Sample Category Title

Dollar Recovering against Europeans, Weak Elsewhere

Dollar is recovering against European majors in early US session but stays weak against commodity currencies. The greenbacks is still trading as the weakest major of the week, troubled by comments from US President Donald Trump regarding it's strength. Released from US, initial jobless claims dropped 1k to 234k in the week ended April 8, below expectation of 245k. It's the 110 straight week of sub-300k reading, longest streak since 1970 and indicates a healthy job market. Continuing claims dropped 7k to 2.03m in the week ended April 1. PPI, however, dropped -0.1% mom March but accelerated to 2.3% yoy. PPI core rose 0.0% mom, and accelerated to 1.6% yoy. Both PPI and core PPI missed expectations. From Canada, new housing price index rose 0.4% mom in February. Manufacturing shipments dropped -0.2% mom. Release in European session, Swiss PPI rose 0.1% mom 1.3% yoy in March. German CPI was finalized at 0.2% mom, 1.6% yoy in March.

Markets question whether Trump would still deliver his promises

In an interview with the Wall Street Journal, US President Donald Trump complained that US dollar "is getting too strong, and partially that's my fault because people have confidence in me. But that's hurting - that will hurt ultimately". He added that "it's very, very hard to compete when you have a strong dollar and other countries are devaluing their currency". Meanwhile, Trump also reversed his position and said that China is "not currency manipulators". And he hailed that Chinese President Xi Jinping "wants to help us with North Korea." Trump also showed in the interview his "respect" for Yellen and suggested that he has not decided whether he would reappoint her for the second term.

The comments regarding Dollar was seen as a factor driving the greenback down. However, it remains to be seen if investors' worries are more than that. To be specific, traders could be getting increasingly doubtful on what Trump would and could do. His failure in health act and travel ban raised a lot of questions on his administrative ability. Now that his stance on China has had a U-turn. And that further raises questions on whether he will deliver his election promises.

China exports surged in March

Talking about China, trade surplus came in at USD 23.9b in March, much higher than expectation of USD 12.b. Exports surged 16.4% yoy, much stronger than expectation of 3.2% yoy and much more reversed the lunar new year decline of -1.3% yoy back in February. Imports, on the other hand, rose 20.3% yoy, slowed from February's 38.1% yoy rise. Imports were, nonetheless, also above expectation of 18.0% yoy. Trade surplus with US jumped to USD 17.74b, up from February's 10.42b. Trade surplus with US for first quarter was at USD 49.6b, just slightly down from 2016 Q1's USD 50.57b. In CNY terms trade surplus was at CNY 164b, more than double of expectation of CNY 76b. It remains to be seen what action would US and Chin take after Trump and Xi agreed to a 100-day plan for trades after last week's summit.

Aussie boosted by strong job data

Australia Dollar is boosted by strong employment data today. Employment grew 60.9k in March, triple of expectation of 20.0k. Prior month's figure was revised up from -6.4k to 2.8k. Full time jobs rose by 74.5k, highest jump in nearly 30 years since December 1987. Part-time jobs dropped -13.6k. Participation rate also rose from 64.6% to 64.8%. Unemployment rate was unchanged at 5.9% as more people are back in the market. Also from Australia, consumer inflation expectation rose 4.1% in April.

Adding to the support to Aussie, RBA said in its semiannual Financial Stability Review that " vulnerabilities related to household debt and the housing market more generally have increased." And, "some riskier types of borrowing, such as interest-only lending, remain prevalent." RBA also expressed the concern that "investors are likely to contribute to the amplification of the cycles in borrowing and housing prices, generating additional risks to the future health of the economy." Today's job number certainly removed much burden on RBA for lowering interest rate again, with the background of worries on housing market bubble. Q1 CPI and GDP will be the next key pieces of data to watch.

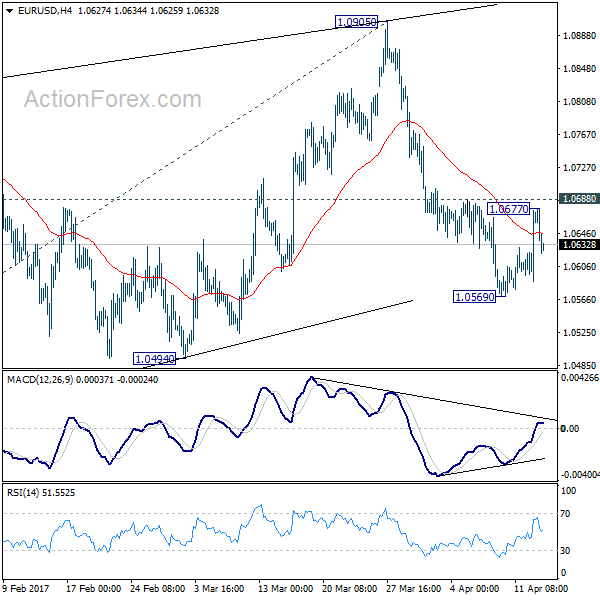

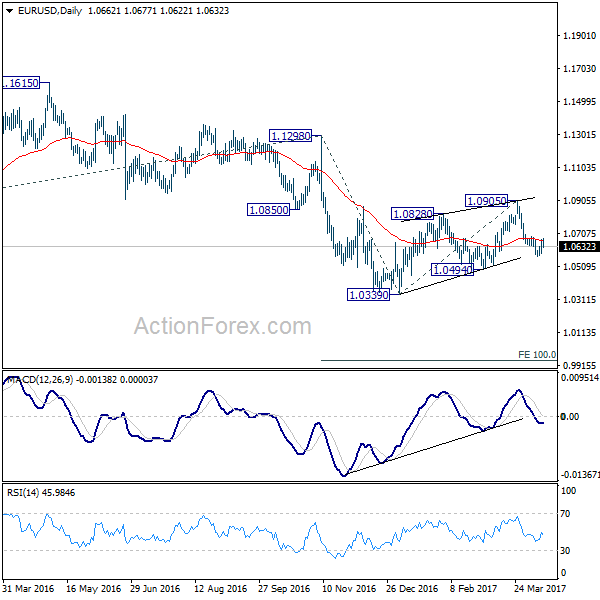

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0611; (P) 1.0642 (R1) 1.0697; More....

EUR/USD recovered to 1.0677 but failed to take out 1.0688 resistance and retreated. Intraday bias remains neutral first. Near term bearish outlook is unchanged. Corrective rise from 1.0339 is likely finished after being rejected by 55 week EMA. And, the larger down trend is ready to resume. Below 1.0569 will turn bias to the downside for 1.0494 support first. Break will confirm this bearish case and send EUR/USD through 1.0339 to 100% projection of 1.1298 to 1.0339 from 1.0905 at 0.9946. On the upside, however, break of 1.0688 resistance will delay the bearish case and turn focus back to 1.0905 resistance instead.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Mar | 4.30% | 4.20% | 4.20% | |

| 01:00 | AUD | Consumer Inflation Expectation Apr | 4.10% | 4.00% | ||

| 01:30 | AUD | RBA Financial Stability Review | ||||

| 01:30 | AUD | Employment Change Mar | 60.9k | 20.0k | -6.4k | 2.8k |

| 01:30 | AUD | Unemployment Rate Mar | 5.90% | 5.90% | 5.90% | |

| 03:15 | CNY | Trade Balance (USD) Mar | 23.9B | 12.5B | -9.1B | |

| 03:15 | CNY | Trade Balance (CNY) Mar | 164B | 76B | -60B | |

| 06:00 | EUR | German CPI M/M Mar F | 0.20% | 0.20% | 0.20% | |

| 06:00 | EUR | German CPI Y/Y Mar F | 1.60% | 1.60% | 1.60% | |

| 07:15 | CHF | Producer & Import Prices M/M Mar | 0.10% | 0.10% | -0.20% | |

| 07:15 | CHF | Producer & Import Prices Y/Y Mar | 1.30% | 0.90% | 1.30% | |

| 12:30 | CAD | New Housing Price Index M/M Feb | 0.40% | 0.20% | 0.10% | |

| 12:30 | CAD | Manufacturing Shipments M/M Feb | -0.20% | -0.70% | 0.60% | |

| 12:30 | USD | PPI M/M Mar | -0.10% | 0.00% | 0.30% | |

| 12:30 | USD | PPI Y/Y Mar | 2.30% | 2.40% | 2.20% | |

| 12:30 | USD | PPI Core M/M Mar | 0.00% | 0.20% | 0.30% | |

| 12:30 | USD | PPI Core Y/Y Mar | 1.60% | 1.80% | 1.50% | |

| 12:30 | USD | Initial Jobless Claims (APR 08) | 234K | 245k | 234k | 235K |

| 14:00 | USD | U. of Michigan Confidence Apr P | 96.6 | 96.9 | ||

| 14:30 | USD | Natural Gas Storage | 2B |

WTI Trades at Mid-Term Major Resistance Zone

The US EIA crude oil inventories figure (the week ending April 7) released on Wednesday, saw the biggest drop in 2.166 million barrels this year.

However, the figure failed to push oil prices higher. WTI and Brent crude oil spot retraced around 1%, and 1.13% respectively on Wednesday.

The reasons for the fall comprise both technical and fundamental factors.

Technically oil prices were trading at the mid-term major resistance zone, where the selling pressure is heavy.

Fundamentally, markets concern whether OPEC will extend the output cut agreement in the May meeting. In addition, the oil supply has been continuously increasing from the thriving US shale industry and some other non-OPEC oil producers.

The price range between 53.00 - 55.00 is the mid-term major resistance zone for WTI spot, where the pressure is heavy.

On the 4-hourly chart, WTI spot broke the downside uptrend line support on Wednesday, indicating the bullish momentum is likely to be restrained at this zone.

The daily Stochastic Oscillator reading is above 80, suggesting a retracement.

The resistance level is at 53.50, followed by 54.00 and 54.50.

The support line is at 53.20, followed by 53.00 and 52.50.

GOLD: Strengthens, Retains Bullishness Offensive

GOLD: The commodity strengthened further on Wednesday leaving risk of more gains on the cards. On the downside, support comes in at the 1,280.00 level where a break will turn attention to the 1,270.00 level. Further down, a cut through here will open the door for a move lower towards the 1,260.00 level. Below here if seen could trigger further downside pressure targeting the 1,250.00 level. Conversely, resistance resides at the 1,290.00 level where a break will aim at the 1,300.00 level. A turn above there will expose the 1,310.00 level. Further out, resistance stands at the 1,320.00 level. All in all, GOLD looks to strengthen further.

Trump U-turns & Dollar Weakness Fails to Support Rand and Lira

The recent escalation of geopolitical risks dominating the financial market headlines has been briefly removed from investors' radars after US President Donald Trump once again took the markets by surprise. This time, President Trump made U-turns on several of his previous public views, making investors wonder whether he could be gradually abandoning some of his core election pledges. While it is not a surprise at all to hear the US President make downbeat comments over the Dollar, backing away from labelling China as a currency manipulator and seemingly supporting the need for lower US interest rates is a real surprise.

Trump reversing away from a previously well-documented aggressive stance on China will go a long way to improving his image in mainland China; it will also be seen by many other observers as an attempt towards improving diplomatic ties, following Chinese President Xi Jinping's recent visit to the United States. Away from diplomacy, this shift in tone should be viewed as a positive development for the financial markets, as it reduces the risk of China abandoning its US Treasury Holdings as a result of the previous risk of President Trump beginning a trade war with China.

Most emerging market currencies across Asia have welcomed the latest comments from the US President, with the majority of currencies across the Asian Pacific moving somewhat higher against the Dollar. Emerging market currencies that are particularly sensitive to speculation around US interest rate rises, such as in Malaysia, Indonesia and perhaps the Indian Rupee, will also applaud comments around the need for lower US interest rates. It has been noted that the Bond markets have benefitted from Trump's unexpected comment that he "likes" the Federal Reserve's low-interest rate policy.

However, the potential for further gains in the Asian emerging market currency space will be attributed to expectations of the Fed pulling the trigger on an interest rate rise once again in June drifting lower and also whether Trump next chooses to take a softer stance on protectionist policies.

While emerging market currencies across Asia have benefitted from Trump's comments, it has not helped to find a bid for either the South African Rand or Turkish Lira. Both currencies are plagued by political risk, with the upcoming referendum in Turkey this weekend giving possible cause for a major event risk over the Easter weekend. The Turkish Lira and South African Rand are obviously not correlated in any way, but with both currencies being plagued by political issues, this is impacting investor confidence and weakening economics that includes impending inflation risks. Inflation risks are going to be a major headline attraction for the Rand over the next couple of months, following the currency being squashed to pieces in recent weeks.

Gold eyes $1300

The 2017 revival in the value of Gold is showing no signs of slipping, after the precious metal climbed to fresh levels not seen since the US Election, getting marginally close to $1290 earlier in trading on Thursday. These are still uncertain times in the financial markets and some would even add global politics, meaning investors are keeping Gold as a close ally when it comes to hedging. The combination of uncertainty when it comes to political risks, the upcoming elections in France, rising geopolitical tensions and doubts over Trump's ability to follow through with his campaign promises presents an ongoing threat to investors entering a period of "risk-off" that is too difficult to ignore when it comes to being encouraged towards Gold.

Sterling backs away from attempt for 1.26

After benefiting from the unwinding of USD positions, it appears that the GBPUSD is at threat of shying away from an attempt to reach 1.26 before the markets close for the Easter holidays. If you ask me, the ongoing uncertainty over Brexit's direction is still enough motivation to maintain a negative mindset towards the Pound. Investors are likely to continue utilising sell-on rally opportunities in the Cable, when the pair climbs near 1.25 with this being the mindset traders have exploited for months.

Daily Technical Analysis: USD/CAD ABCD Pattern Marks The Support

The rate cut wasn't on the table yesterday as economic data in Canada has improved. Slightly hawkish stance of BOC's chief Poloc reflected on the USD/CAD, sending the dollar down straight to W L5 support. At this point, we see an ABCD pattern at D L3 support, so the break of 1.3250 could spur a correction towards 1.3300 where we see a bearish POC (ATR top, EMA89, bearish order block, W L4) within 1.3300-1.3320. Rejections from POC target 1.3220 and 1.3190.

Keep in mind that if 1.3250 is not broken to the upside, we might see a straight drop below 1.3218 for 1.3190 and 1.3145 final D L5 target.

D L3 - Daily Camarilla Pivot (Daily Interim Support)

D H3 - Daily Camarilla Pivot (Daily Interim Resistance)

D H4 - Daily Camarilla Pivot (Strong Daily Resistance)

D L4 - Daily Camarilla Pivot (Very Strong Daily Support)

D L5 - Daily Camarilla Pivot (Strongest Daily Support)

W L5 - Weekly H4 Camarilla (Strongest Weekly Resistance)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

CAC Dips On Trump Dollar Statement, Geopolitical Jitters

The CAC 40 has dropped below the 5100 level, as the index is trading at 5,073.00 in Thursday trade. On the release front, France and Germany both released consumer inflation data. German Final CPI dropped to 0.2%, matching the forecast. French Final CPI took the opposite direction, improving to 0.6%, matching the forecast. On Wednesday, President Donald Trump said in a newspaper interview that the value of the US dollar was too strong and that he was in favor of a low interest rate policy. Trump's comment has sent the greenback lower and is weighing on European stock markets.

European stock markets, including the CAC, are under pressure, as investors remain jittery about rising tensions in Syria and North Korea. The US bombed a Syrian military base last week, in response to a chemical attack by Syrian warplanes. Russia has strongly condemned the US move, chilling relations even further between the US and Russia. President Trump has declared that he has sent “an armada” to the Korean peninsula in response to North Korea firing ballistic missiles, and the escalation in rhetoric between North Korea and the US is weighing on the stock markets.

The hotly contested French presidential election, with the first round on April 23, is sure to have a strong impact on the stock market as we get closer to voting day. The current frontrunners are centrist Emmanuel Macron and far-right leader Marine Le Pen, but the race remains tight and unpredictable. Le Pen has been an outspoken critic of the eurozone and wants to hold a referendum on France's membership in the EU. She is expected to advance to the second round, and Le Pen's success could dampen confidence in the euro and the stock market.

Earlier this week, Federal Reserve Chair Janet Yellen provided some insights into the central bank's plans in 2017. Yellen said that with the economy close to full employment and 2 percent inflation, the Fed was in a better position to reduce its support for the US economy. The minutes of the March meeting indicated that the Fed plans to trim the $4.5 trillion balance sheet, which has ballooned as a result of the huge asset-purchase program which started in response to the financial crisis in 2008. Yellen emphasized that the Fed's policy stance is neutral, as interest rate increases will be gradual, given that the economy is growing at a moderate pace. The Fed is widely expected to raise rates twice more in 2017, with the next rate expected in June. At the same time, some Fed policymakers have come out in favor of three more rate hikes, which would bring the total this year to four moves.

Trump The ‘Manipulator’

Thursday April 13: Five things the markets are talking about

Capital markets were heading into an Easter holiday stupor before President Trump 'intentionally' shook things up in a press conference late Wednesday afternoon.

Trump said that a strong U.S dollar would ultimately hurt their economy and that he prefers a low interest rate policy. The President also reversed his position on China, saying he will not label the Asian nation a currency 'manipulator.” In another reversal, he said he likes and respects Fed Chair Yellen, and that it's too soon to comment on whether he might re-nominate her at the end of her term in 2018.

The dollar has since plunged on his jawboning; gold has rallied to five-month highs, while U.S treasury yields have fallen to five-month lows.

Note: Most financial markets are closed on Friday for the Good Friday holiday, and today's trading volumes are expected to be much lighter than usual.

1. Global stocks see mixed results

In Japan, equities crashed to new four-month low overnight as the yen (¥108.76) spiked to new yearly highs on Trump's currency jawboning. The Nikkei 225 share average ended -0.7% lower, while the broader Topix fell -0.8%, paring an earlier drop of -1.4%.

Note: The Topix has the second-worst performance among developed markets this year, with a loss of -3.3%.

Down-under, Sydney's S&P/ASX 200 dropped -0.7%, falling for the first time in five days as commodity producers led declines. In Singapore, the Straits Times Index lost -0.7%, while in Hong Kong, the Hang Seng fell -0.3%, after earlier rising +0.3%.

In China, stocks inched higher as investors continued to bet on stocks that could benefit from Beijing's plan to build a vast new economic zone, though gains were capped by fears that policy tightening will crimp economic growth. The blue-chip CSI300 index rose +0.2%, while the Shanghai Composite Index added +0.1%.

In Europe, equity indices are trading lower ahead of the long Easter weekend amid ongoing geopolitical tensions. Banking stocks are leading the losses in the Eurostoxx, while energy stocks are trading lower in the FTSE 100.

U.S stocks are set to open in the red (-0.1%).

Indices: Stoxx50 -0.6% at 3,451, FTSE -0.5% at 7,312, DAX -0.3% at 12,113, CAC-40 -0.5% at 5,076, IBEX-35 -0.6% at 10,303, FTSE MIB -0.9% at 19,832, SMI -0.4% at 8,631, S&P 500 Futures -0.1%

2. Oil little changed amid rising U.S. output, Gold higher

Crude oil futures are largely unchanged overnight, with the market torn between rising U.S production and the output cuts being made by OPEC.

Brent crude futures are flat at +$55.86 a barrel, U.S West Texas Intermediate (WTI) crude futures are down -6c at +$53.05 a barrel.

Yesterday's weekly inventory report had something for everyone. Preliminary U.S production estimates in the EIA report suggested that domestic output is still climbing – stockpiles at Cushing, Oklahoma, rose +276k barrels in the week ended April 7.

Nevertheless, the headline print showed an unexpected drop in overall U.S inventories, which fell last week by -2.2m barrels as imports declined by -717k barrels a day.

Note: The IEA Monthly Report noted that the oil market was already very close to balance. They have trimmed 2017 global oil demand growth from +1.4m bpd to +1.32m bpd and raised non-OPEC oil supply growth forecast from +400k bpd to +485k bpd, while OPEC member production declined from +32.0m to +31.68m, compliance of +99% vs. +91% m/m.

Gold (+0.2% to +$1,287.98) has rallied to a five-month peak overnight amid rising tensions over U.S relations with Russia and North Korea. Prices are also being supported by the 'big” dollars slide.

The 'bulls” are eyeing the psychological +$1,300 handle now that the market has penetrated the previous strong resistance point above +$1,280.

3. Global yields fall on Trump rhetoric

Yields on high-rated Eurozone government bonds have fallen to multi-month lows ahead of the U.S open after Trump said he would prefer the Fed to keep interest rates low.

Tracking U.S Treasuries lower, investors have piled into German, Dutch and Finnish debt.

This morning, the German 10-year Bund yield hit its lowest level since early January at +0.181%, down -2 bps. Both Dutch and Finnish debt gave up -2 and -3 bps respectively.

Trump's comments cast doubt on the future pace of Fed rate hikes, and the benchmark U.S Treasury yield dropped a further -5 bps to +2.22%, its lowest level in almost five-months.

Geopolitical and French Presidential election risks have seen the yield on 10-year Bunds fall over -30 bps from its mid-March peak of +0.51% and U.S 10's move from +2.60% to +2.22%.

Note: The gap between French and German 10-year borrowing costs, an indicator of concerns over the election, is at +71.4 bps, +4 points off one-month highs hit earlier this week.

4. The 'Big” dollar takes a dive

President Trump's interview yesterday now sows doubts about the Fed's determination to ‘normalise' its monetary policy sufficiently quickly. This is bad news for the dollar.

Trumps jawboning saw the dollar print fresh lows across the board yesterday and in the overnight session the USD has managed to retrace a small fraction of its losses.

USD/JPY hit a five-month lows in Asia at ¥108.71 and now trades atop its softest level since Trump won the U.S election in Nov. Uncertainty before the French presidential elections is also causing the EUR to give up some of its gains, last down -0.1% at €1.0655.

The Chinese Yuan (CNH) is firmer now that Trump seems to have backed off from his campaign pledge to label China a currency manipulator. The People's Bank of China (PBoC) has guided the yuan (¥6.8651 a +0.4%) to its biggest one-day advance against the dollar in nearly three-months.

Commodity currencies are firmer as well, aided by the weak USD and geo-political concerns. The CAD (C$1.3244) hit a 6-week high after the BoC turned less dovish at its rate decision yesterday.The AUD (A$0.7578) is being supported by stronger jobs data (see below).

5. China trade rebounds, Aussie employment surges

Data overnight showed that China's Trade Balance rebounded to a surplus after last month's surprise deficit.

Exports (in CNY terms) were well above consensus at +22.3% vs. +8.0%e. Imports also beat at +26.3% vs. +15.0%e, and even Crude Oil prices saw an uncharacteristic bounce on China trade with a +20c rise as Mar. imports of +9.24m bpd registered a record high.

China Customs noted that trade is improving as global demand recovers, but also warned that import growth may slow in Q2.

Note: The PBoC has resumed its open market operations after a two-week pause with a ¥110B injection.

In Australia, their employment data also reversed last month's negative surprise. Despite the unemployment rate remaining at +5.9%, net jobs gains recorded a 16-month high at +60.9K vs. +20.3Ke. The participation rate also rose to an eight-month high of +64.8% vs. +64.6%e.

British Pound Rises after Trump’s Comments

British Pound Rises after Trump's Comments

- Sterling rises after Trump's comments

- Bank of Canada holds rates at 0.50%

- UK markets closed over the Easter Break

The US Dollar tumbled broadly and is now trading as the weakest major currency after US President, Donald Trump, talked down the exchange rate.

In an interview with the Wall Street Journal, US President, Donald Trump, complained that the US Dollar is getting too strong and that ultimately that will hurt. On interest rates, Trump affirmed his preference over a low interest rate policy - this has seen the Pound rise to above 1.25 against the US Dollar, and the commodity currencies are broadly higher.

The Bank of Canada appeared confident over the economic growth outlook, although it maintained the policy rate unchanged at 0.50% yesterday. The central bank upgraded the Gross Domestic Product (GDP) growth forecast for this year amidst strong housing market activities in the first quarter.

In Australia, the Australian Dollar has been boosted by strong employment data today. Employment grew 60.9k in March; triple the expectation of 20k.

Today, there is a raft of inflation and Producer Price Index (PPI) data from Europe, as well US employment figures, which will be released this afternoon.

The UK markets are closed over the Easter break, but the global markets will continue to move over the weekend - please contact your Halo Financial currency consultant to discuss strategies over the holiday period.

Happy Easter everyone.

Easter jokes

How do bunnies stay healthy?

Eggsercise

How can you find the Easter bunny?

Eggs (x) marks the spot

What is the end of Easter?

The letter R

Market Update – European Session: IEA Confident That Oil Market Very Close To Balanced

Notes/Observations

FX in focus as Trump cautions about a too strong USD and withdrew a threat to declare China a currency manipulator

Mar Final CPI readings for France and Germany unrevised and move off multi-year highs

IEA confident that oil market already moving very close to balance

Overnight:

Asia:

China Mar Trade Balance moved back to surplus (+$23.9B v +$12.5Be) as exports surge to a 2-year high (Reminder: Feb Trade Balance registered its 1st deficit since Feb 2014)

Australia Mar Employment change hits a 16-month high (+60.9K v +20.0Ke; Unemployment Rate in-line at 5.9%

(KR) Bank of Korea (BOK) leaves 7-Day Rep Rate unchanged at 1.25% (as expected) for its9th straight pause in the current easing cycle, Monetary policy to remain accomodative but rate cut less necessary than before

US govt and other officials warned that North Korea reportedly placed a nuclear device in a tunnel and it may be detonated this Saturday Apr 15th

Europe:

French presidential race tightens further, markets nervious

Germany's Schaeuble says we need a pro-EU France, hopes Le Pen loses

Americas:

President Trump: US dollar is getting too strong; Will not label China a currency manipulator

Brazil Central Bank (BCB) cut Selic Target Rate by 100bps to 11.25% for its 5th straight cut.

Economic Data

(DE) Germany Final CPI M/M: 0.2% v 0.2%e; Y/Y: 1.6% v 1.6%e

(DE) Germany Final CPI EU Harmonized M/M: 0.1% v 0.1%e; Y/Y: 1.5% v 1.5%e

(FI) Finland Mar CPI M/M: 0.0% v 0.5% prior; Y/Y: 0.8% v 1.2% prior

(FR) France Mar Final CPI M/M: 0.6% v 0.6%e; Y/Y: 1.5% v 1.5%e

(FR) France Mar Final CPI EU Harmonized M/M: 0.7% v 0.7%e; Y/Y: 1.5% v 1.5%e

(CH) Swiss Mar Producer & Import Prices M/M: 0.1% v 0.1%e; Y/Y: 1.3% v 0.9%e

(CN) China Mar Foreign Direct Investment (FDI): +6.7% y/y

(IT) Italy Mar Final CPI (Including Tobacco) M/M: 0.0% v 0.0% prelim; Y/Y: 1.4% v 1.4% prelim

Fixed Income Issuance:

(IN) India sold total INR147.8B vs. INR180B indicated in 2022, 2026, 2034 and 2046 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Index snapshot (as of 10:00 GMT)

Indices [Stoxx50 -0.6% at 3,451, FTSE -0.5% at 7,312, DAX -0.3% at 12,113, CAC-40 -0.5% at 5,076, IBEX-35 -0.6% at 10,303, FTSE MIB -0.9% at 19,832, SMI -0.4% at 8,631, S&P 500 Futures -0.1%]

Market Focal Points/Key Themes: European equity indices are trading lower ahead of the long Easter weekend amid ongoing geopolitical tensions; Banking stocks trading sharply lower with shares of SocGen, Santander, and BNP Paribas leading losses seen in the Eurostoxx; shares of Standard Life, RBS, Standard Chartered and HSBC trading weighing in the FTSE 100; heavily weighted peripheral lender FTSE MIB index underperforming as a result; energy stocks trading lower as oil consolidates around yesterday's lows.

Upcoming scheduled US earnings (pre-market) include Apogee Enterprises, Carrefour, Commerce Bankshares, First Horizon National, First Republic Bank, JPMorgan Chase, PNC Financial Services, Wells Fargo, and Yingli Green Energy.

Equities (as of 09:50 GMT)

Consumer Discretionary: [Carrefour CA.FR -0.5% (Q1 sales), Gattaca GATC.UK -10.1% (trading update), Hays HAS.UK -0.7% (Q3 fees), Sodexo Alliance SW.FR +0.3% (H1 results)]

Industrials: [Bauer B5A.DE +3.6% (FY16 results), Scapa SCPA.UK +8.2% (trading update)]

Speakers

BOE Credit Conditions & Bank Liabilities Surveys noted that Lenders saw corporate demand was subdued in Q1as the pace of business lending had eased in recent months. Demand has been higher than expected since the Brexit

Greece govt official: Possible extra Eurogroup meeting in May is possible

Russia Central Bank Dep Gov Yudayeva reiterated view that taking measures to ensure that inflation stayed near the 4% target in both 2018-19 period

Russia Central Bank's Polonsky saw room for cautious rate cuts and reiterates Board view that monetary policy to remain moderately tight

Japan Chief Cabinet Sec Suga reiterated financial stability was important and that would pay close attention to market moves. Markets were aware of geopolitical risks but that the US and global economy remained on firm footing. Would not comment on any specific FX levels

IEA Monthly Report noted that it could be argued confidently that oil market was already very close to balance. Trimmed 2017 global oil demand growth from 1.4M bpd to 1.32M bpd. It raised 2017 Non-Opec oil supply growth forecast from 400K bpd to 485K bpd while Opec production declined from 32.0M to 31.68M, -365K bpd; compliance of 99% v 91% m/m

Currencies

FX markets in the session saw the USD retrace a small fraction of Wed losses after President Trump express concern of a too strong greenback.

USD/JPY hit 5-month lows in Asia at 108.71 which corresponded to the 200-day moving average. The pair at its softest level since Trump won the US election back in early Nov. - The Chinese Yuan currency was firmer after Trump backed off from his campaign pledge to label China a currency manipulator

Commodity currencies were firmer as well – aided by the weak USD and geo-political concerns. The CAD currency (Loonie) hit a 6-week high after the Bank of Canada turned less dovish at rate decision on Wed.

Fixed Income

Bund futures trade at 163.66 up 42 ticks marking fresh contract highs, with Trump overnight comments and potential weekend risk including the Turkish referendum, and the French election vote helping keep futures bid. Futures traded a high of 163.77, with a break back above targeting 163.99 followed by 164.20. A reversal continues to target 163.39 former high followed by 163.18.

Gilt futures trade at 128.73 up 22 ticks trading higher with Bunds, with the overall trend higher remaining in tact. Support moves to 128.16 followed by 127.94 then 127.34. A move above 128.80 high targets 128.96 then 129.29. Short Sterling curve continue to flatten with Jun17Jun18 moving lower to 8.5/9bp, a recent new low.

Thursday's liquidity report showed Wednesday's excess liquidity rose to €1.596T a rose of €3B from €1.593T prior. Use of the marginal lending facility rose to €271M from €265M prior.

Corporate issuance saw $1B come to market via a sole issuer. Daiwa Securities $1B 5 year notes brought weekly issuance to $11.3B, slightly ahead of estimates.

Looking Ahead

(GR) Eurogroup chief Dijsselbloem and German Fin Min Schaeuble to meet on Greece

05:30 (ZA) South Africa Feb Total Mining Production M/M: No est v 1.7% prior; Y/Y: 1.4%e v 1.3% prior

05:30 (HU) Hungary Debt Agency (AKK) to sell Bonds

06:00 (IE) Ireland Mar CPI M/M: No est v 0.6% prior; Y/Y: No est v 0.5% prior

06:00 (IE) Ireland Mar CPI EU Harmonized M/M: No est v 0.5% prior; Y/Y: No est v 0.3% prior

06:00 (UK) DMO to sell combined £B in 1-month, 3-month and 6-month bills (£0.5B, £0.5B and £1.0B respectively)

07:00 (UR) Ukraine Central Bank Interest Rate Decision: Expected to leave Key Rate unchanged at 14.00%

08:00 (PL) Poland Feb Current Account: €0.0Be v €2.5B prior; Trade Balance: €0.Be v €0.2B prior; Exports: €15.3Be v €15.0B prior; Imports: €15.3Be v €14.8B prior

08:00 (BR) Brazil Feb IBGE Services Sector Volume Y/Y: No est v -7.3% prior

08:15 (UK) Baltic Dry Bulk Index

08:30 (US) Mar PPI Final Demand M/M: 0.0%e v 0.3% prior; Y/Y: 2.4%e v 2.2% prior

08:30 (US) Mar PPI Ex Food and Energy M/M: 0.2%e v 0.3% prior; Y/Y: 1.8%e v 1.5% prior

08:30 (US) Mar PPI Ex Food, Energy Trade M/M: 0.2%e v 0.3% prior; Y/Y: No est v 1.8% prior

08:30 (US) Initial Jobless Claims: 245Ke v 234K prior; Continuing Claims: 2.02Me v 2.028M prior

08:30 (US) Weekly USDA Net Export Sales

08:30 (CA) Canada Feb New Housing Price Index M/M: 0.2%e v 0.1% prior; Y/Y: 3.1%e v 3.1% prior

08:30 (CA) Canada Feb Manufacturing Sales M/M: -0.7%e v +0.6% prior

09:00 (RU) Russia Gold and Forex Reserve w/e Apr 7th: No est v $397.9B prior

10:00 (US) Apr Preliminary University of Michigan Confidence: 96.5e v 96.9 prior

10:30 (US) Weekly EIA Natural Gas Inventories

11:00 (BR) Brazil to sell Fixed Rate 2023 and 2027 Bonds

11:00 (BR) Brazil to sell 2017, 2019 and 2020 LTN Bills

17:00 (CL) Chile Central Bank (BCCH) Interest Rate Decision: Expected to leave Overnight Target Rate unchanged at 3.00%

DAX Lower As Trump Takes Aim At Dollar

The DAX has posted losses on Thursday, as the index trades at 12,112.00. On the release front, German Final CPI dropped to 0.2%, matching the forecast. French Final CPI took the opposite direction, improving to 0.6%, matching the forecast. On Wednesday, President Donald Trump said in a newspaper interview that the value of the US dollar was too strong and that he was in favor of a low interest rate policy. Trump’s comment has sent the greenback lower and is weighing on European stock markets.

The DAX continues to lose ground in April, as investors remain jittery about rising tensions in Syria and North Korea. The US bombed a Syrian military base last week, in response to a chemical attack by Syrian warplanes. Russia has strongly condemned the US move, chilling relations even further between the US and Russia. President Trump has declared that he has sent “an armada” to the Korean peninsula in response to North Korea firing ballistic missiles, and the escalation in rhetoric between North Korea and the US is weighing on the stock markets.

German numbers have been a mix this week, as investor confidence jumped, while inflation indicators weakened. The ZEW Economic Sentiment report sparked with a reading of 19.5, crushing the estimate of 13.2. This marked the strongest gain since August 2015, pointing to strong optimism among institutional investors and analysts. However, inflation levels have softened in March. The Wholesale Price Index dropped to a flat 0.0%, compared to 0.5% a month earlier. This was well short of the forecast of 0.4%. The downward trend continued with Final CPI, which dropped to 0.2%, down from 0.6% in February. Eurozone CPI made a big splash in February, when it hit the ECB’s target of 2.0%, and raising speculation that the ECB might need to respond by tightening monetary policy. However, the indicator softened in March to 1.5%, short of the forecast of 1.8%. The softer March inflation numbers have certainly eased the pressure on the ECB, which is not scheduled to reduce its asset-purchase program until December.

Earlier this week, Federal Reserve Chair Janet Yellen said that with the economy close to full employment and 2 percent inflation, the Fed was in a better position to reduce its support for the US economy. The minutes of the March meeting indicated that the Fed plans to trim the $4.5 trillion balance sheet, which has ballooned as a result of the huge asset-purchase program which started in response to the financial crisis in 2008. Yellen emphasized that the Fed’s policy stance is neutral, as interest rate increases will be gradual, given that the economy is growing at a moderate pace. The Fed is widely expected to raise rates twice more in 2017, with the next rate expected in June. At the same time, some Fed policymakers are in favor of three more rate hikes, which would bring the total this year to four moves.