Sample Category Title

Canadian Retail Sales Fall 0.6% In February

'January's strong sales, as well as other recent positive data, still put the first quarter on track for growth of around 3%.' - Andrew Kelvin, TD Securities

A monthly report released by Statistics Canada showed that retail sales slipped more than experts estimated. In February, the amount of sales in the retail sector plunged 0.6% to C$47.8B ($35.1B) after a 2.3% spike in January. Negative growth was recorded in five out of 11 key sectors that represented 67% of the total retail sales. The largest contribution to the February drop was made by the gasoline stations sector, where sales tumbled 3.6% and marked the first decline in three months. The other key contributor was the motor vehicle and parts dealers sector, which posted a 1.8% sales fall for the first time in seven months. In the food and beverage shops sector the weakest sales were registered among liquor stores, which receipts plunged 1.7%. Meanwhile, the largest fall in February occurred in the jewellery, luggage and leather goods stores sub-sector, where sales declined 6.2% in the reported month. In contrast, sales at ordinary clothing and shoe stores soared 3.4% and 2.0%, respectively, and that was enough to offset the overall slip in the clothing sector. In addition, the health and personal care stores sector posted a sales increase of 2.0%. Furthermore, book and music stores also posted a 2.1% gain. Finally, e-commerce sales advanced 27.4% an annual basis, accounting for 2.4% of the total retail sector.

US Crude Oil Inventories Post Third Straight Weekly Decline

'Demand for refined products remains weak for this time of the year, which will be a cause for concern over the coming weeks if demand fails to recover.' - Abhishek Kumar, Interfax Energy's Global Gas Analytics

Last week, US crude oil inventories dropped more than expected, while gasoline and distillate stocks rose markedly, owing to increased production at refineries. The EIA reported on Wednesday that US crude stockpiles fell 3.6M barrels in the week ending April 21, following the preceding week's decline of 1.0M barrels and surpassing expectations for a 1.1M barrel decrease. It marked the third consecutive weekly decline in crude oil inventories and provided support to oil prices. At this time of the year refineries start boosting production ahead of the summer driving season. Therefore, crude inventories are set to fall further, pushing the oil price higher. Refineries' production rose 347,000 barrels per day to 17.3M barrels per day, while the utilisation rate climbed 1.2% to 94.1%, the highest since November 2015. Crude imports rose to 7.8M barrels per day, whereas exports climbed to 1.2M barrels per day, the highest since February 17. Nevertheless, consumption remained subdued, as total production demand dropped 2.2% on an annual basis to 19.5M barrels per day. The EIA also said that gasoline stockpiles advanced 3.4M barrels, while analysts anticipated a 1.0M barrel decline. Moreover, distillate stocks climbed 2.7M barrels, topping expectations for a 1.0M barrel fall.

Bank Of Japan (BoJ) Leaves Its Monetary Policy Unchanged But Cuts Its Inflation Forecast

'Consumer price growth is around zero, which makes all of these price forecasts look overly optimistic. The BOJ upgraded its economic assessment, but this is due more to overseas demand. Japan's labor market is tight, but retailers still want to cut prices.' - Shuji Tonouchi, Mitsubishi UFJ Morgan Stanley Securities

As markets expected, the Bank of Japan left its monetary policy unchanged at its meeting on Thursday; however, policymakers an optimistic and confident view on the economy in the future amid higher oversees demand. The Central bank voted to keep its short-term interest rate at -0.10% and asset purchases unchanged at about 80 trillion yen ($700B) annually. At yesterday's meeting, the Bank also cut its core inflation forecast for the year ending in March 2018 to 1.4% from 1.5%, due to low services and durable goods prices. Moreover, policymakers stated that their inflation projections remained weak and, therefore, the Bank's monetary policy could be kept on hold for an indefinite period of time. Although, the BoJ expressed hopes that inflation would reach its 2% target in the year ending March 2019. Nevertheless, a majority of economists doubt that inflation will pick up as the BoJ forecasts with subdued pay growth putting pressure on consumer spending. Furthermore, back in February, consumer prices rose just 0.2% on an annual basis amid weak consumption. Overall, the Japanese economy is expected to continue expanding at a moderate pace, according to the Bank's projections. However, the BoJ is unlikely to withdraw some of its stimulus in the near-term.

CAD And MXN Recover After Trump Says US Won’t Quit NAFTA

USD’s dead cat bounce

The euphoria that surrounded President Trump's tax plan announcement did not last long as, surprisingly, he failed to provide concrete policy details. After starting the day on the front foot, the US stock market reversed gains and pushed most indices into negative territory. European markets followed Wall Street leads and opened below the neutral threshold on Thursday, with the Euro Stoxx 600 sliding 0.40%. In the FX market, the US dollar was unable to consolidate pre-announcement gains and lost ground against most G10 currencies.

The Canadian dollar was the best performer this morning as it rose 0.35% against the greenback, erasing yesterday's losses completely. After tumbling earlier this week when Trump slapped tariffs on imported Canadian softwood lumber, the loonie got a breath of fresh air amid a declaration that the US will not terminate NAFTA 'at this time' but would rather try to re-negotiate the treaty.

Since the threat of the US leaving NAFTA was the biggest headache for Mexico and Canada, we anticipate that selling pressures on the CAD and the MXN will ease further. However, we believe that we won’t see a sharp rally as the unpredictability of Trump will keep investors on the defensive.

Draghi set to show optimism in Eurozone recovery

Today's European Central Bank meeting is in the middle of the French Presidential election and the European institution certainly welcomed Emmanuel Macron's victory in the first round as there were certainly fears of a second round pitting Jean-Luc Mélenchon against Marine Le Pen.

Now ECB President Mario Draghi, whose press conference will be given at 1.30pm CET, is going to discuss his views regarding the Eurozone recovery. For the time being, it is very likely that the current level of asset purchases (€60 billion) will continue until year-end. We believe that for some more time, the ECB will remain committed to low rates.

Financial markets are clearly not pricing anything else but a Macron victory in France, which seems to rule out any political risks for the ECB. In Europe, economic fundamentals are better, inflation is picking up and unemployment has decreased, even though it remains very high in peripheral countries. So this meeting will be useful to assess the degree of optimism that could lead to a tightening policy in the near future. Markets are likely to price in better confidence and we remain bullish on the Euro in the short-term.

Technical Outlook: AUDUSD Remains Under Strong Pressure, Limited Recovery Keeps Immediate Risk At The Downside

The pair is consolidating on Thursday after suffering heavy losses earlier this week. Wednesday's strong bearish acceleration extended below key supports at 0.7490/70 and dipped to 0.7453 (50% retracement of 0.7159/0.7747 rally) where it found temporary footstep.

Recovery attempts were so far capped by last week's low at 0.7490, which is guarding weekly cloud top at 0.7518 and signaling limited upside. Near-term risk remains turned lower for renewed attempts below cracked 100SMA (0.7463) and yesterday's low (0.7453) to extend bear-phase from 0.7747 (21 Mar high) towards next target at 0.7384 (Fibo 61.8% of 0.7159/0.7747).

Res: 0.7490, 0.7518, 0.7531, 0.7553

Sup: 0.7463, 0.7453- 0.7384, 0.7329

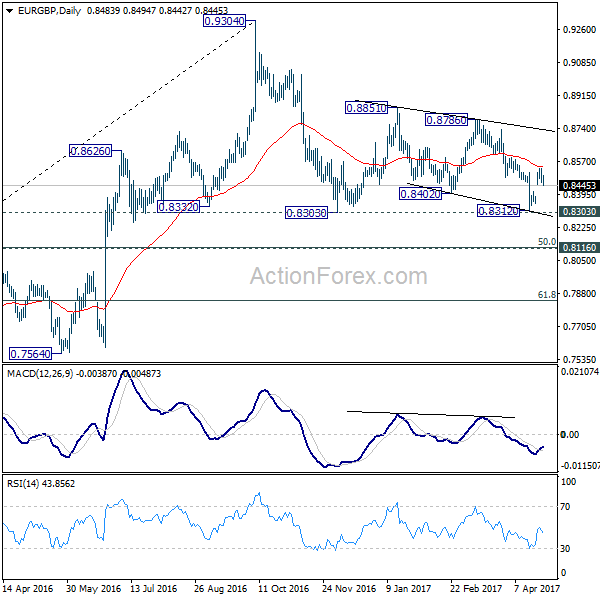

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8452; (P) 0.8491; (R1) 0.8524; More...

A temporary top is in place at 0.8529 and intraday bias is turned neutral and EUR/GBP first. Above 0.8529 will target 0.8786 resistance. Firm break there could bring further rally towards 0.9304 high. Nonetheless, price actions from 0.9304 are seen as a corrective pattern and there is no clear sign of up trend resumption yet. Hence, even in that case, we'll stay cautious on strong resistance below 0.9304. On the downside, below 0.8413 minor support with turn focus back to 0.8303 instead.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. In any case, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Rise from 0.6935 (2015 low) will resume at a later stage to 0.9799 (2008 high). However, sustained break of 0.8116 could bring deeper decline to next key support level at 0.7564 before the correction completes.

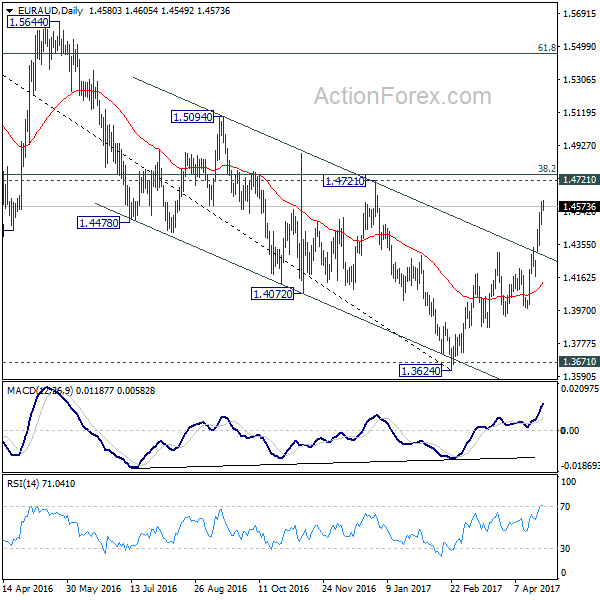

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4501; (P) 1.4550; (R1) 1.4638; More...

A temporary top could be in place at 1.4605 and intraday bias in EUR/AUD is turned neutral for consolidation. Downside of retreat should be contained by 1.4334 support and bring another rise. We're holding on to the case off trend reversal after defending 1.3671 key support. Above 1.4605 will target 1.4721 resistance. Decisive break of 1.4721 will confirm our bullish view.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction could be completed after defending 1.3671 key support. Break of 1.4721 cluster resistance (38.2% retracement of 1.6587 to 1.3624 at 1.4756) should confirm this case and target 61.8% retracement at 1.5455 and above. Overall, we'd expect the up trend from 1.1602 to resume later. However, sustained break of 1.3671 will invalidate our bullish view and would turn extend the fall from 1.6587 towards 1.1602 long term bottom.

Trump’s Tax Reform Plan Could Lead To Rising Deficit

US Treasury Secretary Mnuchin announced Trump's tax reform plan in a press conference yesterday; the biggest tax reform plan since 1986.

Trump has proposed slashing corporate tax from the current rate of 35% to 15%; from one of the highest in the world to one of the lowest. In terms of personal income tax, the current 7 tax bands (minimum 10%, maximum 39.6%) is to be simplified to 3 bands instead (10%,25%,35%). Trump has also called for a repeal of the 3.8% tax on investment income and death tax.

The aim for the plan is to improve corporate competitiveness, encourage US companies to repatriate overseas funds held offshore, create more jobs, and spur economic growth to a 3% target.

The dollar index and US stock markets nudged up ahead of the press conference lifted by market expectations on Trump's tax reform plan. However, it was followed by a retracement after the press conference. Dow Jones and the S & P 500 indexes failed to breach the psychological level at 21000 and 2400 respectively.

Although corporate tax cut will spur economic growth it will also slash more than $600 billion in revenue a year resulting in a rising deficit due to reduced tax revenue.

Trump had planned to finance tax cuts by a reduction in healthcare costs after repealing Obamacare. However, as the new healthcare bill had failed to pass on March 24, the US government's prospective financial stress will likely become heavier. Trump now expects the costs would lead to a 3% annual economic growth.

Trump has also promised a $1 trillion infrastructure plan, with an increase in spending on military defense, which will further add to the government deficit during his presidency.

The tax reform bill will still need Congress's approval to pass. Considering the prospective rising deficit, it is likely that conservative Republicans might not support the tax reform bill. If Trump is unable to get enough support again it will likely lead to substantial market disappointment likely to initiate a USD and Equity sell off.

The European Central Bank (ECB) will announce its interest rate decision at 12:45 BST today. It will be followed by the ECB's press conference at 13:30 BST. Markets expect that the ECB will keep rates on hold and keep the current QE programme unchanged. However, we need to keep an eye on whether the ECB will give hints about prospective gradual QE reduction. US durable goods and core durable goods for March are released at 13:30 BST.

ECB Meeting: Not Ready To Change Tune Yet

Today, the highlight will be the ECB rate decision, followed by a press conference from President Draghi. The forecast is for no change in policy. On Tuesday, the euro surged following a Reuters report that the Bank may communicate a more optimistic bias at its coming meetings. We think it is far too early for that to happen at this gathering. The recent concerns of the officials with regards to a surge in Eurozone's bond yields, combined with the slowdown in the core CPI for March, suggest that the Bank could stay patient for now and wait at least until the June gathering to communicate a more upbeat bias. By that time, political risks that keep a risk premium on European yields may have dissipated further, and the bloc's core CPI may have picked up steam again.

As such, we think that Draghi will probably maintain a cautious tone overall and avoid fueling any tapering expectations today. The euro may experience a pullback in case such signals are seen as dovish, but given the currency's short-term uptrend, we would expect any negative reaction to remain relatively short-lived.

EUR/USD is already in a retreat mode. Yesterday the pair pulled back after it found resistance near the crossroad of the 1.0955 (R2) level and the upside resistance line drawn from the peak of the 2nd of February. However, given that the rate is trading above the longer-term downtrend line taken from the peak of the 3rd of May 2016, we consider the outlook to be positive. We would treat any slide on Draghi's comments as an extension of yesterday's correction and we see the likelihood for such a retreat to stay limited near the 1.0800 territory.

Trump says he will not immediately scrap NAFTA; CAD & MXN jump

CAD and MXN both experienced a relief bounce during the Asian morning Thursday, following news that President Trump will not immediately scrap NAFTA, and will instead renegotiate it. This announcement followed several media reports yesterday that the US administration may issue an executive order declaring its intention to withdraw from the trade agreement. Although these news could keep CAD and MXN supported for a few days, any sustained positive reaction in these currencies seems unlikely, at least not until the trade landscape clears out.

USD/CAD tumbled after it hit the 1.3645 (R3) resistance to stop at the 1.3530 (S1) support level. The rate is now back below the 1.3600 (R2) territory, which is the upper bound of the sideways range it has been oscillating within since September. Therefore, we expect the pair to stay within that range and the slide to continue for a while. A clear dip below 1.3530 (S1) is possible to initially aim for the next support of 1.3490 (S2), defined by Tuesday's low.

As for the US tax announcement yesterday, it was disappointing overall, offering no concrete details regarding the planned reforms, other than what we already knew from media reports and leaks over the past days. Perhaps due to the lack of clarity, both USD and US stock indices moved lower in the aftermath.

BOJ meeting: No surprises

Overnight, the BoJ kept its policy unchanged. The meeting statement contained no major surprises, with the Bank upgrading its assessment for the Japanese economy, but revising down its inflation forecasts. Perhaps due to the lack of new information, there was no reaction in JPY. We continue to expect the officials to keep their framework of QQE with yield curve control intact for the foreseeable future.

As for the rest of today's highlights:

In Sweden, the Riksbank's policy decision will be in focus. Expectations are for this Bank to stand pat as well. At the latest gathering, the Bank shifted to a much more dovish bias, expressing heightened concerns with regards to the strength of SEK. With data after that gathering showing that the nation's CPI slowed in March, we doubt that the Bank will change its dovish tone. This could hurt SEK.

On the indicators' front, Germany's preliminary CPI for April is expected to have accelerated, but given that these data will be released a few minutes ahead of Draghi's press conference, they may attract less attention than usual.

From the US, we get durable goods orders for March. Both the headline and the core figures are expected to have slowed from previously. The forecasts are supported by the nation's ISM manufacturing PMI for the month, where the New Orders sub-index slid somewhat. Something like that could hurt USD somewhat.

EUR/USD

Support: 1.0855 (S1), 1.0825 (S2), 1.0800 (S3)

Resistance: 1.0915 (R1), 1.0955 (R2), 1.1000 (R3)

USD/CAD

Support: 1.3530 (S1), 1.3490 (S2), 1.3455 (S3)

Resistance: 1.3560 (R1), 1.3600 (R2), 1.3645 (R3)

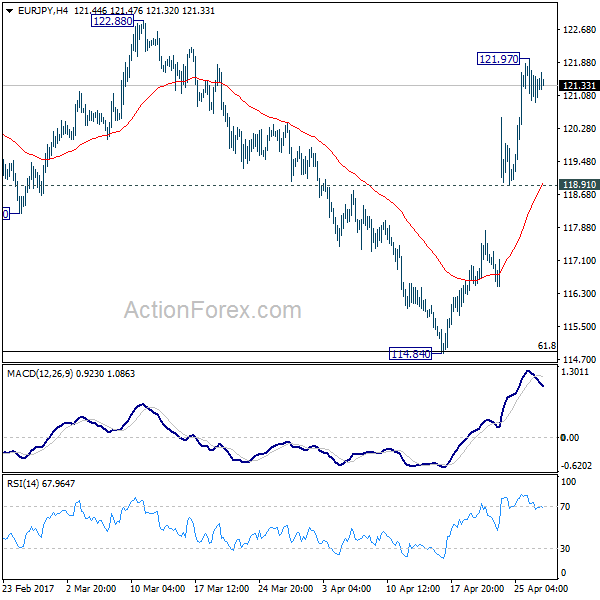

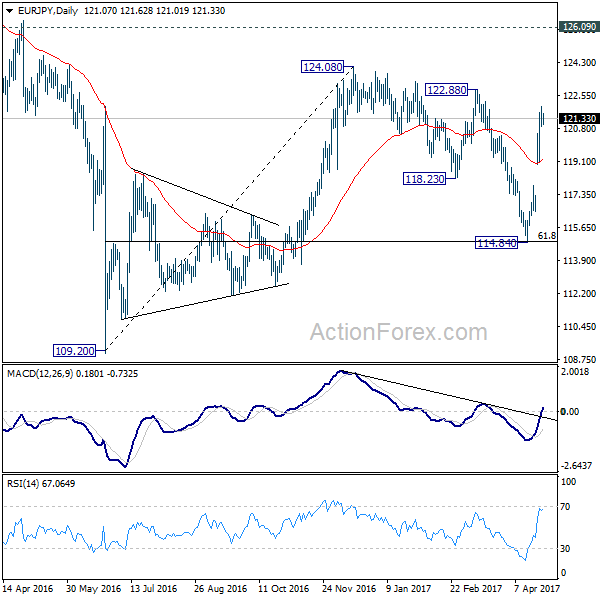

EUR/JPY Daily Outlook

Daily Pivots: (S1) 120.68; (P) 121.32; (R1) 121.74; More...

A temporary top is in place at 121.97 in EUR/JPY and intraday bias is turned neutral first. Some consolidations would be seen but downside should be contained by 118.91 support and bring another rally. Above 121.97 will target 122.88 resistance first. Break will likely resume the larger rally from 109.20. In such case, EUR/JPY should break through 124.08 to 126.09 key resistance level.

In the bigger picture, price actions from 109.20 is still seen as a corrective move for the moment. But current development suggests that the first leg is finished at 109.20, second leg at 114.84. And rise from 114.84 is possibly developing into the third leg. Further rise will now be in favor through 124.08 resistance. Strong break of 126.09 support turned resistance will confirm completion of whole fall from 149.76 at 109.20. In such case, rise from 109.20 is developing into a medium term move for 141.04 and above.