Sample Category Title

Trade Idea : EUR/USD – Stand aside

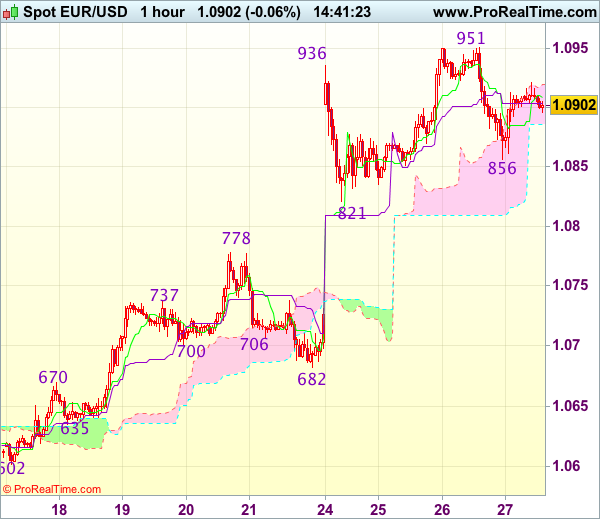

EUR/USD - 1.0902

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.0909

Kijun-Sen level : 1.0904

Ichimoku cloud top : 1.0919

Ichimoku cloud bottom : 1.0886

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite yesterday’s marginal rise to 1.0951, lack of follow through buying and the subsequent retreat to 1.0856 suggest consolidation below this level would be seen and below said support at 1.0856 would bring correction of recent rise to 1.0835-40 but reckon support at 1.0821 would hold from here, bring another rise later.

In view of this, would be prudent to stand aside for now. Only above said resistance at 1.0951 would extend recent upmove from 1.0340 low to 1.0975-80 and possibly towards 1.1000 which is likely to hold on first testing due to loss of momentum, risk from there is seen for a retreat later.

Trade Idea : USD/JPY – Buy at 110.70

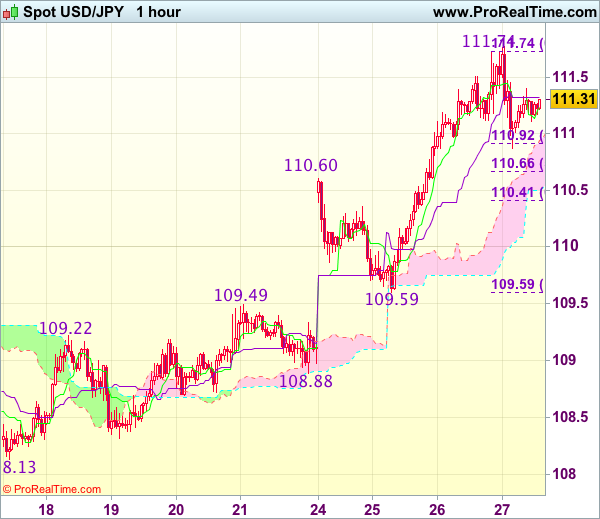

USD/JPY - 111.30

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 111.24

Kijun-Sen level : 111.33

Ichimoku cloud top : 110.94

Ichimoku cloud bottom : 110.50

Original strategy :

Buy at 110.70, Target: 111.70, Stop: 110.35

Position : -

Target : -

Stop : -

New strategy :

Buy at 110.70, Target: 111.70, Stop: 110.35

Position : -

Target : -

Stop : -

As the greenback retreated after rising to 111.78 yesterday, suggesting consolidation below this level would be seen and pullback to 110.60-69 (previous resistance and 50% Fibonacci retracement of 109.59-111.78) cannot be ruled out, however, reckon downside would be limited and 110.40-45 (61.8% Fibonacci retracement) should hold, bring another rise later, above said resistance at 111.78 would signal recent rise from 108.13 low has resumed and extend further gain to 111.90-00 but overbought condition should prevent sharp move beyond another previous resistance at 112.20.

In view of this, would not chase this rise here and would be prudent to buy dollar on subsequent pullback as previous resistance at 110.60 should limit downside, bring another rally. Below 110.40-45 (61.8% Fibonacci retracement of 109.59-111.78) would defer and suggest top is possibly formed, risk weakness to 109.80 but break of support at 109.59 is needed to provide confirmation.

Aussie Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the AUD declined 0.85% against the USD and closed at 0.7474.

LME Copper prices rose 0.4% or $25.0/MT to $5677.5/MT. Aluminium prices rose 0.8% or $14.5/MT to $1957.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7486, with the AUD trading 0.16% higher against the USD from yesterday's close.

Early morning data showed that Australia's import price index registered an unexpected rise of 1.2% on a quarterly basis in 1Q 2017, defying market expectations for a fall of 0.5% and following a gain of 0.2% in the previous quarter. Further, the nation's export price index climbed 9.4% QoQ in 1Q 2017, higher than market consensus for an increase of 8.0%. In the previous quarter, the index had advanced 12.4%.

Elsewhere, in China, Australia's largest trading partner, industrial profits increased 23.8% on an annual basis in March, after registering a rise of 2.3% in the previous month.

The pair is expected to find support at 0.7451, and a fall through could take it to the next support level of 0.7415. The pair is expected to find its first resistance at 0.7523, and a rise through could take it to the next resistance level of 0.7559.

Moving ahead, traders will look forward to Australia's private sector credit data for March, scheduled to be released in the early hours of tomorrow.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Euro Trading Marginally Higher, Ahead Of ECB’s Monetary Policy Decision

For the 24 hours to 23:00 GMT, the EUR declined 0.19% against the USD and closed at 1.0907.

On the economic front, French consumer confidence index remained steady at a level of 100.0 in April, meeting market expectations.

In the US, data revealed that MBA mortgage applications rebounded 2.7% in the week ended 21 April 2017, following a drop of 1.8% in the prior week.

In the Asian session, at GMT0300, the pair is trading at 1.0910, with the EUR trading slightly higher against the USD from yesterday's close.

The pair is expected to find support at 1.0860, and a fall through could take it to the next support level of 1.0810. The pair is expected to find its first resistance at 1.0955, and a rise through could take it to the next resistance level of 1.1000.

Going ahead, all eyes will be on the European Central Bank's (ECB) interest rate decision, scheduled to be announced later today. Also, the Euro-zone's final consumer confidence index and Germany's flash consumer price inflation, both for April, will be on investors' radar. Moreover, the US advance goods trade balance, durable goods orders and pending home sales data, all for March coupled with weekly jobless claims data, slated to release later in the day, will garner a significant amount of market attention.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.

Pound Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the GBP rose 0.18% against the USD and closed at 1.2853.

In the Asian session, at GMT0300, the pair is trading at 1.2861, with the GBP trading 0.06% higher against the USD from yesterday’s close.

The pair is expected to find support at 1.2817, and a fall through could take it to the next support level of 1.2774. The pair is expected to find its first resistance at 1.2890, and a rise through could take it to the next resistance level of 1.2920.

Looking ahead, market participants await the release of UK’s GfK consumer confidence index for April, set to release overnight.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

BoJ Keeps Monetary Policy Unchanged, Upgrades Economic Outlook

For the 24 hours to 23:00 GMT, the USD rose 0.22% against the JPY and closed at 111.20.

On the macro front, Japan's small business confidence index dropped more-than-anticipated to a level of 48.6 in April, compared to market expectations of a fall to a level of 49.4. The index had registered a level of 50.5 in the previous month.

In the Asian session, at GMT0300, the pair is trading at 111.26, with the USD trading marginally higher against the JPY from yesterday's close.

Earlier today, the Bank of Japan (BoJ), in its latest monetary policy meeting, opted to leave the benchmark interest rate steady at -0.1% and kept the yield target for 10-year Japanese government bonds around 0%.

In its quarterly economic outlook report, the central bank offered a more upbeat outlook on the economy, raising Japan's GDP forecast for the 2017-18 fiscal year to 1.6%, from the 1.5% projected in January, amid optimism that a pick-up in overseas demand will help sustain an export-driven economic recovery.

However, the BoJ lowered its inflation forecast to 1.4% from 1.5% for the same period.

The pair is expected to find support at 110.82, and a fall through could take it to the next support level of 110.37. The pair is expected to find its first resistance at 111.74, and a rise through could take it to the next resistance level of 112.21.

Moving ahead, Japan's jobless rate, consumer price inflation, retail trade, large retailers' sales and flash industrial production data, all for March, set to release overnight, will pique investor attention.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Swiss ZEW Expectations Index Declined In April

For the 24 hours to 23:00 GMT, the USD declined 0.03% against the CHF and closed at 0.993.

Macroeconomic data showed that Switzerland's ZEW economic expectations index fell to a level of 22.2 in April, following a reading of 29.6 in the previous month. On the other hand, the nation's UBS consumption indicator climbed to a level of 1.50 in March, after recording a revised level of 1.45 in the prior month.

In the Asian session, at GMT0300, the pair is trading at 0.9929, with the USD trading slightly lower against the CHF from yesterday's close.

The pair is expected to find support at 0.9907, and a fall through could take it to the next support level of 0.9886. The pair is expected to find its first resistance at 0.9959, and a rise through could take it to the next resistance level of 0.9990.

Ahead in the day, investors will focus on Switzerland's trade balance figures for March.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Canadian Retail Sales Surprisingly Declined In February

For the 24 hours to 23:00 GMT, the USD rose 0.32% against the CAD and closed at 1.3615.

The Canadian Dollar lost ground, on reports that the US is considering withdrawal from the North American Free Trade Agreement (NAFTA) between the US, Canada and Mexico.

On the data front, Canada's retail sales unexpectedly dropped 0.6% MoM in February, compared to a revised advance of 2.3% in the previous month, while investors had envisaged for a flat reading.

In the Asian session, at GMT0300, the pair is trading at 1.3558, with the USD trading 0.42% lower against the CAD from yesterday's close.

The pair is expected to find support at 1.3517, and a fall through could take it to the next support level of 1.3476. The pair is expected to find its first resistance at 1.3623, and a rise through could take it to the next resistance level of 1.3688.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

European Open Briefing: Stock Markets Fell After US President Trump’s Tax Reform Announcement Fell Short Of Expectations

Global Markets:

- Asian stock markets: Nikkei down 0.30 %, Shanghai Composite fell 0.40 %, Hang Seng lost 0.05 %, ASX 200 gained 0.05 %

- Commodities: Gold at $1268 (+0.35 %), Silver at $17.52 (+0.50 %), WTI Oil at $49.40 (-0.45 %), Brent Oil at $52.20 (-0.35 %)

- Rates: US 10 year yield at 2.32, UK 10 year yield at 1.09, German 10 year yield at 0.36

News & Data:

- PBOC sets USD/CNY reference rate for today at 6.8896 (vs. yesterday at 6.8845)

- Trump tells Canada, Mexico, he won't terminate NAFTA treaty: White House – RTRS

- Asian shares retreat from highs on doubts over Trump tax plan – RTRS

- Oil prices fall on lingering oversupply concerns – RTRS

Bank of Japan Rate Decision:

- BOJ holds rate at -0.10%, maintains 10yr yield target at 0.00%, as expected

- Japan's economy turning towards moderate expansion

- Economy, price risks tilted towards downside

- Output, exports on upward trend

- Japan economy likely to continue moderate expansion

- Momentum towards hitting 2 percent target lacking

- Long-term inflation expectations remain on weak note

Markets Update:

Stock markets fell after US President Trump's tax reform announcement fell short of expectations. There was a lack of details and the market is still doubting whether the reform will be able to pass in Congress.

The US Dollar came under pressure too. EUR/USD jumped back above 1.09, while GBP/USD is approaching again the 1.29 level. Meanwhile, USD/JPY retraced back to 111 and briefly fell below that level in the Asian session. No surprises from the BoJ, as they left interest rates and the size of their QE programme unchanged.

Nevertheless, commodity currencies remain weak. AUD/USD broke below 0.7480 support and extended losses to 0.7450 yesterday. The charts suggest a move towards 0.73 could follow in the near-term. Price action in NZD/USD is looking quite bearish as well.

The main event today will be the ECB rate decision. The market is no expecting any changes, and Draghi is likely to remain neutral during the press conference. Inflation is still low in the Euro Zone, and it will take some time for the central bank to switch to a more hawkish bias.

Upcoming Events:

- 07:00 GMT – Swiss Trade Balance

- 07:30 GMT – Bank of Japan Press Conference

- 10:00 GMT – Euro Zone Consumer Confidence

- 12:45 GMT – ECB Rate Decision

- 13:00 GMT – German CPI

- 13:30 GMT – US Durable Goods Orders

- 13:30 GMT – US Initial Jobless Claims

- 13:30 GMT – ECB Press Conference

- 15:00 GMT – US Pending Home Sales

Market Update – Asian Session: Trump Nixes Bailing On NAFTA

Asia Mid-Session Market Update: BOJ on hold as expected; Trump nixes bailing on NAFTA; Samsung Electronics shares rise on outlook

US Session Highlights

Stocks remained mostly unchanged on the day after giving up small gains made during the first half of today's session. Investors digested Trump's relatively broad tax reform plan as it was presented. Fixed income become the asset of choice again, as the 10-year yield dropped 3bps on the day. Volume continued to show strength, on NYSE at 3:30pm was 18% above its 3-month average.

Trump proposed an overhaul of the tax system with large reductions in corporate rates and amount of income brackets, though many precise details remain to be fleshed out. In the plan presented today, the corporate tax would be cut from 35% to 15% and the number of income brackets would be reduced from 7 to 3. The top income tax rate would be 35% and the lower brackets would be set to 25% and 10%. The proposal would also look at repealing the inheritance tax and limiting tax deductions.

US markets on close: Dow -0.1%, S&P500 flat, Nasdaq flat

Best Sector in S&P500: Telecommunications

Worst Sector in S&P500: Real Estate

Biggest gainers: EW +10.5%; WYN +9.0%; PRGO +7.7%

Biggest losers: STC -16.8%; CHRW -6.3%; DPS -5.5%

At the close: VIX 10.85 (bps); Treasuries: 2-yr 1.28% (bps), 10-yr 2.32% (bps), 30-yr 2.97% (bps)

US movers afterhours

TER Reports Q1 $0.44 v $0.38e, R$457M v $439Me; Guides Q2 $0.81-0.90 v $0.60e, R$660-700M v $564Me; +11.1% afterhours

UCTT Reports Q1 $0.47 v $0.42e, R$204.6M v $192Me; Guides Q2 adj $0.49-0.55 v $0.33e, R$210-220M v $181Me; +10.4% afterhours

INTU Reports season to date total Turbo Tax units were up 2% y/y; +7.3% afterhours

ALSN Reports Q1 $0.52 v $0.35e, R$499M v $463Me; +6.8% afterhours

WTW Names Mindy Grossman President and CEO, effective in July; +6.0% afterhours

SAM Reports Q1 $0.45 v $0.26e, R$161.7M v $170Me; Affirms FY17 $4.20-6.20 v $5.46e; -0.3% afterhours

ETH Reports Q3 $0.23 v $0.27e, R$180.5M v $184Me; -4.0% afterhours

CTXS Reports Q1 $0.97 v $0.94e, R$663M v $661Me; Guides Q2 $0.97-1.00 v $1.08e, R$685-695M v $693Me; -5.5% afterhours

FFIV Reports Q2 $1.95 v $1.97e, R$518M v $523Me; Guides Q3 $2.01-2.04 v $2.08e, R$520-530M v $537Me; -7.9% afterhours

AMSC; AMSC Guides Q4 rev $15-16M v $24.6Me; -35.7% afterhours

Key economic data

(JP) BOJ LEAVES INTEREST RATE ON EXCESS RESERVES (IOER) UNCHANGED AT -0.10% AND 10-YEAR JGB YIELD TARGET AT AROUND 0.0%; AS EXPECTED

(CN) CHINA MAR INDUSTRIAL PROFITS Y/Y: 23.8% V 2.3% PRIOR

(AU) AUSTRALIA Q1 IMPORT PRICE INDEX Q/Q: 1.2% V -0.5%E; EXPORT PRICE INDEX Q/Q: 9.4% V 8.0%E

(KR) SOUTH KOREA PRELIM Q1 GDP Q/Q: 0.9% V 0.8%E; Y/Y: 2.7% V 2.6%E

(JP) Japan investors net sold ¥1.82T in foreign bonds v sold ¥796B in prior week; Foreign investors net bought ¥258B in Japan stocks v bought ¥315.2B in prior week

Asia Session Notable Observations, Speakers and Press

Asian equity markets are mixed as investors digest the news out of Washington, as Trump administration has clearly shifted into a higher gear on policy. After unveiling the broad outlines to a massive corporate tax cut reduction, White House officials have taken on the trade agenda, as Commerce Min confirmed "investigation into whether aluminum imports compromise national security". This has been perceived as a shot across the bow by Beijing, calling for direct dialogue on handling trading of the metal. In similar vein, White House announced that after speaking with leaders of Canada and Mexico, Pres Trump decided not to terminate NAFTA at this time, as all leaders agreed to "enable renegotiaton of NAFTA deal" at later date.

FX market activity was more volatile on the US policy developments. USD/MXN and USD/CAD fell 1% and 0.5% respectively on NAFTA announcement, while AUD/USD saw session lows on protectionist fears from aluminum action. USD/JPY was little changed in the wake of more upbeat BOJ policy announcement, trading around 111.20. BOJ maintained its yield curve control at 0.0% on the 10-yr JGB yield and -0.1% rate on IOER, but raised its forward GDP estimates for the current year from 1.5% to 1.6% and next year from 1.1% to 1.3%. BOJ also expressed some concerns over slow progress on inflation front, cutting FY17 CPI view from 1.5% to 1.4%. In terms of its assessment, BOJ said Japan's economy has been turning towards a moderate expansion (prior was continues to recover moderately), while also boosting its view of Exports and Industrial Output to "increasing trend" from "picked up".

Among key corporates, Samsung Electronics final Q1 results was below consensus at KRW) Net 7.49T v 8.8Te on Rev of 50.6T v 56.5Te, but the company forecast Net profit to turn higher this year, Capex to increase, and smartphone sales to bounce. SE also announced its first ever dividend and a KRW2.3T buyback, earning praise from activist Elliott Management which had in the past called for a split into a holding vehicle even though the company did not commit to that structure. After initial downside, shares moved higher by about 2%.

China

(US) Commerce Dept confirms opening investigation into whether aluminum imports compromise national security

(CN) China Commerce Ministry: US Commerce Dept mishandled China plywood companies in subsidies probe; Urging US to abide by WTO rules in plywood probe; need a dialogue with Us to address aluminum - press

(CN) China MOFCOM reports Q1 exports to Belt and Road nations +26.2% y/y (28.2% of total exports)

(CN) China Iron and Steel Association (CISA): memorandum signed by President Trump encouraging an investigation of US steel imports is contrary to fair trade and sends a signal of protectionism

Australia

(AU) Australia PM Turnbull expected to impose a Domestic Gas Security Mechanism from July 1 this year and that it would not require legislation in Parliament as it can be imposed as a customs regulation

Korea

(KR) South Korea Trade Ministry raises 2017 export growth outlook to 6-7% v 2.9% prior

(KR) White House administration signs communique directed at North Korea following briefing with US lawmakers

Asian Equity Indices/Futures (00:00ET)

Nikkei -0.2%, Hang Seng flat, Shanghai Composite -0.4%, ASX200 +0.2%, Kospi -0.2%

Equity Futures: S&P500 +0.1%; Nasdaq +0.1%, Dax +0.2%, FTSE100 +0.1%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.0900-1.0920; JPY 111.00-111.40; AUD 0.7470-0.7490; NZD 0.6890-0.6920

June Gold +0.3% at 1,268/oz; June Crude Oil -0.5% at $49.37/brl; July Copper -0.4% at $2.59/lb

SLV iShares Silver Trust ETF daily holdings rise to 10,273 tonnes from 10,178 tonnes prior

(CN) PBOC SETS YUAN MID POINT AT 6.8896 V 6.8845 PRIOR; 3rd straight weaker setting; weakest setting since Apr 12th

(CN) PBOC to inject combined CNY50B v CNY80B prior in 7-day, 14-day and 28-day reverse repos, 8th straight injection

(NZ) New Zealand MoF sells NZ$150M in 2037 bonds

Asia equities / Notables / movers by sector

Samsung Electrocnis, 005930.KR +1.9%, final Q1 results

AIA, 1299.HK, +4.4%, Q1 results

Sands China, 1928.HK, -3.3%, Q1 results

Tokuyama, 4043.JP, +5.8%, sells Malaysia business

Canon, 7751.JP, +3.9%, Q1 results

Yahoo Japan, 4689.JP, -9.9% FY16/17 results

China Minsheng Bank, 1988.HK, +1.3%, Q1 results

China Shipbuilding Industry, 601989.CN, -3.7%, Q1 results

BHP, BHP.AU, -1.0%, weaker on Australia Govt gas export limitation plan

Clean TeQ Holdings, CLQ.AU, +14.8%, results

Ten Networks, TEN.AU, -15.2%; H1 results, going concerns on fuding