Sample Category Title

CAC Drops on Soft French CPI, Hawkish Federal Reserve

The CAC index has lost ground on Thursday, continuing the downward trend seen on Wednesday. The index has dropped 1.21% and is currently trading at 5187.80 points. On the release front, French Final CPI dipped to 0.0%, shy of the estimate of 0.1%. This marked a 4-month low. As well, the eurozone trade surplus fell sharply, coming in at EUR 19.6 billion. This was well short of the forecast of EUR 22.4 billion. On Friday, we'll get another look at inflation, as the eurozone releases Final CPI. The markets are braced for the inflation indicator to drop to 1.4 percent.

France will wrap up parliamentary elections on Sunday, when voters determine the makeup of the 577-seat National Assembly. French President Emmanuel Macron is expected to win a huge majority, with some polls giving Macron's En Marche party a staggering 80% of the vote. A strong majority in parliament will facilitate Macron's pro-business agenda, such as overhauling France's labor laws and making the economy more competitive. Macron is a strong supporter of the European Union, and a Macron-Merkel alliance could strengthen the EU at a time when Brexit and nationalistic parties on the continent have undermined European unity. Macron, who is expected to support a hard line against Brexit, said that the EU would leave the "door open" in case Britain changed its mind and decided to stay in the club, but that is clearly a far-fetched scenario.

US consumer data was soft in May, as CPI and retail sales reports missed the forecasts. CPI declined 0.1%, short of the estimate of 0.2%. Inflation has now declined twice in three months, and the current level of 1.5% is well below the Federal Reserve's target of 2.0%. Retail Sales, the primary gauge of consumer spending, was dismal, coming in at -0.3%, compared to a forecast of +0.1%. This marked the indicator's weakest reading since August 2016. If consumer spending remains weak, it could drag down GDP for the second quarter, as consumer spending accounts for more than two-thirds of economic growth. Although surveys continue to show that US consumers remain optimistic about the economy, this hasn't translated into stronger consumer spending.

As expected, the Federal Reserve raised rates on Thursday by 25 basis points, to a target range of 1.00 percent to 1.25 percent. The rate statement portrayed an optimistic picture, noting that the economy was growing, and the labor market remained strong. As for inflation, which remains stubbornly low, the statement acknowledged that inflation remained below the Fed's target of 2.0%, but expected that goal to be reached in the "medium term". The Fed projected one more rate hike in 2017, and the markets are circling the December meeting as the most likely date. The odds for a September increase are at 18%, compared to 23% a week ago, according to the CME Group. As for a December increase, the odds are currently at 38%. One surprising development was that Fed Chair Janet Yellen outlined a plan to reduce its $4.2 trillion balance sheet (comprised of Treasury bonds and mortgage-backed securities). Yellen was short on specifics, saying that the goal was to begin the normalization "relatively soon". The balance sheet ballooned after the financial crisis in 2008, as the Fed implemented a massive quantitative easing program as part of its accommodative monetary policy, together with interest rates of zero. The gradual reduction in the purchase of these assets signifies an important vote of confidence in the strength of the US economy.

BoE Dissenters Propel Sterling

- European stock markets lose more than 1% today in a rising yield environment amid signs that global central banks are shifting gradually away from ultra-easy monetary policies. US stock markets open around 0.5% weaker with Nasdaq underperforming.

- A trio of Bank of England officials broke ranks with their colleagues in June to push for an immediate increase in interest rates, one of several signals that the UK central bank has moved a step closer to withdrawing the emergency stimulus it put in place after last year's Brexit referendum.

- US eco data printed mixed. June Empire manufacturing (19.8 from -1) and Philly Fed Business Outlook (27.6 from 38.8) both beat consensus. Weekly jobless claims printed at 237k, near historical lows and also better than forecast. May industrial production (0% M/M) and prices indices (import & export prices unexpectedly declined M/M) disappointed.

- UK retail sales plunged in May for the second time in three months as rising inflation ate into the purchasing power of consumers. The volume of goods sold in stores and online fell 1.2% from April, more than the 0.8% decline forecast. Sales excluding auto fuel dropped 1.6%, the most this year.

- US president Donald Trump claimed he was the victim of a witch hunt led by "bad and conflicted people" after it emerged that special prosecutor Robert Mueller was investigating him for possible obstruction of justice in the FBI's Russia probe.

- The SNB said that reducing its huge balance sheet was not on the agenda as political and economic risks had not yet eased sufficiently for it to move away from its ultra-loose monetary policy. The dovish tone signalled the SNB was nowhere close to tightening its policy as it tries to keep a lid on the strong CHF which weighs on the economy.

- Czech PM Sobotka stepped down as leader of the Social Democrats and the party shook up key personnel in a last-moment effort to close the popularity gap with its main rival four months before elections.

- Greece's international lenders prepared to unblock as much as €8.5 billion in loans that Athens desperately needs next month to pay its bills, and to give some idea on what debt relief they may offer over the long term.

- Italy's government won a parliamentary confidence vote on a mini-budget, agreeing to €3.4 billion of deficit-cutting measures to placate the European Commission. The package includes an increase in levies on tobacco and gambling, a renewed crackdown on tax evasion and efforts to boost the tax take from Internet companies.

Rates

Bund correct sharply lower

Core bonds are on the defensive today, losing substantial ground after US data induced gains on Wednesday. The German yield curve bear flattens with yields up between 3.5 bps (30-yr) and 7 bps (5-yr). The bear flattening suggests that the ECB's exit policy remains in focus with several ECB hawks yesterday questioning the necessity to keep the APP unchanged for much longer. The US curve shifts higher too, but yields are up a more moderate 2.7 to 3.1 bps (30-year yield +1.6 bp). UK gilt yields rise up to 10.4 bps (5-yr).

German bonds underperform US Treasuries, but gilts fare the worst after the BoE showed a 5-to-3 split in keeping rates unchanged. This brings UK rate hike expectations forward. However, the Bund had already lost ground when nose-diving gilts drew Bunds lower. Initial Bund selling may have been profit-taking after yesterday's stellar performance. The Bund rally might have been exhausted as the contract-highs came into sight. The US eco data, jobless claims, NY Fed and Philly Fed business surveys were strong and mostly better than expected, even as production disappointed. This contrasts with yesterday's eco data. The relationships between markets was distorted. While bonds went down, so did equities and the Bund underperformance on the US Treasuries didn't prevent dollar gains versus the euro. Oil stabilized after a big fall yesterday. US Treasuries decline started in earnest when US trading got going. Some reconsidering of the nature of the FOMC meeting might have played a role too. The meeting was more hawkish than first considered by the markets, we think.

Currencies

USD extends post-Fed short squeeze

Investors did some more USD short-covering as the Fed intends to extend policy normalisation. EUR/USD dropped further to the 1.1150 area, even as interest rate differentials narrowed against the dollar. USD/JPY also rebound despite a correction in equities.

There were no important eco data in Europe. The post Fed repositioning dominated FX trading. The dollar rebounded as the Fed signalled that it will continue its policy normalisation even as recent data, especially inflation, were no 'grand cru'. Remarkably, the decline of EUR/USD occurred as interest rate differentials between the US and Germany narrow. Something similar occurred in USD/JPY. USD/JPY extended its rebound even as global equities suffered substantial losses. FX markets were positioned too short USD going into yesterday's Fed meeting. These USD shorts still had to be reduced, whatever the developments in other markets. EUR/USD traded in the 1.1165 area around noon. USD/JPY changed hands in the 109.80.

The US, early morning US activity data were mostly stronger than expected. Production data (flat on the month) was also softer than expected. The dollar tried to extend its rebound/short-squeeze after the data, but the move had no strong legs anymore. EUR/USD settled in the mid 1.11 area. So, the test of the 1.13 resistance area is rejected. USD/JPY also remains remarkably solid even as US equities deepen yesterday's losses. The pair trades in the 110.40 area. Despite today's constructive USD/JPY price action, the technical picture on USD/JPY hasn't improved yet. A first minor resistance comes in at 110.81. Especially as equities continue correcting lower, a sustained break higher isn't evident. USD/JPY traders also keep an eye at tomorrow's BOJ policy decision.

BoE dissenters propel sterling

UK retail sales (-1.2% M/M,-1.6% M/M excl. fuel) declined more than expected as price rises due to the weak pound are eroding consumers' purchasing power. Markets (including us) assumed that the BoE would keep a cautious monetary policy approach, giving more weight to easing consumption, slowing wage growth and uncertainty on rather than on higher inflation (2.9% reported for May earlier this week). The BoE as expected left its policy rate (0.25%) unchanged. However, only five members voted to keep rates unchanged. Three members unexpectedly voted in favour of a rate hike as the BOE expects inflation to move beyond 3% in Autumn and as inflation is expected to stay above target for a prolonged period of time. Sterling hardly reacted to the weak retail sales, but jumped higher on the 5-3 vote. EUR/GBP dropped from just below 0.88 to the 0.8725 area (currently 0.8750). Cable jumped from 1.27 to the just below 1.28, but eased again later (currently 1.2775). The substantial support for a rate hike was a surprise, but we maintain the view that the BoE will remain very cautious to raise rates as political and economic uncertainty remains elevated.

Trade Idea Update: GBP/USD – Hold short entered at 1.2790

GBP/USD - 1.2743

Original strategy :

Sold at 1.2790, Target: 1.2690, Stop: 1.2825

Position : - Short at 1.2790

Target : - 1.2690

Stop : - 1.2825

New strategy :

Hold short entered at 1.2790, Target: 1.2690, Stop: 1.2825

Position : - Short at 1.2790

Target : - 1.2690

Stop : - 1.2800

As the British pound ran into resistance at 1.2818 yesterday and has retreated on dollar’s broad-based strength after Fed rate hike, suggesting the rebound d from 1.2635 has ended there and consolidation with mild downside bias remains for weakness to 1.2680-90, however, break there is needed to retain bearishness and bring further fall to 1.2650, then towards said support at 1.2635.

In view of this, we are holding on to our short position entered at 1.2790. Only above said resistance at 1.2818 would defer and risk a strong rebound to 1.2845-50 (61.8% Fibonacci retracement of 1.2978-1.2635) but upside should be limited to 1.2870-80.

Trade Idea Update: EUR/USD – Sell at 1.1190

EUR/USD - 1.150

Original strategy :

Sell at 1.1240, Target: 1.1140, Stop: 1.1275

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1190, Target: 1.1090, Stop: 1.1225

Position : -

Target : -

Stop : -

Although the single currency surged to as high as 1.1296, lack of follow through buying on break of previous resistance at 1.1285 and the subsequent reversal signal top has been formed there, current breach of indicated support at 1.1166 adds credence to this view and bearishness remains for further fall to 1.1125-30, however, near term oversold condition should limit downside to previous support at 1.1109.

In view of this, we are looking to sell euro on recovery as 1.1185-90 should limit upside and bring another decline. Above 1.1225-30 would defer and risk a stronger rebound to 1.1250 but price should falter well below said resistance at 1.1296, bring another decline later.

Trade Idea Update: USD/JPY – Buy at 109.90

USD/JPY - 110.41

Original strategy :

Sold at 109.60, stopped at 109.90

Position : - Short at 109.60

Target : -

Stop : - 109.90

New strategy :

Buy at 109.90, Target: 110.90, Stop: 109.55

Position : -

Target : -

Stop : -

The greenback has rallied again after staging a strong rebound yesterday and resistance at 110.35 was penetrated, suggesting recent decline has indeed ended at 108.82 and upside bias is seen for further gain towards resistance at 110.81, however, break there is needed to retain bullishness and extend the rise from 108.82 low for retracement of recent downtrend to 111.00 and possibly towards 111.25-30.

In view of this, we are looking to buy dollar on pullback as 109.85-90 should limit downside. Only below 109.45-50 would suggest an intra-day top is formed instead, risk weakness to 109.20-25 but price should stay well above said yesterday’s low at 108.82, bring another rebound later.

April Canadian Manufacturing Sales Bode Well for Further Gains in Investment

Highlights:

- Nominal manufacturing sales jumped 1.1% in the month helped by strong gains in petroleum and coal (8.9%) and primary metal (3.8%) that more than offset the motor vehicle component dropping 3.7%.

- Sale volumes increased 0.5% reflecting non-durables rising 1.9% that more than offset a 0.8% drop in the durables component.

- Nominal inventories rose an equally strong 0.9% which contributed to the inventory-to-sales ratio remaining unchanged at 1.35.

- The data is indicative of the manufacturing component of GDP being flat in the month as much of the strength in petroleum and coal manufacturing sales gets discounted on a value added basis. The data remains consistent with our expectation that overall April GDP will remain unchanged in the month following the 0.5% jump in March.

Our Take:

The volume of April manufacturing sales increased at a stronger-than-expected pace both in the month (0.5%) and over the year (1.9%). The annual increase has been helped by the volume of machinery orders surging 13.5% over the past year. It follows indications of a rebound in imports of machinery and equipment in April and solid momentum in engineering employment through March. The burst in overall GDP growth of 3.7% in the first quarter was helped by business investment surging 10.3%. Today's manufacturing report, along with the import and employment data, bodes well for second quarter business investment to build further onto the Q1 surge. We are currently forecasting a 3 1/2% increase though with the risks on the upside. This continued strength reinforces the Bank of Canada's recent comments about economic growth becoming more broadly based. Our expectation is that this broad-based strength will continue through the remainder of this year and that will eventually return the Bank of Canada to tightening mode. In fact, if upcoming data continues to surprise on the upside, there is the clear risk that this tightening could be advanced relative to our current forecast of rate hikes commencing in the first half of 2018.

Dollar Extends Post FOMC Rebound, Sterling Supported by Hawkish BoE

Dollar extends post FOMC rebound in early US session after positive economic data. Initial jobless claims dropped 8k to 237k in the week ended June 10, below expectation of 241k. Four-week moving average rose 1k to 243k. That's the 119 straight weeks initial claims stayed below 300k handle, last seen in early 1970s. Continuing claims rose 6k to 1.935m in the week ended June 3 staying below 2m handle for the 9 straight week, last seen back in 1973. Empire State manufacturing index rebound to 19.8, up from -1. Philly Fed survey though, retreated to 27.6 but beat expectation of 25.0. Industrial production, rose 0.0% in May while capacity utilization dropped to 76.6%.

EUR/USD's fall accelerates today and breaks through 1.1165 minor support. Main focus is now back to 1.1109. As long as this support holds, further rally is still in favor and firm break of 1.1298 key resistance will carry larger bullish implication. However, break of 1.1109 will confirm rejection from 1.1298 and bring deeper pull back. USD/JPY, at this point, is also staying below 110.80 near term resistance and outlook stays bearish until a break of this level. USD/CAD, despite today's rebound, is held well below 1.3387 resistance and maintains bearish outlook.

Dollar's rebound started after yesterday's FOMC rate decision. The overall announcement, including new economic projections, was not as bad as some anticipated. Fed maintained the projection of a total of three rate hike this year. Downward revision in 2017 inflation forecast was somewhat offset by the upward revision in GDP forecast and downward revision in unemployment rate forecast. On other hand, both growth and inflation forecasts for 2018 and 2019 were held unchanged.

Three voted for rate hike in BoE decision

BoE kept bank rate unchanged at 0.25% and asset purchase target at GBP 435b as widely expected. To the markets' surprise two officials joined Kristin Forbes to vote for rate hike this year. That include Michael Saunders and Ian McCafferty. Overall, the statement suggests that MPC policy makers are getting more impatient with surging inflation. The statement noted that "the continued growth of employment could suggest that spare capacity is being eroded, lessening the trade-off that the MPC is required to balance and, all else equal, reducing the MPC's tolerance of above-target inflation." Nonetheless, the central bank also emphasized that any rate hike will be at a "gradual pace and to limited extent".

Also from UK, retail sales dropped more than expected by -1.2% mom in May.

Technically, GBP/USD is staying in tight range above 1.2633 temporary low and lacks clear momentum to extend the recovery from there. EUR/GBP dips sharply to as low as 0.8722 but stays well above 0.8639 near term support. GBP/JPY also recovers today but stays well below 142.75 resistance. There is no change in the near term bearish trend in the Pound yet.

SNB stands pat, Jordan open to further stimulus

SNB held sight deposit rate unchanged at -0.75% as widely expected. Three month LIBOR rate was held at -1.25% to -0.25%. The central bank kept 2017 inflation forecast unchanged at 0.3%. However, for 2018 and 2019, inflation projected was downgraded to 0.3% (from 0.4%) and 1.0% (from 1.1%) respectively. Growth is projected to be at 1.5% this year. SNB President Thomas Jordan said that "available economic indicators suggest that the Swiss economy is on the road to recovery." But he also warned that "certain indicators suggest that the recovery has not yet taken hold in all areas of the economy." Also, "the strong Swiss franc continues to weigh on some industries" and it's still "significantly overvalued".

Jordan seems not concerned with its balance street and said that "our monetary policy remains expansionary for the reasons we've given, namely low inflation, underutilisation of production capacities and a significantly overvalued franc." He also left the door open for further rate cut and said that "all options are still open, we could also cut rates further if needed.

Also from Swiss, PPI dropped -0.3% mom, rose 0.1% yoy in May. Also from Europe, Eurozone trade surplus narrowed to EUR 19.6b in April.

Australia unemployment rate dropped to lowest since 2013

Australia unemployment rate unexpectedly dropped to 5.5% in May, down from 5.7% and below expectation of 5.7%. That's also the lowest number since February 2013. Headline job number showed 42k growth, well above expectation of 10k. Full-time jobs grew 52.1k while part-time jobs fell -10.1k. Participation rate also rose 0.1% to 64.9%. Speculations of a rate cut by RBA receded after the release. On the other hand, New Zealand GDP grew only 0.5% qoq in Q1, below expectation of 0.7% qoq.

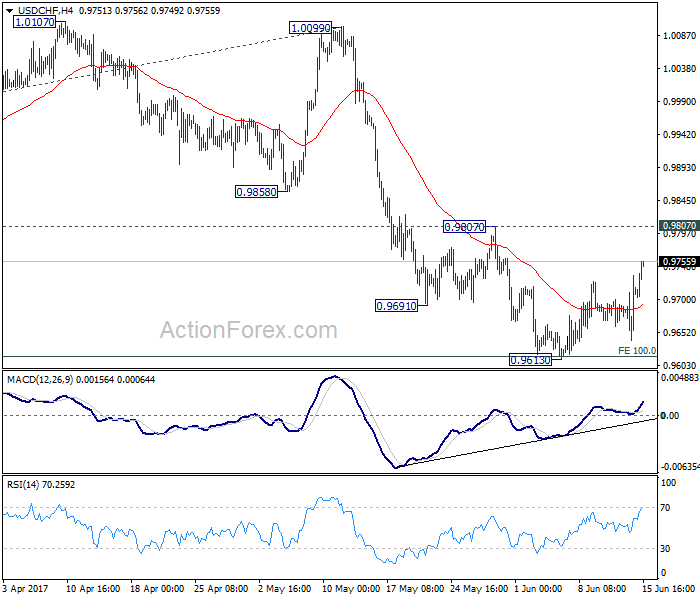

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9654; (P) 0.9694; (R1) 0.9749; More.....

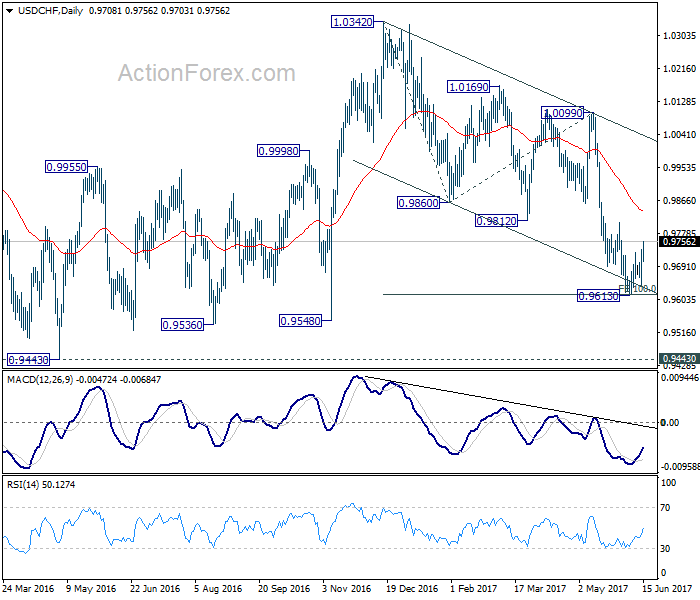

USD/CHF's rebound from 0.9613 extends to as high as 0.9755 so far. However, it's kept well below 0.9807 resistance. Thus, there is no clear indication of reversal yet. As long as 0.9807 stays intact, deeper fall is still in favor. Break of 0.9613 will extend the whole decline from 1.0342 to 0.9548 support and below. We'd start to look for bottoming signal again as it approaches 0.9443 key support level. However, considering bullish convergence condition in 4 hour MACD, break of 0.9807 will indicate near term reversal and turn outlook bullish for 1.0099 resistance next.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | GDP Q/Q Q1 | 0.50% | 0.70% | 0.40% | |

| 01:00 | AUD | Consumer Inflation Expectation Jun | 3.60% | 4.00% | ||

| 01:30 | AUD | Employment Change May | 42.0K | 10.0K | 37.4K | |

| 01:30 | AUD | Unemployment Rate May | 5.50% | 5.70% | 5.70% | |

| 07:15 | CHF | Producer & Import Prices M/M May | -0.30% | 0.00% | -0.20% | |

| 07:15 | CHF | Producer & Import Prices Y/Y May | 0.10% | 0.20% | 0.80% | |

| 07:30 | CHF | SNB Sight Deposit Interest Rate | -0.75% | -0.75% | -0.75% | |

| 07:30 | CHF | SNB 3-Month Libor Lower Target Range | -1.25% | -1.25% | -1.25% | |

| 07:30 | CHF | SNB 3-Month Libor Upper Target Range | -0.25% | -0.25% | -0.25% | |

| 08:30 | GBP | Retail Sales M/M May | -1.20% | -0.90% | 2.30% | 2.50% |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Apr | 19.6B | 22.4B | 23.1B | 22.2B |

| 11:00 | GBP | BoE Rate Decision | 0.25% | 0.25% | 0.25% | |

| 11:00 | GBP | BoE Asset Purchase Target Jun | 435B | 435B | 435B | |

| 11:00 | GBP | MPC Official Bank Rate Votes | 3--0--5 | 1--0--6 | 1--0--7 | |

| 11:00 | GBP | MPC Asset Purchase Facility Votes | 0--0--8 | 0--0--7 | 0--0--8 | |

| 12:30 | CAD | Manufacturing Shipments M/M Apr | 0.90% | 1.00% | ||

| 12:30 | USD | Import Price Index M/M May | -0.30% | -0.10% | 0.50% | 0.20% |

| 12:30 | USD | Empire State Manufacturing Index Jun | 19.8 | 6 | -1 | |

| 12:30 | USD | Initial Jobless Claims (JUN 10) | 237K | 241K | 245K | |

| 12:30 | USD | Philly Fed Manufacturing Index Jun | 27.6 | 25 | 38.8 | |

| 13:15 | USD | Industrial Production May | 0.00% | 0.20% | 1.00% | 1.10% |

| 13:15 | USD | Capacity Utilization May | 76.60% | 76.70% | ||

| 14:00 | USD | NAHB Housing Market Index Jun | 70 | 70 | ||

| 14:30 | USD | Natural Gas Storage | 106B | |||

| 20:00 | USD | Net Long-term TIC Flows Apr | 37.3B | 59.8B |

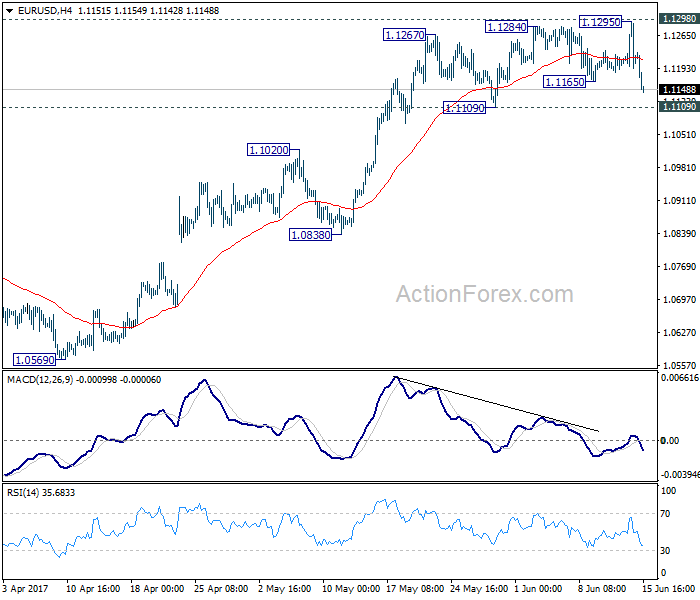

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1189; (P) 1.1206 (R1) 1.1228; More....

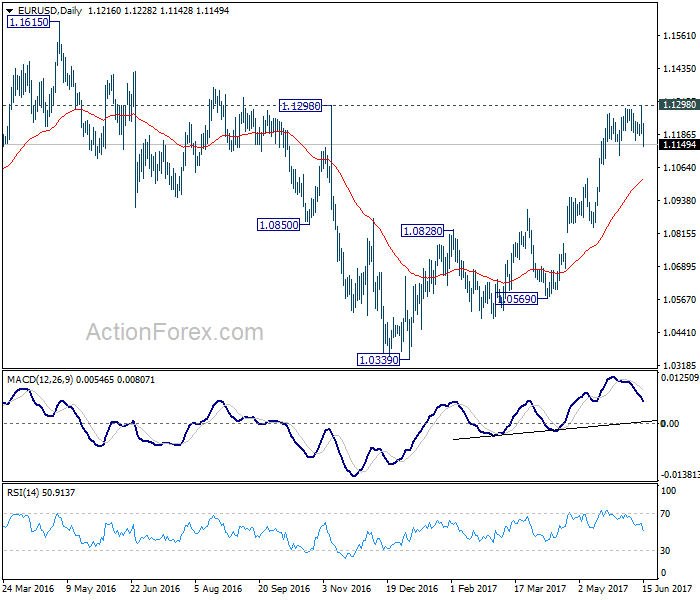

EUR/USD's fall from 1.1295 extends lower today and breaks 1.1165 minor support. Still, it's holding above 1.1109 support and outlook is unchanged. Intraday bias remains neutral with focus on 1.1298 key resistance. Decisive break there will carry larger bullish implication and target 1.1615 resistance next. On the downside, break of 1.1109 support will indicate short term topping and rejection from 1.1298. In such case, intraday bias will be turned to the downside for 1.0838 support.

In the bigger picture, the case for medium term reversal continues to build up with EUR/USD staying far above 55 week EMA (now at 1.0922). Also, bullish convergence condition is seen in weekly MACD. Focus will now be on 1.1298 key resistance. Rejection from there will maintain medium term bearishness and would extend the whole down trend from 1.6039 (2008 high). However, firm break of 1.1298 will indicate reversal. In such case, further rally would be seen back to 1.2042 support turned resistance next.

GBP/USD Mid-Day Outlook

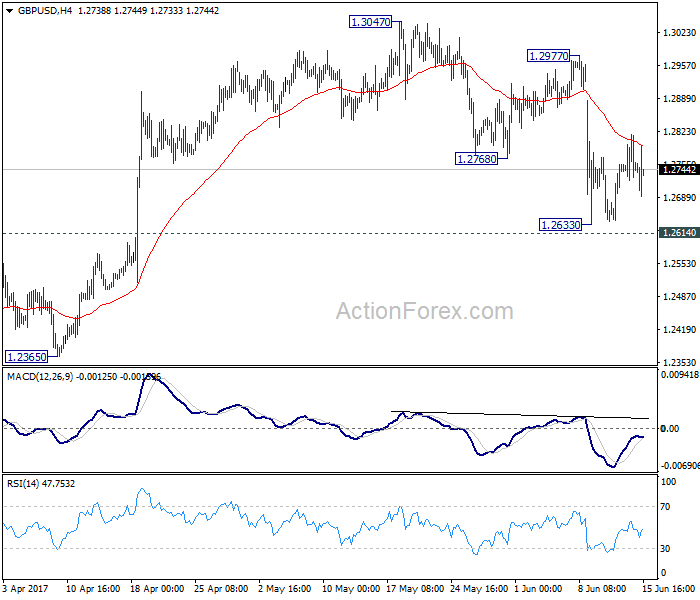

Daily Pivots: (S1) 1.2710; (P) 1.2764; (R1) 1.2804; More...

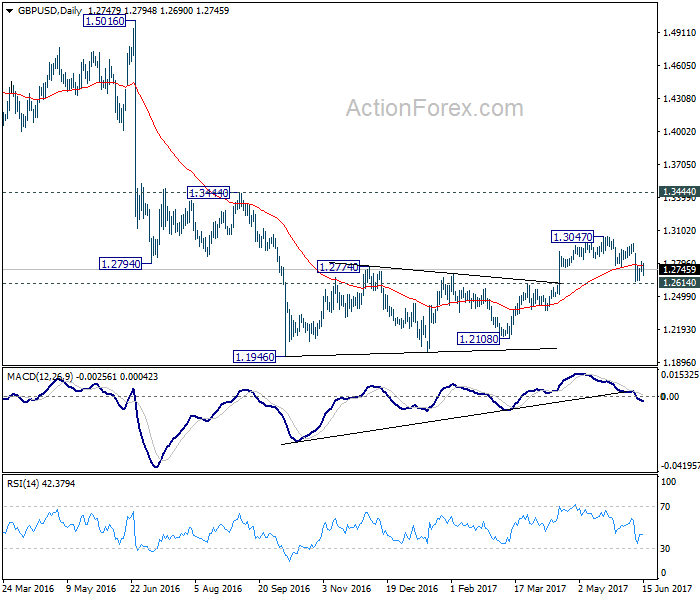

Intraday bias in GBP/USD remains neutral for the moment and consolidation from 1.2633 might extend. Near term outlook remains bearish with 1.2977 resistance intact. We continue to favor the case that consolidation pattern from 1.1946 has completed at 1.3047 already. Decisive break of 1.2614 resistance turned support would confirm our bearish view and target a test on 1.1946 low next. However, break of 1.2977 will dampen our view and turn bias back to the upside for 1.3047 and above.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. Price actions from 1.1946 medium term low are seen as a consolidation pattern, which could have completed after hitting 55 week EMA. Break of 1.1946 low will target 61.8% projection of 1.5016 to 1.1946 from 1.3047 at 1.1150 next. In case the consolidation from 1.1946 extends, outlook will stay remain bearish as long as 1.3444 resistance holds.

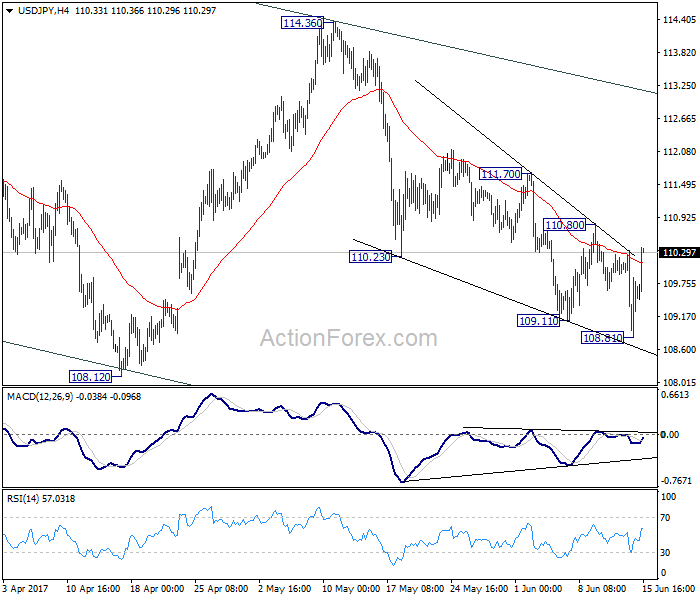

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.79; (P) 109.56; (R1) 110.34; More...

With 4 hours MACD crossed above signal line, intraday bias in USD/JPY is turned neutral first. With 110.80 resistance intact, further decline is still expected to 108.12 low first. Break will extend the whole corrective fall from 118.65 to 61.8% retracement of 98.97 to 118.65 at 106.48. We will look for bottoming sign there. However, break of 110.80 should indicate completion of fall from 114.36. In that case, intraday bias will turned back to the upside for 111.70. Break will target 114.36 key resistance.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.