Sample Category Title

Trade Idea : EUR/USD – Hold long entered at 1.1205

EUR/USD - 1.1248

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 1.1260

Kijun-Sen level : 1.1257

Ichimoku cloud top : 1.1259

Ichimoku cloud bottom : 1.1244

Original strategy :

Bought at 1.1205, Target: 1.1305, Stop: 1.1235

Position : - Long at 1.1205

Target : - 1.1305

Stop : - 1.1235

New strategy :

Hold long entered at 1.1205, Target: 1.1305, Stop: 1.1235

Position : - Long at 1.1205

Target : - 1.1305

Stop : - 1.1235

As the single currency has retreated again after faltering below resistance at 1.1285 in part due to cross-selling against yen, suggesting further consolidation below this level would be seen, however, as long as 1.1235-40 holds, mild upside bias remains for recent upmove to resume after consolidation, above said resistance at 1.1285 would extend rise to another previous chart resistance at 1.1300, break there would encourage for headway to 1.1340-45 but overbought condition should limit upside to chart point at 1.1366.

In view of this, we are holding on to our long position entered at 1.1205. Only below support at 1.1202 would abort and signal top is formed instead, risk weakness towards indicated support at 1.1164, once this level is penetrated, this would signal recent upmove has ended, bring further fall to 1.1130-40 first.

Trade Idea : USD/JPY – Sell at 110.20

USD/JPY - 109.66

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 110.02

Kijun-Sen level : 110.13

Ichimoku cloud top : 111.01

Ichimoku cloud bottom : 110.77

Original strategy :

Sell at 111.00, Target: 110.00, Stop: 111.35

Position : -

Target : -

Stop : -

New strategy :

Sell at 110.20, Target: 109.20, Stop: 110.55

Position : -

Target : -

Stop : -

As the greenback met renewed selling interest at 110.73 yesterday and decline has accelerated after breaking below indicated support at 110.24, confirming our bearish view that recent decline from 114.37 top is still in progress and bearishness remains for further weakness to 109.30-35 (100% projection of 111.71-110.31 measuring from 110.73), then towards 109.00-05 (1.236 times projection) but near term oversold condition should limit downside to 108.70-75, bring rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as previous support at 110.24 should turn into resistance and limit dollar’s upside, bring another decline. Above 110.50 would defer but only break of said resistance at 110.73 would signal low is formed instead.

Technical Outlook: USDJPY Falls Below Daily Cloud On Growing Risk-Off Sentiment

The US dollar fell against Japanese yen to the lowest levels in nearly six weeks on strong risk aversion sentiment, fuelled by escalating geopolitical tension in the Middle East.

The pair eventually took out 200SMA support (110.34) which held downside attempts on Fri/Mon and broke below daily cloud base (110.15) and psychological 110.00 support during Asian session. Fresh extension lower was seen at the beginning of European trading that hit target at 109.58 (Fibo 76.4% of 108.11/114.36 rally. Bears are looking to fill the gap from 24 Apr for extension towards key short-term support at 108.11 (17 Apr low).

Daily studies turned into full bearish setup and support scenario, however, strongly oversold slow stochastic warns of correction.

Broken daily cloud base and 200SMA now act as solid resistances which should ideally cap corrective rallies.

Res: 110.00, 110.36, 110.53, 110.76

Sup: 109.48, 108.87, 108.32, 108.11

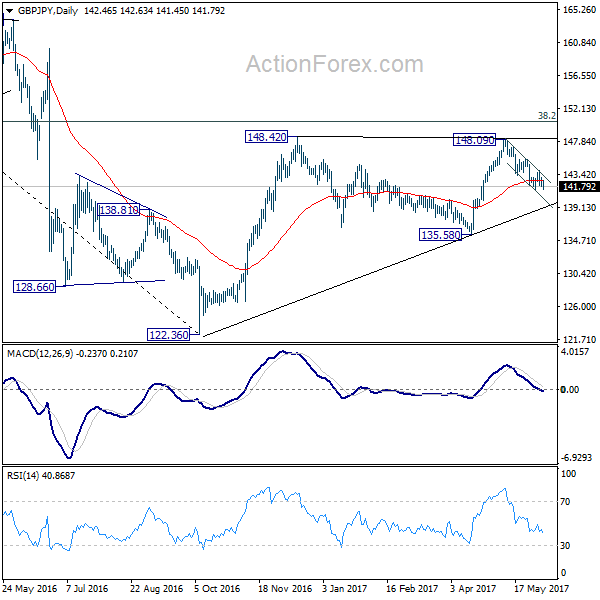

GBP/JPY Daily Outlook

Daily Pivots: (S1) 141.89; (P) 142.49; (R1) 143.13; More....

GBP/JPY is still staying above 141.43 temporary low and intraday bias remains neutral first. On the downside, break of 141.43 will extend the decline from 148.09. In such case, intraday bias is turned to the downside for 61.8% retracement of 135.58 to 148.09 at 140.35. At this point, we'd still expect rebound from 122.36 to resume later. Hence, we'd look for strong support below 140.35 to contain downside and bring rebound. On the upside, break of 143.93 will turn bias back to the upside for 148.09 resistance.

In the bigger picture, rise from 122.36 medium term bottom is still expected to extend to of 195.86 to 122.36 at 150.42. And decisive break there could pave the way to 61.8% retracement at 167.78. However, as the cross is starting to lose upside momentum, rejection below 150.42 and break of 135.58 support will indicate reversal and bring deeper fall back to retest 122.36 instead.

Currencies: Dollar Continues To Struggle, USD/JPY Slips Below The 110 Barrier

Sunrise Market Commentary

- Rates: Sideways ahead of big events on Thursday?

The eco calendar lacks impetus for trading today and tomorrow, suggesting investors will be side-lined ahead of Thursday's big events (ECB meeting, UK election, Comey hearing). The developing crisis in the Gulf region is a wildcard which could influence bond markets via equity markets or oil prices. - Currencies: Dollar continues to struggle; USD/JPY slips below the 110 barrier

Friday's poor US payrolls report kept the dollar in the defensive. This morning, USD/JPY fell below the psychological barrier of 110. FX traders are looking forward that Thursday's multiple event-risk with the UK election, ECB meeting and the hearing of former FBI director Comey. Risk aversion might be negative for USD/JPY, but more neutral for EUR/USD.

The Sunrise Headlines

- US equities traded near opening levels during yesterday's trading session and eventually closed slightly lower. Overnight, Asian stock markets are mixed with Japan underperforming (-0.5%) on a stronger yen.

- Saudi Arabia blamed the tiny Persian Gulf emirate of Qatar for “financing, adopting and sheltering extremists”. Egypt, the UAE, Yemen and Bahrain joined Saudi Arabia in breaking diplomatic and some commercial ties with Qatar

- Industries making up the bulk of the US economy continued to expand at a solid pace in May, adding to signs of steady growth this quarter. The May non-manufacturing ISM printed at 56.9 (vs 57.1 consensus), down from 57.5.

- Australia's central bank kept its policy rate at 1.5% amid growing concerns on the eco outlook. Conditions on the housing market still vary considerably, but there were signs the brisk rises in some markets were “starting to ease.”

- IMF Lagarde has offered a way out of the impasse over Athens' debts that would allow the EMU to release the next aid tranche. She suggested agreeing a deal whereby the IMF would stay on board in the bailout, as Berlin wants, but not pay out further aid until debt relief measures are clarified.

- President Trump will meet with House and Senate leadership today to plot a path forward on health care and tax reform—two of the administration's top legislative priorities that have been stalled in recent months.

- Today's eco calendar is very thin with only EMU retail sales and bond auctions in Austria and Germany (inflation-linked).

Currencies: Dollar Continues To Struggle, USD/JPY Slips Below The 110 Barrier

Dollar struggles; USD/JPY drops below 110 barrier

Trading was mostly technical in nature yesterday. EMU and US eco data had only a limited impact on FX trading. EUR/USD failed to extend its payrolls' gains. The pair even fell prey to modest intraday profit taking in thin trading. EUR/USD closed the session at 1.1254. USD/JPY hovered in a tight range near the post-payrolls lows as equities traded with a cautious negative bias. There was no additional negative fall-out on USD/JPY though. The pair closed the day at 110.45, almost unchanged from Friday.

Overnight, Asian stock markets trade cautiously negative with Japan underperforming. USD/JPY dropped below the post-payrolls lows, triggering additional yen buying. The pair fell below the psychological barrier of 110 to currently trade in the 109.70 area. USD/JPY's decline also weighs slightly on the dollar against the euro. The pair returned to the 1.1275 area, but for now the recent top stays out of reach. The decline of EUR/JPY is helping to cap further gains. The Reserve Bank of Australia as expected left its policy rate unchanged. The Aussie dollar lost temporary ground in lockstep with USD/JPY's decline overnight, but rebounded after the RBA decision. The RBA didn't profoundly change its assessment on the economy.

The eco calendar is almost empty today. Global factors and upcoming event risk will set the tone for FX trading. Markets will especially look forward to Thursday, with the UK Parliamentary elections, the ECB policy meeting and the testimony of former FBI director James Comey to a Senate committee. Political or other event risk mostly only had a temporary impact on global trading recently. This might again be the case this time, but some investor caution is likely until the uncertainty is out of the way. We expect USD/JPY to remain in the defensive short-term. The picture for EUR/USD might be a bit different. The ECB might make some amendments on its forwards guidance and could remove the downside risks to the economy outlook. As such this could be a precursor for more important action in September. Looking at the recent euro rally, a modestly positive change in the ECB's assessment is probably already discounted. This might cap further EUR/USD gains. Some ST squaring of positions/profit taking is possible. A cautious risk-off sentiment and the decline of EUR/JPY makes further EUR/USD gains less easy. We keep a neutral bias on EUR/USD and don't preposition for further gains

Technical picture

The USD/JPY rally ran into resistance in early May. A mini sell-off pushed the pair below the previous top (112.20), making the short-term picture negative. At the end of last week, there were tentative signs that the decline could slow. However, the post-payrolls decline and this morning's break below 110 are making the picture again outright negative. Return action lower in the 108.13/114.37 range remains possible.

Earlier May, EUR/USD failed to break below the 1.0821/1.0778 support (gap). Poor US data and political upheaval propelled EUR/USD north of the 1.1023 range top. The pair initially reached a short-term correction top at 1.1268. There was a minor break after Friday's disappointing US payrolls, but for now there are no follow-through gains. The Trump top/correction top at 1.1300/1.1366 is next resistance. USD sentiment will have to be quite negative to clear this hurdle short-term. For now, we don't preposition for a sustained break of this area. A return below 1.1023 would indicate that the upside momentum has eased.

EUR/USD holding near the post-payrolls top, but no follow-through gains

EUR/GBP

Sterling decline to slow ahead of the election?

Yesterday morning, sterling trade went into the defensive after the terrorist attack in London. However, the losses were modest and sterling soon returned to levels last seen at the end of the previous week. The UK services PMI declined more than expected from 55.8 to 53.8, but the report was largely ignored as an important factor for sterling trading. Quite the reverse, in technical trade, the UK currency even regained ground gradually later in the session. EUR/GBP closed the session at 0.8721. Cable finished the day at 1.2904.

Overnight, the BRC like-for-like sales declined slightly more than expected (-0.4% Y/Y), but we didn't see any lasting impact on sterling trading. There are no other important eco data in the UK today. Markets will try to get some insight on the potential impact of the terrorist attack on the outcome of Thursday's election. The lead of the conservative party is declining, but they are still in pole position. We don't expect a sustained rebound of sterling, but some profit taking of sterling shorts going into the final stage of the election is possible. So, a break of EUR/GBP beyond the recent top might become more difficult. First resistance comes in the 0.8774/88 area. EUR/GBP 0.8655 is a first minor support. A sustained return below the EUR/GBP 0.86 alert would suggest that the worst is over for sterling

EUR/GBP: most of the bad news for sterling discounted?

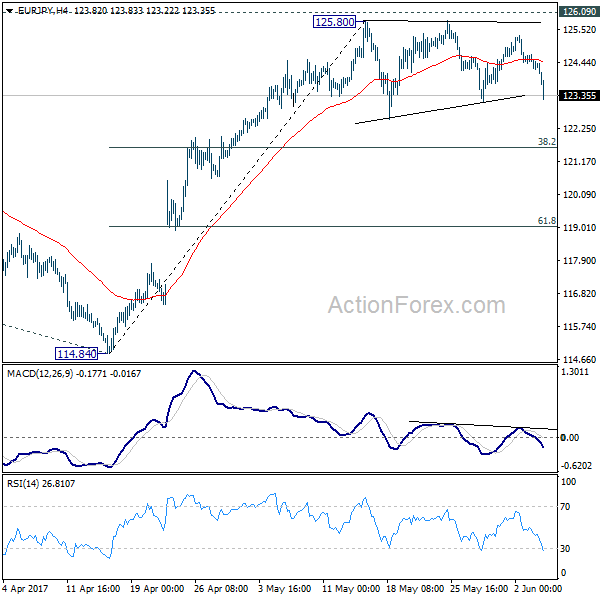

EUR/JPY Daily Outlook

Daily Pivots: (S1) 124.11; (P) 124.40; (R1) 124.62; More...

EUR/JPY drops sharply today but still, price actions from 125.80 are seen as a corrective pattern. In case of deeper fall, downside should be contained by 38.2% retracement of 114.84 to 125.80 at 121.61 to bring rise resumption. We're staying mildly bullish in the cross. And, break of 126.09 key resistance will extend the whole rebound from 109.03 to 100% projection of 109.03 to 124.08 from 114.84 at 129.89. Nonetheless, firm break of 121.61 will dampen our bullish view and bring deeper fall to 61.8% retracement at 119.02.

In the bigger picture, focus is staying on 126.09 support turned resistance. Decisive break there will confirm completion of the down trend from 149.76. And in such case, rise from 109.20 is at the same degree and should target 141.04 resistance and above. Meanwhile, rejection from 126.09 and break of 114.84 will extend the fall from 149.76 through 109.20 low.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4968; (P) 1.5077; (R1) 1.5137; More...

Intraday bias in EUR/AUD stays neutral for consolidation below 1.5226 temporary top. Further rise is still expected 1.4927 support holds. Above 1.5226 will extend the rally from 1.3624 to next medium term fibonacci level at 1.5455. However, break of 1.4927 will indicate short term topping on bearish divergence condition in 4 hour MACD. In such case, intraday bias will be turned back to the downside for 1.4669 support next.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction should be completed at 1.3624 after defending 1.3671 key support. Rise from 1.3642 is now expected to target 61.8% retracement of 1.6587 to 1.3624 at 1.5455. Sustained break there will pave the way to retest 1.6587. In any case, outlook will now stay cautiously bullish as long as 1.4669 support holds.

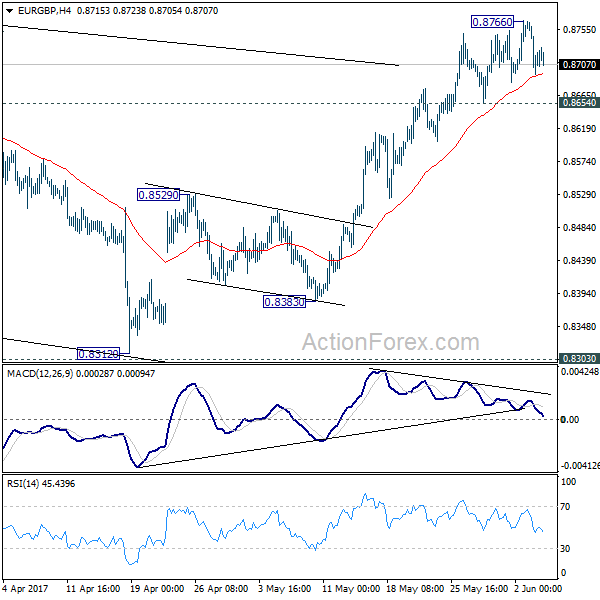

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8687; (P) 0.8727; (R1) 0.8761; More...

Intraday bias in EUR/GBP is turned neutral with a temporary top in place at 0.8766. But further rally is still expected as long as 0.8654 support holds. Above 0.8766 will target 0.8786 resistance and then 0.8851. Decisive break of 0.8851 will pave the way to retest 0.9304 high. However, break of 0.8654 will indicate short term topping on bearish divergence condition in 4 hour MACD. In such case, intraday bias will be turned back to the downside for 55 day EMA (now at 0.8579).

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. The leg from 0.9304 should have completed after testing 0.8332 structural support. But it's too early to say that larger rise from 0.6935 is resuming. Rejection from 0.9304 will extend the consolidation with another falling leg. Meanwhile, firm break of 0.9304 will target 0.9799 (2008 high). In case of another decline, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound.

Market Update – Asian Session: RBA Holds Rates With A Neutral Policy Statement Despite Soft Q1 Current Account

US Session Highlights

(US) MAY FINAL MARKIT SERVICES PMI: 53.6 V 54.0 PRELIM

(US) MAY ISM NON-MANUFACTURING COMPOSITE: 56.9 V 57.1E

(US) APR FINAL DURABLE GOODS ORDERS: -0.8% V -0.5%E; DURABLES EX TRANSPORTATION: -0.5% V -0.4% PRELIM

(US) APR FACTORY ORDERS: -0.2% V -0.2%E

(US) Senate Minority Leader Schumer: ready to work with Pres Trump on a real infrastructure plan

Stock rally slowed to a grind with most indices slightly lower on the day. Concerns over the rift between Saudi Arabia and allies with Qatar weighed on oil. Despite lower crude prices and subdued buying power, the worst performing S&P sectors YTD, Energy and Financials, managed to tick up today, by 0.2% each.

US markets on close: Dow -0.1%, S&P500 -0.1%, Nasdaq -0.2%

Best Sector in S&P500: Energy

Worst Sector in S&P500: Utilities

Biggest gainers: KORS +4.4%; NVDA +3.0%; TSO +2.8%

Biggest losers: INCY -5.7%; MNK -5.1%; BMY -4.8%

At the close: VIX 10.1 (+0.3pts); Treasuries: 2-yr 1.30% (+1bp), 10-yr 2.18% (+2bp), 30-yr 2.84% (+3bps)

US movers afterhours

THO: Reports Q3 $2.11 v $1.87e, R$2.02B v $1.96Be; affirms FY17 capex $130M; +11.5% afterhours

COVS: Agrees to be acquired at $2.45/shr by OpenText for $103M; +9.1% afterhours

ACOR: CVT-301 Phase 3 Data showed significantly improved Motor Function during OFF Periods in Parkinson’s Disease; plans to file NDA in U.S. by end of 2Q17; +9.8% afterhours

SIG: COO Bryan Morgan resigns due to violations of company policy; -0.8% afterhours

CASY: Reports Q4 $0.76 v $0.89e, R$1.85B v $1.87Be; Guides FY18 SS fuel gallons sold +1-2%, SS grocery/merchandise sales +2-4% y/y, operating expenses +9-11% y/y; -3.9% afterhours

Politics

(US) White House wants debt ceiling to be raised by August Congressional recess - press

(US) White House nominates Joseph Otting as the US Comptroller of Currency (OCC) - financial press

(UK) According to Survation Poll taken June 2-3, support for Conservatives Party at 41.5% vs 40.4% for Labour – US financial press

Key economic data

(AU) RESERVE BANK OF AUSTRALIA (RBA) LEAVES CASH RATE TARGET UNCHANGED AT 1.50% (AS EXPECTED)

(AU) AUSTRALIA Q1 CURRENT ACCOUNT BALANCE (A$): -3.1B V -0.5BE; NET EXPORTS OF GDP: -0.7% V -0.4%E

(JP) JAPAN APR LABOR CASH EARNINGS Y/Y: 0.5% V 0.3%E (4-month high)

Asia Session Notable Observations

Asian markets are mixed in the wake of modest declines on Wall St where cash indices fell after two days of large gains. Despite the miss in US economic data and political risk of former FBI director Comey testinony this week, expectations for more than one rate hike by the FOMC are back above 50%, with a tightening this month now seen as nearly 95%-certainty. Risk aversion picked up slightly in the Asia session, as 10-year Treasury yield fell 2bps, USD/JPY plunged over 70pips below 109.70, and US equity futures turned from slightly gains to losses.

Australia economic data and monetary policy were in focus in today's session. Q1 Current Account saw a much bigger drop in Exports as pct of GDP at -0.7%, and analysts are speculating this may result in an annualized q/q contraction in tomorrow's GDP report. RBA stood pat at 1.5% and was also more Neutral than expected, acknowledging the expected slowdown in Q1 GDP but maintaining view of 3% long run growth forecast. RBA also added that business conditions have improved and capacity utilisation has increased.

In China, PBoC skipped its regular daily reverse repo ops but injected CNY498B in medium-term lending facility (MLF) operations. Yuan fix was also set marginally stronger, with the Offshore rate remaining at 6.77.

Speakers and Press

China

(CN) Muddy Waters' Carson Block: China is a massive asset bubble and credit bubble; blow up could start in shadow banking and wealth management

(CN) Analysts expect liquidity conditions to tighten in June amid seasonal factors; Unlikely it will lead to full-scale liquidity crunch - Chinese press

(CN) China Foreign Min Wang Yi announced an agreement had been reached between China and ASEAN countries on a first draft of a framework for a Code of Conduct (COC) for the South

China Sea - press

(CN) China Information Daily: China should continue to push for normalizing IPOs

Japan

(JP) Japan Fin Min Aso: Importance of lowering Japan debt-to-GDP ratio is clear - press

Australia/New Zealand

(AU) AMP's Oliver: Overall picture for Australia economy is subpar growth running well below that assumed by RBA and in the budget - SMH

(AU) Australia Fair Works Council (FWC) to raise Minimum Wage by 3.3%/A$22.20/week for a total of A$694.90/week - press

(AU) ANZ CEO: Australia house prices are very inflated; There is a very low probability of a housing crash - press

(NZ) New Zealand real estate agency Barfoot & Thompson: Auckland region May property sales were 886 units, up from 664 m/m but down from 1,306 y/y; lowest number of sales in the month of May since 2010 - NZ press

Korea

(KR) Bank of Korea (BOK): THAAD dispute may impact talks on Korea-China currency swap - Korean press

(KR) US Nuclear Submarine USS Cheyenne has arrived in Busan, South Korea - Korean press

Asian Equity Indices/Futures (00:15ET)

Nikkei -0.6%, Hang Seng +0.4%, Shanghai Composite -0.2%, ASX200 -1.2%, Kospi closed

Equity Futures: S&P500 -0.1%; Nasdaq -0.1%, Dax -0.3%, FTSE100 -0.3%

FX ranges/Commodities/Fixed Income (00:15ET)

EUR 1.1255-1.1275; JPY 109.75-110.50; AUD 0.7455-0.7490; NZD 0.7125-0.7160

Aug Gold +0.4% at 1,287/oz; July Crude Oil -0.4% at $47.19/brl; July Copper -0.1% at $2.56/lb

iShares Silver Trust ETF daily holdings fall to 10,562 tonnes from 10,601 tonnes prior; 4th straight decline

(CN) PBOC SETS YUAN MID POINT AT 6.7934 V 6.7935 PRIOR; 5th straight firmer Yuan fix; Strongest Yuan fix since Nov 10th

(CN) PBOC skips open market operations v CNY70B prior injected (first skip since May 28th)

(CN) PBOC conducts CNY498B in medium-term lending facility (MLF) operations; Offers 1-year MLF at 3.2% v 3.2% prior

(JP) Japan MoF sells ¥723B v ¥0.8T offered in 30-year 0.8% (0.8% prior) JGBs; Avg yield: 0.817% v 0.819% prior; bid to cover: 3.63x (highest since Oct 2016) v 3.35x prior

Asia equities notable movers

Australia

Musgrave (MGV) +1.4%; Reports high grade gold intersected near surface at Lena

BHP (BHP) -1.3%; Tribeca Partners said to propose some candidates to replace certain BHP directors

Sirtex (SRX) -1.5%; Announces primary endpoint of combined SIRFLOX/FOXFIRE study was not met

Spark Infrastructure (SKI) -2.0%; Cut at Goldman Sachs

APA Group (APA) -4.5%; Cut at Goldman Sachs

Japan

Toshiba (6502) +3.5%; Western Digital reportedly willing to compromise in order to get deal on Toshiba chip unit - Nikkei

Hong Kong

Evergrade (3333) +6.2%; To redeem all of its perpetual bonds by the end of June, ahead of plan

Beijing Capital (2868) +3.0%; May contracted sales

China Aoyuan Property Group (3883) +1.3%; May contracted sales

Shimao Property (813) +5.9; May contracted sales

EURUSD Looks Bullish, Counting Down To ‘Super Thursday’

The US dollar remained rather subdued yesterday and is seen breaking past late May lows. The weakness in the greenback comes amid a soft non-manufacturing PMI report from ISM. The index fell to 56.9 in May, missing estimates of 57.1 and weaker than April's headline print. Factory orders were also seen contracting 0.2% after rising 1.0% in the previous month.

Among commodities, oil prices took a hit after Saudi Arabia, Egypt and Bahrain severed diplomatic ties with Qatar. The nations accused Qatar of supporting terrorist groups. Oil prices initially rose to session highs of $48.40 before giving up the gains and settling at $47.39.

Looking ahead, the RBA's interest rate decision saw no major changes to monetary policy. In the eurozone, the Sentix investor confidence is expected to rise modestly to 27.6, up from 27.4 previously while the Ivey PMI from Canada is expected to show a headline print of 62.0, slightly lower than 62.4.

EURUSD intraday analysis

EURUSD (1.1266): EUR/USD formed an inside bar with price action staying firm within Friday's range high and low. Price action briefly tested the support level at 1.1245 before bouncing off to close above the support. We expect that EURUSD will now continue to push higher especially with the inverse head and shoulders pattern that has emerged at the top. This suggests a continuation to the upside with the next target at 1.1300 followed by 1.1383. The bias changes if EURUSD slips below 1.1245 support level in which case the bullish inverse head and shoulders pattern on the 4-hour chart will be invalidated.

GBPUSD intraday analysis

GBPUSD (1.2977): GBP/USD continues to maintain a modest uptrend, but theprice is seen testing 1.1293 resistance level. A reversal here could see a potential decline in the near term. On the 4-hour chart, there is evidence of a head and shoulders pattern that is shaping up and should be confirmed on a reversal around 1.1293. This pattern could, however, be invalidated if GBPUSD pushes towards 1.3000. To the downside, expect the price level at 1.2800 likely to offer some support but a break down below this level will trigger a move to 1.2600.

XAUUSD intraday analysis

XAUUSD (1284.55): Gold prices are continuing to push higher following the breakout at 1274.00 resistance level. Price action is seen currently filling the gap from April 21 at 1284.87. In the near term, we can expect to see a short term decline back to 1274.00 where support can be established at the previous resistance level. This will keep the bias to the upside with the potential for gold prices to reach as high as 1300.00. To the downside, a break down below 1274.00 will, however, keep gold prices range bound with the bias turning lower below 1263.00.