Sample Category Title

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD, GOLD, WTI CRUDE, DJIA, FTSE100, DAX

EUR/USD

The EUR/USD pair surged to a fresh 2017 high of 1.1479, level last seen on May 2016, with the dollar suffering a major setback after US President's son, D. Trump Jr., made publish an e-mail exchange with Rob Goldstone, a British publicist, who offered to set up meetings with the Russian government to boost Trump's campaign by using documents that would incriminate Hillary Clinton and her dealings with Russia. The scandal sent Wall Street plummeting alongside with the greenback, offsetting news coming from central bankers and pretty much everything else. Dull trading ahead of Yellen's testimony before the Congress and US inflation was interrupted with the news, and anyway, doesn't seem any of both would do something to back a greenback's recovery, as Fed's chair Yellen won't surprise with a hawkish stance, yet on the contrary, anything less than an ultra-hawkish tone will hit the dollar further. Additionally, US inflation has been soft lately, and one good reading won't be enough to convince investors it was just due to temporal factors as the Fed says.

The bullish breakout of its recent range favors a continued advance, although the pair is currently standing at a critical resistance area, as the current price zone has rejected price advances pretty much since January 2015, with a couple of short lived exceptions. Nevertheless, technical readings in the 4 hours chart, are clearly bullish, as technical indicators head north at fresh July highs, whilst the price accelerated above its 20 SMA. October 2015 high at 1.1494 is the immediate resistance, with gains most likely accelerating above this last and scope then to advance up to 1.1713, the high set on August 2015.

Support levels: 1.1380 1.1340 1.1290

Resistance levels: 1.1460 1.1490 1.1525

USD/JPY

The USD/JPY pair retreated from a multi-month high of 114.49, ending the day in the red in the 113.80 region, as political jitters in the US sent the dollar lower against most of its major rivals. As US President Trump struggles to pass the Obamacare repeal bill, news showing that his son was involved with Russian representatives to interfere with the election through "dirt on Clinton," sent USD and its related assets sharply down. During the upcoming Asian session, Japan will release its June Domestic Corporate Goods Price index indicator, which is inflation at factory levels, expected unchanged from previous readings. Still, a divergence in the outcome will weigh on the pair, particularly if the news disappoint, as it will widen the imbalance between both central banks. Technically, the pair stands within a daily ascendant channel, but nearing the base of the figure after the latest slump, at 113.60 for the upcoming session, while in the 4 hours chart, technical indicators have turned sharply lower, now entering negative territory and supporting some additional declines, moreover on a break below the mentioned support.

Support levels: 114.00 113.60 113.10

Resistance levels: 114.40 114.75 115.10

GBP/USD

The GBP/USD pair fell to a fresh 2-week low of 1.2830, with the Pound led lower by MPC members´ comments, with broad dollar's weakness barely enough to halt the slide. Ben Broadbent spoke on globalization and made no comments on monetary policy, but warned about the risk that Brexit will be to UK trade. Haldane, on the other hand, reaffirmed his pledged to raise rates amid resilient inflation and shrinking growth, but given that his stance was already known by the market, his positive comments did little to help the Pound. The UK will release its latest employment figures this Wednesday, with wages seen advancing modestly as well as jobs creation. Should the report disappoint, the Sterling will likely extend its fall this Wednesday. Technically, the pair has broken below the 38.2% retracement of its latest bullish run, now finding resistance around it at 1.2860, while in the 4 hours chart, the 20 SMA maintains a strong bearish slope above the current level, whilst the Momentum indicator continues to lack direction around its 100 level, but the RSI hovers near oversold levels, this last supporting additional declines ahead. The 50% retracement of the same rally stands at 1.2810, now the immediate support.

Support levels: 1.2810 1.2770 1.2730

Resistance levels: 1.2860 1.2895 1.2925

GOLD

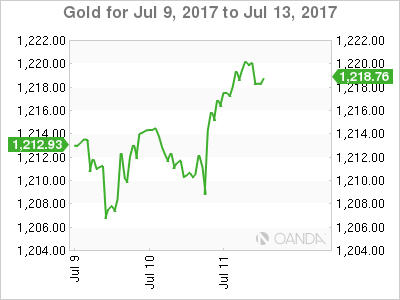

Gold prices bounced on Tuesday on broad dollar's weakness, with spot ending modestly higher, at $1,216.61 a troy ounce. The commodity recovered from a daily low of 1,208.13 after D. Trump Jr. made public sensitive campaign information, showing that Trump was offered help against Clinton. The advance, however, was moderated, amid the cautious tone of gold buyers ahead of Yellen's testimony this Wednesday, and US inflation on Thursday. A dovish tone from Fed's head could send the commodity higher, but the scenario seems quite unlikely. In the meantime, the daily chart shows that the risk remains towards the downside, as the price remains well below all of its moving averages, with the 20 DMA still heading strongly south well above the current level, whilst technical indicators remain flat near oversold levels. In the 4 hours chart, the price has settled above a bearish 20 SMA, while technical indicators lost upward strength after entering positive territory, limiting chances of a stronger recovery, at least at the time being.

Support levels: 1,212,80 1,204.75 1,194.95

Resistance levels: 1,222.10 1,228.00 1,236.50

WTI CRUDE OIL

Crude oil prices edged higher this Tuesday, with West Texas Intermediate futures ending at $45.08 a barrel, helped by news reporting that the OPEC's compliance with its output cut pledge reached 97% in June. Further supporting the commodity was an US EIA report that trimmed its forecast on US production for 2018, also cutting its price outlook to $48.95 from $50.78 previously. Ahead of stockpiles data, the daily chart for the commodity shows that the price stands above a horizontal 20 SMA, while the Momentum indicator aims higher above its 100 level whilst the RSI indicator also turned north, but around 47, rather suggesting this recovery is corrective than confirming additional gains ahead. In the shorter term and according to the 4 hours chart, WTI presents a modest positive tone as the price is above its 20 and 100 SMAs, both lacking directional strength around 44.60, while technical indicators entered positive territory, but lost upward strength. A critical resistance stands at 45.90, where the pair has the 38.2% retracement of its latest decline, and the 200 SMA in the 4 hours chart.

Support levels: 44.60 43.70 43.20

Resistance levels: 45.90 46.60 47.25

DJIA

US indexes closed the day barely changed, with the Dow Jones Industrial Average flat at 21,409.07 after trading over 150 lower intraday, following the latest Trump-Russia scandal's headlines. The Nasdaq Composite advanced roughly 17 points to close at 6,193.31, while the S&P shed 0.08%, to 2,425.53. As tech recovered, General Electric was the best performer within the Dow, up 1.32%, followed by Boeing that which gained 1.22%. Nike led decliners with a 0.92% loss, followed by Merck that shed 0.76%. In the daily chart, the index maintains its neutral stance, with the index stuck around its 20 DMA and technical indicators heading nowhere right above their mid-lines, but still with the downside seen limited, as the 100 and 200 SMAs continue heading higher far below the current level. In the 4 hours chart, the index still hovers around its 20 and 100 SMAs, both horizontal and within a tight range, while technical indicators turned south, but hold within positive territory, favoring a leg lower for this Wednesday but without confirming it yet.

Support levels: 21,366 21,305 21,278

Resistance levels: 21,459 21,515 21,563

FTSE100

The FTSE 100 fell 40 points or 0.55% to close the day at 7,329.76, hurt by news that Pearson closed a $1 billion deal to sell the 22% stake in Penguin Random House to a German company, with investors seeing the deal as undervaluing Pearson's stake in PRH. The company was the worst performer, ending the day 5.14% lower . The second worst performer was Marks & Spencer, down 4.69% after reporting its fiscal first-quarter 2018 like-for-like sales in the U.K. fell 0.5%. A bounce in commodities' prices backed the mining sector, with Glencore being the best performer, up 2.14%, followed by Anglo American and Fresnillo which added over 1% each. From a technical point of view, the daily chart for the index shows that it held below its 100 DMA, meeting selling interest around it, whilst technical indicators stalled their recoveries well below their mid-lines, all of which maintains the risk towards the downside. In the shorter term, and according to the 4 hours chart, the index settled around its 20 SMA, but below the larger ones, whilst technical indicators also lost directional momentum after advancing up to neutral territory.

Support levels: 7,327 7,294 7,256

Resistance levels: 7,386 7,424 7,452

DAX

European major benchmarks closed the day lower, with the German DAX down 0.07%, at 12.437.02, weighed by real estate and building materials' stocks. The indexes hovered within gains and losses for most of the day, with volatility limited ahead of Yellen's testimony this Wednesday. Within the DAX, ThyssenKrupp led advancers, adding 1.96%, followed by Bayerische Motoren that gained 1.77%. Henkel AG was the worst performer, down 1.04%, followed by SAP that shed 0.82% and E.ON that closed down 0.79%. The daily chart for the index shows little change from previous updates, as the index remains trapped between a bullish 20 DMA capping the upside, and a bullish 100 DMA acting as dynamic support today at 12,370, whilst technical indicators head modestly higher within negative territory. Shorter term, and according to the 4 hours chart, a modest positive tone persists, as the benchmark met buying interest on a slide down to a horizontal 20 SMA, while the RSI indicator holds flat around 54 and the Momentum aims higher above its 100 level.

Support levels: 12,432 12,370 12,333

Resistance levels: 12,490 12,541 12,596

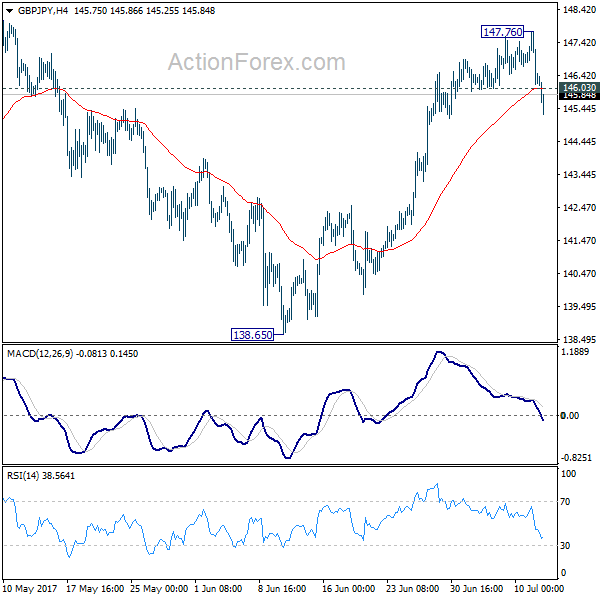

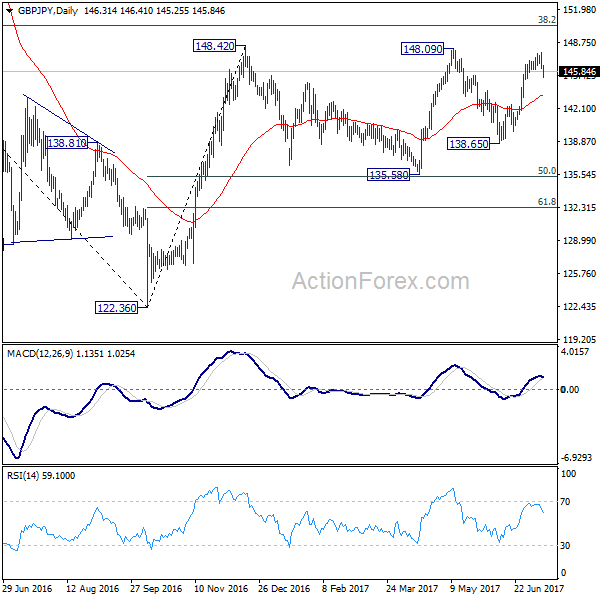

GBP/JPY Daily Outlook

Daily Pivots: (S1) 145.78; (P) 146.77; (R1) 147.39; More....

GBP/JPY's sharp fall and break of 146.03 minor support signals short term topping at 147.76. The came after failing to take out 148.09/42 key resistance zone. Intraday bias is turned back to the downside for 55 day EMA (now at 143.48). Break there will target 135.58 key support level again. On the upside, though, decisive break of 148.09/42 will pave the way to long term fibonacci level at 150.43.

In the bigger picture, rise from medium term bottom at 122.36 is expected to continue to 38.2% retracement of 196.85 to 122.36 at 150.43. Decisive break there will carry long term bullish implications and pave the way to 61.8% retracement at 167.78. In case the sideway pattern from 148.42 extends, we'd be looking for strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside.

Inventories Grease Oils Rise As Gold Rallies Again

Inventories collapse giving a tailwind to crude oil whilst a weaker dollar lifts gold.

OIL

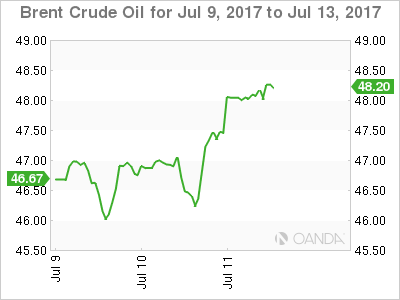

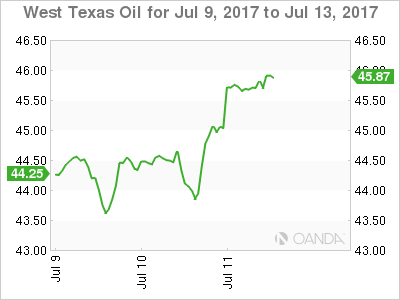

Both Brent and WTI spot staged an impressive two dollar rally in the New York session as the American Petroleum Institute reported a massive 8.1 million barrel drawdown in inventories overnight. All eyes will now turn to the official U.S. Crude Inventories number this evening where the street is forecasting a 3.2 million barrel drawdown.

A larger than expected drawdown will add fuel to the fire and could see both contracts trading towards the top of their recent ranges of 49.50 and 47.00 respectively. With the Energy Information Administration downgrading 2018 U.S. crude production overnight, one suspects that even an undershoot will see both contracts running into buyers on dips in the short term.

Brent spot trades at 48.00 this morning with resistance at 49.00 initially and supports at 47.25.

WTI spot opened at 45.70 today with resistance at 47.00 and support at 44.80.

GOLD

Gold has climbed overnight to open just below 1220 in Asia today. Although the rally was only some 0.20%, this marks the third consecutive higher open in Asia for gold, as it picks itself up off the floor following last Friday's sell off to 1205.

The rally overnight has been driven by a lower U.S. Dollar in general. Investors more than likely taking advantage of more attractive levels to go long ahead of Fed Governor Yellen's two-day testimony to Congress which starts today.

Reaction to the latest developments in the Trump/Russia campaign saga has been strangely muted. Whether the street does not think this is a 'smoking gun,' apathy, Trump-fatigue or a combination of all of the above remains to be seen.

Although the rally from 1205.00 will be pleasing to gold bulls and now becomes technical support ahead of 1200 and 1195, gold faces stern technical resistance in the 1230.00/1231.00 region. This level capped gold multiple times last week and is now also home to the 200-day moving average.

Gold's near term direction will now be at the mercy of whether we get a hawkish Yellen on the Hill today, and potential further developments on Russia's generous offer to assist President Trump's campaign last year.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 130.14; (P) 130.45; (R1) 130.96; More...

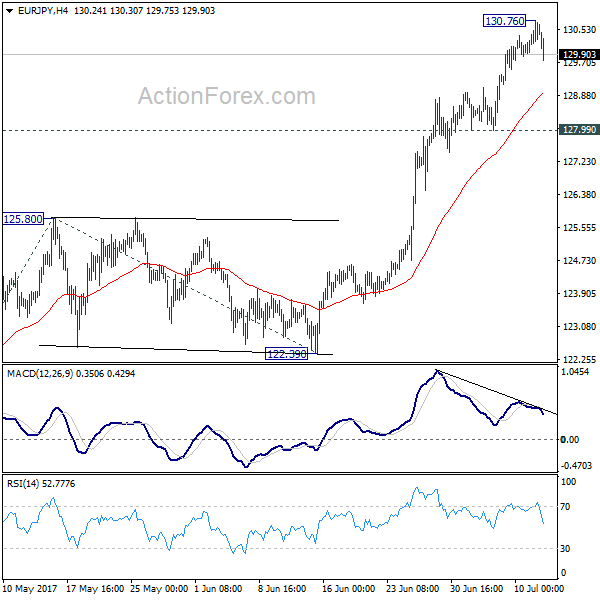

EUR/JPY retreats after hitting 130.76. A temporary top is in place and intraday bias is turned neutral for consolidation. But near term outlook remains bullish as long as 127.99 support holds. Above 130.76 will target 100% projection of 114.84 to 125.80 from 122.39 at 133.35 next. However, considering bearish divergence condition in 4 hour MACD, break of 127.99 will bring deeper pull back 55 day EMA (now at 125.13).

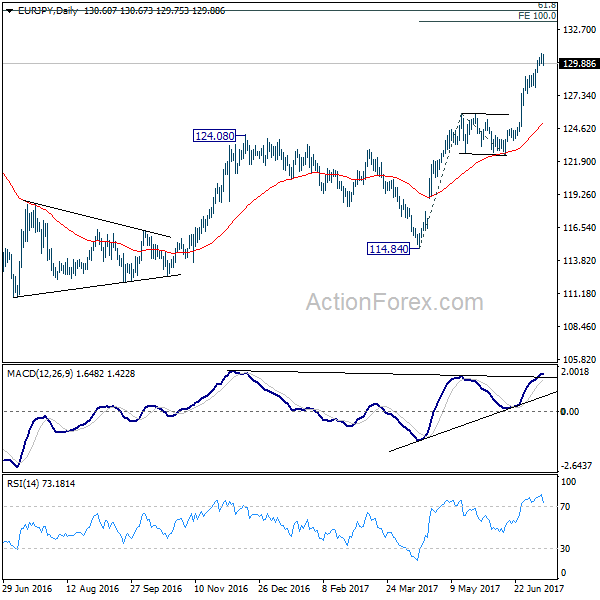

In the bigger picture, the break of 126.09 support turned resistance should have confirmed completion of down trend form 149.76 (2014 high), at 109.03 (2016 low). Current rise from 109.03 would now target 61.8% retracement of 149.76 to 109.03 at 134.20 and above. Medium term outlook will remain bullish as long as 122.39 support holds.

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

As expected, the EURUSD had a bullish momentum yesterday topped at 1.1479. The bias is bullish in nearest term testing 1.1500 – 1.1530 area before targeting 1.1615 key resistance (weekly EMA 200 and 2016 high) this week. Immediate support is seen around 1.1425. A clear break below that area could lead price to neutral zone in nearest term testing 1.1350 – 1.1285 support area but overall I remain bullish and any downside pullback should be seen as a good opportunity to buy.

GBPUSD

The GBPUSD attempted to push higher yesterday topped at 1.2927 but closed lower at 1.2845. As you can see on my daily chart below, price formed a bearish pin bar on daily chart, suggests a bearish continuation scenario after the rejection to move above 1.3050 resistance. The bias remains bearish in nearest term testing 1.2815/00. A clear break and daily close below 1.2800 would expose 1.2635 area this week. Immediate resistance is seen around 1.2927 (yesterday’s high). A clear break above that area could lead price to neutral zone in nearest term testing 1.3000 but key resistance remains at 1.3050 which remains a good place to sell with a tight stop loss.

USDJPY

The USDJPY attempted to push higher yesterday topped at 114.49 but closed lower at 113.94 and hit 113.51 earlier today in Asian session. Overall I remain bullish, but we have a bearish pin bar on daily chart as you can see on my daily chart below suggests a potential bearish pullback. The bias is bearish in nearest term testing 113.35/00 region (H1 EMA 200). A clear break below that area would expose 112.75 region which is a good place to buy with a tight stop loss. On the upside, we need a clear break above 114.49 to continue the bullish scenario targeting 115.00/50 or higher.

USDCHF

The USDCHF attempted to push higher yesterday topped at 0.9696 but closed lower at 0.9638. As you can see on my daily chart below, we have another bearish pin bar after rejection to break above 0.9675 resistance, suggests a bearish view. The bias is bearish in nearest term testing 0.9600 – 0.9550. Immediate resistance is seen around 0.9696. A clear break above that area could lead price to neutral zone in nearest term testing 0.9765 region. On the downside, 0.9550 – 0.9450 area remains a key support and good place to buy with a tight stop loss below 0.9450.

Sterling Lower Ahead Of UK Employment Data

Investors who sought fresh insight into the outlook on UK interest rates were left empty-handed on Tuesday after Bank of England's Deputy Governor Ben Broadbent maintained a safe distance from monetary policy discussions in the speech he gave in Aberdeen. Sellers were swift to exploit this disappointment and to attack the GBPUSD, with prices sliding towards 1.2820 as of writing. Price action suggests that the British Pound may be living on borrowed time, with bulls becoming increasingly exhausted as rate hike speculations become overshadowed by political uncertainty and Brexit woes. Although the hawkish remarks made a couple of weeks ago by BoE's Mark Carney and Andrew Haldane may continue to support rate hike expectations in the background, questions should be asked whether the central bank will actually raise interest rates during such fragile economic conditions.

While the argument for higher rates is that they may be able to tame inflation, this could end up doing more damage than good to the UK economy, which is currently tackling deteriorating fundamentals at home and uncertainty abroad. Higher rates may end up impacting business confidence and pressure consumers even further.

The main risk event for Sterling on Wednesday will be the UK employment report which will be closely scrutinized for any signs of Brexit having an impact on unemployment and wage growth. BoE Hawks could be in store for a rude awakening if wage growth remains subdued and fails to meet market expectations.

From a technical standpoint, the GBPUSD is under pressure on the daily charts. The breakdown below 1.2850 may encourage a further depreciation towards 1.2775.

WTI Crude lurches higher

WTI Crude sprinted higher during Tuesday's trading session with prices clipping $45.80 after reports that the Energy Information Administration (EIA) was lowering its forecast for 2018 production, encouraging investors to profit take. The upside was complimented by a decline in U.S Crude inventories which plunged almost three times more than forecast in the latest week, ultimately exciting oil bulls and easing some oversupply concerns.

Although Saudi Arabia exceeded its oil production cap for June as it pumped 10.07 million barrels, this was eventually overlooked by markets. While further upside could be expected in the short term amid the speculations of a cut in U.S production, gains may be limited by the firm oversupply dynamics of the markets. From a technical standpoint, WTI Crude is experiencing a technical bounce on the daily charts. Sellers still have some control below $47.

Commodity spotlight – Gold

Gold bulls received inspiration on Tuesday as investors sought safety, following reports of emails that show President Donald Trump's son meeting with a Kremlin-linked Russian lawyer prior to the general elections last November. A weakening Dollar supported the metal further as prices found their comfort zone, around $1218. Although the zero-yielding metal has been noticeably pressured by the rising prospects of tighter global monetary policies, the return of uncertainty could support prices in the short term. From a technical standpoint, although Gold has popped higher it still remains under pressure on the daily charts. Sellers may exploit the current technical bounce to send prices lower with $1200 acting as a level of interest.

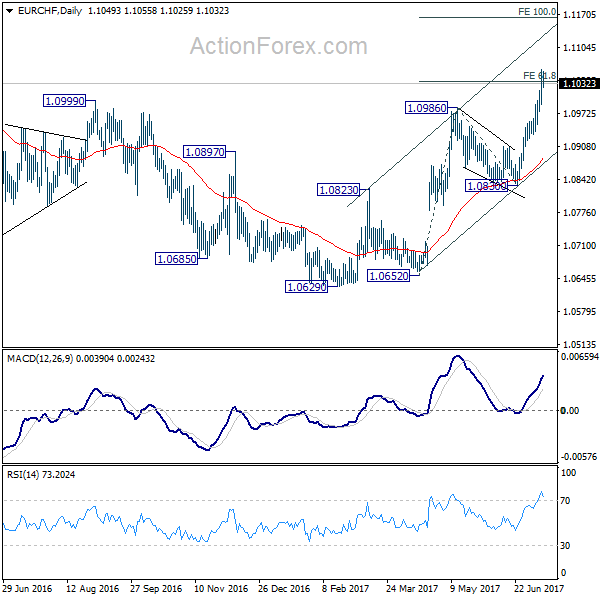

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1013; (P) 1.1037; (R1) 1.1074; More...

EUR/CHF's rise extended to as high as 1.1059 so far and met 61.8% projection of 1.0652 to 1.0986 from 1.0830 at 1.1036. Intraday bias remains on the upside for the moment. Sustained trading above 1.1036 will target 100% projection at 1.1164. On the downside, below 1.1010 minor support will turn bias neutral and bring consolidation before staging another rally.

In the bigger picture, the price actions from 1.1198 are seen as a corrective move. Such correction could have completed after defending 38.2% retracement of 0.9771 to 1.1198 at 1.0653. Decisive break of 1.0999 resistance should target a test on 1.1198 high. For now, this will be the preferred case as long as 1.0830 support holds.

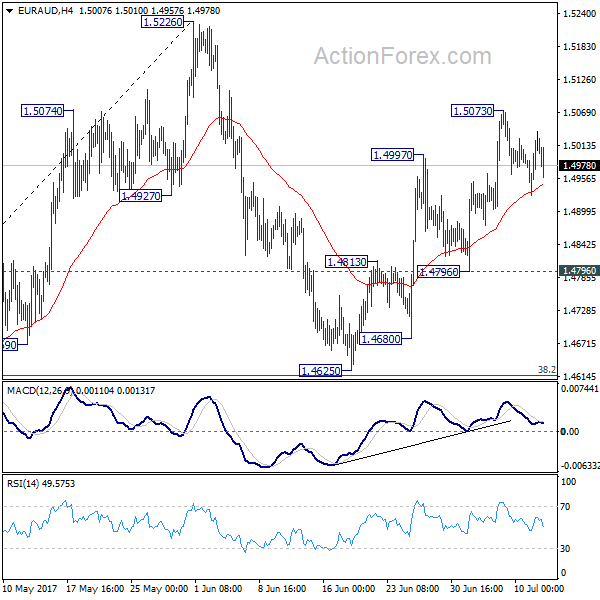

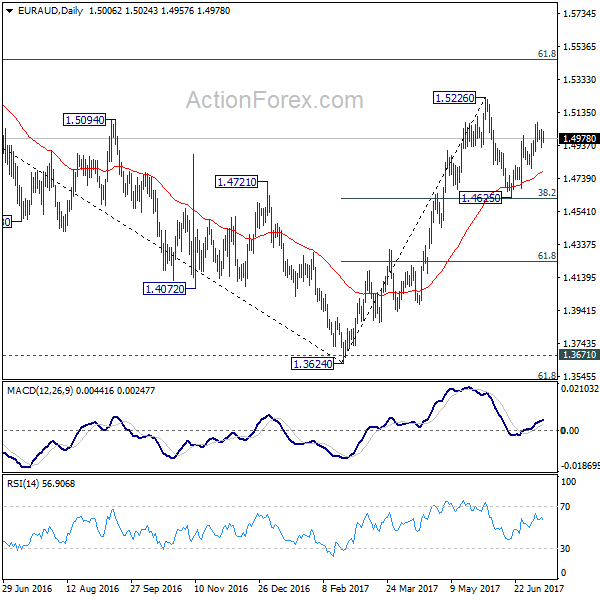

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4948; (P) 1.4992; (R1) 1.5057; More...

Intraday bias in EUR/AUD remains neutral as it's bounded in consolidative trading below 1.5073. As long as 1.4796 minor support holds, further rise remains mildly in favor. Above 1.5073 will target 1.5226 resistance first. Break there will confirm resumption of whole rally from 1.3624. In such case, EUR/AUD would target 1.5455 fibonacci level next. However, break of 1.4796 will turn bias back to the downside for 1.4625 support instead.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction should be completed at 1.3624 after defending 1.3671 key support. Rise from 1.3642 would extend to 61.8% retracement of 1.6587 to 1.3624 at 1.5455. Sustained break there will pave the way to retest 1.6587. However, sustained break of 1.4625 support will dampen this bullish view. In that case, we'll assess the outlook later after looking at the structure and depth of the pull back.

US Political Uncertainty = Lower USD

Markets were somewhat languid as traders focused on today's Congressional Testimony by Fed Chair Yellen, the Bank of Canada interest rate decision and the latest US Crude Oil Inventory data release. However, news was released that President Trump's son, Donald Trump Jr, was told in an email that Russia wanted to aid his father's Presidential campaign. Donald Trump Jr was forced to release damning emails showing that he welcomed what he was told was a Russian government attempt to harm Hillary Clinton's election campaign. The emails show music promoter Rob Goldstone telling the future US president's son that 'the crown prosecutor of Russia' had offered 'to provide the Trump campaign with some official documents and information that would incriminate Hillary and her dealings with Russia and would be very useful to your father' to which Trump Jr. replied 'I love it!'. Could more US Political turmoil be ahead? Such news saw a sell off for USD and US equities.

USDJPY reached highs not seen since early March, trading up to 114.494, representing a 0.4% gain on Tuesday, before giving back these gains to trade as low as 113.31 overnight. Currently, USDJPY is trading around 113.50.

EURUSD has reached levels not seen for 14 months as USD retreated yesterday and EUR has continued to strengthen overnight. Currently, EURUSD is trading around 1.1480 after reaching a high so far today of 1.14888.

NZDUSD was down on the day following reports from the US Geological Survey that a tremor, measuring 6.8 magnitude and at a depth of 6.2 miles, had been registered 122 miles north west of Auckland. After opening at 0.7257, NZDUSD traded down to 0.72011. Currently NZDUSD is trading around 0.7240.

EURGBP reached levels not seen since November last year, trading up to 0.89129 on Tuesday, a 0.75% gain on the day. The recent strength in EUR, coupled with unimpressive UK economic data releases and continued domestic uncertainty in the UK, has resulted in GBP weakness – especially against its European counterpart. EURGBP has strengthened more overnight to reach a high of 0.8938 and is currently trading just below this level at around 0.8930. GBP also weakened against USD trading down from an early high of 1.29268 to a low of 1.28306 on Tuesday. GBPUSD is currently trading around 1.2850.

Gold recovered from early lows set at $1,208.06 to rebound as high as $1,217.27 on Tuesday. Of note were recently released statistics that showed, during the first half of 2017, Indian buyers brought in a full 521 tonnes of gold. This is more than the import total for the whole of 2016, when just 510 tonnes of bullion was imported for the year. If this level is maintained, then imports for all of 2017 could be greater than 1,000 tonnes – an amount not seen for over 5 years. Bullish sentiment remains as Gold is currently trading at the session high of $1,220.43.

Oil gained as much as 1.6% on the day, as OPEC's Secretary General Barkindo, when asked by reporters in Istanbul 'what else the Organization of the Petroleum Exporting Countries could do to ease a global oil glut', replied with 'It is beyond any group of stakeholders, it has to be a collective responsibility of all producers'. WTI is currently trading at the session high around $46.08pb.

Today, at 15:00 BST, Fed Chair Yellen will testify before congress in regards to the current economic conditions in the US and strategy to improve growth. Focus will be on the 'tone' of her testimony and any clues as to future interest rate rises will likely be posed in the Q&A session that follows afterwards.

At the same time, the Bank of Canada releases its Interest Rate decision. Overnight Index Swaps are 'signaling' an 86% probability of an increase from 0.5% to 0.75%, although some market observers are upholding the view that Governor Poloz will keep the key overnight rate steady.

At 15:30 BST the EIA Crude Oil Stocks change report will be released. Another drawdown in US inventories is expected with the consensus being -3.225M, nearly 50% less than the previous draw of -6.299M. Even with a 'reduction' in inventories Oil supply remains strong and, even with the typical higher demand in Summer, prices are likely to remain under pressure.

Currencies: Dollar Sold As Political Noise Weighs

Sunrise Market Commentary

- Rates: US political scene interrupts core bond sell-off

Some risk aversion related to the leaked Trump Jr. emails could remain dominant in the run-up to Yellen's testimony in front of US Congress (positive core bonds). We expect her to hold the Fed's line (start run-off BS soon and 1 more hike in 2017) which shouldn't cause strong market moves. - Currencies: Dollar sold as political noise weighs

The dollar remained in wait-and-see modus after the payrolls. It looked that this pattern would continue going into Yellen's semi-annual testimony. However, a new flaring up of political noise trigger USD selling. The dollar probably needs outright positive news to make a U-turn. Will Yellen's message be strong enough to deliver so?

The Sunrise Headlines

- US stock markets lost around 0.5% after the Trump Jr. emails, but managed to overcome those losses to close nearly unchanged. Overnight, Asian stock markets trade mixed with Japan underperforming (-0.5%).

- The US president's eldest son attended a meeting last year to discuss allegedly incriminating information about Hillary Clinton they were told was being offered by the Russian government in support of Trump's candidacy.

- Fed Governor Brainard embraced the plan to reduce the balance sheet "soon," but suggested her support for any future rate increases will depend in part on how inflation shapes up.

- EU finance ministers called for speedier unloading of bad debt by EU banks and recommended more money be put aside by the banks to protect them from trouble.

- Emerging Europe is facing increasing economic stresses that threaten to unwind some of the political progress made over the of past decades, top IMF official Thomsen said.

- The US Senate will delay the start of its August recess to give lawmakers more time to plough through a backlog of pending nominations and proposed legislation, including healthcare reform.

- Attention turns to Yellen's testimony to US congress. Fed George and ECB Visco are also on the wires. The eco calendar is thin with EMU industrial production and the Fed's beige book. The US, Germany and Portugal tap the market.

Currencies: Dollar Sold As Political Noise Weighs

USD declines further on 'political noise'

The payrolls left markets with a mixed feeling on Friday. Employment growth was strong, but wages disappointed again. It didn't help the dollar. EUR/USD hovered within reach of the recent highs. The recent rise in core (US/EMU) yields kept USD/JPY better supported. It looked that this pattern could continue till Yellen's testimony before Congress today. However, soft comments from Fed's Brainard and the release of new emails on contacts of Donald Trump Jr with Russia spoiled the game. The dollar was hit quite hard on this flaring up of political uncertainty. EUR/USD closed the session at 1.1467. USD/JPY reversed part of its recent gain even as the congruent correction on the US equity markets was limited and short-lived. USD/JPY closed the day at 113.94.

This morning, Asian equities are trading mixed to slightly softer in the wake of yesterday's US political developments. The dollar remains in the defensive. USD/JPY is declining further in the 113 big figure (currently at around 113.45) even as the BOJ raised bond purchases in the 3-5-year sector to prevent a further rise in Japanese yields. EUR/USD trades with a positive bias, setting a new correction top in the 1.1489 area. Asian investors are looking forward to the Testimony of Fed's Yellen before Congress. The trade-weighted USD (95.55 area) is nearing the recent lows.

Today, EMU data (May production) will have no big impact. Early this morning, markets will look out whether there is any further fall-out from the Trump-Russia commotion on global (equity) markets. The damage should be limited, but the weaker dollar might weigh on European equities. The focus will be on Yellen's Testimony before Congress. The written testimony will be published at 14.30 CET. The Q&A will start after 16.00 CET. We expect Yellen to keep a balanced approach. She will probably confirm the start of a gradual reduction of the Fed 's balance sheet in the near term. She might be a bit less outspoken on the timing of additional rate hikes. She will probably confirm the Fed's intentions on policy normalisation, but reiterate that the Fed remains data-dependent.

Dollar sentiment remained fragile after the payrolls. Yesterday's political noise in the US forced more stale USD-longs out of their positions. The dollar clearly needs outright good news to succeed a sustained rebound. We expect Yellen's message to be positive, but balanced. This is probably not enough to change fortunes for the dollar short-term. Friday's CPI and retail sales are a next important milestone

Yesterday, the Trump headlines clearly were a short-term negative for the dollar. On the other hand, there are signals that Republicans in Congress are stepping up efforts to strike a deal on healthcare in the near future. If so, the prospect for tax cuts might become more realistic further down the road. At some point, such a scenario could help to put a floor for the dollar. However, in a day-to-day perspective, it is probably too early to play this card.

EUR/USD: Political noise weighs on the dollar. EUR/USD sets new correction top

EUR/GBP

Technical picture: USD looking for a bottom

A combination of hawkish ECB comments and weaker US eco data pushed EUR/USD above the 1.1300/66 resistance area. The payrolls were not good enough to trigger a sustained USD rebound. A next resistance in the 1.15 area is looming. LT-correction tops stand at 1.1616/1.1714. A break would end the long consolidation period that followed the sharp decline of EUR/USD in 2014/early 2015. Such a key area will be difficult to break for now. A return below the 1.13 area would be a first indication of a loss in upside momentum. EUR/USD 1.119 is the next important support.

The USD/JPY rally ran into resistance in early May and the pair returned lower in the 108.13/114.37 range. The post-Fed USD rebound pushed the pair above the 112.13 correction top, but follow-through gains remain modest. So, the jury is still out. USD/JPY 114.37 resistance was tested, but for now the test is rejected. This at least suggests a pause in the recent USD/JPY uptrend. Sterling hit as market questions rate hike chances

Sterling was in the defensive yesterday. There were few eco data to guide trading. Some cautious comments from BoE Broadbent on the UK economy post-Brexit weighed on sterling. The rise in EUR/USD later in the session also supported EUR/GBP. EUR/GBP closed the session at 0.8925. Cable didn't profit from the USD decline and closed the session at 1.2848.

This morning, there were again headlines from BoE Broadbent. In an interview, Broadbent indicated that he is not ready to support a rate hike anytime soon. This weighs further on sterling. Later today, the UK labour market data will be published. Employment growth is expected to remain solid, but wage growth to remain soft. If confirmed, this scenario won't help sterling much. From a technical point of view, EUR/GBP set a minor top north of the 0.8854/66 resistance (2017 top). A sustained break didn't occur, causing some consolidation last week. However, a sharp short-squeeze propelled the pair north of 0.89 yesterday. Quite some sterling negative news should already be discounted at current levels. Even so, the short-term trend remains euro positive/sterling negative. A test of the 0.90 barrier might be on the cards.

EUR/GBP technical break higher