Sample Category Title

Technical Outlook: GBPUSD – Bulls Eye 1.2950/1.3000 Targets, UK GDP Data In Focus

Cable is maintaining bullish near-term bias after strong rally on Thursday that posted new, marginally higher high at 1.2914 but closed few pips below previous top at 1.2904.

Technicals are bullish but overbought on both, daily and weekly chart and warn of correction, although no firmer bearish signals seen so far.

The pair is awaiting release of UK Q1 GDP data, which may boost the price towards 1.2950/1.3000 targets on upside surprise, while release below expectation would deflate the price and risk test pivotal supports at 1.2806 (rising 10SMA) and 1.2770 (former consolidation floor).

Res: 1.2914, 1.2944, 1.3000, 1.3055

Sup: 1.2886, 1.2837, 1.2806, 1.2770

Currencies: Euro Rebound Blocked By Soft Draghi Comments

Sunrise Market Commentary

- Rates: Dovish Draghi pushes European bonds higher

Today's trading may be interesting. Eco data may be slightly bond negative, but overwhelmed by geopolitical risk & weekend habit to de-risk positions, end-of month buying, technical consideration (Bund) and the impact of yesterday's ECB meeting (European bonds). - Currencies: Euro rebound blocked by soft Draghi comments

Yesterday, EUR/USD declined off the recent recovery top as ECB's Draghi dismissed calls for a policy normalization. Today , the EMU CPI and the US Q1 growth take center stage. There might be some further profit taking on the EUR/JPY and EUR/USD if sentiment on risk eases and if European bond yields decline further after yesterday's soft ECB speak.

The Sunrise Headlines

- US equities ended nearly flat (Dow, S&P) to modestly higher (NASDAQ). The S&P held within reach of the all-time highs but a retest didn't occur maybe as investors wanted to see results of Alphabet & Amazon and Q1 GDP.

- Asian equities show modest to moderate losses overnight as geopolitical risks on North Korea flared up. Trump said he sees chances of a major, major conflict with the country though he prefers a diplomatic solution.

- A Saturday EU summit in Brussels will serve as a stage for EU leaders to talk up unity and warn British officials against sowing division in the hope of securing a better exit deal. UK PM May said the rest of Europe will line up to oppose us.

- The U.S. government will remain open, for a few days at least. Lawmakers filed a 7-day stopgap spending bill that buys more time for them to cobble together an omnibus package. Trump says he will sign the bill if presented to him.

- Brent oil had a rollercoaster ride, threating the $50/barrel level on news Libya will restart two of its largest oil fields and doubts the OPEC production cuts will be enough to push inventories lower. However, a spectacular rebound followed.

- Alphabet and Amazon spun out some earnings magic. The former posted $20.12 billion in sales, above the $19.75 billion estimate, and profit topped consensus. Amazon beat by 40 cents and projected revenue that may exceed the consensus in Q2. Both shares skyrocket in after trading.

- Busy calendar today with EMU inflation, US, France and UK Q1 GDP releases and US Michigan consumer sentiment highlights going toward next week's FOMC meeting. European earning results include Barclays, Sanofi, RBS…

Currencies: Euro Rebound Blocked By Soft Draghi Comments

Euro rebound blocked after ECB press conference

On Thursday, the Trump tax plan didn't provide clear guidance for the dollar. The focus for euro trading turned to the ECB's press conference. ECB's Draghi kept a balanced message. Good growth is counterbalanced by soft underlying inflation. So, for now, there is no strong enough reason for FX markets to anticipate early steps to policy normalisation. The interest rate differential between the dollar and the euro widened. EUR/USD dropped from 1.09 to the mid 1.08 area and closed the session at 1.0873. USD/JPY held a sideways range in the lower half of 111.

Overnight, Asian equities are ceding modest ground even as some tech bellwethers in the US posted strong results after the close. Geopolitical tensions (North Korea) an end of month profit taking are probably to blame. Japanese eco data were mostly good, confirm a further gradual recovery, but the CPI data remained soft. The yen trades little changed. USD/JPY still holds a tight range in the low 111 area. EUR/USD maintains yesterday's post-ECB decline and trades around 1.0865.

Today, the eco calendar is again well filled. EMU April HICP inflation is expected to rebound to 1.8% Y/Y for the headline and 1% Y/Y for the core from respectively 1.5 and 0.7% Y/Y in March. We see upside risks as German and Spanish CPI surprised on the upside. France, Spain and Belgium publish Q1 GDP figures. We expect solid figures. In the US, Q1 GDP, Michigan consumer sentiment and the Chicago PMI will be published. Q1 GDP is expected at a meagre 1% Q/Qa. Q1 US growth will be disappointing, but risks are on the upside of expectations.

In a daily perspective, the eco data might be mixed for EUR/USD trading. Of late, higher EMU price data had the potential to support the euro, but the figure shouldn't come as a surprise. At the same time, markets look convinced by yesterday's soft ECB inflation assessment. If sentiment on risk would turn a bit softer (end of month profit taking?) and if European yields decline a bit further after yesterday's soft ECB speak, EUR/JPY and the EUR/USD might lose some further ground. A cautious risk sentiment might also be a slightly negative for USD/JPY. So, the topside in EUR/USD looks a bit better protected after this week's rally.

This week, FX trading was driven by the global risk trade as (European) political event risk eased. This supported USD/JPY but also EUR/USD and EUR/JPY. Market speculation that the decline in EMU political event risk could bring forward the ECB normalisation process supports the euro, too. However this hope is erased, at least temporary, after ECB's Draghi's press conference yesterday. From a technical point of view, the rebound of USD/JPY suggests a bottoming out process might have started, but the pair needs to regain the 112.20 level (neckline ST double bottom) to improve the picture. EUR/USD extensively tested the topside of the MT range (1.0874/1.0906 area) late March. The pair returned to the range top after the French election and set minor new highs. We look out how this test turns out. If EUR/USD would regain the 1.10 barrier, next resistance comes in in the 1.1145/1.13 area (US pre/post-election swings). The jury is still out, but we are not convinced that the time is already ripe for a sustained break higher of EUR/USD.

EUR/USD rebound running into resistance as ECB's Draghi dismisses calls for early policy normalization

EUR/GBP

EUR/GBP eases after this week's rebound

Sterling already received a better bid on Wednesday and the rebound continued on Thursday. We didn't see any specific story behind move. Cable jumped temporary north of 1.29 and then settled near the big figure. EUR/GBP drifted back south to the 0.8450 area. At noon, the CBI reported sales were very strong at a multi month high, supported by good weather conditions. The report was sterling supportive, but sterling had already realized an important part of its intraday gains at the time of the publication. In the afternoon, EUR/GBP trading joined the euro decline after the ECB press conference. The pair closed the session at 0.8425 (from 0.8487). Cable finished the session at 1.2904.

Overnight, GFK consumer confidences declined slightly from -6 to -7, in line with expectations. Today, the first estimate of the Q1 UK GDP will be published. An easing of growth to 0.4% Q/Q from 0.7% Q/Q is expected. A soft report shouldn't come as a surprise for markets and only the details from the supply side will be available. So given the GBP positive momentum, we don't expect a strong negative sterling reaction. A softer euro might also weigh slightly on EUR/GBP.

Early last week, EUR/GBP dropped below EUR/GBP 0.84 support, (temporary) improving the sterling picture. The pair came within reach of the key 0.8305 support (Dec low), but no real test occurred. After this week's rebound, the range bottom is better protected. Longer term, Brexit-complications remain a potential negative for sterling. Nevertheless on technical considerations we are inclined to reconsider a cautious EUR/GBP buy-on-dips approach

EUR/GBP correcting lower .as post-Macron rebound peters out

ECB’s Survey Of Professional Forecasters Is Also Due For Release

Market movers today

Today brings US GDP figures for Q1. The Fed Atlanta GDP nowcast shows growth in Q1 of 0.5% q/q AR, softdata indicates growth in the region of 1.5-2.0%. We expect to land somewhere in between and forecast GDP growth of 1.0% q/q AR in Q1.

We will also get PCE core inflation for Q1. If the current trend in monthly PCE core increases continues (implying increases of around 0.1% m/m), PCE core inflation would come in at 2.2% q/q AR. However, note that although this may give the impression that inflation has reached its target, the Fed is more concerned about PCE core inflation y/y, which w ll be significantly below 2% almost no matter what the March print comes in at.

Today, the euro area flash inflation figure is due for release. Following the decline in headline inflation to 1.5% y/y in March, we look for an increase to 1 .8% y/y in April (revised from 1.7% after higher German and Spanish data yesterday). In line with the fall in March, this is due mainly to the early timing of Easter in 2016, which is causing volatility in prices of package holidays. This is also reflected in core inflation, which we estimate will increase to 1.0% y/y in April from 0.7% y/y in March. Looking beyond the Easter volatility, we expect headline inflation to decrease below 1.5% y/y, as the support from the oil price fades, while core inflation should also be back around 0.8-0.9% y/y.

ECB's Survey of Professional Forecasters is also due for release. The longer term (fiveyear) inflation expectations in the survey have been stable at 1.8% over the past year.

In Scandinavia it is t ime for labour data in Norway and retail sales in Norway and Sweden.

Selected market news

The ECB kept policy rates, the QE programme and its forward guidance unchanged at yesterday's meeting: Importantly, the ECB still expects policy rates 'to remain at present or lower levels for an extended period of time. That said, the ECB did sound slightly more optimist icon the euro area growth out look, but still underlined that the underlying inflation pressure remains subdued.

The market took its direction from the inflation comments and European bond markets rallied. Also the comment from Draghi that it was not up to the ECB, but the national central banks to ease the tensions in the repo-market supported especially the short -end of the German curve. The EUR suffered slightly on he 'dovish' interpretation.

The Swedish Riksbank was also seen as 'dovish' yesterday as the QE programme was extended for yet another six months and as the rate path was flattened. Note though that the decision to extend the QE programme was a tie and was only carried out as Governor was in favour. We have been posit ive on Swedish bonds for quite a while and the extension of the QE purchases supported this view. The Swedish krona on the other hand suffered on the QE extension.

The US equity market ended marginally higher as the market tried to digest a whole bunch of policy news ranging from the Trump tax plan, to the mixed signals regarding the future for the Naftatrade agreement and the looming government shut -down. But in factlittle news came during the day to guide the markets.

Daily Technical Outlook And Review: EUR/USD, GBP/USD, AUD/USD, USD/JPY, USD/CAD, USD/CHF, DOW 30, GOLD

A note on lower timeframe confirming price action...

Waiting for lower timeframe confirmation is our main tool to confirm strength within higher timeframe zones, and has really been the key to our trading success. It takes a little time to understand the subtle nuances, however, as each trade is never the same, but once you master the rhythm so to speak, you will be saved from countless unnecessary losing trades. The following is a list of what we look for:

- A break/retest of supply or demand dependent on which way you're trading.

- A trendline break/retest.

- Buying/selling tails ... essentially we look for a cluster of very obvious spikes off of lower timeframe support and resistance levels within the higher timeframe zone.

- Candlestick patterns. We tend to only stick with pin bars and engulfing bars as these have proven to be the most effective.

EUR/USD

Kicking this morning's report off with a quick look-see at the weekly chart shows that the pair remains hovering above the 2016 yearly opening level at 1.0873/ resistance at 1.0819. However, it might be worth waiting for the weekly candle to close shop before presuming that these said resistances are consumed. Down on the daily candles we can see that price has spent last two days easing from a trendline resistance extended from the high 1.0828. Consequent to this, the unit is now positioned within inches of support coming in at 1.0850.

After failing to sustain gains beyond the 1.09 handle yesterday, H4 bears clocked a low of 1.0851. While a bounce from this region could be seen given the aforementioned daily support in play at the moment, the 1.08 handle also looks a reasonable possibility for a bounce.

Our suggestions: Why the 1.08 boundary? Well, It converges beautifully with February's opening level at 1.0801, a H4 AB=CD 161.8% Fib at 1.0794 taken from the high 1.0949 and a H4 61.8% Fib retracement at 1.0784 drawn from the low 1.0682. What's more, notice a daily support is seen just below it at 1.0776 (the next support below the current daily level mentioned above). So, while price could obviously ignore 1.08 today and rally from the current daily support, we feel the 1.08 level quite simply has more to offer and is worth the wait.

Data points to consider: US Advance GDP figures at 1.30pm, FOMC member Brainard speaks at 6.15 pm, closely followed by FOMC member Harker who speaks 7.30pm GMT+1.

Levels to watch/live orders:

- Buys: 1.0776/1.08 ([dependent on the time of day, a long from here is possible without the need for additional confirmation] stop loss: 1.0773).

- Sells: Flat (stop loss: N/A).

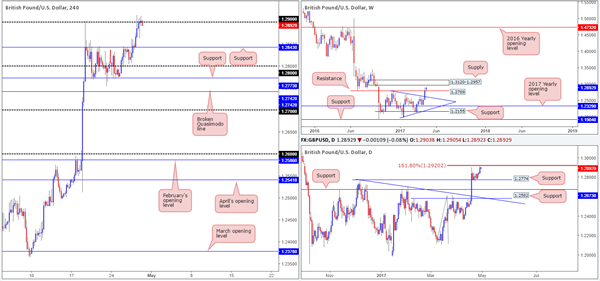

GBP/USD

Following a H4 consolidation between 1.2844/1.2776 that lasted a good few days, H4 bulls finally rose up and took charge yesterday, marching up to the 1.29 handle. Closely supporting this psychological band is a daily AB=CD 161.8% Fib extension seen at 1.2920 (Taken from the low 1.2108). Also noteworthy is weekly action. Following the prior week's (marginal) close beyond resistance at 1.2789, the bulls look poised to extend north up to supply drawn from 1.3120-1.2957.

With the above notes in mind, where does this leave us? Well, shorting from 1.09 today is a possibility with stops placed above the 1.2920 reigon. This, of course, could be considered a risky move though given where weekly price looks to be headed. As such, the team has decided to side step the short from 1.29 and wait to see if price can reach the H4 mid-level resistance at 1.2950 owing to how close this level is located to the above said weekly supply.

Our suggestions: Wait and see if H4 price shakes hands with 1.2950. Should this come to fruition, we'd then require a reasonably sized H4 bear candle to form (preferably a full-bodied candle) to confirm sellers are active.

Data points to consider: UK Prelim GDP figures at 9.30am. US Advance GDP figures at 1.30pm, FOMC member Brainard speaks at 6.15 pm, closely followed by FOMC member Harker who speaks 7.30pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 1.2950 region ([waiting for a reasonably sized H4 bear candle to form before pulling the trigger is advised] stop loss: ideally beyond the candle's wick).

AUD/USD

During the course of yesterday's sessions, the H4 candles aggressively whipsawed through both the AB=CD 127.2% Fib ext. at 0.7458 and nearby mid-level support at 0.7450. At this stage, nevertheless, the odds of price breaching these two levels today are high. Our reasoning lies within the higher-timeframe structures. Check out the weekly chart. The bulls initially attempted to rotate from the support area seen at 0.7524-0.7446, but has thus far been unsuccessful. This has left price trading within the lower limits of this zone. Also of interest is the daily chart. Yesterday's movement chalked up a clear-cut indecision candle around the bottom edge of a support area at 0.7449-0.7506 (seen lodged within the current weekly support area).

Our suggestions: The weakness seen from the bid-side of this market at the moment makes us reluctant to take longs. On that note, we would, should a decisive H4 close be seen beyond 0.7450, look to trade short on any retest (if it's accompanied by a full-bodied H4 bearish candle that is) seen to the underside of this number, targeting 0.7400 as an initial take-profit target.

Data points to consider: US Advance GDP figures at 1.30pm, FOMC member Brainard speaks at 6.15 pm, closely followed by FOMC member Harker who speaks 7.30pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Watch for price to engulf 0.7450 and then look to trade any retest seen thereafter ([waiting for a H4 full-bodied bear candle to form following the retest is advised] stop loss: ideally beyond the candle's wick).

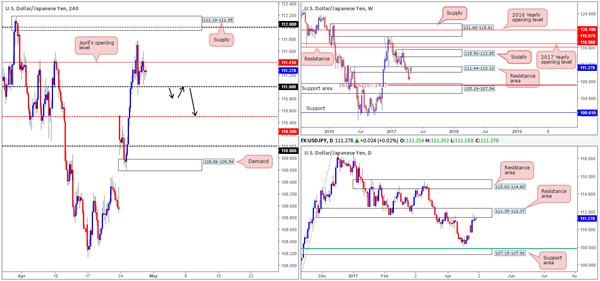

USD/JPY

Over the past couple of days, the H4 candles have experienced a considerable amount of choppy action between April's opening level at 111.41 and the 111 handle. Directly above this range is a supply seen at 112.19-111.95, whereas beyond 111 is a mid-level support seen at 110.50. Aiding the bears at the moment is a weekly resistance area at 111.44-110.10 and a daily resistance area drawn from 111.35-112.37.

Our suggestions: Given the higher-timeframe structures currently in motion, the overall tone is biased to the downside, in our opinion. Because of this, we're looking for a H4 close to print below 111 today. This – coupled with a retest that's followed up with a H4 bearish rejection (preferably a full-bodied candle) would be enough evidence to short down to at least the H4 mid-level support at 110.50.

Data points to consider: US Advance GDP figures at 1.30pm, FOMC member Brainard speaks at 6.15 pm, closely followed by FOMC member Harker who speaks 7.30pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Watch for price to engulf the 111 handle and then look to trade any retest seen thereafter ([waiting for a H4 full-bodied bear candle to form following the retest is advised] stop loss: ideally beyond the candle's wick).

USD/CAD

In recent sessions, we saw the H4 candles surpass the 1.36 handle and touch gloves with a H4 mid-level resistance at 1.3650/resistance pegged at 1.3662. Despite the current resistances in play right now, the higher timeframes strongly suggest further buying may be on the cards. Over on the weekly timeframe, price is not only seen respecting the 2017 yearly opening level at 1.3434 as support, it also recently broke above a well-defined double-top formation seen around the 1.3588 neighborhood (green circle). In addition to this, the recent break of daily supply at 1.3598-1.3559 (now acting support area), in our view, confirms the weekly bull's strength. The next upside target seen beyond here comes in at 1.3859-1.3700: a supply zone which happens to house the 2016 yearly opening level at 1.3814 (the weekly timeframe's next upside target) within.

Our suggestions: In essence, our desk is looking for H4 price to close above the current H4 resistances. A long on any retest of these levels is valid up to the 1.37 band. It is here we'd advise tightening your position. Not only because it is a psychological level, but also due to it denoting the lower edge of the current daily supply. Ultimately though, we would be looking to take full profit around the 1.38 region, essentially marking the 2016 yearly opening line.

Data points to consider: US Advance GDP figures at 1.30pm, FOMC member Brainard speaks at 6.15 pm, closely followed by FOMC member Harker who speaks 7.30pm. Canadian GDP numbers at 1.30pm GMT+1.

Levels to watch/live orders:

- Buys: Watch for price to engulf 1.3662 and then look to trade any retest seen thereafter ([waiting for a H4 full-bodied bull candle to form following the retest is advised] stop loss: ideally beyond the candle's tail).

- Sells: Flat (stop loss: N/A).

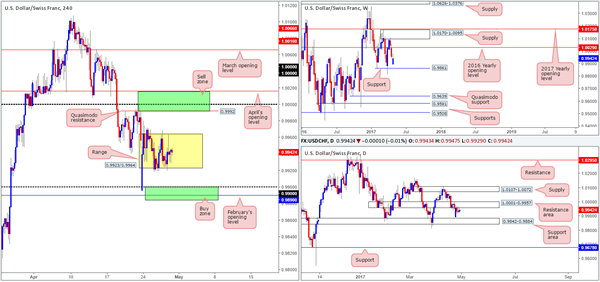

USD/CHF

For the past few days, the H4 candles have been busy chiseling out a consolidation between 0.9923/0.9964. Above this range, we can see a H4 Quasimodo resistance level coming in at 0.9992, closely followed by parity (1.0000) and then April's opening level at 1.0016. To the downside, however, there's the 0.99 handle, which is shadowed closely by February's opening line at 0.9890. Over on the daily chart, the pair remains capped by a resistance area seen at 1.0001-0.9957. Assuming that the bears remain in control here, the Swissy may eventually pay a visit to the support area penciled in at 0.9842-0.9884.

Our suggestions: As far as we can see, there's equal opportunity to trade this pair both long and short today. For shorts, we have the 1.0016/0.9992 region, and for longs there's the 0.9884/0.99 base. Both zones, as you can probably see, boast daily structure. The only grumble we would have if we were to take a long from the said area is the fact that weekly price could potentially push the market through our H4 buy zone to shake hands with support at 0.9861.

Data points to consider: US Advance GDP figures at 1.30pm, FOMC member Brainard speaks at 6.15 pm, closely followed by FOMC member Harker who speaks 7.30pm. SNB Chairman Jordan speaks at 9am GMT+1.

Levels to watch/live orders:

- Buys: 0.9884/0.99 ([waiting for a reasonably sized H4 bull candle to form before pulling the trigger is advised] stop loss: ideally beyond the candle's tail).

- Sells: 1.0016/0.9922 ([waiting for a reasonably sized H4 bear candle to form before pulling the trigger is advised] stop loss: ideally beyond the candle's wick).

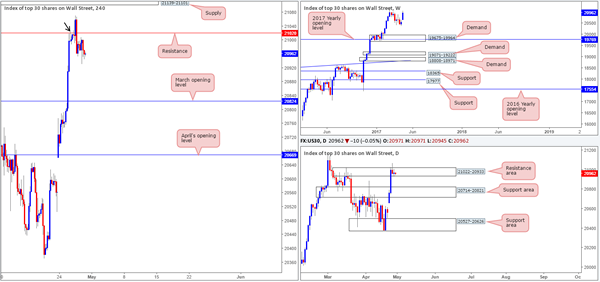

DOW 30

As can be seen from the daily timeframe this morning, the candles are struggling to breach the resistance area coming in at 21022-20933. This, we believe, is all that's stopping the DOW from reaching fresh record highs! A decisive close above here would very likely seal the deal. Right now though, it seems the bears are in control. With little support seen over on the H4 timeframe until we reach March's opening level at 20824, there's a chance that we may see more pressure come in from the bears!

Our suggestions: Based on the above notes, a short from the H4 resistance at 21020 could be an option considering that it merges closely with 21028: a H4 Quasimodo resistance level seen marked with a black arrow. However, taking into account that the broader focus on this index remains north, waiting for a H4 bearish rejection candle to form off 21020 (preferably a full-bodied candle) before committing to a short is advised. This, of course, by no means guarantees a winning trade, but what it will do is show seller intent off a high-probability resistance level.

Data points to consider: US Advance GDP figures at 1.30pm, FOMC member Brainard speaks at 6.15 pm, closely followed by FOMC member Harker who speaks 7.30pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 21020 region ([waiting for a reasonably sized H4 bear candle to form before pulling the trigger is advised] stop loss: ideally beyond the candle's wick).

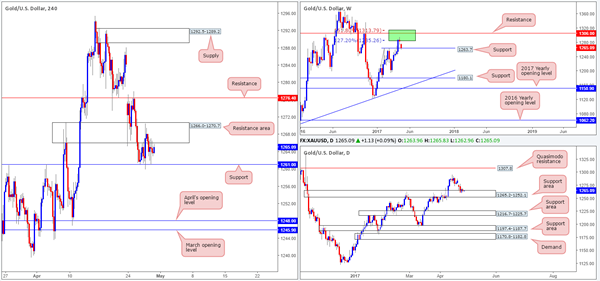

GOLD

The yellow metal, as you can see, remains capped by the H4 resistance area at 1266.0-1270.7 and H4 support level at 1261.0. This is quite something considering that we have a daily support area at 1265.2-1252.1 and a weekly support level at 1263.7 both in play at the moment! Although shorts look tempting beyond the current H4 support level down to April's opening level at 1248.0, we just would not feel comfortable selling here knowing what's lurking beneath us on the higher timeframes! Unfortunately, even with a decisive push to the upside, H4 buyers will have to almost immediately contend with resistance marked at 1276.4.

Our suggestions: Neither a long nor short seems attractive at this time. It appears we're trapped from both ends! With this being the case, remaining on the sidelines may very well be the better path to take today.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

European Open Briefing: The ECB Kept Rates And Their QE Programme Unchanged

Global Markets:

- Asian stock markets: Nikkei down 0.20 %, Shanghai Composite fell 0.35 %, Hang Seng declined 0.40 %, ASX 200 lost 0.15 %

- Commodities: Gold at $1266.30 (+0.05 %), Silver at $17.37 (+0.20 %), WTI Oil at $49.40 (+0.90 %), Brent Oil at $52.20 (+0.80 %)

- Rates: US 10 year yield at 2.29, UK 10 year yield at 1.06, German 10 year yield at 0.30

News & Data:

- Japan Mar National CPI (YoY): 0.2% Est. 0.3%

- Japan Mar National CPI Ex-Fresh Food (YoY): 0.2% Est. 0.2%

- Japan Mar Unemployment Rate: 2.8% Est. 2.90%

- Japan Mar Job/Applications Ratio: 1.45 Est. 1.43

- Japan Mar P Industrial Production (MoM): -2.1% Est. -0.80%

- Japan Mar P Industrial Production (YoY): 3.3% Est. 3.90%

- Japan Mar Retail Sales (MoM): 0.2% Est. -0.30%

- Japan Mar Retail Sales (YoY): 2.1% Est. 0.5%

- Australia Q1 PPI (YoY): 1.3%

- Australia Q1 PPI (QoQ): 0.5%

- New Zealand March Trade Balance NZD (MoM): 332m Est. 370m

- New Zealand March Trade Balance NZD (YoY): -3.67bn Est. -3.706bn

- New Zealand March Exports NZD (MoM): 4.65bn Est. 4.66bn

- New Zealand March Exports NZD (YoY): 4.31bn Est. 4.016bn

- New Zealand March Building Permits (MoM): 1.8%

- South Korea March Industrial Production (MoM): 1.5% Est. 1.5%

- South Korea March Industrial Production (YoY): 3.0% Est. 4%

- South Korea May Business Survey Manufacturing: 84

- South Korea May Business Survey Non-Manufacturing: 78

Markets Update:

The ECB kept rates and their QE programme unchanged, as expected by the market, but maintained their easing bias. This put the Euro under pressure again. EUR/USD fell from 1.0920 to a low of 1.0857 in Asia. Key support is now seen at 1.0780, followed by the weekend gap at 1.0730.

Meanwhile, the Pound is showing strength again, also party driven by strong cross flows (GBP buying against commodity currencies). GBP/USD broke above 1.29 resistance and should test 1.30 soon. Further gains beyond that seem likely in the near-term.

The USD/JPY rally has paused. Overnight, the pair consolidated in a 111.10-35 range. Should it break below 111 support, a retest of 110 seems likely. Overall, the downtrend is still alive, and the technical outlook for the pair negative.

NZD/USD is under a lot of pressure. It broke below key support at 0.6860, which suggests that losses will extend to at least 0.6670 in the near-term.

Upcoming Events:

- 06:30 GMT – French GDP

- 07:00 GMT – German Retail Sales

- 07:45 GMT – French CPI

- 09:00 GMT – SNB Chairman Jordan speaks

- 09:30 GMT – UK GDP

- 10:00 GMT – Euro Zone CPI

- 13:30 GMT – US GDP

- 13:30 GMT – Canadian GDP

- 15:00 GMT – US Michigan Consumer Sentiment

- 14:45 GMT – US Chicago PMI

Market Update – Asian Session: Japan’s Deluge Points To Economic Growth But Soft Inflation

US Session Highlights

Stock were subdued today, with little change in Blue chips and broader market indices. Techs, instead, continued to rally, pushing the NASDAQ to a new all-time high at 6,050, before closing slightly lower. Of the S&P sectors, Energy showed the largest decline at 1.1%, while Consumer Discretionary posted the largest gain at 0.5%.

US markets on close: Dow flat, S&P500 +0.1%, Nasdaq +0.4%

Best Sector in S&P500: Technology

Worst Sector in S&P500: Telecommunications

Biggest gainers: UA +9.9%; INTU +8.5%; XLNX +7.4%

Biggest losers: TDC -8.2%; FFIV -7.5%; EQT -7.0%

At the close: VIX 10.4 (-0.5pts); Treasuries: 2-yr 1.26% (flat), 10-yr 2.30% (-2bps), 30-yr 2.97% (-1bps)

US movers afterhours

WDC Reports Q3 $2.39 v $2.16e, R$4.65B v $4.54Be; +7.0% afterhours

GOOGL Reports Q1 $7.73 v $7.48e, R$24.8B (includes $4.6B TAC) v $19.7Be; +4.3% afterhours

CERN Reports Q1 $0.59 v $0.58e, R$1.26B v $1.23Be; +4.1% afterhours

AMZN Reports Q1 $1.48 v $1.03e, R$35.7B v $35.4Be; +3.9% afterhours

MSFT Reports Q3 $0.73 v $0.69e, R$22.1B v $23.6Be; -0.5% afterhours

INTC Reports Q1 $0.66 v $0.65e, R$14.8B v $14.8Be; -3.6% afterhours

KLAC Reports Q3 $1.62 v $1.54e, R$913.8M v $894Me; -3.6% afterhours

BIDU Reports Q1 $1.00 v $0.85e, R$2.45B v $2.32Be; CFO to step down, effective on appointment of successor; -3.8% afterhours

SBUX Reports Q2 $0.45 v $0.45e, R$5.3B v $5.42Be; -4.7% afterhours

FTNT Reports Q1 $0.17 v $0.15e, R$340.6M v $335Me; -7.2% afterhours

ATHN Reports Q1 $0.32 v $0.46e, R$285M v $297Me; -16.8% afterhours

Key economic data

(JP) JAPAN MAR JOBLESS RATE: 2.8% V 2.9%E (matches lowest rate since Jun 1994)

(JP) JAPAN MAR OVERALL HOUSEHOLD SPENDING Y/Y: -1.3% V -0.5%E

(JP) JAPAN APR TOKYO CPI Y/Y: % V -0.2%E; CPI EX-FRESH FOOD Y/Y: -0.1% V -0.2%E

(JP) JAPAN MAR NATIONAL CPI Y/Y: 0.2% (5-month low) V 0.3%E ; CPI EX FRESH FOOD (CORE) Y/Y: 0.2% V 0.2%E

(JP) JAPAN MAR PRELIMINARY INDUSTRIAL PRODUCTION M/M: -2.1% (biggest decline since June of 2016) V -0.8%E; Y/Y: 3.3% V 3.9%E

(JP) JAPAN MAR RETAIL SALES M/M: +0.2% V -0.3%E; RETAIL TRADE Y/Y: 2.1% (22-month high) V 1.5%E

(JP) JAPAN MAR VEHICLE PRODUCTION Y/Y: 4.7% V 11.2% PRIOR

(AU) AUSTRALIA Q1 PPI Q/Q: 0.5% V 0.5%; Y/Y: 1.3% (5-quarter high) V 0.7% PRIOR

(AU) AUSTRALIA MAR PRIVATE SECTOR CREDIT M/M: 0.3% V 0.5%E; Y/Y: 5.0% V 5.1%E

(NZ) NEW ZEALAND MAR BUILDING PERMITS M/M: -1.8% V +17.2% PRIOR

(NZ) NEW ZEALAND MAR TRADE BALANCE (NZ$): +332M V +370ME; First surplus in 9 months

(KR) SOUTH KOREA MAR INDUSTRIAL PRODUCTION M/M: 1.0% V 1.5%E; Y/Y: 3.0% V 4.0%E

Asia Session Notable Observations, Speakers and Press

Asian indices are tracking lower despite the modest gains in US indices as traders express caution over geopolitical and policy risks stemming out of Washington and Beijing. In his "100-day in office" milestone interview, President Trump turned his focus to both North and South Korea. On the former, Trump said it is his "biggest worry" and that it would be very difficult to resolve situation diplomatically, adding that "we could end up having a major, major conflict with North Korea." Subsequently, however, Trump criticized the current trade deal with South Korea, noting that US is owed $1B by Seoul for the deployment of THAAD missile defense system. In China, banking regulators have turned more of their focus on the property sector, tightening loans to developers and urging banks to monitor financing risks.

In FX, dollar majors traded little changed despite the cautious tone in stocks, with US GDP report coming into focus in early Friday session. NZD/USD remained in a tight range despite New Zealand hitting a trade surplus for the first time in 9 months, as exports to China jumped over 40% y/y. Japan saw a wide range of mixed economic data - national CPI slowed to a 5-month lows and industrial output y/y decline was the biggest in 9 months, while unemployment was better than expected matching 1994 lows and annualized retail trade reaching near 2-year high.

China

(CN) Some China banks said to have tightened loans to property developers - Chinese press

Japan

(JP) Japan Fin Min Aso: Plan to hold bilateral finance dialogue with China on May 6th - press

Australia/New Zealand

(NZ) RBNZ remains concerned by elevated property prices; Expects to publish debt-to-income consultation paper in about 6 weeks - press

Korea

(KR) US State Sec Tillerson: China has told US govt it warned N Korea not to conduct another nuclear test - Fox interview

(KR) BOK: To keep accommodative policy as demand-side inflation pressures are modest; Consumption rising steadily on perception of economic improvement

(KR) US Pres Trump: To renegotiate or terminate the South Korea trade deal; Wants $1B payment for THAAD missile defense system - press

(KR) South Korea Defense Ministry: Unchanged in view that US should pay for THAAD - Korean press

(US) Pres Trump: North Korea is my biggest worry; Would love to resolve situation diplomatically, but its "very difficult" - press interview

Asian Equity Indices/Futures (01:00ET)

Nikkei -0.4%, Hang Seng -0.5%, Shanghai Composite -0.4%, S&P/ASX200 -0.1%, Kospi -0.2%

Equity Futures: S&P500 flat; Nasdaq flat, Dax -0.1%, FTSE100 -0.2%

FX ranges/Commodities/Fixed Income (01:00ET)

EUR 1.0855-1.0875; JPY 111.05-111.35; AUD 0.7460-0.7475; NZD 0.6870-0.6890

June Gold +0.1% at 1,268/oz; June Crude Oil +1.2% at $49.55/brl; July Copper -0.1% at $2.60/lb

SPDR Gold Trust ETF daily holdings fall 0.9 tonnes to 853.4 tonnes

(CN) PBOC SETS YUAN MID POINT AT 6.8931 V 6.8896 PRIOR; 4th straight weaker setting; weakest setting since Apr 12th

(CN) PBOC to inject combined CNY80B v CNY50B prior in 7-day, 14-day and 28-day reverse repos, 9th straight injection; For the week, injects CNY70B v CNY170B in prior week

(CN) China Finance Ministry auctions CNY10B in 3-month bills at avg yield of 2.944% v 2.919% prior

(AU) Australia MoF (AOFM) sells A$800M in 5.75% 2022 Bonds; avg yield: 2.1198%; bid-to-cover: 4.68x

(JP) Japan MoF sells ¥1.99T v ¥2.2T indicated in 2-yr 0.1% JGBs; Avg yield: -0.193% v -0.206% prior; bid to cover: 5.51x v 3.82x prior

Australia’s Private Sector Credit Grew Less-Than-Expected In March

For the 24 hours to 23:00 GMT, the AUD declined 0.11% against the USD and closed at 0.7466.

LME Copper prices rose 0.2% or $9.0/MT to $5686.5/MT. Aluminium prices declined 0.2% or $3.0/MT to $1954.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7469, with the AUD trading slightly higher against the USD from yesterday's close.

Early morning data showed that Australia's private sector credit rose 0.3% on a monthly basis in March, lower than market expectations for an advance of 0.5%. In the previous month, the private sector credit had registered a similar rise.

The pair is expected to find support at 0.7440, and a fall through could take it to the next support level of 0.7411. The pair is expected to find its first resistance at 0.7495, and a rise through could take it to the next resistance level of 0.7521.

Going ahead, market participants will await the release of Australia's AiG performance of manufacturing index for April, slated to release over the weekend.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

ECB Maintains Ultra-Loose Monetary Policy

For the 24 hours to 23:00 GMT, the EUR declined 0.36% against the USD and closed at 1.0868, after the European Central Bank (ECB) President, Mario Draghi, gave no hints to curtail its massive bond-buying programme in the coming months.

The ECB, at its latest monetary policy meeting, maintained the key interest rate at 0.00% and left its monetary stimulus programme unchanged. In a post-meeting statement, the ECB President, Mario Draghi, reiterated that the central bank could increase the size or duration of its asset-buying programme if inflation looks set to fall far back below its target of near 2.0%. Nevertheless, Draghi expressed optimism over the Euro-zone's economic recovery, noting that it was increasingly solid, but stated that inflation pressures in the region remain subdued and are yet to show a convincing upward trend.

On the macro front, the economic sentiment indicator in the common currency region surged to a ten-year high level of 109.6 in April, amid increased optimism over the health of the region's economy. The index had registered a revised reading of 108.0 in the previous month. Additionally, the region's final consumer confidence index was confirmed at -3.6 in April, compared to a reading of -5.0 in the prior month.

Elsewhere, in Germany, the preliminary consumer price index advanced more-than-anticipated by 2.0% YoY in April, highlighting that inflation in the Euro-zone's largest economy is picking up, as an economic upswing continues and the labour market strengthens. Market participants had envisaged for a rise of 1.9%, following a gain of 1.6% in the previous month.

Macroeconomic data released in the US indicated that advance goods trade deficit widened less-than-anticipated to a level of $64.8 billion in March, from a revised deficit of $63.9 billion in the prior month. Also, the nation's initial jobless claims advanced to a level of 257.0K last week, topping market expectations of a rise to a level of 245.0K. In the prior week, initial jobless claims had recorded a revised level of 243.0K. Moreover, the nation's pending home sales eased 0.8% in March, less than market expectations for a fall of 1.0%. In the prior month, pending home sales had registered a rise of 5.5%.

Further, the nation's seasonally adjusted flash wholesale inventories registered an unexpected drop of 0.1% in March, defying investor consensus for an advance of 0.2% and following a rise of 0.4% in the previous month.

Another economic data revealed that the US flash durable goods orders rose less-than-expected by 0.7% in March, growing at its slowest pace since December 2016. Markets expected durable goods orders to rise 1.3%, after recording a gain of 1.8% in the prior month.

In the Asian session, at GMT0300, the pair is trading at 1.0866, with the EUR trading slightly lower against the USD from yesterday's close.

The pair is expected to find support at 1.0833, and a fall through could take it to the next support level of 1.0801. The pair is expected to find its first resistance at 1.0915, and a rise through could take it to the next resistance level of 1.0965.

Ahead in the day, investors will look forward to the Euro-zone's flash inflation figures for April and Germany's retail sales for March. Moreover, in the US, flash annualised GDP for Q1 and final Michigan consumer sentiment index for April, both slated to release later in the day, will garner a lot of market attention.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

UK’s GfK Consumer Confidence Dipped To A 4-Month Low Level In April

For the 24 hours to 23:00 GMT, the GBP rose 0.37% against the USD and closed at 1.2900.

In the Asian session, at GMT0300, the pair is trading at 1.2907, with the GBP trading a tad higher against the USD from yesterday's close.

Overnight data indicated that UK's GfK consumer confidence fell to a four month low level of -7.0 in April, meeting market expectations and compared to a reading of -6.0 in the prior month. Moreover, the nation's Lloyds business barometer climbed to a level of 47.0 in April. In the previous month, the index had registered a level of 35.0.

The pair is expected to find support at 1.2867, and a fall through could take it to the next support level of 1.2828. The pair is expected to find its first resistance at 1.293, and a rise through could take it to the next resistance level of 1.2954.

Looking ahead, traders would focus on UK's flash GDP for Q1 and Nationwide house prices for April, scheduled to release in a few hours.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Japan’s Jobless Rate Surprisingly Remained Steady In March, While Inflation Came In Softer Than Expected In The Same Month

For the 24 hours to 23:00 GMT, the USD marginally rose against the JPY and closed at 111.25.

In the Asian session, at GMT0300, the pair is trading at 111.1, with the USD trading 0.13% lower against the JPY from yesterday's close.

Overnight data revealed that Japan's jobless rate surprisingly remained unchanged at 2.8% in March, compared to market expectation for a rise to 2.9%. Meanwhile, the nation's national consumer price index (CPI) climbed less-than-anticipated by 0.2% YoY in March, compared to an advance of 0.3% in the prior month, while markets had envisaged for a gain of 0.3%. On the other hand, flash industrial production in Japan slid 2.1% MoM in March, higher than market expectations for a drop of 0.8%. Industrial production had risen 3.2% in the prior month.

Other economic data indicated that the nation's seasonally adjusted retail trade unexpectedly climbed 0.2% in March, confounding market expectations for a fall of 0.3% and compared to a revised advance of 0.3% in the previous month. In contrast, the nation's large retailers' sales fell 0.8% in March, after recording a drop of 2.7% in the prior month.

The pair is expected to find support at 110.88, and a fall through could take it to the next support level of 110.67. The pair is expected to find its first resistance at 111.45, and a rise through could take it to the next resistance level of 111.81.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.