Sample Category Title

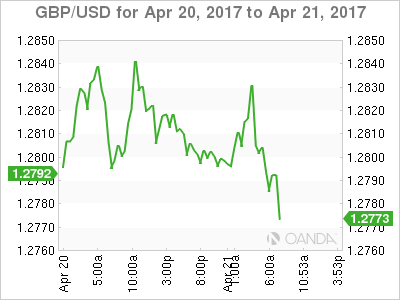

Trade Idea Update: GBP/USD – Buy at 1.2710

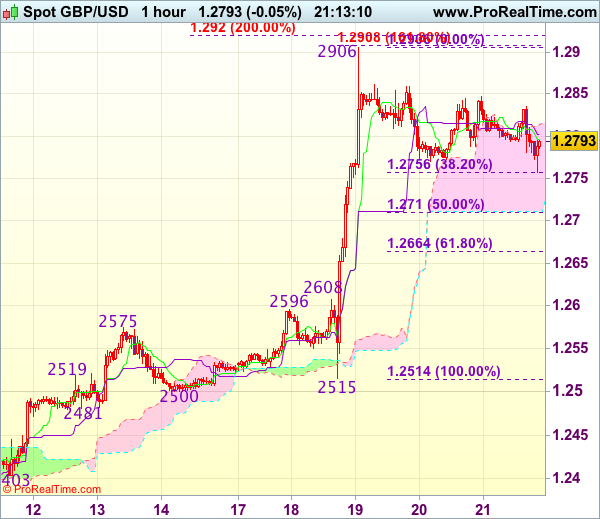

GBP/USD - 1.2788

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2814

Kijun-Sen level : 1.2817

Ichimoku cloud top : 1.2810

Ichimoku cloud bottom : 1.2711

Original strategy :

Buy at 1.2710, Target: 1.2850, Stop: 1.2675

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2710, Target: 1.2850, Stop: 1.2675

Position : -

Target : -

Stop : -

Cable has remained confined within familiar range and further sideways trading is in store, however, downside should be limited to 1.2755-60 (38.2% Fibonacci retracement of 1.2515-1.2906) and reckon 1.2700-10 would hold, bring another rally, break of 1.2755069 would signal the pullback from 1.2906 has ended, bring retest of this level, break there would extend recent upmove to 1.2920-30 (2 times extension of 1.2365-1.2575 measuring from 1.2500), then 1.2950 but loss of near term upward momentum should prevent sharp move beyond 1.2990-00 (1.236 times projection of 1.2109-1.2616 measuring from 1.2365 and psychological resistance).

In view of this, would not chase this rise here and would be prudent to buy cable on subsequent pullback as downside should be limited to 1.2710 (50% Fibonacci retracement of 1.2515-1.2906), bring another rise. Below 1.2700 would defer and signal top has been formed, risk correction to 1.2660-65 (61.8% Fibonacci retracement of 1.2515-1.2906) and price should stay well above 1.2608-16 (previous resistance now support).

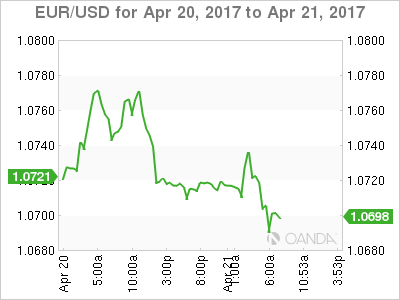

Trade Idea Update: EUR/USD – Hold long entered at 1.0690

EUR/USD - 1.0700

Original strategy :

Bought at 1.0690, Target: 1.0790, Stop: 1.0655

Position : - Long at 1.0690

Target : - 1.0790

Stop : - 1.0655

New strategy :

Hold long entered at 1.0690, Target: 1.0790, Stop: 1.0655

Position : - Long at 1.0690

Target : - 1.0790

Stop : - 1.0665

Euro’s retreat after rising to 1.0778 yesterday suggests a temporary top has been made there and consolidation with mild downside bias is seen for marginal weakness from here, however, reckon downside would be limited and bring another rise later to 1.0783-85 (61.8% projection of 1.0602-1.0737 measuring from 1.0700), then 1.0800-10 but loss of near term upward momentum should prevent sharp move beyond 1.0825-30, risk from there is seen for a retreat to take place later.

In view of this, we are holding on to our long position entered at 1.0690. Only below previous resistance at 1.0670 (now support) would abort and signal top is formed instead, bring correction towards previous support at 1.0635 which is likely to hold from here.

Trade Idea Update: USD/JPY – Stand aside

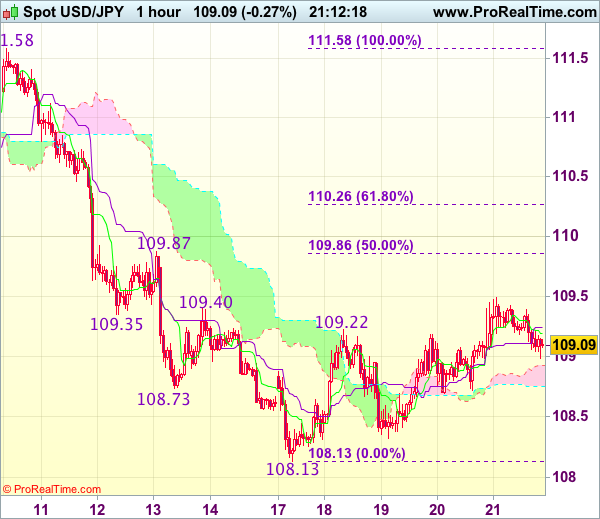

USD/JPY - 109.10

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although yesterday’s anticipated rebound to 109.49 adds credence to our near term bullish view for the erratic rise from 108.13 to bring retracement of recent decline, reckon upside would be limited to 109.86-87 (50% Fibonacci retracement of 111.58-108.13 and previous resistance), however, price should falter below 110.25-30 (61.8% Fibonacci retracement) and bring retreat later.

In view of this, would not chase this rise here and would be prudent to stand aside for now. Below 108.65-70 would suggest top is formed, bring weakness to 108.30-32, break there would signal the rebound from 108.13 has ended, bring retest of this level first.

CAC Quiet as Investors Cautious Ahead of French Vote

The CAC is showing little change on Friday, following strong gains in the Thursday session. Currently the CAC is trading at 5073.50. On the release front, French and Eurozone Manufacturing PMIs both beat their estimates, and the Eurozone current account surplus easily beat expectations. On Saturday, US Treasury Secretary Robert Mnuchin will speak at the International Monetary Fund meeting in Washington. On Sunday, France goes to the polls for the first round of the presidential election.

European investors are holding their breath, as France goes to the polls on Sunday, in the first round of the presidential election. The election campaign has been divisive and turbulent, in one of the tightest elections in years. The four front-runners (in a crowded field of 11) are all within a few percentage points of one another. Given the tightness and unpredictability of the race, final opinion polls have become market-movers. The CEC posted strong gains on Thursday, following an opinion poll which showed Emmanuel Macron opening a slight lead with 25% of the vote, just ahead of far-right candidate Marie Le Pen with 22%. Le Pen's platform includes sharp curbs on immigration and a referendum on France's membership in the European Union. If Le Pen does better than predicted, investor sentiment could send the stock markets lower. A shooting in Paris on Thursday which killed a policeman and a tourist have stretched taut nerves even further, as security and the terrorism threat remain one of the key issues in the campaign. The markets are expecting more volatility ahead of and following the election, and French banks will be staffed throughout Sunday night in order to respond quickly to the election results. Traders should be prepared for volatility from the CEC in the Monday session.

The eurozone economy continues to expand, and this was underscored by strong PMIs out of Europe. Eurozone, French and German PMIs all pointed to expansion in the services and manufacturing sectors. Manufacturing data was particularly encouraging, as Eurozone and French Manufacturing PMIs beat expectations. However, these strong readings failed to move the CAC, as investors are keeping low ahead of the French election on Sunday. There was more positive news as the eurozone's current account surplus jumped to EUR 37.9 billion, well above the estimate of EUR 26.3 billion.

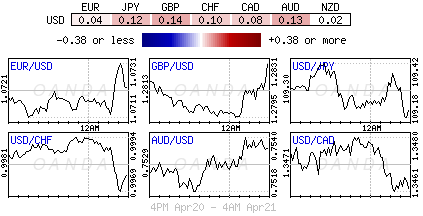

With the US economy in good shape, the markets are expecting interest rates to continue rising in 2017. The Fed has broadly hinted that it will gradually raise rates this year, but it's unclear how many times Janet Yellen will press the rate trigger. Most analysts are expecting two more moves this year, but there have been calls from some Fed policymakers for three more hikes. However, soft retail sales and CPI numbers in March are likely to make the Fed more dovish, and on Tuesday, the Atlanta and New York Federal Reserve lowered their outlook for US economic growth for the first quarter. The Fed can point to a labor market that is close to capacity as well as strong consumer confidence, but surprisingly, this has not translated into stronger consumer spending, a key driver of economic growth. The Fed is unlikely to make a move in May, but June is a strong possibility. However, the odds of a June move are showing a surprising amount of volatility, and the latest CME Group reading shows the likelihood a 1/4 point hike have jumped to 58%, up from 51% earlier this week.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0688; (P) 1.0733 (R1) 1.0759; More....

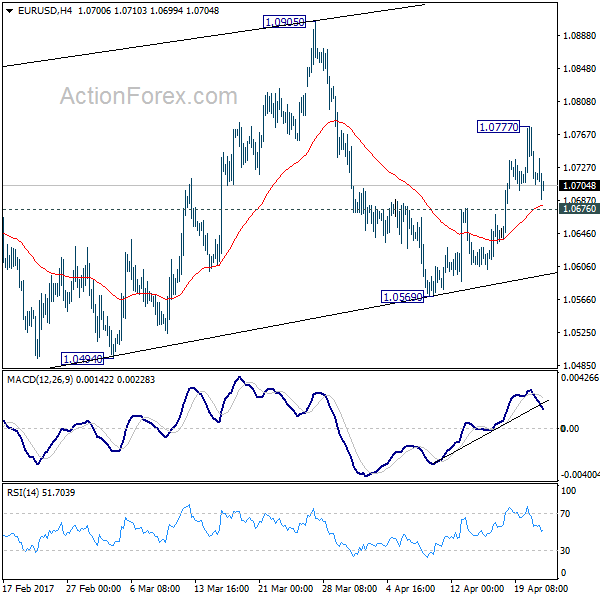

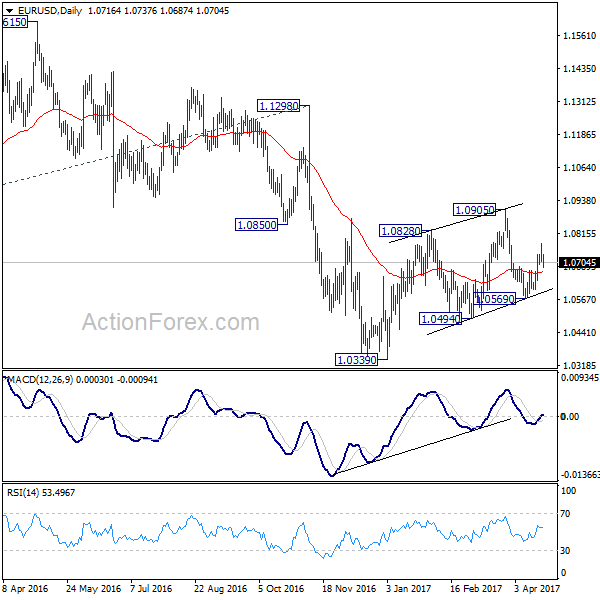

EUR/USD's retreat from 1.0777 extends lower today but it's still staying above 1.0676 minor support. Intraday bias remains neutral and another rise is still in favor. Above 1.0777 will target 1.0905 and above. But still, choppy rise from 1.0339 is still seen as a correction. Hence, we'll pay attention to topping signal above 1.0905 again, as we'd expect larger down trend to resume later. On the downside, break of 1.0676 minor support will turn intraday bias back to the downside for 1.0569 instead.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.

Euro Weakens Further as French Presidential Elections Looms

Euro dips further today as markets are lighting up positions ahead of the first round of French presidential election this Sunday. Far right Marine Le Pen and centrist Emmanuel Macron are still tipped to come out as winners and head to the run-off on May 7. But yesterday's terrorist attack in Paris could stir up some uncertainties. In particular, far left leader Jean-Luc Melenchon has rather strong momentum in the past two weeks and emerged as a real contender. Euro would very likely suffer if Melenchon could slip into the run-off and take Macron's place. Both Le Pen and Melenchon are euro-sceptic, just at two different extremes. But the common currency could have a relieve rally next week if the election delivers no surprise.

Eurozone PMIs came in strong

Eurozone PMI manufacturing rose to 56.8 in April, up from 56.2, and beat expectation of 56.1. Eurozone PMI services Rose to 56.2, up from 56.0 and beat expectation of 56.0. Germany PMI manufacturing dropped to 58.2, down from 58.3 but beat expectation of 58.1. Germany PMI services dropped to 54.7, down from 55.6 and missed expectation of 55.5. France PMI manufacturing surged to 55.1, up from 53.3 and beat expectation of 53.2. France PMI services rose to 57.7, up from 57.5 and beat expectation of 57.2. Markit noted that "there is a good outlook for the year - it looks like the upturn has legs. With numbers like these, people are going to start edging up their forecasts."

EU Brexit negotiation document leaked

According to a leaked draft EU Brexit negotiation document, UK will be required to pay off the obligations after Brexit, remain subject to EU court and, be required to let relatives of European immigrants settle in UK. And the keys of the negotiation would be about protecting rights of three million EU citizens living in UK. Meanwhile, EU will insist on having ECJ jurisdiction to enforce the rules during the transition period. And that would be in direct conflict with UK as Prime Minister Theresa May would seen to end that ECJ jurisdiction in UK. While EU might consider alternative dispute system for the treaty, it would be under the condition on equivalence to the ECJ.

Finnish RM Orpo: No one will want to follow Brexit

Finland's Finance Minister Petteri Orpo said that UK's "divorce" with EU is "inevitably going to be so painful that no one will want to feel it for themselves." And it's going to be a "precedent no one will want to follow." Meanwhile Orpro is confident that "there should be no slowdown in developing the EU because of Brexit." Instead, the member states should "push even harder". Separatrly, EU Brexit negotiator Michel Barnier said that the so called EUR 60b "Brexit bill" is not "revenge" no punishment" and he emphasized that "we don't want to ask the Brits to pay a single euro more than" their legal obligations.

On the data front...

Canada CPI slowed to 1.6% yoy in March, below expectation of 1.8% yoy. CPI core-trim slowed to 1.4% yoy, CPI core-medium slowed to 1.7% yoy, CPI core-common was unchanged at 1.3% yoy. UK retail sales dropped -1.8% mom in March. Japan PMI manufacturing rose to 52.8 in April, up from 52.4 and beat expectation of 52.5. Also from Japan, tertiary industry index rose 0.2% mom in February.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0688; (P) 1.0733 (R1) 1.0759; More....

EUR/USD's retreat from 1.0777 extends lower today but it's still staying above 1.0676 minor support. Intraday bias remains neutral and another rise is still in favor. Above 1.0777 will target 1.0905 and above. But still, choppy rise from 1.0339 is still seen as a correction. Hence, we'll pay attention to topping signal above 1.0905 again, as we'd expect larger down trend to resume later. On the downside, break of 1.0676 minor support will turn intraday bias back to the downside for 1.0569 instead.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | JPY | PMI Manufacturing Apr P | 52.8 | 52.5 | 52.4 | |

| 04:30 | JPY | Tertiary Industry Index M/M Feb | 0.20% | 0.30% | 0.00% | -0.20% |

| 07:00 | EUR | France Manufacturing PMI Apr P | 55.1 | 53.2 | 53.3 | |

| 07:00 | EUR | France Services PMI Apr P | 57.7 | 57.2 | 57.5 | |

| 07:30 | EUR | Germany Manufacturing PMI Apr P | 58.2 | 58.1 | 58.3 | |

| 07:30 | EUR | Germany Services PMI Apr P | 54.7 | 55.5 | 55.6 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Apr P | 56.8 | 56.1 | 56.2 | |

| 08:00 | EUR | Eurozone Services PMI Apr P | 56.2 | 56 | 56 | |

| 08:00 | EUR | Eurozone Current Account (EUR) Feb | 37.9B | 26.3B | 24.1B | |

| 08:30 | GBP | Retail Sales M/M Mar | -1.80% | -0.30% | 1.40% | |

| 12:30 | CAD | CPI M/M Mar | 0.20% | 0.40% | 0.20% | |

| 12:30 | CAD | CPI Y/Y Mar | 1.60% | 1.80% | 2.00% | |

| 12:30 | CAD | CPI Core - Trim Y/Y Mar | 1.40% | 1.60% | ||

| 12:30 | CAD | CPI Core - Median Y/Y Mar | 1.70% | 1.90% | ||

| 12:30 | CAD | CPI Core - Common Y/Y Mar | 1.30% | 1.30% | ||

| 13:45 | USD | Manufacturing PMI Apr P | 53.9 | 53.3 | ||

| 13:45 | USD | Services PMI Apr P | 53.7 | 52.8 | ||

| 14:00 | USD | Existing Home Sales Mar | 5.61M | 5.48M |

French Election Monitor: Markets Hold Their Breath as First Election Round Draws Near

As election day for the first round of France's presidential election approaches on Sunday, the result remains unpredictable, with the four leading candidates Marine Le Pen, Emmanuel Macron, François Fillon and Jean-Luc Mélenchon head to head in the polls. Around 30% of voters are still undecided, as outlined in French Election Monitor #2, 18 April. The market reaction afterwards will depend largely on the candidate combination in the second round and we see three broad risk scenarios, depending on the chances of an EU sceptic proceeding to the second round and subsequently winning the presidency (see below). While a run-off between Fillon and Macron would be the lowest risk scenario, with no EU sceptic reaching the second round, we see a face-off between the two EU sceptics Le Pen and Mélenchon as the highest risk scenario, with the biggest adverse market reaction. A 'surprise' scenario where we see, for example, Le Pen significantly outperforming the polls, gaining some 30-49% of the vote in the first round, should also be considered a high-risk scenario, as, in this case, the predictive power of second round polls would also be highly questionable, even if her contender is Macron.

Voting stations will open at 08:00 CEST on Sunday and close at 19:00 in small towns and 20:00 in big cities. Voting in the French overseas constituencies will take place on Saturday, to ensure that voting takes place before any preliminary results are published. Exit polls by the main TV and radio channels are due to be published at 20:00 on Sunday and have been relatively accurate in the past. Keep an eye out for voter turnout estimations released during the day. Lower participation, as suggested by the polls, would be likely to boost Le Pen's chances of winning, as her supporters remain the most certain of their choice.

Official election results will be released by the Ministry of the Interior over the course of the night and updated continually as new results come in district by district. Due to France's overseas territories, the final result will probably be released on Monday around midday. However, unless the race is very tight, the votes from the overseas territories should not move the result much and we should have a good indication of the outcome around midnight or in the early hours of Monday morning.

French PMI Hits 71 Month High

- Sterling remains strong ahead of UK retail data

- NZD unchanged by slip in consumer confidence

- French PMI hits 71 month high

Yet another murderous fanatic has paid the price for his attack on French police but not before he killed one officer and injured others. I guess we must all be grateful we don't understand what would possess someone to take such meaningless violence onto the streets. That's what marks the rest of us out as sane.

New Zealand consumer confidence slipped a little in April but remains at average levels. Most analysts seem to expect the RBNZ to start raising interest rates in the early part of 2018 and not before. The NZ Dollar remains surprisingly strong in spite of that but slowing housing prices in Auckland and elsewhere have taken the shine off consumer optimism.

The French Purchasing Managers' Indices came out much better than expected this morning; in fact the manufacturing sector index is at a 71 month high. We await the German and EU data this morning and the forecasts are good. Perhaps the Euro will pick up some strength from that but nervousness ahead of the 1st round of the French Presidential election will temper any positive-Euro vibe, even though Marine Le Pen has committed to a referendum before taking France out of the Euro.

We'll get the UK retail sales data this morning as well. The markets are looking for a small dip after last month's very positive 1.4% rise. However, improved weather could have tipped the high street sales into a positive figure. Sterling is riding high but struggling to get above solid resistance at €1.20 and $1.30. If those levels were to break though, there is loads of upward momentum due to be unleashed. Any hint of BOE rate hikes would do it and positive consumer activity is a good catalyst for that.

This afternoon brings Canadian inflation data and a little dip from the previous 2.0% level is forecast. The Canadian Dollar has slipped a little of late, in line with US Dollar weakness and in the absence of major commodity rises. Perhaps lower inflation would cause the Canadian Dollar to slip through to C$1.75 against the Pound.

And Happy Birthday Ma'am. It is her Majesty the Queen's 91st Birthday today (the real one, not the procession one) and, may I say you are looking very well on it Your Highness. This is also the day that it is believed Rome was founded, Henry VIII came to the throne, Manfred von Richthofen, 'The Red Baron' was killed and it is the day that Mark Twain (real name Samuel Langhorne Clemens, passed away. One of my favourite Mark Twain quotes is "I am an old man and have known many troubles but most of them never happened," oh and he wrote, 'I didn't attend the funeral but I sent a nice letter saying I approved of it.')

Short Jokes

My new thesaurus is terrible. Not only that but it's also surprisingly circumnavigation.

What is E.T. short for? Because he only has little legs.

What do you call a fake noodle? Impasta.

www.conjunctivitis.com....a site for sore eyes.

A French cheese factory exploded. Des Brie everywhere.

I have a new camera. A nice Chinese couple gave it to me down by Tower Bridge. I couldn't understand what they were saying but they stood together and smiled as I walked away.

EUR Direction Depends On Paris Winner

The dollar has been on the back foot for most of this week on fading hopes that the new Trump administration will not be able to push through fiscal stimulus any time soon.

After the Republicans' failure to repeal the Affordable Care Act last month, investors have been paring their dollar 'reflation' positions, believing that Trump will not be able to deliver on his election promises of tax cuts and infrastructure spend any time soon.

Not helping the dollar bulls is U.S data, it's been perceived as being soft of late – in March, CPI posted its first monthly decline in seven-years, while non-farm payrolls (NFP) also fell short of expectations.

Market focus is firmly on this Sunday's first round of the French election. It's expected to be a two-horse race with Macron handily beating Le Pen in the run-off in a fortnight's time.

1. Stocks get support from Mnuchin comments

In Japan, indices rallied to a two-week high overnight as investors bet that U.S tax reforms are finally gaining traction. U.S Treasury Secretary Mnuchin said the Trump administration will 'very soon' unveil a tax reform plan and expects Congress to approve it this year. The Nikkei 225 gained +1.0% – for the week, it gained +1.6%, posting its first weekly gain in six-weeks, while the broader gained +1.1%.

In Hong Kong, stocks edged lower in thin trading, as investors took to the sidelines ahead of the French presidential election on Sunday. Both the benchmark Hang Seng index and the China Enterprises Index lost -0.1%.

In China, stocks posted their worst week this year as tighter regulatory scrutiny and concerns over the broader economic outlook dampened investors' risk appetite. The blue-chip CSI300 index rose +0.2%, while the Shanghai Composite Index was flat. For the week, the CSI300 was down -0.5%, while the SSEC lost -2.2%.

In Europe, equity indices are trading mixed, but generally lower, as market participants remain cautious after the recent terror attack in Paris. Banking stocks generally higher in the Eurostoxx, while commodity and mining stocks are supporting the FTSE 100.

In the U.S, equities are expected to open in the black (+0.1%).

Indices: Stoxx50 -0.5% at 3,425, FTSE +0.1% at 7,124, DAX flat at 12,025, CAC-40 -0.8% at 5,040, IBEX-35 -0.4% at 10,336, FTSE MIB -0.4% at 19,763, SMI -0.2% at 8,541, S&P 500 Futures +0.1%.

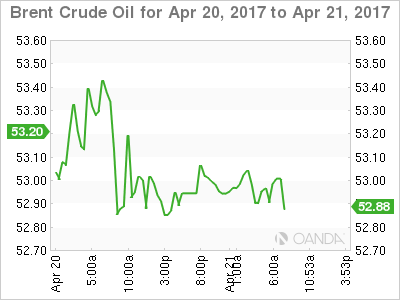

2. Oil dips, on course for biggest weekly drop in a month

Oil prices are lower ahead of the U.S open and are on course for their biggest weekly drop in a month over doubts that an OPEC-led production cut will restore balance to an oversupplied market.

Brent futures are trading at +$52.87 a barrel, down -12c from yesterday's close and are set for a -5.5%+ weekly drop. U.S light crude (WTI) is at +$50.61 a barrel, down -10c and on course for a -5%+ percent weekly decline.

Despite the Saudi's and Kuwait favouring extending their production limiting deal with non-OPEC member producers into H2, the Russian's have declined to say whether they would adhere to an extension before a joint meeting on May 25.

Not helping with the supply issues is U.S data this week showing that their production numbers have jumped by almost +10% in the past 11-months.

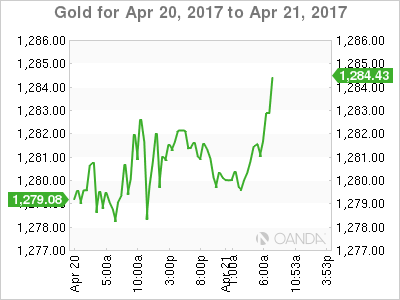

Gold prices are steady (down -0.1% at +$1,280.01 per ounce) with safe-haven demand remaining intact as investors kept an eye on the French presidential vote that is seen as too close to call.

3. ECB to show a steady hand

The ECB meet next week (April 27) and the market expects President Draghi to be playing it safe after the first round of French presidential elections.

The ECB chief is expected to reiterate that the bank is serious about its forward guidance and that policy rates will only go up after the end of its QE program.

Note: Lower French yields imply a more steady-as-she-goes approach to the future.

Heading into Sunday's vote, the yield on 10-year French government debt has hit its weakest level in three-months and the gap between it and its German equivalent has fallen to its tightest in three-weeks.

The yield on U.S 10's has slid -1 bps to +2.23% after a +3 bps advance Thursday. Most other eurozone bond yields are little changed on the day.

4. EUR direction depends on Paris winner

Investors appear to be unwilling to carry too much risk heading into Sunday's Presidential election.

Currently, consensus expects a market-friendly outcome, which should support the EUR (€1.0706) and provide further opportunity to purchase USD/JPY (¥109.14).

Note: The options market continues to see a hefty demand for protection against a sharp EUR move after the vote.

A worst-case scenario for markets would be far-right candidate Le Pen and far-left candidate Melenchon making it to the May 7 vote, but a strong victory for Le Pen would also unsettle markets. Either scenario could see the EUR quickly drop to its 15-year lows atop of €1.0340's. Alternatively, a solid victory for centrist candidate Emmanuel Macron could see it rise to €1.10-1.1200.

The pound (£1.2800) is under pressure from this morning's weak retail sales print (see below).

5. U.K. Retail Sales Drop in March as Inflation Hits Consumers

Data this morning showed that U.K retail sales fell sharply last month, as price increases fuelled by the pound's (£1.2801) sharp post-Brexit vote caused consumers to curb spending.

Sales in March fell by -1.8% m/m, significantly more than the -0.1% fall expected. Compared with March last year, sales rose by +1.7%, again well below expectations.

The U.K's all-important consumer made a negative contribution to the quarterly economic growth for the first time since late 2010 – Sales fell by -1.4% in Q1.

Note: This comes at an awkward time for PM Theresa May, who began divorce proceedings from the E.U in March.

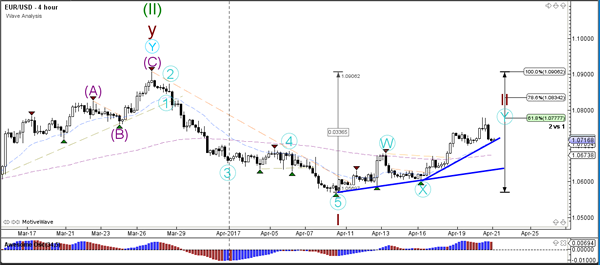

Daily Technical Analysis: EUR/USD Turns Bearish After Hitting 61.8% Fibonacci Target At 1.0775

Currency pair EUR/USD

In yesterday's trading the EUR/USD broke above the 50% Fibonacci retracement level of wave 2 (brown) and continued with a bullish push towards the 61.8% Fib at 1.0775. Price stopped at this Fib level and made a bearish retracement, which is now testing the support trend line (blue) – see 1 hour chart.

The EUR/USD completed a wave 5 (pink) as expected in yesterday's wave analysis. Price is now at the trend line (blue) which is a bounce or break spot. A bearish break could indicate a first signal that a bearish reversal is occurring.

Currency pair EUR/USD

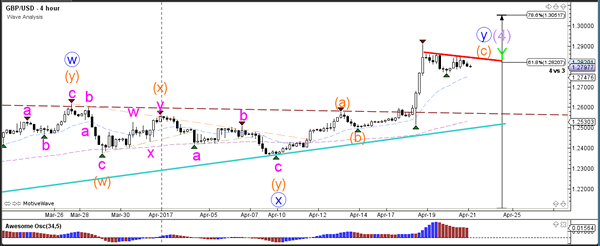

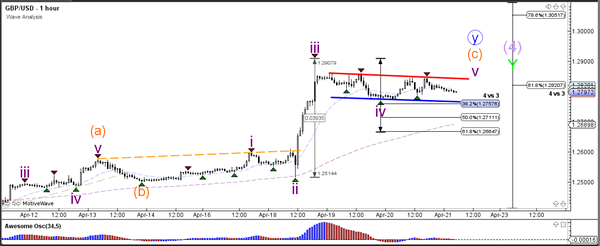

The GBP/USD remains at the 61.8% Fibonacci level of wave 4 (purple). The consolidation zone could indicate a potential reversal or a sideways zone for a new bullish breakout towards the 78.6% Fibonacci level.

The GBP/USD retracement is a bull flag chart pattern which has reached the 38.2% Fibonacci retracement level at 1.2750. A break below the 61.8% Fibonacci level invalidates wave 4 (purple) where a break above the bull flag (red) could see a wave 5 (purple) develop.

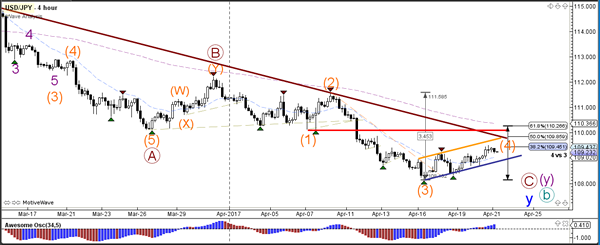

Currency pair USD/JPY

The USD/JPY is building a bear flag chart pattern within a wave 4 correction (orange), which would become invalid if price retraced above the bottom of wave 1 (red line). A break below the bottom of the bull flag (blue) could indicate a bearish breakout and completion of wave 4 (orange).

The USD/JPY is building an ABC (purple) zigzag correction towards the Fibonacci levels of wave 4 (orange).