Sample Category Title

Summary 12/16 – 12/20

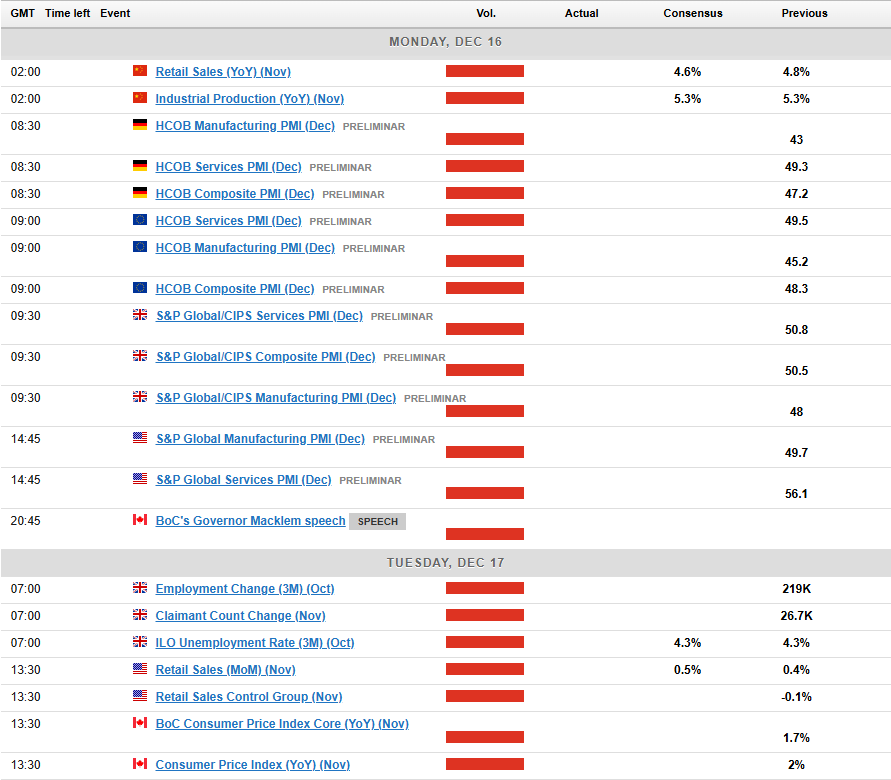

Monday, Dec 16, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Nov | 46 | |

| 22:00 | AUD | Manufacturing PMI Dec P | 49.4 | |

| 22:00 | AUD | Services PMI Dec P | 50.5 | |

| 23:50 | JPY | Machinery Orders M/M Oct | 1.20% | -0.70% |

| 00:30 | JPY | Manufacturing PMI Dec P | 49.2 | 49.0 |

| 00:30 | JPY | Services PMI Dec P | 50.5 | |

| 02:00 | CNY | Industrial Production Y/Y Nov | 5.30% | 5.30% |

| 02:00 | CNY | Retail Sales Y/Y Nov | 5.00% | 4.80% |

| 02:00 | CNY | Fixed Asset Investment (YTD) Y/Y Nov | 3.50% | 3.40% |

| 04:30 | JPY | Tertiary Industry Index M/M Oct | -0.10% | -0.20% |

| 07:30 | CHF | PPI M/M Nov | 0.20% | -0.30% |

| 07:30 | CHF | PPI Y/Y Nov | -1.80% | |

| 08:15 | EUR | France Manufacturing PMI Dec P | 43 | 43.1 |

| 08:15 | EUR | France Services PMI Dec P | 46.4 | 46.9 |

| 08:30 | EUR | Germany Manufacturing PMI Dec P | 43.8 | 43 |

| 08:30 | EUR | Germany Services PMI Dec P | 49.2 | 49.3 |

| 09:00 | EUR | Eurozone Manufacturing PMI Dec P | 45.3 | 45.2 |

| 09:00 | EUR | Eurozone Services PMI Dec P | 49.4 | 49.5 |

| 09:30 | GBP | Manufacturing PMI Dec P | 48.1 | 48 |

| 09:30 | GBP | Services PMI Dec P | 50.9 | 50.8 |

| 13:15 | CAD | Housing Starts Y/Y Nov | 246K | 241K |

| 13:30 | USD | Empire State Manufacturing Dec | 6.4 | 31.2 |

| 14:45 | USD | Manufacturing PMI Dec P | 49.4 | 49.7 |

| 14:45 | USD | Services PMI Dec P | 55.7 | 56.1 |

| 23:30 | AUD | Westpac Consumer Confidence Dec | 5.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Nov | |

| Forecast: | Previous: 46 | ||

| 22:00 | AUD | Manufacturing PMI Dec P | |

| Forecast: | Previous: 49.4 | ||

| 22:00 | AUD | Services PMI Dec P | |

| Forecast: | Previous: 50.5 | ||

| 23:50 | JPY | Machinery Orders M/M Oct | |

| Forecast: 1.20% | Previous: -0.70% | ||

| 00:30 | JPY | Manufacturing PMI Dec P | |

| Forecast: 49.2 | Previous: 49.0 | ||

| 00:30 | JPY | Services PMI Dec P | |

| Forecast: | Previous: 50.5 | ||

| 02:00 | CNY | Industrial Production Y/Y Nov | |

| Forecast: 5.30% | Previous: 5.30% | ||

| 02:00 | CNY | Retail Sales Y/Y Nov | |

| Forecast: 5.00% | Previous: 4.80% | ||

| 02:00 | CNY | Fixed Asset Investment (YTD) Y/Y Nov | |

| Forecast: 3.50% | Previous: 3.40% | ||

| 04:30 | JPY | Tertiary Industry Index M/M Oct | |

| Forecast: -0.10% | Previous: -0.20% | ||

| 07:30 | CHF | PPI M/M Nov | |

| Forecast: 0.20% | Previous: -0.30% | ||

| 07:30 | CHF | PPI Y/Y Nov | |

| Forecast: | Previous: -1.80% | ||

| 08:15 | EUR | France Manufacturing PMI Dec P | |

| Forecast: 43 | Previous: 43.1 | ||

| 08:15 | EUR | France Services PMI Dec P | |

| Forecast: 46.4 | Previous: 46.9 | ||

| 08:30 | EUR | Germany Manufacturing PMI Dec P | |

| Forecast: 43.8 | Previous: 43 | ||

| 08:30 | EUR | Germany Services PMI Dec P | |

| Forecast: 49.2 | Previous: 49.3 | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Dec P | |

| Forecast: 45.3 | Previous: 45.2 | ||

| 09:00 | EUR | Eurozone Services PMI Dec P | |

| Forecast: 49.4 | Previous: 49.5 | ||

| 09:30 | GBP | Manufacturing PMI Dec P | |

| Forecast: 48.1 | Previous: 48 | ||

| 09:30 | GBP | Services PMI Dec P | |

| Forecast: 50.9 | Previous: 50.8 | ||

| 13:15 | CAD | Housing Starts Y/Y Nov | |

| Forecast: 246K | Previous: 241K | ||

| 13:30 | USD | Empire State Manufacturing Dec | |

| Forecast: 6.4 | Previous: 31.2 | ||

| 14:45 | USD | Manufacturing PMI Dec P | |

| Forecast: 49.4 | Previous: 49.7 | ||

| 14:45 | USD | Services PMI Dec P | |

| Forecast: 55.7 | Previous: 56.1 | ||

| 23:30 | AUD | Westpac Consumer Confidence Dec | |

| Forecast: | Previous: 5.30% | ||

Tuesday, Dec 17, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 07:00 | GBP | Claimant Count Change Nov | 26.7K | |

| 07:00 | GBP | ILO Unemployment Rate (3M) Oct | 4.30% | 4.30% |

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Oct | 5.00% | 4.80% |

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Oct | 4.60% | 4.30% |

| 08:00 | CHF | SECO Economic Forecasts | ||

| 09:00 | EUR | Germany IFO Business Climate Dec | 85.6 | 85.7 |

| 09:00 | EUR | Germany IFO Current Assessment Dec | 84 | 84.3 |

| 09:00 | EUR | Germany IFO Expectations Dec | 87.5 | 87.2 |

| 10:00 | EUR | Germany ZEW Economic Sentiment Dec | 7 | 7.4 |

| 10:00 | EUR | Germany ZEW Current Situation Dec | -91 | -91.4 |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Dec | 12.5 | |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Oct | 11.9B | 13.6B |

| 13:30 | CAD | New Housing Price Index M/M Nov | -0.40% | |

| 13:30 | CAD | CPI M/M Nov | 0.00% | 0.40% |

| 13:30 | CAD | CPI Y/Y Nov | 2.00% | |

| 13:30 | CAD | CPI Core M/M Nov | 0.40% | |

| 13:30 | CAD | CPI Median Y/Y Nov | 2.40% | 2.50% |

| 13:30 | CAD | CPI Trimmed Y/Y Nov | 2.50% | 2.60% |

| 13:30 | CAD | CPI Common Y/Y Nov | 2.10% | 2.20% |

| 13:30 | USD | Retail Sales M/M Nov | 0.50% | 0.40% |

| 13:30 | USD | Retail Sales ex Autos M/M Nov | 0.40% | 0.10% |

| 13:55 | USD | Redbook Index Y/Y (Dec 13) | 4.20% | |

| 14:15 | USD | Industrial Production M/M Nov | 0.10% | -0.30% |

| 14:15 | USD | Capacity Utilization Nov | 77.20% | 77.10% |

| 15:00 | USD | Business Inventories Oct | 0.20% | 0.10% |

| 15:00 | USD | NAHB Housing Market Index Dec | 46 | 46 |

| 21:45 | NZD | Current Account (NZD) Q3 | -10.45B | -4.83B |

| 23:50 | JPY | Trade Balance (JPY) Nov | -0.45T | -0.36T |

| GMT | Ccy | Events | |

|---|---|---|---|

| 07:00 | GBP | Claimant Count Change Nov | |

| Forecast: | Previous: 26.7K | ||

| 07:00 | GBP | ILO Unemployment Rate (3M) Oct | |

| Forecast: 4.30% | Previous: 4.30% | ||

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Oct | |

| Forecast: 5.00% | Previous: 4.80% | ||

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Oct | |

| Forecast: 4.60% | Previous: 4.30% | ||

| 08:00 | CHF | SECO Economic Forecasts | |

| Forecast: | Previous: | ||

| 09:00 | EUR | Germany IFO Business Climate Dec | |

| Forecast: 85.6 | Previous: 85.7 | ||

| 09:00 | EUR | Germany IFO Current Assessment Dec | |

| Forecast: 84 | Previous: 84.3 | ||

| 09:00 | EUR | Germany IFO Expectations Dec | |

| Forecast: 87.5 | Previous: 87.2 | ||

| 10:00 | EUR | Germany ZEW Economic Sentiment Dec | |

| Forecast: 7 | Previous: 7.4 | ||

| 10:00 | EUR | Germany ZEW Current Situation Dec | |

| Forecast: -91 | Previous: -91.4 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Dec | |

| Forecast: | Previous: 12.5 | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Oct | |

| Forecast: 11.9B | Previous: 13.6B | ||

| 13:30 | CAD | New Housing Price Index M/M Nov | |

| Forecast: | Previous: -0.40% | ||

| 13:30 | CAD | CPI M/M Nov | |

| Forecast: 0.00% | Previous: 0.40% | ||

| 13:30 | CAD | CPI Y/Y Nov | |

| Forecast: | Previous: 2.00% | ||

| 13:30 | CAD | CPI Core M/M Nov | |

| Forecast: | Previous: 0.40% | ||

| 13:30 | CAD | CPI Median Y/Y Nov | |

| Forecast: 2.40% | Previous: 2.50% | ||

| 13:30 | CAD | CPI Trimmed Y/Y Nov | |

| Forecast: 2.50% | Previous: 2.60% | ||

| 13:30 | CAD | CPI Common Y/Y Nov | |

| Forecast: 2.10% | Previous: 2.20% | ||

| 13:30 | USD | Retail Sales M/M Nov | |

| Forecast: 0.50% | Previous: 0.40% | ||

| 13:30 | USD | Retail Sales ex Autos M/M Nov | |

| Forecast: 0.40% | Previous: 0.10% | ||

| 13:55 | USD | Redbook Index Y/Y (Dec 13) | |

| Forecast: | Previous: 4.20% | ||

| 14:15 | USD | Industrial Production M/M Nov | |

| Forecast: 0.10% | Previous: -0.30% | ||

| 14:15 | USD | Capacity Utilization Nov | |

| Forecast: 77.20% | Previous: 77.10% | ||

| 15:00 | USD | Business Inventories Oct | |

| Forecast: 0.20% | Previous: 0.10% | ||

| 15:00 | USD | NAHB Housing Market Index Dec | |

| Forecast: 46 | Previous: 46 | ||

| 21:45 | NZD | Current Account (NZD) Q3 | |

| Forecast: -10.45B | Previous: -4.83B | ||

| 23:50 | JPY | Trade Balance (JPY) Nov | |

| Forecast: -0.45T | Previous: -0.36T | ||

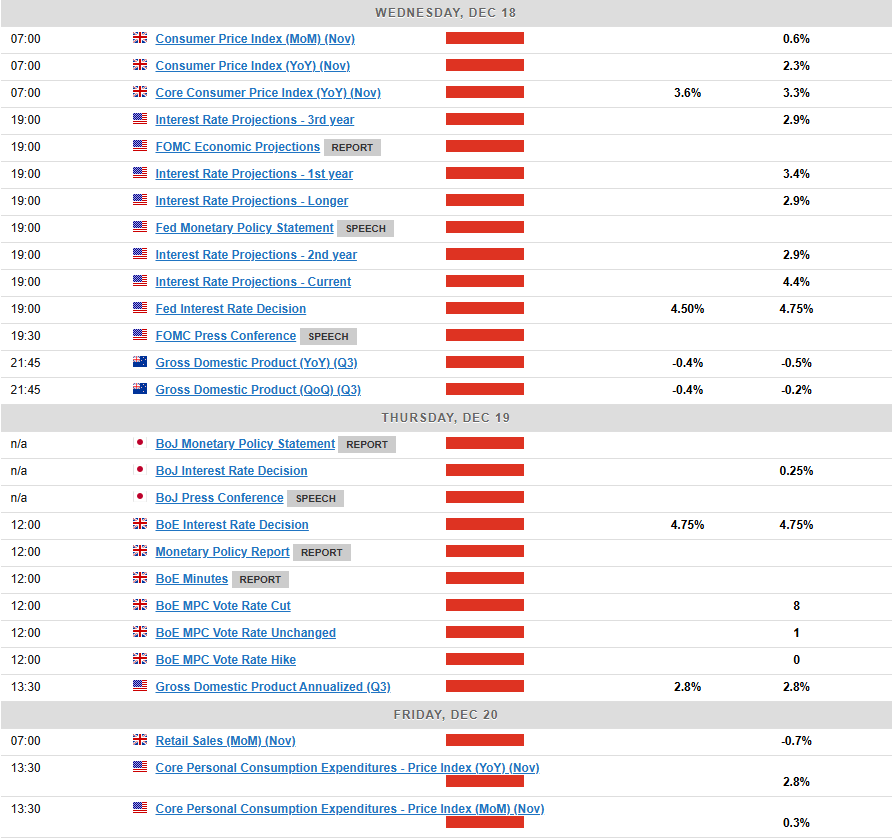

Wednesday, Dec 18 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | AUD | Westpac Leading Index M/M Nov | 0.20% | |

| 07:00 | GBP | CPI M/M Nov | 0.60% | |

| 07:00 | GBP | CPI Y/Y Nov | 2.60% | 2.30% |

| 07:00 | GBP | Core CPI Y/Y Nov | 3.60% | 3.30% |

| 07:00 | GBP | RPI M/M Nov | 0.50% | |

| 07:00 | GBP | RPI Y/Y Nov | 3.40% | |

| 07:00 | GBP | PPI Input M/M Nov | 0.10% | |

| 07:00 | GBP | PPI Input Y/Y Nov | -2.30% | |

| 07:00 | GBP | PPI Output M/M Nov | 0% | |

| 07:00 | GBP | PPI Output Y/Y Nov | -0.80% | |

| 07:00 | GBP | PPI Core Output M/M Nov | 0.30% | |

| 07:00 | GBP | PPI Core Output Y/Y Nov | 1.70% | |

| 10:00 | EUR | Eurozone CPI Y/Y Nov F | 2.30% | 2.30% |

| 10:00 | EUR | Eurozone CPI Core Y/Y Nov F | 2.70% | 2.70% |

| 13:30 | USD | Building Permits Nov | 1.43M | 1.42M |

| 13:30 | USD | Housing Starts Nov | 1.35M | 1.31M |

| 13:30 | USD | Building Permits Change Nov | -0.40% | |

| 13:30 | USD | Current Account (USD) Q3 | -286B | -267B |

| 15:30 | USD | Crude Oil Inventories | -1.4M | |

| 19:00 | USD | Fed Interest Rate Decision | 4.50% | 4.75% |

| 19:30 | USD | FOMC Press Conference | ||

| 21:45 | NZD | GDP Q/Q Q3 | -0.20% | -0.20% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | AUD | Westpac Leading Index M/M Nov | |

| Forecast: | Previous: 0.20% | ||

| 07:00 | GBP | CPI M/M Nov | |

| Forecast: | Previous: 0.60% | ||

| 07:00 | GBP | CPI Y/Y Nov | |

| Forecast: 2.60% | Previous: 2.30% | ||

| 07:00 | GBP | Core CPI Y/Y Nov | |

| Forecast: 3.60% | Previous: 3.30% | ||

| 07:00 | GBP | RPI M/M Nov | |

| Forecast: | Previous: 0.50% | ||

| 07:00 | GBP | RPI Y/Y Nov | |

| Forecast: | Previous: 3.40% | ||

| 07:00 | GBP | PPI Input M/M Nov | |

| Forecast: | Previous: 0.10% | ||

| 07:00 | GBP | PPI Input Y/Y Nov | |

| Forecast: | Previous: -2.30% | ||

| 07:00 | GBP | PPI Output M/M Nov | |

| Forecast: | Previous: 0% | ||

| 07:00 | GBP | PPI Output Y/Y Nov | |

| Forecast: | Previous: -0.80% | ||

| 07:00 | GBP | PPI Core Output M/M Nov | |

| Forecast: | Previous: 0.30% | ||

| 07:00 | GBP | PPI Core Output Y/Y Nov | |

| Forecast: | Previous: 1.70% | ||

| 10:00 | EUR | Eurozone CPI Y/Y Nov F | |

| Forecast: 2.30% | Previous: 2.30% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Nov F | |

| Forecast: 2.70% | Previous: 2.70% | ||

| 13:30 | USD | Building Permits Nov | |

| Forecast: 1.43M | Previous: 1.42M | ||

| 13:30 | USD | Housing Starts Nov | |

| Forecast: 1.35M | Previous: 1.31M | ||

| 13:30 | USD | Building Permits Change Nov | |

| Forecast: | Previous: -0.40% | ||

| 13:30 | USD | Current Account (USD) Q3 | |

| Forecast: -286B | Previous: -267B | ||

| 15:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -1.4M | ||

| 19:00 | USD | Fed Interest Rate Decision | |

| Forecast: 4.50% | Previous: 4.75% | ||

| 19:30 | USD | FOMC Press Conference | |

| Forecast: | Previous: | ||

| 21:45 | NZD | GDP Q/Q Q3 | |

| Forecast: -0.20% | Previous: -0.20% | ||

Thursday, Dec 19, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| JPY | BoJ Interest Rate Decision | 0.25% | 0.25% | |

| 00:00 | AUD | Consumer Inflation Expectations Dec | 3.80% | |

| 00:00 | NZD | ANZ Business Confidence Dec | 64.9 | |

| 07:00 | EUR | Germany GfK Consumer Confidence Jan | -22 | -23.3 |

| 07:00 | CHF | Trade Balance (CHF) Nov | 6.20B | 8.06B |

| 09:00 | EUR | Eurozone Current Account (EUR) Oct | 33.5B | 37.0B |

| 12:00 | GBP | BoE Interest Rate Decision | 4.75% | 4.75% |

| 12:00 | GBP | MPC Official Bank Rate Votes | 0--2--7 | 0--8--1 |

| 13:30 | USD | Initial Jobless Claims (Dec 13) | 240K | 242K |

| 13:30 | USD | GDP Annualized Q3 F | 2.80% | 2.80% |

| 13:30 | USD | GDP Price Index Q3 F | 1.90% | 1.90% |

| 13:30 | USD | Philly Fed Manufacturing Index Dec | 1.9 | -5.5 |

| 15:00 | USD | Existing Home Sales Nov | 4.11M | 3.96M |

| 15:30 | USD | Natural Gas Storage | -190B | |

| 21:45 | NZD | Trade Balance (NZD) Nov | -1951M | -1544M |

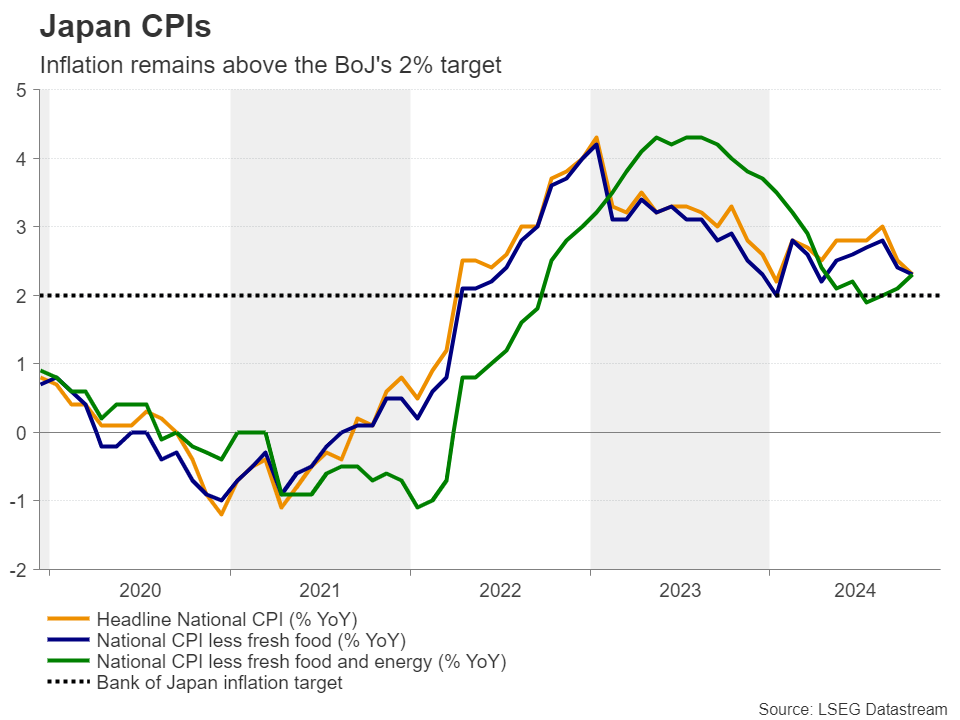

| 23:30 | JPY | National CPI Y/Y Nov | 2.30% | |

| 23:30 | JPY | National CPI Core Y/Y Nov | 2.60% | 2.30% |

| 23:30 | JPY | National CPI Core-Core Y/Y Nov | 2.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| JPY | BoJ Interest Rate Decision | ||

| Forecast: 0.25% | Previous: 0.25% | ||

| 00:00 | AUD | Consumer Inflation Expectations Dec | |

| Forecast: | Previous: 3.80% | ||

| 00:00 | NZD | ANZ Business Confidence Dec | |

| Forecast: | Previous: 64.9 | ||

| 07:00 | EUR | Germany GfK Consumer Confidence Jan | |

| Forecast: -22 | Previous: -23.3 | ||

| 07:00 | CHF | Trade Balance (CHF) Nov | |

| Forecast: 6.20B | Previous: 8.06B | ||

| 09:00 | EUR | Eurozone Current Account (EUR) Oct | |

| Forecast: 33.5B | Previous: 37.0B | ||

| 12:00 | GBP | BoE Interest Rate Decision | |

| Forecast: 4.75% | Previous: 4.75% | ||

| 12:00 | GBP | MPC Official Bank Rate Votes | |

| Forecast: 0--2--7 | Previous: 0--8--1 | ||

| 13:30 | USD | Initial Jobless Claims (Dec 13) | |

| Forecast: 240K | Previous: 242K | ||

| 13:30 | USD | GDP Annualized Q3 F | |

| Forecast: 2.80% | Previous: 2.80% | ||

| 13:30 | USD | GDP Price Index Q3 F | |

| Forecast: 1.90% | Previous: 1.90% | ||

| 13:30 | USD | Philly Fed Manufacturing Index Dec | |

| Forecast: 1.9 | Previous: -5.5 | ||

| 15:00 | USD | Existing Home Sales Nov | |

| Forecast: 4.11M | Previous: 3.96M | ||

| 15:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: -190B | ||

| 21:45 | NZD | Trade Balance (NZD) Nov | |

| Forecast: -1951M | Previous: -1544M | ||

| 23:30 | JPY | National CPI Y/Y Nov | |

| Forecast: | Previous: 2.30% | ||

| 23:30 | JPY | National CPI Core Y/Y Nov | |

| Forecast: 2.60% | Previous: 2.30% | ||

| 23:30 | JPY | National CPI Core-Core Y/Y Nov | |

| Forecast: | Previous: 2.30% | ||

Friday, Dec 20, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:15 | CNY | 1-Y Loan Prime Rate | 3.10% | 3.10% |

| 01:15 | CNY | 5-Y Loan Prime Rate | 3.60% | 3.60% |

| 07:00 | GBP | Retail Sales M/M Nov | 0.40% | -0.70% |

| 07:00 | EUR | Germany PPI M/M Nov | 0.30% | 0.20% |

| 07:00 | EUR | Germany PPI Y/Y Nov | -1.10% | |

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Nov | 15.5B | 17.4B |

| 13:30 | CAD | Retail Sales M/M Oct | 0.40% | 0.40% |

| 13:30 | CAD | Retail Sales ex Autos M/M Oct | 0.50% | 0.90% |

| 13:30 | USD | Personal Income M/M Nov | 0.40% | 0.60% |

| 13:30 | USD | Personal Spending Nov | 0.50% | 0.40% |

| 13:30 | USD | PCE Price Index M/M Nov | 0.20% | |

| 13:30 | USD | PCE Price Index Y/Y Nov | 2.30% | |

| 13:30 | USD | Core PCE Price Index M/M Nov | 0.20% | 0.30% |

| 13:30 | USD | Core PCE Price Index Y/Y Nov | 2.80% | |

| 15:00 | USD | Michigan Consumer Sentiment Index Dec F | 74 | 74 |

| 15:00 | EUR | EurozoneConsumer Confidence Dec P | -14 | -14 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:15 | CNY | 1-Y Loan Prime Rate | |

| Forecast: 3.10% | Previous: 3.10% | ||

| 01:15 | CNY | 5-Y Loan Prime Rate | |

| Forecast: 3.60% | Previous: 3.60% | ||

| 07:00 | GBP | Retail Sales M/M Nov | |

| Forecast: 0.40% | Previous: -0.70% | ||

| 07:00 | EUR | Germany PPI M/M Nov | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 07:00 | EUR | Germany PPI Y/Y Nov | |

| Forecast: | Previous: -1.10% | ||

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Nov | |

| Forecast: 15.5B | Previous: 17.4B | ||

| 13:30 | CAD | Retail Sales M/M Oct | |

| Forecast: 0.40% | Previous: 0.40% | ||

| 13:30 | CAD | Retail Sales ex Autos M/M Oct | |

| Forecast: 0.50% | Previous: 0.90% | ||

| 13:30 | USD | Personal Income M/M Nov | |

| Forecast: 0.40% | Previous: 0.60% | ||

| 13:30 | USD | Personal Spending Nov | |

| Forecast: 0.50% | Previous: 0.40% | ||

| 13:30 | USD | PCE Price Index M/M Nov | |

| Forecast: | Previous: 0.20% | ||

| 13:30 | USD | PCE Price Index Y/Y Nov | |

| Forecast: | Previous: 2.30% | ||

| 13:30 | USD | Core PCE Price Index M/M Nov | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 13:30 | USD | Core PCE Price Index Y/Y Nov | |

| Forecast: | Previous: 2.80% | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Dec F | |

| Forecast: 74 | Previous: 74 | ||

| 15:00 | EUR | EurozoneConsumer Confidence Dec P | |

| Forecast: -14 | Previous: -14 | ||

Weekly Economic & Financial Commentary: Sticky Inflation, Sticky Wicket for the Fed

Summary

United States: Sticky Inflation, Sticky Wicket for the Fed

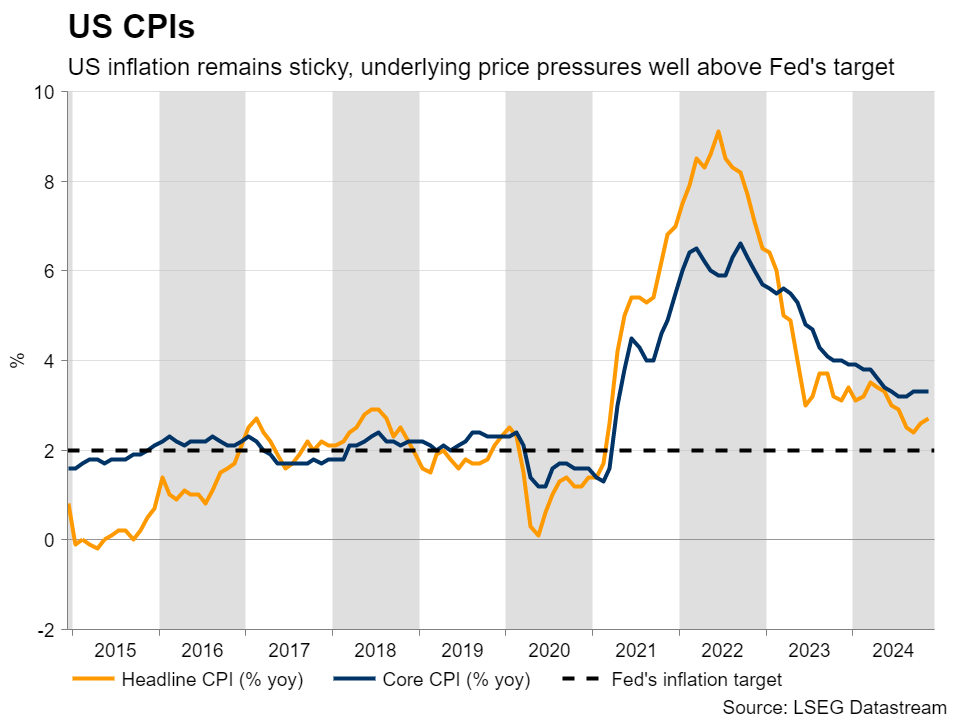

- Price data this week showed that inflation remains stubbornly above the FOMC's target. Overall inflation has trended sideways in recent months, and while we do not expect this week's data to prevent the Fed from cutting another 25 bps next week, it will likely contribute to the Committee dialing back its guidance for additional easing ahead.

- Next week: Retail Sales (Tue.), Industrial Production (Tue.), Personal Income and Spending (Fri.)

International: Center Stage for Foreign Central Banks This Week

- It was a very active week for foreign central banks. The European Central Bank cut rates 25 bps, and we view the dovish accompanying statement as consistent with steady easing at every meeting through next June. Meanwhile, the Swiss National Bank and Bank of Canada opted for more aggressive easing, with both delivering 50 bps rate cuts. On the flip side, Brazil's central bank announcement was very hawkish, as officials increased the Selic rate 100 bps and explicitly signaled same-sized increases at the next two policy meetings.

- Next week: Eurozone PMIs (Mon.), Bank of Japan Policy Rate (Thu.), Bank of England Policy Rate (Thu.)

Interest Rate Watch: A Year in Review for Rates: Exiting Inversion

- Coming into 2024, there was significant uncertainty about the path ahead for U.S. interest rates. Rate cuts from the FOMC have yielded lower short-term interest rates, but longer-term yields have risen this year amid reduced odds of a "hard landing" and rising estimates for r-star.

Credit Market Insights: Diverging Paths for HELOCs and Credit Cards

- Consumer spending has driven record-high credit card balances, while HELOC usage has plateaued despite falling borrowing rates. These trends suggest that consumers are still relying significantly on credit cards to support their spending habits.

Topic of the Week: If History Is Any Guide

- The 1930 Smoot-Hawley and 2017-2019 trade wars have taught us that countries are unlikely to stand down in the face of U.S. tariff increases. Who buys U.S. exports, and what goods are at risk?

Markets Weekly Outlook – Will Fed Rate Cut and BoJ Decision Spur Volatility?

- Markets had a volatile week, with US 100 (Nasdaq 100) reaching new highs and a strong likelihood of a Fed rate cut next week.

- Major central bank meetings dominate the week ahead.

- The BoJ faces a tough decision on whether to raise interest rates, with recent data supporting a hike.

- The US Dollar Index (DXY) is at a crucial resistance level, and its performance may be influenced by the Fed’s interest rate decision and outlook.

Week in Review: Uptick in US Inflation a Concern?

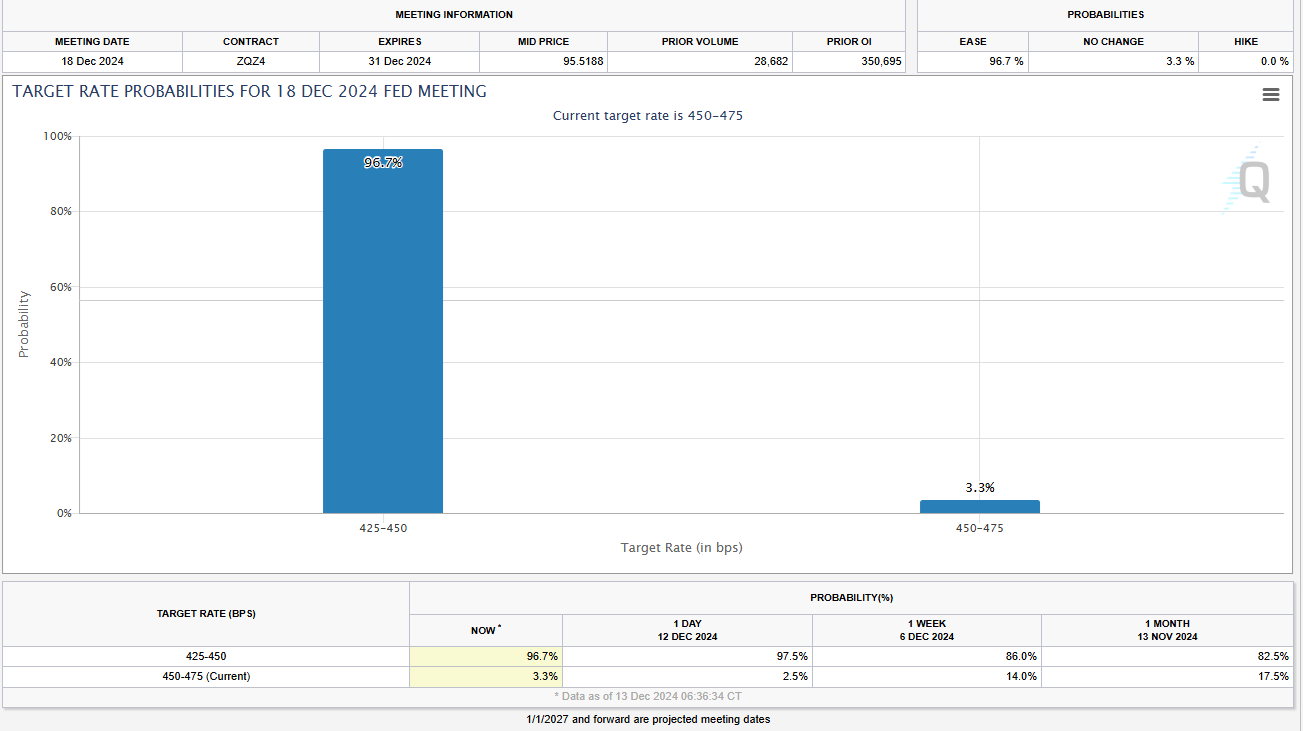

An interesting week that saw swings from risk off to risk on sentiment helping to push US Equities to fresh highs. A strong batch of US Data keeps the likelihood of a Fed Rate cut next week strong and languishing above the 90% threshold heading into the weekend.

Source: CME FedWatch Tool (click to enlarge)

Recent increases in both the US CPI and PPI data have raised eyebrows regarding resurgent inflation in 2025. This comes against the backdrop of proposed tariffs by incoming President Donald Trump. With that in mind however, many believe the US Dollar will strengthen due to this and it is a plausible scenario as Yields are also expected to rise.

The train of though around tariffs has been well discussed with ING Thinks James Knightley putting it “prices are going to rise, particularly if Trump’s tariff plans are as bold as promised on the campaign trail. And growth could rise in the short term. But timing is everything. If tariffs kick in early, and aren’t compensated for by big tax cuts, there’s going to be a real squeeze on household spending power.” I have to admit that i tend to agree with the narrative.

These concerns make the upcoming PCE data more important to the Fed as we head into 2025, with my base case being a December cut and January hold.

Wall Street Indexes were mixed this week with the Nasdaq 100 on course for a positive finish thanks in large part to chip stocks. The Nasdaq 100 is doing better than its Wall Street peers after Broadcom gave a positive outlook. This boosted excitement about artificial intelligence and helped raise the value of chip stocks dragging the index closer to the 22000 handle.

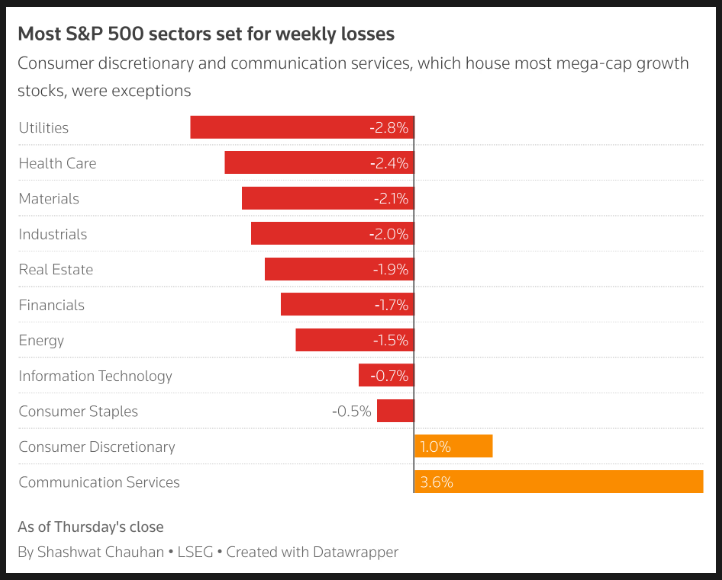

Wall Street indexes appear to be taking a break after recent gains and some strong economic data before the Fed’s meeting. This has put the S&P 500 and Dow on track for losses this week.

Source: LSEG (click to enlarge)

Oil prices recorded its first weekly gain in three weeks despite both OPEC and IEA downgrading their forecasts for both 2024 and 2025. Stimulus measures announced by China’s politburo for now though appear to be supporting Oil prices and keeping Brent above the crucial $70 a barrel mark.

The DXY enjoyed a positive week and as a result weighed on its G7 counterparts and many emerging market currencies as well. The early week US Dollar strength may in part have been down to haven appeal following events in Syria over the past two weeks. The DXY is languishing in a crucial area heading into a massive week and is likely to play a big role as the month and year draws to a close.

Gold prices enjoyed a strong start to the week thanks in part to renewed haven appeal and the resumption of Gold purchases by the Peoples Bank of China following a near six-month hiatus. However, the strong PPI data and potential profit taking on Gold ahead of a busy week have left the precious metal trading up just around 1% for the week at 2660 at the time of writing. A stark contrast from Thursdays highs around the 2720 and ounce handle. Any further signs of instability in Syria heading into next week could be crucial in the precious metals next move as well as the outlook by the US Federal Reserve moving forward into 2025.

The Week Ahead: Fed to Cut Rates, BoE Set to Hold as BOJ Face a Tough Choice

Asia Pacific Markets

The week ahead in the Asia Pacific region sees some key economic data releases and events.

In China, the final data report of the year will come out next Monday. Key economic indicators are expected to show modest improvement. Industrial production may grow by 5.6% compared to last year, retail sales are likely to speed up to 5.1% growth year-on-year, and fixed asset investment could stay steady with a small increase to 3.5% year-to-date.

Stimulus announcements by China last week adds another layer of intrigue around China. Market participants are hoping that the announcements over the past week will finally lead to a surge in demand.

In Japan, the Bank of Japan is meeting on Thursday. There are expectations for an interest rate hike next week, although it might be a close decision. Recent data, like strong wage growth, higher-than-expected inflation, and improved GDP figures, back the idea of a hike.

However, one local wire in Japan reported that there is a growing view that a premature rate hike should be avoided unless there is a significant risk of inflation rising. This may give the BoJ some food for thought.

Europe + UK + US

In developed markets, the focus moves back to Central Banks with both the Federal Reserve and the Bank of England (BoE) interest rate decisions.

The Federal Reserve is expected to reduce rates by another 25 basis points on December 18. Inflation hasn’t moved much closer to the Fed’s 2% target recently. However, the Fed also monitors the job market closely. Signs like slower job growth and rising unemployment support the decision to adjust rates closer to a neutral level. That said, the rate cuts are likely to slow down in 2025 unless inflation improves significantly or the job market weakens much more.

The Fed’s preferred inflation measure, the core PCE deflator, is expected to be around 0.2%, based on recent data from the CPI and PPI reports.

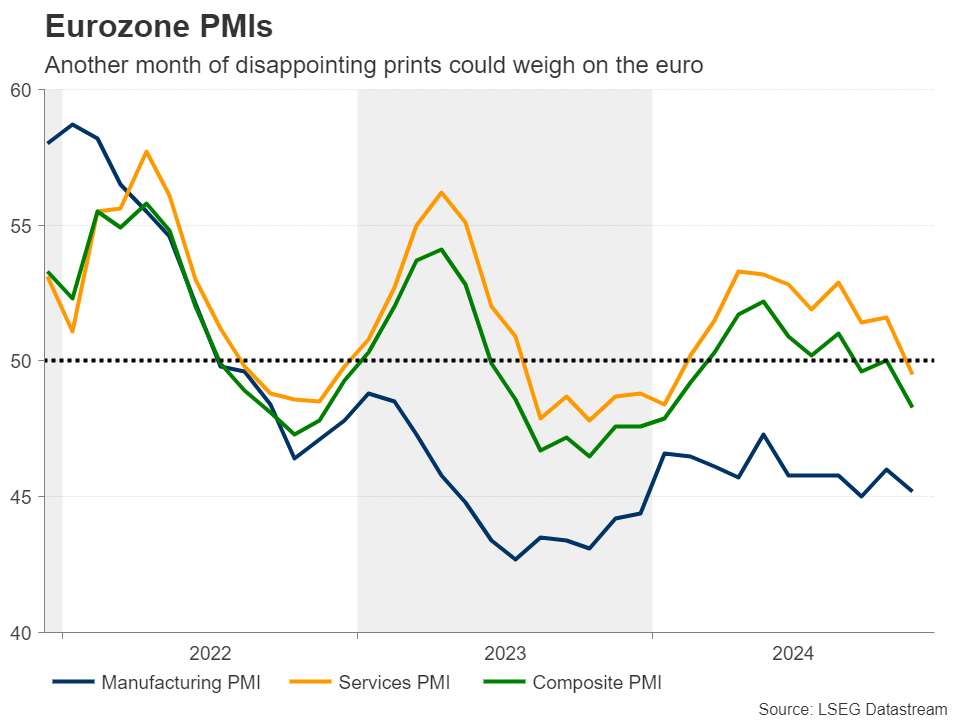

In Europe the week is a bit quieter with the biggest data release being PMI data. Given the struggle with growth the Euro Area is experiencing, this is a key release and one that could stoke volatility and the probability of potential rate cuts from the ECB. There is also a speech by Christine Lagarde at the start of the week which may shed more light on this past week’s rate cut.

In the UK we have a busy week with labor data kicking things off. The unemployment rate has been quite unpredictable due to well-known data issues. However, there are clear signs that the job market is slowing down. Despite this, wages haven’t been affected yet and might even rise slightly next week because of unusual comparisons with last year’s numbers.

Headline inflation is expected to increase more than the Bank of England predicted, partly due to a small rise in services inflation. This measure, which is important to the BoE, is likely to stay around 5% during the winter. This is mostly because of stubbornly high costs in areas like travel and rents, which the Bank doesn’t seem too concerned about.

The Bank of England (BoE) appears comfortable with reducing rates every other meeting. Since rates were cut in November, I don’t think there will be another cut before the February meeting.

Chart of the Week

This week’s focus is back to the US Dollar Index which is once again in the key area around the 107.00 handle.

I thought this may be a prudent time to look at the performance of the US Dollar post the 2016 US election for a historical perspective.

After both the 2016 and 2024 elections, stocks and the US dollar went up. However, in 2017, the dollar lost strength, entering a downward trend that lasted most of the year. This weakness in the dollar helped support a steady rise in U.S. and global stock markets.

Looking at where the US Dollar Index is currently resting in a key area of resistance. Will the recent uptick in inflation be a driving force for the US Dollar moving forward or will the Fed succeed in keeping things on an even keel?

The DXY has struggled to find acceptance above the 107.00 handle, will this time prove to be different?

A rejection here may lead to a retest of support at 106.50 and the 106.00 handle respectively.

A breach of 107.00 will need to prove that it has found acceptance above this level before i will be convinced of a sustainable move. The Fed interest rate meeting could be the catalyst for this especially if they taper rate cut expectations for 2025.

US Dollar Index (DXY) Daily Chart – December 13, 2024

Source: TradingView.Com (click to enlarge)

Key Levels to Consider:

Support

- 106.50

- 106.00

- 105.00

Resistance

- 107.50

- 108.00

- 109.00

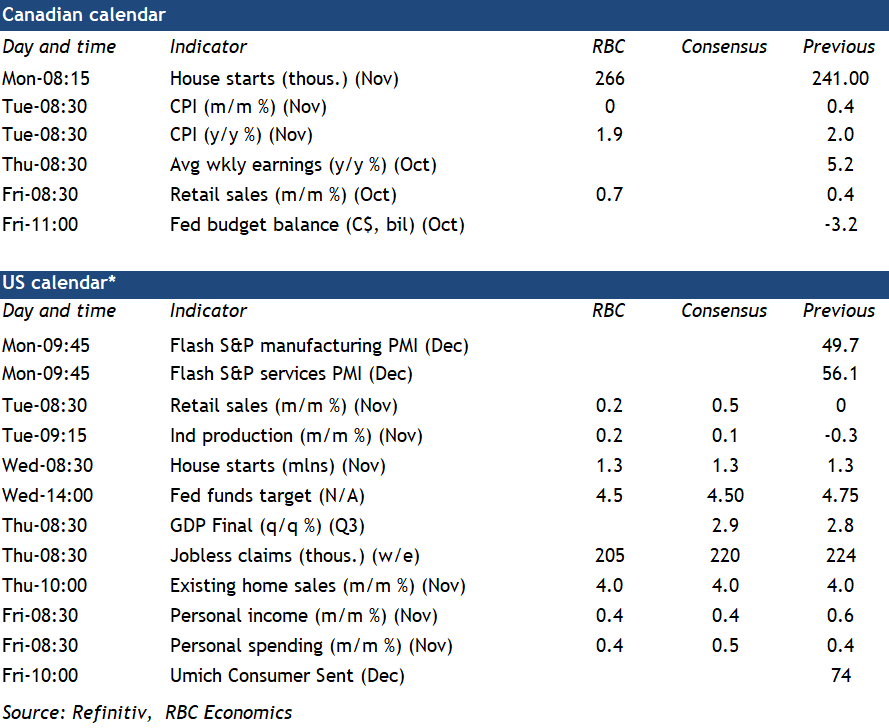

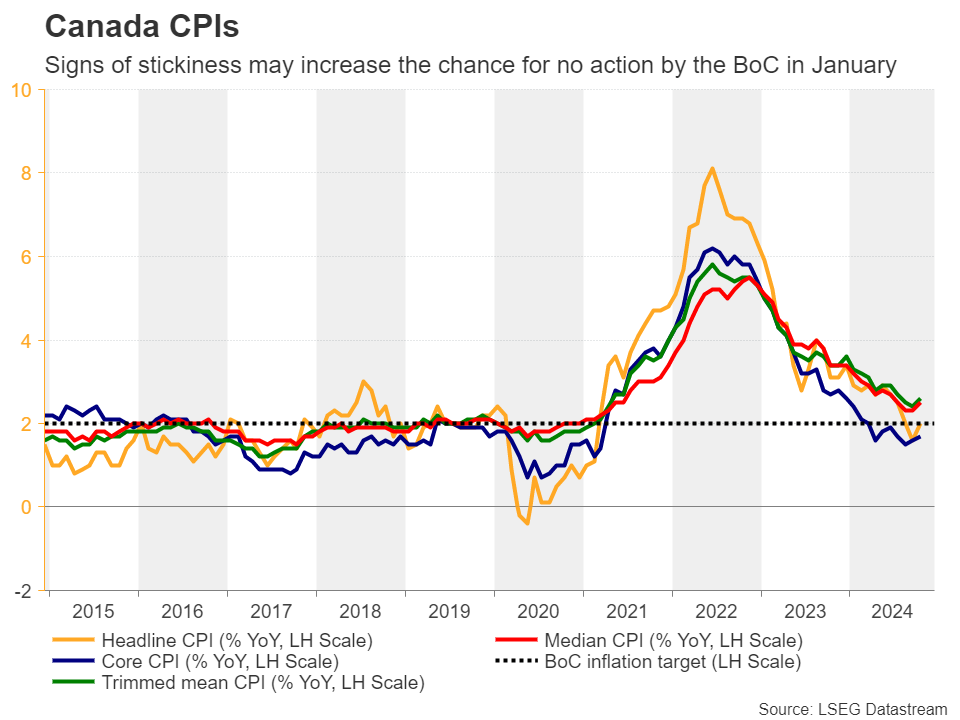

Canadian Inflation Likely Headed Lower, U.S. Fed to Cut by 25 bps

Canadian consumer price index growth is expected to have eased slightly in November after picking up in October, which is consistent with a persistently softening economy that’s left broader inflation pressures tracking at or below the Bank of Canada’s 2% target.

We expect headline inflation to have eased to 1.9% in November. Price growth in both food and energy inflation are expected to have held largely steady year-over-year at around 3% and -2.7%, respectively. But, we look for growth excluding those components to drop to 2.1% from 2.3% in October.

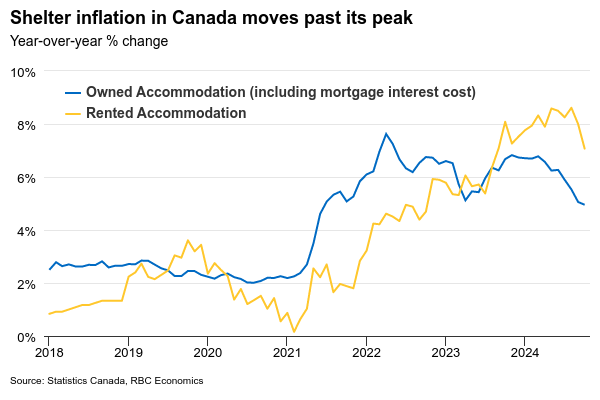

Shelter inflation still accounts for a disproportionate share of overall inflation, but should show further signs of slowing in November. Mortgage interest costs were still up almost 15% from a year ago in October, and accounted for over a quarter of annual consumer price growth. But, that is down from a 30% growth peak in 2023 and will continue to slow following interest rate cuts. Rent inflation also likely eased as a drop in current market asking rents flow through to lease renewals.

Annual growth in the BoC’s preferred “core” measures, such as CPI trim and median, are both expected to tick lower following a rise in October, averaging 2.5%. The breadth of inflation pressures remained relatively narrow in October even with readings picking up. That likely persisted in November.

Unlike Canada where inflation pressures have eased, a resilient U.S. economy has meant inflation has been stickier than previously expected. Headline U.S. inflation picked up slightly to 2.7% in November, while the U.S. Federal Reserve’s “supercore” measure held at an elevated 4.3% on a three-month annualized basis.

Those trends will be closely watched by the Fed, but shouldn’t prevent another interest rate cut on Wednesday. Chair Jerome Powell hinted in recent communications that the central bank doesn’t need to rush rate cuts, but labour markets have also been gradually softening and inflation is still lower than it was at the start of this year. The level of the Fed funds rate is still likely higher than it needs to be for inflation to continue to edge broadly toward the Fed’s 2% objective.

We continue to think the Fed will cut by 25 basis points in December and January before hitting a pause with the fed funds rate at a restrictive 4%-4.25% range. As we have highlighted before, a solid domestic demand backdrop, in no small part tied to a large government budget deficit, would need to be offset by tighter monetary policy.

Week ahead data watch

- We expect Canadian housing starts to grow by 10% in November, reaching 266K.

- October SEPH data will be watched closely for further signs of softening in the labour market. Given slower hiring demand, we expect job openings to weaken further and wage growth to slow.

- Canadian retail sales likely increased by 0.7% in October, in line with StatsCan’s preliminary estimate. Auto sales were up 1.7%, down from the 4.7% in September. Sales at gas station rebounded in October as prices rose.

- We expect U.S. retail sales to tick up again (+0.2%) in November, slowing from the 0.4% growth in October. Auto and gas station sales were both higher during that month.

- U.S. personal spending likely grew by 0.4% in November, matching the pace in October. We expect personal income to edge up by the same amount (+0.4%) as wage growth remained robust in the U.S.

- U.S. industrial production likely ticked higher in November, by 0.2%, supported growth in auto manufacturing.

Fed Preview: Gauging for Neutral

- We expect the Fed to cut the policy rate target by 25bp in the December meeting. The Fed could also cut the ON RRP facility rate by an additional 5bp, but we do not expect this to have a significant impact on the policy stance (see p. 2).

- Markets have fully priced in next week's cut. Main focus will be on updated rate projections, and especially on the FOMC's latest view on the terminal rate level. 2024 and 2025 GDP and inflation forecasts will likely get revised slightly higher.

- We think the Fed is likely to continue cutting rates faster than markets expect also in 2025. If the 'dots' continue to signal several cuts for 2025, UST yields could shift lower and EUR/USD edge higher upon announcement.

Since the FOMC participants filed their latest economic projections in mid-September, market pricing for real terminal policy rate has shifted roughly 60bp higher. Real 1y forward OIS curve stabilizes around 1.7-1.8% level, which is 0.8-0.9% above the September median real long-term dot. While 25bp cut next week is mostly a done deal, the true focus is on how FOMC's terminal rate view has shifted alongside markets.

While part of the increase in market pricing can be attributed to term premium (NY Fed's ACM model estimate for 10y term premium is roughly 30bp higher than 3M ago), markets are discounting in expectations of more resilient economy and supportive fiscal policy.

But while we wait for the details on the latter, we struggle to see why the Fed should suddenly be more concerned with the economy overheating again. This week's CPI data showed continuing cooling in both housing and non-housing services inflation, suggesting that the underlying disinflation trend remains on track. The ratio of job openings to unemployed has stabilized around 1.1, which suggests labour market balance is slightly cooler than before the pandemic. Both market and survey-based measures of inflation expectations remain well aligned with the 2% target.

Still low level of mortgage applications and weak commercial loan demand signals from the Fed's latest SLOOS data also suggest current policy stance remains restrictive. As such, we think the Fed can continue to reduce rates towards neutral not just next week, but also into 2025. And when it comes to estimating the neutral level, we do not think the magnitude of the shift in market pricing is quite yet justified. More modest upward-shift in longer-term dots could be a dovish surprise for the markets.

We expect minor positive revisions to GDP and inflation forecasts for 2024 & 2025 but think 2026 forecasts will remain stable. We think Powell will aim for a neutral tone in his remarks, but he is still likely to verbally open the door for slowing the pace of cuts, in line with what we have heard from other Fed commentators lately. Markets are currently pricing in only 6bp for the January meeting, and we do not expect a dramatic re-pricing after next week, as the decision ultimately hinges on data released later on. 10-12bp (or close to 50/50) would be a fair level at this stage in our view. Markets' most likely scenario includes 25bp rate cuts in every other meeting during H1 2025, but we still believe the Fed will end up cutting rates in every meeting until June.

ON RRP cut would not predict an imminent end to QT

The Fed could also deliver a 5bp additional technical reduction to the ON RRP rate as

discussed in the November minutes, which would align it with the lower bound of the Fed

Funds target range. We do not think it would have a significant impact on the overall policy

stance, but rather, such a move should be seen as a sign of the Fed wanting to err on the

side of caution amid the risk of repeating the repo market turmoil in September 2019.

All else equal, the reduction would make it less attractive for money market funds to park

cash into the facility, which could then provide a positive boost to markets’ liquidity

conditions. ON RRP usage peaked above USD2300bn around two years ago, but the level

has already declined to around USD150bn, meaning the impact would be modest either

way.

Market-based overnight repo rate (SOFR) has traded mostly in tandem with the Fed Funds

rate over past years, but as liquidity conditions have gradually tightened due to QT, SOFR

has seen occasional spikes around month and quarter turn dates. The very latest fixings

have been on the higher side again, which could increase the likelihood of the cut.

If the Fed does decide to cut the ON RRP rate, Powell would certainly face questions about

the future of QT, which is still draining liquidity at a rough pace of USD40bn/month.

However, the near-term liquidity outlook does not appear too concerning in our view. The

US debt ceiling suspension ends at the beginning of 2025, which means that the government

will start to utilize its cash balance to fund the ongoing deficits until the ceiling is lifted or

suspended again. This could theoretically boost liquidity by as much as USD775bn over

the course of H1 2025. If the remaining funds from the ON RRP facility would also get

drained back to the market, the level of bank reserves could even start rising again despite

the QT. As such, we do not expect the Fed to halt the QT before H2 2025 at earliest. Read

more from the STIR section of RtM USD – December cut in the horizon, 10 December).

Weekly Focus – The Season for Rate Cuts

As economic data continues to confirm that the inflation problem is more or less over, there is no longer a need for central banks to maintain restrictive levels of interest rates. Hence, this has been a week of rate cuts, and we expect next week to be the same - with some important nuances and exceptions.

The European Central Bank delivered the expected 25bp cut, although in our view they could easily have gone for 50bp, given weak growth indicators and the fact that euro area interest rates remain well above estimates of what the neutral level is and hence are still serving to dampen the economy further. However, the bank did signal a clearer path ahead for more cuts, and the market is coming around to our expectation that the deposit rate will be cut from the current 3% to 1.5% during 2025. One reason for the gradually lower outlook over the last month and generally increasing pessimism on the European economy was the weak PMI growth indicators from the euro area in November, so it will be very interesting to see the December numbers in the coming week. If they do not show clear improvement (and we do not expect them to), we are likely looking at a GDP decline in Q4. Note, though, that we will also get the January PMI before the next ECB rate decision. Both the Swiss and the Canadian central banks did cut by 50bp this week, which in the case of the former was a bit more than expected.

In the US, both we and the consensus expect a 25bp rate cut to be announced on Wednesday. Interest will likely centre on communication about the rate outlook for 2025, where we will get an update to the so-called dot plot showing what members of the monetary policy committee expect. Since we last got this update in September, market pricing has moved sharply towards fewer rate cuts, as the economy looks strong and as the Republican election victory could mean loser fiscal policy. However, inflation is well on track to reach its 2% target which was again confirmed by November data this week, and data for loans and credit continue to suggest that current monetary policy is quite restrictive. We see a strong case for the central bank to maintain its signal of a string of rate cuts in 2025, at least until we have more clarity over the fiscal policy outlook.

We expect the Bank of England to keep the Bank Rate unchanged at 4.75% on Thursday 19 December, sticking to its gradual easing cycle. While we get the labour market report for October/November and November inflation just days before, we do not expect this to move the needle of the immediate decision but prove more important for the 2025 outlook. We expect Sweden and Norway to remain very different also this week, with Sweden cutting rates again and signalling more to come, while Norway will likely hold tight, see the market movers section.

One central bank looking to increase rates rather than cutting them is the Bank of Japan. We have previously seen the upcoming December meeting as a likely date for that, but as support for the yen no longer seems acute, we think the Bank of Japan will stay on hold on Friday, and we push our expectation for the next rate hike to January.

Yearly Technical Outlook 2025 – EURUSD, GBPUSD, USDJPY

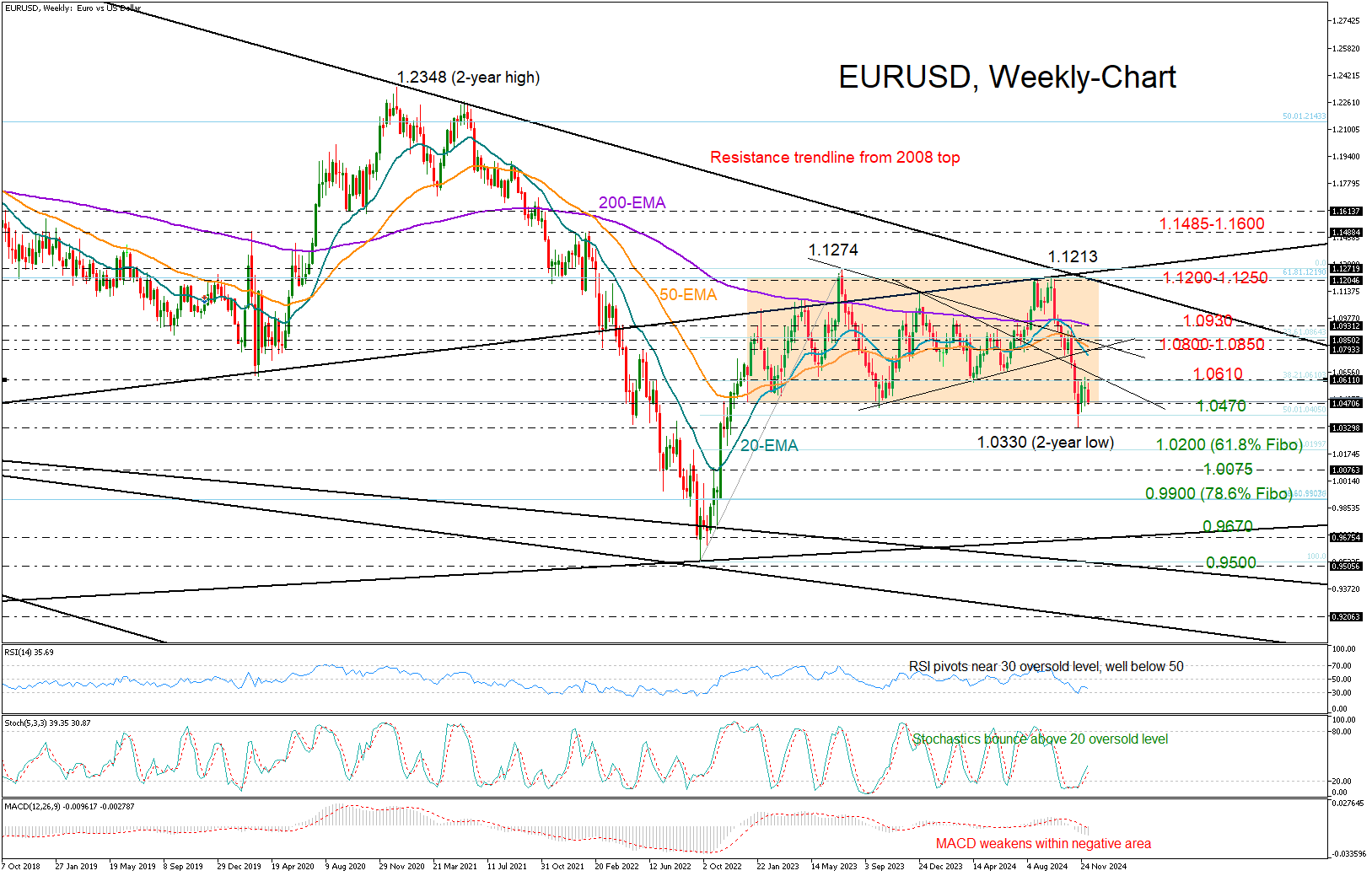

EURUSD: No light at the end of the tunnel

EURUSD is down by 4.78% year-to-date and has been stuck in a range since the ECB signaled the end of its rate hike cycle more than a year ago. Despite a boost from a dovish Fed, the euro has struggled due to the ECB’s rate cut policy, a stagnated economy, political instability, and geopolitical conflicts in Ukraine and the Middle East, pushing the pair to a two-year low of 1.0330.

Looking into 2025, volatility is likely to continue with ongoing divergences in monetary policy between the ECB and the Fed, political jitters, and potential tariff headwinds from Trump. The technical picture also displays a grim outlook.

Although the pair escaped a bearish break below a rectangle, with the technical indicators pointing to oversold conditions, there is no guarantee that the price could transition to a sustainable uptrend.

The bearish double top formation and the rejection from the 2008 resistance trendline near 1.1213 and around the 61.8% Fibonacci retracement of the 2000-2008 upleg sent a red warning in September. Then, the 20-weekly exponential moving average (EMA) crossed below the 50-weekly EMA after failing to move above the 200-weekly EMA, further strengthening the case of a bearish reversal.

If the pair sinks below 1.0470 and 1.0330, it may initially pause near the 1.0200 level before and then test parity within the 0.9900-1.0075 zone. Moving lower, the price could visit the tentative support line, which connects the 2000 and 2022 lows, at 0.9670.

For bulls, breaking above 1.1200-1.1250 is key, but resistance at 1.0610 and 1.0800-1.0850 followed by some challenging sessions around the 200-weekly SMA at 1.0930 could hold the pair back. A move past 1.1200-1.1250 could open the door to 1.1485-1.1600.

The mean estimate for the end of 2025 from 50 key global financial institutions reporting to Refinitiv is at 1.0500, with forecasts ranging between 1.1130 and 0.9900.

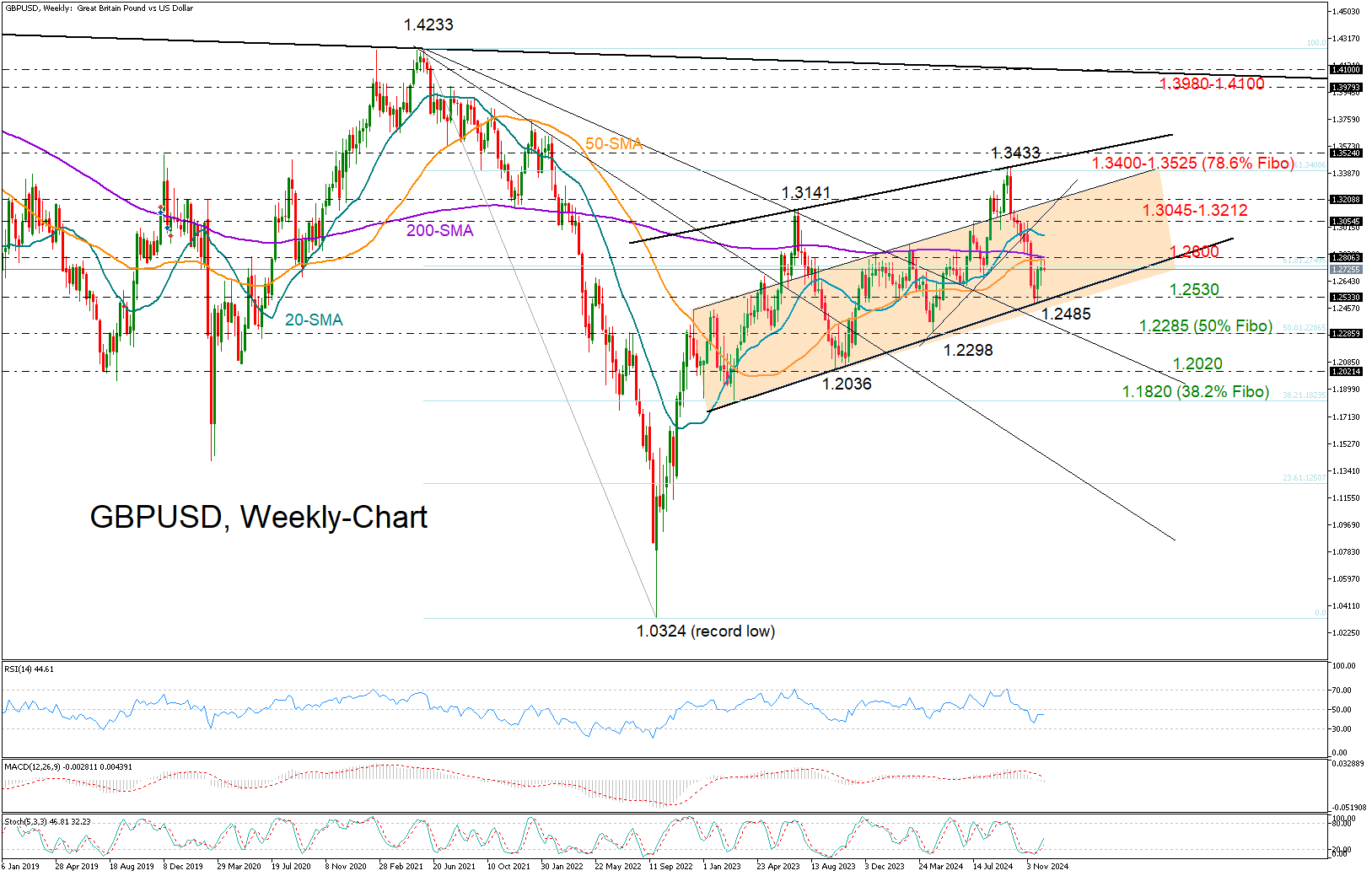

GBPUSD: May chase more gains

GBPUSD did not have an impressive performance either but a political shift to the left in July and a relatively more conservative rate cut policy from the Bank of England offset selling pressures, leaving the pair with a negligible gain of 0.36% year-to-date.

Inflation is back above the central bank’s 2.0% target and the impact from the new fiscal budget, which forces businesses to increase their social insurance contribution in April, is unknown. With futures markets suggesting a relatively gradual monetary easing, and the UK chancellor hoping for an ambitious economic partnership with the EU, GBPUSD could remain supported. However, a struggling economy and trade disputes could prevent a trend continuation toward the pre-pandemic levels above 1.4000.

Having rotated near a familiar ascending trendline, there is potential for a continuation higher as both the RSI and the stochastic oscillator have changed direction to the upside. A confirmation could come above 1.2800, while a completion of a golden cross between the 50- and 200-weekly simple moving averages (SMAs) could fuel more optimism, shifting the spotlight toward the next barrier at 1.3045-1.3212. A steeper increase could face a major battle within the 1.3400-1.3525 area.

Alternatively, a slide below 1.2530 could see a test of the 50% Fibonacci retracement of the 2021-2022 downtrend at 1.2285. If that floor cracks, the selloff could exacerbate toward the 1.2020 support area or even lower to the 38.2% Fibonacci of 1.1820. Additional declines from there would downgrade the long-term picture.

The mean estimate for December 2025 from 50 key global financial institutions reporting to Refinitiv is at 1.2800 versus 1.2672 predicted for December 2024. The highest forecast is at 1.3600 and the lowest is at 1.2000.

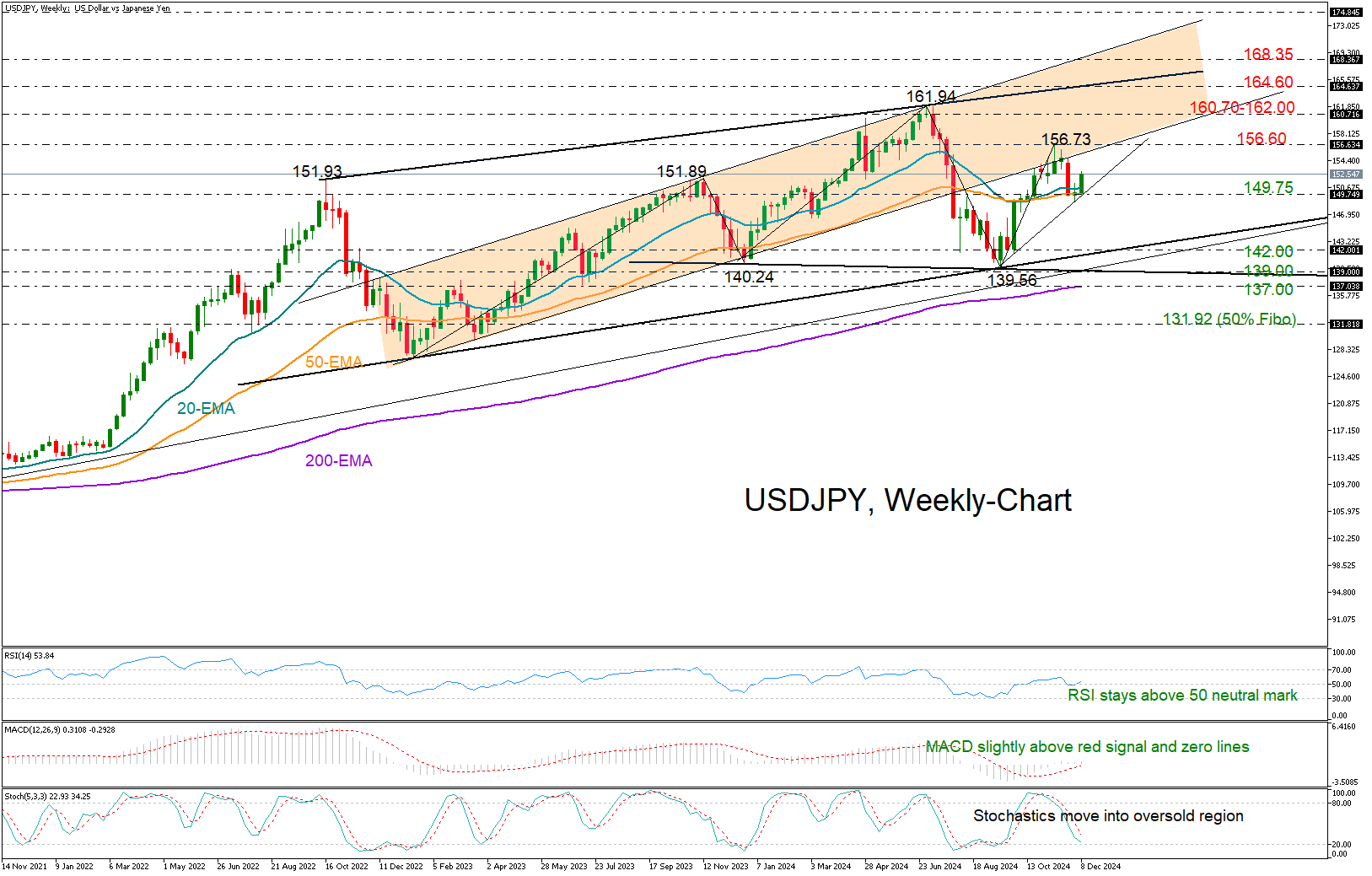

USDJPY: Could sail through the waves

USDJPY is up 8.11% year-to-date, rebounding from a summer sell-off to remain above 150.00 as the Fed leaned towards gradual rate cuts.

With President Trump lifting his threat to fire Jay Powell before his term ends in 2026, monetary guidance could produce continuity. The greenback has been benefiting from resilient economic conditions. Hence, the health of the US economy and particularly inflation and employment expectations could be key catalysts for the greenback as investors are uncertain about the impact of Trump’s potential deep tax cuts and import tariffs. On the other hand, potential rate hikes delivered by the BoJ could weigh on the pair.

Technically, USDJPY seems to be trading within a bullish channel, recently setting a foothold near its 20- and 50-weekly SMAs at 149.75. If that floor holds and the bulls pierce through the 156.60 wall, the recovery phase could extend toward July’s multi-year top of 161.94 or mark a new higher high near the channel’s upper band currently seen near 164.60. Then, the spotlight could fall on the steep ascending line at 168.35, a break of which could see an acceleration toward 174.85.

Still, the technical outlook is not completely out of risks. A bearish head and shoulders pattern could take shape if the price confirms a lower high at 156.73 and subsequently corrects below the 139.00 area. If the 200-weekly exponential moving average (EMA) currently at 137.00 proves fragile too, the pair could suffer a painful decline toward 131.92.

The mean estimate for December 2025 from 50 key global financial institutions reporting to Refinitv is at 147.00 versus 151.75 predicted for December 2024. The highest forecast is at 160.00 and the lowest at 125.00.

Week Ahead – Fed, BoJ and BoE Conclude End-Year Policy Decisions

- Fed seen cutting in December, pausing in January

- BoJ leans towards keeping rates steady

- BoE seen ending 2025 on the sidelines as well

- Flash PMIs, UK and Canada CPIs, and core PCE also on tap

Fed seen taking the sidelines in January

Following the RBA, the BoC, the SNB and the ECB, the central bank bonanza continues next week, with the Fed on Wednesday, and the BoJ and the BoE on Thursday.

Although Wednesday’s data suggested that US inflation was a little bit hotter than in October, market participants became more convinced that the Fed will press the rate-cut button next week, almost fully penciling in a quarter-point reduction. Having said that though, the probability for policymakers taking the sidelines in January has soared to around 80%.

It seems that market participants took the words of several policymakers seriously, who appeared willing to vote in favor of a rate cut at the upcoming meeting, but they also stuck to their guns that a slower rate-reduction path moving forward is necessary.

That belief may be the result of president-elect Trump’s pledge to impose hefty tariffs on imports from around the globe, especially China, as well as his promise for massive corporate tax cuts. These policies are seen as fueling inflation, which has been proving sticky even before Trump’s plans are enacted.

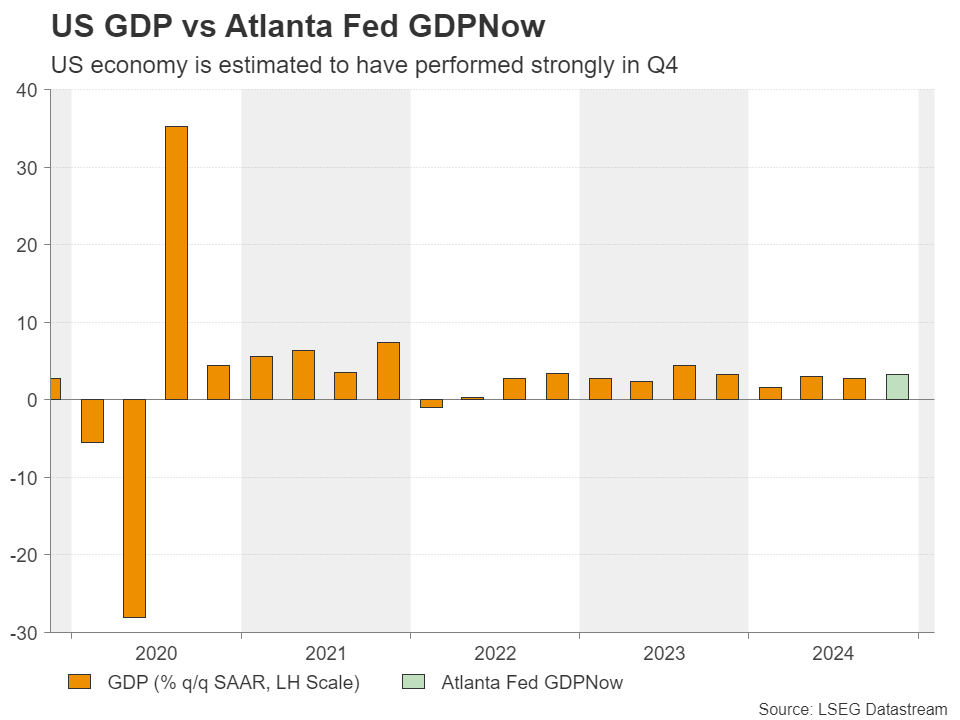

The stellar performance of the US economy corroborates the notion that Fed officials do not need to rush into lowering interest rates, something also noted by Fed Chair Powell himself. The Atlanta Fed GDP now model is pointing to a strong 3.3% QoQ SAAR growth in Q4, while the latest employment report confirmed that the labor market remains robust and that October’s dismal print was just an outlier, a one-off occasion due to strikes and adverse weather conditions.

Mind the dots

With all that in mind, a 25bps cut itself is unlikely to shake the markets much. Investors may focus more on hints and clues on how likely a January pause is, as well as on how many rate cuts policymakers are contemplating throughout 2025.

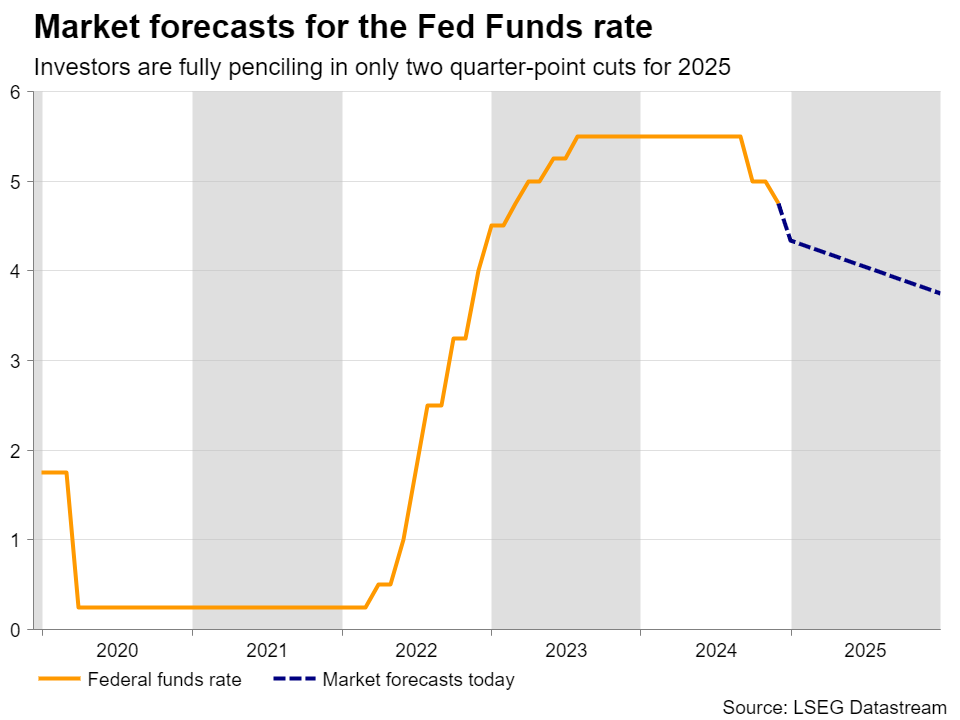

Taking next week’s reduction out of the equation, Fed fund futures are pointing to another 50bps worth of reductions by next December. Combined with an already strong chance for a pause at the first gathering of the year, this poses some downside risks for the US dollar.

Even if Fed Chair Powell corroborates the notion of a January pause, a median dot for 2025 pointing to more than 50bps worth of rate cuts could disappoint market expectations and thereby weigh on the greenback. At the same time, bets of lower-than-currently expected borrowing costs combined with Trump’s tax cuts, may be celebrated on Wall Street, with equity indices continuing to explore uncharted territories.

Bank of Japan - to hike or not to hike?

Passing the ball to the BoJ, up until very recently, investors were expecting 15bps worth of a rate increase at this gathering, or a 60% chance for a quarter-point hike. However, that probability dropped to around 25% after board member Nakamura said that, although he is not opposed to rate hikes, the decision should be data dependent.

His remarks disappointed those expecting the BoJ to finish the year with a hike, but yet, traders are nearly fully pricing in a quarter-point increase by March as Governor Ueda and his colleagues maintained their readiness to hike again due to an expanding economy, rising wages, and above-target inflation.

This means that there are upside risks for the yen. A rate hike by the BoJ next week could offer strong support, but even if officials decide to stand pat, strong hints that an increase at the turn of the year is warranted could still prove beneficial.

BoE appears in no rush to cut rates

A few hours later, the central bank torch will be passed to the BoE. Contrary to the Fed, investors are seeing only a 10% chance of a 25bps cut at this gathering. They are not even fully pricing in one before March.

Last month, policymakers lowered the Bank rate from 5.0% to 4.75% but raised their inflation forecasts as finance minister Reeves announced massive government spending in her first budget.

Combined with recent remarks from Governor Bailey that there is still “a distance to travel”, this prompted investors to anticipate no action before the turn of the year and around 75bps worth of reductions by the end of 2025.

The relatively hawkish BoE bets helped the pound to be the only major currency that has not lost ground against the greenback in 2024, and to strongly outperform the neighboring euro as the ECB is expected to cut interest rates by another 115bps in 2025. Trump’s tariff threats pose another risk for the Eurozone and the common currency.

Ergo, should the BoE maintain a hawkish stance, the pound is likely to remain supported. It could even finish the year higher against the US dollar if the Fed disappoints current market expectations.

Flash PMIs, CPIs and more

What could add extra pressure on the euro next week may be another round of disappointing PMIs on Monday. The preliminary numbers from France and Germany are coming out ahead of the Eurozone’s prints and signs of more economic struggles in these two nations, which are also face political uncertainty, could intensify headaches for euro traders.

The UK and US preliminary S&P Global PMIs are also out on the same day, but they may attract less attention than the Euro area prints as pound and dollar traders may have their attention fixed on the BoE and Fed central bank decisions.

That said, pound traders may be tempted to incorporate the UK jobs data for October and the UK CPI numbers for November, due out on Tuesday and Wednesday, into their expectations heading into Thursday’s decision. So, the pound could experience some early volatility before Bailey and co. announce their decision. The UK retail sales are due out on Friday.

On Friday, the agenda also includes the US core PCE index for October, which is the Fed’s preferred inflation gauge and is accompanied by the personal income and spending data for the same month.

Speaking about inflation, following the BoC’s decision to cut interest rates by 50bps this week, loonie traders may turn their attention to Canada’s CPI data on Wednesday.

Although policymakers opted for the bigger move, Governor Macklem said that further reductions would be more gradual. Now, investors are seeing a 40% probability for the Bank to stand pat at the January meeting and signs of inflation stickiness may increase that chance, thereby adding some support to the Canadian dollar.

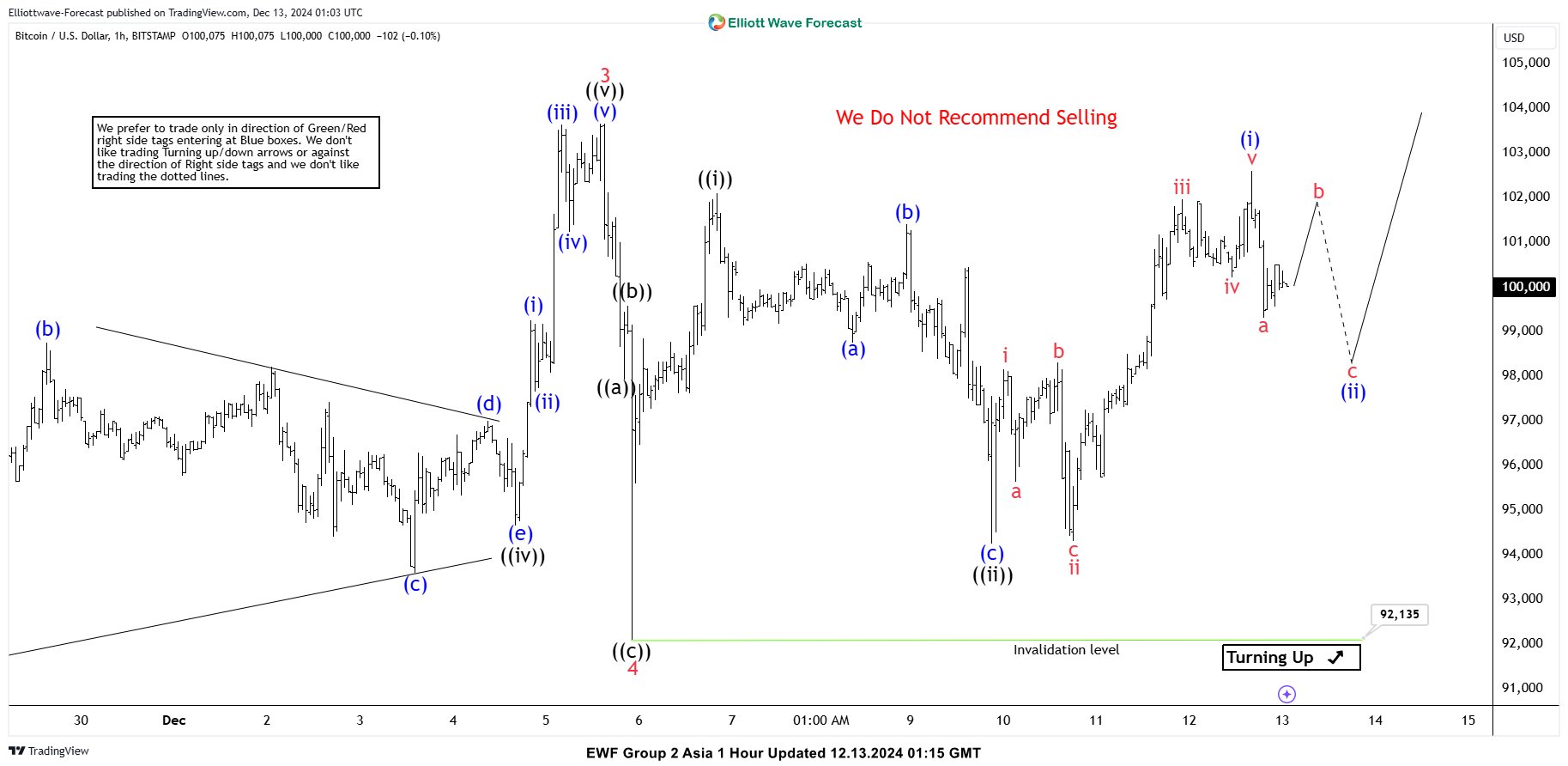

Bitcoin BTCUSD Forecasting the Rally After 3 Waves Pull Back

Hello fellow traders. In this technical article we’re going to take a quick look at the Elliott Wave charts of Bitcoing BTCUSD , published in members area of the website. As many of our members are aware, the crypto has given us good buying opportunities recently. BTCUSD is showing impulsive bullish sequences in the cycle from the 52598 low , that are calling for a further strength. In the further text we are going to explain the Elliott Wave Forecast.

BTCUSD Elliott Wave 1 Hour Chart 12.10.2024

BTCUSD completed wave 4 (red) at the 92154 low and wave ((ii)) (black) at the 94275 low. Both corrections formed Elliott Wave Zig Zag patterns. Currently, we are near completing the intraday pullback (ii) (blue). As long as the price stays above the 94275 low, and more importantly above the 92154 low, we expect further strength in the crypto. This could ideally lead to new highs. We advised against selling

BTCUSD Elliott Wave 1 Hour Chart 12.13.2024

Bitcoin held above the 94275 low and rallied further, as expected. The current view suggests that we completed a 5-wave rally from the 94275 low, labeled as (i) blue. We may see a 3-wave pullback toward the 50-61.8% Fibonacci zone, around 98392-97406, before more upside. The next target area to the upside is between 106326 and 110716.

Ethereum (ETHUSD) Forecast: Anticipating the Rally After a 3-Wave Pullback

Hello fellow traders. In this technical article we’re going to take a quick look at the Elliott Wave charts of Ethereum (ETHUSD) , published in members area of the website. As many of our members are aware, the crypto is showing impulsive bullish sequences in the cycle from the August 2024low , that are calling for a further strength. In the further text we are going to explain the Elliott Wave Analysis.

ETHUSD Elliott Wave 1 Hour Chart 12.10.2024

ETHUSD completed wave 4 (blue) at the 3490 low, forming Elliott Wave Zig Zag pattern. Currently, we are close to completing the intraday pullback ((ii)) (black). As long as the price stays above the 3490 low, we expect further strength in the crypto. This could potentially lead to new highs. We advise against selling and prefer the long side.

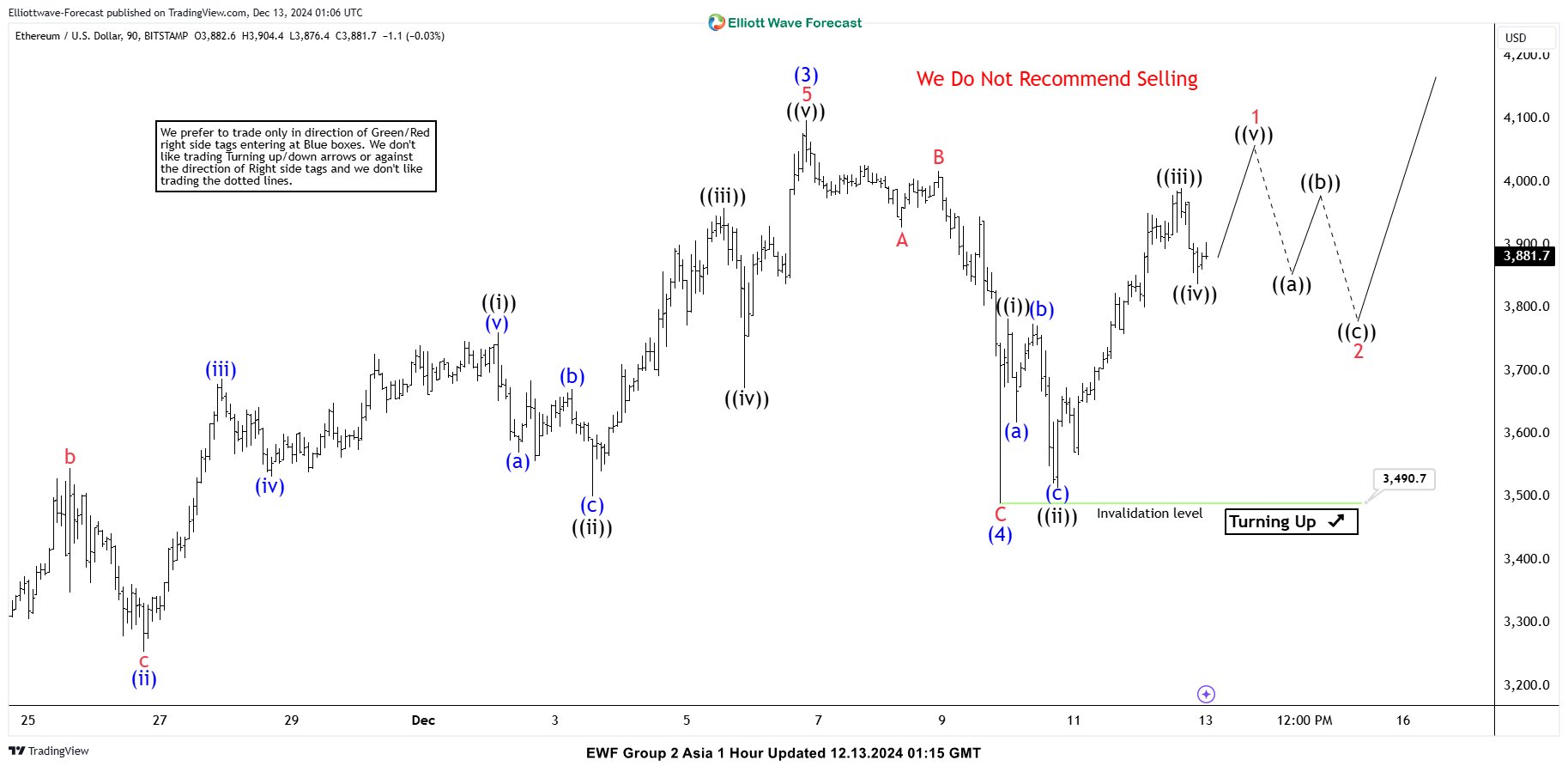

ETHUSD Elliott Wave 1 Hour Chart 12.13.2024

Ethereum held above the 3490 low and rallied further, as expected. The current view suggests that we’ve completed 3 waves up so far. Another high would be ideal to complete the 5-wave cycle from the 3490 low. A break above the (3) blue peak (the December 6th high) would confirm that the next leg up is in progress. After this break, we can look to buy intraday dips again in the 3, 7, and 11 swings.