Sample Category Title

A ‘Taxing’ Day For Dealers

A 'Taxing' Day for Dealers

As expected, the Trump administration rolled out the Tax reform roadshow on Wednesday. Given the market’s lofty expectations, traders are viewing it as little more than a road map, rather than the much ballyhooed 'big announcement', because the statement did not provide any comprehensive details. While the essence of the proposal is reflationary and indeed, dollar bullish in a very market friendly positive way, the argument remains for, and further clarity is required on how the tax cut’s deficit ramifications will be offset. Fiscal reforms present a real revenue drain amidst disquieting concerns of the current trajectory for the US deficit. Look for the US administration to revisit the contentious repeal of Obamacare, which also will present another hurdle for risk. Overall, an incredibly Taxing day for traders.

As for the government shutdown, chatter in the Foggy Dew suggests that the legislators will need another week to settle their differences to avoid a shutdown, this despite reports suggesting otherwise. It is all a bit confusing and will likely go down to Friday’s deadline.

While dealers were connecting the tax reform dots, commodity currencies were sideswiped by a report in Politico that the Trump Administration is weighing an executive order to withdraw from NAFTA by officially starting a six-month review period. Predictably, the CAD and MXN have weakened notably on this, but there has been lots of foreshadowing of this move, dating back to mid-March.

Amid all the soundbites, FOMC members have reiterated that they respond to data, rather than Trump uncertainty; yet the market is responding to latter.

Canadian Dollar

Another tough day on the Canada post. While the CAD initially benefited from a larger drop in crude inventories, it was steamrolled by the NAFTA headlines. The bounce in WTI was then unwound after a Bloomberg report that stated Saudi Arabia was losing market share to Iran and Iraq. Traders now think that maybe production cuts may not be extended, and so the balancing act goes on.

Japanese Yen

Despite the USDJPY move overnight, the currency of choice remains the EURJPY, which should underpin the USDJPY near term. We again find ourselves caught in a vortex of headlines driven trade, which tends to muddy the fundamentals. But with risk sentiment expected to reassert itself, it is challenging not to view the USDJPY higher in this environment.

On the BoJ front, no changes are expected, and it is far too early to expect any hawkish delivery from a BOJ that is likely erring on an inflation overshoot before signalling any hike.

Australian Dollar

The AUD has been beaten down after yesterday’s CPI report, which suggests that the RBA will remain accommodative for the foreseeable future and the acute bid that transpired on the USD post-US Tax rhetoric. The NAFTA talk has not only weighed on USDCAD overnight but commodity currencies, as the market re-visits US protectionism and possible announcements on import tax policy.

Dollar Rises Ahead Of Japanese And European Central Bank Announcements

BOJ and ECB expected to stand pat despite improving economic indicators

The USD is higher across the board on Wednesday after US Treasury Secretary Steve Mnuchin and Chief Economic Adviser Gary Cohn presented the outline of the Trump tax reform. Billed as the biggest tax cut in US history its main goal is to unlock growth. The Trump administration had squandered its honeymoon period in Washington by introducing controversial policies on immigration and healthcare instead of the pro-growth reforms signalled right after Trump was victorious in the November elections. A return to pushing those policies could spark the return of the reflation trade, also known as the Trump trade.

The Bank of Japan (BOJ) will publish its Monetary Policy Statement on Wednesday, April 26 at 11:30 pm EDT. The central bank is not likely to update its policy during the April meeting. BOJ Governor Haruhiko Kuroda said on April 20 that the current quantitive easing (QE) program would remain in place for some time. The strength of the JPY has been an obstacle in reaching the central bank’s goal of 2 percent inflation. The BOJ is expected to lower its inflation forecast and upgrade its economic growth outlook.

The European Central Bank (ECB) will release its minimum bid rate on Thursday, April 27 at 7:45 am EDT. ECB President Mario Draghi was active last week talking down a premature tapering as there remain multiple downsides risks to the economy. The market was optimistic after the results of the first round of presidential elections in France. With a Macron and Le Pen second round the worst case scenario was avoided and the EUR rose but until May 7 there are still a lot that could change despite the polls pointing to a healthy Macron lead. After the results of Brexit and the US elections polls do not command the same trust that they used to.

The EUR/USD lost 0.378 percent in the last 24 hours. The single currency is trading at 1.0895 after the Trump administration got back on track with their pro-growth policies. Too early to call the return of the Trump trade, specially with a possible disappointment on Friday as the first estimate of the Q1 GDP will be released.

European economic indicators have been light this week. The German Ifo business climate index rose to 112.9 a six year high as executives are more optimistic about the current state of the German economy. The ECB press conference will be a highlight for investors looking for insights into its QE program after it scaled it back to 60 billion euros a month (from 80 billion euros). The EUR has benefited from a reduction in risk after the first round of the French elections, but there is still more to come not only in the second round, but with the end of the two party system the parliamentary elections are now even more relevant.

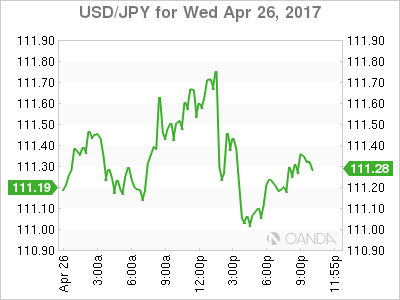

The USD/JPY gained 0.232 percent on the Wednesday trading session. The pair is trading at 111.37 as the USD got a boost from the Trump administration’s announcement of its tax reform plans. The BOJ will stand pat on rates and the size of its massive QE program even as there are some positive signs of economic growth. The inflation benchmark of 2 percent remains out of reach however as the current rate hovers around 0.3 percent.

The JPY has been used as a safe haven during volatile times, working against the work of the BOJ. US military actions and the French election made it a natural refuge as the USD and EUR were sold in favour of the Japanese yen. With the return of risk appetite and a reversal of fortune for the greenback it has advanced more than 2 percent against the JPY after touching weekly lows of 108.72.

Market events to watch this week:

Wednesday, April 26

11:50pm JPY Monetary Policy Statement

Thursday, April 27

Tentative JPY BOJ Outlook Report

Tentative JPY BOJ Policy Rate

2:30am JPY BOJ Press Conference

7:45am EUR Minimum Bid Rate

8:30am EUR ECB Press Conference

8:30am USD Core Durable Goods Orders m/m

8:30am USD Unemployment Claims

Friday, April 28

4:30am GBP Prelim GDP q/q

8:30am CAD GDP m/m

8:30am USD Advance GDP q/q

Does Geopolitical Risk Require A Shift In Thinking On Gold?

Up until recently, we had been speaking about shorting gold on the blog. Price was sitting at a major higher time frame resistance level and the opportunity was there to manage our risk around it.

But then the US launched missiles into Syria, tensions on the Korean peninsula escalated and most recently, the French elections all threw a metaphorical spanner in the works.

So does this shift in the geopolitical landscape to a more risk off environment mean that gold becomes a buy?

XAU/USD Daily:

Taking a look at the daily chart, you can see that price has broken above the higher time frame resistance level that we were looking to use as a risk management level for potential shorts.

With this level now gone, should our thinking change with it? If you're in the ‘trade a level until it's broken' camp, then the answer would be yes.

XAU/USD Hourly:

Zooming in to the hourly chart, you can see that after breaking above the higher time frame resistance level, price has now pulled back to retest it this time as support.

This could be viewed as confirmation that the level has in fact held as support and now you would look to buy any short term pullbacks. One such pullback that I've marked in green on the hourly chart above.

Tax Plan Follows The Script

As we anticipated, the trade was to sell-the-fact on the Trump tax plan. The bulk of currencies finished the day unchanged despite some volatility, the only real movers were the commodity currencies, which lagged. The Asia-Pacific calendar is quiet as we count down to the ECB. A new USD trade has been posted alongside supproting charts moments ago.

Yesterday we wrote about the Trump trading plan: to react to the first hints of action, then exit when he delivers. The market followed the script on Wednesday as he delivered his long-touted tax plan.

As anticipated, it wasn't a plan. It was a one-page, bullet point draft of a dozen principles that he hopes to achieve. It mirrored his campaign pledged and much of it was leaked.

The market's response was to unwind a portion of the rally in risk assets since Friday in anticipation of the news. USD/JPY sagged 70 pips to 111.00. The US dollar fell by a smaller margin elsewhere and the S&P 500 gave up an 8 point gain to finish down 1 point.

We will look for more opportunities to trade Trump in the future.

One continues to be CAD and MXN. The White House will likely announce its intention to pull out of NAFTA in the days ahead, according to reports. The Mexican peso was especially hit hard because it would leave the nations without a trade deal. Canada would fall back on the 1987 FTA if no new deal is reached, and that's similar to NAFTA.But if it's similar to NAFTA, Trump could hate it as well. Certainly the door is now open to a radically different trading relationship between the three nations.

USD/CAD didn't break Tuesday's high on the news but it's nearby and the close above 1.3600 is a bullish technical signal. The pair didn't break higher in part because Canadian Feb retail sales ex-autos were slightly better than expected and with a big upward revision to the prior. Also notable for the pair is that oil couldn't hang onto a gain despite a bullish inventory report.

Also on the commodity front, AUD/USD was cut down on yesterday's CPI report. In US trading, it broke below the April lows and that could set up more technical trouble.The only possible catalyst in today's Asia-Pac session is Q1 import/export prices at 0130 GMT but that's a longshot. The consensus on imports is -0.5% and exports is +8.0%.

The bigger story will come Thursday with the ECB decision. Sources reports suggest references to downside risks will be removed and that may help the euro maintain its upside momentum.

Sterling Steady as Markets Eye Trump Tax Talk

GBP/USD is showing little movement on Wednesday, as the pair trades at 1.2840. On the release front, there hasn't been much data for the markets to analyze. There are no British releases, and the sole US event was Crude Oil Inventories. The weekly indicator came in at -3.6 million barrels, compared to the estimate of -1.1 million. On Thursday the US releases two major indicators – Core Durable Goods Orders and unemployment claims.

The negotiations between Britain and the EU are expected to be lengthy and difficult, and EU leaders don't appear to be in a generous mood, as they met in Brussels on Monday to discuss a united front in the Brexit talks. Britain wants any deal to include financial services, but the Europeans are working on a draft that would exclude the financial sector unless it is governed by EU rules. There are also likely to be sharp disagreements over the size of Britain's debt to the EU, among other major issues. For now, the British government is concentrating on the June election, but after that things could get nasty between the sides. If the Brexit talks run into trouble, market sentiment could take a dive and that could spell trouble for the British pound.

One of President Trump's key campaign planks was tax reform, both for corporations and individuals. Trump is expected to make a key announcement about his tax proposal on Wednesday. Of particular interest to the corporate sector, Trump is expected to propose reducing the corporate tax rate from 35% to 15%, and lowering the tax on multinationals' overseas profits from 35% to 10%. Any tax reform proposals from the White House will require a stamp of approval from Congress, so Trump's proposal should be viewed as a blueprint that is a long way off from becoming law. It will be interesting to see the reaction to Trump's tax plan. Trump's first 100 days in office have been rocky, so it will be a significant step forward for the president if Congress and the stock markets give a thumbs-up to his plan. However, if the president is short on details, as has often been the case, the ensuing disappointment from investors could send the dollar downwards.

US consumer confidence levels remain high, but there was some disappointment as CB Consumer Confidence dropped to 120.3 in April, missing the estimate of 123.7. The softer than expected reading boosted the euro in the Monday session. What is troubling analysts is that strong consumer confidence numbers have not translated into increased consumer spending, a key component of economic growth. This trend has been labeled the "hard/soft discrepancy" (confidence being 'soft', while actual spending being 'hard'). This was underscored in March retail sales numbers, which came in at a flat 0.0%, shy of the forecast. Next up is Preliminary GDP on Thursday, which is expected at 1.3 percent. An unexpected GDP reading could have a sharp impact on EUR/USD.

Trump’s Latest Lumber Tariff Helps Little on US Deficit. Political Implication can be Huge

USDCAD consolidated after a brief break about 1.36, following US' announcement to impose anti-subsidy tariff on softwood lumber imports from Canada. US Commerce Secretary Wilbur Ross indicated that the "countervailing duties" would range from 3-24% and would be imposed on 5 Canadian lumber exporters including West Fraser Timber Co., after concluding that Canada subsidizes its industry in a way that hurts the US. Ross added that the move is a sign to other trading partners that the US is planning stricter enforcement of trade laws. Canada responded by saying that the tariff is "unfair and punitive". In a joint statement from Foreign Minister Chrystia Freeland and Natural Resources Minister Jim Carr, it was noted that Canada "will vigorously defend the interests of the Canadian softwood lumber industry, including through litigation". It reiterated that "a negotiated settlement is not only possible but in the best interests of both countries". Risk to the loonie is to the downside in the near-term on heightened possibility of a trade war. Canada's economy is more vulnerable to a US-Canada trade war as 75% of its exports go to the US and this contributes to about 20% of Canada's economy.

A Brief History of US-Canada Softwood Lumber Trade Dispute

While the softwood lumber trade dispute between the US and Canada can be dated back to as early as the 1800s, explicit agreements have not been made until 1982. The US was dissatisfied with the Canadian government's policy that private lumber firms in British Columbia, Ontario, Alberta and Quebec are allowed to source trees from public land. However, in the US, the majority of lumber is cut from private lands, thus increasing the production cost. Softwood lumber was not covered under NAFTA, a trade agreement that the US has indicated intention to renegotiate in coming months, but appeared under a side agreement that expired in October 2015.

More a Political than Trade/Economic Issue

The US' softwood lumber imports from Canada amounted to about US$5B last year, approximately 85% of total US lumber imports. Yet, this only contributed to less than 2% of Canada's exports to the US, at US$295B. Meanwhile, Canada has a trade surplus of US$5.5B in coniferous wood, of which the majority was softwood lumber, last time. The figure is also small when compared with the total trade balance of US$85.2. Assuming the tariff is 20%, it covers only about 0.3% of US total imports. The overall impacts on US GDP growth or inflation are minimal. Interestingly, the key destinations of Canada's lumber exports in the US are Washington, Texas, New York, Oregon, Michigan, Pennsylvania, Massachusetts, Minnesota, North Carolina and Illinois. Most these states are with great presence of the Democratic Party and are politically important in the 2018 midterm elections.

While denying that the softwood lumber tariff is the beginning of NAFTA negotiations, the market has turned nervous that the US would adopt a stricter trade policy in order to promote his "American First" rhetoric. Indeed, Trump mentioned last week that he would "address" the trade problem on dairy products, accusing that Canada's move to change the class of some milk products has "put farmers in Wisconsin and New York state out of business". Again, we are suspicious that Trump's move has political incentive. The US runs a US$110M surplus in milk and milk-related products with Canada last year, with Canada exporting US$58M whilst importing US$168M from the US. The 2 states mentioned by Trump are also running surpluses with Canada in this category. Wisconsin, the first congressional district represented by Republican Paul Ryan, has a US$20M milk and milk-related surplus with Canada. The current Speaker of the House is also the proposer of the controversial border tax arrangement. New York, the 16th congressional state represented by Chuck Schumer, the Senate minority leader, has a US$22M surplus.

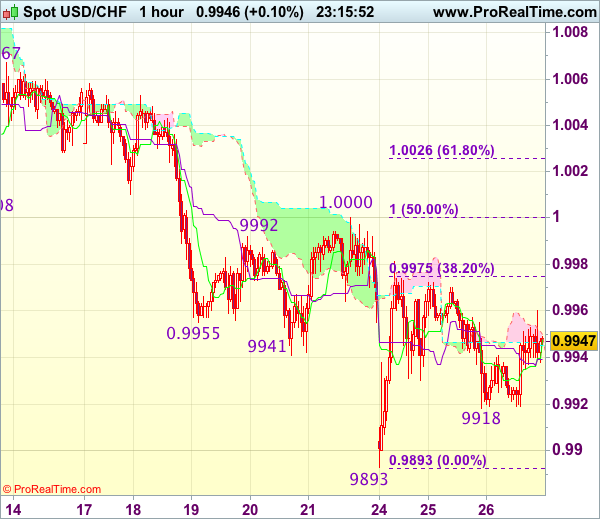

Trade Idea Wrap-up: USD/CHF – Stand aside

USD/CHF - 0.9943

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9948

Kijun-Sen level : 0.9939

Ichimoku cloud top : 0.9950

Ichimoku cloud bottom : 0.9945

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although dollar retreated yesterday to as low as 0.9918, as the greenback has rebounded today, retaining our view that further sideways trading above this week’s low at 0.9893 would take place and another bounce to 0.9981 cannot be ruled out, however, break of 1.0000-08 resistance is needed to signal low is formed instead, bring rebound to 1.0025-30 (61.8% Fibonacci retracement of 1.0108-0.9893), however, price should falter below resistance at 1.0067.

As near term outlook is still mixed, would be prudent to stand aside in the meantime. Below said support at 0.9918 would bring retest of 0.9893 but break there is needed to confirm recent decline from 1.0108 has resumed and extend weakness to 0.9865-70 (2 times extension of 1.0108-1.0008 measuring from 1.0067), however, reckon support at 0.9831 would hold from here, bring rebound later.

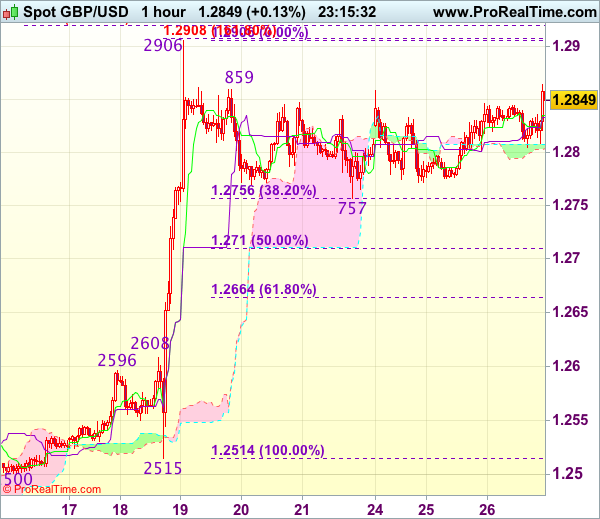

Trade Idea Wrap-up: GBP/USD – Stand aside

GBP/USD - 1.2840

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2835

Kijun-Sen level : 1.2833

Ichimoku cloud top : 1.2808

Ichimoku cloud bottom : 1.2804

Original strategy :

Buy at 1.2710, Target: 1.2850, Stop: 1.2675

Position : -

Target : -

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite intra-day brief bounce to 1.2864, lack of follow through buying on break of indicated resistance at 1.2859 suggests further sideways trading would be seen and pullback to 1.2805-10 cannot be ruled out, however, reckon Friday’s low at 1.2757 would limit downside and price should stay well above 1.2700-10 (50% Fibonacci retracement of 1.2515-1.2906), bring another rally. Above 1.2865-70 would signal the pullback from 1.2906 has ended, bring retest of this level, break there would extend recent upmove to 1.2920-30 (2 times extension of 1.2365-1.2575 measuring from 1.2500), then 1.2950 but reckon 1.2990-00 (1.236 times projection of 1.2109-1.2616 measuring from 1.2365 and psychological resistance) would hold.

In view of this, would not chase this rise here and would be prudent to buy cable on subsequent pullback as downside should be limited to 1.2710 (50% Fibonacci retracement of 1.2515-1.2906), bring another rise. Below 1.2700 would defer and signal top has been formed, risk correction to 1.2660-65 (61.8% Fibonacci retracement of 1.2515-1.2906) and price should stay well above 1.2608-16 (previous resistance now support).

Trade Idea Wrap-up: EUR/USD – Stand aside

EUR/USD - 1.0880

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.0923

Kijun-Sen level : 1.0911

Ichimoku cloud top : 1.0865

Ichimoku cloud bottom : 1.0809

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite intra-day marginal rise to 1.0951, lack of follow through buying and current retreat suggest consolidation below this level would be seen and downside risk remains for retracement to 1.0870, break there would suggest an intra-day top is formed, bring further fall to 1.0850 but reckon support at 1.0821 would hold from here, bring another rise later.

In view of this, would be prudent to stand aside for now. Only above said resistance at 1.0951 would extend recent upmove from 1.0340 low to 1.0975-80 and possibly towards 1.1000 which is likely to hold on first testing due to loss of momentum, risk from there is seen for a retreat later.

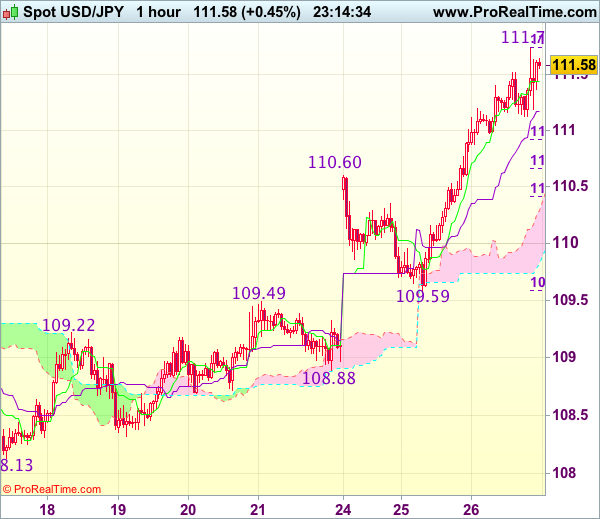

Trade Idea Wrap-up: USD/JPY – Buy at 110.70

USD/JPY - 111.60

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 111.43

Kijun-Sen level : 111.17

Ichimoku cloud top : 110.29

Ichimoku cloud bottom : 109.83

Original strategy :

Buy at 110.70, Target: 111.70, Stop: 110.35

Position : -

Target : -

Stop : -

New strategy :

Buy at 110.70, Target: 111.70, Stop: 110.35

Position : -

Target : -

Stop : -

The greenback surged after finding renewed buying interest at 109.59 and broke above previous resistance at 110.60, adding credence to our view that recent rise from 108.13 low is still in progress and bullishness remains for this move to bring at least a strong retracement of early downtrend, hence further gain to resistance at 111.75-80 would be seen, break would extend gain towards 112.00, however, overbought condition should prevent sharp move beyond another previous resistance at 112.20.

In view of this, would not chase this rise here and would be prudent to buy dollar on subsequent pullback as previous resistance at 110.60 should limit downside, bring another rally. Below 110.30-35 (61.8% Fibonacci retracement of 109.59-111.51) would defer and suggest top is possibly formed, risk weakness to 109.80 but break of support at 109.59 is needed to provide confirmation.