Sample Category Title

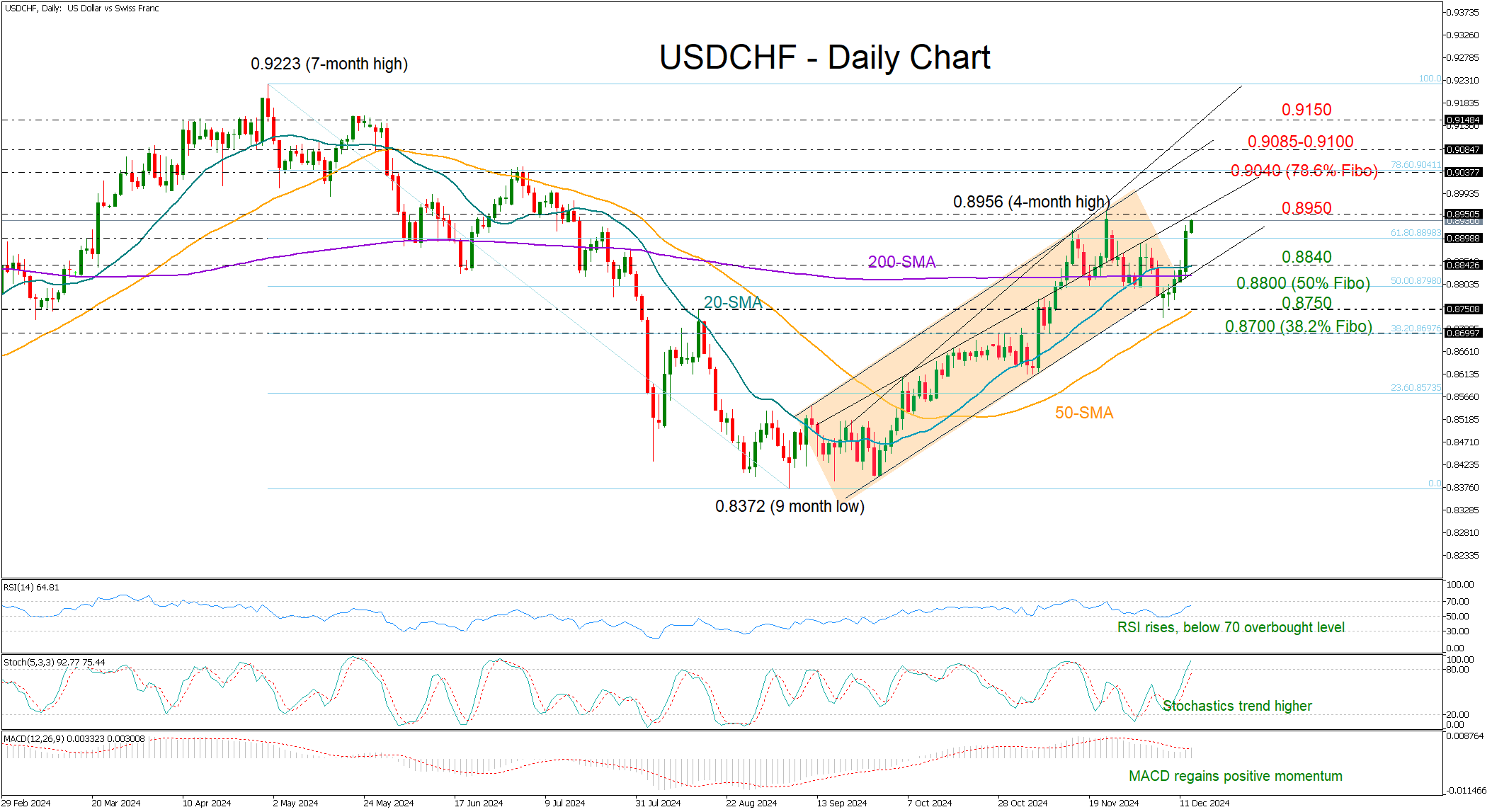

USDCHF Bulls Back and Want to Stay

- USDCHF bounces back, dismisses bearish risks below 0.8800

- Bulls take control, aim for new higher highs

USDCHF staged an impressive rebound after falling as low as 0.8733, an action which initially seemed like the completion of a bearish head and shoulders pattern below the 200-day simple moving average and the 0.8800 number.

Now back in a bullish channel, the pair is willing to meet November’s high of 08956. There is more fuel in the tank according to the technical indicators as the RSI and the stochastic oscillator are rising and are still some distance below their overbought levels. Another encouraging sign is the bullish cross between the 20- and 200-day SMAs, which signals a trend continuation to the upside.

If the price were to close above the 0.8950 zone, the rally could gear up to the 0.9040 barrier, the 78.6% Fibonacci retracement of the previous downtrend. A victory there could provide fresh impetus toward the 0.9070-0.9100 constraining region, while a faster rally could reach the 0.9150 mark.

On the downside, sellers may wait for a slide below the 20-day SMA at 0.8840 before targeting the 50% Fibonacci of 0.8800. An extension lower could pause near the 50-day SMA at 0.8750 and if this cracks as well, putting the upward trend into question, there might be a quick decline toward the 38.2% Fibonacci of 0.8700.

In summary, USDCHF is bullish in the short-term picture and could mark new higher highs if the 0.8950 bar gives the green light.

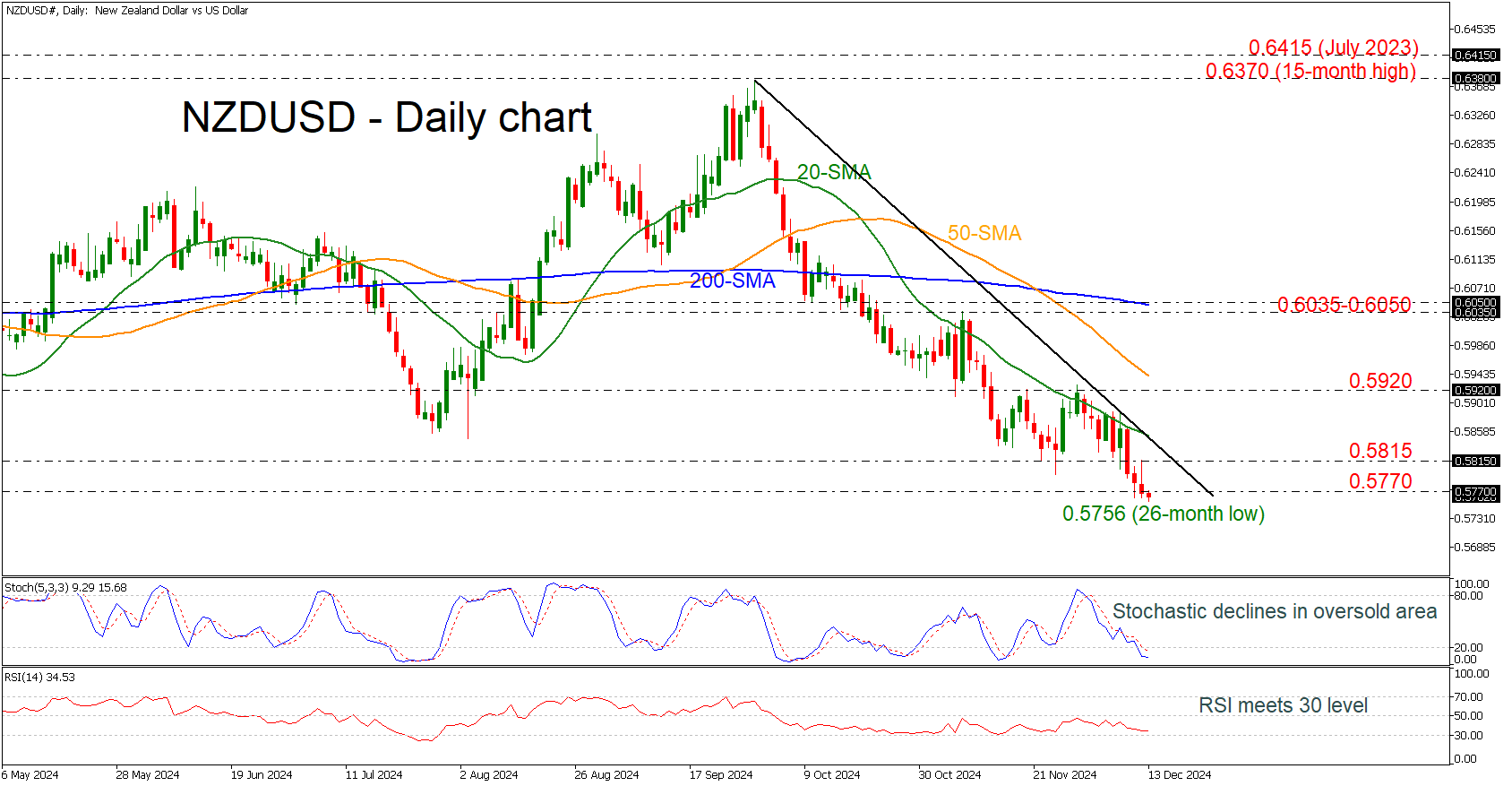

NZDUSD Dives to 26-Month Low

- NZDUSD continues the strong selling interest

- Stochastic and RSI keep moving south

NZDUSD plunged to a fresh lower low, recording a 26-month low at 0.5756. The pair is endorsing the steep descending tendency that started on September 30 with the technical oscillators confirming the negative momentum. The stochastic is standing in the oversold area, while the RSI is falling near the 30 level.

If the market continues with its bearish structure, the next levels for traders to keep in mind are the round numbers of 0.5700 and 0.5600 before the October 2022 bottom at 0.5510.

On the other hand, if the bulls gain control, the pair could touch the 0.5770 immediate resistance, followed by the 0.5815 level and the 20-day simple moving average (SMA) at 0.5850, which coincides with the downtrend line. A break above this area could pave the way for a test of the 0.5920 resistance ahead of the 50-day SMA at 0.5940.

In a nutshell, NZDUSD is significantly heading south in the short-term view, being ready to exit the long-term trading range of 0.6380-0.5770.

Gold Prices Recovered, But Future Hinges on USD Trends

Gold prices stabilised around 2,690.00 USD per troy ounce on Friday. The quotes fell by almost 1% in the previous session, as investors assessed the latest US economic data. The statistics prompted a rally in the yields of US treasury bonds.

US manufacturing prices rose more than expected in November, fuelling concerns about the future trajectory of inflation, which could climb further and remain above the Federal Reserve's 2025 target.

Meanwhile, initial claims for unemployment benefits reached a two-month high, significantly exceeding forecasts and underscoring risks of a deterioration in the US labour market.

Investors continue to expect the US Federal Reserve to lower interest rates by 25 basis points next week. They also anticipate future rate cuts in 2025, although their magnitude is uncertain.

A Federal Reserve rate cut is a positive signal for Gold. As the precious metal does not generate coupon yield, rate reductions lower the opportunity cost of holding Gold, making such investments more attractive for traders.

Technical analysis of XAU/USD

The Gold market has established a consolidation range around the level of 2,675.55. Following an upward breakout, a growth wave pushed the price to 2,726.26. A corrective movement towards 2670.66 is unfolding, after which another upward movement towards 2,743.85 is anticipated. This bullish scenario is supported by the MACD indicator, with its signal line positioned above zero and indicating upward momentum.

On the H1 chart, Gold is undergoing a correction towards 2,670.66. A rise to 2,697.77 could occur shortly, followed by a potential decline to the same level. Once this target is achieved, the possibility of initiating a new growth wave to 2,735.70 is expected, with a possible further extension to 2743.85. This analysis is corroborated by the Stochastic oscillator, whose signal line is currently above 50 and moving towards 80, suggesting continued upward potential.

AUD/USD: Surviving at 0.6360 Key Support (For Now) But Long-Term Trend Remains Bearish

- RBA has shifted to a less hawkish monetary policy stance.

- The interest rate swaps market has started to price in a higher chance of the first RBA interest rate cut to come in February 2025.

- The 2-year and 10-year yield spreads between Australian government sovereign bonds and US Treasuries continued to narrow.

- Growing risk for AUD/USD to stage a major bearish breakdown below 0.6360.

The price actions of the AUD/USD have tumbled as expected since our last publication and hit the 0.6400/0.6360 major support zone as highlighted. The Aussie dollar was the worst performer among the major currencies as it shed -2.70% against the US dollar based on a one-month rolling basis as of 13 December.

RBA has turned less hawkish

Fig 1: Major trends of 2-year & 10-year yield spreads of AU sovereign bonds/US Treasuries as of 13 Dec 2024 (Source: TradingView, click to enlarge chart)

Even though the Australian central bank, RBA maintained its policy cash rate at 4.35% during its last monetary policy meeting of 2024 on Tuesday,10 December, unchanged for the ninth consecutive time, RBA Governor Bullock has sounded less hawkish now versus her prior press conferences.

During her press conference on Tuesday, she highlighted inflationary pressures had declined in Australia, and RBA officials had also taken notice of the weakness in the private sector of the economy. Hence, it is a dovish tilt that moves in line with the tonality of RBA’s latest monetary statement which stated, “some of the upside risks to inflation appear to have eased”.

The interest rate swaps market has started to price in a higher chance of the first RBA interest rate cut to come in early Q1 next year with a chance of around 70% on a February easing. The RBA is the sole developed nation central that has yet to cut interest rates, other than the Bank of Japan (BoJ) which is an outlier.

In addition, the 2-year and 10-year yield spreads between Australian government sovereign bonds and US Treasuries have continued to narrow and are trading at -0.28% and -0.03% respectively (see Fig 1). These observations suggest that Australia’s fixed-income market is getting less attractive than US fixed-income instruments which indirectly may assert longer-term downside pressure on the AUD/USD.

Bearish momentum remains intact

Fig 2: AUD/USD medium-term& major trends as of 13 Dec 2024 (Source: TradingView, click to enlarge chart)

The price actions of the AUD/USD have continued to oscillate within a medium-term descending channel since its retest on the long-term secular descending trendline resistance from February 2021 swing high on 30 September 2024.

It has broken below a major ascending trendline from the 13 October 2023 swing low and it is now testing the major support at 0.6360 (swing lows of 26 October 2023, 19 April 2024, and 5 August 2024).

In addition, the daily RSI momentum indicator has continued to exhibit bearish conditions which suggests further potential weakness in the price actions of AUD/USD.

0.6560 key medium-term pivotal resistance (also the 50-day moving average), and a break with a daily close below 0.6360 may trigger a multi-week to multi-month impulsive down move sequence with the next medium-term supports coming in at 0.6200 and 0.6130.

However, a clearance above 0.6560 negates the bearish tone for a potential squeeze up to retest the next medium-term resistances at 0.6690 and 0.6810.

GBP/USD Declines Following UK GDP Data Release

Today, the UK GDP changes for October were published, as reported by Forex Factory (month-on-month):

→ Actual = -0.1%;

→ Forecast = +0.1%;

→ Previous = -0.1%.

The data revealed a slowing UK economy, defying analysts’ optimistic expectations. According to Reuters and other outlets, the latest GDP figures:

→ Could strengthen traders’ expectations of a more rapid interest rate cut by the Bank of England in 2025;

→ Undermine the target announced last week by Prime Minister Keir Starmer to make the UK the fastest-growing economy among G7 nations.

Technical Analysis of the GBP/USD 4-Hour Chart

→ From its December high (when a false breakout of the psychological 1.29 level occurred), the pound has weakened by approximately 1.4%, with the RSI indicator dipping into oversold territory for the first time this month.

→ The bullish trajectory (highlighted in blue), formed since late November, has lost its relevance after a breakout, suggesting bears are attempting to resume the downtrend within the red-shaded channel.

→ The 1.2615 level, which has repeatedly influenced the price (marked with arrows), may continue to act as support.

Looking ahead, the Bank of England’s meeting next Thursday is likely to trigger heightened volatility. While interest rates are expected to remain unchanged, any surprises could significantly impact the current bearish momentum.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

AUDCHF: Bearish Outlook

The Australian Dollar (AUD) edged higher on Thursday, recovering some ground against the US Dollar (USD) after the release of US jobs data. The AUDUSD pair is trading at 0.6392, marking a 0.36% increase. Mixed US economic data impacted the Greenback. The US Bureau of Labor Statistics (BLS) reported that initial jobless claims jumped to 242,000 for the week ending December 7, surpassing expectations of 220,000. Meanwhile, November's Producer Price Index (PPI) data showed headline inflation rose 3% year-on-year, exceeding the forecast of 2.6%. Core PPI also climbed to 3.4% year-on-year, higher than the projected 3.2%. Despite this, the US Dollar Index (DXY) remained firm at 106.79.

On the other hand, strong Australian employment figures supported the AUD. Job growth in November beat estimates, with 35,600 jobs added versus the expected 25,000, while the unemployment rate dipped to 3.9%, better than the forecast of 4.2%.

Due to the optimistic employment data, the market odds for a February rate cut by the Reserve Bank of Australia (RBA) dropped from 70% to 50%. However, the RBA maintained a dovish tone, expressing confidence that inflation is steadily moving toward its target.

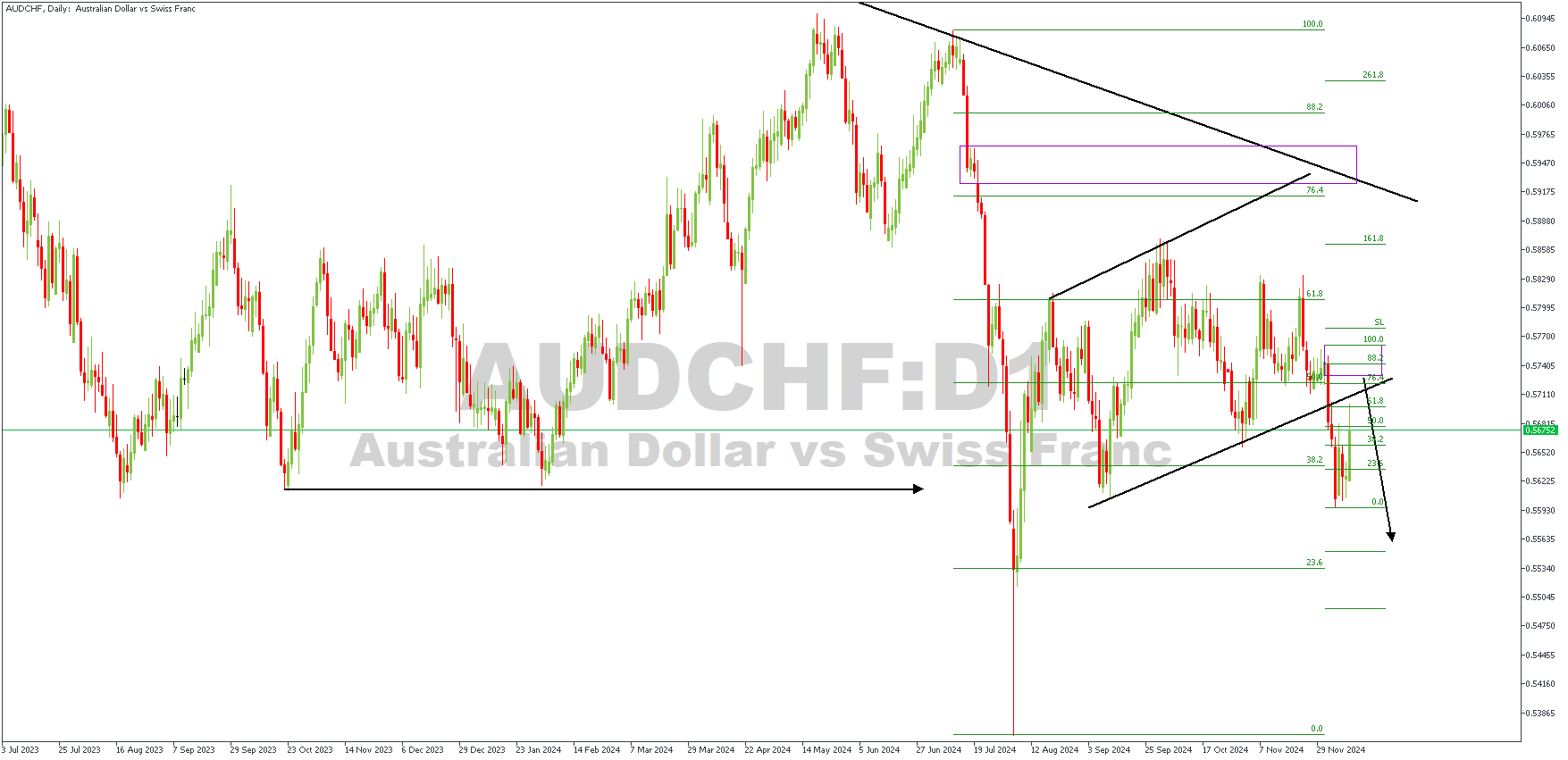

AUDCHF – D1 Timeframe

On the daily timeframe price chart of AUDCHF, we see that the price has recently broken below the trendline support of a channel pattern and is currently retracing toward the trendline for a retest. The trendline enjoys confluence from factors like the rally-base-drop supply zone and the 76% Fibonacci retracement level.

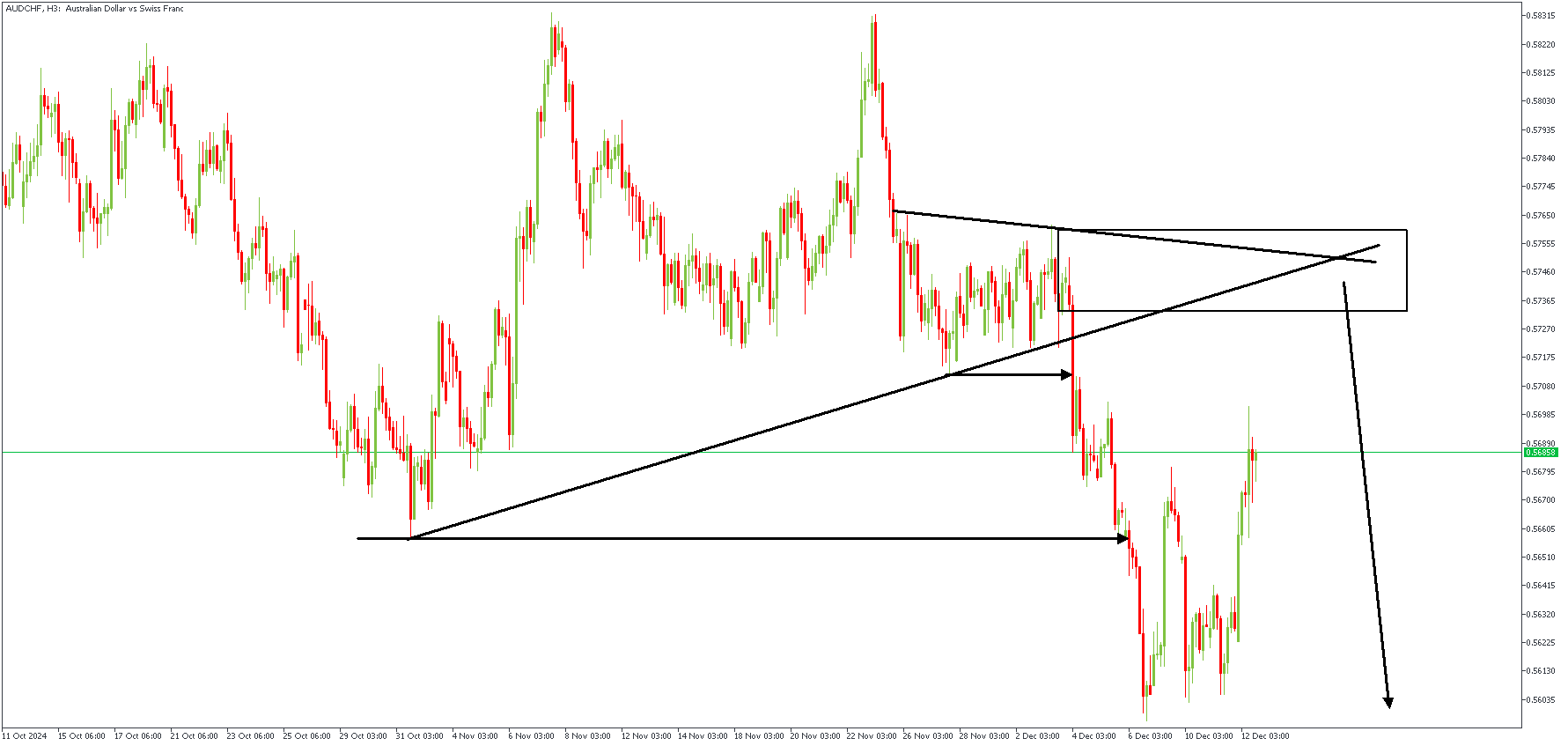

AUDCHF - H3 Timeframe

The 3-hour timeframe lends further support to the bearish argument. We see the confluence of two resistance trendlines converging within the supply zone. On this basis, a rejection from the highlighted zone can be considered a bearish entry.

Analyst's Expectations:

- Direction: Bearish

- Target: 0.55510

- Invalidation: 0.57631

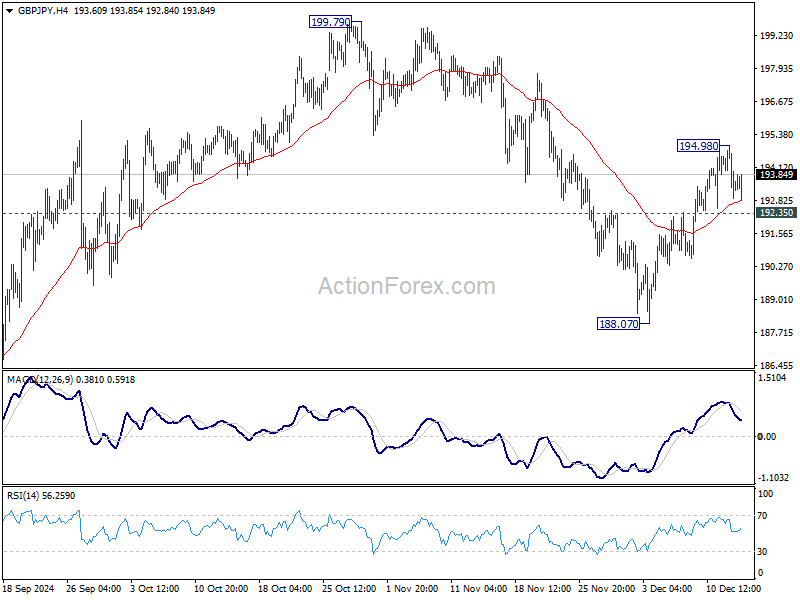

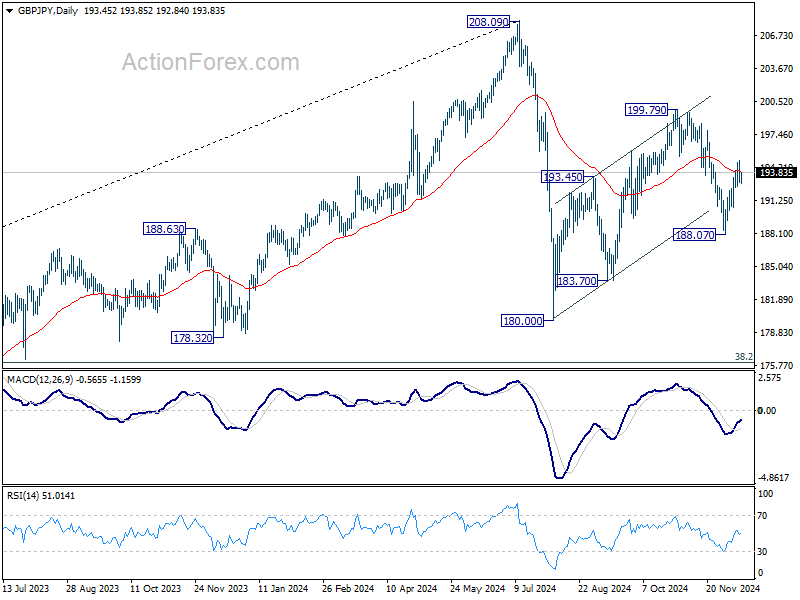

GBP/JPY Daily Outlook

Daily Pivots: (S1) 192.60; (P) 193.80; (R1) 194.66; More...

Intraday bias in GBP/JPY is turned neutral again with current retreat. On the downside, break of 192.35 minor support will bring deeper fall to 188.07. Firm break there will revive the bearish case that whole corrective rise from 180.00 has completed with three waves up to 199.79. On the upside, above 194.98 will resume the rebound towards 199.79 resistance.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

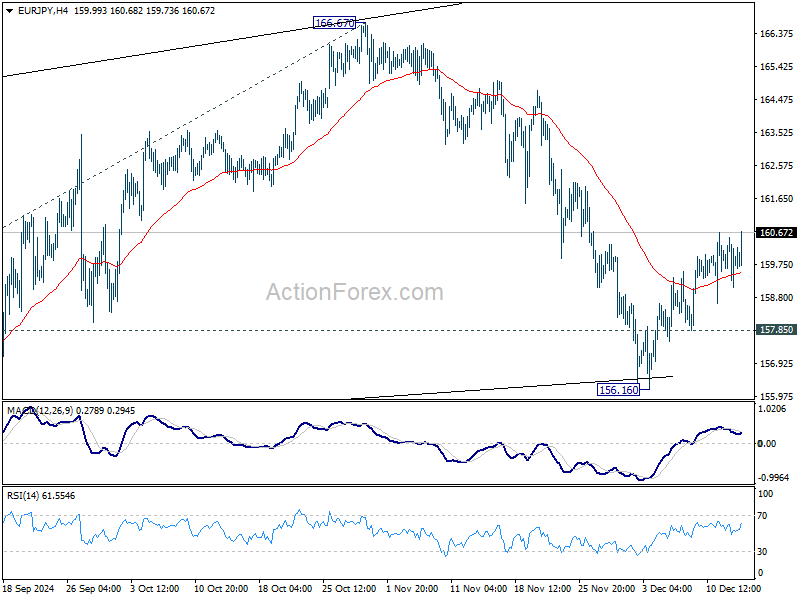

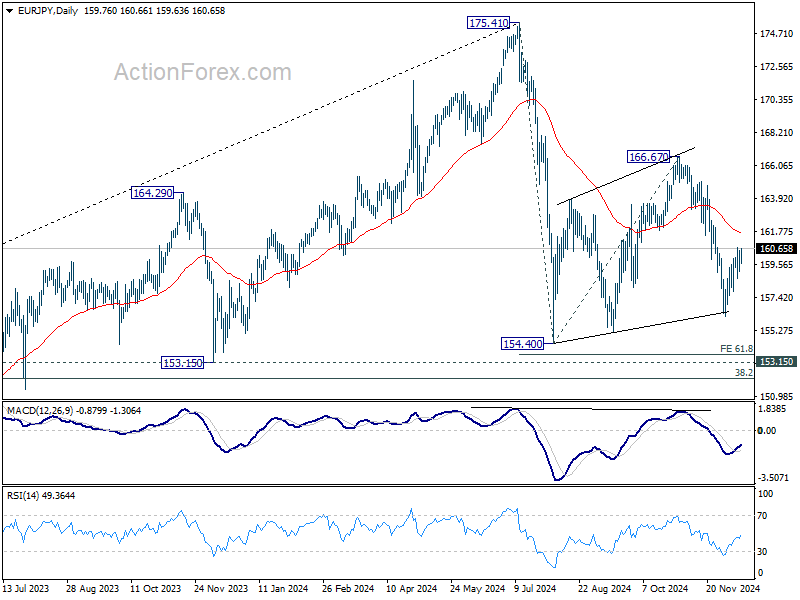

EUR/JPY Daily Outlook

Daily Pivots: (S1) 159.08; (P) 159.81; (R1) 160.52; More...

No change in EUR/JPY's outlook. While rebound from 156.16 might extend higher, it's still seen as a corrective rise. Further decline is expected as long as 55 D EMA (now at 161.65) holds. On the downside, below 157.85 minor support will bring retest of 156.16 first. Break there will target 154.40 low next.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

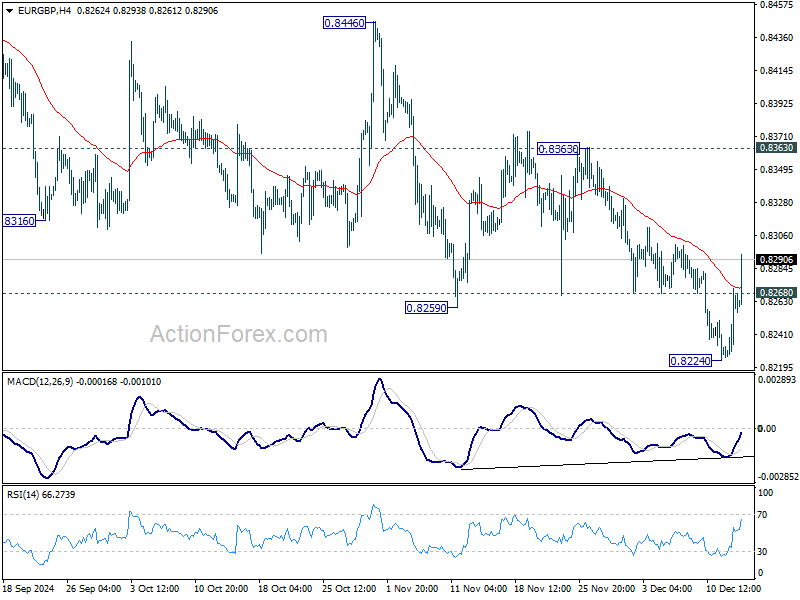

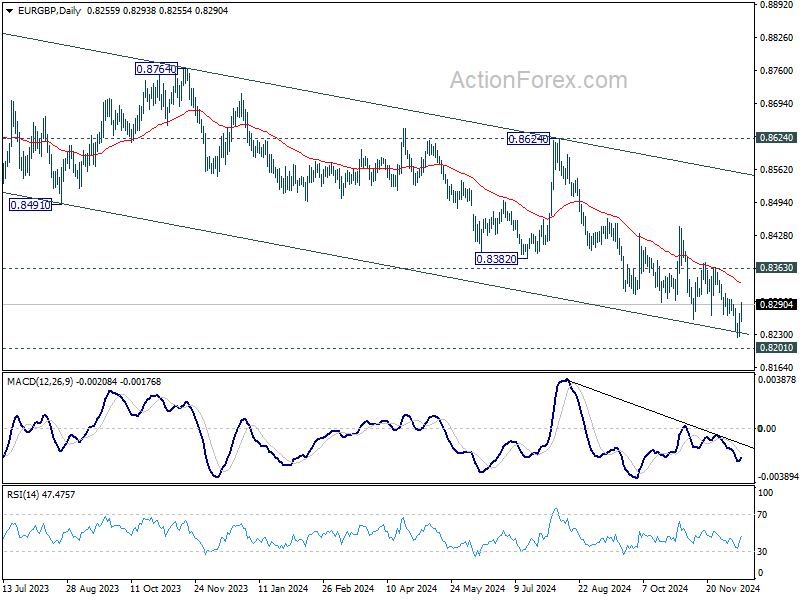

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8233; (P) 0.8253; (R1) 0.8279; More...

EUR/GBP rebounded strongly ahead of 0.8201 support. Considering the strong momentum, intraday bias is back on the upside for 0.8363 resistance. Decisive break there will be suggest near term bullish reversal and target 0.8446 resistance and above. In case of another decline through 0.8224, focus will be on bottoming sign as it approaches 0.8201 again.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

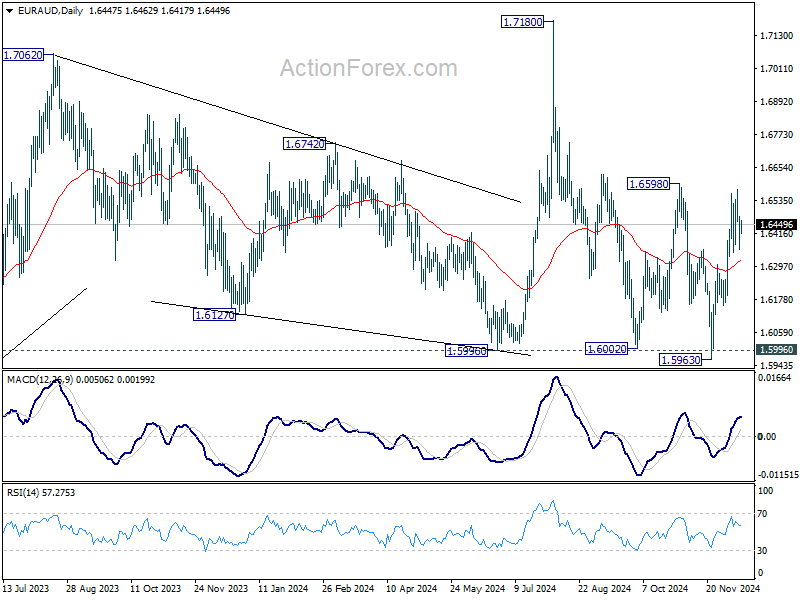

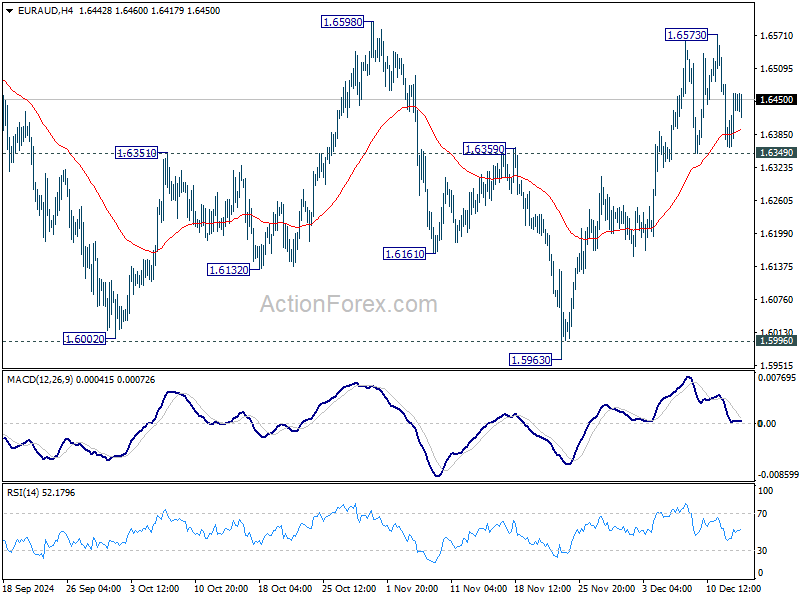

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6368; (P) 1.6429; (R1) 1.6496; More...

Intraday bias in EUR/AUD stays neutral and more consolidations could be seen. But further rally remains in favor as long as 1.6349 support holds. On the upside, decisive break of 1.6598 resistance should confirm that whole fall from 1.7180 has complete with three waves down to 1.5963. Further rise should then be seen to retest 1.7180 next. Nevertheless, firm break of 1.6359 will indicate rejection by 16598, and turn bias back to the downside.

In the bigger picture, EUR/AUD is still holding on to 1.5996 key support despite brief breach. Larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5995 will indicate that such up trend has completed. Deeper decline would be seen to 61.8% retracement of 1.4281 to 1.7180 at 1.5388, even as a correction.