker confidence – and upbeat worker compensation plans among small businesses in the NFIB survey. That said, the process of firming inflationary pressures is proving slower than expected.

Outside of the U.S., improving global growth appears to be emboldening other central banks to consider reducing stimulus. The Bank of Canada saw through soft inflation figures and raised its overnight lending rate this week for the first time in 7 years. Meanwhile, tightening talk has gained further traction at the Bank of England, and the European Central Bank looks to announce a taper schedule of its asset purchases later this year. Such convergence in monetary policy direction would help the Fed's interest rate normalization plans, but for now all eyes remain firmly on inflation.

Canada - Where to From Here?

Market moves this past week were dominated by the Bank of Canada's decision to hike its key policy interest rate by 25 basis points to 0.75% on Wednesday. The increase was largely expected by markets, but the hawkish tone of the statement and press-conference pushed the loonie up by more than a cent in anticipation of a faster pace of future rate hikes (Chart 1). Further supporting the Canadian dollar were soft U.S. data and higher oil prices, which rose by more than $2 U.S. per barrel as of Friday morning.

If there was a 'missing piece' going into Wednesday's monetary policy decision, it was inflation – which has been trending lower in recent months. This softness was attributed by the Bank of Canada to special factors such as electricity rebates. But, 'core' inflation measures, designed to provide a picture of the trend excluding such idiosyncratic factors, also weakened. Regardless, this was a departure from earlier communication that had suggested inflation was being held back by past economic shocks and should thus be near a turning point.

Regardless of what is driving current inflation, it is increasingly clear that the Bank of Canada will look through it. Governor Poloz likened relying on current inflation to guide monetary policy as "driving using only the rear-view mirror". Extending this metaphor further, we would argue that monetary policy 'driving' more resembles using a video game (or simulation), as his decisions rely on what models suggest inflation will do. While the economic backdrop generally supports gradual monetary tightening, there nevertheless would have been little harm in waiting slightly to begin increasing rates, were it not for the aggressive communication strategy to prep markets for Wednesday's decision.

Indeed, with another robust quarter of economic growth looking increasingly likely, and a broadening of growth drivers, emergency-level interest rates are no longer needed. In fact, the current tracking suggests that 2017 growth is likely to slightly outpace the Bank of Canada's upgraded forecasts (Chart 2). This suggests that the path forward is likely paved with further interest rate increases.

The key questions are therefore: how aggressive will the Bank of Canada be in removing monetary stimulus; and what factors could delay further interest rate increases? Given the healthy near-term growth outlook, the Bank will seek to remove the remainder of the 2015 policy rate cuts later this year, likely at its October meeting. Once that is accomplished, a more gradual pace is likely. We expect one 25 basis point hike every six months or so, aiming to balance support for an ongoing growth rotation while containing inflationary pressures.

Governor Poloz focused on 'data dependency' as guiding the path forward. The Bank of Canada is forecasting further deceleration in inflation in the near term. Making inflation unlikely to have much bearing on Poloz's thinking over the coming quarters, unless the deceleration is severe. More important will be the evolution of non-commodity business investment and export dynamics going forward. These will serve as important bellwethers for the durability of Canadian economic growth and any sustained weakness in these categories will likely give the Bank of Canada cause for concern.

Canada: Upcoming Key Economic Releases

Canadian Manufacturing Sales - May

Release Date: July 19, 2017

April Result: 1.1% m/m

TD Forecast: 1.0% m/m

Consensus: 0.7% m/m

The manufacturing renaissance underpinning the recovery in the goods sector is expected to continue into May with a forecasted 1.0% m/m increase in manufacturing sales. Underpinning our forecast is a strong rebound in motor vehicle shipments after a 3.7% decline last month, presaged by a sharp rise in auto exports while a further improvement in metal/mineral products should add to the headline strength. However, there are a few offsetting factors to consider - we expect a sizeable contraction in wood product shipments following the new softwood lumber tariffs and gasoline sales will be negatively impacted by falling prices at the pump. Due to an offsetting increase in core producer prices, we would look for volumes to be in line with the nominal print, which would leave real manufacturing sales growth at its strongest level since late 2014 on a year-ago basis.

Canadian Consumer Price Index - June

Release Date: July 21, 2017

Previous Result: 0.1% m/m

TD Forecast: 0.0% m/m

Consensus: 0.0% m/m

We look for June headline inflation to slip further to 1.1% y/y vs 1.3% y/y in May, reflecting unchanged prices on the month. The lift from energy prices on a year-ago basis is expected to turn to a drag, led by lower gasoline prices, while food price deflation should dissipate in line with rising agricultural prices. We expect continued strength in shelter costs as presaged by the ongoing acceleration in the new housing price index, while falling vehicle prices remains a downside risk. We look for more signs of stabilization in the core metrics of inflation (CPI common, trimmed mean and median), which averaged a cycle low of 1.3% y/y in May. However, a continued downward pull from lagged effects of slack cannot be ruled out.

Canadian Retail Sales - May

Release Date: July 21, 2017

April Result: 0.8% m/m; ex-auto: 1.5% m/m

TD Forecast: 0.3% m/m, ex-auto: -0.1%

Consensus: 0.4% m/m, ex-auto: 0.4%

Retail sales are forecast to advance by a moderate 0.3% m/m in May, led by a further pickup in motor vehicle sales. In contrast to the United States, we have yet to see any plateau in Canadian auto sales thus far in 2017 and there are indications that May might have been another record setting month. This will help to offset a sizeable drag from lower gasoline prices and housing related purchases and will leave ex-auto sales 0.1% lower on the month, though volumes should outperform the nominal print. Existing home sales in the Toronto region fell by roughly 25% in May following the introduction of new macroprudential regulations, which should constrain demand for furniture and other household furnishings. Elsewhere, we look for continued labour market gains (full time employment rose by 77k during the month) to support household spending in the near-term before the combination of higher interest rates and a more tepid housing outlook introduce a healthy cooling to the retail sector over the second half of the year.

Week Ahead Dollar Stumbles on Soft Inflation and Retail Sales Drop

US CPI and retail sales miss raise concerns on further Fed rate hikes

The US dollar is lower across the board after the release of the US retail sales and consumer price index (CPI) data on Friday. The CPI was unchanged from June and retail sales in the United States fell for the second month in a row. The Fed is confident that inflation is low due to temporary factors and anticipates that a strong labour market will lift inflation via wage increases. The disappointing data raises concerns about the U.S. Federal Reserve's plan of action in the second half of the year. The central bank is expected to raise rates at least once and start trimming its balance sheet before the end of 2017 but persistent soft inflation could derail those well laid plans.

Next week will kick off with the release of China's updated gross domestic product (GDP) calculation for the second quarter. The new methodology will include the contributions from health care, tourism and the so-called new economy. It is unclear how gradual the introduction of the new calculation will be with estimates calling for a 6.9 percent gain. China's National Bureau of Statistics will release the GDP quarterly data on Sunday, July 16 at 10:00 pm EDT.

UK inflation has accelerated this year in the aftermath of the Brexit vote. The drop in the pound has hit British households as the pace of inflation has outgunned wage growth, leaving real wage growth in negative territory for 2017. The Office for National Statistics will publish the British consumer price index (CPI) on Tuesday, July 18 at 4:30 am EDT. Inflation was 2.9 percent last month and analysts are forecasting a repeat of that print, but there is risk it comes at 3 percent.

Central banks appear to have coordinated their change in rhetoric to a more hawkish tone following the lead of the U.S. Federal Reserve in 2017. The Bank of Japan (BOJ) and the European Central Bank (ECB) are not expected to make big announcements this week, but rather make some remarks to prepare the market for eventual changes later in the year. The BOJ is likely to mention the improvement of economic fundamentals but with weak inflation the central bank is not anticipated to make any change to its stimulus program. The BOJ will release its monetary policy statement on Wednesday, July 19 near midnight EDT and hold a press conference on Thursday, July 20 at 2:30 am EDT. The ECB could tweak the language of its statement to signal a tapering of its bond buying program. Given the communication fails in the past from the ECB the central bank could cause a bigger reaction in the market. The ECB will publish the minimum bid rate on July 20 at 7:45 am EDT and President Mario Draghi will hold a press conference at 8:30 am EDT.

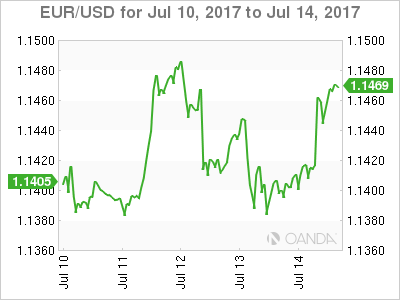

The EUR/USD gained 0.562 percent in the last five days. The single currency is trading at 1.1449 as a dovish Fed and disappointing economic indicators put downward pressure on the USD. Fed Chair Janet Yellen had two back to back days of testimonies before US Congress and the Senate. Although she did not stray far from earlier rhetoric this time the read was more dovish with less confidence on the growth trajectory of the US economy. The Fed Chair's comments and the drop in CPI and retail sales puts in question how much room the central bank really has to push through another rate hike. The lack of momentum of the US economy despite a solid job market could leave a balance sheet reduction as the only tool left in the Fed's bag.

Political uncertainty in Washington on health care reform and the escalating Russian probe has not helped the USD. Gold and the JPY have risen as safe havens for investors concerned on the ability of the Trump Administration to pass pro-growth legislation when its encumbered by political hurdles. Softer economic data is not a disaster for the USD, but combined with rising political risk will make the market pare back growth expectations going forward.

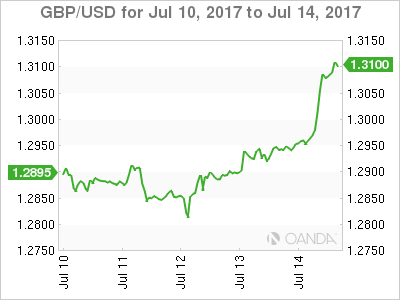

The GBP/USD gained 1.527 percent in the last five days. Cable is trading at 1.3078 as inflationary pressure might force the Bank of England (BoE) to hike soon at the same time the Fed is facing lack of inflation in the US complicating the path of further rate hikes. The currency pair started the week just below the 1.29 price level and was at weekly lows as the BoE deputy governor issues new Brexit warnings that thought to be Fed dovish comments started the GBP bounce.

Soft data in the US and expectations of the UK over performing in the same indicators with a strong retail sales and inflation data could propel the pound higher. Longer term the fog of Brexit continues to hang over the future of the UK economy with ratings agencies and the central bank concerned about what type of deal Britain can agree with the European Union.

Market events to watch this week:

Sunday, July 16

- 10:00 pm CNY GDP q/y

- 10:00pm CNY Industrial Production y/y

Monday, July 17

- 6:45 pm NZD CPI q/q

- 9:30 pm AUD Monetary Policy Meeting Minutes

Tuesday, July 18

- 4:30 am GBP CPI y/y

Wednesday, July 19

- 8:30 am USD Building Permits

- 10:30 am USD Crude Oil Inventories

- 9:30 pm AUD Employment Change

- Tentative JPY Monetary Policy Statement

Thursday, July 20

- Tentative JPY BOJ Outlook Report

- Tentative JPY BOJ Policy Rate

- 2:30 am JPY BOJ Press Conference

- 4:30 am GBP Retail Sales m/m

- 7:45 am EUR Minimum Bid Rate

- 8:30 am EUR ECB Press Conference

- 8:30 am USD Unemployment Claims

Friday, July 21

- 8:30 am CAD CPI m/m

- 8:30 am CAD Core Retail Sales m/m

*All times EDT