Sample Category Title

Canada Housing Starts Bounce Back in June

- Housing starts rose to 213k units in June (on a seasonally adjusted annualized basis), recouping most of the ground lost over the last two months. This pushed the six-month moving average close to a 5-year high of 215k units.

- Gains were widespread during the month with both single-detached (+10%) and multi-unit (+9%) starts rising.

- Regionally, strength stemmed largely from Ontario (+24k) and Quebec (+8k), while Newfoundland and Labrador and PEI also recorded increases during the month. Ontario more than erased the losses sustained in May. On the flipside, starts declined in B.C. (-9k) and the Prairies (-6k), with Alberta and Manitoba accounting for the bulk of the Prairie losses.

Key Implications

- The bounce back in housing starts in June puts the second quarter pace of homebuilding at 204k units – a decline of roughly 8% relative to the first quarter. As such, homebuilding activity will detract from growth during the quarter. Having said that, the overall economy remains on track to expand by close to 3% during Q2.

- While we see no harm in the Bank of Canada waiting until October to hike rates, there is a very real possibility that the first rate hike in seven years will come as early as tomorrow. Should the rate hiking cycle be brought forward, Canada's housing market is likely to be slightly weaker than we currently expect. The impact of higher rates – be it now or later this year – will be most pronounced in regions where affordability is the lowest – such as Vancouver and Toronto.

- The GTA housing market is still adjusting to the Ontario Fair Housing Plan which appears to be having the desired effect of cooling the market, with sales and price growth slowing. While starts did pause in May, the rebound in June suggests that the impact on new home construction may not be as long-lasting. Indeed, while the province's housing starts are unlikely to return to the highs seen early this year, we expect them to hold near current levels going forward.

- For the country as a whole, homebuilding activity is expected slow modestly over the remainder of the year, but remain close to the 200K mark for the foreseeable future.

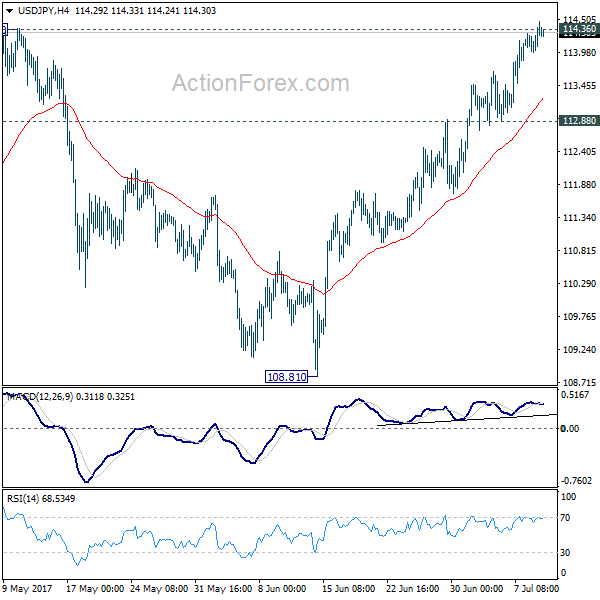

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.83; (P) 114.06; (R1) 114.26; More...

Intraday bias in USD/JPY remains on the upside with focus on 114.36 resistance. Decisive break of 114.36 resistance will confirm our bullish view that corrective pull back from 118.65 has completed at 108.12. In that case, further rally would be seen to retest 118.65. On the downside, break of 112.88 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85.

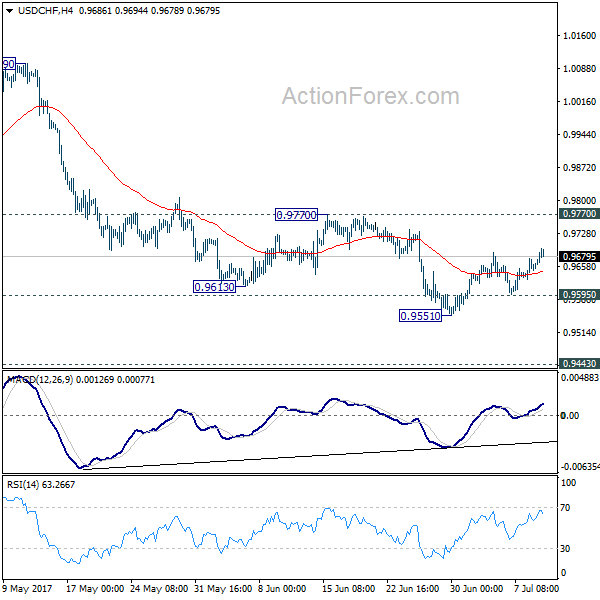

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9632; (P) 0.9653; (R1) 0.9677; More......

USD/CHF's corrective rise from 0.9551 extends higher today and could rally further. But upside is expected to be limited by 0.9770 resistance and bring fall resumption. Below 0.9595 minor support will turn intraday bias back to the downside. In such case, USD/CHF should fall through 0.9551 support resume the whole fall from 1.0342 and target 0.9443 key support level next. We'd expect strong support from there to bring rebound. Meanwhile, firm break of 0.9770 will indicate near term reversal, on bullish convergence condition in 4 hour MACD.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

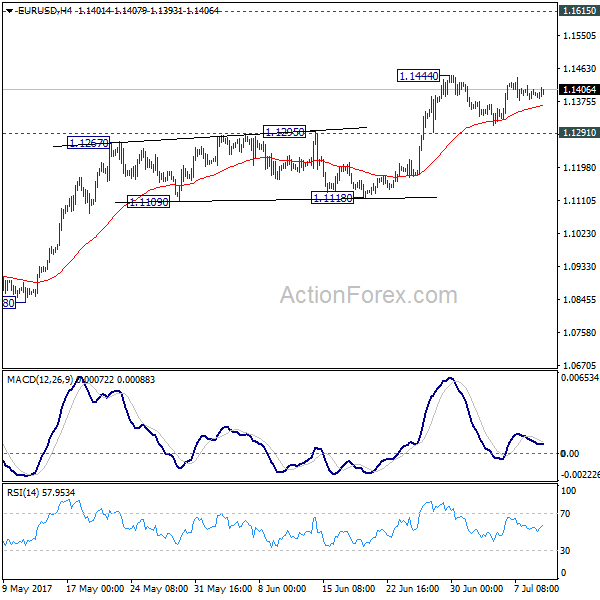

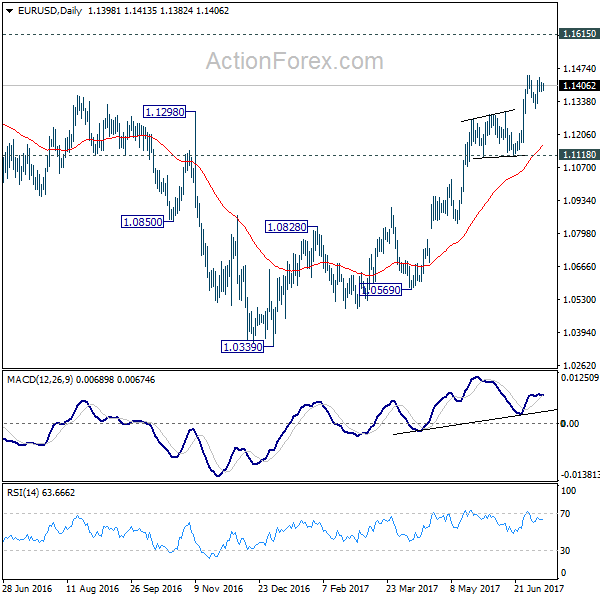

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1380; (P) 1.1399 (R1) 1.1417; More.....

Range trading in EUR/USD continues below 1.1444 short term top and intraday bias stays neutral. Another fall cannot be ruled out. But downside should be contained by 1.1291 resistance turned support to bring rise resumption. Break of 1.1444 will extend the rally from 1.0339 low to 1.1615 resistance next. Meanwhile, break of 1.1291 will turn focus back to 1.1118 support instead.

In the bigger picture, the firm break of 1.1298 resistance further affirm medium term reversal. That is an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Further rise would be seen to 55 month EMA (now at 1.1763). Sustained break there will pave the way to 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 next. This will now remain the favored case as long as 1.1118 support holds.

Pound Pummeled on Broadbent Comments

Sterling has turned lower after a speech by Bank of England Deputy Governor Ben Broadbent.

GBP is down -0.21% at £1.2861

Of late, sterling had found support on rhetoric from Bank of England (BoE) policymakers have hinted at a possible rate rise.

Mr. Broadbent did not mention monetary policy in his speech to the Scottish Council for Development and Industry, in Aberdeen, but was cautious on Brexit's impact on trade.

Mr. Broadbent said "a significant curtailment of trade with Europe would force the U.K to shift away from producing the things it's been relatively good at."

The market is paring back its bets on a rate hike actually happening at all this year

GBP/USD trades down -0.2% at £1.2855, down from £1.2917 before the speech. EUR/GBP is at €0.8865 vs. €0.8834 beforehand.

CAC Edges Lower, Markets Await Yellen

The CAC index has inched higher in the Monday session. Currently, the index is currently trading at 5156.30 and is down 0.27% on the day. On the release front, Eurozone Sentix Investor Confidence edged up to 28.4, above the estimate of 28.1. There are no French events on the schedule. On Wednesday, the Eurozone releases Industrial Production and Fed chair Janet Yellen will testify before the House Financial Services Committee.

French president Emmanuel Macron ran on a campaign of political and economic change, and the French government has acted quickly, promising to lower its budget deficit to the 3 percent of GDP. The 3 percent rule is required by the EU, but Brussels has chosen to turn a blind eye to the many members who run deficits above 3 percent. This move sends a message to the ECB that France is serious about economic reform. The French government is also eager to take advantage of Britain's departure from the European Union. The government wants to project a "finance-friendly" image, which is critical in France's efforts to lure financial sector jobs which are being relocated from London to the continent. On Tuesday, Prime Minister Edouard Philippe told a banking conference in Paris that he wants the city to become Europe's main financial hub after Brexit. This will be a tall order, as Frankfurt will likely be the most attractive choice for German and other companies that are downsizing their operations in London. Still, Philippe's comments underscore that France is looking for a bigger role on the international scene, and Brexit is a unique economic and political opportunity for Macron.

There was good news on the US employment front, as Nonfarm Payrolls rebounded in June, climbing to 222 thousand, its second highest gain in 2017. Although the markets reacted positively to the solid Nonfarm Payrolls report, expectations of a third rate hike in 2017 are tepid. A rate increase in September is very unlikely, with the odds pegged at just 13%, according to the CME Group. As for December, the likelihood of a rate hike is 50%, so the markets will need plenty of convincing that the Fed plans to make a move. What factors will raise the odds of a rate increase? First, second quarter growth will have to improve, after a weak performance in the first quarter, in which GDP rose just 1.4%. Second, stronger inflation levels would boost speculation of a rate hike. Currently, inflation is well below the Fed's target of 2%, and although Janet Yellen recently stated that the factors weighing on inflation were temporary, investors aren't convinced. Third, the Fed has outlined plans to reduce its bloated balance sheet, but has avoided providing any specifics. If the Fed started to lower the balance sheet in September, such a move would mark a vote of confidence in the economy and raise speculation of a rate hike to follow in December.

AUD/NZD Proceeds With Uptrend As Expected

The AUD/NZD went exactly as planned rejecting from the POC zone. Our previous AUD/NZD analysis showed a strong support which was respected and the pair proceeds with uptrend. The pair is above W H3 and D H5 which suggests strong uptrend. If we see a retracement, pay attention to POC 1.0465-85 (50.0, ATR pivot, W H3, D H5/H4, EMA89, inner trend line). As you can see this is the cluster of support so now moment buyers might be waiting for another chance to push the price higher. If the price breaks and closes above 1.0550, we might see 1.0600 - W H5 level.

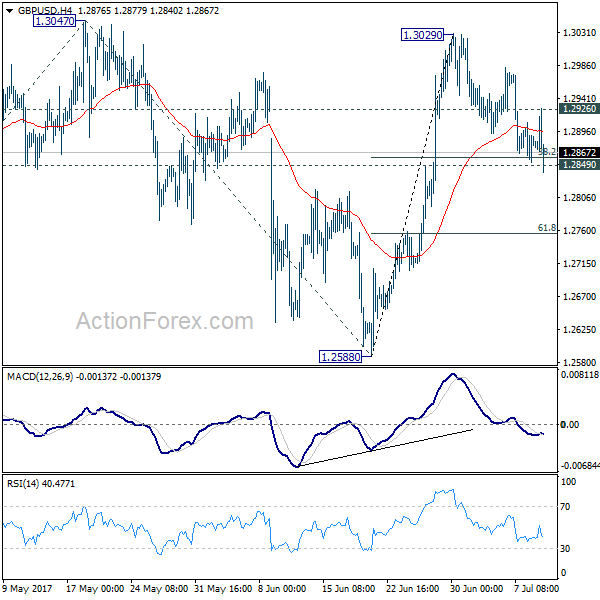

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2853; (P) 1.2881; (R1) 1.2907; More...

GBP/USD's corrective pull back from 1.3029 extends lower today and hits 1.2840. But it quickly recovers after hitting 1.2849 support. Intraday bias remains neutral first. We'd still expect downside to be contained by 1.2849 support to bring rise resumption. Above 1.2926 minor resistance should turn bias back to the upside for 1.3047 resistance. Break will target 61.8% projection of 1.2108 to 1.3047 from 1.2588 at 1.3168 next. However, sustained break of 1.2849 will dampen our near term bullish view and turn focus back to 1.2588 support.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is now in favor, overall outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

Sterling Dips after BoE Broadbent Comments, No Hint Equals No Hike?

The financial markets lack a general theme today. DOW opens flat and is set to extend recent range trading. European indices are trading mixed at the time of writing with FTSE and CAC in red. The strong rebound in Nikkei earlier today had no follow through in other markets. Gold is struggling in tight range between 1210/5 while WTI crude oil is bounded between 44/45. In the currency markets, Sterling dips notably as markets are disappointed by the lack of hints on monetary policy from BoE deputy. New Zealand Dollar remains the weakest for today, followed by Swiss Franc and Yen. Technical development in Sterling will be closely watched in the US session. Key levels are 1.2849 in GBP/USD, 0.8879 in EUR/GBP and 146.03 in GBP/JPY.

BoE Broadbent gave no hints on monetary policy

BoE Deputy Governor Ben Broadbent warned of risks of trade after Brexit. He noted that "a significant curtailment of trade with Europe would force the U.K. to shift away from producing the things it's been relatively good at, and therefore tends to export to the EU, and towards the things it currently imports and is relatively less good at." In particular, he cited the example of moving away from services exports that could hurt income and raise costs of food and machinery. While Broadbent didn't touch on monetary policies directly, his cautious tone argues that the is unlikely to vote for a rate hike in the next MPC meeting in August.

Released from UK, BRC retail sales monitor rose 1.2% yoy in June.

Australia firm on business conditions, Kiwi tumbles

Australia NAB business confidence rose 1 point to 9 in June. Business conditions gauge improved 4 points to 15. Most industrial performed well with strongest gains in wholesale, construction and manufacturing. On the other hand, mining was the worst performer due to falling commodity prices. The business conditions index is indicate back at pre-financial crisis level.

But confidence lagged behind and recorded slower rise in recent months. NAB noted that "we continue to be pleasantly surprised by just how upbeat the business sector is, given the context of a fairly beleaguered household sector that has been weighed down by limited wages growth and record levels of debt". However, it also warned that long term outlook could easily "underperform the RBA's upbeat expectations as important growth drivers (LNG exports, commodity prices and housing construction) begin to fade". Also from Australia, home loans rose 1.0% in May.

New Zealand dollar tumbles today as government data showed retail spending on credit and debit cards was unchanged in June. Some economists pointed out that's an import miss as there was expectations of a boost from the British and Irish Lions' rugby tour.

Elsewhere, Japan M2 rose 3.9% yoy in June, machine tools orders rose 31.1% in June. Canada housing starts rose to 213k in June. .

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2853; (P) 1.2881; (R1) 1.2907; More...

GBP/USD's corrective pull back from 1.3029 extends lower today and hits 1.2840. But it quickly recovers after hitting 1.2849 support. Intraday bias remains neutral first. We'd still expect downside to be contained by 1.2849 support to bring rise resumption. Above 1.2926 minor resistance should turn bias back to the upside for 1.3047 resistance. Break will target 61.8% projection of 1.2108 to 1.3047 from 1.2588 at 1.3168 next. However, sustained break of 1.2849 will dampen our near term bullish view and turn focus back to 1.2588 support.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is now in favor, overall outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Retail Sales Monitor Y/Y Jun | 1.20% | 0.50% | -0.40% | |

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Jun | 3.90% | 3.90% | 3.90% | 3.80% |

| 1:30 | AUD | NAB Business Confidence Jun | 9 | 7 | 8 | |

| 1:30 | AUD | Home Loans May | 1.00% | 1.50% | -1.90% | |

| 6:00 | JPY | Machine Tool Orders Y/Y Jun P | 31.10% | 24.50% | ||

| 12:15 | CAD | Housing Starts Jun | 213K | 200K | 195K |

DAX Ticks Higher as Investors Search for Cues

The DAX index has inched higher in the Tuesday session, as the index is up 0.20% on the day. Currently, the DAX is at 12,468.00. On the release front, there are no eurozone or German releases. On Wednesday, Germany releases WPI and the Eurozone publishes Industrial Production. In the US, Federal Reserve Chair Janet Yellen will testify before the House Financial Services Committee.

The German economy has looked solid in 2017, buoyed by strong consumer spending as well as an increased demand for German products, notably machinery. The manufacturing sector continues to expand, and Industrial Production improved to 1.2% in May, crushing the forecast of 0.2%. A strong export sector has led to an improved trade balance, and the trade surplus climbed to EUR 20.3 billion in May, which was the second highest surplus this year. The IMF has upgraded its forecast for the German growth to 1.8 percent in 2017, up from its estimate of 1.6 percent in April. Other eurozone members are not enjoying the same fiscal stability, and the question of the fiscal stance of the eurozone as a whole was a key topic as eurozone finance ministers met in Brussels on Monday. Germany has opposed attempts to define the bloc's fiscal stance as expansionary, and at the Monday meeting, the finance ministers agreed to aim for a"broadly neutral" stance. The European Commission wants to see Germany divert more resources to investment and public spending, given that the country is enjoying high growth.

Last week's US employment numbers were a mixed bag. Nonfarm Payrolls rebounded in June, climbing to 222 thousand. This easily beat the estimate of 175 thousand and marked a 4-month high. However, wage growth remained stuck at 0.2%, shy of the forecast of 0.3%. Weak wage growth has remained soft throughout the first half of 2017, which is somewhat puzzling, as the labor market remains extremely tight, with an unemployment rate of 4.4%. As well, there are widespread reports of a lack of qualified workers, but this hasn't translated into higher wages.

The markets reacted positively to the solid Nonfarm Payrolls report, but there expectations of a third rate hike in 2017 remain lukewarm. A rate increase in September is very unlikely, with the odds pegged at just 13%, according to the CME Group. As for December, the likelihood of a rate hike is 50%, so the markets will need plenty of convincing that the Fed plans to make a move. What factors will raise the odds of a rate increase? First, second quarter growth will have to improve, after a weak performance in the first quarter, in which GDP rose just 1.4%. Second, stronger inflation levels would boost speculation of a rate hike. Currently, inflation is well below the Fed's target of 2%, and although Janet Yellen recently stated that the factors weighing on inflation were temporary, investors aren't convinced. Third, the Fed has outlined plans to reduce its bloated balance sheet, but has avoided providing any specifics. If the Fed started to lower the balance sheet in September, such a move would mark a vote of confidence in the economy and raise speculation of a rate hike to follow in December.