Sample Category Title

European Open Briefing: The Federal Reserve Raised Rates Yesterday

Global Markets:

- Asian stock markets: Nikkei down 0.40 %, Shanghai Composite lost 0.05 %, Hang Seng declined 0.90 %, ASX 200 fell 1.10 %

- Commodities: Gold at $1267 (-0.70 %), Silver at $16.95 (-1.10 %), WTI Oil at $44.50 (-0.10 %), Brent Oil at $47.00 (+0.05 %)

- Rates: US 10-year yield at 2.13, UK 10-year yield at 0.93, German 10-year yield at 0.23

News & Data

- Australia Employment Change 42k vs 10k expected

- Australia Unemployment Rate 5.5 % vs 5.7 % expected

- Australia Participation Rate 64.9 % vs 64.8 % expected

- Australia MI Inflation Expectations 3.6 % vs 4.0 % previous

- New Zealand GDP q/q 0.5 % vs 0.7 % expected

- New Zealand GDP y/y 2.5 % vs 2.7 % expected

- Global stocks pressured by report on Trump probe, Fed hike, soft U.S. data – RTRS

- Fed raises rates, unveils balance sheet cuts in sign of confidence – RTRS

- U.S. consumer prices, retail sales weaken in May – RTRS

Markets Update:

The Federal Reserve raised rates yesterday, as expected by the market. The statement and projections were slightly more hawkish though, with the central bank saying that the recent weakness in inflation is largely transitory. The US Dollar came under pressure ahead of the FOMC, due to soft inflation and retail sales numbers, but recovered after the announcement.

The Australian Dollar rallied overnight, after stronger than expected employment data. AUD/USD rose from 0.7585 to a high of 0.7630. The pair eventually lost momentum, as resistance around 0.7630 proved again to be tough. However, the outlook is positive and intraday support is now seen at 0.7570 and 0.7520.

The New Zealand Dollar had a weak performance after NZ GDP data missed expectations. NZD/USD fell from 0.7310 to 0.7230 overnight. A break below 0.72 support could signal a pullback towards 0.7120 support.

Price action in the other major pairs was unusually quiet. The Euro is again consolidating around 1.12, while USD/JPY is struggling to get back to 110.

Today, both the Swiss National Bank and the Bank of England will decide on interest rates. No changes are expected, but the BoE meeting could be more interesting as inflation continues to rise in the UK.

Upcoming Events:

- 07:45 BST – French CPI

- 08:15 BST – Swiss CPI

- 08:30 BST – SNB Rate Decision

- 08:30 BST – SNB Press Conference

- 09:00 BST – Italian CPI

- 09:30 BST – UK Retail Sales

- 10:00 BST – Euro Zone Trade Balance

- 12:00 BST – Bank of England Rate Decision

- 12:00 BST – Bank of England Meeting Minutes

- 13:30 BST – US Philadelphia Fed Manufacturing Index

- 14:15 BST – US Industrial Production

- 14:15 BST – US Manufacturing Production

- 15:00 BST – US NAHB Housing Market Index

Market Morning Briefing: The Fed Hiked The Rates As Expected

STOCKS

Dow (21374.56, +0.22%) has been moving in line with our expectation as mentioned yesterday and could head towards our target of 21600 in the next 3-4 sessions.

Dax (12805.95, +0.32%) made an intra-day high of 12798 yesterday but came off sharply from there. Note that 13000 is a crucial near term resistance which if holds could push back the index towards 12400 again. Only on a confirmed break above 13000 could we become more bullish on Dax.

Shanghai (3132.56, +0.06%) closed near 3130 in line with what we had mentioned yesterday. A bounce back towards 3170 is on the cards for the near term.

Nikkei (19797.46, -0.43%) has bounced from immediate support near 19755 and while that holds, the index could rise back towards 20100 in the near term.

Nifty (9618.15, +0.12%) also came down to almost support levels near 9570 before again bouncing back to levels above 9600. While 9570-9550 holds, there is still scope for a sharp bounce towards 9700.

COMMODITIES

Muted price action had been seen in Gold (1267), as it remains in a slow corrective move which may take it to the support of 1242 but if the support holds, a quick bounce towards 1307 can’t be ruled out. Silver (16.97) is also hovering around its resistance of 16.95. A close above that could open up 17.60 as well.

Copper (2.57) is trading within the narrow range of 2.56-2.68. Only above 2.68, higher resistances of 2.84 can come into consideration. We will remain bullish on copper while it is trading above 2.55 regions on a closing basis.

On 10th of March, 2017, we had written in MB that 'Immediate support for Brent is at 45.42 and WTI at 44. We would not be surprised if we will see these levels within a few weeks of time” and those levels have almost come. At the same we had also warned yesterday that irrespective of oversold condition, a less than expected negative inventory (actual -1.7 vs. expected -2.3) could bring the bearish possibility again into consideration and the same had also happened. Now, considering the short term oversold sate, we may see some profit taking rally in Brent (47.02) and WTI (44.70) towards their respective resistances of 51.25 for Brent and 47 for WTI respectively. But the trend is still bearish in the medium term time frame. Any corrective bounce may face extreme selling pressure at the higher levels and could open up lower levels like 42 and 42.60 for both Brent and WTI respectively.

FOREX

The Fed hiked the rates as expected and laid out plans to trim the $4.5 trillion balance sheet. Dollar weakened briefly but the bullish reversal chances remain open.

Contrary to expectations, Dollar Index (96.94) made a fresh low at 96.32 before bouncing back near 97.00 but the technical picture hasn’t changed much as the upside reversal chances remain open but requires a break above 97.20-30 to confirm it.

Euro (1.1218) invalidated our Triangle pattern and registered a fresh high at 1.1296 but the stiff rejection at the higher levels imply inherent weakness which would be confirmed on a break below 1.1160.

Dollar-Yen (109.55) was rejected exactly from our resistance of 110.35 to a fresh low at 108.80 but the sharp recovery suggests that the Dollar bulls are still at play. The downside looks limited to 108.00 but a break above 110.35 may take it to 111.00 initially above which comes 113.00.

Pound (1.2740) briefly tested the major resistance 1.2800 but the failure to sustain the higher levels keeps the trend weak. Immediate support comes at 1.2600.

Aussie (0.7602), contrary to expectations, surged above 0.7600 on the back of much better than expected employment data (+42k against expectations of +10k in May). It is not clear at the moment if it will be able to test the higher resistance of 0.7700-50 levels without a correction and we prefer to wait for 1-2 sessions for clarity. Trend remains up with immediate support coming at 0.7550-20.

Dollar-Rupee (64.30) is trading at 64.30 in the NDF right now, totally indifferent to the Fed policy. It remains to be seen if the ECB meet today can move it. Repeat - the support of 64.30-20 is expected to hold and push it back to 64.60-80.

INTEREST RATES

The US yields moved lower and entered into the oversold territory. The 10Yr (2.13%) is trading at its crucial support and could bounce from these levels. The 30YR (2.77%) is also hovering around its crucial support of 2.79 and a close above that could open up 2.88 and 2.94 levels respectively .

The Japan-US 10YR (2.08%) is trying to break below immediate support levels and in case it falls sharply, could pull down Dollar-Yen with itself in the coming sessions. .

The German-US 10Yr (-1.91%) and the German-US 2YR (-2.06%) have bounced from immediate support levels and are heading towards medium term resistances which if holds, could again push off the yield spreads to lower levels. Euro could move up or remain stable in the next couple of sessions before falling off to lower levels.

FOMC: Model Dominates the Outlook Over Current Inflation

Today, the FOMC raised the fed funds target rate and will make further adjustments depending on the path of incoming data. This policy path is consistent with past guidance, but we are skeptical about what lies ahead.

Future Expected Inflation Dominates Current Inflation

The FOMC raised its target for the federal funds rate by one-quarter percentage point and made some slight adjustments to its interest rate forecast going forward. The minimal changes to the Fed's dot plot projections were also reflected in the economic forecasts. Real GDP growth was left essentially unchanged throughout the forecast horizon. The projection for the core PCE deflator was lowered for both 2017 and 2018 by 0.1 percentage point. Inflation, as measured by the PCE deflator, is expected to gradually rise but remain below the 2 percent target (top chart). The FOMC's full employment target has been more or less met.

From the FOMC's point of view, the model matters more than current inflation numbers. Based upon a low unemployment rate relative to expectations for full employment, future inflation should be rising as this model projects expected inflation toward the Fed's two percent goal.

Have Model Then Generate Dot-Plot

Given the model's projection of higher inflation, the FOMC projects one more rate hike in 2017, which also remains our forecast. However, this is highly dependent on a move upward in inflation. If inflation does not pick up, we expect no move in September. The dots showed 2018 and longerrun projections unchanged (middle chart).

The Fed's longer-run median projection for the neutral fed funds rate is three percent; with a two percent inflation target, the real long-run fed funds rate is implicitly one percent. Such a low real funds rate indicates something about potential growth inconsistent with the goals of the current presidential administration.

The Fed's Balance Sheet: Some Guidance, but Questions Remain

This afternoon's release was accompanied by an addendum providing additional details regarding the Fed's plans to normalize its balance sheet. The Fed stopped short of setting a specific time at which normalization would commence, only saying that they expected to begin implementing the program "this year." The Fed also refrained from setting a target end date/balance sheet size that would mark the end of normalization. The Fed did, however, confirm that it will implement normalization by decreasing its reinvestments of principal payments on maturing securities.

Specifically, the Fed will set a "cap" on the dollar amount of principal payments it will not reinvest, with all payments above this cap reinvested. The Fed anticipates that the cap will initially be $6 billion per month for Treasury securities and $4 billion per month for agency debt and mortgagebacked securities. The caps will then increase in steps of $6 billion and $4 billion, respectively, at three month intervals over a 12 month period until the caps reach $30 billion and $20 billion, respectively. On balance, this would be a relatively modest and gradual first step in reducing the Fed's sizable $4.5 trillion balance sheet.

Fed Raises Rates Hoping Inflation Turns Soon

As widely expected, the Federal Open Market Committee (FOMC) raised the target range for the federal funds rate by 25 basis points to between 1 and 1-1/4 percent.

The Committee also expects to begin normalizing the balance sheet later this year, having outlined a plan to gradually reduce its holdings by tapering reinvestments in its Treasury and MBS portfolio. The Fed expects to cap runoff at $10 billion per month initially ($6bn for UST/$4bn for MBS) before raising it to $50bn per month within a year with the same 60/40 split between UST and MBS.

The Committee was somewhat sanguine on the economy, indicating that activity has been "rising moderately" while the labor market "continued to strengthen" as job gains "moderated but have been solid" and unemployment declined. The statement highlighted consumer spending has accelerated recently, while business investment continued to expand. Inflation was viewed as having "declined recently" while the core measure is running "somewhat below 2 percent," but expected to stabilize near the target over the medium-term. At the same time, inflation expectations were viewed as little-changed and still low.

The Summary of Economic Projections saw the Committee lower its unemployment forecasts by 0.2 to 0.3 percentage points through 2019, anticipating the jobless rate to average 4.3% this year and 4.2% over the subsequent two years, with the Committee's view of unemployment over the longer-term 0.1pp lower at 4.6%. At the same time, the FOMC revised its near-term inflation outlook, lowering its 2017 average for PCE and core PCE deflator by 0.3 and 0.2pp, respectively, given the weaker data to date. GDP projections were slightly higher at 2.2% for this year (from 2.1% as of March SEP), but remained unchanged for 2018 and 2019, at 2.1 and 1.9%, respectively.

The SEP interest rate projections were largely unchanged, with the median dot still suggesting one more hike later this year, with three apiece next year and in 2019. The median projection for the equilibrium rate hasn't changed, but the range has tightened to between 2.5% to 3.5%.

There was one dissenter with Kashkari (FRB Minneapolis) voting against the remaining Committee members, given his preference to keep the rate unchanged.

Key Implications

This statement was largely as expected, with the Fed emphasizing the continued labor market improvement and accelerating economic growth as reasons to be optimistic for the economic and inflationary outlook. As such, the Fed appears unfazed by the recent inflationary slowdown, viewing it as temporary despite another weak CPI print this morning. Echoing that view was the SEP, which lowered near-term inflation projections, but left the forecasts for the coming years unchanged.

Given the lower inflation projections it was somewhat surprising that the dots were little changed, suggesting another rate hike and the beginning of the normalization process later this year. The Fed did lower its view of the natural rate of unemployment, albeit slightly, suggesting that the Committee is chalking up some of the current inflation misses to what appears to be a lower than previously believed unemployment rate gap.

At this point, we expect the Fed to pay very close to inflation numbers going forward. Should the low unemployment begin to generate the anticipated wage and inflation gains, another rate hike is very much a possibility later this year, as is the start of balance sheet normalization. However, should inflation continue missing, we would expect the Fed to pare back its rhetoric and likely further lower its projections for the natural rate of unemployment.

No Surprise as the Fed Raises Rates, Continues to Signal Gradual Tightening

Highlights:

- Today's rate hike brings the target range for the fed funds rate up to 1.00-1.25%.

- The statement was upbeat on the economic backdrop and labour market conditions. The Committee is "monitoring inflation developments closely" although that is not new to this policy statement.

- Updated projections show slightly stronger growth is expected this year. Inflation was revised lower for 2017 but is forecast to return to 2% thereafter.

- The unemployment rate has been revised lower by 0.2-0.3 percentage points over the forecast horizon. The rate is seen remaining below its longer run level, which was revised down to 4.6%.

- The fed funds 'dot plot' was little changed. Most Committee members expect another rate hike this year, and a median of three more increases are seen as appropriate next year.

- The Fed expects to begin normalizing its balance sheet this year. The announced monthly caps on holdings that will not be reinvested imply a gradual and predictable shrinking of asset holdings.

Our Take:

Today's rate hike was fully expected and the Fed made few waves with their policy statement and updated projections. There were further details on the Committee's plan to begin normalizing the balance sheet, a process they said is likely to start this year. The Fed is going to lengths to prime markets for a change in their reinvestment policy, likely with 2013's 'taper tantrum' in mind. Their cautious approach is consistent with our view that the central bank will take a pass on raising rates in September when we expect they will begin tapering. Aside from that pause, we look for the Fed to continue gradually raising rates and think today's meeting reinforces our forecast. Chair Yellen downplayed unexpectedly low inflation readings in recent months, attributing much of the shortfall to one-off price declines. She also indicated that conditions are in place for inflation to move higher. We agree that a tight labour market and above-trend growth should help reverse recent moderation in inflation. As such, further removal of accommodation is needed to keep monetary policy from falling behind the curve.

GBP/USD Retesting Support/Resistance Level

Forward we walk!

After GBP/USD's election price action to end last week, price has now printed a clean technical pullback.

Open up your MT4 charts and take a look at the GBP/USD daily:

GBP/USD Daily:

This is a range that we've been following on the blog for quite a while now and one that was only broken as Theresa May called the election.

At the time, markets of course didn't expect Corbyn's Labour Party to do as well as they did and priced accordingly. But now we know the result, price dropped back to it's starting price and normal price action has resumed.

Normal price action that involves respecting support/resistance levels on pullbacks and as we've said in previous posts featuring GBP/USD, this is a level that has been respected numerous times on both sized now. There is no questioning the validity of this level.

Fed Surprises But It Is Enough To Turn The Dollars Tide

Fed surprises but it is enough to turn the dollars tide

The Feds were completely unfazed by the soft May CPI report. Mind you the last minute data miss was unlikely to alter their long-term view but none the less we are perhaps witnessing US core CPI becoming the most important data print for traders to key on for the remainder of 2017, even more so than NFP.

The dollar collapsed on the soft CPI data print as dealers viewed three consecutive months of benign core inflation more trend than transitory. The fall in 10-year yield to 2.10 was staggering as was the 100 pip drop on USDJPY as the volatility suggests that the CPI print will be the cornerstone for establishing USD bias for the remainder of 2017.

But it was a case more of two sessions as the Greenbacks morning swoon gave way to an afternoon dollar recovery amidst very hawkish price action.Mind you the bucks recovery should be taken with a grain of salt given the morning CPI induced sell off. The Greenback surprising support came as Feds stuck to their script while adding a couple of shockers by underscoring more balance sheet guidance than the markets expected and downplaying the benign core CPI inflation metrics

While the dollar and US yields have come off overnight lows there remains considerable doubt among investors that the US economy is running hot enough or that inflation will significantly turn the corner to warrant the current FOMC members rate hike expectations.As if in defiance to the markets view an unapologetically hawkish Janet Yellen has left more than a few scratching their heads wondering what actual inflation red light is causing the Feds to tap the stimulus brakes. Their inflation rhetoric was over the top hawkish referencing this year’s run of exceptionally tepid US core inflation prints “ one -off.” The markets are viewing this data more negatively than the Fed which begs the question, are the Fed’s inflation models of crystal balls that much clearer than everyone else’s? Given the market’s glass half full view of the Feds, I suspect traders will have a tough time digesting this overly confident inflation communique from Dr Yellen and will unlikely turn the tide for the beleaguered dollar

However, the real hawkish surprise was offered up in the complete detail regarding balance sheet normalisation. Unexpectedly the Fed has issued an addendum to its ‘Policy Normalization Principles and Plans’ it will allow $6 billion of Treasuries to roll off the balance sheet and increase in steps of $6bn at three-month intervals over 12 months until it reaches $30bn per month. Without question, they delivered way more details than was expected and it’s not such a stretch to assume that the Feds will commence this roll off in September.

But for the beleaguered greenback, the Feds are not the only game in town as the lack of progress on the US economic policy agenda will be an onerous burden for the US dollar through 2017. With more central banks joining the QE taper club, interest rate differentials will likely play less favourably into the dollar hand, so despite short-term dollar reprieves, until the Tump administration gets their economic house in order the dollar could struggle to regain its mantle as king of the hill.

Japanese Yen

Predictably the biggest mover overnight was JPY. And despite the unexpectedly hawkish FED, USDJPY has failed to recover the overnight loss and is struggling for traction in early trade weighed down by the risk fallout from the latest Trump headlines suggesting that special counsel Mueller is investigating President Trump for possible obstruction. .Equity futures wobbled on the news and given investors sensitivity to all things US political risk we could see some follow through on this headline.But so far in early trade 109.30 USDJPY has held as perhaps investors are all too accustomed to these headlines and are more or less desensitised to Trump noise.

Euro

The Euro remains well supported on dips despite the ECB guidance suggesting a status quo on hold approach. Investors remain bullish and appear poised to add on to EUR longs

British Pound

Focus remains on election fallout while the BOE looks through the higher inflation print as little more than a pass-through function of the weaker pound. Given the political landmines dotting the UK landscape, selling GBP on rallies should offer the greatest risk-reward until further clarity on Brexit negations is forthcoming

Australian Dollar

The Australian dollar continues to trade constructively as the market lean suggests early year consternation over employment and inflation may be overplayed as the market sits tight just awaiting critical jobs and inflation expectations corroborating the RBA view to look through soft economic prints in Q1

USD/CAD Canadian Dollar Lower After Fed Rate Hike

The Canadian dollar depreciated on Wednesday after the U.S. Federal Reserve raised the benchmark US interest rate by 25 basis points as expected. The Fed also outlined the plans to gradually reduce its massive balance sheet later this year. The American central bank Chair was not concerned with inflation remaining weak and attributed current levels to temporary effects such as cellphone bills and drug prices. Earlier today the Consumer Price Index (CPI) and the core CPI came in lower than expected. CPI showed a contraction of 0.1 percent and the core CPI which is the Fed’s favourite measure of inflation grew less than expected at 0.1 percent. US retail sales also disappointed with a 0.3 percent contraction on both the headline and core numbers.

The loonie got a boost earlier this week when two officials from the Bank of Canada (BoC) discussed the possibility of reducing stimulus after the economy is displaying consistent growth. The Canadian dollar rallied after those comments and only the mighty Fed rate hike is keeping the CAD down.

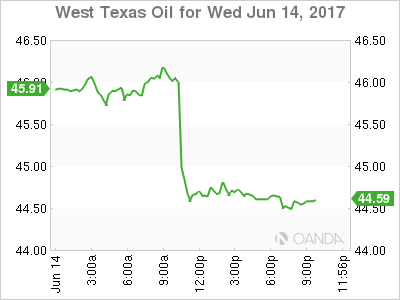

For a second week in a row the oil inventories sank crude prices. This time it was not a buildup of crude stocks, but a large build of weekly gasoline inventories. The price of WTI fell more than 3 percent but did not drag the loonie down as the currency was still trading on the back of the comments from Bank of Canada officials.

The sugar deal between the US and Mexico appears to have been finalized. It marks the end of a years long dispute is intended to avoid tariffs on Mexican exports of the sweetener to the US. Mexico had already threatened to walk out of the NAFTA negotiations if tariffs are part of the conversation. The sugar agreement has rubbed producers on both sides the wrong way as some compromises were made in all sides. The NAFTA renegotiation is scheduled for the Fall after the US has already started the process to have those talks by late August.

The USD/CAD gained 0.364 in the hour after the Fed released its policy statement. The currency pair is trading at 1.3250 very close to the daily high after the end of the press conference by Fed Chair Janet Yellen. The loonie was up against the USD in the morning as US data disappointed but due to the timing would have little effect on the upcoming decision of the US central bank. The anticipated US rate hike came into being and will pressure the Bank of Canada (BoC) to keep up if it doesn’t want the rate gap to widen more if the Fed follows with another rate hike in September or December.

Another big concern for the Canadian central bank is the state of household debt. It dipped slightly in the first quarter but remains near record highs and could prove to be a big problem if the central bank takes too long to hike rates or if the move is too sudden. The ratio of debt to disposable income is a staging 166.9 percent. The central bank seems to be preparing the market even if the move could come near the end of the year or in early 2018.

Oil lost 3.614 percent on Wednesday. The price of West Texas Intermediate is trading at $44.70 after the release of the weekly crude inventories in the US by the Energy Information Administration (EIA) showed a lower than expected drawdown of 1.7 million barrels and a surprise buildup in gasoline stocks of 2.1 million barrels when a draw of 1 million was expected once again put downward pressure on crude. Low energy prices will keep global inflation under control and could foil the plans of the US Fed of another rate hike if US inflation does not pick up before the end of the year.

Market events to watch this week:

2:00 pm USD FOMC Statement

2:00 pm USD Federal Funds Rate

2:30 pm USD FOMC Press Conference

6:45 pm NZD GDP q/q

9:30 pm AUD Employment Change

Thursday, June 15

3:30 am CHF Libor Rate

3:30 am CHF SNB Monetary Policy Assessment

3:30 am CHF SNB Press Conference

4:30 am GBP Retail Sales m/m

7:00 am GBP MPC Official Bank Rate Votes

GBP Monetary Policy Summary

GBP Official Bank Rate

8:30 am USD Unemployment Claims

Tentative JPY Monetary Policy Statement

Friday, June 16

Tentative JPY BOJ Policy Rate

2:30 am JPY BOJ Press Conference

8:30 am CAD Core Retail Sales m/m

8:30 am USD Building Permits

Fed Hardly Blinks, AUD Jobs Next

Fed day was a wild ride that started with soft data and sudden worries about a dovish Fed and ended with Yellen sticking to the Fed plan. The dollar did a 200 pip round trip but at the end of the day the Australian dollar led the way and the Swiss franc lagged. Aussie jobs are due next. Our Dax was stopped out at 12880.

Soft CPI and retail sales reports caused a quick rethink on the Fed among analysts and in markets. Core inflation rose 1.7% y/y compared to 1.9% expected and retail sales were down 0.3% compared to a flat reading expected.

In the aftermath, USD/JPY crumbled to 108.95 from 110.30 as Treasury yields dropped to post-election lows. But the euro chart was telling. Resistance at the election-night high of 1.1299 held and the 100-pip rally stalled.

As a small panic set in among dollar bulls, Goldman Sachs and JPMorgan warned that a Fed communication shift was going to happen. It didn't.

The Fed statement was virtually unchanged. There was a nod to lower inflation but no wavering in the forecast for a return to 2% inflation in the medium term. In addition, the forecasts didn't change except for lower unemployment.

The dollar bears hung on for every word from Yellen's press conference but finally threw in the towel when she blamed low inflation on one-off effects. The euro completely retraced the rally and hit a session low at 1.1193. USD/JPY rebounded as high as 109.89.

It's important to note that while Yellen was confident in her assessment, she said inflation would be watched closely and highlighted data dependency. Given low expectations of a hike in September, there are some upside risks but there won't be any answer with a light eco calendar until the end of the month.

One spot where the calendar (and the currency) is hot is Australia. At 0130 GMT the May employment report is expected to show 10K new jobs with unemployment at 5.7%. Technically, AUD/USD is looking more constructive after a break of the April highs and the 200-dma on Wednesday.

Dollar Recovers after Not that Dovish Fed Hike

Dollar recovers after Fed doesn't disappoint the market and raised federal funds rate by 25bps to 1.00-1.25%. Minneapolis Fed President Neel Kashkari dissented and voted for standing pat this time. But the greenback is supported by the fact that Fed didn't change inflation forecast for 2018 and 2019. Also, Fed maintained interest rate projections unchanged for 2017 and 2018. Fed released an "addendum to the political normalization principles" laying down the guidelines to shrink its balance sheet. Overall, even though the greenback was sold off after CPI disappointment earlier today, it's kept above key support level around 1.13 handle against Euro and more stimulus is needed to trigger sustained breakout.

In short, Fed raised 2017 GDP growth forecast to 2.2%, up from 2.1%. For 2018 and 2019, Fed projects GDP growth to be at 2.1% and 1.9%, unchanged from prior forecast. Forecasts on unemployment rate were revised down to 4.3% in 2017, 4.2% in 2018 and 4.2% in 2019, down from 4.5% for all the three years in prior projections. Headline CPE was revised to 1.6% in 2017, down from 1.9%. But for 2018 and 2019, headline PCE forecasts were kept unchanged at 2.0%. Core PCE forecast for 2017 was also revised to 1.7% , down from 1.9%. And, core PCE forecasts for 2018 and 2019 were also kept unchanged at 2.0%.

Meanwhile Fed fund rate projections were kept unchanged at 1.4% and 2.1% in 2017 and 2018 respectively. That means Fed is still projecting another rate hike this year. Rate projection for 2019 was just revised slightly down to 2.9%, down from 3.0%.

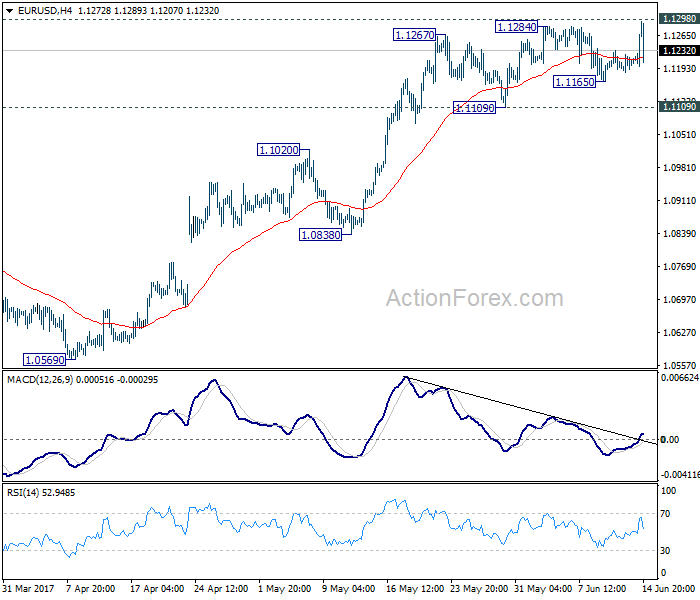

EUR/USD surged to as high as 1.2615 earlier today but hesitate ahead of 1.1298 resistance. The pair retreated after FOMC announcement. While we're staying bullish with 1.1109 support intact, at this point, there is no clear momentum to break through 1.1298 key resistance to confirm medium term bullish reversal yet.