Sample Category Title

EUR/USD Monitoring Resistance At 1.1300, GBP/USD Holding Below 1.3000, USD/JPY Consolidating.

EUR/USD Monitoring resistance at 1.1300

EUR/USD is trading higher towards strong resistance at 1.1300 (09/11/2017 high). Hourly support can be found at 1.0842 (11/05/2017 low). Strong support is now given at 1.0682 (21/04/2017 base) and key support can be found at 1.0494 (22/02/2017 low). Expected to continue growing higher.

In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD Holding below 1.3000.

GBP/USD is trading sideways. Hourly resistance is given at 1.3048 (18/05/2017 high). Hourly support are given at 1.2831 (04/05/2017 low) and1.2757 (21/04/2017 low). An unlikely break of this last support would indicate further weakness. Expected to push higher.

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY Consolidating.

USD/JPY has exited the symmetrical triangle and keeps pushing lower despite ongoing bullish consolidation. Hourly support is given at 110.24 (18/05/2017 low). Stronger support is located at 108.13 (17/04/2017 low). Other key supports lie at a distant 106.04 (11/11/2016 low). The road is now wide-open for further decline.

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

Energy And Precious Metals Mark Time In Asia

A resurgent dollar in Asia sees oil and gold trade slightly lower, but they remain constructive in the larger technical picture ahead of event risk this week.

Oil had a steady night with an upward bias as traders chose to buy dips in prices during the New York session rather than chase the market to new highs. Both Brent and WTI contracts posted new monthly highs, at one stage up over one percent before drifting lower later in the session to mark a sideways day when all was said and done.

The OPEC/Non-OPEC production cut extension seems now fully priced in for Thursdays meeting and it will likely take either a surprise extension of the length of the deal or a larger than anticipated cut to give oil renewed topside impetus. However, a weaker dollar generally should ensure that barring any other news; crude remains bid on dips as we head into Thursday.

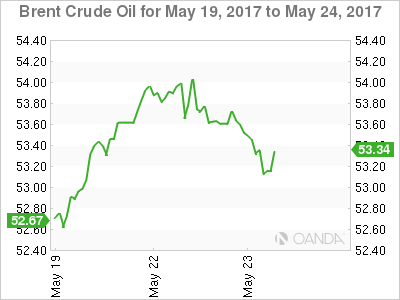

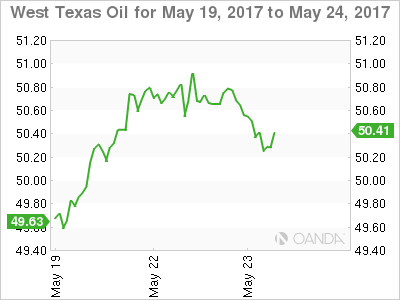

OIL

Brent spot trades at 53.30 and has fallen below its 100-day moving average at 53.40. It has initial support at 53.00 followed by 52.50. Resistance is at 54.25 with a break opening a possible move to 54.50.

WTI spot has failed to close above its 100-day moving average for the 2nd day in a row. It lies just above current levels at 50.80. The next resistance is the overnight high at 51.05 followed by 52.00. Intraday support is being tested as we speak at 50.40 and is followed by 49.50.

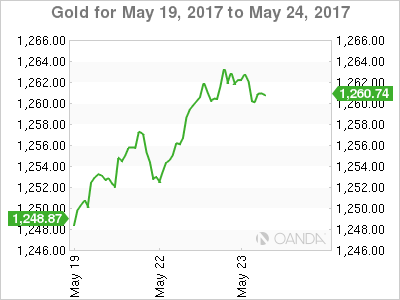

Gold

Gold continues to trade constructively as the U.S. Dollar fell overnight following Chancellor Merkel’s comments. Gold rallied from 1256 to close around 1260 before catching another tail wind in early Asia trading, moving higher to 1263. Nervousness ahead of Thursday’s OPEC meeting should see traders continue to hedge risk by buying gold on dips over the next few days.

Gold has initial resistance at Thursday’s high of 1265 and then at 1270. Support appears initially at 1251.80 and then the 200-day moving average and a daily double bottom at the 1245.70 area. Only a daily close below this level would suggest the technical picture for gold has changed.

Market Update – European Session: Major European PMI Data Point To Accelerating Growth, German IFO Hits Multi-Year High

Notes/Observations

Steady market tone despite risk-off tone; price action saw little reaction to the UK blast being investigated as a terrorist incident.

Major European Manufacturing PMI handily beat expectations for multi-year highs (France, Germany and Euro Zone all beat estimates)

German IFO hits its highest level since 2011 as German economy shrugs off Brexit and Trump policies

Overnight:

Asia:

Japan May Preliminary PMI Manufacturing saw its 9th consecutive expansion but hit a 6-month low (52.0 v 52.7 prior

China Foreign Min Wang Yi: Called on North Korea to abide by UN Council rules; reiterated view that all parties should exercise restraint

PBOC Advisor Sheng Songcheng: Monetary policy adjustments is a trial and error process; The central bank will not excessively adjust monetary policy

Europe:

UK Manchester Police responded to reports of explosion at Manchester Arena; confirmed almost two dozen dead, over four dozen injured; incident being treated as terrorist incident; govt parties suspend campaigning ahead of June 8th elections

Eurogroup chief Dijsselbloem confirmed had not reached an overall deal on Greece debt as unable to close a gap in views; reiterated view that was very close to an agreement on Greece. Conclusion on Greek debt could be reached on June 15th Eurogroup meeting. IMF was impressed by Greek reforms but will wait for final discussion on debt in June before deciding whether to join bailout

Greece Fin Min Tsakalotos: Had difficult discussion on Greek debt clarity; It was the duty of IMF and EU states to bridge the gap

Americas:

President Trump's budget said to seek $3.6T in US spending cuts over 10 years; Seeks to sell half of US strategic petroleum reserve (SPR) to raise $16.5B. Forecasted FY17 deficit at $603B and at $440B in FY18. Forecasted 2017 US real GDP growth at 2.3%; 2018 US real GDP growth at 2.4%; 2019 US real GDP growth at 2.7%; Saw 3.0% GDP growth starting in 2021

President Trump said to have made requests in March that Director of National Intelligence Coats and NSA director Rogers deny collusion between his campaign and Russia

S&P maintained Brazil sovereign rating at BB; revised outlook to Watch Negative from Negative

Energy:

Saudi Oil Minister: no final decision on extending output cuts will occur until the OPEC meeting Thursday. New output deal will be similar to the prior and everyone was in agreement on a 9 month extension.

Iraq oil min Al-Luaibi: After meeting with Saudi counterpart, we agreed that production agreement should be extended for 9 months

UAE Energy Min: Supported extension of agreement for another term

Mexico Dep Energy Min: Supported 9-month extension of oil supply cut agreement

Economic Data

(SG) Singapore Apr CPI M/M: -0.3% v -0.1e; Y/Y: 0.4% v 0.5%e; CPI Core Y/Y: 1.7% v 1.5%e

(DE) Germany Q1 Final GDP Q/Q: 0.6% v 0.6%e; Y/Y: 1.7% v 1.7%e; GDP NSA Y/Y: 2.9% v 2.9%e

(DE) Germany Q1 Private Consumption Q/Q: 0.3% v 0.3%e, Government Spending Q/Q: 0.4% v 0.3%e; Capital Investment Q/Q: 1.7% v 1.7%e; Construction Investment Q/Q: 2.3% v 2.5%e, Domestic Demand Q/Q: 0.2% v 0.5%e, Exports Q/Q: 1.3% v 1.5%e; Imports Q/Q: 0.4% v 1.0%e

(CH) Swiss Apr Trade Balance (CHF): 2.0B v 3.0B prior; Real Exports M/M: -2.5% v 1.8% prior; Real Imports M/M: +2.6% v +0.6% prior

(JP) Japan Apr National Dept Store Sales: +0.7 v -0.9% prior; Tokyo Dept Store Sales: -0.8 v -0.2% prior

(FR) France May Business Confidence: 105 v 105e; Manufacturing Confidence: 109 v 108e

(FR) France May Preliminary Manufacturing PMI: 54.0 v 55.2e (8th month of expansion), Services PMI: 58.0 v 56.7e; Composite PMI: 57.6 v 56.6e

(DE) Germany May Preliminary Manufacturing PMI: 59.4 v 58.0e (30th month of expansion and highest since Apr 2011), Services PMI: 55.2 v 55.5e, Composite PMI: 57.3 v 56.6

(SE) Sweden Apr Unemployment Rate: 7.2% v 7.1%e; Unemployment Rate (Seasonally Adj): 6.7% v 6.5%e

(TW) Taiwan Apr Industrial Production Y/Y: -0.6% v +4.2%e

(EU) Euro Zone May Preliminary Manufacturing PMI: 57.0 v 56.5e (46th straight month of growth and highest since April 2011), Services PMI: 56.2 v 56.4e v 56.4 prior, Composite PMI: 56.7e v 56.8 prior

(DE) Germany May IFO Business Climate: 114.6 v 113.1e (highest level since 2011), Current Assessment: 123.2 v 121.0e, Expectations Survey: 106.5 v 105.4e

(UK) Apr Public Finances (PSNCR): -£15.5B v +£27.7B prior; Public Sector Net Borrowing: £9.6B v £8.0Be, Central Government NCR: -£15.2B v +£18.3B prior, PSNB ex Banking Groups: £10.4B v £8.7Be

(HK) Hong Kong Apr CPI Composite Y/Y: 2.0% v 1.5%e

(NG) Nigeria Q1 GDP Y/Y: -0.5% v +0.3%e

Fixed Income Issuance:

(BE) Belgium Debt Agency (BDA) opened its book to sell EUR-denominated Jun 2037 OLO Bonds via syndicate; guidance seen +10bps to mid-swaps; order book approaching €9.0B

(ID) Indonesia sold total IDR14.0T in 3-month and 9-month Bills; 10-year, 12-year and 20-year Bonds

(SE) Sweden sold SEK10B vs. SEK10B indicated in 3-month bills; Avg Yield: -0.7198% v -0.6892% prior; bid-to-cover: 3.18x v 2.17x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx50 +0.6% at 3598, FTSE +0.2% at 7509, DAX +0.3% at 12660. CAC-40 +0.7% at 5359, IBEX-35 +0.9% at 10885, FTSE MIB +0.6% at 21449, SMI -0.4% at 9049, S&P 500 Futures +0.1%]

Market Focal Points/Key Themes European Indices are trading modestly higher buoyed by stronger PMI and IFO data out of Europe, with the exception of the Swiss SMI which currently trades down over 0.3%. Positive earnings also added to sentiment with shares of Homeserve rising sharply in the UK following earnings which beat forecasts, and Greencore shares also an out performer after reporting first half results. Aveva shares on the other hand down close to 5% following there results. US home builder Toll Brothers reported strong results with a beat on both the top and bottom line. Looking to the US morning, notable earners include Autozone, DSW and Cracker Barrel.

Equities

Consumer discretionary [Greencore [GNC.UK] +6.5% (Earnings), Homeserve [HSV.UK] +14% (Earnings), Entertainment One [ETO.UK] +1.8% (Earnings), Hugo Boss [BOSS.DE] -1.2% (Guidance)]

Industrials: [KWS Saat [KWS.DE] +2.1% (Earnings), Lem Holdings [LEHN.CH] +7% (Earnings)]

Technology: [Aveva [AVV.UK] -5% (Earnings)]

Telecom: [Nokia [NOK1V.FI] +% (Sign patent license and business collaboration agreement with Apple, settle all litigation)

Healthcare: [Genomic Vision [GV.FR] +26% (Collaboration with Astrazeneca)]

Utilities: [Severn Trent [SVT.UK] +0.9% (Earnings)]

Speakers

Norway Central Bank (Norges) Gov Olsen: Central banks were gaining control of deflation but could not count on oil prices rising much above $50-55/barrel

IMF chief Lagarde: Global financial stability continues to improve while global uncertainty remained fairly high

Portugal Fin Min Centeno stated that he expected an agreement on Greece debt at next Eurogroup meeting (**Note: scheduled for Jun 15th). Policies were more important than the next head of ECB

German IFO Economists noted that German companies want to export more as inventories have grown. Q2 GDP growth pointing to 0.6% and neither Brexit or Trump policies have had concrete effect on German economy. France election of Macron was a positive signal and giving a tailwind to EU

Euro Zone bank resolution body (SRB) chief Koenig: Bad loans must be address by EU authorities

Kuwait Oil Min Almarzooq: all agreed on 6 months of extension of cuts, but not everyone is on board for a 9-month extension

Currencies

EUR/USD was near 6-month high initially aided by comments on Monday from German Chancellor Merkel reiterated that larget German surpluses were aided by a weak EUR currency. The region received further impetus as the major European PMI data pointed to accelerating growth and the German May IFO Business Climate survey hit a multi-year high. The strong data giving credence that ECB could soon take steps to begin normalizing its policy. Dealers did note that recent comments from ECB's Weidmann (Germany) that easy policy was still appropriate at this time dimmed prospect for any change in language in June.

GBP/USD was holding up well despite the terror incident in Manchester UK that killed approx. two dozen and injured dozens more. The pair was holding just below the 1.30 handle. Dealer did not that cable has had three recent failures ahead of 1.3050 option barrier level.

The JPY currency (Yen) befitted from safe-haven flows following the UK terror incident. USD/JPY was softer by 0.2% but holding above the 111 level just ahead of the NY morning.

Fixed Income

Bund futures trade at 160.72 down 20 ticks, approaching the lows from last week's trading range. Resistance lies near the April 27th high of 162.01 level followed by 163.68. A break of 160.01 support level could see lows target 159.01 followed by 157.50.

Gilt futures trade at 128.39 higher by 3 ticks, slightly reacting from the mixed public finances data. Last week's rally respected both the 129.00 handle and the 129.14 April 18th high. Price is still consolidating below the 128.51 level and finds key support at the 127.52 support level. An acceleration lower could test the 126.74 region. Resistance stands at noted 128.51 level then 129.14 followed by 132.80.

Tuesday's liquidity report showed Monday's excess liquidity dropped lower to €1.627T a decline of €11B from €1.638T prior. Use of the marginal lending facility fell to €212M from €216M prior.

Corporate issuance saw over $20.1B come to market via 8 issues headlined by Becton Dickinson $9.7B in an 8-part senior unsecured note offering and Enel Finance $5B in a 3-part senior note offering

Looking Ahead

(NG) Nigeria Central Bank Interest Rate Decision: Expected to leave Interest Rates unchanged at 14.00%

(UR) Ukraine Apr Industrial Production M/M: No est v 8.9% prior; Y/Y: -2.0%e v -2.7% prior

(IT) Italy Debt Agency (Tesoro) announces upcoming CTZ and Inflation link (BTPei) auction for Fri, May 26th

(AR) Argentina May Consumer Confidence Index: No est v 46.2 prior

05.30 (UK) Weekly John Lewis LFL sales data

05:30 (EU) ECB allotment in 7-Day Main Refinancing Tender

05:30 (HU) Hungary Debt Agency (AKK) to sell 3-month Bills

05:30 (DE) Germany to sell €5.0B in 2019 Schatz

05:30 (UK) DMO to sell £850M in 0.125% I/L 2036 Gilts

06:00 (UK) May CBI Retailing Reported Sales: 10e v 38 prior, Total Distribution: 31e v 44 prior

06:00 (TR) Turkey to sell 6-month Bills

06:45 (US) Daily Libor Fixing

07:30 (TR) Turkey May Real Sector Confidence (Seasonally Adj): 107.1e v 106.3 prior; Real Sector Confidence (unadj): 109e v 111.2 prior

07:30 (TR) Turkey May Capacity Utilization: 75.2%e v 78.4% prior

07:45 (US) Weekly Goldman Economist Chain Store Sales

08:00 (HU) Hungary Central Bank (NBH) Interest Rate Decision: Expected to leave Base Rate unchanged at 0.90%

08:00 (BR) Brazil Mid-May IBGE Inflation IPCA-15 M/M: 0.2%e v 0.1% prior; Y/Y: 3.7%e v 4.4% prior

08:15 (UK) Baltic Dry Bulk Index

08:30 (CA) Canada Mar Wholesale Trade Sales M/M: +1.0%e v -0.2% prior

08:55 (US) Weekly Redbook Sales

09:00 (EU) Weekly ECB Forex Reserves:

09:00 (MX) Mexico Mar Retail Sales M/M: 0.3%e v 2.4% prior; Y/Y: 5.5%e v 3.6% prior

09:00 (US) Fed's Kashkari (dissenter)

09:00 (HU) Hungary Central Bank Gov Matolcsy post rate decision statement

09:00 (RU) Russia announces weekly OFZ bond auction

09:30 (BR) Brazil Apr Current Account: $1.2Be v $1.4B prior; Foreign Direct Investment (FDI): $5.5Be v $7.1B prior

09:45 (US) May Preliminary Markit Manufacturing PMI: 53.1e v 52.8 prior, Services PMI: 53.3e v 53.1 prior, Composite PMI: No est v 53.2 prior

10:00 (US) Apr New Home Sales: 610Ke v 621K prior

10:00 (US) May Richmond Fed Manufacturing Index: 15e v 20 prior

10:00 (PT) Portugal PM Costa in parliament

11:00 (FR) ECB's Coeure 9France) on panel in Paris

11:30 (US) Treasury to sell 4-week and 52-week Bills

12:00 (DE) German Chancellor Merkel at event

13:00 (US) Treasury to sell 2-Year Notes

15:00 (AR) Argentina Apr Trade Balance: -$0.1Be v -$0.9B prior

15:00 (AR) Argentina Mar Economic Activity Index (Monthly GDP) M/M: No est v -1.% prior; Y/Y: +1.0%e v -2.2% prior

15:00 (US) Fed's Kashkari (dissenter)

16:30 (US) Weekly API Oil Inventories

17:00 (US) Fed's Harker (voter, hawk) in NY

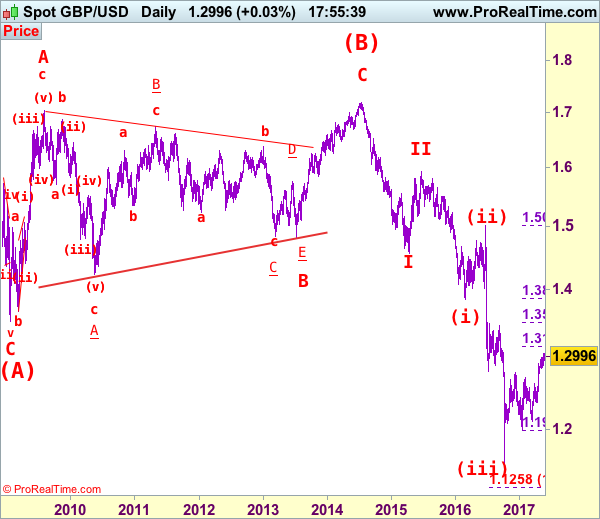

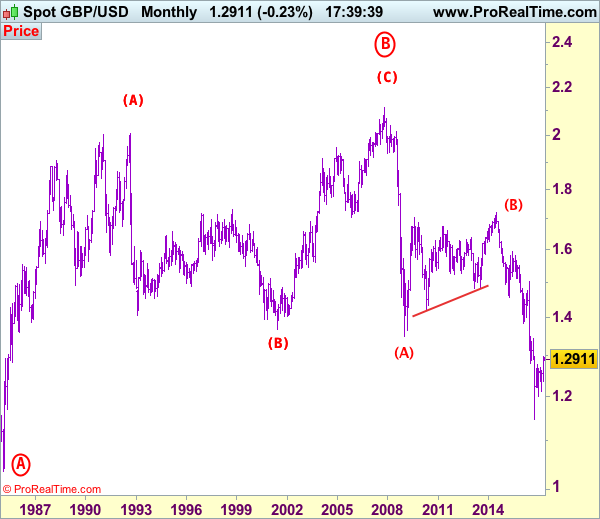

GBP/USD Elliott Wave Analysis

GBP/USD – 1.2977

GBP/USD – Wave 4 is unfolding as an (A)-(B)-(C) and could have ended at 1.7192

Although the British pound has risen again and rose to as high as 1.3048, loss of upward momentum should prevent sharp move beyond 1.3100 and risk is seen for a retreat to take place, below 1.2885-90 would bring pullback to 1.2844 support, however, downside should be limited to 1.2800 and previous support at 1.2757 (previous 4th of a lesser degree) should attract renewed buying interest and bring another rally towards 1.3140-50 (38.2% Fibonacci retracement of 1.5018-1.1986) but risk from there has increased for a retreat later.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has possibly ended at 1.7192, below support at 1.4232 would add credence to this count, then further fall to 1.4000 level would follow but reckon downside would be limited to 1.3655 support and price should stay above previous support at 1.3500.

On the downside, whilst initial pullback to 1.2885-90 cannot be ruled out, reckon downside would be limited to 1.2844 and 1.2757 support should attract renewed buying interest, bring another upmove. Below previous resistance at 1.2706 (now support) would signal a temporary top is formed, bring retracement of recent upmove to 1.2650-60 but previous resistance at 1.2616 (tentatively wave i top) should remain intact.

Recommendation: Buy at 1.2760 for 1.3000 with stop below 1.2660.

Longer term - Cable's rise from 1.0520 (Feb 1985) to 2.0100 (September 1992) is seen as [A], the decline to 1.3682 is labeled as (B) and (C) wave rally has ended at 2.1162 (9 Nov, 2007) which is also the top of larger degree wave B with circle. The selloff from there is a 5-waver with wave (A) ended at 1.3500 (23 Jan 2009), wave (B) itself is labeled as A: 1.6733, triangle wave B: 1.4813 and wave C as well as top of wave (B) ended at 1.7192 (2014), hence the selloff from there is an impulsive wave (C) with wave I : 1.4566, wave II 1.5930, an extended wave III is unfolding and already exceeded our downside target at 1.3500 and 1.3000, hence weakness to 1.2500 and possibly 1.2000 cannot be ruled out, however, price should stay well above psychological level at 1.0000.

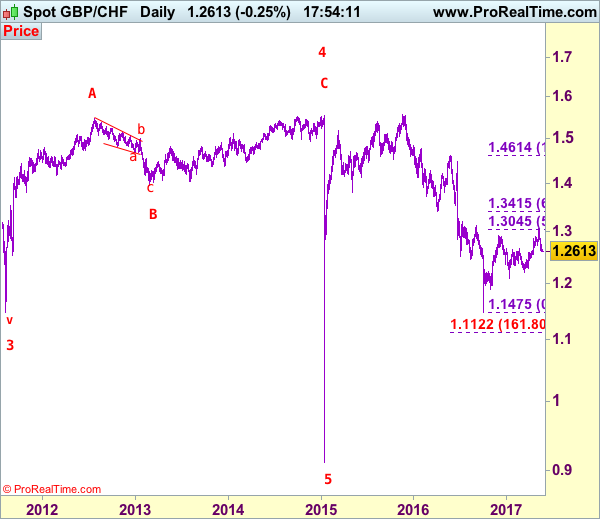

GBP/CHF Elliott Wave Analysis

GBP/CHF – 1.2615

GBP/CHF – Circle wave v ended at 0.9106 and major correction has commenced for subsequent gain to 1.5547.

Despite rising to 1.3069 earlier this month, the subsequent sharp retreat together with the breach of support at 1.2729 suggest top has possibly been formed there and consolidation with downside bias is seen for the fall from there to bring at least a retracement of recent rise to 1.2550-55, then 1.2490-00, however, break of support at 1.2440-45 is needed to add credence to this view and extend further fall to another previous support at 1.2285 but price should stay above 1.2215 support.

To recap the larger degree count, the selloff from 2.4965 (July 2007) is the beginning of wave V with circle and is labeled as 1: 2.3760, 2: 2.4425, wave 3 extension ended at 1.1470, followed by wave 4 at 1.5547, the quick rebound from 0.9106 suggests wave 5 as well as entire circle wave V could have ended there, hence consolidation with mild upside bias is seen for major correction to take place, bring initial test of 1.5547 (previous 4th of a lesser degree).

On the upside, whilst recovery to 1.2690-00 cannot be ruled out, reckon 1.2790-00 would limit upside and bring another decline later. Above 1.2860-65 would suggest first leg of decline from 1.3069 has ended, bring a stronger rebound to 1.3000 but said resistance at 1.3069 should remain intact.

Recommendation: Sell at 1.2800 for 1.2500 with stop below 1.2900.

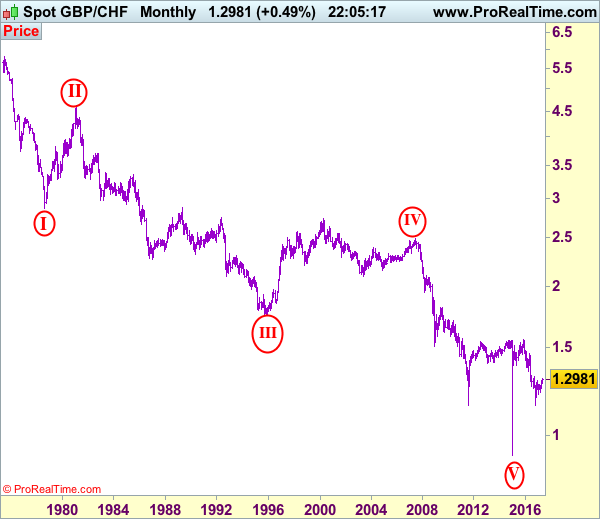

On the Monthly chart, the longer-term count is that major downtrend is under way with circle wave I at 2.8645 (Sep 1.978), then wave II with circle at 4.6175 (Feb 1981), the wave III with circle ended at 1.7425 (Nov 1995) and followed by wave IV with circle at 2.4965 (July 2007 with a short wave C) and wave V with circle has possibly ended at 0.9106. A monthly close above 1.5547 would add credence to this view, bring major correction to 1.7000, then towards psychological level at 2.0000.

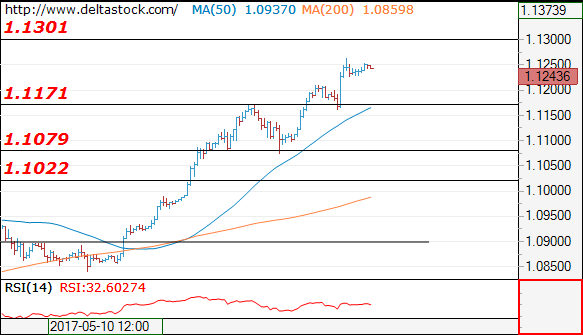

EUR/USD Analysis: Near 1.1250 Mark On Tuesday

'German Chancellor Angela Merkel described the shared currency as 'too weak.' – Alexandria Arnold and Dennis Pettit, Bloomberg

Pair's Outlook

After the fundamental move of the Euro against the US Dollar, which broke the medium term ascending channel pattern, the currency exchange rate continued to trade near the 1.1250 mark on Tuesday morning. The pair is most likely going to reach the 1.13 mark soon, as it faces no resistance up to that level. Meanwhile, from a fundamental perspective markets are grasping the comments of the German Chancellor in regards to the ECB and the weakening of the Euro. However, the bottom line is that Merkel does not like how the ECB has weakened the common currency.

Traders' Sentiment

SWFX traders remain with an unchanged opinion, as 60% of open positions remain short. Meanwhile, 58% of trader set up orders are to buy the Euro.

GBP/USD Analysis: Attempts To Prolong Consolidation

'Bulls would be eyeing for a follow through momentum beyond 1.3040-50 immediate hurdle, above which the pair is likely to aim towards reclaiming the 1.3100 handle and head towards testing 1.3125-30 resistance area, marking 38.2% Fibonacci retracement level of post-Brexit downslide.' – Haresh Menghani (based on FX Street)

Pair's Outlook

Monday ended with the Sterling remaining completely unchanged against the US Dollar, with the pair attempting to return into its consolidation trend's borders. In order for this to be confirmed the British Pound is required to close in the red zone today, below the weekly pivot point as well. The second closest support lies only around 1.2930, formed by the 20-day SMA and the weekly S1. However, technical indicators suggest the bullish momentum is likely to prevail; in case it does, the Cable is likely to reach the 1.31 mark within the next two weeks.

Traders' Sentiment

Traders are still neutral towards the Pound, holding 51% of short and 49% of long positions. At the same time, the share of purchase orders inched down from 60 to 56%.

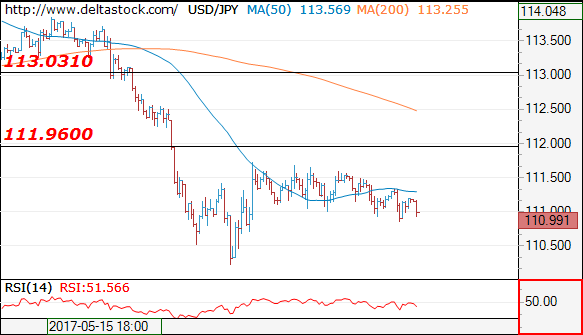

USD/JPY Analysis: Stuck Between 110.50 And 111.75

'USD/JPY-slightly bearish. We expect the pair may move towards 110.80.' – Fullerton Markets (based on Investing.com)

Pair's Outlook

The USD/JPY pair has been trading rather calmly since last week's sharp decline, managing to retain its positions above the 111.00 major level. The given pair now appears to be contained within a specific trading range, with the 55-day SMA and the weekly PP representing the upper border, and the monthly PP with the lower Bollinger band-the lower one. Additionally, strong demand rests around the 110.00 mark, which should limit any deeper losses should the immediate support fail. Meanwhile, technical indicators imply the Greenback is to outperform the Yen again, but due to lack of impetus the nearest resistance is likely to remain intact today.

Traders' Sentiment

There are 60% of traders holding short positions, while 55% of all pending orders are to acquire the US Dollar.

Gold Analysis: Near 1,260 Level

'We suspect that gold will respond more forcefully going into Tuesday's session as geopolitical tensions start to rise again.' – Edward Meir, INTL FCStone (based on Reuters)

Pair's Outlook

During the early hours of Tuesday's trading session the yellow metal's price fluctuated near the 1,260 mark without a clear direction. However, on a larger scale it can be understood that the bullion is still in the surge, which began after reaching the support cluster near the 1,250 level. Due to that fact it can be assumed that the commodity price eventually will reach the nearest technical resistance, which is near the 1,270 mark, as at that level there is a resistance cluster made up of three various levels of significance.

Traders' Sentiment

Traders sentiment remains firm, as 51% of open positions are short, and 67% of trader set up orders are long.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1243

The upmove is still underway, targeting 1.1300 major resistance. Initial intraday support lies at 1.1210 and crucial on the downside is 1.1160 low.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1300 | 1.1300 | 1.1210 | 1.1022 |

| 1.1300 | 1.1300 | 1.1160 | 1.0838 |

USD/JPY

Current level - 110.99

Despite the neutral bias, the outlook here remains positive, for a rise towards 11.90, en route to 113.00 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 111.90 | 114.30 | 111.00 | 109.40 |

| 113.00 | 115.60 | 111.20 | 108.12 |

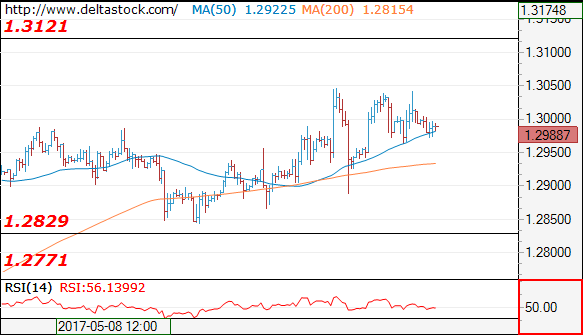

GBP/USD

Current level - 1.2988

A break through the static 1.3050 will challenge directly 1.3120 area. Crucial support on the downside is projected at 1.2830

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3050 | 1.3120 | 1.2900 | 1.2770 |

| 1.3120 | 1.3500 | 1.2830 | 1.2610 |