Sample Category Title

Elliott Wave Analysis: EURUSD Breaking Higher

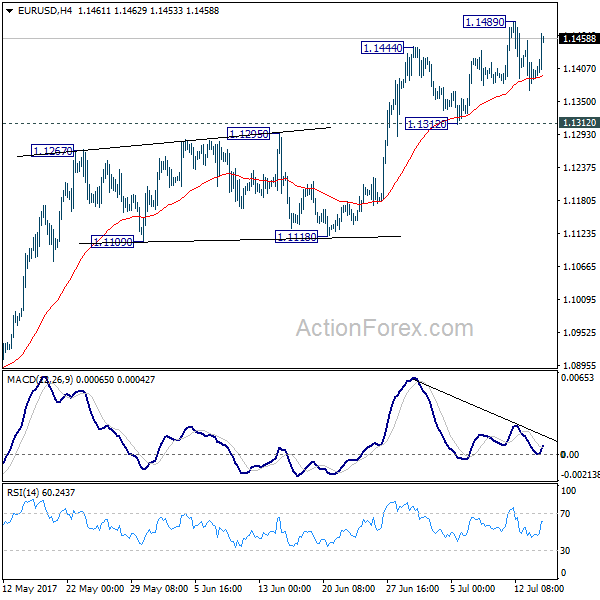

USD is falling after bad US CPI and Retail sales data. We see EURUSD turning up sharply following a break above the upper channel line which suggests that pair accomplished a three wave set-back and that market is underway to a new high. There is room for 1.1500, or even 1.1550.

USD Suffers after Data, But No EUR/USD Topside Break

- European equities traded sideways in a tiny range during European trading hours, but start losing ground in the US session. US stock markets opened marginally higher, unnerved by lacklustre earnings from several financial institutions.

- US consumer prices were unchanged in June as the cost of gasoline and mobile phone services declined further, pointing to benign inflation (1.6% Y/Y) that could cast doubts on the Federal Reserve's ability to increase interest rates for a third time this year.

- US retail sales unexpectedly fell in June (-0.2% M/M) for a second straight month, which could temper expectations of strong acceleration in economic growth in the second quarter. US industrial production rose by 0.4% M/M in June, slightly beating consensus (0.3% M/M).

- The EMU's trade in goods surplus inched up in May as import and export values both grew on the back of another bumper performance in Germany. Official trade figures from Eurostat show the bloc's seasonally adjusted surplus in goods rose 2.1% from €18.6bn to €19.7bn in May. The reading was just below an average forecast of €20bn.

- The European Central Bank is keen to keep its asset purchases open-ended rather than setting a potentially distant date on which bond-buying will stop, to retain flexibility in case the outlook sours, three sources familiar with the discussion said.

- JP Morgan's equity and fixed income trading revenues were at the low end of already low estimates, while investment banking fared better than expected. Its shares fell 1.4% pre-market. Citigroup posted a healthy beat on EPS but whiffed on equities trading. Its stock was little changed while Wells Fargo fell 1.3% after its earnings.

Rates

Core bonds profit from disappointing US eco data

Global core bonds traded with a minor upward bias in the run-up to key US eco data. The European eco calendar was empty and equity/commodity markets didn't provide input from a risk sentiment point of view. The first, and most important, batch of US eco figures disappointed. Both headline US CPI and US retail sales failed to beat (rather low) consensus. Core bonds profited with US Treasuries outperforming German Bunds. Fed chair Yellen's subtle warning on subdued inflation echoed in investors' minds. The downside in US Treasuries now seems protected in the run-up to the July 26 FOMC meeting and with potential US political upheaval in mind (Russian investigation; health care bill). US industrial production rose marginally more than forecast (0.4% M/M), but couldn't turn the tide going into the weekend.

At the time of writing, the US yield curve drops 2.8 bps (2-yr) to 5.3 bps (5-yr) lower. The belly of the US curve outperforms the wings. The German yield curve bull flattens with yields 0.9 bps (2-yr) to 3.5 bps (30-yr) lower. On intra-EMU bond markets, 10-yr yield spread changes versus Germany range between -2 bps and +2 bps with Italy (-5 bps), Spain (-6 bps) and Portugal (-6 bps) outperforming.

Currencies

USD suffers after data, but no EUR/USD topside break

Markets counted down to the US CPI and retail sales today. The US CPI was marginally softer than expected, but the retail sales showed quite a substantial miss. US yields and the dollar declined, but the damage could have been worse. Especially the rise of EUR/USD remains modest. The pair trades currently in the 1.1450 area. USD/JPY is hit hard (currently 112.40 area).

Overnight, Asian equities traded mixed, awaiting key US data later today. USD/JPY regained the 113 mark as markets expect the BOJ to maintain its cap on the 10-year government bond yield even as rates in other major economies are trending higher. However, the USD/JPY rise had no strong momentum. EUR/USD remained in wait-and-see modus, holding in the low 1.14 area

There were no important data in EMU. During the morning session, trading in European equities, bonds and in the major FX cross rates was confined to very tight ranges as investors didn't want to add positions ahead of the key US CPI and retail sales data. EUR/USD settled just north of 1.14. USD/JPY hovered in the low 113 area.

US headline inflation was marginally softer than expected (1.6% Y/Y). The miss in the June retail sales was more substantial (-0.2% M/M vs 0.1% M/M expected). The combination of soft inflation and disappointing retail sales pushed US yields up to 5 bps lower. However, given the recent focus on inflation, the damage could have been worse. The dollar also ceded ground. Especially, USD/JPY was hit hard. The pair dropped from the 113+ area to fill bid in the 112.27 area. The loss of the dollar against the euro was more modest. The pair jumped higher in the 1.14 big figure, but a real test of the 1.1489 top didn't occur (yet). The US production data released later in the session were slightly stronger than expected. As usual, the impact was limited. At best, they slowed the decline of the dollar. EUR/USD trades in the 1.1460 area, but trading remains volatile. EUR/JPY is changing hands in the 1.1460/65 area.

No UK specific news to guide sterling trading

There was hardly any UK specific news to guide sterling trading today. There were plenty of press articles on the UK accepting the principle of a financial settlement, but the debate had no impact on sterling trading. EUR/GBP held an extremely tight sideways range around the 0.88 pivot. EUR/GBP hardly profited from the post-US-CPI rebound of EUR/USD which can be seen as a tentative sign of underlying sterling strength. Cable rebounded north of 1.30 on the overall decline of the dollar.

US Inflation Continued to Slip Lower in June

Highlights:

- The all items index was unchanged month-over-month in June but the year-over-year rate of inflation slipped to 1.6% from 1.9% in May.

- Just less than one third of CPI categories were growing at 2% year-over-year in June.

- Energy prices fell for the fourth time in five months. Gasoline prices, which have been a major factor in those declines, are now little changed relative to a year ago.

- Food prices were flat in June but up from year-ago levels as the disinflationary impact from that component continues to wane.

- Consumer prices excluding food and energy rose by just 0.1% for a third consecutive month. The year-over-year rate of core inflation was unchanged at a two-year low of 1.7%.

- Wireless phone services prices were down 13% year-over-year, exerting a 0.2 percentage point drag on headline inflation.

Our Take:

After three months of inflation readings falling well short of expectations, today's report was a bit closer to consensus with the headline index coming in just 0.1 percentage point below expectations while the core inflation rate was unchanged as anticipated. It's not much, but that should come as some relief to the Fed. They have attributed some of the recent slowing to transitory factors, but further disappointment would make that position more difficult to defend. In testimony to Congress earlier this week, Chair Yellen once again expressed confidence that increased resource utilization will ultimately put upward pressure on prices. But with concerns that the link between economic slack and inflation has weakened, we think the Fed will want to see some evidence of rising prices as they continue to scale back stimulus. We look for the Fed to announce plans to begin shrinking their balance sheet in September, holding off on a rate hike at that time to gauge the market impact of tapering. That brief pause should give policymakers some time reassess the trend in inflation ahead of what we expect will be another rate increase in December.

US: Another Modest Inflation Reading in June

The headline consumer price index (CPI) was unchanged (0.0% m/m) in June, weaker than the 0.1% increase markets were expecting. A 1.6% drop in energy prices on the month and flat food prices offset a 0.1% increase in core prices. Inflation on a year-on-year basis continued to cool, and now sits at 1.6%, the lowest reading since last October.

Given the loss of headline inflationary momentum in recent months, all eyes were on core inflation where a modest 0.1% increase brought the streak of soft readings to the fourth straight month. Core inflation was 1.7% year-on-year in June, matching the previous months' pace.

Within the core, services inflation posted a moderate 0.2% m/m increase, supported by higher prices for shelter (+0.2% m/m). Prices for medical care (+0.4%), motor vehicle insurance (+1.0%), education(+0.3%) and personal care (+0.3%) all increased. These gains were partly offset by lower prices for airline fares (-2.7%), both new (-0.3%) and used (-0.7%) vehicles, and wireless telephone services (-0.8%).

Overall the tug of war in core inflation between falling goods prices (-0.1%) and rising services prices (+0.2%) continued in June. That dynamic has been in place since 2014, exacerbated by a strong U.S. dollar. Now, the services side of the rope is losing some strength. Core services inflation was 2.5% y/y in June, a notable cooling from the 3.2% pace in Q3 2016. Meanwhile core goods prices are in deflationary territory, down 0.6% from a year ago, a pace that has been reasonably steady over the past year.

Key Implications

Well, it could have been worse. Bond yields are lower on the disappointment in June inflation, but we take some solace from the fact that prices for core services continued to post moderate 0.2% monthly increases, deflation in core goods let up slightly in June and some areas of idiosyncratic price declines have reversed. Moreover, the deflationary impact of a stronger U.S. dollar over the past two and a half years is expected to ebb in the coming months given the dollar performance as of late.

Earlier this week, Fed Chair Janet Yellen emphasized the idiosyncratic nature of the recent loss of momentum in core inflation. While one-off price drops in specific categories are part of the story, it doesn't explain the entire weakening in inflation seen in measures of inflation that strip out such volatility (trimmed mean or median CPI). Inflation has weakened across many advanced economies, suggesting that a broader phenomenon – such as persistent economic slack globally – may be playing a role.

Given an increasingly tight labor market, we expect inflation pressures to build through the remainder of the year, but the process is proving slower than expected. This adds considerable risk to the pace of Fed hikes over the rest of this year and in 2018.

US: Retail Sales Decline for the Second Consecutive Month in June

Retail sales fell 0.2% in June according to the advance Census Bureau report. This was well below expectations for a 0.1% gain, although it comes atop of an upward revision - May's sales were revised up to a decline of 0.1% from 0.3% reported previously.

Sales excluding autos also declined 0.2%, as receipts at motor vehicle & parts dealers (+0.1%) were largely flat in line with the lackluster performance in auto sales during the month. Gasoline station purchases fell 1.3% on lower prices, with sales excluding autos and gas down a more subdued 0.1%, but still below the flat reading expected by the street.

Excluding gas, autos, building materials (+0.5%), and food services (-0.6%), the so-called 'control group' used in calculating GDP, was down 0.1% on the month - also below the flat reading that was expected. Sales in the control group were dragged down by miscellaneous (-3.1%), department stores (-0.7%) and sporting goods (-0.6%). These were more than offset by gains in non-store and e-commerce retailers (+0.4%), general merchandise (+0.4%), and health & personal care stores (+0.3%).

Key Implications

The weak retail sales print in June is without a doubt a disappointment as far as the resilience of the consumer is concerned. While the slight upward revision to May helps offset some of the bleakness in the June print and some of the weakness in the headline can be attributed to weak price backdrop (telegraphed in the CPI report released at the same time) leaving our second quarter GDP estimate largely unchanged near 3%, the story is less upbeat as far as momentum heading into the third quarter.

Given the weak handoff in the control group consumption appears to be decelerating closer to the 2% mark heading into the third quarter. Together with the relatively broad-based weakness in discretionary spending categories, it leaves us somewhat concerned and somewhat puzzled - particularly given the continued strength in the labor market in recent months.

The weakness is both the retail sales and CPI report is likely to be a key topic of discussion when the Fed meets at the end of the month. While we don't expect much to come from that meeting and still expect the Fed is to proceed with its normalization of the balance sheet come September, expecting an improvement in data flow in the coming months, another hike later this year seem less and less likely at this point.

U.S Retails Sales Disappoint, Inflation Unchanged

U.S Retail sales decreased a seasonally adjusted -0.2% in June from May (revised -0.1%). The market was expecting a +0.1% rise. It's the first back-to-back sales drop since July and August 2016.

The consumer-price index (CPI) was unchanged in June from May. Excluding the often-volatile categories of food and energy, core-CPI rose +0.1%.

If officials conclude the weakness is broader than a few one-off events, continued subdued readings on core-inflation could put pressure on the Fed's rate-raise plan.

The Fed has signalled it will raise short-term interest rates once more this year and also begin to reduce the size of its balance sheet.

Fed funds are pricing a +40% chance of a Dec Fed hike.

USD remains under pressure against G10 (€1.1444, £1.2993, ¥112.52, C$1.2692). U.S 10-years -4 bps at +2.31%

Details:

- US Commerce Jun Retail Sales -0.2%; Consensus +0.1%

- US Jun Consumer Prices 0.0%; Consensus +0.1%

- US Jun Retail Sales Ex-Autos -0.2%

- US Jun CPI Ex-Food & Energy +0.1%; Consensus +0.2%

- US Jun Retail Sales, Ex-Autos & Ex-Gas -0.1 %

- US Jun Consumer Prices Increase 1.6% From Year Earlier; Core CPI Up 1.7% Over Year

- US May Retail Sales Revised to -0.1%

- US Jun CPI Energy Prices -1.6%; Food Prices 0.0%

- US May Retail Sales and Ex-Autos Unrevised at -0.3%

- US Real Average Weekly Earnings +0.5% In Jun

Pound Higher on Soft US Consumer Data

GBP/USD has posted gains in Friday's North American session. Currently, GBP/USD is trading at the 1.30 level. In economic news, there are no British events on the schedule. In the US, it was a disappointing day as CPI and retail sales missed their estimates. Later in the day, the US releases UoM Consumer Sentiment, which is expected to improve to 95.1 points.

In the US, consumer spending and inflation numbers disappointed in June, sending the US dollar broadly lower. With the US economy showing signs of a slowdown and inflation levels at low levels, the markets were hoping for some strong numbers. However, the data was softer than expected. CPI posted a flat reading of 0.0%, shy of the forecast of 0.1%. There was no relief from retail sales, which declined 0.2%, compared to an estimate of +0.2%. Retail sales have now declined for a second straight month, renewing concerns that second quarter growth could be soft, which would be bad news for the US dollar.

The spotlight was on Janet Yellen this week, as she testified before congressional and senate committees about the Federal Reserve's monetary policy report, which was released last week. Yellen's comments didn't contain anything unexpected, and the markets treated her appearances before lawmakers as a non-event. Yellen reiterated that the Fed planned to raise rates "gradually", and added that the Fed would begin trimming its balance sheet before the end of the year. The Fed chair didn't provide any timelines, but the most likely timelines are September for a balance sheet reduction, with a rate hike to follow in December. However, despite Yellen's assurances, the markets remain lukewarm about a rate hike before the end of the year. Investors are concerned that the US economy has slowed down in 2017 and may not need another rate hike. In her testimony before a congressional committee, Yellen repeated that she believes the factors weighing on inflation are temporary. However, she acknowledged that with inflation well below the Fed's target of 2%, "there could be more going on there". Early in the year, the Fed all but signed on the dotted line that it would raise rates three times in 2017, but a third rate hike has become a serious question mark, with the odds of a December hike continuing to dip. According to the CME Group, the current odds for a December increase are just 43%.

The British economy has been churning out some weak data, raising fears that the "Brexit bite" may be taking a toll on the economy. Last week's PMIs, which are important gauges of activity in the construction, manufacturing and services sectors, all softened in June, pointing to weaker expansion than a month earlier. Wage growth continues to slow, and dipped to 1.8% in May, marking the first time it has fallen below the 2.0% level since February 2016. The reading is also worrisome as it shows that inflation has overtaken wage growth, meaning that real wages for the British worker are falling. The BoE is divided on whether to raise rates before the end of the year, and policymakers are in an unenviable position regarding a rate hike – the economy may not need another rate hike, but inflation is running at 3%, well above the BoE's target. A weak British currency has contributed to high inflation, while at the same reducing the purchasing power of the British consumer.

Gold Shoots Higher as US CPI, Retail Sales Disappoint

Gold has posted strong gains Friday's North American session. Currently spot gold is trading at $1229.80 per ounce and is up 1.03% on the day. On the release front, consumer data was soft, as CPI and retail sales missed their estimates. Later in the day, the US releases UoM Consumer Sentiment, which is expected to improve to 95.1 points.

With the US economy slowing gears in 2017, Friday's inflation and consumer spending numbers marked an important report card. The results were not positive, as CPI and retail sales reports were softer than expected. CPI posted a flat reading of 0.0%, shy of the forecast of 0.1%. There was no relief from retail sales, which declined 0.2%, compared to an estimate of +0.2%. Retail sales have now declined for a second straight month, renewing concerns that second quarter growth could be soft, which would be bad news for the US dollar.

All eyes were on Janet Yellen this week, as she testified before congressional and senate committees about the Federal Reserve's monetary policy report, which was released last week. Yellen's comments didn't contain any gold nuggets, and the markets shrugged off her testimony. Yellen reiterated that the Fed planned to raise rates "gradually", and added that the Fed would begin trimming its balance sheet before the end of the year. The Fed chair didn't provide any timelines, but the most likely timelines are September for a balance sheet reduction, with a rate hike to follow in December. However, despite Yellen's assurances, the markets remain lukewarm about a rate hike before the end of the year. Investors are concerned that the US economy has slowed down in 2017 and may not need another rate hike. In her testimony before a congressional committee, Yellen repeated that she believes the factors weighing on inflation are temporary. However, she acknowledged that with inflation well below the Fed's target of 2%, "there could be more going on there". Early in the year, the Fed all but signed on the dotted line that it would raise rates three times in 2017, but a third rate hike has become a serious question mark, with the odds of a December hike continuing to dip. According to the CME Group, the current odds for a December increase are just 43%.

GBPUSD: Follows Through Higher On Recovery

GBPUSD: The pair continues to trade in a range but followed through higher on the back of its Thursday gains during Friday trading session. Support lies at the 1.2950 level where a break will turn attention to the 1.2900 level. Further down, support lies at the 1.2850 level. Below here will set the stage for more weakness towards the 1.2800 level. Conversely, resistance stands at the 1.3050 levels with a turn above here allowing more strength to build up towards the 1.3100 level. Further out, resistance resides at the 1.3150 level followed by the 1.3200 level. On the whole, GBPUSD continues to face upside pressure.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1360; (P) 1.1407 (R1) 1.1445; More.....

Intraday bias in EUR/USD stays neutral for the moment. And consolidation from 1.1489 could extend. Below 1.1312 will bring deeper retreat. But downside should be contained by 1.1118 support to bring rise resumption. On the upside, break of 1.1489 will extend recent rally from 1.0339 to 1.1615 key resistance next.

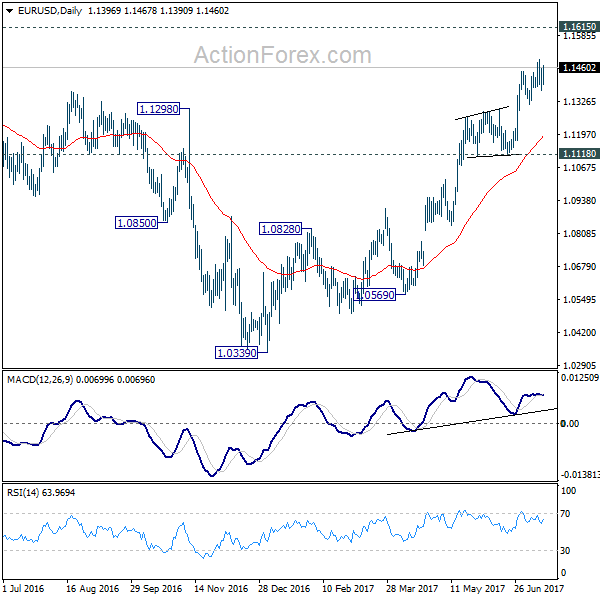

In the bigger picture, the firm break of 1.1298 resistance further affirm medium term reversal. That is an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Further rise would be seen to 55 month EMA (now at 1.1763). Sustained break there will pave the way to 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 next. This will now remain the favored case as long as 1.1118 support holds.