Sample Category Title

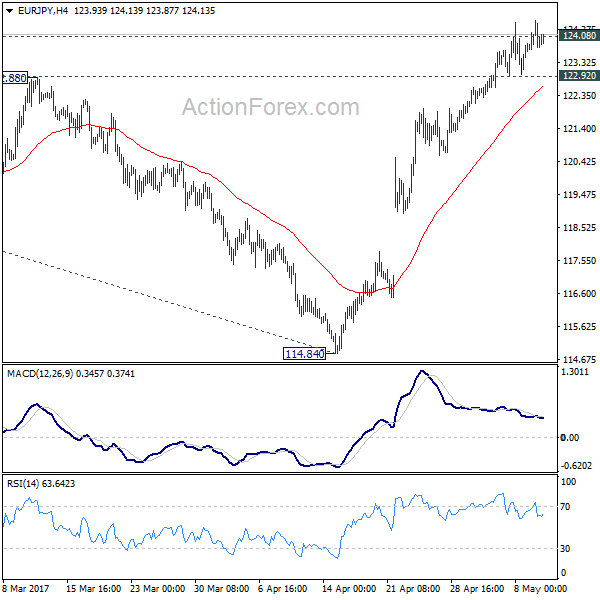

EUR/JPY Daily Outlook

Daily Pivots: (S1) 123.55; (P) 124.04; (R1) 124.45; More...

No change in EUR/JPY's outlook despite diminishing upside moment as seen in 4 hour MACD. Further rally is expected with 122.92 minor support intact. Firm break of 124.08 resistance will confirm resumption of whole rise from 109.20. In that case, EUR/JPY would target 126.09 resistance first. Break there will pave the way to 100% projection of 109.03 to 124.08 from 114.84 at 129.89. On the downside, below 122.92 minor support will turn bias to the downside and bring pull back.

In the bigger picture, focus is back on 126.09 support turned resistance. Decisive break there will confirm completion of the down trend from 149.76. And in such case, rise from 109.20 is at the same degree and should target 141.04 resistance and above. Meanwhile, rejection from 126.09 and break of 114.84 will extend the fall from 149.76 through 109.20 low.

Chinese PPI And CPI Inflation Figures Have Been Released This Morning

Market movers today

With a thin global calendar, focus is on Scandinavia inflation with the release of the Danish and Norwegian figures for April. The Danish figure should be unchanged but the Norwegian print is more interesting after weak inflation in recent months has prompted markets to shift the spot light from oil and growth to inflation. We estimate core inflation climbed to 1.9% y/y, well below Norges Bank's projections in its last monetary policy report (2.1%) but this could still allay some of the fears that inflation will fall far enough to trigger further rate cuts.

In Sweden, the Riksbank minutes from the last monetary policy meeting will be released. The minutes will be followed closely as they cover the meeting when the Riksbank surprisingly decided to extend the QE programme. The Swedish Prospera inflation expectations are also due for release today.

ECB president Draghi is scheduled to speak in the Dutch parliament in the afternoon and focus will be on whether the latest jump in core inflation as well as Macron winning the French presidency have changed the ECB's monetary policy stance. In our view, the elimination of the Frexit risk has paved the way for a more hawkish communication at the next ECB meeting in June, but regarding the inflation out look, we expect the ECB to await more information in judging whether the latest rise is due to the timing of Easter or higher underlying price pressure.

Selected market news

Former French prime minister, Manuel Val ls, has reported he wants to run under president-elect Macron's new political movement i n th e upcoming parliamen tary election. Macron aims to put candidates up in all 577 constituencies and the candidates are expected to be announced on Thursday. the election out come will be decisive for how much of Macron's policy proposals he can actually implement and the risk remains that Macron's parliamentary majority will be unstable and fragmented, see Research France: Clouds lift over Europe after Macron wins presidency, 8 May.

Chinese PPI and CPI inflation figures have been released this morning and confirm our view that some of the engines fuelling reflation are losing steam. PPI inflation fell sharply to 6.4% y/y in April from 7.6% in March and below consensus expectations at 6.7%. Hence, it seems PPI inflation peaked at the beginning of the year when it was quite high due to the big increases in commodity prices in 2016. The peak in commodity price inflation was one of the reasons we believed the reflation theme was fading, see Research: Global reflation set to lose steam, 3 April.

US President Trump has fired FBI director James Comey at a time when the agency was investigating Russia's i nterference in l ast year's election, see Bloomberg. Democrats alleged it was an effort to cut short the Russia probe and demanded a special prosecutor to carry the process forward.

ECB Research: Hawkish Wording But Changed Forward Guidance Less Likely

- Fading political uncertainty implies the way has been paved for more hawkish communication from the ECB at the meeting in June, bringing renewed market focus to the ECB's exit strategy.

- The ECB has many other options than removing the ‘or lower levels' phrase in its forward guidance on policy rates and in order to avoid a tightening of financial conditions a more cautious approach seems likely.

- The ECB's key challenge is a lack of wage pressure and as long as there are no signs of improvement in the underlying price pressure, the ECB seems to stick to its policy stance in terms of policy rates, QE purchases and forward guidance.

Market's attention could again turn to the ECB's exit strategy

The political risk in the euro area has been reduced considerably with Macron winning the French presidency and market's attention could again turn to the ECB's exit strategy. In our view, the way has been paved for a more hawkish communication at the next meeting on 8 June when the ECB will also have the next inflation print for May and updated inflation projections. In our view, a more hawkish wording should not be seen as a sign of near-term actually tightening. Instead, it should reflect there are a lot of soft words in the introductory statement (see next page), which need to be taken out gradually before actually tightening the monetary policy. Related to this, we still believe the ECB will extend its QE purchases by EUR40bn per month going into next year as the underlying price pressure remains weak. This also implies it is premature to believe in rate hikes any time before 2019, in our view.

There has been a lot of discussion about whether the ECB will change its forward guidance on policy rates and remove the ‘or lower levels' phrase at the upcoming meeting in June. The Governing Council discussed such a change at the meeting in March after which the market priced in a 10bp deposit rate hike from the ECB already this year. If the ECB makes this change to its forward guidance, it is likely to have considerable market implications with the pricing of policy rate hikes again being moved forward. However, such a price action does not seem to be what the ECB wants already, as the communication from prominent ECB members turned much more dovish in an attempt to dampen the speculation about rate hikes after the meeting in March.

Another argument against the ECB changing its forward guidance should be that the ECB communicates it has not seen sufficient evidence to change its assessment about the inflation outlook. Related to this, Draghi has said that ’before making any alterations to the components of our stance – interest rates, asset purchases and forward guidance – we still need to build sufficient confidence that inflation will indeed converge to our aim’. Hence, the question should be whether the reduced political uncertainty changes the ECB’s inflation outlook. While there could be some positive impact on economic sentiment and hence activity, the past year’s experiences are that the economic situation is resilient to political uncertainty. Added to this, a better economic outlook is not yet enough to generate higher underlying price pressure as there is a large amount of slack in the labour market. In light of this, it is key for the ECB to get wage growth up, see Euro area wage growth should stay subdued, not supporting core inflation significantly..

The ECB has other options than changing forward guidance

Instead of changing the forward guidance when it remains unclear whether the inflation outlook has improved, the ECB is in our view more likely to again remove some of its dovish wording. So far this has been the strategy from the ECB, as it at the meeting in March removed a sense of urgency in taking further actions as the introductory statement no longer included ‘if warranted to achieve its objective, the Governing Council will act by using all the instruments available within its mandate’. Likewise, at the meeting in April the ECB moved in a slightly more hawkish direction as it described the risks surrounding the growth outlook as still being tilted to the downside but moving in a more balanced configuration after characterising these downside risks as being less pronounced in March.

Hikes are premature as the ECB will follow its forward guidance

We have continuously argued it is premature to price hikes from the ECB as we expect the ECB to stick to its sequencing entailed in the forward guidance, thereby not hiking rates before having ended QE. Given our expectation of a QE extension of at least six months this should at the earliest happen in the second half of next year. In line with this, prominent ECB members have recently attempted to explain the reasoning behind the sequencing of the exit strategy. In a dovish speech Draghi argued that ‘in a multi-country monetary union such as the euro area made up of segmented national financial markets, asset purchases are inevitably more difficult to calibrate, more complex to implement and more likely to produce side-effects than other instruments. So it is natural that we turned to them only after other, more conventional options were becoming exhausted. Similarly, lowering interest rates into negative territory in a largely bank-intermediated financial system was a step into uncharted waters’. Along the same lines, ECB’s Chief economist Peter Praet argued that ’our policy instruments act as strong complement. For instance, the downward pressure that APP exerts on term premia is strengthened by the negative interest rate policy and the rate forward guidance that offers an expected horizon for continuing that policy in the near term’.

An argument behind the speculation about ECB hikes could reflect a perception that the ECB felt a need to support the banking sector, which should be suffering after the long period of negative policy rates. However, the ECB does not seem to consider bank profitability as a big problem as Draghi has recently said: ‘As household deposit rates have been sticky at zero, banks’ net interest rate margins have fallen somewhat. However, the impact on bank profitability has been offset by the positive effects of easier financial conditions on the volume of lending and the reduction in loan-loss provisions, as monetary policy has lifted economic prospects’. During the latest press conference he reiterated this message by saying that ‘the negative rates in conjunction with the other elements of our easing package have turned out to be powerful in terms of easing financial conditions and the potential negative side effects have so far been limited.”

A question remains whether the ECB could later change its sequencing strategy. On this issue executive board member Benoît Cæuré said: ‘The choice of sequencing of policy instruments will be the outcome of our regular assessment of the medium-term price stability outlook, reflecting the state-dependent nature of our expectations of the horizon over which our policy instruments are likely to be maintained’. However, his view is not shared by Praet who later said: ‘A deviation from the path of policy that is consistent with our past communication is not only costly in terms of policy credibility in general. It would also scale back an important source of stimulus that is behind the performance of the economy that we observe today’.

China’s PPI Inflation Fell Further From High Level

China's headline CPI accelerated to +1.2% y/y in April, from +0.9% a month ago, as mainly driven by the recovery of food disinflation. Food price contracted -3.5% y/y, following a -4.4% drop in March. Nonfood inflation rose to 2.4% y/y in April from +2.3% a month ago. Core inflation (excluding food and energy) improved to +2.1% y/y from +2% in March. Such level should be in line with the government's target.

PPI moderated to +6.4% in April from +7.6% in March. The deceleration came in more than expectations. A key contributor to the slowdown was commodity prices which slowed further in April as low base effects dissipated. Global prices also pulled back after the strong rally earlier in the year.

Import growth decelerated

China's trade surplus widened to US$ 38.05B in April, from US$ 23.93B a month ago. This also came in higher than expectations of US$ 35.5B. However, the reading was down -4.5% from the same period last year. Exports expanded +8% y/y while imports were up +11.9%, moderating from the +16.4% and +20.3% growth in March, respectively. Both readings came in below consensus.

Note that this is the first month since last October that China's headline import growth was worse than expectations. In renminbi terms, exports grew +14.3% y/y, while imports jumped +18.6%, during the period. Both were higher than market expectations.

The market was focused on the import growth, of which the slowdown was mainly driven by diminished commodity demand, especially in iron ore, copper and crude oil. Import growth shrank in both value and volume terms, signaling not only commodity prices, but also domestic demand, were the causes. We believe the Chinese government's tightening measures has played an important role in causing such phenomenon.

FX reserve rose for a third consecutive month

PBOC's FX reserve rose for a third consecutive month to US$3.03 trillion in April, marking a +US$21B increase from a month ago. The State Administration of Foreign Exchange attributed the increase to balanced foreign exchange supply and demand and renminibi's appreciation against US dollar. The market estimated that the reserve increased US$ 15-25B after adjusting for valuation effect.

China's FX reserve slumped over the past two years after reaching a peak of US$ 3.99 trillion in mid-2014, as the government struggled to rescue the severe depreciation of renminbi by selling foreign currencies. Over 2015 and 2016, the country's FX reserve contracted –US$ 0.83 trillion while USDCNY soared +12%. The reserved broke below US$ 3 trillion in January 2017 before stabilizing. For the first four months of this year, renminibi's movement has been steady. Note that PBOC's FX position and SAFE flow data should also be considered to monitor China's underlying FX flow situation.

Government to adopt tighter measures

The Chinese government would maintain its 'prudent and neutral' monetary policy, adopting tighter measures so as to prevent overheating in certain industries. As such, the overall growth momentum might continue to moderate in coming months, while the financial sector would face challenges over the tighter regulatory measures. Yet, the government would stay cautious to ensure the growth target would be achieved.

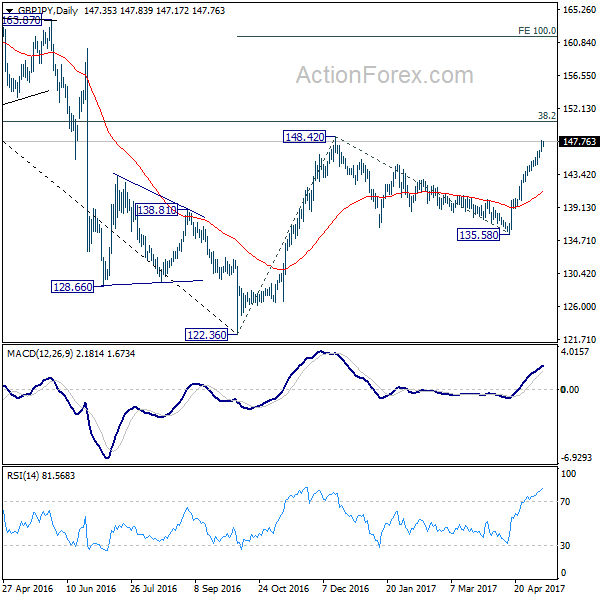

GBP/JPY Daily Outlook

Daily Pivots: (S1) 146.62; (P) 147.25; (R1) 148.06; More....

GBP/JPY's rally extends to as high as 147.86 so far and intraday bias remains on the upside for 148.20 resistance. As noted before, whole rally should 122.36 is resuming. Break of 148.20 will target 150.42 long term fibonacci level first. Break there will pave the way to 100% projection of 122.36 to 148.42 from 135.58 at 161.64. On the downside, below 145.64 minor support will turn bias neutral and bring consolidation before staging another rise.

In the bigger picture, based on current momentum, rise from 122.36 bottom should be developing into a medium term move. Break of 38.2% retracement of 195.86 to 122.36 at 150.42 should pave the way to 61.8% retracement at 167.78. This will now be the favored case as long as 135.58 support holds.

Dollar Retreats Mildly, But Firm as Supported by Yield and Fed Expectations

Dollar retreats mildly today but remains the strongest major currency for the week. The greenback is firmly supported by expectation of a June Fed hike. And comments from Fed officials indicate that they are looking through the weakness in Q1 and maintain their preference on the policy path for the year. A total of three rate hikes is the base case and Fed will start shrinking the balance sheet by the end of the year. This expectation is also reflected in treasury yields. 10 year yield rose 0.031 to close at 2.407 overnight, above 2.391 near term resistance. The development now opens up the case for a retest of March high at around 2.62. Meanwhile, Swiss Franc and Japanese Yen remain the weakest ones as political risks in Europe eased.

Kansas City Fed George and Dallas Fed Kaplan support more accommodation removal

Kansas City Fed President Esther George said yesterday the US economy is on track to grow at "a slightly above-trend rate". And, weakness in Q1 didn't change her view on that. She noted that "all told, while the recent GDP report and auto sales may be flashing yellow, numerous other indicators remain solid green." Hence, "continuing the gradual removal of monetary accommodation is the appropriate course for the Fed." Also, FOMC "must begin to adjust the size and composition of its securities holdings" later in the year. And, "once it begins, however, the runoff in the portfolio should be on autopilot and not reconsidered at each subsequent Fed meeting."

Dallas Fed President Robert Kaplan said that "the base case for removal of accommodation is three times this year". He also noted that he is "very cognizant of the fact that inflation pressures have been more muted." But he sees risks as "pretty balanced" and "it could easily be the case that the economy will unfold in a stronger way than I expect and we could do more."

NIESR: No BoE move before completing Brexit deal

In UK, the National Institute of Economic and Social Research said that BoE won't chance its monetary policies before conclusion of Brexit negotiation with EU. NIESR head of macroeconomic modeling and forecasting Simon Kirbay said that "we assume that interest rates remain unchanged until we exit the European Union." And, "if the chance of a transitional deal does begin to materialize, it might well be that the Bank of England brings forward the point at which it raises interest rates, but at the moment, that doesn't appear to be on the cards." In a report published today, NIESR left 2017 and 2018 UK growth forecast unchanged, at 1.7% and 1.9% respectively. Inflation is projected to peak at 3.4% at the end of 2017. BoE will have its Super Thursday tomorrow and is widely expected to keep monetary policies unchanged.

BoJ might release calculations on impact of stimulus exit

BoJ Governor Haruhiko Kuroda said today that BoJ might release the details of the study of stimulus withdrawal and the impact on its balance sheet. And he emphasized that "it is very important to explain in easy-to-understand terms how monetary policy could affect the BOJ's financial health". Regarding monetary policies, Kuroda said that he's "not thinking about changing the policy mix right now". And "the amount of our bond purchases may vary depending on financial market conditions at the time. But this has no implications for monetary policy going forward." Regarding the economy, Kuroda said that "while global economic growth is gaining momentum, various uncertainties remain".

China CPI accelerated

China's headline CPI accelerated to 1.2% yoy in April, up from 0.9% a month ago, as mainly driven by the recovery of food disinflation. Food price contracted -3.5% yoy, following a -4.4% drop in March. Non-food inflation rose to 2.4% yoy in April from 2.3% a month ago. Core inflation (excluding food and energy) improved to 2.1% yoy from 2% in March. Such level should be in line with the government's target. PPI moderated to 6.4% in April from 7.6% in March. The deceleration came in more than expectations. A key contributor to the slowdown was commodity prices which slowed further in April as low base effects dissipated. Global prices also pulled back after the strong rally earlier in the year.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 146.62; (P) 147.25; (R1) 148.06; More....

GBP/JPY's rally extends to as high as 147.86 so far and intraday bias remains on the upside for 148.20 resistance. As noted before, whole rally should 122.36 is resuming. Break of 148.20 will target 150.42 long term fibonacci level first. Break there will pave the way to 100% projection of 122.36 to 148.42 from 135.58 at 161.64. On the downside, below 145.64 minor support will turn bias neutral and bring consolidation before staging another rise.

In the bigger picture, based on current momentum, rise from 122.36 bottom should be developing into a medium term move. Break of 38.2% retracement of 195.86 to 122.36 at 150.42 should pave the way to 61.8% retracement at 167.78. This will now be the favored case as long as 135.58 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BOJ Summary of Opinions at April 26-27 Meeting | ||||

| 1:30 | CNY | CPI Y/Y Apr | 1.20% | 1.10% | 0.90% | |

| 1:30 | CNY | PPI Y/Y Apr | 6.40% | 6.70% | 7.60% | |

| 5:00 | JPY | Leading Index Mar P | 105.5 | 104.8 | ||

| 12:30 | USD | Import Price Index M/M Apr | 0.20% | -0.20% | ||

| 14:30 | USD | Crude Oil Inventories | -0.9M | |||

| 18:00 | USD | Monthly Budget Statement Apr | -176.2B | |||

| 21:00 | NZD | RBNZ Rate Decision | 1.75% | 1.75% |

The Crude Oil War Everyone Keeps Talking About Just Arrived

Key Points:

- WTI benchmark prices remain under pressure around $46.11 a barrel.

- Nigerian production likely to expand with refinery investment.

- OPEC needs to determine an effective strategy lest oil continues to decline.

Crude oil has had to travel a highly rocky path over the past few weeks as the commodity has been beset by ongoing concern over the growing glut of supply.Subsequently, WTI prices have slumped fairly convincingly over the past few weeks with the benchmark currently trading around the $46.11 a barrel mark. However, with both sides of the battle readying for action, things could be about to get a lot worse for crude prices.

A war between OPEC and U.S. shale producers has clearly been brewing for some time with the upstart shale plays attempting to eat into the cartel's market share. At the time, OPEC's primary strategy was to run out the clock on the shale industry by increasing supply and pushing prices below their marginal cost of extraction and thereby make much of the sector unprofitable. However, as proof that the law of unintended consequences reigns supreme, the U.S. oil industry responded by increasing R&D budgets and finding new, and cheaper, alternatives to extracting shale oil. Subsequently, OPEC now faces fighting a rear guard action as the Shale Industry continues to increase their rig count and productive output.

In addition, the latest market news seems to suggest that Nigeria, Africa's largest oil producer, is now building new refineries to revitalise their industry and allow Lagos to increase their supply output. This poses an additional nail in OPEC's strategy of cohesion and supply reduction and further complicates the cartels direction on cuts.

The reality is that with shale oil's marginal extraction costs constantly falling the time is now for OPEC to pounce and drive some concerted action to rebalance the oil market. In fact, rather than cutting prices, which only seeks to shed market share to the U.S. and Canadian producers, the cartel needs to rapidly expand production and drive the price to historic lows. As difficult as such a move would be, it would cause havoc within the U.S. and Canadian sectors and force an urgent re-balancing of markets.

Obviously, any such move would be fraught with the danger of splintering amongst the various OPEC members, as well as adding to global deflationary pressures. Additionally, there is also plenty of political risk given that many of the Middle Eastern nations rely upon buoyant oil revenues to effectively balance their books. However, without some drastic action the cartel will only continue to diminish in power and it's hard to see how they can effectively fight of the technologically superior shale and oil sand sector.

Ultimately, whichever way OPEC chooses to go will be a difficult battle but it's clear that the war has started and won't let up until either side fires their last shot. Regardless, depressed crude oil prices are likely here to stay for at least the medium term whilst the battle continues to rage.

EURCHF Poised To Tumble

Key Points:

- Post-election rally is running short on momentum.

- Technical bias is moving towards bearish.

- Losses could extend to the 1.09 handle.

Some strong buying pressure over the past 48 hours has put the EURCHF in a rather precarious position which suggests a correction is now on the cards. Indeed, we are seeing a number of important technical signals beginning to shift to bearish which could see even the 1.09 handle challenged within a number of sessions.

Firstly, and probably most obviously, the proximity of the pair to the 1.0979 mark should have a few alarm bells ringing for the bulls. This price has repeatedly proven itself to be a point of inflection for the EURCHF and we have no real reason to doubt that this latest challenge will be met with a similar fate to those seen previously. What’s more, the presence of the long-term descending trend line is bound to work against the bulls and encourage the bears to wrest control back from their counterparts.

However, we can also look to a number of other instruments to support our bias as they are also highly suggestive of a near-term slide for the EURCHF. In particular, the stochastic and RSI oscillators paint a clear picture of what is likely to be next. Specifically, both instruments are deeply overbought territory which would typically indicate that selling pressure is set to pick up as the bulls exhaust themselves. Moreover, the Bollinger bands are highly divergent which drastically limits chances of a second breakout taking place.

Once momentum has reversed, we expect to see losses extend to around the 1.09 handle within a week or so. Currently, expectations are that this support remains intact in the absence of a major fundamental upset for a number of reasons. For one, it coincides with the 23.6% Fibonacci level. However, a more compelling reason to suggest that the level will hold is due to the fact that this price has also been a historical reversal point on numerous occasions.

Ultimately, upside risks are looking very limited moving forward and the downside risks are multiplying at a notable rate. Furthermore, given the recent uptick in volatility, any correction to the downside could be more severe than we would normally forecast so don’t get caught out by being late to the party or by ignoring the deteriorating technical bias.

Aussie Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the AUD declined 0.49% against the USD and closed at 0.7347.

LME Copper prices rose 0.6% or $30.0/MT to $5496.0/MT. Aluminium prices declined 0.3% or $5.0/MT to $1874.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7353, with the AUD trading 0.08% higher against the USD from yesterday's close.

On the macro front, in China, Australia's largest trading partner, the consumer price index (CPI) advanced 1.2% on an annual basis in April, exceeding market expectations for a gain of 1.1%. In the previous month, the CPI had registered a rise of 0.9%. Meanwhile, the nation's producer price index (PPI) climbed less-than-expected by 6.4% YoY in April, compared to market consensus for an increase of 6.7%. The PPI had risen 7.6% in the previous month.

The pair is expected to find support at 0.7330, and a fall through could take it to the next support level of 0.7306. The pair is expected to find its first resistance at 0.7373, and a rise through could take it to the next resistance level of 0.7392.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

German Exports And Imports Hit Record High Level In March

For the 24 hours to 23:00 GMT, the EUR declined 0.39% against the USD and closed at 1.0880.

On the economic front, Germany's seasonally adjusted trade surplus widened more-than-expected by €25.4 billion in March, as both exports and imports surged to a record high level, thus pointing towards robust overseas and domestic demand. The nation registered a revised surplus of €20.0 billion in the previous month, while markets expected the nation's surplus to widen to a level of €21.5 billion. Additionally, the nation's exports rose more-than-anticipated by 0.4% on a monthly basis in March, compared to a revised rise of 0.9% in the previous month. Further, imports sharply rebounded by 2.4% MoM in March, compared to a drop of 1.6% in the previous month.

On the other hand, the nation's seasonally adjusted industrial production fell 0.4% MoM in March, lower than market expectations for a fall of 0.7%. Industrial production had registered a revised rise of 1.8% in the prior month.

Macroeconomic data released in the US indicated that JOLTs job openings climbed more-than-expected to a level of 5743.0K in March, compared to a revised reading of 5682.0K in the prior month, while investors had envisaged for a rise to a level of 5725.0K. Moreover, the nation's final wholesale inventories surprisingly climbed 0.2% in March, compared to a drop of 0.1% in the preliminary print. In the prior month, the wholesale inventories had registered a rise of 0.4%. Meanwhile, the nation's NFIB small business optimism index eased less-than-anticipated to a level of 104.5 in April, compared to a level of 104.7 in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.0891, with the EUR trading 0.1% higher against the USD from yesterday's close.

The pair is expected to find support at 1.0857, and a fall through could take it to the next support level of 1.0823. The pair is expected to find its first resistance at 1.0929, and a rise through could take it to the next resistance level of 1.0967.

Going forward, market participants will draw their attention to a speech by the European Central Bank (ECB) President, Mario Draghi, in Dutch Parliament, scheduled in a few hours. Also, the US monthly budget statement for April and MBA mortgage applications data, slated to release later today, will garner significant amount of market attention.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.