Sample Category Title

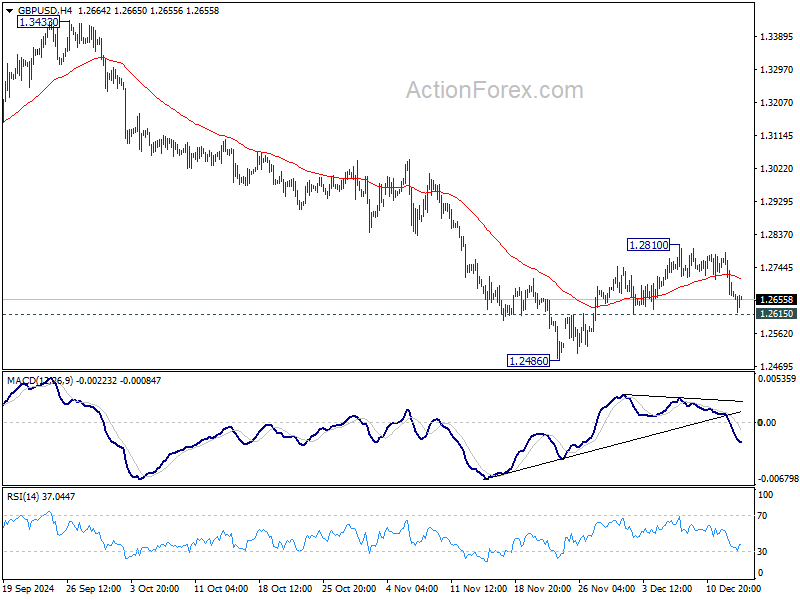

Cable Dips Further After Weak UK Data, Consolidation May Precede Fresh Push Lower

GBPUSD fell further on Friday, holding in red for the third consecutive day, driven by stronger dollar and additionally pressured by unexpectedly weak UK Oct GDP numbers.

Fresh weakness tested support at 1.2618 (last week’s low / 100WMA) and pressure nearby Fibo support at 1.2610 (61.8% retracement of 1.2487/1.2811 upleg), where bears faced headwinds.

Near term action may pause for consolidation, before renewed attack at 1.2618/10 pivots, loss of which to open way towards next targets at 1.2563/40 (Fibo 76.4% / lower 20-d Bollinger band) and expose key short-term supports at 1.2500 / 1.2487 (psychological / Nov 22 low).

Initial resistance lays at 1.2673 (20DMA) guarding 1.2700/11 (psychological / falling 10DMA) which should cap upticks and keep near-term bears in play.

Daily studies are predominantly negative (MA’s in bearish setup / south-heading 14-d momentum is approaching the centreline) with additional negative signals from weekly chart (reversal pattern is forming / converging 10/200WMA about to form death-cross).

Res: 1.2673; 1.2711; 1.2735; 1.2750

Sup: 1.2619; 1.2563; 1.2500; 1.2487

Sunset Market Commentary

Markets

European yields and the euro today gained minor further ground after succeeding an intraday reversal yesterday after the ECB 25 bps cut (to 3.0%). First post-meeting comments from ECB policy makers confirmed that more easing will follow. Internal debate on the pace (Kazaks still keeps the door open for a bigger step) and the end-point continues (Villeroy sees bets on 100 bps + easing as reasonable). Still, gradualism apparently is seen guiding ECB policy for now (Centeno, amongst others). Comments didn’t change the recent tentative bottoming in EMU yields. German yields today add between 1.0 bps (2.0-y) and 2.5 bps (10-y). US yields show a broadly similar pattern (2-y + 1.5 bps; 30-y +2.5 bps) as markets are counting down to next week’s FOMC meeting. French president Macron naming François Bayrou as new Prime minister (cf infra) had only limited impact on markets. The euro initially also tried a (corrective?) rebound. EUR/USD intraday filled offers in the 1.052 area, but the move ran into resistance as US traders joined (currently 1.05). The 1.0335 support survives going into the weekend. The yen underperformed. The BOJ Tankan report published this morning was ok, but it wasn’t able to counterbalance market rumours that the BOJ considers to wait with a rate hike at next weeks policy meeting. UD/JPY extends its recent rebound (153.4). Equities in EMU (Eurostoxx 50 and S&P 500 +0.3%) show modest gains. Oil also gains marginally ($ 73.6 p/b).

Sterling of late outperformed the euro as it was considered avoiding/being less sensitive to a long range of negative developments that haunted the single currency. However, a set of mixed UK data grabbed the market focus today. According to UK GFK confidence, UK consumers turned a bit more optimistic on their personal financial situation, but still have low confidence on the overall UK economy, currently and in the year ahead. UK monthly production (October) was unexpectedly weak (-0.6% M/M after already a 0.5% monthly decline in September). Services and construction output also disappointed resulting in a -0.1% monthly GDP estimate. Mid-morning, the BOE/Ipsos inflation attitudes survey showed that consumers assessed current inflation to have declined (4.8% from 5.2% in August), but expectations on future inflation rose again for all time horizons (3.0% from 2.7% 12 months ahead, 2.8% from 2.6% in the following year and 3.4% to 3.2% long term). Weak activity and high inflation expectations for sure isn’t something for the BoE to feel comfortable about. UK yields currently trade marginally higher (1 bp across the curve), but doesn’t help sterling. EUR/GBP earlier this week looked like preparing a real test of the key 0.8203 2022 low. Today’s data apparently provided the perfect mix for investors to scale back some EUR/GBP shorts. The pair jumped from 0.826 to currently test the 0.83 big figure, admittedly with some minor support from the euro, too.

News & Views

Fresh Bundesbank forecasts suggest the German economy will barely grow next year after having contracted this year. 2024 forecasts were lowered form a 0.3% growth prediction in June to -0.2% while output next year would expand by just 0.2% (vs 1.1% earlier). The Bundesbank does not exclude another year of negative growth if president-elect Trump makes good on his tariffs threats. If he would slap a 10% levy on European imports and 60% on Chinese goods, Buba estimates this could knock between 0.2-0.6 ppts of GDP next year. “The German economy is not only struggling with persistent economic headwinds, but also with structural problems,” Bundesbank President Joachim Nagel said, adding that the labour market is now also showing signs of finally succumbing. Growth for 2026-2027 is seen at 0.8% and 0.9%. Inflation would ease from 2.5% this year to 2.4-2.1-1.9% in the following years.

French president Macron announced François Bayrou as France’s new prime minister. His predecessor Michel Barnier, presiding over a minority government, was ousted last week in a no-confidence vote after pushing through a budget bill that angered the opposition from (far) left and right. Bayrou is a centrist politician with a market-oriented view of the economy but equally supports social measures such as taxing the wealthy. His appointment, however, immediately drew oppositional backlash from all sides of the political spectrum. It suggests his task of addressing France’s derailed public finances won’t be much easier than Barnier’s. Assuming unrelenting opposition from the political extremes, Bayrou will need support of the Socialists and perhaps the Greens without alienating the right-wing flank to pass a budget. France budget deficit is expected at 6% of GDP this year, double the 3% EU limit.

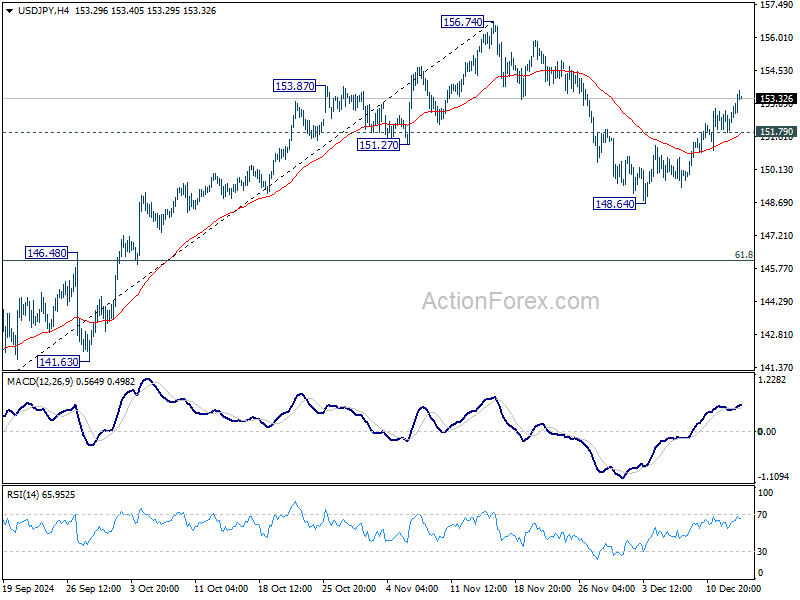

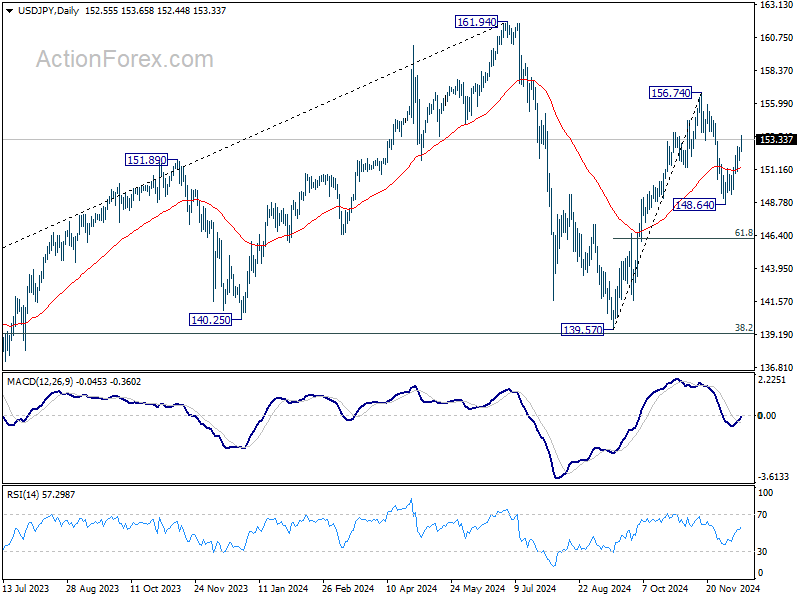

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 152.05; (P) 152.41; (R1) 153.03; More...

USD/JPY's rally from 148.64 is still in progress, and intraday bias stays on the upside for retesting 156.75. Firm break there will confirm resumption of whole rally from 139.57. On the downside, below 151.79 minor support will turn intraday bias neutral first. But risk will stay on the upside as long as 148.64 support holds, in case of retreat.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

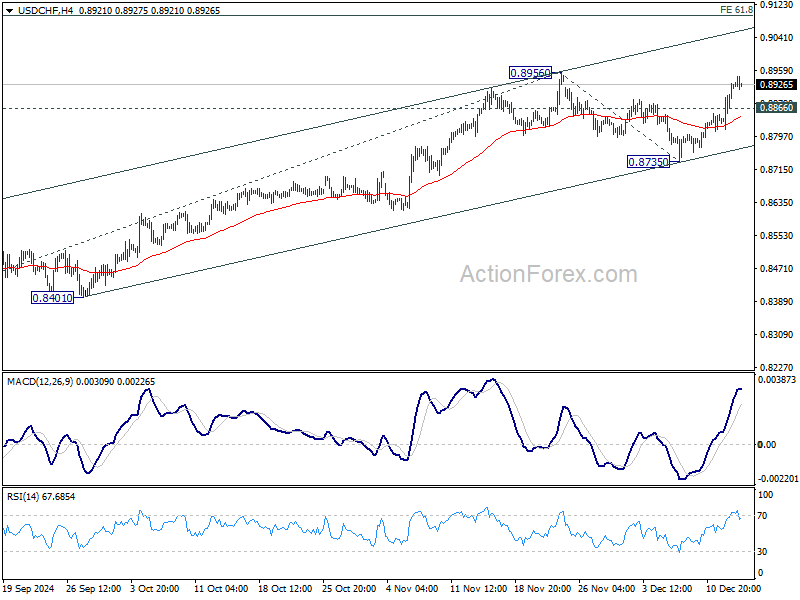

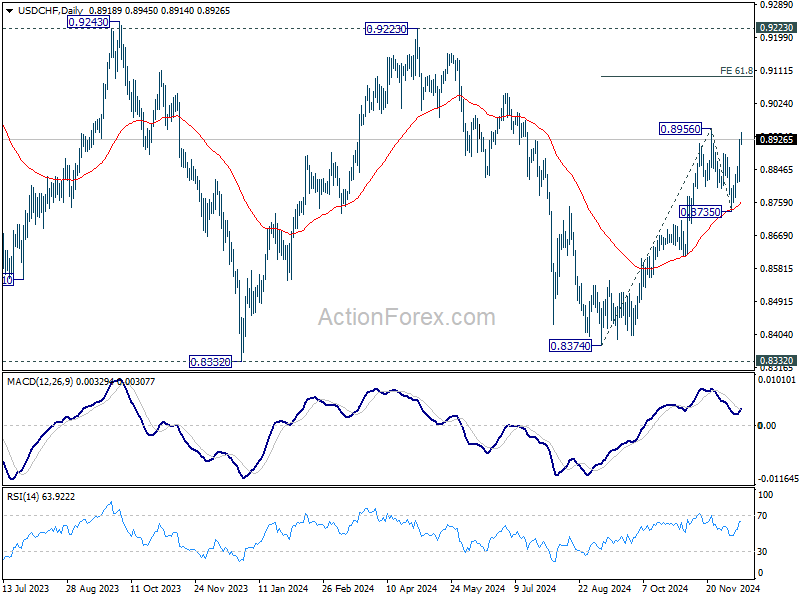

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8851; (P) 0.8890; (R1) 0.8962; More…

Intraday bias in USD/CHF remains on the upside for the moment. Firm break of 0.8965 resistance will resume the whole rally from 0.8374. Next target is 61.8% projection of 0.8374 to 0.8956 from 0.8735 at 0.9095. On the downside, below 0.8866 minor support will turn intraday bias neutral first. But risk will stay on the upside as long as 0.8735 support holds, in case of retreat.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

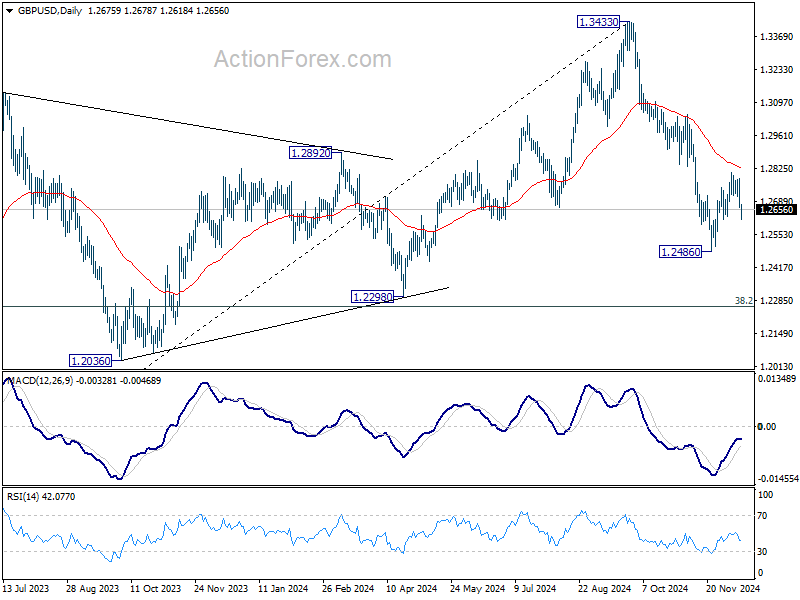

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2631; (P) 1.2710; (R1) 1.2752; More...

GBP/USD is still holding above 1.2615 minor support with today's decline. Intraday bias remains neutral first. Decisive break of 1.2615 will confirm that corrective rebound from 1.2486 has completed at 1.2810 already. Retest of 1.2486 should be seen next, and break there will resume whole decline from 1.3433 to 1.2298 cluster support zone.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern.

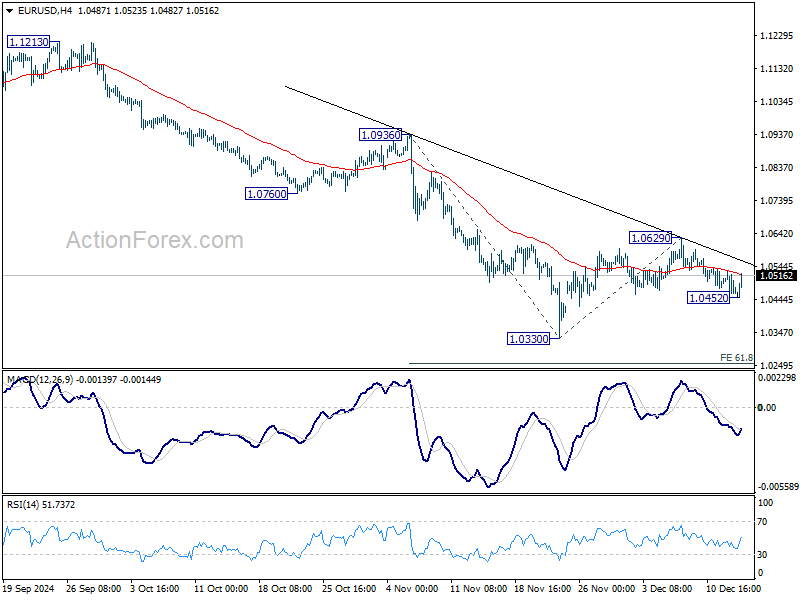

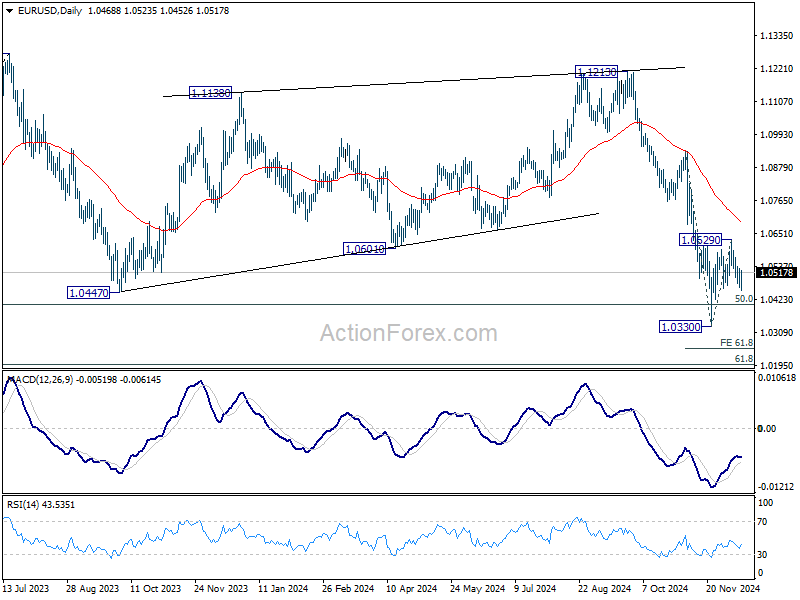

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0443; (P) 1.0487; (R1) 1.0510; More...

EUR/USD recovered notably after dipping to 1.0452 briefly and intraday bias is turned neutral again. Outlook is unchanged that corrective rise from 1.0330 should be completed at 1.0629, and further decline is expected. Below 1.0452 will bring retest of 1.0330, and then resume the fall form 1.1213 to 61.8% projection of 1.0936 to 1.0330 from 1.0629 at 1.0254. Also, in this case, sustained trading below 1.0404 key fibonacci level will carry larger bearish implication.

In the bigger picture, focus stays on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.

Euro Rebounds on ECB Gradualism, Sterling Struggles

The Euro rebounded broadly today, buoyed by reassurances from a number of ECB officials that the central bank remains committed to a gradual approach to policy easing. Yesterday's 25bps rate cut appears to have had solid consensus backing, with no indications that a more aggressive 50bps cut was even seriously debated. Despite recent economic softness in the Eurozone, ECB is maintaining a measured strategy without overreacting to weak activity data. Though the Euro remains lower against the Dollar for the week, its recovery against Sterling and Swiss Franc adds momentum to its performance.

Sterling, however, faced a challenging session after UK GDP data revealed a contraction for October, undermining confidence in the government’s recent pledge to boost economic growth. While this setback adds pressure to an already fragile outlook, it is unlikely to shift BoE’s stance on policy easing significantly. A BoE survey released today highlighted that long-term inflation expectations have risen to 3.4% in November, the highest level since May 2022, up from 3.2% in August. Additionally, the survey revealed that 33% of respondents expect interest rates to rise in the next 12 months, compared to 29% in the previous quarter. These findings suggest BoE will maintain its gradual approach to rate adjustments.

Overall for the week so far, Dollar is currently the strongest, followed by Aussie, and then Loonie. Yen is the worst, followed by Swiss Franc, and then Kiwi. Euro and Sterling are positioning in the middle.

In Europe, at the time of writing, FTSE is up 0.04%. DAX is up 0.08%. CAC is up 0.22%. UK 10-year yield is up 0.0185 at 4.383. Germany 10-year yield is up 0.371 at 2.248. Earlier in Asia, Nikkei fell -0.95%. Hong Kong HSI fell -2.09%. China Shanghai SSE fell -2.01%. Singapore Strait Times rose 0.03%. Japan 10-year JGB yield fell -00103 to 1.041.

ECB officials signal more rate cuts Ahead, gradual path to neutral

A day after ECB reduced its deposit rate by 25 basis points to 3.00%, key ECB officials provided insights into the central bank's outlook, reinforcing expectations for further easing in 2025. Comments from various members of the Governing Council suggest a shared commitment to a cautious but consistent approach to policy normalization.

French ECB Governing Council member François Villeroy de Galhau explicitly stated, “There will be more rate cuts next year, more rate cuts plural,” emphasizing alignment with market forecasts. The swap market currently prices around 120 basis points of rate reductions by the end of 2025.

Similarly, Spanish member José Luis Escrivá noted the prevailing consensus for “moves of 25 basis points downwards,” allowing for regular assessment of disinflationary progress.

Irish ECB member Gabriel Makhlouf highlighted the clarity in the rate trajectory while maintaining a data-driven approach: “The exact pace and number of further reductions depend on inflation outturns continuing to move in line with our projections.”

Portuguese member Mário Centeno added that rates could approach the 2% level within a few quarters, barring new economic shocks.

Comments from Luxembourg’s Gaston Reinesch pointed to the possibility of reaching a 2.5% deposit rate by early spring, implying consecutive 25bps cuts in January and March.

Latvian member Martins Kazaks kept the door open for larger adjustments if warranted, while Austria’s Robert Holzmann reiterated alignment with forecasts, noting that rates would ultimately settle closer to neutral.

Eurozone industrial production stagnates in Oct

Eurozone industrial production stagnated in October, recording 0.0% mom growth, in line with expectations. The data reflects mixed performance across sectors. While output for capital goods rose by 1.7%, intermediate goods production remained unchanged. On the downside, energy production dropped sharply by -1.9%, while durable and non-durable consumer goods contracted by -1.8% and -2.3%, respectively,.

Across the broader EU, industrial production showed a modest increase of 0.3% mom, driven by strong gains in select countries. Ireland led the pack with a 5.7% increase, followed by Denmark at 5.4% and Poland at 3.5%. However, significant declines were observed in Lithuania (-7.5%), Belgium (-6.2%), and Croatia (-3.9%).

UK economy contracts -0.1% mom in Oct, dragged down by weak production

UK GDP fell by -0.1% mom in October, disappointing expectations for 0.1% mom growth. The decline was primarily driven by a -0.6% mom contraction in production output, with no growth observed in services and a -0.4% mom decline in construction output.

On a rolling three-month basis, GDP showed a marginal increase of 0.1% in the period ending October, compared to the prior three-month period. This modest growth was supported by a 0.1% expansion in services and a 0.4% rise in construction output. However, production output contracted by -0.3%, weighing on overall performance.

Japan's Tankan Survey: Manufacturing Confidence Improves to 14

Confidence among Japan’s major manufacturers showed a modest recovery in Q4, breaking a two-quarter decline. The Tankan large manufacturing index rose to 14 from 13, slightly exceeding market expectations. However, the outlook dipped marginally from 14 to 13, though still better than the anticipated 11.

In contrast, the non-manufacturing sector, which includes services, saw its index decline to 33 from 34, marking the first deterioration in two quarters. The outlook for non-manufacturers held steady at 28.

On a bright note, large Japanese companies across sectors plan to boost capital expenditure by 11.3% in the fiscal year ending March 2025. This is a notable increase from the 10.6% projection in the September survey and surpasses market forecasts of 9.6%.

NZ BNZ PMI falls to 45.5, 21st month of contraction

New Zealand’s BNZ Performance of Manufacturing Index dipped from 45.7 to 45.5 in November, marking its lowest reading since July 2024 and extending the contraction streak to 21 consecutive months. Despite some improvement in select components, the sector remains under significant strain, highlighting the challenges of achieving a meaningful turnaround.

Production weakened further, dropping from 44.0 to 42.5, signaling continued struggles in output. New orders also plunged from 48.5 to 44.8, underlining the persistent lack of demand. In contrast, employment improved modestly from 46.0 to 46.9, and finished stocks edged higher from 47.8 to 49.3. Deliveries saw the most notable recovery, rising from 44.9 to 49.9, yet still narrowly missed returning to expansion territory.

The sentiment among respondents remains predominantly negative, with 56% of comments in November reflecting pessimism, slightly up from 53.5% in October. Recurring concerns revolve around weak order volumes and the enduring pressures of high living costs. However, this negativity has moderated from its peak of 71.1% in mid-2024, suggesting some stabilization.

Doug Steel, Senior Economist at BNZ, noted that while manufacturers are beginning to show improved confidence about the future, “the main message of a manufacturing sector still under significant pressure remains. There is scant evidence of a general turnaround in activity to date.”

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0443; (P) 1.0487; (R1) 1.0510; More...

EUR/USD recovered notably after dipping to 1.0452 briefly and intraday bias is turned neutral again. Outlook is unchanged that corrective rise from 1.0330 should be completed at 1.0629, and further decline is expected. Below 1.0452 will bring retest of 1.0330, and then resume the fall form 1.1213 to 61.8% projection of 1.0936 to 1.0330 from 1.0629 at 1.0254. Also, in this case, sustained trading below 1.0404 key fibonacci level will carry larger bearish implication.

In the bigger picture, focus stays on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.

ECB officials signal more rate cuts Ahead, gradual path to neutral

A day after ECB reduced its deposit rate by 25 basis points to 3.00%, key ECB officials provided insights into the central bank's outlook, reinforcing expectations for further easing in 2025. Comments from various members of the Governing Council suggest a shared commitment to a cautious but consistent approach to policy normalization.

French ECB Governing Council member François Villeroy de Galhau explicitly stated, “There will be more rate cuts next year, more rate cuts plural,” emphasizing alignment with market forecasts. The swap market currently prices around 120 basis points of rate reductions by the end of 2025.

Similarly, Spanish member José Luis Escrivá noted the prevailing consensus for “moves of 25 basis points downwards,” allowing for regular assessment of disinflationary progress.

Irish ECB member Gabriel Makhlouf highlighted the clarity in the rate trajectory while maintaining a data-driven approach: “The exact pace and number of further reductions depend on inflation outturns continuing to move in line with our projections.”

Portuguese member Mário Centeno added that rates could approach the 2% level within a few quarters, barring new economic shocks.

Comments from Luxembourg’s Gaston Reinesch pointed to the possibility of reaching a 2.5% deposit rate by early spring, implying consecutive 25bps cuts in January and March.

Latvian member Martins Kazaks kept the door open for larger adjustments if warranted, while Austria’s Robert Holzmann reiterated alignment with forecasts, noting that rates would ultimately settle closer to neutral.

Eurozone industrial production stagnates in Oct

Eurozone industrial production stagnated in October, recording 0.0% mom growth, in line with expectations. The data reflects mixed performance across sectors. While output for capital goods rose by 1.7%, intermediate goods production remained unchanged. On the downside, energy production dropped sharply by -1.9%, while durable and non-durable consumer goods contracted by -1.8% and -2.3%, respectively,.

Across the broader EU, industrial production showed a modest increase of 0.3% mom, driven by strong gains in select countries. Ireland led the pack with a 5.7% increase, followed by Denmark at 5.4% and Poland at 3.5%. However, significant declines were observed in Lithuania (-7.5%), Belgium (-6.2%), and Croatia (-3.9%).

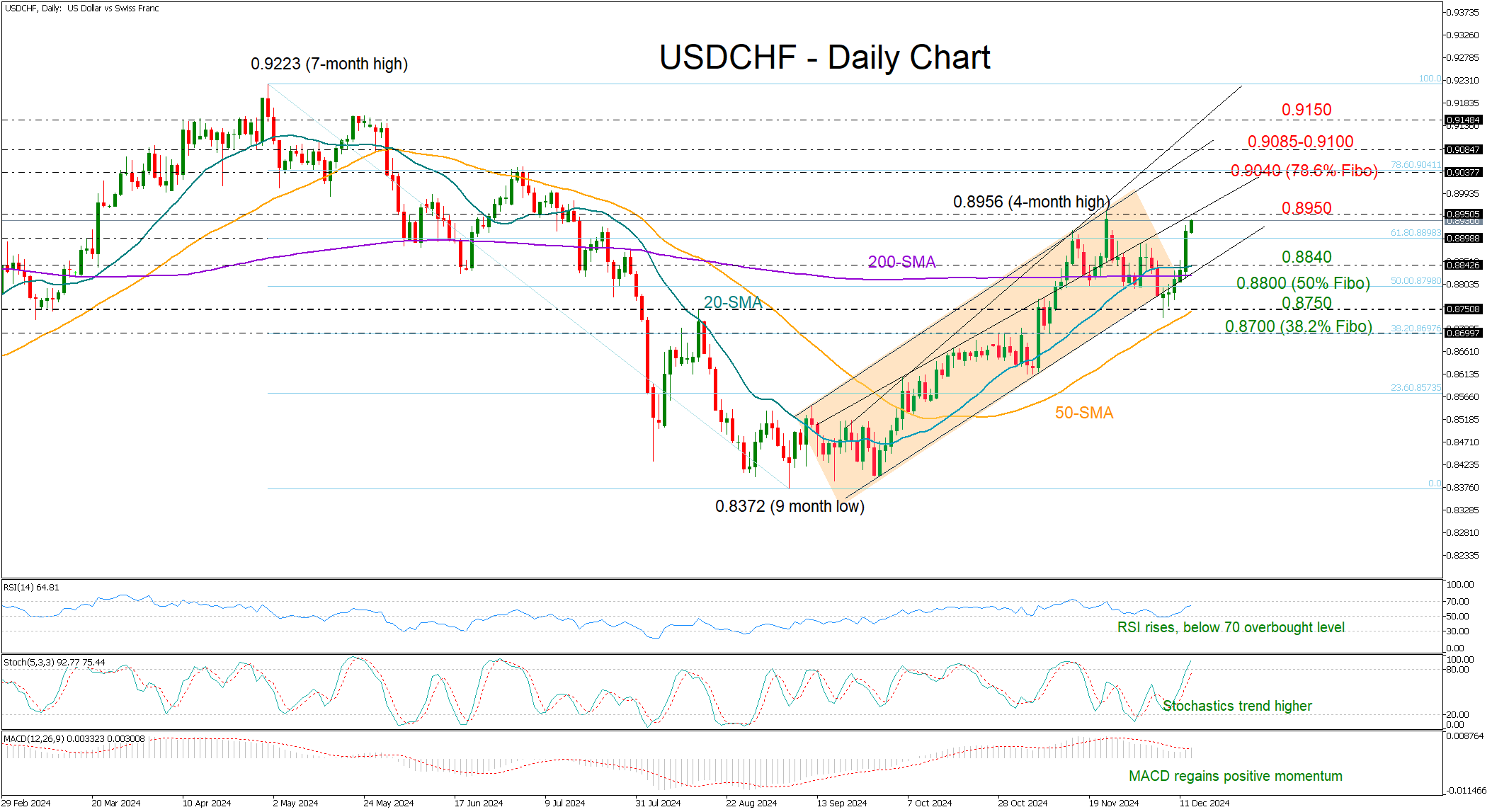

USDCHF Bulls Back and Want to Stay

- USDCHF bounces back, dismisses bearish risks below 0.8800

- Bulls take control, aim for new higher highs

USDCHF staged an impressive rebound after falling as low as 0.8733, an action which initially seemed like the completion of a bearish head and shoulders pattern below the 200-day simple moving average and the 0.8800 number.

Now back in a bullish channel, the pair is willing to meet November’s high of 08956. There is more fuel in the tank according to the technical indicators as the RSI and the stochastic oscillator are rising and are still some distance below their overbought levels. Another encouraging sign is the bullish cross between the 20- and 200-day SMAs, which signals a trend continuation to the upside.

If the price were to close above the 0.8950 zone, the rally could gear up to the 0.9040 barrier, the 78.6% Fibonacci retracement of the previous downtrend. A victory there could provide fresh impetus toward the 0.9070-0.9100 constraining region, while a faster rally could reach the 0.9150 mark.

On the downside, sellers may wait for a slide below the 20-day SMA at 0.8840 before targeting the 50% Fibonacci of 0.8800. An extension lower could pause near the 50-day SMA at 0.8750 and if this cracks as well, putting the upward trend into question, there might be a quick decline toward the 38.2% Fibonacci of 0.8700.

In summary, USDCHF is bullish in the short-term picture and could mark new higher highs if the 0.8950 bar gives the green light.