Sample Category Title

Pound Edges Higher on Stronger UK Sales Growth

The British pound has posted slight gains in the Tuesday session. In North American trade, GBP/USD is trading at 1.2760. On the release front, British CBI Realized Sales impressed with a gain of 12 points, crushing the estimate of 4 points. As well, the BoE released its Financial Stability report.

British Prime Minister Theresa May gambled and lost, as she squandered her majority in parliament. May has had to deal with domestic critics, some who have been blistering in their attacks on her poor performance in the election. With the Brexit talks finally underway, May has to deal with European leaders who are still fuming at Britain's decision to depart the European Union. There was finally some good news on Monday for the embattled May, who reached an agreement with the DUP, a small Irish party, after weeks of negotiations. The DUP will not formally join the government, but has committed to support the government on its legislative agenda, Brexit and the budget. In return, May will provide Northern Ireland with an additional one billion pounds over the next two years. The deal should provide May with some breathing room in parliament, allowing her to shift gears from damage control and focus on the economy and the Brexit negotiations.

It's report card on Thursday, as the US releases Final GDP for the first quarter. Preliminary GDP, which was released in May, came in at 1.2%, and this is the forecast for the upcoming GDP report. Recent economic data has been softer than expected, notably construction and manufacturing reports. US durable goods releases were weak in May. Core Durable Goods broke a streak of two straight declines, but the weak gain of 0.1% missed expectations. Durable Goods declined 1.1%, its sharpest decline since June 2016. The slowdown in orders of business equipment could weigh on second quarter growth. Last week, it was the turn of construction numbers to disappoint, as Housing Starts and Building Permits both missed expectations. Consumer spending has also been softer than expected, and if Final GDP falls short of the modest estimate of 1.2%, the dollar could respond with losses.

Draghi Propels EUR/USD Close to the 1.13 Resistance

- European stocks markets lost up to 0.75% today. They managed to overcome an initial downleg, but eventual grinded lower on the back of a stronger euro and higher European rates. US stock markets opened nearly unchanged with Nasdaq again underperforming (-0.5%, correction tech rally).

- German bunds dropped and the euro shot higher following comments from ECB president Draghi that the euro area economic recovery remained on track, with signs of resurgent reflationary pressures (as opposed to the deflationary pressures previously). Still, Draghi did stress that caution in normalising monetary policy was warranted

- The BoE's Financial Stability Report set out plans to increase capital requirements for UK lenders to tackle risks posed by the recent rapid growth in consumer credit and prepare for the uncertain outcome of Brexit talks. Additionally, next month the BoE will publish new guidelines for consumer lending to ensure risks are managed.

- The IMF has cut US growth forecasts to 2.1% for 2017 and 2018 (previously 2.3% and 2.5%), calling the Trump budget proposal forecasts unrealistic. It suggested the US to stay open to trade and to skilled based immigration. It also stressed the importance of the financial regulation and of an independent Fed to continue raising interest rates.

- US eco data surprised on the upside of forecasts. Consumer confidence increased from 117.6 to 118.9 while consensus expected a decline to 116. The "expectations" component disappointed though. The Richmond manufacturing Fed index improved from 1 to 7 in June (vs 5 expected).

- Italy's consumer and manufacturing confidence surprised to the upside and stayed at elevated levels, boding well for the Q2 hard data to come.

Rates

Sharp correction lower of core bonds on Draghi

Just when traders were at risk of falling asleep after days of directionless trading, ECB president Draghi surprised them by explaining how the ECB could gradually unwind its non-conventional stimulus measures. It was clearly a turnaround of the ECB president, even if he remained very cautious and suggested that policy changes should be very gradually and depending on improving dynamics in the economy. "As the economy continues to recover, a constant policy stance will become more accommodative, and the central bank can accompany the recovery by adjusting the parameters of its policy instruments -- not in order to tighten the policy stance, but to keep it broadly unchanged." While Mario Draghi repeated that the governing council needs to be patient in letting inflation pressures build, his remarks should be considered as an early signal that policy will be adapted with a formal announcement of tapering likely at the September meeting, if the economy and inflation evolve as expected. He sounded also rather at ease with the recent low inflation readings which he attributed to energy effects and which don't ask for an immediate ECB reaction. "Our analysis suggests that the drivers of low oil prices at present are mainly supply factors, which a central bank can typically look through. And even if supply factors affect the path of inflation for some time, with inflation expectations secure, they should not ultimately affect the inflation trend". Draghi added that deflation is off the table and reflationary forces are working their way through the economy.

The Bund turned south and continued its march lower, gradually but surely. The euro gained more ground, equities fell, while US Treasuries followed Bunds. The German yield curve increased by 4.5 (2-yr) to 8 bps (5-yr). US yields rose 3.5 to 4.4 bps the belly slightly underperforming. The underperformance of the 5-yr clearly suggests the significance for the monetary policy outlook. On the intra-EMU bond market, yield spreads versus Germany were little changed.

Currencies

Draghi propels EUR/USD close to the 1.13 resistance

Modestly hawkish comments from ECB Draghi drove trading in the major FX cross rates today. EUR/USD started a protracted intraday uptrend and trades currently in the high 1.12 area. The 1.13 resistance is within reach. USD/JPY dropped temporary lower as sentiment turned risk-off. However, the pair returned to the high 112 area, supported by a rise in core bonds yields.

Asian equities traded mixed this morning. USD/JPY held near the recent highs hovering in the high 111 area. However a test of the 112.13 resistance didn't occur. EUR/USD settled in the 1.11 area. The recent sideways trading persisted.

European equities opened in a cautious risk off modus. Mid-morning, the headlines of a speech of ECB's Draghi at the ECB forum in Portugal triggered volatility across markets. The ECB president repeated that the EMU economy still needs ample monetary stimulation. However, he also mentioned that deflationary forces in the economy were replaced by reflationary ones. He also indicated that very gradual changes to the ECB stimulation might occur. EUR/USD moved to the 1.13 area and USD/JPY to 112, even as European equities were left with decent losses.

There was no new drivers to guide trading at the start of the US session. Traders keep a cautious wait-and-see modus ahead of Fed Yellen's speech later today.

UK government deal no big help for sterling

Two factors dominated sterling trading today: the comments from ECB president Draghi at the ECB forum in Sintra and the BoE's Financial stability report. The Draghi comments propelled the euro across the board. EUR/GBP jumped to the 0.8820 area . However, there were also modest positive spill-over effects on cable. The pair trended higher in the 1.27 big figure. In the financial stability report, the BOE showed some discomfort with easing credit standards UK banks are applying for consumer credit. The bank increased the cyclical capital buffer from June 2018 to address this issue. These measures can be considered as some kind of monetary tightening. In the end it might make a rate high (slightly) less probable. As such it can also be considered sterling negative. Especially EUR/GBP remained well bid after the publication of the financial stability report. EUR/GBP is trading in the 0.8845 area. 0.8854/66 resistance is within reach. The impact on cable was far less obvious as the pair mostly followed the EUR/USD rebound. The pair trades currently in the 1.2770/80 area.

Yen Steady as US Consumer Confidence

USD/JPY is trading quietly in the Tuesday session. In North American trade, the pair is trading at the 112 level. On the release front, there are no Japanese events on the schedule. In the US, CB Consumer Confidence XX . On Wednesday, Bank of Japan Governor Haruhiko Kuroda will address the ECB Forum of Central Bankers in Sintra, Portugal.

The Bank of Japan didn't stray from its message in the Summary of Opinions from its June policy meeting. Policymakers said that inflation would likely remain at low levels for an extensive period, and the bank's ultra-loose accommodative policy would stay in place until a stronger economy pushed up prices. The BoJ has been consistent in this message, but is mindful that a stronger Japanese economy has increased speculation that the bank might be planning an exit strategy from its stimulus program. In the summary, board members acknowledged that it was important for the BoJ to clearly communicate to the markets that the bank has no plans withdraw monetary stimulus anytime soon. Lower oil prices have contributed to weak inflation levels in Japan, and Governor Kuroda has reiterated that the BoJ will not tighten policy until inflation moves closer to the bank's target of 2.0%.

Investors are casting a nervous glance at Thursday, when the US releases Final GDP for the first quarter. Preliminary GDP, which was released in May, came in at 1.2%, and this is the forecast for the upcoming GDP report. Recent economic data has been softer than expected, notably construction and manufacturing reports. US durable goods releases were weak in May. Core Durable Goods broke a streak of two straight declines, but the weak gain of 0.1% missed expectations. Durable Goods declined 1.1%, its sharpest decline since June 2016. The slowdown in orders of business equipment could weigh on second quarter growth. Last week, it was the turn of construction numbers to disappoint, as Housing Starts and Building Permits both missed expectations. Consumer spending has also been softer than expected, and if Final GDP falls short of the modest estimate of 1.2%, the dollar could respond with losses.

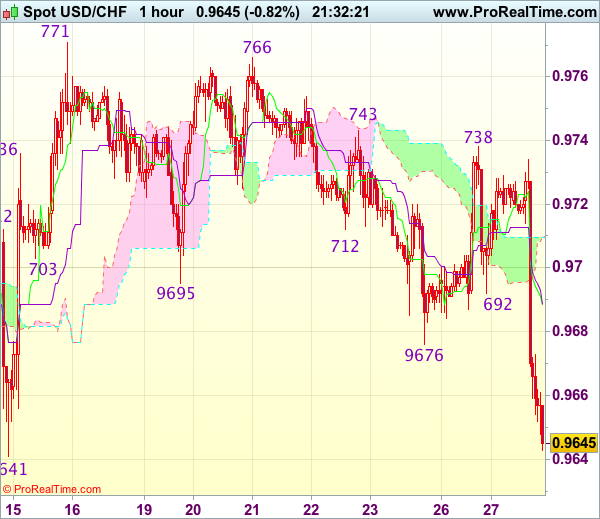

Trade Idea Update: USD/CHF – Sell at 0.9680

USD/CHF - 0.9647

New strategy :

Sell at 0.9680, Target: 0.9580, Stop: 0.9715

Position : -

Target : -

Stop : -

The greenback met renewed selling interest at 0.9738 and has dropped sharply on dollar’s broad-based weakness vs European currencies, suggesting the decline from 0.9771 top is still in progress and bearishness remains for further weakness towards recent low at 0.9613, however, break there is needed to provide confirmation that downtrend has resumed for further fall to 0.9575-80 and later towards 0.9550.

In view of this, we are looking to sell dollar on recovery as previous support at 0.9676 should turn into resistance and limit dollar’s upside, bring another decline. Above another previous support at 0.9692 would defer and risk a stronger rebound to 0.9715-20 but only break of resistance at 0.9738-43 would signal low is formed.

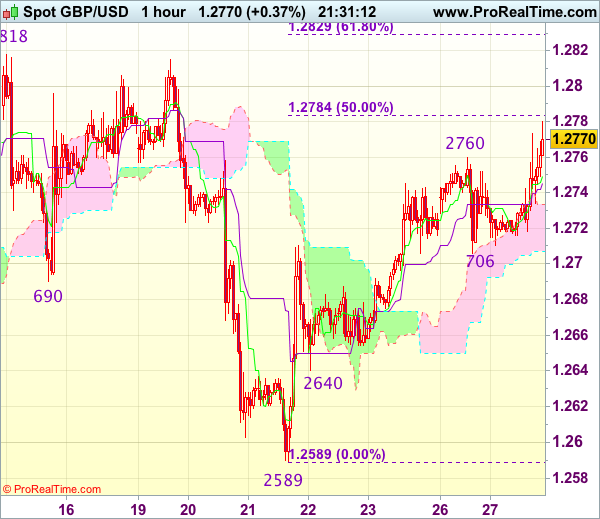

Trade Idea Update: GBP/USD – Buy at 1.2710

GBP/USD - 1.2771

New strategy :

Buy at 1.2710, Target: 1.2810, Stop: 1.2675

Position : -

Target : -

Stop : -

As cable has risen again after finding renewed buying interest at 1.2706, suggesting the erratic rise from 1.2589 low is still in progress and upside bias is seen for further gain to 1.2780-85 (50% Fibonacci retracement of 1.2978-1.2589), then towards resistance at 1.2818, however, break of latter level is needed to retain bullishness and extend the aforesaid rise to 1.2830 (approx. 61.8% Fibonacci retracement).

In view of this, would not chase this move here and would be prudent to buy cable on pullback as said support at 1.2706 should limit downside. Below 1.2680 would defer and suggest an intra-day top is formed instead, risk weakness to 1.2660 but support at 1.2640 should remain intact.

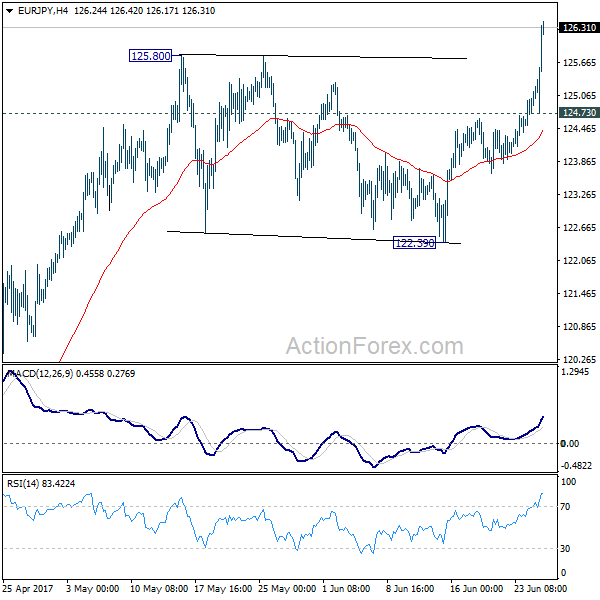

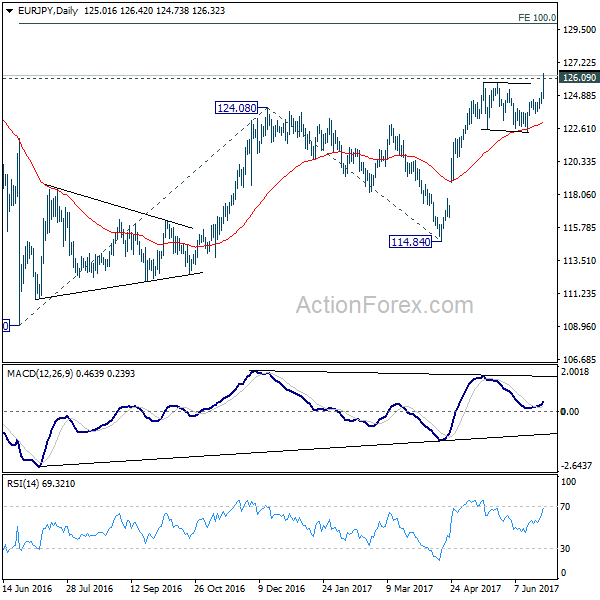

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 124.60; (P) 124.87; (R1) 125.34; More...

EUR/JPY surges to as high as 126.24 and broke 125.80/126.09 resistance zone. The development indicates resumption of rise from 114.84 and that from 109.03. Intraday bias is back on the upside for 100% projection of 109.03 to 124.08 from 114.84 at 129.89. On the downside, below 124.73 minor support will turn bias neutral first. But outlook will stay bullish as long as 122.39 support holds.

In the bigger picture, focus is staying on 126.09 support turned resistance. Decisive break there will confirm completion of the down trend from 149.76. And in such case, rise from 109.20 is at the same degree and should target 141.04 resistance and above. Meanwhile, rejection from 126.09 and break of 114.84 will extend the fall from 149.76 through 109.20 low.

Trade Idea Update: EUR/USD – Buy at 1.1260

EUR/USD - 1.1299

New strategy :

Buy at 1.1260, Target: 1.1360, Stop: 1.1225

Position : -

Target : -

Stop : -

The single currency has rallied today and just broke above previous resistance at 1.1296, confirming recent upmove has resumed and bullishness is seen for further gain to 1.1335-40 (50% projection of 1.0839-1.1296 measuring from 1.1119), then towards 1.1360, however, near term overbought condition should prevent sharp move beyond 1.1400 (61.8% projection), risk from there is seen for a retreat later.

In view of this, would not chase this rise here and would be prudent to buy euro on pullback as 1.1250-60 should limit downside. Below the Kijun-Sen (now at 1.1240) would defer and risk test of previous resistance at 1.1220 but break there is needed to confirm an intra-day top is formed, bring correction towards 1.1180-85 later.

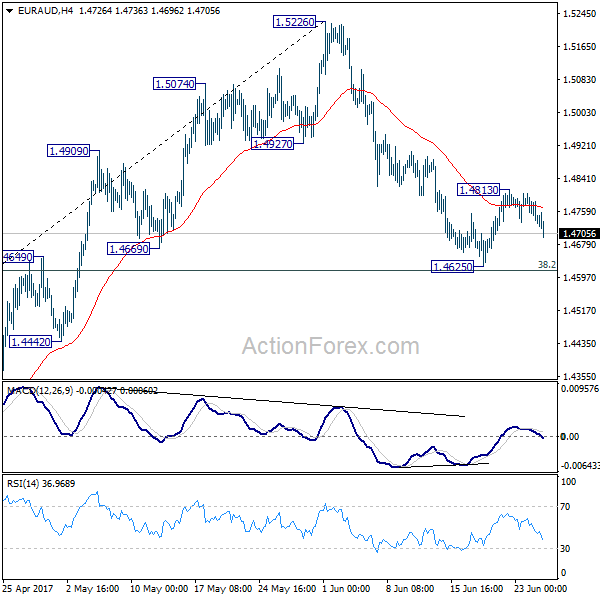

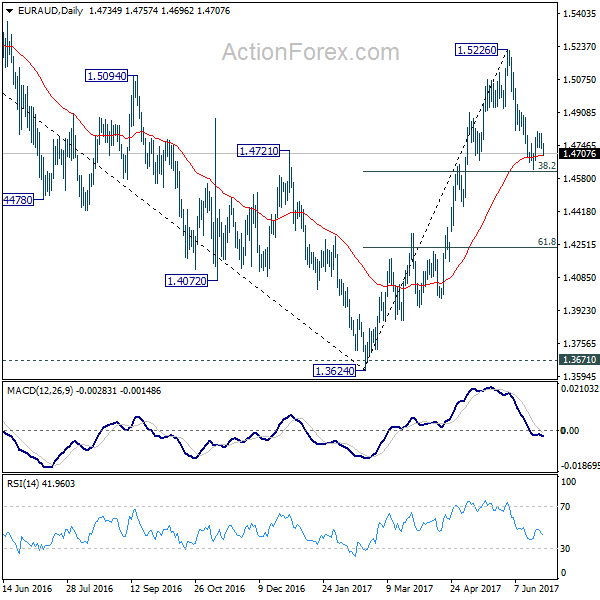

EUR/AUD Mid-Day Outlook

Daily Pivots: (S1) 1.4714; (P) 1.4758; (R1) 1.4785; More...

EUR/AUD's strong rise and break of 1.4813 indicates resumption of rebound from 1.4625. The development is in line with the view that pull back from 1.5226 has completed, ahead of 38.2% retracement of 1.3624 to 1.5226 at 1.4614. Intraday bias is turned back to the upside for retesting 1.5226 first. On the downside, below 1.4680 will turn bias back to the downside for 1.4625.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction should be completed at 1.3624 after defending 1.3671 key support. Rise from 1.3642 would extend to 61.8% retracement of 1.6587 to 1.3624 at 1.5455. Sustained break there will pave the way to retest 1.6587. However, sustained break of 1.4669 support will dampen this bullish view. We'll assess the outlook later after looking at the structure and depth of the pull back.

DAX Dips as Draghi Says ECB Stimulus to Continue

The DAX index has lost ground in the Tuesday session. Currently, the index is at 12,679.50, down 0.72%. On the release front, there are no German or eurozone releases. Earlier in the day, ECB President Mario Draghi addressed the ECB Forum on Central Banking. On Wednesday, Draghi will again address the forum, and Germany will release Import Prices.

The markets were listening closely as ECB President Mario Draghi addressed the ECB Forum on Tuesday, and although the euro responded positively, Draghi's message to the markets was essentially "more of the same". Draghi acknowledged that economic indicators were showing a broadening recovery in the eurozone, but pointed to inflation as the barrier to tightening policy. Draghi defended the bank's loose accommodative policy, saying that it had pushed inflation higher, but stimulus was needed until inflation becomes "durable and self-sustaining". Germany is not happy with the ECB's current monetary policy, as it feels that tighter policy is more appropriate for the strong German economy. For his part, Draghi has no intentions of altering current policy until inflation moves closer to the ECB's target of 2 percent, and he has been consistent in this message.

It was a busy weekend in Italy, as the Italian government announced that would bail out two ailing banks, Banca Popolare di Vicenza and Veneto Banca. This deal will cost the Italian taxpayer 5.2 billion euros, and the government provided additional guarantees of 12 billion euros. Italy has already agreed to bail out another Italian bank, Monte dei Pashci di Siena, for up to 6.6 billion euros. The Italian government has set aside 20 billion euros to bail out struggling banks, and potentially may have used up the entire amount for these bailouts, depending on how the actual size of the bailouts. European stock markets reacted positively to the move, and Deustche Bank and Commerzbank both started the week with gains. The bailouts remove a major headache for European regulators and should strengthen the fragile Italian banking sector, which has had times been in crisis mode, threatening the stability of the eurozone financial sector.

AUD/NZD is Supported at 1.0360

Today we witnessed a slowing growth in the NZ Trade Balance, which fell below forecasts. It has followed a string of positive data from NZ, but as we saw last week, in my opinion. there was a slightly dovish stance from the RBNZ. Despite this, the NZD has made gains against the AUD for the past 3 months, particularly as Iron Ore, Gold and LNG prices have been retreating, thus being negative for the AUD. We are very close to the Daily long term trend line since April 2015, and we might see supports around 1.036.

That being said, the POC zone (D L4, ATR low, trend line, historical buyers) comes within 1.0360-75 and a retrace within the zone should spike the price up. Important level to watch is also 1.0394 and X cross of trend line and D H3. A continuation and daily close above 1.0433 will possibly prolong an uptrend move in the pair targeting 1.0475 and 1.0525. A daily close below 1.0350 could negate this scenario.