Sample Category Title

Trade Idea Update: USD/CHF – Buy at 1.0030

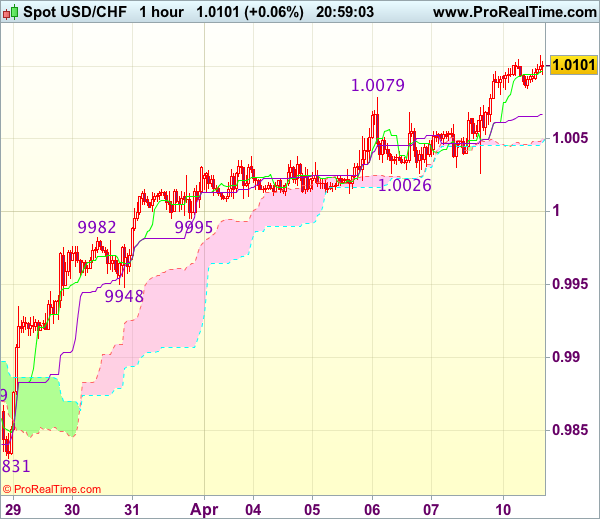

USD/CHF - 1.0094

Original strategy :

Buy at 1.0030, Target: 1.0130, Stop: 0.9995

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0030, Target: 1.0130, Stop: 0.9995

Position : -

Target : -

Stop : -

The greenback has maintained a firm undertone after Friday’s rally, adding credence to our bullish view that recent upmove from 0.9813 is still in progress and upside bias remains for this move to extend further gain to previous resistance at 1.0109, then towards 1.0140-45, however, loss of upward momentum should prevent sharp move beyond another previous resistance at 1.0171, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy dollar on pullback as support at 1.0026 should limit downside. Below minor support at 0.9995 would defer and suggest top is possibly formed, risk correction to 0.9960 but support at 0.9948 should hold from here.

Trade Idea Update: GBP/USD – Sell at 1.2450

GBP/USD - 1.2404

Original strategy :

Sell at 1.2450, Target: 1.2350, Stop: 1.2485

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.2450, Target: 1.2350, Stop: 1.2485

Position : -

Target : -

Stop : -

As the British pound found good support around 1.2365-66 and has recovered, suggesting consolidation above this level would be seen an above the Kijun-Sen (now at 1.2418) would bring recovery towards 1.2450-55 before prospect of another decline, below said support at 1.2365-66 would extend recent decline from 1.2616 to 1.2350, then towards 1.2325-30 but near term oversold condition should limit downside and reckon 1.2300 would hold from here.

In view of this, would not chase this fall here and would be prudent to sell cable on recovery as 1.2450-60 should limit upside. Above the upper Kumo (now at 1.2469) would defer and suggest low is formed instead, risk test of resistance at 1.2506 first, break there would confirm, then a stronger rebound to 1.2525-30 would follow.

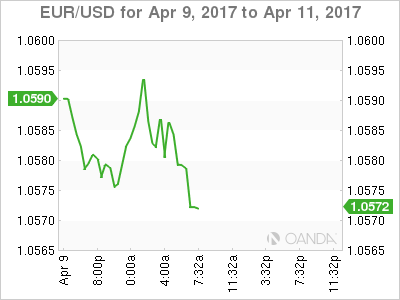

Trade Idea Update: EUR/USD – Sell at 1.0635

EUR/USD - 1.0586

Original strategy :

Sell at 1.0635, Target: 1.0535, Stop: 1.0670

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0635, Target: 1.0535, Stop: 1.0670

Position : -

Target : -

Stop : -

The single currency ran into renewed selling interest at 1.0667 on Friday (after NFP) and has dropped again, the breach o indicated support at 1.0600 adds credence to our bearish view that the decline from 1.0906 is still in progress and may extend further weakness towards 1.0550-55 (50% projection of 1.0906-1.0635 measuring from 1.0689), then 1.0525-30, however, near term oversold condition should prevent sharp fall below 1.0500, risk from there is seen for a rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 1.0635 (previous support now resistance) should limit upside. Only a firm break above said resistance at 1.0667 would abort and suggest low is formed instead, risk a stronger rebound to 1.0689, then 1.0702.

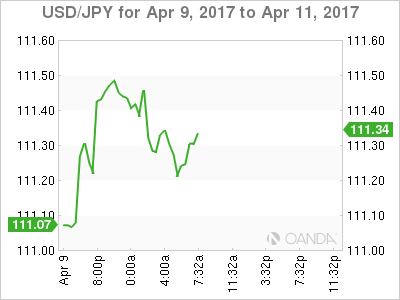

Trade Idea Update: USD/JPY – Buy at 110.90

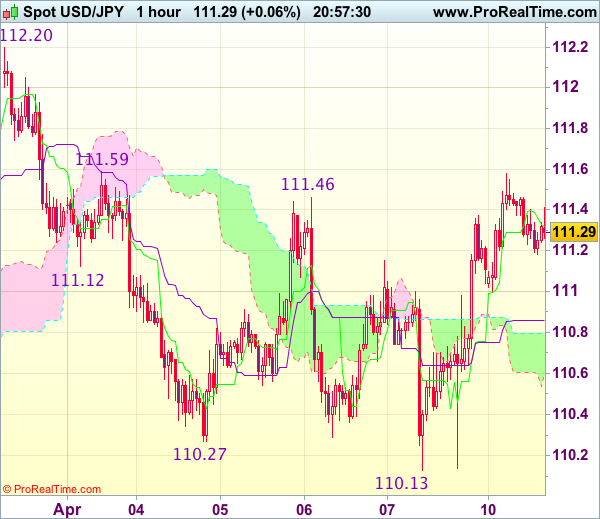

USD/JPY - 111.27

Original strategy :

Buy at 110.90, Target: 111.90, Stop: 110.55

Position : -

Target : -

Stop : -

New strategy :

Buy at 110.90, Target: 111.90, Stop: 110.55

Position : -

Target : -

Stop : -

Although the greenback fell to as low as 110.13 late last week, as dollar has staged a strong rebound after holding above indicated support at 110.11, retaining our view that further consolidation above this level would be seen and mild upside bias is for test of 111.59 resistance, a break there would signal the fall from 112.20 has ended, then a stronger rebound to 111.90-00 would follow but said resistance at 112.20 should hold and choppy trading within 110.11-112.20 would continue.

In view of this, we are looking to buy dollar on dips but one should exit on such rebound. Below the lower Kumo (now at 110.60) would signal an intra-day top is formed instead, risk weakness to 110.40 but only break of said support at 110.11-13 would confirm medium term decline has resumed for further subsequent fall to 109.80-85 (1.618 times projection of 112.20-111.12 measuring from 111.59) but price should hold above 109.50-55 (100% projection of 112.20-110.27 measuring from 111.46).

Geopolitical Risks Leave Markets on Edge

Global stocks were mixed during trading on Monday, with participants adopting a defensive stance after the heightened geopolitical risks weighed heavily on sentiment. Asian shares simply struggled for direction amid the cautious trading mood and the noticeable anxiety has limited gains in Europe. With the lingering sense of caution creating a lacklustre trading atmosphere, Wall Street may struggle to find the momentum needed to venture higher this afternoon. Stock markets could come under renewed selling pressure, as geopolitical risks are compounded with the messy mixture of political uncertainty, Brexit woes and Trump developments.

Dollar Index breaks above 101.00

The Dollar Index breached above the 101.00 resistance level on Friday, after markets received March's mixed US jobs report positively. Although the dismal NFP figure of 98k initially sparked some jitters, this was swiftly countered by the unexpected decline in unemployment rates that dropped to their lowest levels in almost 10 years at 4.5%. The upside seen in the Dollar was complimented by hawkish comments from the Fed's Dudley, which bolstered speculation of more rate hikes this year. Whilst the geopolitical risks and renewed expectations of further rate hikes may support the Dollar bulls, the ongoing concerns over Trump's ability to move forward with tax reforms could create some headwinds and limit gains down the line.

Sterling slides below 1.2400

Sterling was exposed to steep losses last week, following the unexpected drop in the British manufacturing output which reignited concerns over the health of the UK economy as it prepares to depart from the EU. A resurgent Dollar from the mixed NFP report fuelled the downside and provided a foundation for bears to drag prices below the 1.2400 level. With the bias towards Sterling firmly bearish amid the ongoing Brexit uncertainty, further downside may be expected with any technical bounces seen an opportunity for sellers to attack prices lower. From a technical standpoint, bears need a solid daily close below 1.2370 which could open a path lower towards 1.2300.

Currency spotlight - EURUSD

The growing uncertainty ahead of the upcoming French presidential elections has haunted investor attraction towards the Euro. Markets are still weighing the possibility of Eurosceptic Marine Le Pen winning the elections and the jitters have translated to downside further shocks for the Euro. With the Dollar back in fashion amid the speculations of higher US rates, the EURUSD remains under intense selling pressure. From a technical viewpoint, the EURUSD fulfils the prerequisites of a bearish trend on the daily charts as there have been consistently lower highs and lower lows. The solid breakdown below 1.0600 could encourage a further decline back towards 1.0500.

Commodity spotlight - Gold

The explosive combination of Dollar strength and risk aversion left Gold chaotic on Friday, with prices eventually concluding the week below $1260. While the metal remains supported in the medium to longer-term amid the geopolitical tensions and political risks across the globe, the renewed rate hike expectations could enforce downside pressures in the short term. Gold's trajectory on the daily charts remains tilted to the upside, with bulls in firm control above the $1240 higher low. From a technical standpoint, a solid daily close above $1260 is needed for any further upside. In an alternative scenario, a breakdown below $1240 may open a path back towards the $1225 support.

AUD/USD Trades at Short-Term Major Support Zone

AUD/USD has turned bearish since the end of March, seeing 6 bearish sessions out of the 7 trading sessions, marking the worst weekly performance this year.

The slump was caused by the strengthening of USD and the fall in iron ore prices.

The current trend remains bearish. On the 4-hourly chart, the price still trades below the 10 and 20 SMAs.

This morning during early European session, AUD/USD hit a 12-week low of 0.7475, the significant support level at 0.7500 was broken.

The range between 0.7475 - 0.7500 is the short-term major support zone.

The bulls are attempting to recover the level at 0.7500. If the bulls are unsuccessful in breaching 0.7500 and holding above the support line at 0.7475, the likelihood will be that the downtrend will continue, and the bears will test the next significant support line at 0.7450.

Conversely, if the bulls are successful in holding the downtrend, we will likely see a rebound here.

Both the daily and 4-hourly Stochastic Oscillator readings are below 20, suggesting a rebound.

The resistance level is at 0.7500, followed by 0.7520 and 0.7535.

The support line is at 0.7475, followed by 0.7450 and 0.7430.

Keep an eye on the Fed Chair Yellen's speech at 21:10 BST this evening, as it will likely affect the strength of USD and the trend of AUD/USD.

DAX Edges Lower To Start off Week, German Investor Confidence Next

The DAX Index has edged lower in Monday trading. Currently, the DAX is trading at 12,208.69. In economic news, Eurozone Sentix Investor Confidence jumped to 23.9, beating the estimate of 20.1 points. On Tuesday, Germany releases ZEW Economic Sentiment, a key indicator which should be treated as a market-mover.

The eurozone economy has shown stronger growth in the first quarter, and this has been reflected in the DAX ,which has recorded gains of 4.8 percent during this time. Germany has led the way, with strong manufacturing and services numbers. With economic conditions improving, investor confidence levels have followed suit and posted strong numbers in Q1. Eurozone Sentix Investor Confidence climbed to 23.9 points in April, pointing to strong optimism among investors and analysts. On Tuesday, Germany releases ZEW Economic Sentiment, which surveys the mood of German investors. The markets are expecting a strong reading for April, with the indicator expected to climb to 13.2 points, up from 12.8 points in March.

The US labor market remains very tight, but there was surprising news on Friday, as Nonfarm Payrolls was a big disappointment. The economy produced just 98 thousand jobs in March, way off the forecast of 174 thousand. However, the DAX shrugged off the weak numbers. The good news is that the weak reading was not accompanied by higher unemployment numbers. The unemployment rate dropped to 4.5% and jobless claims fell sharply to 234 thousand. This means that the soft payrolls report is unlikely to change the Fed's expected course of action of two more hikes in 2017 (a majority of FOMC voting members favor two more hikes, while some members have called for three more hikes this year). According to the CME Group, the markets have circled June as the next likely date for a hike, which is priced in at 67 percent. The Fed would like to see inflation move closer to its target of two percent, and we'll get a look at consumer inflation reports on Friday.

Technical Outlook: Crude Oil Maintains Strong Bullish Stance

US oil maintains strong bullish stance on Monday and holding above Friday's closing level at $52.27, after rally spiked to $52.92, the highest since 08 Mar.

Strong bullish sentiment is supported by bullish daily studies and Friday's close above $51.97 (Fibo 61.8% of $55.01/$47.06 downleg), seeing scope for test of next target at $53.13 (Fibo 76.4% retracement.

Slow stochastic on daily chart turned north and entered again overbought territory after briefly reversing lower, signaling that correction signals are on hold.

Session low at $52.29 marks initial support, ahead of broken Fibo 61.8% at $51.97 and broken daily 55SMA at $51.63.

Res: 52.68; 52.92; 53.13; 53.78

Sup: 52.29; 51.97; 51.63; 51.49

The ‘Mighty’ Dollar Finds Geopolitical Support

Monday April 10: Five things the markets are talking about

Capital markets are showing resilience this morning in the face of last Friday's weaker than expected non-farm payroll report (NFP) and heightened geopolitical tensions, with demand for haven assets fade a tad.

While the U.S jobs report was weaker than some had expected, it's consistent with the U.S. economy growing at +2% this year, the miss is being shrugged off as a one-off due to weather impact.

Nevertheless, geopolitical risk remains a concern in the wake of Syria strikes last week as a U.S destroyer approaches the Korean peninsula.

Last week's meeting between China President Xi and President Trump is being viewed as a success. The world's largest economy has reportedly offered improved market access for U.S financial sector investments and beef exports in a move to avert a trade war.

In Europe, this week features price data from several countries including the U.K, Germany, France and Italy. Given the ECB's focus on its inflation target, this data will be important for the Bank's policy assessment later this month.

Elsewhere, China will release price data along with its merchandise trade numbers, while both Australia and the U.K release their respective jobs report.

In North America, the biggest news is likely to be Friday's U.S retail sales report where no change is expected (+0.2%). On Wednesday, the BoC publishes its monetary policy announcement.

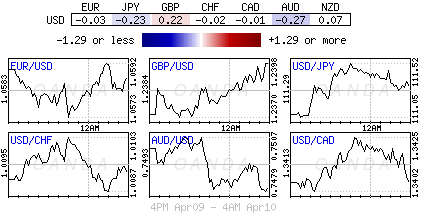

1. Global equities see mixed response to geopolitical tensions

Global stocks are starting this holiday-shortened week stuck in neutral ahead of U.S. earnings season.

Note: Stocks have traded flat over the past month as investors, after the +10% rise since last November's lows, have taken valuations above the long-term averages - 16 times forward earnings, compared to a 15-year average of about +14 times.

In Japan, the Topix index rose +0.7%, advancing for a second day, while the Nikkei was up on a weak yen (¥111.30) with financials outperforming on rising U.S yields.

Elsewhere, the Aussie S&P/ASX 200 Index added +0.9%. In Hong Kong, the Hang Seng index fell -0.1%, while China's Shanghai Composite slipped -0.5%. In South Korea, the Kospi index declined -0.9%, dropping for a fifth consecutive day for the longest losing streak in 10-months.

In Europe, equity indices are trading generally lower. Banking stocks are trading mixed in the Eurostoxx despite while commodity and mining stocks are lower in the FTSE 100.

U.S stocks are set to open in the 'black' (+0.1%).

Indices: Stoxx50 -0.3% at 3,483, FTSE flat at 7,351, DAX -0.1% at 12,210, CAC-40 -0.5% at 5,110, IBEX-35 -0.4% at 10,486, FTSE MIB -0.2% at 20,252, SMI -0.5% at 8,599, S&P 500 Futures +0.1%

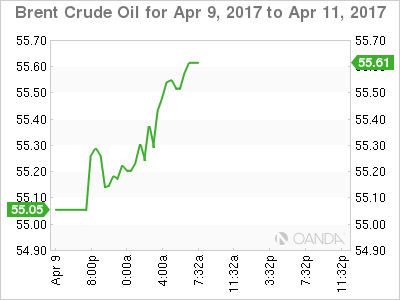

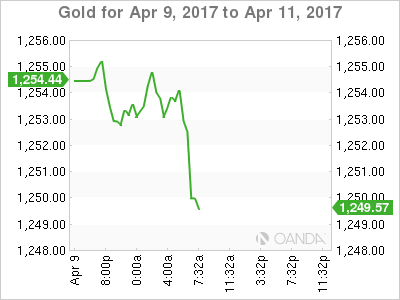

2. Oil up on strong demand, uncertainty over Syria, gold lower

Currently, oil prices are being supported by strong demand and uncertainty over the conflict in Syria. For the time being, a run-up in U.S drilling activity is keeping a lid on these gains.

Brent crude futures are at +$55.49 per barrel, up +25c, or +0.45% from Friday's close, while U.S West Texas Intermediate (WTI) crude futures are up +25c, or +0.46% at +$52.48 a barrel.

However, another increase in U.S. oil drilling - for the twelfth consecutive week and taking the count to 672 rigs, which is the highest since August 2015 - is keeping investors from breaking last week's one-month highs of over +$56 per barrel.

Note: Although Syria has limited oil production; its location in the Middle East and alliances with big oil producers raises concerns about spreading conflict that could disrupt crude shipments. Both Russia and Iran, staunch allies of Syria, condemned the attacks.

In oil supply fundamentals, the market remains oversupplied, even with efforts led by the OPEC to cut supplies to support global prices.

Gold prices remain steady (unchanged at $1,253.86 per ounce) with growing geopolitical tensions continuing to drive safe-haven demand.

Yesterday, aides to Trump differed on where Syrian/U.S policy was heading. However, U.S Secretary of State Tillerson has warned that the Syrian strikes are a warning to other nations, including North Korea.

3. French debt still an issue

Data from the Japanese MoF overnight showed record selling of French government bonds by domestic investors in February. Investors sold -¥1.504T of French debt or OAT's that month.

It was by far the most heavily sold government bond asset in Japan, as net selling of U.S Treasury's - the second most heavily sold asset - amounted to just +¥127B. The French are heading to the polls to elect a new president on April 23. The second round is scheduled for May 7.

Note: Some market participants continue to forecast more selling. Currently, French/Bund spread is at +70 bps, off from February's high of +80 bps.

Elsewhere, the yield on 10-year Aussie bonds backed up +2 bps to +2.57%, while U.S 10's fell -1 bps to +2.37%, after climbing +4 bps on Friday.

4. The 'mighty' dollar finds geopolitical support

Aside of geopolitical support, the USD is finding support from Fed rhetoric.

The Fed's typically more 'dovish' voter Dudley, whose recent comments are being perceived to be increasingly more 'hawkish.' Also, Fed member Bullard also noted that the underwhelming U.S jobs report fro March is in line with their view of +2% inflation and modest growth.

Ahead of the U.S open, the USD is trading atop of its three-week high, aided by geopolitical risks. The EUR (€1.0577) is a tad lower despite continued improvement in the regions confidence data. Data this morning showed that Sentix climbed to 23.9 vs. 20.1e.Teh single unit continues to be pressured by regional political concerns ahead of the French elections. USD/JPY is higher, up +0.3% at ¥111.35 aided by Fed's Dudley affirmation that the Fed was getting closer to shrinking its balance sheet.

Elsewhere, South Korea's won (KRW) fell -0.7%, sinking for a fifth consecutive day and the longest losing streak this year, while the AUD fell -0.2% (A$0.7489) after February home-loan data was weaker than expected.

5. Euro implied volatility surges on new French polls

Market nerves over the outcome of the France's presidential election have increased this morning after the far-left politician Jean-Luc Melenchon jumped in the latest polls, making the election a 'viable' four-way contest. This is supporting the probability of a second-round contest between the Communist-backed candidate and the anti-euro Marine Le Pen.

French/Bund spreads have widened + 3 bps, while the CAC (-0.5%) coming under renewed pressure.

Note: Emmanuel Macron remains the front-runner. Current polls show him tied with Marine Le Pen in the first round of the election, on April 27, but trouncing the National Front leader by -20% in the May 7 runoff.

Note: Liquidity heading into the Easter holiday in Europe is expected to exacerbate the moves in rates and currency markets.

Federal Reserve Chair Yellen Will be Speaking Later Today

- Dollar strengthens against Asian currencies

- Federal Reserve Chair Yellen will be speaking later today

- Bank of Canada (BoC) will be the highlight of the week

Overnight, the Dollar edged mildly higher, but quickly turned to mixed fortunes. The USD is somewhat supported by comments from Federal Reserve officials. St. Louis Federal Reserve President, James Bullard, reiterated opinions of other officials and said the Federal Reserve could start winding down its $4.5T balance sheet later this year. In contrast, New York Federal Reserve President, William Dudley, spoke on Friday and said that shrinking the balance sheet would only prompt a "little pause" in tightening. Weaker employment growth in the US reported on Friday did not affect risk appetite significantly and equity markets emerged relatively unscathed, as did the Dollar. The Dollar also seems to have strengthened as President Trump's threats of tariffs on Chinese goods have been scaled down since the election campaign and the two day summit between the US President and Chinese leader Xi Jinping were conducted in a constructive manner. Both stated that a quick trade agreement needs to be in place and China were also open to renewed access to the financial sector and abolished tariffs on certain US goods.

Today, Federal Reserve Chair, Janet Yellen, will speak, so markets await hints of her view on rates and balance sheet. It is likely that US President Donald Trump's implementation of his election promises of fiscal stimulus could be another factor, and more than likely a main focus.

The Bank of Canada (BoC) rate decision will be the highlight of the week. The Bank of Canada is widely expected to keep their interest rate unchanged at 0.50%. The tone of the statement could remain slightly dovish, in spite of improvements in economic data. Nonetheless, the Canadian Dollar will likely follow more on oil prices as West Texas Intermediate (WTI) crude oil could be heading back to 55.24 resistances due to geopolitical tensions.

In addition to that, we have a busy week on the data front, with UK Inflation and Employment data, German ZEW, the China Consumer Price Index (CPI), Producer Price Index (PPI) and Trade Balance, Australian Employment figures, the US Consumer Price Index (CPI) and Retail Sales data, all of which will be closely watched in a holiday shortened week, ahead of the long Easter weekend.

Spring jokes

Why did the farmer bury all his money?

To make his soil rich!

What did the summer say to the spring?

Help! I'm going to fall.

What kind of garden does a baker have?

A "flour" garden.