Sample Category Title

Is The Bank Of Canada Going To Shift To A Dovish Bias?

Today, all eyes will be on the Bank of Canada rate decision. The forecast is for the Bank to remain on hold once again. Policymakers maintained a neutral to dovish tone the last time they met, balancing every upbeat comment about the economy with a worried follow-up remark. The key message we got was that economic data are improving, but the Bank thinks it is too soon to materially alter its concerned stance, mainly due to uncertainties related to the outlook for trade.

Indeed, BoC policymakers now probably feel vindicated about their cautious view, considering that shortly after that policy meeting, the US imposed tariffs on Canada. Given also that some recent economic data have been soft, with the core CPI rate falling further in April and February's GDP stagnating, we consider it likely that the BoC will maintain, if not amplify further, its concerned message. Something like that could reverse some of CAD's recent gains. However, we should note that the currency's forthcoming direction may be decided to a large extent by the outcome of the OPEC & non-OPEC meeting tomorrow as well, considering Canada's heavy reliance on oil exports.

USD/CAD traded somewhat lower yesterday during the European morning, but the decline was halted near the 1.3460 (S2) support level and the rate then rebounded to break above the resistance (now turned into support) barrier of 1.3510 (S1). In case of a worried tone today by the BoC, the current rebound could continue and aim for the 1.3570 (R1) resistance territory. If the bulls manage to overcome that level, they could initially aim for the key hurdle of 1.3600 (R2).

FOMC minutes: Is a June rate hike on the cards?

In the US, the Fed will release the minutes from its May policy meeting, where the Committee kept its policy unchanged and offered very few hints regarding the timing of the next rate hike. The most noteworthy point in the statement was that policymakers view the slowdown in Q1 GDP as transitory, implying this softness will not deter them from hiking rates again in the near-term should growth rebound in Q2. Besides that point, the statement was more or less a reiteration of the previous one and as such, we expect investors to scan the minutes for any clear clues as to whether the next hike is likely to come as early as June.

At the time of writing, the probability for a June hike rests at 83%. If the minutes confirm the Bank is likely to act again as early as June, that probability could rise further and the dollar may gain somewhat. Having said that though, given the elevated expectations for a June action, any signs in the minutes that the Fed may not act as the market currently expects could generate a notable negative reaction in USD, in our view.

USD/JPY traded higher yesterday, breaking above the resistance (now turned into support) barrier of 111.50 (S1). Should the FOMC minutes confirm the Bank is likely to raise rates again in June, we could see the rate move higher and challenge the 112.35 (R1) resistance zone. On the other hand, any cautious signals indicating that a June action is not as likely as market pricing suggests could cause the bears to retake control and push the battle notably lower. A decisive break below the 111.50 (S1) support could initially aim for 111.00 (S2).

As for the rest of today's highlights:

During the European morning, the economic calendar is relatively light. The only noteworthy indicator we get is Norway's oil investment survey for Q2, though no forecast is available.

As for the US economic indicators, we get existing home sales for April.

We have two speakers on the agenda: ECB President Mario Draghi and ECB Executive Board Member Peter Praet. We think that market participants are likely to focus primarily on Draghi's comments, amid heightened speculation regarding the prospect of a more optimistic tone by the ECB at one of its upcoming meetings.

USD/CAD

Support: 1.3510 (S1), 1.3460 (S2), 1.3410 (S3)

Resistance: 1.3570 (R1), 1.3600 (R2), 1.3640 (R3)

USD/JPY

Support: 111.50 (S1), 111.00 (S2), 110.50 (S3)

Resistance: 112.35 (R1), 113.10 (R2), 113.80 (R3)

German Investor Morale Improves More Than Expected In May

'Today's strong German data add to the evidence that, not only the German economy, but the entire euro zone economy could become the positive growth surprise of 2017.' - Carsten Brzeski, ING

The mood of German investors improved markedly in May, official data showed on Tuesday. The Munich-based Ifo Institute for Economic Research reported that its Business Climate Index climbed to 114.6 points in the reported month, following April's 113.0 and surpassing analysts' expectations for an increase to 113.1. That marked the strongest reading since 1991. May's jump was mainly driven by Emmanuel Macron's victory in the French 2017 Presidential Election, which boosted confidence across the Euro zone. Taking into account the stronger-than-expected Ifo Index and other quite optimistic economic data, the German economy is set to hit a 0.6% growth rate in the second quarter. The Ifo Institute's economist Klaus Wohlrabe noted that Brexit and the US President Donald Trump's policies had not had an impact on the German economy yet. The largest sentiment improvement was seen in the manufacturing sector. Strong economic growth is expected to provide a significant support to the Chancellor Angela Merkel's Party ahead of the September General Election.

Canadian Wholesale Sales Rebound But Less Than Expected In March

'We still have ground to recover. I think there's more room to grow before we're going to peak out.' - Todd Hirsch, ATB Financial

Canadian wholesale sales rose less than expected in the third month of the year, data revealed on Tuesday. Statistics Canada reported that the value of Canadian wholesale trade climbed 0.9% in March, surpassing the C$60B mark for the first time, up from the preceding month's upwardly revised gain of just 0.3%. Nevertheless, March's figure missed analysts' expectations, as they anticipated an increase of 1.1% during the reported month. In volume terms, sales were up 0.6% in March. Gains were registered in four out of seven subsectors, representing 60% of the wholesale trade total. Sales of building materials and supplies surged 3.9%, boosted by higher demand for lumber, millwork and hardware as well as metal services. In the meantime, sales of beverages and tobacco increased 1.1% between February and March. However, two biggest subsectors posted unexpected drops. Sales of machinery and supplies fell 0.5%, whereas sales of motor vehicles and parts plunged 0.2% in March. Overall, wholesale sales were up 3.6% year-over-year in the Q2, the biggest quarterly gain since the second quarter of 2008.

US New Home Sales Drop 11.4% In April

'Demand for housing remains strong and the usual list of support factors hasn't changed, with the key items being job growth and wage gains.' - Jennifer Lee, BMO Capital Markets

New home sales in the United States dropped more than expected last month, probably amid weaker demand. The Department of Commerce reported on Tuesday that sales of new houses dropped 11.4% to a seasonally adjusted annualised pace of 569K units in April, following the prior month's upwardly revised pace of 642K units, the highest since October 2007, and falling behind expectations for a decrease to a 611K-unit pace. On an annual basis, new home sales were up 0.5% in April. The average selling price dropped to $309.2K in April from $318.7K seen in the preceding month. Despite April's unexpected drop, analysts suggested that the housing market maintained its momentum and would continue growing in the upcoming months, supported by low mortgage rates. New home sales plunged in all four regions; however, the largest drop of 26.3% was registered in the West. The inventory level rose 1.5% to 268K units last month, the highest since July 2009. AT the past month's sales pace it would likely take 5.7 months to sell all houses available on the market.

EUR/USD Analysis: Retreats Below Significant Resistance

'The euro's 7 percent gain this year means it's the best-performing currency against the dollar among the Group of 10 industrialized nations. History suggests its advance may carry on.' – Mark Gilbert, Bloomberg

Pair's Outlook

After a retreat back below the 1.12 mark during the second half of Tuesday's trading session the EUR/USD currency exchange rate has retreated below a significant resistance. On Wednesday early morning the pair was flat below the combined resistance of the monthly R2 at 1.1187 and the 61.80% Fibonacci retracement level at the 1.1190 mark. As the pair remains flat, it can be clear that clues are being expected to reveal the future short term direction. Two possibilities exist. In the case of a breaking of the resistance, the 1.13 mark will be in reach. On the other hand a decline to the weekly PP at 1.1114 might occur.

Traders' Sentiment

SWFX traders are clearly bearish in regard to the pair, as 59% of open positions are short, and 53% of trader set up orders are to sell.

GBP/USD Analysis: Another Drop Expected

'There is still scope for further upside in the near term. The long-term downtrend currently stands at approximately 1.35 and it is still possible that we could see that tested before the dollar begins to reassert itself.' – Charles Stanley (based on PoundSterlingLive)

Pair's Outlook

The GBP/USD currency pair weakened on Tuesday, resulting in the consolidation trend's preservation. Consequently, the British Pound should edge lower for another day, with the 1.29 major level likely to be the bottom, despite the 20-day SMA and the weekly S1 forming support around 1.2930. On a slightly larger scale the given pair should be unable to drop under 1.2830, where the consolidation trend's lower border, the lower Bollinger band, the weekly S2 and the wedge's support line all form a strong demand cluster. This point is also likely to be able to shift polarity and spark sufficient GBP-buying for a solid surge above 1.30, eventually.

Traders' Sentiment

Traders retain a neutral outlook towards the Sterling, with 52% of all open positions being short. Still 56% of all orders are to buy the Pound.

USD/JPY Analysis: Keeps Edging Higher

'The rise in Treasury yields is supporting the dollar. It appears that speculative buying of Treasuries has run its course, with Trump concerns and geopolitical risks no longer fresh news.' – Daiwa Securities (based on Reuters)

Pair's Outlook

The USD/JPY pair edged higher yesterday, but managed to overperform, as it breached the immediate resistance area. As a result, the US Dollar is now likely to keep appreciating against the Yen, even though technical indicators are unable to confirm that. The nearest area to limit the gains now rests around 112.60, represented by the monthly R1, the 20 and the 100-day SMAs, but the Buck could experience trouble reaching that far up. Technical indicators in the daily timeframe, however, are unable to confirm the possibility of the positive outcome, but in the longer timeframes they do suggest the Greenback is to keep climbing higher.

Traders' Sentiment

There are 55% of traders holding short positions (previously 60%), while the share of buy orders remains unchanged at 55%.

Gold Analysis: Remains Above 1,250 Mark

'Gold could face more pain if tonight's FOMC (Federal Open Market Committee) minutes shows that the Fed is on course for two to three more rate hikes this year.' – Jeffrey Halley, OANDA (based on Reuters)

Pair's Outlook

The yellow metal's price remains above the 1,250 mark, as the strong support cluster just below that level holds its ground. However, fundamental shifts in the market are possible, as US monetary policy makers will affect the strength of the bullion from the US Dollar's side. The FOMC meeting minutes will reveal, how many and what kind of Federal Funds Rate decisions might take place in the future. Although, from a technical perspective the surge of the bullion should continue, as the SMAs should push it higher soon.

Traders' Sentiment

SWFX market sentiment remains almost neutral, as 52% of open positions are short. However, 67% of trader set up orders are to buy the bullion.

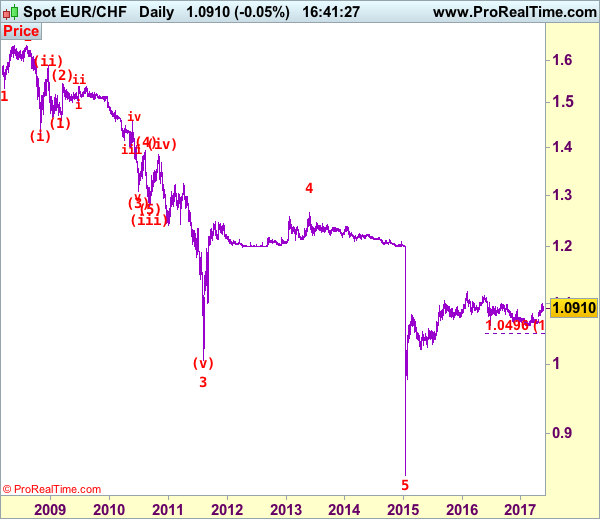

EUR/CHF Elliott Wave Analysis

EUR/CHF : 1.0947

EUR/CHF: Major wave 5 trough ended at 0.8426 and correction has commenced from there for subsequent gain towards 1.1400-1.1500.

As the single currency has retreated after meeting resistance at 1.0988 earlier this month, retaining our view that consolidation below this level would be seen, however, reckon downside would be limited to 1.0860-65 and bring another rise later, above said resistance at 1.0988 would confirm recent rise has resumed and extend further gain to another previous resistance at 1.1001, break there would extend the rise from 1.0622 low (2016 low) to 1.1018, then 1.1050 but reckon resistance at 1.1107 would limit upside and price should falter well below 2016 high at 1.1129.

To recap our preferred count, the decline from 1.6828 (end wave (B)) is labeled as the beginning of wave (C) which should unfold as an impulsive move with 1: 1.5326, 2: 1.6377 and wave 3 is sub-divided into (i): 1.4300, (ii): 1.5880 and wave (iii) is still unfolding with (1): 1.4577, (2): 1.5448 and wave (3) is an extended 3rd with i: 1.5006, ii: 1.5383, wave iii: 1.3073, then wave iv ended at 1.3925 and wave v at 1.3073, wave (4) ended at 1.3925 and wave (5) has ended at 1.2765 which also marked the low of wave (iii) and wave (iv) has ended at 1.3835 and wave (v) as well as larger degree wave 3 has ended at 1.0075. The selloff from 1.2650 signals wave 4 has ended there and we are taking a view that the wave 5 could also have ended 0.8426, hence consolidation is seen with mild upside bias for rebound to 1.1000 first, then towards 1.1400.

On the downside, expect pullback to be limited to 1.0860-65 and bring another rise later. Below 1.0825-30 would defer and suggest top is possibly formed, bring weakness to said support at 1.0792 but only a daily close below there would add credence to this view, then further fall to 1.0780 and possibly previous minor resistance at 1.0720 would follow. Looking ahead, only a drop below 1.0720 would suggest top is formed instead, risk weakness towards said support at 1.0656 first.

Recommendation: Hold long entered at 1.0905 for 1.1105 with stop below 1.0805.

The long-term downtrend started from 1.9626 (Apr 1985) to 1.4166 (Sep 1995) is treated as wave (A) with A:1.6285 (Dec 1987), B: 1.9342 (May 1992) and C: 1.4166, then wave (B) ended at 1.6828 with A: 1.7147 (Feb 1997), B: 1.4398 (Sep 2001), C: 1.6828 (Nov 2007), therefore, wave (C) is now in progress with the breakdown indicated as above. This wave (C) already met indicated downside target at 1.1455/60 and 1.1300, it could have ended at 0.8426, consolidation with mild upside bias is seen for gain to 1.1000 and later towards 1.2000.

Technical Outlook: USDJPY – Extension Above Daily Cloud Shows Hesitation At 112.00 Zone

The pair emerges above daily cloud on Wednesday, on extension of Tuesday's strong rally that left long-tailed and long-body daily bullish candle.

Today's break above 111.81 pivot (daily cloud top / Fibo 38.2% of 114.36/110.23) was bullish signal but the rally was so far capped by falling daily Tenkan-sen line (112.05), showing hesitation at psychological 112.00 barrier.

In addition, a plethora of barriers that lies above and consisting of 10SMA (112.26), 20SMA (112.42) and 100SMA (112.58) may limit recovery rally.

Daily studies are mixed and see minimum requirement on close above daily cloud to signal further upside. However, lift above daily MA barriers is needed to confirm bullish continuation.

Otherwise, risk of recovery stall and fresh weakness could be expected on early upside rejection.

Release of US data and FOMC minutes, due later today would give more clues about near-term direction.

Res: 112.05, 112.26, 112.42, 112.58

Sup: 111.61, 111.37, 110.74, 110.50