Sample Category Title

Trade Idea Update: GBP/USD – Sell at 1.2850

GBP/USD - 1.2785

Original strategy :

Sell at 1.2845, Target: 1.2745, Stop: 1.2880

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.2850, Target: 1.2750, Stop: 1.2885

Position : -

Target : -

Stop : -

As the British pound has surged again after staged a strong rebound yesterday, suggesting further consolidation above last week’s low at 1.2635 would be seen and initial upside risk remains for gain to 1.2815-20, however, reckon 1.2845-50 (61.8% Fibonacci retracement of 1.2978-1.2635) would hold from here, bring retreat later, below 1.2720-25 would bring weakness to 1.2680-85 but break of latter level is needed to signal the rebound from 1.2635 has ended, then fall to 1.2650 would follow.

In view of this, we are looking to sell cable on recovery as 1.2845-50 should limit upside. Above 1.2870-80 would suggest recent decline has ended at 1.2635 instead, risk a stronger rebound to 1.2905-10 and possibly 1.2930 but price should falter well below resistance at 1.2978.

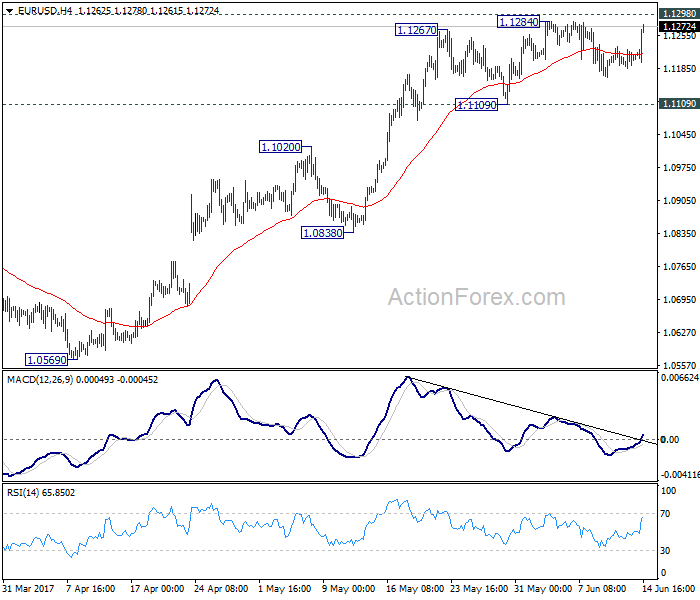

Trade Idea Update: EUR/USD – Buy at 1.1235

EUR/USD - 1.1273

Original strategy :

Sold at 1.1230, stopped at 1.1240

Position : - Short at 1.1230

Target : -

Stop : - 1.1240

New strategy :

Buy at 1.1235, Target: 1.1335, Stop: 1.1200

Position : -

Target : -

Stop : -

The single currency has rallied in US opening on dollar’s broad-based weakness, suggesting the correction from 1.1285 has ended at 1.1166 last week, hence consolidation with upside bias is seen for retest of this level, however, break there is needed to confirm recent upmove has resumed and extend further gain to previous chart resistance at 1.1300, break there would encourage for headway to 1.1340-45 and later towards chart point at 1.1366.

In view of this, we are looking to turn long on pullback. Below 1.1195-00 would abort and prolong choppy trading below 1.1285, risk weakness to 1.1185, then towards said support at 1.1166 which is likely to hold from here.

Another Soft Inflation Reading in May Presents a Challenge for the Fed

The headline consumer price index (CPI) fell 0.1% month-on-month in May. The main culprit was a 2.7% decline in energy prices, led by plummeting gasoline prices. That cooled inflation on a year-on-year basis to 1.9%, and marks the first reading below 2% since last November.

With the drop in energy prices largely expected, all eyes were on core inflation, where a modest 0.1% increase continued the recent string of soft readings. Core inflation now sits at 1.7% year-on-year, the lowest reading in two years.

Core inflation remained modest as many categories saw price declines. These included apparel (-0.3%, m/m), airline fares (-2.7%), communication (-0.2%) and medical care services (-0.1%). Still, looking at broader core services, prices were up 0.2% in May, stronger than the previous two months' pace.

The key shelter index, which accounts for one third of the CPI basket, rose 0.2% on the month, as rents rose 0.3%, and owner-occupied housing increased 0.2%. Shelter costs are up 3.3% over the past 12 months, and have been a key factor lifting services inflation over the past two years.

More surprising was another decline in core goods prices (-0.3%). That marks the third monthly drop in a row, and leaves prices 0.8% lower than a year-ago. The U.S. dollar has generally weakened so far in 2017, but this is not yet showing up in higher prices at the consumer level.

Key Implications

While May's inflation report was not likely to sway the Fed from its rate hike later this afternoon, today's report will likely give the Fed pause as it considers rate hikes over the remainder of the year. We take some reassurance from the fact that prices for core services have firmed somewhat. And, while core goods prices continued to be weak in May, price pressures are building at the import and producer level. It is likely only a matter of time before these are passed on to consumers.

Given these upstream price pressures, and an increasingly tight labor market, we expect inflation pressures to build through the remainder of the year. Particularly for goods inflation, where the dampening impact of a strong U.S. dollar is increasingly in the rear view mirror. Still, the fact that these price pressures are proving slow to show up does add considerable risk to further Fed hikes later this year.

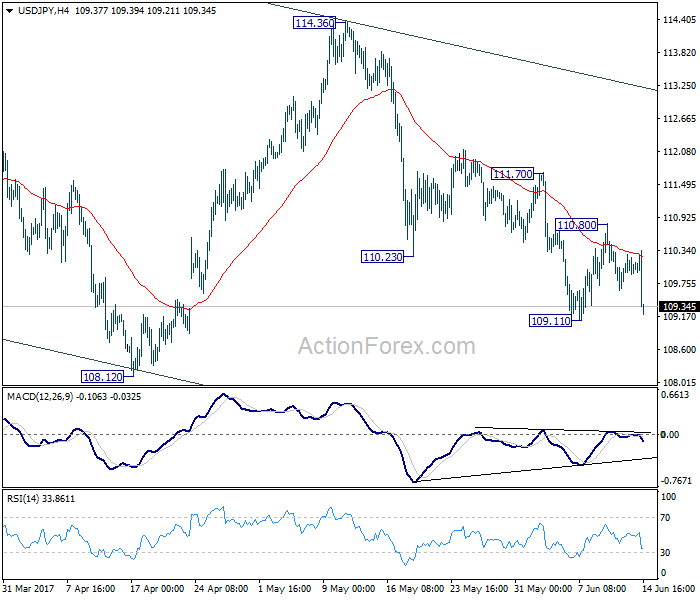

Trade Idea Update: USD/JPY – Sell at 109.70

USD/JPY - 109.36

New strategy :

Sell at 109.70, Target: 108.70, Stop: 110.05

Position : -

Target : -

Stop : -

The greenback ran into renewed selling interest at 110.35 and has dropped sharply in NY morning, current breach of 109.63 and 109.38 support signal rebound from 109.11 has ended at 110.81 earlier, hence retest of this level would be seen, break there would confirm recent decline has resumed for weakness to 109.00, then 108.75-80, however, near term oversold condition would limit downside and reckon 108.50 would hold.

In view of this, we are looking to sell dollar on recovery as 109.70-80 should limit upside. Above 110.00-05 would defer and prolog consolidation but only break of resistance at 110.35 would signal an intra-day low is formed instead, bring another bounce to 110.50, then towards said resistance at 110.81.

Retail Sales Pull Back in May

Retail sales fell 0.3% m/m in May according to the advance Census Bureau report. This fell shy of consensus expectations for a flat reading.

Sales at gasoline station sales fell 2.4%, largely reflecting lower prices. Sales at motor vehicle & parts dealers also fell 0.2%.

Excluding autos and gas, sales were flat on the month, but this came atop an upwardly revised 0.5% gain in April (previously reported at 0.3%). By category, the sharpest drop came in electronics (-2.8%), following two months of decent gains.

The 'control group' (excluding gas, autos, building materials, and food services) was also flat on the month. But again, the weak print comes atop a decent upward revision to 0.6% (from 0.2%).

Once again, non-store retailers showed consistent gains (+0.8%). The category is up 12.4% year-on-year and continues to take market share from traditional bricks and mortar retailers.

Key Implications

This was a soft report, but the weakness in May was made up for by the size of the upward revision to sales in March and April. Moreover, as confirmed in today's CPI report, some of the weakness is on the price side. In real terms, personal consumption expenditures are still in good stead, expected to advance by around 3% in the second quarter.

With the shift in buying patterns away from malls and toward online retailers, the advance retail sales measure has become a less reliable leading indicator. The recent pattern on spending data has been for upward revisions on subsequent estimates. This may be expected to continue going forward.

Later this afternoon the Fed will likely announce another 25 basis point increase in the fed funds rate, bringing the rate to a range of 1%-1.25%. If anything is going to delay the pace of future rate hikes it is a continuation of weak nominal spending data. Stay tuned.

CAC Gains Ground as Federal Reserve Hike Looms

The CAC index has posted slight gains in the Wednesday session, climbing 0.68 percent. On the release front, Eurozone Industrial Production climbed 0.5%, matching the estimate. There are a number of key events in the US, highlighted by the Federal Reserve rate announcement. As well, the US will release retail sales and CPI reports.

French President Emmanuel Macron is expected to cruise to a massive victory on Sunday, when France holds the second round of parliamentary elections. Polls point to Macron's En Marche party winning as much as 80% of the seats in the National Assembly. Macron is a strong supporter of the European Union, and a Macron-Merkel alliance could strengthen the EU at a time when Brexit and nationalistic parties have undermined European unity. Macron met with British Prime Minister Theresa May on Wednesday, and with one leader heading for a massive majority, with the other clinging onto power by her fingernails, was irony that simply couldn't be missed. Macron, who is expected to support a hard line against Brexit, stated that the EU would leave the "door open" in case Britain changed its mind. That is a far-fetched scenario, of course. As for May, she continues to exude an air of "business as usual", saying that the Brexit talks would commence as planned on June 19.

The Federal Reserve is widely expected to raise interest rates at the Wednesday meeting, so the markets will be focusing on the language of the rate statement and economic projections. The markets have priced in a rate hike at close to 100%, with an increase by 25 basis points raising rates to 1.25%. What is less clear, however, is what the Fed has planned in the second half of 2017. Analysts are predicting that the Fed will deliver a "dovish hike", meaning that together with the rate increase, the Fed rate statement will be cautious in tone, and dovish regarding additional rate hikes. Earlier in the year, three rate hikes in 2017 seemed almost a given, but currently, the odds of a September move are just 28%. There are two key items which could affect European stock markets. First, the Fed Economic Projections will detail forecasts of inflation, growth and unemployment, and most importantly, the rate hike path. With the US economy performing better in the second quarter, there's a strong likelihood that the Fed will not moderate its rate hike projections,which is good news for the dollar. Secondly, the markets will be looking for details regarding its plan to lower the $4.2 trillion balance sheet. If the Fed outlines a plan to reduce its holding in H2, the dollar could respond positively. Another variable is the political paralysis which has engulfed Washington. With the Trump administration spending most of its energy on damage control, little progress is being made with regard to Trump's agenda of tax reform and major spending on infrastructure. The markets are becoming more skeptical about Trump's ability to work with Congress, and if this sentiment is shared by the Fed, it is likely to sound dovish regarding rate hikes in September or December.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1189; (P) 1.1206 (R1) 1.1228; More....

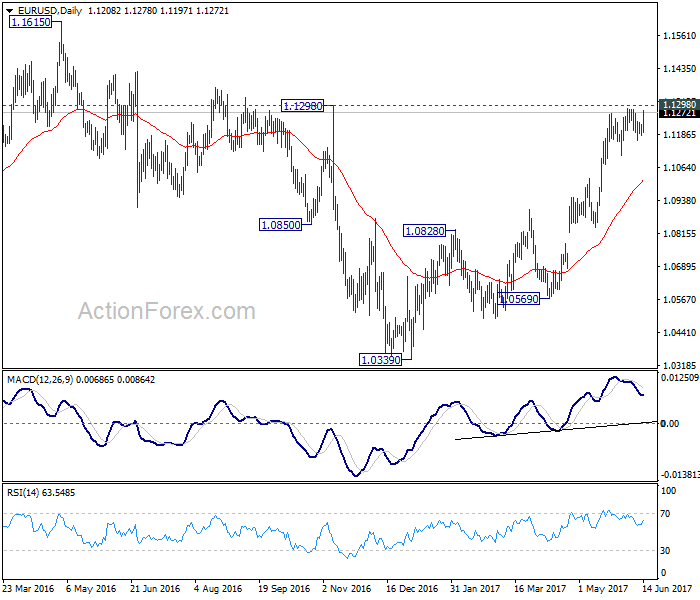

EUR/USD rebounds strongly in early US session but it's staying below 1.1284/1298 resistance zone. Intraday bias remains neutral at this point first. Main focus remain on 1.1298 key resistance. Decisive break there will carry larger bullish implication and target 1.1615 resistance next. On the downside, break of 1.1109 support will indicate short term topping and rejection from 1.1298. In such case, intraday bias will be turned to the downside for 1.0838 support.

In the bigger picture, the case for medium term reversal continues to build up with EUR/USD staying far above 55 week EMA (now at 1.0922). Also, bullish convergence condition is seen in weekly MACD. Focus will now be on 1.1298 key resistance. Rejection from there will maintain medium term bearishness and would extend the whole down trend from 1.6039 (2008 high). However, firm break of 1.1298 will indicate reversal. In such case, further rally would be seen back to 1.2042 support turned resistance next.

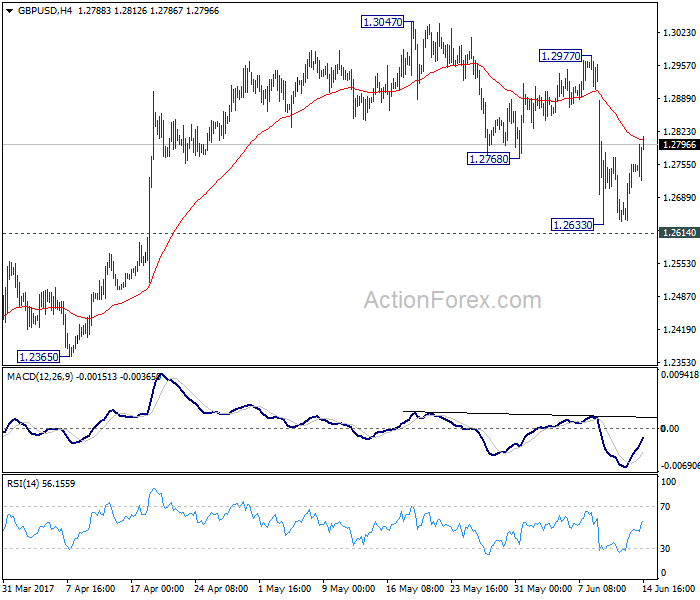

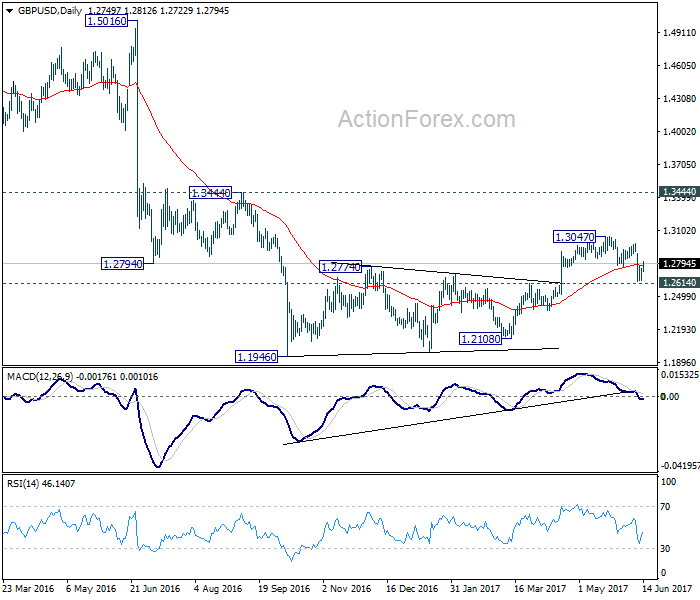

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2676; (P) 1.2716; (R1) 1.2791; More...

GBP/USD's rebound from 1.2633 continues today but still, intraday bias remains neutral first. Upside is expected to be limited below 1.2977 resistance to bring fall resumption. We continue to favor the case that consolidation pattern from 1.1946 has completed at 1.3047 already. Decisive break of 1.2614 resistance turned support would confirm our bearish view and target a test on 1.1946 low next. However, break of 1.2977 will dampen our view and turn bias back to the upside for 1.3047 and above.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. Price actions from 1.1946 medium term low are seen as a consolidation pattern, which could have completed after hitting 55 week EMA. Break of 1.1946 low will target 61.8% projection of 1.5016 to 1.1946 from 1.3047 at 1.1150 next. In case the consolidation from 1.1946 extends, outlook will stay remain bearish as long as 1.3444 resistance holds.

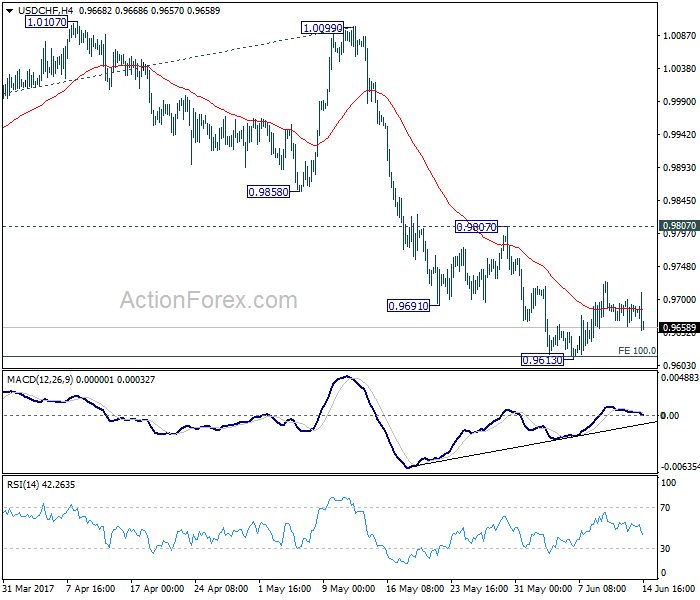

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9672; (P) 0.9683; (R1) 0.9697; More.....

USD/CHF weakens in early US session but stays above 0.9613. Intraday bias remains neutral first. As long as 0.9807 resistance holds, outlook remains cautiously bearish and deeper fall is expected. Break of 0.9613 will extend the whole decline from 1.0342 to 0.9548 support and below. We'd start to look for bottoming signal again as it approaches 0.9443 key support level. However, considering bullish convergence condition in 4 hour MACD, break of 0.9807 will indicate near term reversal and turn outlook bullish for 1.0099 resistance next.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.56; (P) 109.99; (R1) 110.37; More...

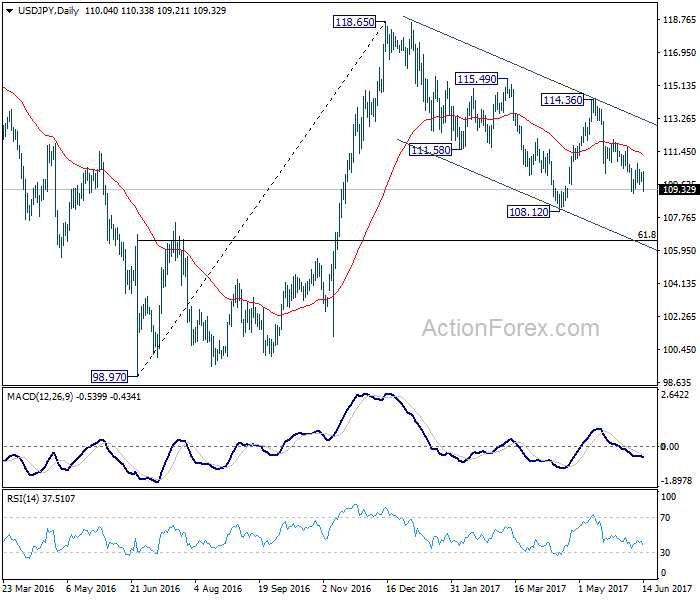

USD/JPY drops sharply in early US session but stays above 109.11 temporary low. Intraday bias remains neutral first. Near term outlook stays bearish with 111.70 resistance intact and further decline is expected. Break of 109.11 will resume the fall from 114.36 and target 108.12 low first. Break will extend the whole corrective fall from 118.65 to 61.8% retracement of 98.97 to 118.65 at 106.48. We will look for bottoming sign there. Meanwhile, break of 110.70 will indicate near term reversal and turn bias back to the upside for 114.36 resistance instead.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.