Sample Category Title

Currencies: Dollar Rebounds

Sunrise Market Commentary

Rates: Core bonds lose ground, but be aware of risk sentiment

With French election risk out of the way, focus may shift to the potentially key June ECB and Fed meetings. Anticipation on hawkish outcomes could push the German and US yields back higher The fragile picture of commodity markets, historically low volatility, and record equity prices are a risk scenario which could lift safe haven assets in case of a risk-off correction.

Currencies: Dollar rebounds

Yesterday, the dollar captured a better bid. EUR/USD fell prey to profit taking after the Macron victory. USD/JPY profited from the resilience of US equities and a rise in US yields. Today, the eco calendar is thin. Some further pro-USD repositioning might be on the cards.

The Sunrise Headlines

- US stocks closed flat yesterday, after Apple shares surged to an all-time high and the Vix index closed at its lowest point since 1993. Overnight, Asian stock markets trade mixed.

- The Australian dollar eased to four-month lows after disappointing retail sales (-0.1% M/M) figures reinforced expectations of steady interest rates for months to come.

- German production fell a smaller-than-expected 0.4% in March (expected -0.7% M/M), but February production was slightly downwardly revised to 1.8% from 2.2%. It confirms strong activity in Germany. The trade surplus widened to €25.4B from 20B previously, even as exports lagged imports.

- Saudi Arabia's oil minister said that oil producers would "do whatever it takes" to rebalance the market and that he expected a global deal on cutting crude output to be extended to the end of 2017 or possibly longer.

- The former head of the US Department of Justice told Congress that she had warned the White House in January that Michael Flynn, the first national security adviser appointed by Donald Trump, could be blackmailed by Russia.

- South Koreans headed to voting stations today to elect a new leader, looking to move on from a corruption scandal that brought down former President Park Geun-hye and shook the political and business elite to the core.

- Today's eco calendar remains thin with only US NFIB small business optimism. Austria, the Netherlands, Germany (inflation-linked) and the US tap the market. Fed governors Kashkari, Rosengren and Kaplan are scheduled to speak.

Currencies: Dollar Rebounds

Dollar rebounds as euro rally runs into resistance

On Monday, a buy-the-rumour, sell-the-fact correction after Macron's victory caused a modest reversal on earlier EUR/USD, EUR/JPY and USD/JPY gains. EUR/USD tested the 1.10 level in Asia, but declined throughout the session and closed at 1.0924. The European equity correction initially also weighed on USD/JPY, but the pair found a better bid as US equities were very resilient and USD bond yields reversed an early decline. USD/JPY finished at 113.26 (from 112.76 on Friday).

Overnight, Asian equity markets trade narrowly mixed in the absence of new eco info. EUR/USD stabilizes in the 1.0930 area. USD/JPY maintains yesterday's gains and trades in the 113.30 area. Of late, price declines in several industrial commodities weighed on the Aussie dollar. Today, a domestic factor, disappointing retail sales, were to blame for a further AUD/USD to the 0.7355 area.

Today, the US calendar only contains the JOLTS Job Openings and the NFIB small business confidence, no market movers. We expect them to come out at healthy levels. Various Fed governors will speak on non-monetary policy themes. Ultrahawk George, on the contrary, speaks on the balance of economic risks and monetary policy. She might warn that the Fed risks to be behind the curve, but she's an outsider inside the FOMC and her comments shouldn't carry much weight. So, little guidance for USD trading today.

Yesterday, the euro fell prey to post-Macron profit taking. At the same time, the dollar was in good shape as US equities outperformed Europe and as US yields maintained an upward bias. The post-Macron equity correction shouldn't go far. This might continue to support USD/JPY. For EUR/USD the picture remains indecisive. Markets are still looking for signs that the ECB will change its communication at the June meeting. The euro recently already anticipated on such a scenario. If there is no additional news on this issue, the euro rally might (temporary) slow. At the same time, the downside of the dollar is becoming better protected. So, some further technical correction in EUR/USD toward to the 1.0821 (Spike higher after first round victory of Macron) is likely.

From a technical point of view, USD/JPY bottomed out in April and regained the 112.20 resistance last week. This improved the technical picture. The rebound continues in a gradual way, but looks quite robust. Next intermediate resistance comes in at 115.51. EUR/USD extensively tested the topside of the MT range (1.0874/1.0906 area) late March. The pair returned to the range top after the first round of the French election and broke above the 1.09/1.0950 resistance at the end of last week. However, the break isn't confirmed. A sustained break would improve the ST picture. Next resistance stands at 1.1129 (62% retracement) and at 1.1366 (correction top). A decline below 1.0821 would suggest that the dollar is regaining traction against the euro. A ST EUR/USD correction might occur as the pair is unwinding overbought conditions.

R/USD topside test again rejected. Some further post-Macron correction might be on the cards

EUR/GBP

EUR/GBP joins post-Macron euro correction

The global post-Macron reaction dominated UK trading yesterday. EUR/GBP corrected south and finished the session at 0.8442 (from 0.8473). The decline of EUR/USD (relative strength of the dollar) weighted slightly on cable. The pair dropped to the 1.2930 area and closed the session at 1.2940.

Overnight, the UK BRC like-for-like sales rebounded by an impressive 5.6% Y/Y (from -1.0% Y/Y in March). However, the figure was probably distorted by the timing of Easter. Sterling's reaction remained limited. There are no important eco data on the agenda today. Technical considerations will prevail for sterling trading. Markets will look forward to the BoE's policy meeting and the quarterly inflation report (Thursday). We don't expect the BoE to herald a big change before the Parliamentary election. Soft Q1 growth gives the BoE the room not to hurry to signal a rate hike anytime soon.

Two weeks ago, EUR/GBP dropped below EUR/GBP 0.84 support, (temporary) improving the sterling picture. The pair came within reach of key 0.8305 support (Dec low), but no real test occurred. After a late April EUR/GBP rebound, the range bottom is better protected. Longer term, Brexit-complications remain potentially negative for sterling. On technical considerations we slightly prefer a EUR/GBP buy-on-dips approach.

EUR/GBP: trading within a tight 0.83/0.85 range

Market Update – Asian Session: Aussie Retail Sales Disappoint While Japan Wage Inflation Shrinks

US Session Highlights

(US) Apr Labor Market Conditions Index Change: 3.5 v 1.0e

(US) April Conference Board Employment Trends: 132.64 v 131.58 in March

(US) Fed's Bullard (non-voter, dovish): Fed's current policy rate setting is appropriate; US economy looks like it's in a low growth state

(US) Fed’s Mester (hawkish, non-voter): actions must be taken before Fed policy goals are fully met; reiterates calls for further rate hikes and trimming balance

(US) New York Fed Consumer Expectations Apr survey: households expecting finances to improve rises to 44%; April inflation expectations 3 years ahead to 2.9% v 2.7% prior

The S&P touched new all-time highs before retreating and closing flat on the day. The VIX reached lows not seen since 1993, dropping 8% to 9.7. The outperforming S&P sector was energy, thanks to higher oil prices, rising 0.8%.

US markets on close: Dow flat, S&P500 flat, Nasdaq flat

Best Sector in S&P500: Energy

Worst Sector in S&P500: Materials

Biggest gainers: NWL +11.9%; CTL +5.1%; COH +4.8%

Biggest losers: TSN -6.1%; LYB -4.0%; INCY -3.8%

At the close: VIX 9.8 (-0.8pts); Treasuries: 2-yr 1.33% (flat), 10-yr 2.38% (+2bps), 30-yr 3.01% (+3bps)

US movers afterhours

MAR Reports Q1 $1.01 v $0.90e, R$5.56B v $4.91Be; +4.9% afterhours

BLDR Reports Q1 $0.11 v $0.05e, R$1.53B v $1.49Be; Adjusted EBITDA $76.1M v $61.8M y/y; gross margin 24.5% v 25.0% y/y; +4.8% afterhours

P Reports Q1 -$0.24 v -$0.34e, R$316M v $318Me; Announces $150M investment by KKR; Confirms ongoing strategic review; +3.2% afterhours

BKD Reports Q1 -$0.68 (GAAP*) v $0.48e, R$1.22B v $1.21Be; +2.9% afterhours

OTEX Reports Q3 $0.45 v $0.53e, R$593M v $608Me; raises dividend 15% to $0.132 from $0.115 (indicated yield 1.52%); Operating margin 29.1% v 31.4% y/y; -9.7% afterhours

NVRO Reports Q1 -$0.50 v -$0.26e, R$68.4M v $68.1Me- Affirms FY17 R$31-320M v $318Me (prior $310-320M); -14.5% afterhours

HTZ Reports Q1 -$1.61 v -$1.00e, R$1.92B v $1.89Be; International car rental rev $411M, -5% y/y; US car rental rev $1.35B, -4% y/y; -17.7% afterhours

Key economic data

(JP) JAPAN MAR LABOR CASH EARNINGS Y/Y: -0.4% (biggest decline in 21 months) V 0.5%E ; REAL EARNINGS (EX-INFLATION) Y/Y: -0.8% V 0.0% PRIOR

(AU) AUSTRALIA MAR RETAIL SALES M/M: -0.1% (2nd straight decline) V +0.3%E; Q/Q ex-inflation: +0.1% V 0.5%E

(NZ) ANZ: New Zealand Apr non-tradable inflation m/m 0.0% v 0.2% prior, y/y: 2.2% v 2.2% prior

Asia Session Notable Observations, Speakers and Press

Asia indices mixed after a flat day on Wall St where S&P500 hit record intraday high and Vix saw a multi-year low. Australia underperforming ahead of the release of its FY17/18 budget, with retailers slumping on much weaker than expected Aussie Retail Sales. CBA shares also trading lower following Q3 results. AUD/USD fell nearly 40pips toward 0.7350 on the release.

Japan wage inflation posted its biggest y/y decline in nearly 2 years, and BOJ Gov Kuroda noted central bank is prepared to do more policy adjustment if needed, sending USD/JPY pair to session highs near 113.40.

China press speculated Terms of Trade could turn to deficit this year on rising imports following overnight Apr Trade data. CASS researchers also warned new home prices may decline amid property curbs.

China

(CN) China's NDRC said to plan a meeting with power companies about coal quality - press

(CN) China Passenger Car Association (PCA): Jan-Apr vehicle sales 7.27M units, -1.7% y/y

(CN) China Academy of Social Sciences (CASS): New home prices may fall in 2017 - press

(CN) China may see Terms of Trade at a deficit this year amid growth in Imports - Chinese press

Japan

(JP) Moody's: Japan to become more sensitive to BOJ recalibrations

(JP) BOJ Gov Kuroda: Reiterates Japan’s virtuous economic cycle is strengthening

Australia/New Zealand

(AU) Australia Foreign Investment Review Board (FIRB): Investment gains mainly driven by real estate

(AU) Australia Govt considering a levy on big four banks under new budget - Australian press

(NZ) NZIER's Shadow Board: RBNZ should adopt tightening bias

Asian Equity Indices/Futures (01:00ET)

Nikkei -0.1%, Hang Seng +0.3%, Shanghai Composite flat, ASX200 -0.6%, Kospi closed

Equity Futures: S&P500 flat; Nasdaq flat, Dax -0.1%, FTSE100 -0.1%

FX ranges/Commodities/Fixed Income (01:00ET)

EUR 1.0920-1.0935; JPY 113.15-113.40; AUD 0.7352-0.7398; NZD 0.6900-0.6925

June Gold +0.1% at 1,228/oz; June Crude Oil +0.1% at $46.47/brl; July Copper -0.4% at $2.48/lb

SPDR Gold Trust ETF daily holdings fall 1.2 tonnes to 851.9 tonnes; 4th straight decline

(CN) PBOC SETS YUAN MID POINT AT 6.9037 V 6.8947 PRIOR

(CN) PBOC skips open market operations (3rd straight skip)

(JP) Japan MoF sells ¥2.08T v ¥2.3T offered in 10-year 0.1% JGBs; Avg yield: 0.030% v 0.064% prior; bid to cover: 3.76x v 3.96x prior

(AU) Australia MOF sells A$150M in 2030 bonds; avg yield 0.8288%; bid-to-cover 3.10x

Asia equities notable movers

Australia

Incitec Pivot (IPL) +2.9%; H1 result

Commonweath Bank (CBA) -3.6%: Q3 resut

Beach Energy (BPT) -0.7%; interest in AWE (AWE +5.6%)

JB Hi Fi (JBH) -4.8%, Harvey Norman (HVN) -3.7%; Australia retail sales

Japan

IHI (7013) +3.8%, FY16/17 result

Mitsubihi Heavy (7011) +0.5%, FY16/17 result

TEPCO (9501) +3.3%; To set retail gas prices as much as ~8% cheaper than Tokyo Gas f

Subaru (7270) -3.8%; FY16/17 result

United Arrows (7606) -5.8%; FY16/17 result

Hong Kong

Longfor Properties (960) +0.2%; Apr result

Great Wall Motor (2333) -0.1%; Apr sales

International Entertainment (1009) +0.6%; FY guidance

Daily Technical Outlook And Review: EUR/USD, GBP/USD, AUD/USD, USD/JPY, USD/CAD, USD/CHF, DOW 30, GOLD

A note on lower timeframe confirming price action...

Waiting for lower timeframe confirmation is our main tool to confirm strength within higher timeframe zones, and has really been the key to our trading success. It takes a little time to understand the subtle nuances, however, as each trade is never the same, but once you master the rhythm so to speak, you will be saved from countless unnecessary losing trades. The following is a list of what we look for:

- A break/retest of supply or demand dependent on which way you're trading.

- A trendline break/retest.

- Buying/selling tails ... essentially we look for a cluster of very obvious spikes off of lower timeframe support and resistance levels within the higher timeframe zone.

- Candlestick patterns. We tend to only stick with pin bars and engulfing bars as these have proven to be the most effective.

EUR/USD

As anticipated, the single currency shook hands with the large psychological number 1.10/ H4 161.8% Fib ext. at 1.1007 drawn from the low 1.0851 and sold off. Bolstering this area was not only two weekly 127.2% Fib extensions at 1.1016/1.0954 (red zone) taken from the lows 1.0340/1.0493, but also a daily trendline resistance extended from the high 1.1616. Well done to any of our readers who managed to jump aboard here!

With the H4 mid-level support at 1.0950 now out of the picture, price is currently seen teasing a H4 trendline support etched from the high 1.0947. Also of note is May’s opening level pegged just below at 1.0902/psychological handle 1.09.

Our suggestions: Attempting to join the bearish momentum seen from the above said higher-timeframe structures is chancy given we have the following supports (green area) in view:

- May’s opening level pegged just below at 1.0902/psychological handle 1.09.

- 2016 yearly opening level at 1.0873 (see weekly chart).

- Daily support at 1.0850.

On account of this, we now favor longs. However, we will not become buyers in this market UNTIL we witness a reasonably sized bullish rotation candle form within the noted green zone (preferably a full-bodied candle).

Data points to consider: FOMC member Kaplan speaks at 9.15pm GMT+1.

Levels to watch/live orders:

- Buys: 1.0850/1.09 ([waiting for a reasonably sized H4 bull candle [preferably a full-bodied candle] to form before pulling the trigger is advised] stop loss: ideally beyond the candle’s tail).

- Sells: Flat (stop loss: N/A).

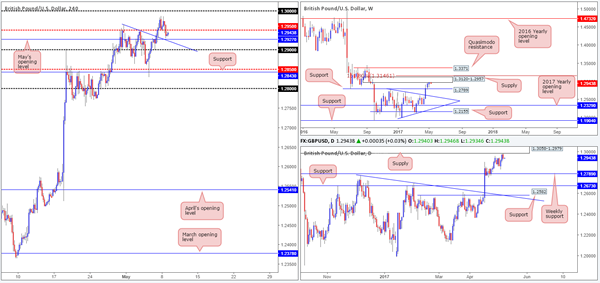

GBP/USD

As can be seen from the H4 chart, price was unable to sustain gains beyond the mid-level resistance 1.2950 during yesterday’s segment. This move was likely influenced by the fact that both weekly and daily action are currently seen trading at the underside of supplies at the moment (1.3120-1.2957/1.3058-1.2979).

Despite this, the downside to this market looks incredibly limited. There’s a H4 trendline support extended from the high 1.2965, May’s opening level at 1.2927 and the nearby round number at 1.29 to contend with!

Our suggestions: In the absence of clearer price action, opting to stand on the sidelines may very well be the better path to take today.

Data points to consider: FOMC member Kaplan speaks at 9.15pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

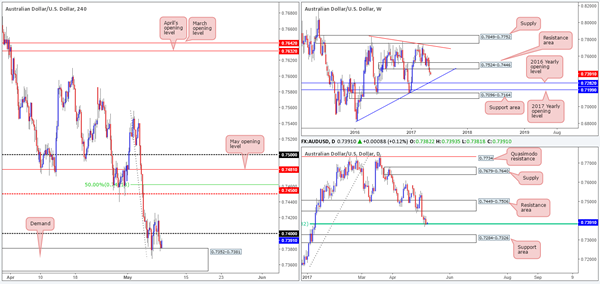

AUD/USD

Coming in from the top this morning, we can see that weekly bears continue to push this market lower after breaking through the support zone at 0.7524-0.7446. Should this momentum continue, it’s likely that the trendline support extended from the low 0.6827 and 2016 yearly opening level at 0.7282 will be brought into the picture.

Down on the daily candles, the long-term 61.8% Fib’ support at 0.7832 (drawn from the low 0.7159) appears to be on the verge of giving way. A violation of this hurdle will bring the support area at 0.7284-0.7326 into view, which intersects beautifully with the above noted weekly trendline support and sits just above the 2016 yearly opening level.

Jumping across to the H4 chart, the buyers and sellers have been seen battling for position around the 0.74 handle since Thursday last week. Also noteworthy here is the demand coming in at 0.7352-0.7381.

Our suggestions: Despite the H4 chart showing demand in play, the higher-timeframe structures suggest that this market may be headed lower. With that said, this places traders in a rather precarious position: sell into H4 demand or buy into potential higher-timeframe flow?

As far as we can see, technical elements are mixed at the moment leaving us with little choice but to remain flat for now.

Data points to consider: Aussie retail sales figures at 2.30am, Aussie Annual budget release at 10.30am. FOMC member Kaplan speaks at 9.15pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

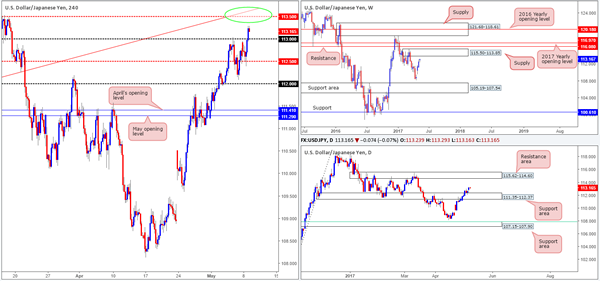

USD/JPY

USD/JPY bulls went on the offensive yesterday and pulled the H4 candles above the 113 handle. Consequent to this, the H4 mid-level resistance at 113.50 is now in sight, which happens to intersect nicely with a H4 trendline resistance pegged from the low 111.68 (green circle).

Although 113.50 is a possible sell zone, traders might want to take into consideration that the weekly candles show room to advance up to the supply area at 115.50-113.85. This – coupled with daily action also showing room to stretch up to a resistance area coming in at 115.62-114.60, signals potential weakness around 113.50!

Our suggestions: Instead of looking to short from 113.50, our team’s focus is on buying any retest seen off the 113 handle. Be that as it may, before our desk commits here, we’d need to see a reasonably sized H4 bull candle form following the retest – ideally a full-bodied candle. Frist take-profit target would, of course, be 113.50, followed by the underside of weekly supply at 113.85.

Data points to consider: FOMC member Kaplan speaks at 9.15pm GMT+1.

Levels to watch/live orders:

- Buys: 113 region ([waiting for a reasonably sized H4 bull candle [preferably a full-bodied candle] to form before pulling the trigger is advised] stop loss: ideally beyond the candle’s tail).

- Sells: Flat (stop loss: N/A).

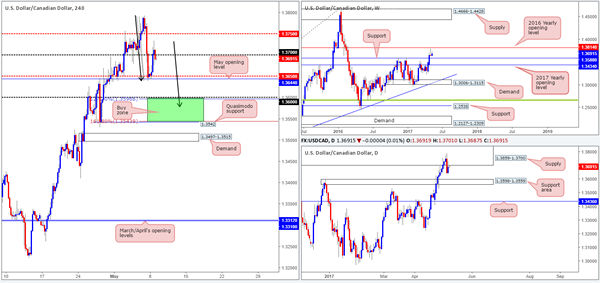

USD/CAD

In recent trading, the pair managed to recover well from May’s opening level at 1.3644/H4 mid-level support at 1.3650. However, the 1.37 handle has so far proven to be a bit of a challenge to overcome. What’s also notable from a technical perspective, however, is the possible H4 AB=CD structure taken from the high 1.3793 (black arrows). Although the 1:1 pattern terminates just below the 1.36 handle, a bullish rotation from here is still highly likely. Note the daily support area coming in at 1.3598-1.3559 and the weekly support level drawn from 1.3588!

Our suggestions: Quite simply, our team is looking for long opportunities between the 127.2/161.8% AB=CD Fib’ extensions at 1.3542/1.36 today. In an ideal world, we’d want to see a reasonably sized H4 full-bodied bull candle form within this green zone. The reason we require additional confirmation here is to avoid the possibility of getting stopped out on any fakeout seen to the H4 demand planted below at 1.3497-1.3515.

Data points to consider: FOMC member Kaplan speaks at 9.15pm GMT+1.

Levels to watch/live orders:

- Buys: 113 region ([waiting for a reasonably sized H4 bull candle [preferably a full-bodied candle] to form before pulling the trigger is advised] stop loss: ideally beyond the candle’s tail).

- Sells: Flat (stop loss: N/A).

USD/CAD

In recent trading, the pair managed to recover well from May’s opening level at 1.3644/H4 mid-level support at 1.3650. However, the 1.37 handle has so far proven to be a bit of a challenge to overcome. What’s also notable from a technical perspective, however, is the possible H4 AB=CD structure taken from the high 1.3793 (black arrows). Although the 1:1 pattern terminates just below the 1.36 handle, a bullish rotation from here is still highly likely. Note the daily support area coming in at 1.3598-1.3559 and the weekly support level drawn from 1.3588!

Our suggestions: Quite simply, our team is looking for long opportunities between the 127.2/161.8% AB=CD Fib’ extensions at 1.3542/1.36 today. In an ideal world, we’d want to see a reasonably sized H4 full-bodied bull candle form within this green zone. The reason we require additional confirmation here is to avoid the possibility of getting stopped out on any fakeout seen to the H4 demand planted below at 1.3497-1.3515.

Data points to consider: FOMC member Kaplan speaks at 9.15pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 1.0016/1.0000 ([waiting for a reasonably sized H4 bear candle [preferably a full-bodied candle] to form before pulling the trigger is advised] stop loss: ideally beyond the candle’s wick).

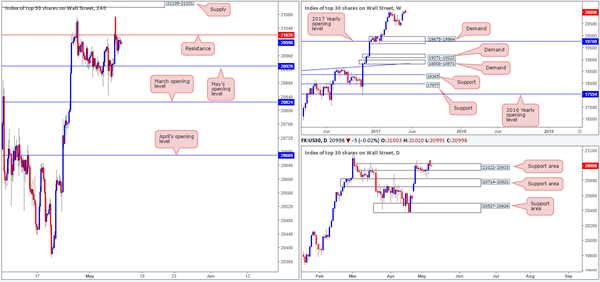

DOW 30

According to daily structure, the resistance area at 21022-20933 could very soon become a zone of support. In the event that this does come to fruition, we’re confident that the index will look to punch to fresh record highs. However, the H4 candles remain capped beneath the resistance level pegged at 21020 for now. This line and the nearby supply zone seen above it at 21139-21101 are, in our opinion, the only barriers now stopping the DOW from popping higher.

Our suggestions: Given where price is positioned on the weekly and daily charts, we do eventually expect the unit to punch higher and continue trending northbound. Nevertheless, we will not become buyers in this market until we witness a decisive H4 close beyond the current H4 supply zone.

Data points to consider: FOMC member Kaplan speaks at 9.15pm GMT+1.

Levels to watch/live orders:

- Buys: Once the H4 supply at 21139-21101 is taken out, longs will be permitted.

- Sells: Flat (stop loss: N/A).

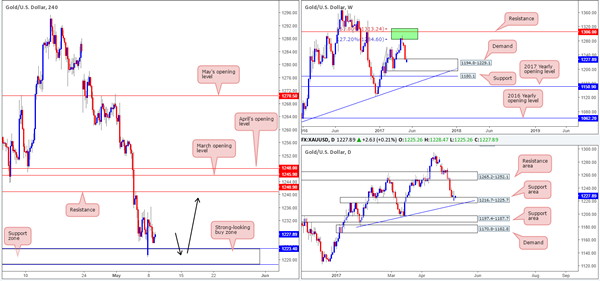

GOLD

Kicking this morning’s report off with a look-see at the weekly timeframe, we can see that the bulls are beginning to make an appearance from within the walls of demand coming in at 1194.8-1229.1. Along the same lines, daily action remains trading around a support zone coming in at 1216.7-1225.7. Therefore, higher-timeframe structure favors the bulls at this point.

Over on the H4 chart, the H4 support zone at 1218.5-1223.4 (seen lodged within the limits of the said weekly and daily structures) remains intact after being tested during yesterday’s segment.

Our suggestions: In view of the bigger picture (see above), our desk remains biased to the upside. The H4 support area mentioned above is still on our radar for potential longs today. Ideally though, we’d want to see a reasonably sized H4 bull candle present itself here – a full-bodied candle would be perfect – before we commit. As for take-profit targets, the H4 resistance at 1240.9 still looks reasonable for partial profits.

Levels to watch/live orders:

- Buys: 1218.5/1223.4 ([waiting for a reasonably sized H4 bull candle to form before pulling the trigger is advised] stop loss: ideally beyond the candle’s tail).

- Sells: Flat (stop loss: N/A).

Daily Technical Analysis: EUR/USD Builds RW Reversal Pattern At 1.10 Resistance

Currency pair EUR/USD

The EUR/USD is building a rising wedge (RW) reversal chart pattern (red/blue) at the psychological round level of 1.10. Price has now reached the support line of the pattern which is a bounce or break zone. A bearish break could start a larger bearish correction whereas a bullish bounce could see price challenge the resistance (red) line.

The EUR/USD broke the mini support level (dotted blue) after bouncing at the 61.8% Fibonacci level of wave 2 (brown). The correction could be part of a 123 (brown) or ABC. The wave 4 (brown) is invalidated if price breaks above the 50% Fib of wave 4.

Currency pair GBP/USD

The GBP/USD has bounced at the resistance line (red) of the uptrend channel (red/green). A bullish break could see price move towards the Fibonacci targets of wave 5 (purple) whereas a bearish break could start a reversal.

The GBP/USD seems is building a bearish retracement within a potential wave 4 (grey), which would become invalidated if price manages to break below the top of wave 1 (green line).

Currency pair USD/JPY

The USD/JPY managed to break above the previous top and is now continuing with the uptrend channel towards the Fibonacci targets of wave 5 (brown).

The USD/JPY is extending the bullish 5th wave (brown/orange) after completing an ABC correction (grey) and breaking above the resistance trend lines (dotted orange).

European Open Briefing: Markets Reacted Positively To The Outcome Of The French Election

Global Markets:

- Asian stock markets: Nikkei gained 2.40 %, Shanghai Composite lost 0.90 %, Hang Seng rose 0.30 %, ASX 200 up 0.50 %

- Commodities: Gold at $1230 (+0.30 %), Silver at $16.47 (+1.20 %), WTI Oil at $46.80 (+1.20 %), Brent Oil at $49.75 (+1.30 %)

- Rates: US 10-year yield at 2.36, UK 10-year yield at 1.12, German 10-year yield at 0.42

News & Data

- China Trade Balance (USD) Apr: 38.05B Est. (35.20B), Prior (23.92B)

- China Exports (YoY) Apr: 14.3% Est. (16.80%), Prior (22.30%)

- China Imports (YoY) Apr: 18.6% Est. (29.30%), Prior (26.30%)

- Australia NAB Business Confidence Apr:13, Prior (6)

- Australia NAB Business Conditions Apr: 14, (Prior 14, revised 12)

- Australia Building Approvals (MoM) Mar: -13.4%, Est. (-4.00%), Prior (8.3%)

- Australia Building Approvals (YoY) Mar: -19.9%, Est. (-10%), Prior (-4.90%)

- PBoC Fixes USDCNY Reference Rate At 6.8947 (prev fix: 6.8884)

CFTC Positioning Data:

- EUR short 2K vs 21K short last week. Shorts trimmed by 19K

- GBP short 81K vs 91K short last week. Shorts trimmed by 10K

- JPY short 30K vs 27K short last week. Shorts increased by 3K

- CHF short 18K vs 17K short last week. Shorts increased by 1K

- CAD short 48K vs 43K short. Shorts increased by 5K

- AUD long 43K vs 43K long. Unchanged

- NZD short 12K vs 15K short last week. Shorts trimmed by 3K

Markets Update:

Markets reacted positively to the outcome of the French election. While it was already expected that the centrist candidate Macron will win, stock markets in Asia extended gains. European equities are likely to open higher as well, and a gain of at least 1 % seems likely in the German DAX and French CAC index.

The Euro declined overnight, after starting the trading day above 1.10. The Macron win was already priced in, which is why the currency run out of momentum. EUR/USD fell back to 1.0955. Nevertheless, the technical outlook remains positive and the pair should find strong support at 1.09 and 1.0870.

The safe havens JPY and CHF fell in Asia. Demand for precious metals is likely to remain weak in the short-term too, unless a new risk-off theme emerges in the market. Key resistance in Gold is seen at $1235.

Upcoming Events:

- 07:00 BST – German Factory Orders

- 09:30 BST – UK Halifax House Price Index

- 13:35 BST – FOMC Member Bullard speaks

The Week Ahead:

Tuesday, May 9th

- 02:30 BST – Australian Retail Sales

- 06:45 BST – Swiss Unemployment Rate

- 07:00 BST – German Trade Balance

- 14:00 BST – FOMC Member Kashkari speaks

- 15:00 BST – US JOLTs Job Openings

- 18:00 BST – FOMC Member Rosengren speaks

- 21:15 BST – FOMC Member Kaplan speaks

Wednesday, May 10th

- 02:30 BST – Chinese CPI

- 02:30 BST – Chinese PPI

- 07:45 BST – French Trade Balance

- 13:00 BST – ECB President Draghi speaks

- 15:30 BST – US Crude Oil Inventories

- 22:00 BST – RBNZ Rate Decision

- 22:00 BST – RBNZ Statement

- 23:00 BST – RBNZ Governor Wheeler speaks

Thursday, May 11th

- 00:50 BST – Japanese Current Account

- 07:00 BST – German WPI

- 08:15 BST – Swiss CPI

- 08:30 BST – SNB Chairman Jordan speaks

- 09:30 BST – UK Industrial Production

- 09:30 BST – UK Manufacturing Production

- 09:30 BST – UK Trade Balance

- 12:00 BST – Bank of England Rate Decision

- 12:00 BST – Bank of England Meeting Minutes

- 12:00 BST – Bank of England Inflation Report

- 13:30 BST – US Initial Jobless Claims

- 13:30 BST – US PPI

Friday, May 12th

- 07:00 BST – German GDP

- 10:00 BST – Euro Zone Industrial Production

- 13:30 BST – US Retail Sales

- 13:30 BST – US CPI

- 15:00 BST – US Michigan Consumer Sentiment

Australia’s Retail Sales Drop For The Second Straight Month In March

For the 24 hours to 23:00 GMT, the AUD declined 0.11% against the USD and closed at 0.7383.

LME Copper prices declined 1.2% or $64.5/MT to $5466.0/MT. Aluminium prices declined 1.5% or $28.0/MT to $1879.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7361, with the AUD trading 0.3% lower against the USD from yesterday's close, on the back of disappointing retail sales data in Australia.

Early morning data showed that Australia's seasonally adjusted retail sales unexpectedly dropped 0.1% on a monthly basis in March, declining for the second consecutive month and confounding market consensus for a rise of 0.3%. In the prior month, retail sales had fallen by a revised 0.2%.

The pair is expected to find support at 0.7334, and a fall through could take it to the next support level of 0.7307. The pair is expected to find its first resistance at 0.7406, and a rise through could take it to the next resistance level of 0.7451.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Investor Confidence Jumped To A Nearly 10-Year High Level In May

For the 24 hours to 23:00 GMT, the EUR declined 0.46% against the USD and closed at 1.0923.

On the data front, the Euro-zone's Sentix investor confidence index rose more-than-expected to a level of 27.4 in May, notching its highest level since July 2007, as investors grew optimistic about the region's current economic outlook and as worries over political populism across the Euro bloc ebbed. The index had registered a reading of 23.9 in the prior month, while investors had envisaged for an advance to a level of 25.2.

Elsewhere, in Germany, the seasonally adjusted factory orders advanced 1.0% MoM in March, rising for second straight month and surpassing market expectations for a gain of 0.7%. Factory orders had registered a revised gain of 3.5% in the previous month.

In the US, data indicated that the labour market conditions index climbed to a level of 3.5 in April, after recording a revised rise of 3.6 in the previous month and compared to market expectations for an advance to a level of 1.0.

In the Asian session, at GMT0300, the pair is trading at 1.0926, with the EUR trading marginally higher against the USD from yesterday's close.

The pair is expected to find support at 1.0895, and a fall through could take it to the next support level of 1.0865. The pair is expected to find its first resistance at 1.0976, and a rise through could take it to the next resistance level of 1.1027.

Moving ahead, market participants focus on Germany's trade balance and industrial production data, both for March, slated to release in a few hours. Moreover, in the US, final wholesale inventories and JOLTS job openings, both for March along with the NFIB small business optimism index for April, will be eyed by investors.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

UK’s House Prices Fell For The First Time In 3 Months In April

For the 24 hours to 23:00 GMT, the GBP declined 0.16% against the USD and closed at 1.2937.

In economic news, UK's Halifax house prices unexpectedly dropped 0.1% in April, compared to market consensus for a rise of 0.1%. In the previous month, house prices had registered a flat reading.

In the Asian session, at GMT0300, the pair is trading at 1.294, with the GBP trading slightly higher against the USD from yesterday's close.

Overnight data revealed that the nation's BRC retail sales across all sectors advanced 5.6% YoY in April, compared to a drop of 1.0% in the prior month, while market participants were anticipating for a gain of 0.5%.

The pair is expected to find support at 1.2916, and a fall through could take it to the next support level of 1.2893. The pair is expected to find its first resistance at 1.2974, and a rise through could take it to the next resistance level of 1.3009.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading Higher In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.39% against the JPY and closed at 113.26.

In the Asian session, at GMT0300, the pair is trading at 113.18, with the USD trading 0.07% lower against the JPY from yesterday’s close.

Early this morning, data showed that Japan’s labour cash earnings surprisingly dropped 0.4% on an annual basis in March, after registering a 0.4% gain in the previous month.

The pair is expected to find support at 112.57, and a fall through could take it to the next support level of 111.95. The pair is expected to find its first resistance at 113.59, and a rise through could take it to the next resistance level of 113.99.

Moving ahead, investors await the Bank of Japan’s (BoJ) summary of opinions report, slated to release overnight.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Swiss Franc Trading A Tad Higher This Morning, Ahead Of Swiss Unemployment Rate Data

For the 24 hours to 23:00 GMT, the USD rose 0.94% against the CHF and closed at 0.9985.

On the data front, Switzerland's total sight deposits climbed to a level of CHF573.1 billion in the week ended 05 May, from CHF571.4 billion in the previous week.

In the Asian session, at GMT0300, the pair is trading at 0.9982, with the USD trading marginally lower against the CHF from yesterday's close.

The pair is expected to find support at 0.9912, and a fall through could take it to the next support level of 0.9841. The pair is expected to find its first resistance at 1.0022, and a rise through could take it to the next resistance level of 1.0061.

Ahead in the day, all eyes will be on Switzerland's unemployment rate data for April.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.