Sample Category Title

Market Update – European Session: UK Retail Sales Miss Expectations, No Surprises Expected From BOE

Notes/Observations

SNB leaves policy steady but reiterates concerns about CHF currency (Franc)

UK retail sales miss expectations as accelerating inflation squeezed British wallets

No surprises expected from BOE; to maintain its policy steady

Eurogroup expected to approve Greece 2nd bailout review; works towards achieving a sustainable debt solution

Overnight

Asia:

New Zealand Q1 GDP came in softer-than expected (Q/Q: 0.5% v 0.7%e; Y/Y: 2.5% v 2.7%e

Australia Jun Consumer Inflation Expectation it's a 6-month low (3.6% v 4.0% prior)

Australia May Employment Change saw its 3rd straight month of increases (+42.0K v +10.0Ke); with Unemployment Rate hitting a 4-year low (5.5% v 5.7%e)

Europe:

UK govt said to plan a 'very generous' post-Brexit offer to EU citizens. To guarantee EU nationals living in the UK the same rights as they currently hold. Expected to move cutoff date for citizens' rights from March 2017 to Brexit day in 2019

Chancellor of Exchequer Hammond to make case at Mansion House speech for a ‘pragmatic Brexit'

German Chancellor Merkel: Europe was ready for Brexit talks; door to Europe was open but decision is up to the British

ECB's Rimsevics (Latvia): ECB should be predictable and not cause any surprises. Forward guidance was important and did not want to have any surprises

Americas:

FOMC raised Fed Funds target by 25bps to 1.00-1.25% range ( as expected) in a 8-1 vote (Kashkari again dissented). It saw cutting reinvestment beginning in 2017 and expanded on quarterly basis until it reached $30M/month for treasuries and $20B/month in mortgaged-backed securities

Fed chair Yellen Press Conference: noted that it had not seen any evident upward pressure on inflation; Fed credibility had not been impaired; quite essential to have policies to get inflation to target

Special counsel Mueller said to be investigating President Trump for possible obstruction of justice

US Senate voted by 97-2 margin to increase Russia sanctions due to alleged interference in 2016 elections/annexation of Crimea/support from Syria Govt

Economic Data

(SE) Sweden May PES Unemployment Rate: 3.7% v 3.8% prior

(FR) France May Final CPI M/M: 0.0% v 0.1%e; Y/Y: 0.8% v 0.8%e

(FR) France May Final CPI EU Harmonized M/M: 0.0% v 0.0%e; Y/Y: % v 0.9%e, CPI Ex-Tobacco Index: 101.28 v 101.31e

(CH) Swiss May Producer & Import Prices M/M: -0.2% v -0.1%e; Y/Y: 0.1% v 0.2%e

(CH) Swiss National Bank (SNB) left its Deposit Interest Rate unchanged at -0.75% and maintained the 3-Month Libor Range unchanged between -0.25 to -1.25% (as expected)

(IT) Italy May Final CPI (including tobacco) M/M: -0.2% v -0.2% prelim; Y/Y: 1.4% v 1.4% prelim

(IT) Italy May Final CPI EU Harmonized M/M: -0.1% v -0.2% prelim; Y/Y: 1.6% v 1.5%e v 1.5% prelim

(UK) May Retail Sales (Ex Auto Fuel) M/M: -1.6% v -1.0%e; Y/Y: 0.6% v 1.9%e

(UK) May Retail Sales (Inc Auto Fuel) M/M: -1.2% v -0.8%e; Y/Y: 0.9% v 1.6%e

(IT) Italy Apr General Government Debt: €2.270T v €2.260T prior (record high)

(EU) Euro Zone Apr Trade Balance (Seasonally Adj): €19.6B v €22.0Be ; Trade Balance: €17.9B v €28.5Be

Fixed Income Issuance:

(ES) Spain Debt Agency (Tesoro) sold totyal €4.23B vs. €4.0-5.0B indicated range in 2022, 2027, 2032 and 2037 bonds

Sold €1.82B in 0.4% Apr 2022 SPGB; Avg yield: 0.215% v 0.369% prior; Bid-to-cover: 1.41x v 2.18x prior

Sold €1.06B in 1.5% Apr 2027 SPGB; Avg yield: 1.395% v 1.548% prior; Bid-to-cover: 1.78x v 1.43x prior

Sold €690M in 5.75% July 2032 SPGB; Avg Yield 1.925% v 2.116% prior; Bid-to-cover: 1.47x v 1.65x prior

Sold €630M in 4.20% Jan 2037 SPGB; Avg Yield: 2.314% v 2.604% prior; Bid-to-cover: 1.58x v 1.54x prior

(FR) France Debt Agency (AFT) sold total €7.955B vs. €7.0-8.0B indicated range in 2020, 2022 and 2023 Oats (4 tranches)

Sold €2.40B in 0.00% Feb 2020 Oat; Avg Yield: -0.48% v -0.45% prior; Bid-to-cover: 2.65x v 2.10x prior

Sold €2.166B in 0.00% May 2022 Oat; Avg yield: -0.22% v -0.12% prior; Bid-to-cover: 1.62x v 1.86x prior

Sold €1.656B in 3.00% Apr 2022 Oat; avg yield: -0.26% v -0.06% prior; Bid-to-cover: 1.91x v 2.44x prior

Sold €1.733B in 4.25% 2023 Oat; Avg Yield: -0.06% v -0.14% prior; Bid-to-cover: 2.00x v 1.95x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx50 -0.8% at 3518, FTSE -0.7% at 7423, DAX -0.6% at 12725, CAC-40 -0.9% at 5197, IBEX-35 -1.2% at 10645, FTSE MIB -0.4% at 20870, SMI -0.4% at 8817, S&P 500 Futures -0.5%]

Market Focal Points/Key Themes European Indices trade lower across the board following on from a rate rise as well as weaker inflation and retail sales figures out of the US. The UK also posted Retail sales which fell short of expectations as rising inflation and falling wage growth weigh. On the corporate front DFS trades sharply lower after the Furniture retailer cut EBITDA guidance, whilst OHL trades higher after OHL Mexico is to be acquired for MXN27/shr. Looking ahead key events include the BoE rate decision at 12BST, whilst in the US, scheduled earnings include Kroger and Bob Evans Farms.

Equities

Consumer discretionary [Poyry [POY1V.FI] +29% (Raised guidance), Majestic Wines [WINES.UK] -2.8% (Earnings), DFS [DFS.UK] -22% (Cuts outlook), Wizz Air [WIZZ.UK] -8% (Placing), Next [NXT.UK] -3% (Analyst Downgrade), H&M [HMB.SE] -3% (May Sales)]

Industrials: [OHL [OHL.ES] +13% (Magenta Infraestructura, IFM Global Infrastructure Fund to acquire OHL Mexico for MXN27/shr)]

Healthcare: [Basilia [BSLN.CH] +6.7% (Licence agreement with Pfizer)]

Speakers

Swiss National Bank (SNB) quarterly policy statement reiterated CHF currency (Franc) remained significantly overvalued and would remain active in FX markets and intervene if necessary . To regularly reassess the need for an adjustment of the countercyclical capital buffer

SNB's Jordan post rate decision press conference: Inflation remained very low; expansionary monetary policy remained necessary to ensure price stability. Inflation expectations were within the range that was consistent with SNB's definition of price stability

SNB's Zurbruegg: To monitor mortgage-market developments and assess the need for any capital-buffer adjustment. More progress needed on bank resolution

SNB's Maechler: Inflation outlook in major economies were muted

SNB Financial Stability Report saw conditions of Swiss banking sector continuing to improve. Low interest rates carry some risks for financial stability

Greece Econ Min Papadimitriou said to accuse German Fin Min Schaeuble of being "dishonest" by blocking debt relief despite his acknowledgement that Athens has implemented significant reforms

Romania President: To ask ruling coalition to solve internal crisis after Social Democrats party withdrew support for its PM

Currencies

USD maintained a firmer tone in the aftermath of the FOMC rate decision. Markets had priced in a ‘dovish Fed rate hike'. However, a rather upbeat tone on the US economy and path for interest-rate increases remained intact despite recent disappointing economic data

GBP was softer ahead of the BOE rate decision. More weak UK data weighted upon the pound. May UK retail sales data seemed to confirm that accelerating inflation squeezed British wallets. GBP/USD probing the lower end of the 1.27 level just ahead of the NY morning. No surprises expected from the BOE with the vote to keep policy steady expected to remain at 7-1 with Forbes again likely to be the sole dissenter in her last policy meeting.

EUR/USD dipping below the 1.12 level with the move attributed to the more ‘hawkish Fed' commentary from Thursday.

Fixed Income

Bund futurestrade at 165.17 down 23 ticks after topping out at 165.55. Resistance lies near the 165.95 level followed by 166.21. A break of the 164.65 support level could see lows target 163.70 followed by 160.30.

Gilt futures trade at 129.81 lower by 41 ticks, along with other core bonds. The focus remains the BOE Rate decision at 12PM London time. Gilts have been rising steadily since May 9th. Price still finds initial support at the 129.14 level, with key support at the 128.27 support level. An acceleration lower could test the 127.43 region. Resistance lies at the 130.28 level followed by 132.65.

Thursday's liquidity report showed Wednesday's excess liquidity fell to €1.6760T a slight gain of €2.5B from €1.6785T prior. Use of the marginal lending facility rose to €180M from €178M prior.

Corporate issuance saw over $500M come to market via 1 issue from Yapi Ve Kredi senior unsecured note offering

Looking Ahead

(ID) Indonesia Central Bank (BI) Interest Rate Decision: Expected to leave Reverse Repo Rate unchanged at 4.75%

(PE) Peru May Unemployment Rate: 7.2%e v 6.8% prior

(PE) Peru Apr Economic Activity (Monthly GDP) Y/Y: 1.0%e v 0.7% prior

(CO) Colombia May Consumer Confidence Index: No est v -12.8 prior

05:30 (HU) Hungary Debt Agency (AKK) to sell 12-month bills

05:30 (HU) Hungary Debt Agency (AKK) to sell Floating Rate Notes

05:30 (IE) Ireland Debt Agency (NTMA) to sell €500M in 12-month Bills

05:50 (FR) France Debt Agency (AFT) to sell €1.0-1.5B in 2025, 2027 and 2047 I/L bonds (Oatei)

06:45 (US) Daily Libor Fixing

07:00 (UK) Bank of England Bank (BOE) Interest Rate Decision: Expected to leave Interest Rates unchanged at 0.25%; maintain Asset Purchase Target (AFT) at £435B

07:00 (TR) Turkey Central Bank (CBRT) Interest Rate Decision: Expected to leave Benchmark Repurchase Rate unchanged at 8.00% (all key rates unchanged)

08:15 (UK) Baltic Dry Bulk Index

08:30 (US) Jun Empire Manufacturing: +5.0e v -1 prior

08:30 (US) Jun Philadelphia Fed Business Outlook: 24.9e v 38.8 prior

08:30 (US) May Import Price Index M/M: -0.1%e v 0.5% prior; Y/Y: 2.9%e v 4.1% prior; Import Price Index (ex-petroleum) M/M: No est v 0.4% prior

08:30 (US) May Export Price M/M: 0.2%e v 0.2% prior; Y/Y: No est v 3.0% prior

08:30 (US) Initial Jobless Claims: 241Ke v 245K prior; Continuing Claims: 1.92Me v 1.917M prior

08:30 (US) Weekly USDA Net Export Sales

09:00 (RU) Russia Gold and Forex Reserve w/e Jun 9th: No est v $406.9B prior

09:00 (BE) Belgium Apr Trade Balance: No est v -€1.5B prior

09:00 (CA) Canada May Existing Home Sales M/M: No est v -1.7% prior

(EU) European Finance Ministers (Eurogroup) meet in Luxembourg

09:15 (US) May Industrial Production M/M: 0.2%e v 1.0% prior; Capacity Utilization: 76.8%e v 76.7% prior, Manufacturing Production: 0.1%e v 1.0% prior

10:00 (US) Jun NAHB Housing Market Index: 70e v 70 prior

10:30 (US) Weekly EIA Natural Gas Inventories

11:30 (IL) Israel May CPI M/M: 0.4%e v 0.2% prior; Y/Y: 0.7%e v 0.7% prior

12:00 (IS) Iceland May International Reserves (ISK): No est v 684B prior

12:00 (CA) Canada to sell 3-Year Bonds

15:00 (CO) Colombia Apr Industrial Production Y/Y: -5.6%e v +4.8% prior

15:00 (CO) Colombia Apr Retail Sales Y/Y: -2.1%e v +1.9% prior

16:00 (US) Apr Total Net TIC Flows: No est v -$0.7B prior; Long-term TIC Flows: No est v $59.8B prior

18:00 (CL) Chile Central Bank (BCCH) Interest Rate Decision: Expected to leave Overnight Rate Target unchanged at 2.50%

BoE Meeting To Be Dominated By Doves

The political chaos in Westminster, uncertainty over the UK's economic outlook and ongoing Brexit concerns should encourage the Bank of England to 'stand pat' on rates in Thursday's MPC meeting. With the central bank highly unlikely to make any changes to monetary policy amid the instability, investors will most likely direct their attention towards Mark Carney for insights on how he plans to tackle the various challenges thatthe UK political climate and Brexit developments have presented.

While inflation in the UK has hit a four-year high at 2.9%, wage growth remains subdued and this creates further headaches for the BoE. Although raising interest rates to cool inflation is seen as a practical strategy, it may simply end up pressuring borrowers ultimately eroding business confidence and pinching consumers further.

Prior to the anticipated BoE meeting, the British Pound was vulnerable to heavy losses following the disappointing 1.2% decline in UK retail sales in May which fueled fears of Brexit negatively impacting the UK economy. UK retail sales have plunged for the second time in three months as rising inflation diminishesthe purchasing power of consumers. With wage growth struggling to keep up with inflation, concerns may mount over the sustainability ofthe UK's consumer-driven economic growth.

Fundamentally, Sterling remains gripped by political uncertainty while ongoing Brexit woes have obstructed upside gains. With recent economic data following a negative trajectory, Sterling bears could be instilled with enough inspiration to send the GBPUSD towards 1.2600.

Yellen dishes out hawkish surprise

Financial markets were caught completely off guard during late trading on Wednesday after the Federal Reserve adopted a firmly hawkish stance and even displayed some optimism overeconomic growth despite mounting concerns over weak inflation. The tone of caution investors were anticipating from the Fed was replaced by a strong determination to continue tightening in response to falling employment while accepting the prolonged periods of weak inflation this year. Although the hawkish surprise offered a temporary boost to the Dollar, markets have not bought into this newfound optimism as expectations of another interest rate increase in 2017 currently stands below 50%.

With the recent economic developments in the US encouraging FOMC members to trim their medium estimates for inflation to 1.6% this year, the central bank may be in no rush to hike rates again in the coming months. It should be kept in mind that US consumer prices unexpectedly declined in May and retail sales recorded their biggest drop in 16 months which questions whether the Federal Reserve has become excessively hawkish. While the Fed has repeatedly stated that this period of economic softness is 'transitory' this will be put to the test in the coming months as participants heavily scrutinize economic data.

The central bank also shared details about how it would reduce its massive $4.5 trillion balance sheet this year which complimented the hawkish rhetoric.

All in all, there seems to be a disconnect between what the markets anticipate and what the Fed is signaling with investors needing more persuasion on the Federal Reserve's ability to raise rates again. This persuasion could be in the form of improving economic data but until then, the Dollar Index remains under pressure on the daily charts with further weakness opening a path towards 96.50.

Oil markets drowned by oversupply fears

WTI Crude was exposed to heavy losses on Wednesday with selling activity invading Thursday's trading session after an unexpectedly large build in gasoline inventories fuelled oversupply fears. It is becoming quite clear that despite OPEC's valiant efforts to rebalance the saturated markets by trimming output, the global glut continues and has left oil trading at depressed levels.

With the bearish price action on WTI Crude suggesting that those who were heavily bullish on the commodity maybe having second thoughts, the upside may be limited. I believe sentiment towards oil remains heavily bearish and further losses should be expected as oversupply concerns inspire sellers to attack the commodity ruthlessly.

USD/CHF Trading Mixed, USD/CAD Bearish Breakout, AUD/USD Wide-Open For Further Increase.

USD/CHF Trading mixed.

USD/CHF continues its decline despite some ongoing consolidation. Hourly resistance can be found at 0.9727 (09/06/2017 high). Strong resistance is given at 1.0107 (10/04/2017 high). Expected to show continued weakness towards hourly support at 0.9614 (06/06/2017 low).

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/CAD Bearish breakout.

USD/CAD has strongly declined. Hourly support found at 1.3324 (13/04/2017 high) has been broken. Expected to show continued weakness.

In the longer term, there is now a death cross with the 50 dma crossing below the 200 dma indicating further downside pressures. Strong resistance is given at 1.4690 (22/01/2016 high). Long-term support can be found at 1.2461 (16/03/2015 low)

AUD/USD Wide-open for further increase.

AUD/USD is pushing higher since the pair has failed to reach hourly support given at 0.7329 (09/05/2017 low). As long as prices remain below resistance at 0.7608 (17/04/2017 high), there are nonetheless strong downside risks.

In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.

EUR/USD Weakening, GBP/USD Volatility Increases, USD/JPY Ready For Another Leg Lower.

EUR/USD Weakening.

EUR/USD is trading lower. The pair is still trading below strong resistance given at 1.1300 (09/11/2017 high). Hourly support is given at 1.1110 (22/05/2017 low) has been broken. Stronger support lies at 1.0842 (11/05/2017 low) and key support is given at 1.0494 (22/02/2017 low). Expected to show renewed bullish pressures.

In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD Volatility increases.

GBP/USD is now pushing up and down around former hourly support given at 1.2757 (21/04/2017 low). Hourly resistance lies at 1.3046 (18/05/2017 high). Expected to show further decline.

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY Ready for another leg lower.

USD/JPY 's short-term bearish pressures are back. The pair is bouncing lower. Hourly support can be found at 108.89 (14/06/2017 high). Strong support is located at 108.13 (17/04/2017 low). Hourly resistance is given at 110.81 (09/06/2017 high). Other key supports lie at a distance 106.04 (11/11/2016 low). Wide-open for further decline.

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

Technical Outlook: US Oil Eyes Key $43.74 Support After Another Hit From Oil Inventories Data

US oil remains under strong pressure and posted marginally lower low at $44.37 9te lowest since early May) on Thursday, following sharp fall after data on Wednesday.

EIA report showed draw in crude inventories of 1.7 million barrels for the week ended June 2, which was well below forecasted draw of 2.7 million barrels.

Another hit came from unexpected build of gasoline inventories which rose by 2 million barrels, compared to forecasted draw of 0.45 million barrels.

Oil prices remain pressured by global oversupply, particularly in rising production of US shale oil and non-OPEC oil producers which offsets OPEC efforts to stabilize oil prices by extension of oil production cut.

Technical studies remain firmly bearish and see scope for final push towards key support at $43.74 (05 May low). Wednesday's long bearish candle weighs heavily, however, oversold daily studies suggest the price may take a break before final push lower, but no firmer bullish signals seen so far. Falling 10SMA ($46.16) and Tenkan-sen ($46.38) mark strong resistances.

Res: 44.79, 45.19, 45.55, 46.16

Sup: 44.37, 44.00, 43.74, 43.56

Trade Idea: GBP/USD – Sell at 1.2850

GBP/USD – 1.2755

Recent wave: Wave V of larger degree wave (III) has ended at 1.1986 and major correction has commenced from there for gain to 1.3000 and 1.3140-50

Trend: Near term down

Original strategy :

Sell at 1.2850, Target: 1.2650, Stop: 1.2910

Position: -

Target: -

Stop: -

New strategy :

Sell at 1.2750, Target: 1.2650, Stop: 1.2810

Position: -

Target: -

Stop:-

Sterling ran into resistance at 1.2818 and has retreated sharply on dollar’s broad-based strength, suggesting the rebound from 1.2635 has ended there, hence consolidation with downside bias is seen for weakness to 1.2670-75, however, break of said support at 1.2635 is needed to confirm recent decline from 1.3048 top has resumed for retracement of recent upmove to 1.2600 but downside should be limited to 1.2550 and reckon previous support at 1.2515 would hold from here.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has ended at 1.7192, the subsequent selloff is the larger degree wave (C) which is still unfolding with minor wave (III) of larger degree wave 3 ended at 1.1986, hence wave (IV) correction is in progress which could either be a triangle wave (IV) of a complex formation but upside should be limited to 1.3500 and price should falter well below 1.4000, bring another decline in wave (V) of 3 for weakness to 1.1500, then 1.1200.

On the upside, expect recovery to be limited to 1.2750-55 and 1.2790-00 should hold, bring another decline. Above said resistance at 1.2818 would defer and risk a stronger rebound to 1.2860-70 would but price should falter below 1.2900, bring another selloff later.

Trade Idea: GBP/JPY – Sell at 140.40

GBP/JPY - 139.25

Recent wave: Medium term low formed at 120.50 and (A)-(B)-(C) major correction has commenced with (A) leg ended at 148.45, hence wave (B) is unfolding for retreat to 131.00-10.

Trend: Near term down

Original strategy:

Sell at 141.50, Target: 139.50, Stop: 142.10

Position: -

Target: -

Stop: -

New strategy :

Sell at 140.40, Target: 138.50, Stop: 141.00

Position: -

Target: -

Stop:-

As sterling has retreated after meeting resistance at 140.90 yesterday, suggesting the rebound from 138.70 has possibly ended there and consolidation with downside bias remains, break of said support at 138.70 would confirm recent decline from 148.10 top has resumed for further subsequent weakness to 138.45-50, then towards 138.00, however, near term oversold condition should limit downside to 137.50 today.

In view of this, would not chase this fall here and we are looking to sell sterling again on recovery as 140.40-50 should limit upside. Above said resistance at 140.90 would defer and risk a stronger recovery to 141.15-20, then 141.50, however, still reckon upside would be limited to 142.00 and price should falter below resistance at 142.75, bring another decline later.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.

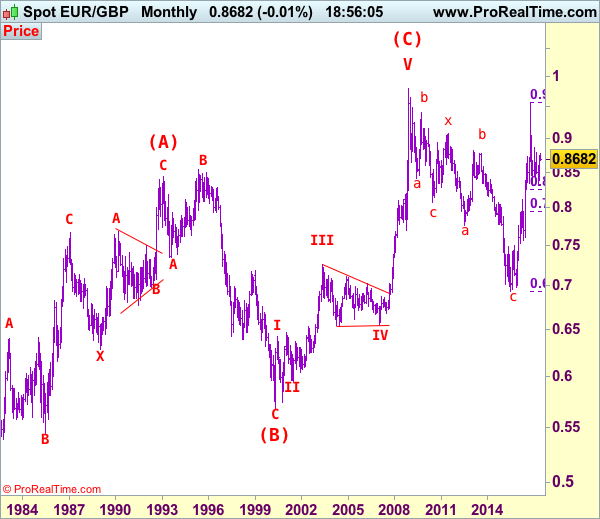

EUR/GBP Elliott Wave Analysis

EUR/GBP – 0.8679

EUR/GBP – The major (A)(B)(C)-(X)-(A)(B)(C) correction from 0.9805 is unfolding and 2nd (A) has possibly ended at 0.6936.

As the single currency has risen again and broke above previous resistance at 0.8857, adding credence to our bullishness for the erratic rise from 0.8304 to extend further gain to 0.8900, then towards 0.8940-50 (50% Fibonacci retracement of 0.9576-0.8304), however, loss of upward momentum should prevent sharp move beyond 0.9000 psychological level and price should falter below 0.9090-00 (61.8% Fibonacci retracement) and bring retreat later.

Our latest preferred count is that the wave V of a 5-wave series from 0.5682 ended at 0.9805 earlier and major from there has possibly ended at 0.8067 as A-B-C-X-A-B-C. We are keeping our view that the entire correction from 0.9805 has possibly ended at 0.7756 and as labeled as the attached daily chart and impulsive move from 0.9084 has ended at 0.7756 as a 5-waver which marked either the (C) wave or the A leg of (C), a daily close above resistance at 0.8831 would suggest (C) leg has ended and headway towards 0.9084.

On the downside, whilst initial pullback to 0.8740-45 cannot be rule out, reckon 0.8680-90 would limit downside and bring another rise later. A daily close below support at 0.8652 would suggest top is possibly formed and risk weakness towards 0.8600-05 but reckon downside would be limited to 0.8550 and previous support at 0.8524 should hold from here, bring rebound later.

Recommendation: Buy at 0.8680 for 0.8880 with stop below 0.8580

Euro's long term uptrend started in Feb 1981 at 0.5039 and is unfolding as a (A)-(B)-(C) move with (A): 0.8433 (Feb 1993), (B): 0.5682 (May 2000) and impulsive wave (C) should have ended at 0.9805 with wave III ended at 0.7254 (May 2003), triangle wave IV at 0.6536 (23 Jan 2007) and wave V as well as wave (C) has ended at 0.9805.

We are keeping an alternate count that only wave III ended at 0.9805 and the correction from there is the wave IV and may extend weakness to 0.7700, however, it is necessary to see a daily close above resistance at 0.9143 would change this to be the preferred count.

Euro Yawns As Fed Raises Rates, Markets Eye Eurozone Final CPI

The euro has posted slight losses in the Thursday session, as EUR/USD is trading at 1.1170. In economic news, the eurozone surplus dropped sharply, coming in at EUR 19.6 billion. This was well short of the forecast of EUR 22.4 billion. In the US, today's major release is unemployment claims, which is expected to dip to 241 thousand. On the manufacturing front, the markets are braced for a soft reading from Philly Fed Manufacturing Index, with an estimate of 25.5 points. On Friday, the eurozone releases Final CPI and the US will publish Building Permits and Housing Starts.

US consumer numbers were soft on Thursday, as CPI and retail sales reports missed estimates. CPI declined 0.1%, short of the estimate of 0.2%. This was the second decline in three months, as inflation is currently at 15%, well below the Federal Reserve's target of 2.0%. Retail Sales, the primary gauge of consumer spending was dismal, coming in at -0.3%, compared to a forecast of +0.1%. This marked the indicator's weakest reading since August 2016. Weak retail sales is clearly an area of concern – the soft reading could drag down GDP for the second quarter, as as consumer spending accounts for more than two-thirds of economic growth. Although surveys continue to show that US consumers remain optimistic about the economy, this hasn't translated into stronger consumer spending. The euro initially posted gains following the release of this data, but the dollar was able to recover.

As expected, the Federal Reserve raised rates on Thursday by 25 basis points, to a target range of 1.00 percent to 1.25 percent. The rate statement portrayed an optimistic picture, noting that the economy was growing, and the labor market remained strong. As for inflation, which remains stubbornly low, the statement acknowledged that inflation remained below the Fed's target of 2.0%, but expected that goal to be reached in the “medium term”. The Fed projected one more rate hike in 2017, and the markets are circling the December meeting as the most likely date. The odds for a September increase are at 18%, compared to 23% a week ago, according to the CME Group. As for a December increase, the odds are currently at 38%. One surprising development was that Fed Chair Janet Yellen outlined a plan to reduce its $4.2 trillion balance sheet (comprised of Treasury bonds and mortgage-backed securities). Yellen was short on specifics, saying that the goal was to begin the normalization “relatively soon”. The balance sheet ballooned after the financial crisis in 2008, as the Fed implemented a massive quantitative easing program as part of its accommodative monetary policy, together with interest rates of zero. The gradual reduction in the purchase of these assets signifies an important vote of confidence in the strength of the US economy.

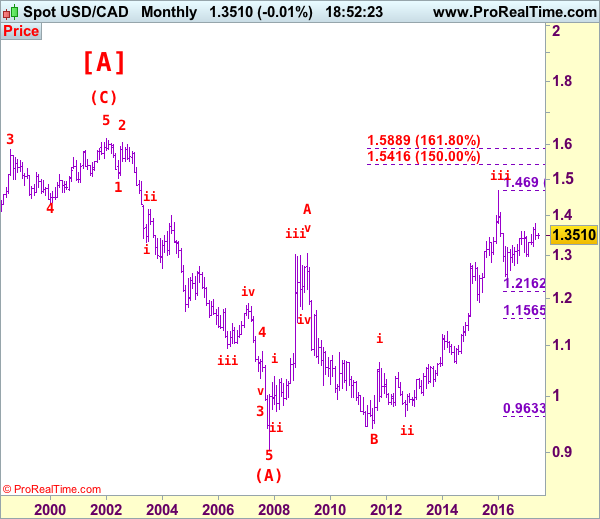

USD/CAD Elliott Wave Analysis

USD/CAD – 1.3280

USD/CAD – Wave v ended at 0.9407 and a-b-c correction may extend gain to 1.4700

The greenback finally dropped in line with our bearish expectation, our short position entered at 1.3530 finally met our downside target at 1.3330 with 200 points profit, this anticipated selloff adds credence to our view that top has been formed at 1.3794 and the breach of previous support has reinforced our view that the rebound from 1.2969 ha ended at 1.3794, then further weakness to 1.3150 and then 1.3100 would be seen, however, oversold condition should limit downside and reckon previous support at 1.3056 would hold, price should stay above psychological support at 1.3000.

We are keeping our view that the wave b from 1.0657 (a leg top) has possibly ended at 0.9633 with (a): 0.9800, wave (b): 1.0447 and wave c at 0.9633, the subsequent rise from there is now treated as wave c exceeded indicated upside target at 1.3770-80 and 1.4000 and wave (3) has possibly ended at 1.4690 and wave (4) correction has commenced for retracement back to 1.2832 support, then 1.2410-20.

On the daily chart, our latest preferred count remains that the A of (B) rally from 0.9059 low (7 Nov 2007) unfolded into an impulsive wave with i: 0.9059-1.0380, ii ended at 0.9819, iii at 1.3019 followed by triangle wave iv at 1.2026 , then wave v formed a top at 1.3066 and also ended the wave A. The wave B is unfolding as an double three a-b-c-x-a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c at 1.0784, followed by wave x at 1.1725, another set of a-b-c unfolded with 2nd a at 0.9931, 2nd b at 1.0674. the 2nd c has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3900 had been met and gain to 1.4700 would follow.

On the upside, whilst initial recovery to 1.3310-15 cannot be ruled out, reckon upside would be limited to 1.3350 and previous support at 1.3387 (now resistance) should hold, bring another decline. A daily close above 1.3387 would suggest low is possibly formed, bring a stronger rebound to 1.3425-30, break there would add credence to this view, then further gain to 1.3490-00 would follow but resistance at 1.3547 should remain intact.

Recommendation: Short entered at 1.3530 met target at 1.3330 with 200 points profit an d would stand aside for this week.

Longer term - The selloff from 1.6194 (21 Jan 2002) to 0.9059 (07 Nov 2007) is viewed as (A) wave which is a 5-waver as labeled on the monthly chart as below, the subsequently rally is labeled as (B) with impulsive A leg of (B) ended at 1.3066, wave B of (B) is unfolding which has either ended at 0.9407 or would extend one more fall but downside should be limited to 0.9200 and 0.9000 should hold.