Sample Category Title

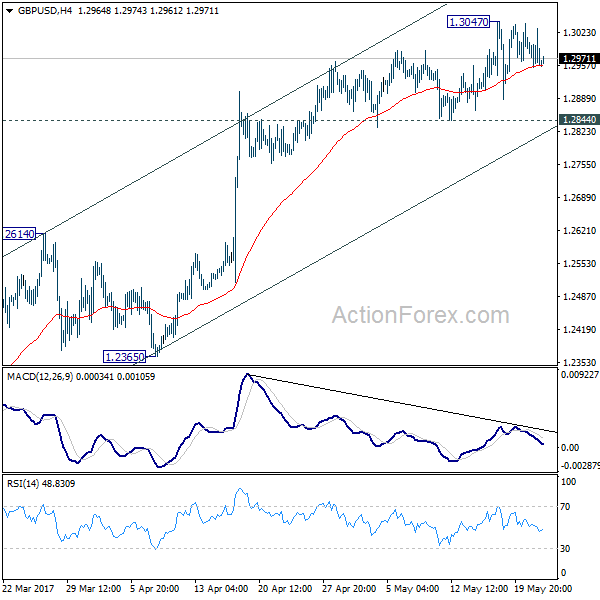

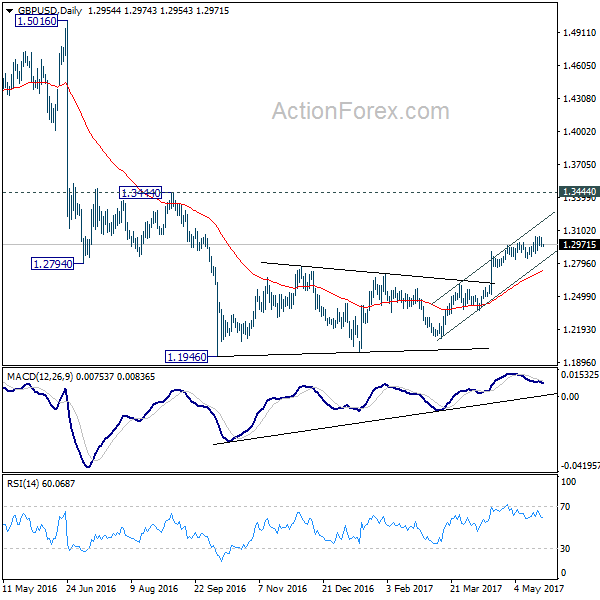

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2931; (P) 1.2982; (R1) 1.3012; More...

Intraday bias in GBP/USD remains neutral as consolidation from 1.3047 continues. As long as 1.2844 minor support holds, further rise remains mildly in favor. Nonetheless, as we are still viewing price actions from 1.1946 as a corrective move, we'd expect upside to be limited below 1.3444 resistance to bring near term reversal. On the downside, break of 1.2844 will indicate short term topping and turn bias back to the downside for 1.2614 resistance turned support first.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There are signs of reversal, like breaking of 55 week EMA, weekly MACD turned positive, and monthly MACD crossed above signal line. But still, break of 1.3444 resistance is need to confirm medium term bottoming. Otherwise, outlook will remains bearish for extend the down trend through 1.1946 low.

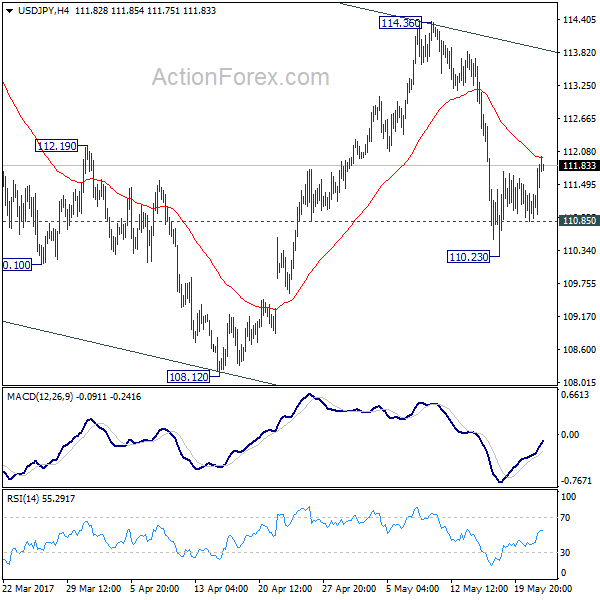

USD/JPY Daily Outlook

Daily Pivots: (S1) 111.14; (P) 111.49; (R1) 112.13; More...

USD/JPY's rebound from 110.23 extended higher today and is pressing 4 hour 55 EMA. There is no change in the view that rise from 110.23 is a corrective move. Below 110.85 minor support will turn bias to the downside to extend the fall from 114.36 to 108.12 low. Break there will resume the whole decline from 118.65. In that case, we'll look for bottoming signal again at 61.8% retracement of 98.97 to 118.65 at 106.48.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9719; (P) 0.9741; (R1) 0.9780; More.....

A temporary low is in place at 0.9691 in USD/CHF and intraday bias is turned neutral first. Some consolidations would be seen but upside of recovery is expected to be limited by 0.9858 support turned resistance to bring another decline. Whole fall from 1.0342 is still in progress and below 0.9691 will target 100% projection of 1.0342 to 0.9860 from 1.0099 at 0.9617. We'll start to look for reversal signal below there.

In the bigger picture, USD/CHF is bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level.

Dollar Recovered as Markets Firmed Up June Fed Hike Expectations, FOMC Minutes and BoC Awaited

US markets closed mildly higher overnight as investors were relieved that US President Donald Trump's first budget plan contained no surprise. DJIA closed up 43.08 pts, or 0.21% at 20937.91. S&P 500 gained 4.4 pts or 0.18% to close at 2398.42. Nikkei follows in Asian session and is trading up 100 pts at the time of writing. US 10 year yield also ended up 0.031 at 2.285. Dollar recovered as markets firmed up their expectation of a June Fed hike. Fed fund futures are pricing in 83.1% chance of that. In other markets, gold dips mildly but is holding above 1250 handle for the moment. WTI crude oil's recent surge is still in progress and is holding above 51.50. Focus will turn to FOMC minutes and BoC rate decision today.

Philadelphia Fed Harker: June Hike is a distinct possibility

Philadelphia Fed President Patrick Harker said that June hike is a "distinct possibility ... quite possible". And he also noted that "a month or two in the wrong direction isn't enough to make me lose faith." Harker reiterated his support for two more rate hike this years. Regarding Fed's plan to shrink its balance sheet, he pointed out the two questions of "when" and "how". For the "when" part, Harker didn't give a specific date but he did think "we'll start sometime this year". And, for the "how" part", he said it will be "predictable, slow and as boring as possible".

Minneapolis Fed President Neel Kashkari expressed some of his concerns on the economy. He noted that the US is "closer" to full employment but he cautioned that "we don't know how far the shore is". Also, he said that "right now inflation is going in the wrong direction". Kashkari is a known dove who was the sole dissenter against Fed's rate hike back in March.

BoC to stand pat today

BoC rate decision will be a focus today too and the central bank is widely expected to keep interest rate unchanged at 0.50%. Recent economic data from Canada have been solid with job gains for six straight month. Consumer spending grew at healthy pace with support from rising home values. But BoC Governor Stephen Poloz has been reluctant to turn more upbeat on the economy and maintained that it's still playing catch up to the US.

UK raised threat level to "critical"

In UK, Prime Minister Theresa May raised the nation's threat level and warned that another terrorist attack "may be imminent". Alert level was lifted from "severe" to its highest "critical". May announced the mover after an emergency meeting of the security cabinet, with conclusion that the attacker of Monday's bombing in Manchester could be part of a larger network. And May warned that the prospect of of wider plot was "a possibility we cannot ignore".

On the data front...

Released in Asian session today, New Zealand trade surplus widened to NZD 578m in April, larger than expectation of NZD 267m. That's also the larger trade surplus since 2015. Exports jumped 9.8% yoy to NZD 4.8b. Imports rose 4.9% yoy to NZD 4.2b. Australia Westpac leading index dropped -0.1% mom in April. Looking ahead, German Gfk consumer sentiment, US house price index and existing home sales will be featured.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9719; (P) 0.9741; (R1) 0.9780; More.....

A temporary low is in place at 0.9691 in USD/CHF and intraday bias is turned neutral first. Some consolidations would be seen but upside of recovery is expected to be limited by 0.9858 support turned resistance to bring another decline. Whole fall from 1.0342 is still in progress and below 0.9691 will target 100% projection of 1.0342 to 0.9860 from 1.0099 at 0.9617. We'll start to look for reversal signal below there.

In the bigger picture, USD/CHF is bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Apr | 578M | 267M | 332M | 277M |

| 00:30 | AUD | Westpac Leading Index M/M Apr | -0.10% | 0.10% | ||

| 06:00 | EUR | German GfK Consumer Sentiment Jun | 10.2 | 10.2 | ||

| 13:00 | USD | House Price Index M/M Mar | 0.60% | 0.80% | ||

| 14:00 | CAD | BoC Rate Decision | 0.50% | 0.50% | ||

| 14:00 | USD | Existing Home Sales Apr | 5.65M | 5.71M | ||

| 14:30 | USD | Crude Oil Inventories | -1.8M | |||

| 18:00 | USD | FOMC Minutes May 3 Meeting |

USD/CAD Canadian Dollar Lower After USD Rebound Ahead Of BoC

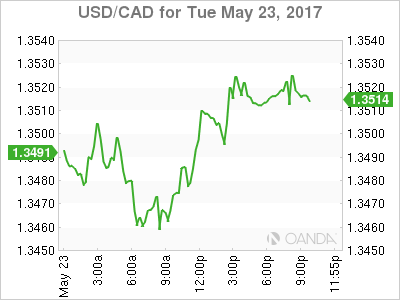

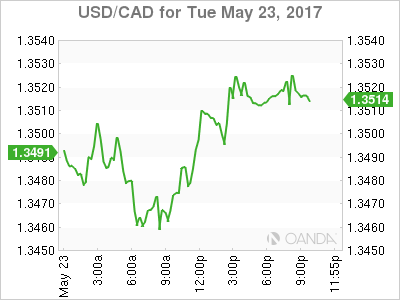

The Canadian dollar is trading lower at 1.3523 after the USD erased all loses versus the loonie on Tuesday. The greenback regained traction ahead of the release of the U.S. Federal Reserve minutes from the monetary policy meeting earlier in May. The Fed is heavily anticipated to hike rates in the next meeting with the market searching for insights on the document released on Wednesday.

Building materials and supplies drove Canadian wholesale trade 0.9 percent higher in March. There sales figures were the lone economic data release on Tuesday following the Victory day holiday. Investors will be awaiting the rate decision by the Bank of Canada (BoC). The Canadian central bank will release its rate statement on Wednesday, May 24 at 10:00 am EDT. The BoC is heavily expected to hold rates unchanged despite growing pressure from a hot house market in major cities. The CAD has been caught between a falling loonie and the more aggressive tone of the US regarding the NAFTA renegotiation. The US has set in motion the process needed to renegotiate the deal in late August. BoC Governor Stephen Poloz is expected to address the household debt and real estate market with mentions about the upcoming trade negotiations.

The release of weekly US oil inventories at 10:30 am EDT will impact the USD/CAD pair given the high correlation between crude prices and the loonie. The tone of the rhetoric from the Canadian central bank and the actual change in the American oil inventory will be a preamble for the release of the Fed minutes at 2:00 pm EDT. The Fed did not update its benchmark rate from its 75 to 100 basis points range and offered little clues on the brief statement released after the FOMC meeting ended. The notes from the monetary policy meeting will shed some light on the different opinions from members on the current rate hike path and a long shot but also the possibility of a time frame for its plans to reduce its massive balance sheet.

The USD/CAD gained 0.105 percent in the last 24 hours. The currency pair is trading at 1.3523 after the USD staged a comeback in the North American trading session. The pair went from a daily low of 1.3456 and quickly went above the 1.35 price level to near daily highs where it is currently trading. Oil prices boosted the loonie on Monday and early trading Tuesday coupled with a strong wholesale trade data in Canada but as traders booked their profits on a weak USD and repositioned for a slightly hawkish Fed minutes the greenback bounced back.

The Bank of Canada is forecasted to hold as the economy is still struggling to regain the momentum is lost with the drop in oil prices two years ago. With the Fed all set to hike rates in June, this will widen the interest rate gap between the two economies. Trade disputes and the more aggressive tactics by the US to solve them are also a concern as Canada exports two-thirds of exports to its southern neighbour.

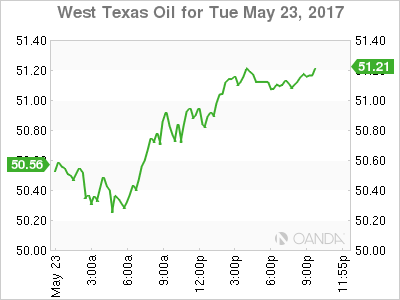

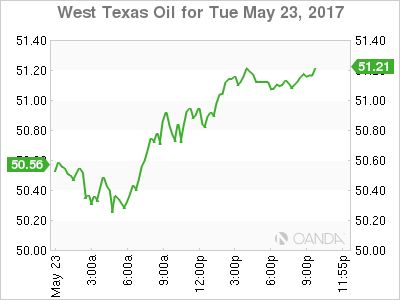

The price of oil gained 0.926 percent on Tuesday. The West Texas Intermediate is trading at $51.14 ahead of Wednesday's release of the weekly US crude inventories. Another drawdown is awaited, marking 7 contractions in a row in US inventories. The US President Donald Trump proposed to sell half of the strategic oil reserve starting in October. Ironically the fund was started in 1975 to avoid a repeat of gas price surges during the Arab oil embargo. The Organization of the Petroleum Exporting Countries (OPEC) is now once again cutting production, but even with all the members and other influential producers such as Russia they can only keep the price stable. US production has grown to the point where it could justify the sale of the emergency stocks stored in Louisiana and Texas. Although it is hard for this to be approved by congress, specially now, but it does send a signal to OPEC ahead of Thursday's meeting on their cut production agreement extension.

Market events to watch this week:

Wednesday, May 24

- 8:45am EUR ECB President Draghi Speaks

- 10:00 am CAD BOC Rate Statement

- 10:00 am CAD Overnight Rate

- 10:30 am USD Crude Oil Inventories

- 2:00 pm USD FOMC Meeting Minutes

- 10:00pm NZD Annual Budget Release

Thursday, May 25

- 4:30 am GBP Second Estimate GDP q/q

- All Day ALL OPEC Meetings

- 8:30 am USD Unemployment Claims

Friday, May 26

- 8:30 am USD Core Durable Goods Orders m/m

- 8:30 am USD Prelim GDP q/q

Dollar Rebounds Awaiting Fed Minutes

US oil inventories, Bank of Canada and FOMC minutes to drive markets

The US dollar is higher against most major pairs after staging a recovery ahead of the release of the Federal Open Market Committee (FOMC) May meeting minutes on Wednesday, May 24 at 2:00 pm. The Fed hosted no press conference in May, leaving the market to wait for the minutes to gather insights into the views of the central bank on the path of rates for the reminder of the year. The CME FedWatch tool is showing a 83.1 percent probability of a rate hike based on futures fed funds prices. Fed speakers have issued mix rhetoric, but so far the rate hike remains firmly on the table for the meeting to be held on June 13 and 14.

The Bank of Canada (BoC) will release its rate statement on Wednesday, May 24 at 10:00 am EDT. The central bank is heavily expected to hold rates unchanged despite growing pressure from a heating up house market in major cities. The CAD has been caught between a falling loonie and the more aggressive tone of the US regarding the NAFTA renegotiation. The US has set in motion the process needed to renegotiate the deal in late August. BoC Governor Stephen Poloz is expected to address the household debt and real estate market with mentions about the upcoming trade negotiations.

US weekly oil inventories will be release at 10:30 am EDT by the Energy Information Administration (EIA). The forecast calls for a 2.4 million barrel drawdown to make it 7 contractions in a row. Oil prices have been caught between the efforts of the Organization of the Petroleum Exporting Countries (OPEC) to limit global production with their production cut agreement and the US shale producers ramping up operations to take advantage of stable prices. The release of the weekly inventories one day before the OPEC meeting in Vienna anticipated to end with the announcement of a 6 to 9 month extension will impact commodity currencies.

The EUR/USD lost 0.396 percent in the last 24 hours. The single pair is trading at 1.1197 after the USD rebounded ahead of the release of the May’s FOMC meeting minutes. The turmoil the Trump Administration has found itself into after the firing of FBI Director James Comey has put downward pressure on the USD. The pro-growth policies expected at the beginning of Trump’s term have hit another wall as further divisions within the Republican party could emerge delaying them until the last quarter of the year, or maybe well into 2018.

Monetary policy divergence still favours the dollar. The U.S. Federal Reserve is set to hike in June to leave the benchmark rate in a range of 100 to 125 basis points. Investors will be looking at the notes from the central bank meeting to look for more details on the balance sheet wind down which is forecasted to take place in the second half of the year.

The USD/CAD gained 0.072 percent in the last 24 hours. The currency pair is trading at 1.3518 after the USD staged a comeback in the North American trading session. The pair went from a daily low of 1.3456 and quickly went above the 1.35 price level where it is currently trading. Oil prices boosted the loonie on Monday and early trading Tuesday coupled with a strong wholesale trade data in Canada but as traders booked their profits on a weak USD and repositioned for a slightly hawkish Fed minutes the greenback bounced back.

The Bank of Canada is forecasted to hold as the economy is still struggling to regain the momentum is lost with the drop in oil prices two years ago. With the Fed all set to hike rates in June, this will widen the interest rate gap between the two economies. Trade disputes and the more aggressive tactics by the US to solve them are also a concern as Canada exports two thirds of exports to its southern neighbour.

The price of oil gained 0.926 percent on Tuesday. The West Texas Intermediate is trading at $51.14 ahead of Wednesday’s release of the weekly US crude inventories. Another drawdown is awaited, marking 7 contractions in a row in US inventories. The US President Donald Trump proposed to sell half of the strategic oil reserve starting in October. Ironically the fund was started in 1975 to avoid a repeat of gas price surges during the Arab oil embargo. The Organization of the Petroleum Exporting Countries (OPEC) is now once again cutting production, but even with all the members and other influential producers such as Russia they can only keep the price stable. US production has grown to the point where it could justify the sale of the emergency stocks stored in Louisiana and Texas. Although it is hard for this to be approved by congress, specially now, but it does send a signal to OPEC ahead of their meeting on Thursday to extend their agreement to cut production.

Market events to watch this week:

Wednesday, May 24

- 8:45am EUR ECB President Draghi Speaks

- 10:00 am CAD BOC Rate Statement

- 10:00 am CAD Overnight Rate

- 10:30 am USD Crude Oil Inventories

- 2:00 pm USD FOMC Meeting Minutes

- 10:00pm NZD Annual Budget Release

Thursday, May 25

- 4:30 am GBP Second Estimate GDP q/q

- All Day ALL OPEC Meetings

- 8:30 am USD Unemployment Claims

Friday, May 26

- 8:30 am USD Core Durable Goods Orders m/m

- 8:30 am USD Prelim GDP q/q

Fed Focus To Sharpen

With Trump overseas the focus on politics is fading at the same time as the June 14 FOMC meeting comes into focus. The New Zealand dollar was the top performer while the euro lagged as it finally gave up some ground. Kuroda and Australian construction work are up next.

The US dollar caught a bid late in New York trade on Tuesday as Treasury yields moved higher. Yesterday's speech from Brainard generally avoided monetary policy except for a nod towards soft core inflation in the Q&A. The thinking was that she would have said something more if she was planning to argue against a June hike. The same could be said about another dove in Kashkari. He said he wants to see more economic data before making up his mind.

The thinking in the market is as follows: If the dovish contingent at the Fed hasn't been swayed yet, there's no hope of swinging the moderates and hawks in time for June 14.

There is still time for a shift before the June 3 blackout period starts. A full slate of top-tier data is due before then and one to watch will be the FOMC minutes on Wednesday. They will likely skew hawkishly because they're from May 3, when officials had more confidence about inflation and growth. But if the Fed wants to sneak in a hint about patience, it's an opportunity.

Before that, the BOJ's Kuroda speaks at 0000 GMT in Tokyo. Expectations are low for any kind of shift from the BOJ at the moment so any hint might enliven JPY trading.

For AUD traders, the Q1 construction work report is due at 0130 GMT. The consensus is for a 0.5% decline to compound a 0.2% drop in Q4 2016. Any miss is likely to move AUD as the RBA keeps a close eye on data.s

EUR/USD Extends Gains, But Rally to Slow?

- European equities opened little changed as uncertainty after the Manchester terrorist attack weighed on sentiment. However, European markets soon returned to risk-on modus as EMU eco data were very strong. Gains eased slightly in afternoon trading but most European indices still show gains of about 0.5%.

- US equities futures traded in positive territory for most of the day, but open only with marginal gains of 0.1%/0.2% as a big part of the post-Trump losses are reversed and as key technical levels are again coming within reach.

- European PMI confidence indicators indicated that European growth will stay strong in the second quarter. The May EMU composite PMI remained at the highest level in more than six years (56.8). According to IHS Markit the PMI pointed to 0.7% Q/Q in the quarter of 2017.

- German business morale as measures by Ifo brightened more than expected in May to hit its highest level on record since 1991. Both current conditions index (123.2 from 121.4) and the expectations component (106.5 from 105.2) improved further, indicating that Europe's biggest economy is firing on all cylinders.

- President Donald Trump is set to propose a raft of politically sensitive cuts in his first full budget, for the fiscal year that starts in October, a proposal that some analysts expected would be put aside by lawmakers. Trump wants lawmakers to cut $3.6 trillion in government spending over 10 years according to a preview given to reporters.

- The Brexit squeeze on British consumers has hurt the government's finances as well as retailers, data showed on Tuesday. A stalling of sales tax revenues, a barometer of the economy, helped to widen Britain's budget deficit by more than expected. A separate survey showed business confidence among retailers declined at the fastest pace since 2012.

- The Hungarian central bank left its benchmark rate unchanged at 0.90% for the 12th month. Recent strong economic data failed to convince policy makers to change tactics. Rate-setters remain ready to use targeted instruments to ease conditions further if inflation remains persistently below target.

Core bonds little changed; Schatz auction fails.

Core bonds trade flat (Germany) to slightly higher (US Treasuries) in an uneventful session. Strong EMU data weighted in the morning session on the Bund and helped equities higher. From noon onwards, the Bund struggled higher, but without much conviction, but limiting the losses. The Schatz auction went poorly (see below) while the Belgium new 20-year syndicated OLO attracted strong demand and was priced sharply (see below). There was a lot of talk about the US budget proposals, but ultimately it was considered as a non-starter and thus left US Treasuries untouched. At the time of writing, US yields decline modestly between 0.8 bp (2-yr) to 1.8 bps (5-yr). The German 2-yield rises by 2.7 bp while yields at the remainder of the German curve are almost flat.

In EMU bond markets 10-yr yield spreads narrowed slightly for semi-core and Ireland (-2 bp), while Italy outperformed (-4 bps). Greece trades 15 bps wider as a result of the inability of the Greek creditors to cling a deal on debt relief. That means there is still no certainty Greece will receive the next tranche of its bailout loan. That is needed to repay €7B of maturing bonds and coupons.

Belgium sold successfully €3B of its 20 yr benchmark (June 2037) at mid-swaps +8. The debt agency allocated less than investors expected after the book totalled more the €15B. As a consequence, Belgium outperformed at the 20-yr sector. The German Schatz auction (€5B 0% June 2019)) was again very poor. The bid/cover amounted to only 0.9 (€3.965B). The Bundesbank retained more than €1B for its market regulation which brought the official bid/cover at 1.2. There was an unusual tail of 2 cents. The Schatz 2-yr underperformed the German curve.

EUR/USD extends gains, but rally to slow?

Today, the trends of the previous days persisted. USD/JPY (111.10) struggled to make any further gains even as sentiment on risk remained constructive for most of the session. The euro remained well bid supported by very strong EMU confidence data. The EUR/USD touched a new intraday top but trades currently again in the 1.1235 area. The jury is still out, but the pace of the Euro rally shows tentative signs of slowing.

Overnight, the terrorist attack in Manchester dominated the press headlines, but the impact on global markets was modest. The yen traded marginally stronger (USD/JPY 111.00). EUR/USD (1.1250 area) held near the recent highs even as negotiations on a solution for the Greek debt involving the IMF again didn't reach a conclusion.

European equities opened mixed to slightly lower. EUR/USD dropped temporary to the 1.1225 area before the start of European equity trading. However, a series of impressive EMU eco data reactivated a European risk trade. The EMU PMI remained at the highest level in more than six years. German IFO confidence even printed the best level since the early 90's. That data suggest ongoing strong growth in the second quarter and question the need for an extremely accommodative ECB policy stance. Core bond yields rose gradually further. Especially short-term interest rate differentials narrowed in favour of the euro. EUR/USD touched a new correction top in the 1.1268 area. As was the case of late, USD/JPY again hardly profited from the risk-on sentiment. The pair held a tight range mostly in the low 111-area.

There were no important early morning data in the US. US investors debated the new budget plan of the Trump administration. However, the plan contained aggressive spending cuts and it is unclear how the budget gap will be solved. All this makes it very unlikely a similar plan will pass in Congress. If anything, the plan might be a negative for the dollar. The US PMI report was mixed with manufacturing (52.5) printing slightly softer than expected, but services was stronger than expected (54.00). Even so, the report doesn't help risky assets or the dollar. EUR/USD trades in the 1.1235/40 area. USD/JPY still struggles not the fall below the 111 big figure.

EUR/GBP sets a new ST correction top

Today, the news flow on the UK and the UK economy remained sterling negative. The terrorist attack in Manchester yesterday evening weighed on sterling overnight, but the losses were limited. During the morning session, the April budget deficit was reported wider than expected. VAT revenues disappointed indicating a loss of dynamics in consumer spending. The CBI May reported sales were also softer than expected. At the same time, the euro remained in good shape as EMU eco data indicating ongoing strong growth in Q2. EUR/GBP touched a new correction top in the 0.8675 area around noon. Afterwards, the euro rally shifted into lower gear. EUR/GBP trades currently in the 0.8650 area. The intraday picture of cable was more diffuse. The pair hovered sideways in the upper half of the 1.29 big figure. The pair still fails to sustain north of 1.30 even as USD sentiment remains fragile.

Yen Unchanged Despite Disappointing Japanese Data

USD/JPY continues to have a quiet week. In Tuesday's North American session, the pair is trading just above the 111 line. On the release front, Japanese Flash Manufacturing PMI dropped to 52.2, short of the forecast of 52.9 points. Japanese All Industries Activity declined 0.6%, weaker than the forecast of -0.4%. US data also stumbled on Tuesday. New Home Sales dropped to 569 thousand, well short of the forecast of 611 thousand. As well, the Richmond Manufacturing Index dropped to just 1 point, compared to a forecast of 15 points. On Wednesday the Federal Reserve will release the minutes of its policy meeting earlier this month.

The Fed is likely to raise rates at the June policy meeting, but the odds of a rate hike have been showing an unusual amount of movement. In late April, a rate hike was priced in at just 50%. The odds have jumped higher in May, and currently the markets have priced in a hike at 78%. Leaving a June hike aside, a key question is how many more hikes does the Fed have in mind for 2017? On Monday, FOMC member Robert Kaplan stated that three interest increases in 2017 was "appropriate". Earlier in the year, there was speculation that the Fed might raise rates four times in 2017, but with inflation still below the Fed target of 2.0%, three moves is a more likely scenario. The Fed minutes are expected to underscore support for a June move, but many not shed much light on what happens after that.

With President Trump overseas for his first trip abroad, the White House presented Trump's 21018 budget to lawmakers in Congress on Tuesday. Trump campaigned on slashing government spending, and the budget lives up to that promise, with major cuts to the Medicaid and the food stamp programs. Trump has outlined an ambitious program to cut government spending by $3.6 trillion in the next 10 years and achieving a balanced budget by 2020. The budget includes $25 billion for paid leave after childbirth and some $200 billion for infrastructure programs. Trump's budget will face a tough sale on Capitol Hill, with both Democrats and Republicans likely to demand changes. Still, with the cloud of scandals around dismissed FBI director James Comey lingering in the air, Trump can point to the budget as a step forward in his agenda to rein in government spending.

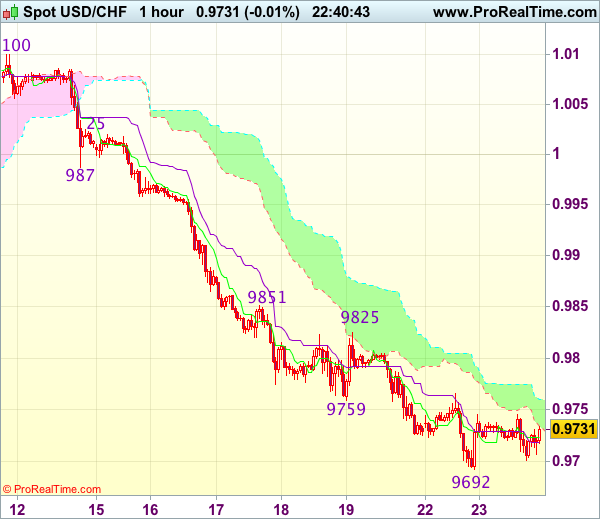

Trade Idea Wrap-up: USD/CHF – Hold long entered at 0.9700

USD/CHF - 0.9721

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9723

Kijun-Sen level : 0.9719

Ichimoku cloud top : 0.9760

Ichimoku cloud bottom : 0.9734

Original strategy :

Bought at 0.9700, Target: 0.9800, Stop: 0.9690

Position : - Long at 0.9700

Target : - 0.9800

Stop : - 0.9690

New strategy :

Hold long entered at 0.9700, Target: 0.9800, Stop: 0.9690

Position : - Long at 0.9700

Target : - 0.9800

Stop : - 0.9690

Although dollar has remained under pressure and marginal weakness from here cannot be ruled out, as long as yesterday’s low at 0.9692 holds, prospect of another rebound remains, above 0.9765-70 would suggest low is possibly formed, bring subsequent bounce to 0.9800 but reckon upside would be limited to 0.9825 and previous resistance at 0.9851 should remain intact, bring another decline later.

In view of this, we are holding on to our long position entered at 0.9700. Below 0.9670-75 would risk weakness to 0.9650 but still reckon downside would be limited to 0.9620-25 and bring another rebound later.