Sample Category Title

(FED) FOMC Statement Release Date: June 14, 2017

Information received since the Federal Open Market Committee met in May indicates that the labor market has continued to strengthen and that economic activity has been rising moderately so far this year. Job gains have moderated but have been solid, on average, since the beginning of the year, and the unemployment rate has declined. Household spending has picked up in recent months, and business fixed investment has continued to expand. On a 12-month basis, inflation has declined recently and, like the measure excluding food and energy prices, is running somewhat below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee continues to expect that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace, and labor market conditions will strengthen somewhat further. Inflation on a 12-month basis is expected to remain somewhat below 2 percent in the near term but to stabilize around the Committee's 2 percent objective over the medium term. Near term risks to the economic outlook appear roughly balanced, but the Committee is monitoring inflation developments closely.

In view of realized and expected labor market conditions and inflation, the Committee decided to raise the target range for the federal funds rate to 1 to 1-1/4 percent. The stance of monetary policy remains accommodative, thereby supporting some further strengthening in labor market conditions and a sustained return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. The Committee will carefully monitor actual and expected inflation developments relative to its symmetric inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. The Committee currently expects to begin implementing a balance sheet normalization program this year, provided that the economy evolves broadly as anticipated. This program, which would gradually reduce the Federal Reserve's securities holdings by decreasing reinvestment of principal payments from those securities, is described in the accompanying addendum to the Committee's Policy Normalization Principles and Plans.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; Charles L. Evans; Stanley Fischer; Patrick Harker; Robert S. Kaplan; and Jerome H. Powell. Voting against the action was Neel Kashkari, who preferred at this meeting to maintain the existing target range for the federal funds rate.

How Will BoE Respond to Latest UK Developments?

BoE Adds Hung Parliament to List of Economic Uncertainties Days Before Brexit Talks Begin

The Bank of England announces its latest monetary policy decision on Thursday at a time of significant uncertainty for the country. A hung parliament in, what was, an entirely unnecessary snap election was the worst preparation for Brexit negotiations which are due to begin next week.

BoE policy makers will meet on Thursday to discuss another possible problem facing the country during all of this, rising inflation. In fact, rising prices are largely linked to the above problems, with the UKs vote to leave the EU a year ago triggering the substantial depreciation in the pound that drove up the cost of goods from abroad.

Policy makers must now determine whether the factors that drove inflation well beyond its 2% target are just temporary or represent a longer term challenge for price stability. With headline inflation at 2.9% in May and core inflation slightly lower at 2.6%, the decision for the central bank is not as straightforward as it would like during what is already a complicated time for the country.

Especially when growth is already slowing and the consumer - a hugely important part of the economy - is feeling the pinch.

Real Wage Growth vs Retail Sales

Source - Thomson Reuters Eikon

Policy makers have already previously indicated that they will only tolerate a little more upside on growth or inflation before voting for tighter policy which should technically make a hike a possibility on Thursday and yet, under the circumstances I think this is extremely unlikely. Any form of tightening would catch markets completely off-guard and could therefore generate quite a reaction, although again, this seems very unlikely.

What Can We Expect on Thursday?

The voting on both interest rates and asset purchases is expected to remain unchanged from the last meeting with only one policy maker of the eight - Kristin Forbes - voting for a hike. Forbes will leave her role on the Monetary Policy Committee at the end of the month leaving little support, it would seem, for any policy tightening.

With this in mind, it will be interesting to see how the BoE balances higher inflation with managing expectations, particularly in the absence of a press conference which we only get every three months alongside the inflation report.

All eyes will be on the minutes and the voting and should the central bank give the impression that tighter policy is a real possibility in the months ahead, it will be interesting to see how much the pound rises - if at all - given all of the uncertainty weighing it down. Typically, currencies appreciate in response to an event that is typically more hawkish than anticipated.

The FTSE would also likely be sensitive to any changes in policy stance or outlook, with its negative correlation with sterling also likely impacting its moves in the aftermath of such an outcome.

Hard Data Shock Pre-Fed

Once is not a problem, twice is not unusual but a 3rd consecutive monthly slowdown in US inflation accompanied by a back-to-back decline in retail sales should deal a fresh blow to the assumption that US bond yields and their currency ought to find their rallying ways due to superior fundamentals. Today's twin data release highlights the Lame Duck nature of today's anticipated Fed hike, highlighting the eroding probabilities for an H2 Fed tightening.

We should watch whether the language in the statement shall add more weight to slowing inflation and pay growth as well look out for any dissents to the assumed hike. The central Fed Funds rate view in the dot plot shall be scrutinized on whether it would be lowered to 2 hikes this year (i.e. no more tightening assuming a hike today). If maintained at 3 hikes, then watch out for the dot plot on growth and Yellen's press conference.

Traders will find pockets of consolidation between the 10-15 minutes following the release of the FOMC statement and before the Fed chair Yellen begins her prepared remarks. The final wave of trading volatility is likely to emerge from the Q&A session when the probability for further Fed action shall be weighed through Yellen's discussion of bond sales, weakening wage growth and tepid consumer demand. Both of our Premium USD trades are in the green.

Gold Moves Higher as US Consumer Numbers Slip

Gold has posted considerable gains in the Wednesday session, as XAU/USD is up 0.72%. In North American trade, spot gold is trading at $1275.77 per ounce. consumer data was soft, as retail sales and CPI posted declines of 0.3% and 0.1%, respectively. Later in the day, the Federal Reserve announces its benchmark rate, which is expected to increase by 25 basis points to 1.25 percent. On Thursday, we'll get a look at the weekly unemployment claims report, with an estimate of 241 thousand.

All eyes are on the Federal Reserve, which will release a rate statement later on Wednesday. The Fed is widely expected to raise interest rates by a quarter point to 1.25%, but there's still plenty of anticipation, as analysts will be focusing on the language in the rate statement and as well as the Fed's economic projections. Analysts are expecting a "dovish hike", meaning that together with the rate increase, the Fed rate statement will be cautious in tone, and dovish regarding additional rate hikes. A dovish message could pour cold water on a rate hike in September and boost gold prices. Earlier in the year, three rate hikes in 2017 seemed almost a given, but currently, the odds of a September move are just 28%. There are two key items which could affect gold prices. First, the Fed Economic Projections will detail forecasts of inflation, growth and unemployment, and most importantly, the rate hike path. With the US economy performing better in the second quarter, there's a strong likelihood that the Fed will not moderate its rate hike projections,which is good news for the dollar. Secondly, the markets will be looking for details regarding its plan to lower the $4.2 trillion balance sheet. If the Fed outlines a plan to reduce its holding in H2, the dollar could respond positively. Another variable is the political paralysis which has engulfed Washington. With the Trump administration spending most of its energy on damage control, little progress is being made with regard to Trump's agenda of tax reform and major spending on infrastructure. The markets are becoming more skeptical about Trump's ability to work with Congress, and if this sentiment is shared by the Fed, it is likely to sound dovish regarding rate hikes in September or December.

Pound Shrugs off Soft Employment Numbers, Fed Rate Announcement Next

The British pound has posted slight gains in the Wednesday session. GBP/USD is up 0.43%, as it trades at the 1.28 line. On the release front, it's been a busy day. In the UK, wage growth dropped to 2.1%, short of the estimate of 2.4%. Unemployment rolls dropped 7.3 thousand, missing the forecast of 12.5 thousand. In the US, consumer data was soft, as retail sales and CPI posted declines of 0.3% and 0.1%, respectively. Later in the day, the Federal Reserve announces its benchmark rate, which is expected to increase by 25 basis points to 1.25 percent. On Thursday, the UK releases retail sales, and the BoE will make a rate announcement, with the rates expected to remain at 0.25%. In the US, the major release is unemployment claims, with an estimate of 241 thousand.

After a bruising election which saw the Conservatives squander a comfortable majority, a chastened Prime Minister May met with French President Emmanuel Macron on Wednesday. The two leaders are moving in opposite directions; one leader is heading for a massive majority, while the other is clinging onto power by her fingernails and may be forced out of office in the near future. Macron, who is expected to support a hard line against Brexit, stated that the EU would leave the "door open" in case Britain changed its mind. That, however, is a far-fetched scenario. As for May, she continues to exude an air of "business as usual", and insisted that the Brexit talks would commence as planned on June 19. Will the talks start on time? There are reports that European officials will ask for a delay, given the political turmoil in Britain. On Tuesday, Denmark's Finance Minister, Kristian Jensen, said that he hoped that the inconclusive UK vote would lead to a "time out", so that the UK can rethink its approach to Brexit. The Europeans, stung by Brexit, are not feeling much sorrow for May's troubles, and she will have to soften her approach her previously hard-nosed approach to Brexit. If the new government expresses a willingness to negotiate a "soft Brexit", which keeps the UK in the single market, this would be a positive development for British businesses, and could boost the pound, which has taken a beating since the Brexit vote last June.

The Federal Reserve be on center stage on Wednesday, when it announces the new benchmark rate. The Fed is widely expected to raise interest rates by a quarter point to 1.25%, so the markets will be focusing on the language of the rate statement and economic projections. What is less clear, however, is what the Fed has planned in the second half of 2017. Analysts are predicting that the Fed will deliver a "dovish hike", meaning that together with the rate increase, the Fed rate statement will be cautious in tone, and dovish regarding additional rate hikes. Earlier in the year, three rate hikes in 2017 seemed almost a given, but currently, the odds of a September move are just 28%. There are two key items which could affect European stock markets. First, the Fed Economic Projections will detail forecasts of inflation, growth and unemployment, and most importantly, the rate hike path. With the US economy performing better in the second quarter, there's a strong likelihood that the Fed will not moderate its rate hike projections,which is good news for the dollar. Secondly, the markets will be looking for details regarding its plan to lower the $4.2 trillion balance sheet. If the Fed outlines a plan to reduce its holding in H2, the dollar could respond positively. Another variable is the political paralysis which has engulfed Washington. With the Trump administration spending most of its energy on damage control, little progress is being made with regard to Trump's agenda of tax reform and major spending on infrastructure. The markets are becoming more skeptical about Trump's ability to work with Congress, and if this sentiment is shared by the Fed, it is likely to sound dovish regarding rate hikes in September or December.

Euro Hits 7-Month High against Dollar after Weak US CPI and Retail Sales ahead of FOMC; Sterling Reverses Post-UK...

The dollar fell after the release of a weak set of US data that would be disappointing for the Federal Reserve, which is expected to deliver a 25-basis point rate hike later today. The broadly weaker greenback helped sterling erase losses made from weak UK wage data.

Both US CPI and retail sales numbers for May came in short of expectations, which resulted in the dollar index falling to a seven-month low of 96.32 after having risen to as high as 97.11. Against the yen, the dollar slid to 108.94 yen from 110.33, the lowest since April 21.

Headline CPI was weaker than expected at -0.1% month-on-month in May, reversing a prior increase of 0.2%. It was expected to remain flat. Meanwhile, year-on-year CPI rose 1.9% versus a prior 2.2%. The further deceleration in core inflation to 1.7% year-on-year was the lowest since May 2015. It was forecast to match the prior 1.9% rise.

The US retail sales data showed a 0.3% month-on-month decline in the headline number last month from the prior 0.3% rise. Retail sales ex-autos were also down by the same amount and the control group (ex auto, gasoline, food service and building materials) was flat on the month. There were some minor upward revisions to April's figures but not enough to offset the shortfall in May.

Despite today's weak data, the markets are still expecting the Fed to hike rates after concluding a two-day policy meeting today. The data likely isn't weak enough for them to not deliver, however, it wouldn't be surprising if the communication is dovish regarding the pace of future hikes particularly given the recent weakness in core CPI. It is widely expected that the Fed will deliver a 25 basis-point increase to the Fed funds target rate to between 1.00% to 1.25%.

Sterling reversed earlier session losses made after a disappointing UK employment report and rose briefly above the key $1.2800 level. The pound slipped against the dollar to $1.2722 on weaker-than-expected UK earnings data which showed average weekly earnings rose 2.1% year-on-year in April and just 1.7% year-on-year for the ex-bonus number, the lowest in more than two years. The disappointing data add to concerns that low wage growth will dampen UK consumer spending amid rising inflation. The data reinforce those expecting that the Bank of England will not change monetary policy at tomorrow's policy meeting.

The euro rose to its highest in seven months against the greenback to hit $1.1295, after the dollar broadly weakened on the release of the soft US data. There was little impact earlier in the session to Eurozone industrial production data which rose 0.5% month-on-month in April, as expected. March was revised higher to a reading of 0.2%.

The loonie extended gains today, pressuring the USD/CAD pair to a low of C$1.3163, down from Friday's C$1.3537 high after comments from Bank of Canada officials this week that hinted to a rate increase later this year.

Gold jumped to a peak of $1279.37 an ounce from $1264.18, driven by a broadly weaker dollar.

Oil prices fell after the report from the Energy Information Administration showed US crude inventories declined last week as refineries increased output. WTI crude slid to $45.08 a barrel immediately after the data from an earlier high of $46.45.

Strong Gains for Yen as US Retail Sales, CPI Disappoint

USD/JPY has posted considerable losses on Wednesday, as the pair is down 0.70 percent. In the North American session, the pair is trading at 109.25. On the release front, Japanese Revised Industrial Production rebounded strongly in April, posting a gain of 4.0 percent. This was just shy of the forecast of 4.1 percent. In the US, consumer data was weak, as retail sales and CPI posted declines of 0.3% and 0.1%, respectively. Later in the day, the Federal Reserve announces its benchmark rate, which is expected to increase by 25 basis points to 1.25 percent. On Thursday, the US releases unemployment claims, with an estimate of 241 thousand.

In recent months, Federal Reserve policymakers have been sending out broad hints that a rate hike is on the way, and the markets expect the Fed to make a move later on Wednesday. The markets have priced in a rate hike at close to 100%, but there is still plenty of anticipation in the air, as analysts will be focusing on the language of the rate statement. Analysts are predicting that the Fed will deliver a "dovish hike", meaning that together with the rate increase, the Fed rate statement will be cautious in tone, and dovish regarding additional rate hikes. Earlier in the year, three rate hikes in 2017 seemed almost a given, but currently, the odds of a September move are just 28%. There are two key items which could affect the US dollar. First, the Fed's Economic Projections will detail forecasts of inflation, growth and unemployment, and most importantly, the rate hike path. With the US economy performing better in the second quarter, there's a strong likelihood that the Fed will not moderate its rate hike projections,which is good news for the dollar. Secondly, the markets will be looking for details regarding its plan to lower the $4.2 trillion balance sheet. If the Fed outlines a plan to reduce its holding in H2, the dollar could respond positively. Another variable is the Fed's view of the political paralysis which has engulfed Washington. With the Trump administration spending most of its energy on damage control, little progress is being made with regard to Trump's agenda of tax reform and major spending on infrastructure. The markets are becoming more skeptical about Trump's ability to work with Congress, and if this sentiment is shared by the Fed, it is likely to sound dovish regarding rate hikes in September or December.

The BoJ will be in the spotlight on Thursday, as it releases a rate statement, followed by a press conference with BoJ Governor Haruhiko Kuroda. The BoJ has maintained an ultra-loose monetary policy in order to prop up inflation and domestic demand. Although the economy has recently received a boost from stronger global demand, inflation remains well below the central bank's 2.0% target, and consumer demand has been soft. The BoJ is unlikely to shift directions and tighten policy anytime soon, but analysts will be combing through the rate statement and Kuroda's follow-up comments, looking for nuances in BoJ language. A key component of the BoJ's policy has been bond purchases, but the bank has slowly been reducing these purchases, and could make reference to the slowdown in the bond-buying program on Thursday. If the central bank's tone is more hawkish than expected, the yen could respond with gains.

Trade Idea Wrap-up: USD/CHF – Hold short entered at 0.9720

USD/CHF - 0.9654

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9677

Kijun-Sen level : 0.9677

Ichimoku cloud top : 0.9695

Ichimoku cloud bottom : 0.9682

Original strategy :

Sold at 0.9720, Target: 0.9620, Stop: 0.9715

Position : - Short at 0.9720

Target : - 0.9620

Stop : - 0.9715

New strategy :

Hold short entered at 0.9720, Target: 0.9620, Stop: 0.9715

Position : - Short at 0.9720

Target : - 0.9620

Stop : - 0.9715

Dollar’s retreat after meeting resistance at 0.9728 late last week has retained our bearishness and consolidation with mild downside bias remains for weakness to indicated level at 0.9640, however, break there is needed to signal the rebound from 0.9613 has ended, bring retest of this level first. A break below this level would extend recent decline to 0.9600-05 (50% projection of 1.0100-0.9692 measuring from 0.9808) later.

In view of this, we are holding on to our short position entered at 0.9720. Above said resistance at 0.9728 would abort and signal a temporary low has been formed at 0.9613 last week instead, bring a stronger rebound to 0.9761 resistance but price should falter below resistance at 0.9808.

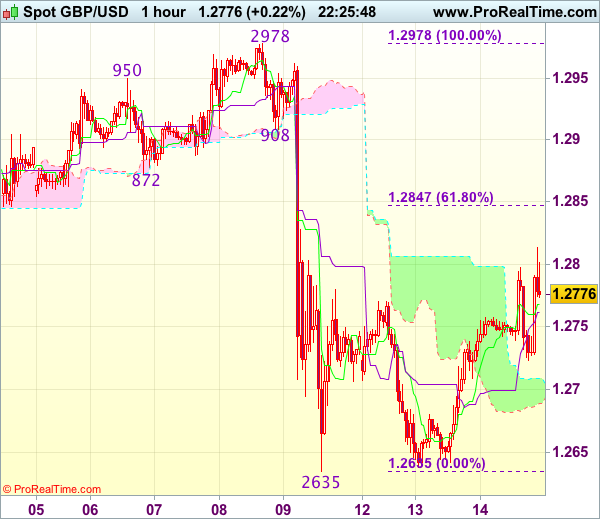

Trade Idea Wrap-up: GBP/USD – Sell at 1.2850

GBP/USD - 1.2772

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2768

Kijun-Sen level : 1.2761

Ichimoku cloud top : 1.2709

Ichimoku cloud bottom : 1.2689

Original strategy :

Sell at 1.2850, Target: 1.2750, Stop: 1.2885

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.2850, Target: 1.2750, Stop: 1.2885

Position : -

Target : -

Stop : -

As the British pound has surged again after staged a strong rebound yesterday, suggesting further consolidation above last week’s low at 1.2635 would be seen and initial upside risk remains for gain to 1.2815-20, however, reckon 1.2845-50 (61.8% Fibonacci retracement of 1.2978-1.2635) would hold from here, bring retreat later, below 1.2720-25 would bring weakness to 1.2680-85 but break of latter level is needed to signal the rebound from 1.2635 has ended, then fall to 1.2650 would follow.

In view of this, we are looking to sell cable on recovery as 1.2845-50 should limit upside. Above 1.2870-80 would suggest recent decline has ended at 1.2635 instead, risk a stronger rebound to 1.2905-10 and possibly 1.2930 but price should falter well below resistance at 1.2978.

Trade Idea Wrap-up: EUR/USD – Buy at 1.1235

EUR/USD - 1.1278

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 1.1247

Kijun-Sen level : 1.1244

Ichimoku cloud top : 1.1207

Ichimoku cloud bottom : 1.1199

Original strategy :

Buy at 1.1235, Target: 1.1335, Stop: 1.1200

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1235, Target: 1.1335, Stop: 1.1200

Position : -

Target : -

Stop : -

The single currency has rallied in US opening on dollar’s broad-based weakness and indicated resistance at 1.1285 was breached, adding credence to our bullish view that recent upmove has resumed, hence upside bias remains for further gain to previous chart resistance at 1.1300, break there would encourage for headway to 1.1340-45 and later towards chart point at 1.1366.

In view of this, we are looking to turn long on pullback. Below 1.1195-00 would abort and prolong choppy trading below 1.1285, risk weakness to 1.1185, then towards said support at 1.1166 which is likely to hold from here.