Sample Category Title

RBA Remains on Hold, But Tilts Somewhat Dovish

The Reserve Bank of Australia remained on hold today, as was widely anticipated. However, the statement had a somewhat dovish tone compared to the previous one, in our view. The Bank indicated that some labor market indicators have softened recently, while it noted that the recently announced supervisory measures with regards to lending could ease financial stability risks.

This suggests to us that once these measures take effect, the Bank would be more flexible to cut rates again if needed, without being concerned that its actions would amplify risks to the economy. Thus, although our base case scenario is still for the RBA to remain on hold in the foreseeable future, further weakness in economic indicators, could encourage officials to act without much hesitation. We believe that the picture will become much clearer on the 26th of April, when we get the nation's CPI data for Q1.

AUD/USD tumbled following the release of the meeting statement, falling below the key support (now turned into resistance) obstacle of 0.7600 (R1). This move confirms a forthcoming lower low on the 4-hour chart and combined with the Bank's dovish language, increases the likelihood for the pair to stay on the back foot for a while. The upcoming meeting between US President Trump and Chinese President Xi Jinping on Thursday could also prove negative for the currency. Any talks of increased protectionism in the global arena could weigh on the currencies of heavily trade-oriented nations, such as AUD and NZD. At the time of writing, the rate is testing the 0.7580 (S1) area, where a decisive dip is possible set the stage for our next support of 0.7550 (S2).

Today's highlights:

During the European day, we get the UK construction PMI for March. The forecast is for the index to have declined, albeit marginally. Nonetheless, following the unexpected tumble in the manufacturing index for the month, we see the risks surrounding the construction forecast as skewed to the downside, perhaps for a greater than expected slide. In such a case, GBP could come under renewed selling pressure. We prefer to exploit further pound weakness against the yen, which continued to strengthen yesterday. GBP/JPY slid and is currently testing the 137.50 (S1) support zone. A disappointing construction PMI today could push the rate below that hurdle and pave the way for the key territory of 137.00 (S2). However, a clear close below that barrier is needed to turn the broader outlook negative as well.

From Eurozone, we get retail sales for February, while from the US, the trade balance and factory orders for the same month are coming out.

We have only one speaker on the schedule: ECB President Mario Draghi. Following the latest media reports that investors over-interpreted the ECB's signals at the March policy meeting, and the subsequent slowdown in the bloc's CPI prints for March, it would be interesting to hear what the ECB chief has to say.

AUD/USD

Support: 0.7580 (S1), 0.7550 (S2), 0.7530 (S3)

Resistance: 0.7600 (R1), 0.7625 (R2), 0.7650 (R3)

GBP/JPY

Support: 137.50 (S1), 137.00 (S2), 136.50 (S3)

Resistance: 138.70 (R1), 139.10 (R2), 140.00 (R3)

Canadian Dollar Dips To 3-Week Low, Trade Balance Next

USD/CAD continues to gain ground this week. In the Tuesday session, the pair has reached a high of 1.3447, its highest level since March 15. On the release front, Canada and the US will both release Trade Balance. Canada's trade surplus is expected to edge lower to C$0.7 billion. In the US, the trade deficit is forecast to narrow to $46.0 billion.

Canada's GDP expanded 0.6 percent, above the forecast of 0.3 percent. This marked a 7-month high for GDP, and raises hopes that a strong US economy will boost its northern neighbor. Although the Canadian economy has been churning out decent numbers, lower oil prices have had a negative impact on the Canadian economy and also weighed on the Canadian dollar, which continues to lose ground. Later in the week, we'll get a look at Canadian Employment Change, which is expected to post a modest gain of 5.7 thousand.

The US economy hasn't missed a beat in 2017, and the markets are expecting strong data for the first quarter. The CB consumer confidence report soared to 125.6 in March, and strong consumer confidence levels should translate into increased consumer spending, a key component of economic growth. GDP for the fourth quarter was revised to 2.1%, up from 1.9% in the previous GDP report. With the economy headed in the right direction, the discussions around the monetary policy tables are not whether the Fed will raise rates, but will it press the rate trigger two or three more times in 2017. The markets will be paying close attention to the minutes of the March meeting, when the Fed raised rates by a quarter-point, to a range of 0.75-1.00%. Any hints about the timing of the next hike, as well as the tone of the minutes are factors which could move the currency markets on Wednesday. The markets considered the rate statement overly cautious, and this sentiment sent the US dollar broadly lower. If the reaction to the minutes is one of disappointment, the dollar could again head downwards.

GBPCHF Beware Of Head And Shoulders At 1.2440

The GBP/CHF has formed head and shoulders pattern (Bearish SHS) with a clear double bottom at 1.2441. Bearish SHS could breakout below at 1.2440 aiming for D L5/ W L4 confluence 1.2415 and 1.2383. If the pair retraces to POC (top of the right shoulder, D H3, ATR pivot) 1.2515-30 we might see a rejection towards above mentioned targets. So traders should pay attention to POC rejection or breakout below 1.2440.

D H3 - Daily Camarilla Pivot (Daily Resistance)

POC - Point Of Confluence (The zone where we expect price to react - aka entry zone)

W L4 - Weekly L3 Camarilla (Very Strong Weekly Support)

D L4- Daily L4 Camarilla ( Very Strong Daily Support)

D L5- Daily L4 Camarilla ( Strongest Daily Support)

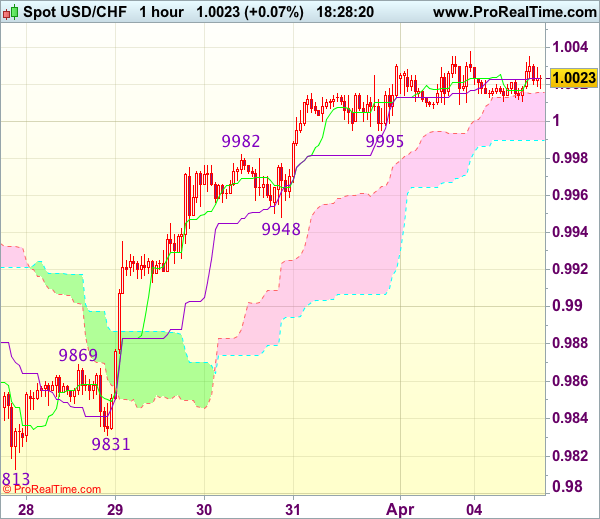

Trade Idea Update: USD/CHF – Buy at 0.9950

USD/CHF - 1.0027

Original strategy :

Buy at 0.9950, Target: 1.0050, Stop: 0.9915

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9950, Target: 1.0050, Stop: 0.9915

Position : -

Target : -

Stop : -

As the greenback has maintained a firm undertone after last week’s rally above 1.0003 resistance, suggesting recent rise from last week’s low at 0.9813 is still in progress and bullishness remains for this move to extend gain to previous support at 1.0060 (now resistance), however, loss of upward momentum should prevent sharp move beyond resistance at 1.0109, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy dollar on pullback as said support at 0.9948 should limit downside. Below 0.9931 (50% Fibonacci retracement of 0.9831-1.0031) would abort and signal top is formed instead, bring correction to 0.9905-10 (61.8% Fibonacci retracement) but reckon previous resistance at 0.9869 would hold from here.

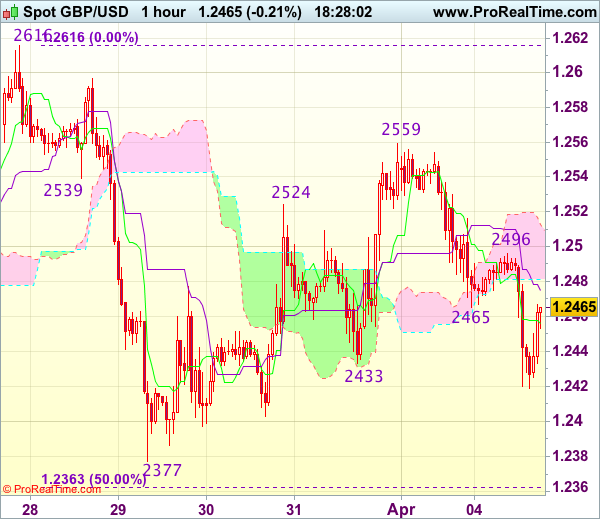

Trade Idea Update: GBP/USD – Hold short entered at 1.2465

GBP/USD - 1.2457

Original strategy :

Sold at 1.2465, Target: 1.2365, Stop: 1.2500

Position : - Short at 1.2465

Target : - 1.2365

Stop : - 1.2500

New strategy :

Hold short entered at 1.2465, Target: 1.2365, Stop: 1.2500

Position : - Short at 1.2465

Target : - 1.2365

Stop : - 1.2500

Although cable has rebounded after finding support at 1.2419 and minor consolidation above this level would be seen, reckon the Kijun-Sen (now at 1.2475) would limit upside and bring another decline later, below said support at 1.2419 would extend weakness to 1.2400, break there would add credence to our view that the rebound from 1.2377 has ended at 1.2559, bring further fall towards support at 1.2377. Looking ahead, only a drop below 1.2377 would confirm the fall from 1.2616 is still in progress for subsequent decline towards key support at 1.2335.

In view of this, we are holding on to our short position entered at 1.2465 but one should exit on such decline. Only break of said resistance at 1.2496 would abort and suggest an intra-day low is formed instead, risk a stronger rebound to 1.2525-30.

EUR/GBP Bulls Retreat Under Resistance At 0.8600

The European Central Bank president Draghi will make a speech at 15:30 BST today, it will likely affect the Euro and Euro crosses.

EUR/GBP has rebounded since yesterday, after hitting a 5-week low of 0.8485.

The bulls attempted to test the near-term major resistance level at 0.8600 in early morning, where the 10-day SMA converges (on the daily chart).

The bulls still have momentum, however, be aware that the selling pressure at this level is heavier. The bullish momentum is likely to be restrained here, prior to the next rally.

The 4-hourly Stochastic Oscillator reading is around 70, suggesting a retracement.

The resistance level is at 0.8565, followed by 0.8580 and 0.8600.

The support line is at 0.8550, followed by 0.8535 and 0.8520.

Trade Idea Update: EUR/USD – Sell at 1.0730

EUR/USD - 1.0651

Original strategy :

Sell at 1.0730, Target: 1.0610, Stop: 1.0765

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0730, Target: 1.0610, Stop: 1.0765

Position : -

Target : -

Stop : -

As the single currency has remained under pressure after falling to 1.0642 yesterday, adding credence to our bearish view that the decline from 1.0906 top is still in progress and bearishness remains for this fall to extend further weakness to 1.0620-25, then test of previous chart support at 1.0600, however, a sustained breach below the latter level is needed to retain downside bias for subsequent selloff to 1.0570-75 first, otherwise, risk from there is seen for a rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 1.0730-40 should limit upside. Only a firm break above resistance at 1.0773 would suggest low is formed instead, bring a stronger rebound to 1.0800 but resistance at 1.0827 should remain intact.

Market Update – European Session: Spain Continues With Its Improving Employment Trend

Notes/Observations

Quiet session; focus on key end-of-week events: US payroll data and President Trump/China President Xi meeting in Florida

Spain's Net Unemployment registers its biggest ever decline for the month of March (-48.8K v -40.9K)

Overnight:

Asia:

RBA keeps Cash Rate Target unchanged at 1.50% (as expected). Says view consistent with sustainable growth in the economy and achieving the inflation target over time. Reiterated view that domestic inflation remained quite low but was expected to pick up over the course of 2017

BOJ Gov Kuroda reiterated view that was too early to discuss an exit from current monetary policy. Exit strategy to vary depending on economy and markets. BOJ ETF purchases are not distorting market function

South Korea Mar CPI registered its highest annual pace since June 2012 (2.2% v 2.1%e)

Europe:

UK House of Commons Brexit committee noted that PM May had been urged by to carry out a full economic and legal assessment of the implications for Britain if it failed to sure a trade deal with the EU. Must publish cost reaching no deal in Brexit talks

Americas:

Fed's Harker (hawk, FOMC voter): reiterated three hikes in 2017 would be appropriate; US inflation was moving slowly but surely upward

Senate Judiciary Committee approved Gorsuch nomination to Supreme Court; sent nomination to full Senate floor. Senate Democrats now have 41 votes against cloture, sufficient to filibuster nomination of Neil Gorsuch to the Supreme Court

Economic Data

(ES) Spain Mar Net Unemployment M/M: -48.8K v 0.9Ke (Biggest decline ever for month of March)

(IT) Italy Q4 YTD Budget Deficit to GDP: 2.4% v 2.5% prior

(BR) Brazil Mar FIPE CPI (Sao Paulo) M/M: 0.1% v 0.1%e

(UK) Mar Construction PMI: 52.2 v 52.5e (7th month of expansion)

(EU) Euro Zone Feb Retail Sales M/M: 0.7% v 0.5%e; Y/Y: 1.8% v 1.0%e

Fixed Income Issuance:

(EU) EFSF opened book to sell 2024 and 2045 bonds via syndicate

(ES) Spain Debt Agency (Tesoro) sold total €4.63B vs. €4.0-5.0B indicated range in 6-month and 12-month Bills

(ID) Indonesia sold total IDR4.46 in 2-year, 4-year, 7-year and 15-year Project based Sukuk (PBS)

(AT) Austria Debt Agency (AFFA) sold total €1.32B vs. €1.32B indicated in 2023 and 2027 RAGB bonds

(ZA) South Africa sold total ZAR2.35B vs. ZAR2.35B indicated in 2026, 2036 and 2048 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Index snapshot (as of 10:00 GMT)

Indices [Stoxx50 -0.1% at 3,470, FTSE +0.4% at 7,314, DAX -0.1% at 12,241, CAC-40 flat at 5,086, IBEX-35 +0.1% at 10,337, FTSE MIB -0.2% at 20,193, SMI +0.1% at 8,643, S&P 500 Futures -0.2%]

Equities

Consumer discretionary [ASOS ASC.UK -6.2% (H1 results), Topps Tiles TPT.UK -6.9% (H1 update), Bunzl BNZL.UK +1.8% (2 acquisitions)]

Consumer Staples [Suedzucker SZU.DE -9.5% (Analyst downgrade), ITE Group ITE.UK +4.3% (Trading update), Carl Zeiss AFX.DE +1.3% (prelim H1)]

Materials: [Nanoco NANO.UK -18% (H1 results, lowers outlook)]

Financials: [Grenkeleasing GLJ.DE +3.5% (Q1 update)]

Technology: [Sophos Grp SOPH.UK +11.4% (Raised outlook, resolves patent dispute)]

Energy: [Seadrill SDRL.NO -41% (Amendments to Secured Credit Facilities), Polarcus PLCS.NO -3.5% (Vessel utilization)]

Speakers

BOE Financial Policy Committee (FPC) Mar 22nd Minutes: Concerned rapid growth in unsecured lending to British consumers; could principally represent a risk to lenders if accompanied by weaker lending standards

Sweden Central Bank (Riksbank) Dep Gov Floden: PMI data was a sign for growth but it remained to be seen what growth meant for inflation

RBA Gov Lowe: More home loan curbs would be considered if needed. Reiterates need to see improvement in job market to know economy is strengthening

Eurogroup Chief Dijsselbloem reiterated he had no intention to step down as Eurogroup chief; looking to speak in EU Parliament

EU Official: Greece talks in Brussels today could be an important stepping stone. Greek hurdles were political and not technical. Talks moving beyond July payments would be detrimental

Russia govt said not to be planning any measures to counter gains in RUB currency (ruble). It saw the Ruble currency weakening in H2 due to oil and rate cuts

Moody's on South Africa: Will not be issuing any decision on sovereign rating on Friday, Apr 7th. To issue decision after concluding downgrade review that could take 1-3 months from now

Turkey Fin Min Agbal: Inflation might be back to single digits by Dec; upward trajectory to continue

Currencies

US Treasury yields at 5-week low helping to push the USD/JPY pair below 110.50 in the session. Some dealers also noting that BoJ and government advisors had been floating the idea of how to move away from yield curve control. Nonetheless BoJ's Kuroda did reiterated his dovish stance that it was premature to discuss an exit strategy from the central bank's aggressive easing policy.

EUR/USD hovered in the mid-1.06 area as price action continued the repricing of ECB rate outlook as various officials noted . ECB chief economist Praet continues, after yesterday ' s push back of rate hikes from Praet

RBA kept its policy steady with a dovish tilt and this helped the AUD/USD hit a 3-week low below 0.7560 area.

Spot gold at 1-month highs aided by geopolitical worries with the metal at $1,258/oz

Fixed Income:

Bund futures trade at 162.35 up a further 26 ticks trading at new one month highs with further momentum higher targeting 162.65 followed by 162.98 then Feb contract high at 163.12. Analysts eye support at 161.63 followed by 161.34 then 161.06.

Gilt futures trade at 128.40 up 13 ticks aided by a slight miss in UK construction PMI data. Resistance moves to 128.96 followed by 129.24. Support moves to 127.75 then 127.34 followed by 127.05. Short Sterling futures curve continues to flatten with futures trading flat to up 2bp along the curve. Jun17Jun18 spread falls to 13.5/14bp down 2.5bp from yesterday.

Tuesday's liquidity report showed Monday's excess liquidity fell to €1.444T a fall of €68B from €1.512T prior. Use of the marginal lending facility fell to €212M from €285M prior.

Corporate issuance saw $2.75B come to market via 5 issuers in a slow start to the quarter, headlined by Progressive Corp $850M 30 year offering, and Cimarex Energy $750M 10 year offering. Issuance for the week is expected to be around $25B.

Looking Ahead

(RU) Russia Mar Sovereign Wealth Fund Balances: Reserve Fund: No est v $16.1B prior; Wellbeing Fund: No est v $72.6B prior

(BR) Brazil Mat CNI Consumer Confidence: No est v 104.4 prior

05.30 (UK) Weekly John Lewis LFL sales data - 05:30 (EU) ECB allotment in 7-Day Main Refinancing Tender

05:30 (HU) Hungary Debt Agency (AKK) to sell 3-month Bills

05:30 (DE) Germany to sell €1.0B in 0.1% Apr 2026 Indexed-bonds

05:30 (BE) Belgium to sell €1.3-1.7B in 3-Month and 6-Month Bills

06:00 (IE) Ireland Mar Unemployment Rate: No est v 6.6% prior

06:00 (TR) Turkey to sell Zero 2018 Bonds; Yield: % v 11.67% prior; bid-to-cover: x v 6.86x prior

06:45 (US) Daily Libor Fixing

07:30 (TR) Turkey Mar Real Effective Exchange Rate (REER): No est v 88.83 prior

07:45 (US) Weekly Goldman Economist Chain Store Sales

08:00 (BR) Brazil Feb Industrial Production M/M: +0.7%e v -0.1% prior; Y/Y: 0.4%e v 1.4% prior

08:00 (NO) Norway Central Bank (Norges) Gov Olsen speaks in Oslo

08:00 (RU) Russia announces weekly OFZ bond auction - 08:15 (UK) Baltic Dry Bulk Index

08:30 (US) Feb Trade Balance: -$44.6Be v -$48.5B prior

08:30 (CA) Canada Feb Int'l Merchandise Trade: C$0.6Be v C$0.8B prior

08:30 (SI) Slovenia Debt Agency to sell 12-month and 18-month Bills

08:30 (NZ) Fonterra Global Dairy Trade Auction

08:55 (US) Weekly Redbook Sales

09:00 (EU) Weekly ECB Forex Reserves

09:00 (MX) Mexico Feb Leading Indicators M/M: No est v -0.20 prior

09:30 (EU) ECB's Draghi speaks in Frankfurt

09:30 (EU) ECB announces Covered-Bond Purchases

10:00 (US) Feb Factory Orders: 1.0%e v 1.2% prior; Factory Orders Ex-Transportation: No est v 0.3% prior

10:00 (US) Feb Final Durable Goods Orders: 1.7%e v 1.7% prelim; Durables Ex-Transportation : No est v 0.4% prelim; Capital Goods Orders (Non-defense ex aircraft): No est v -0.1% prelim, Capital Goods Shipments (Non-defense/ex-aircraft): No est v +1.0%prelim; Durables Ex-Defense: No est v 2.1% prelim

10:00 (DK) Denmark Mar Foreign Reserves (DKK): 470.8Be v 466.6 prior

11:00 (BR) Brazil to sell I/L 2022, 2026, 2035 and 2055 Bonds - 11:30 (US) Treasury to sell 4-Week Bills

15:00 (CO) Colombia Mar Total PPI M/M: No est v -0.6% prior; Domestic PPI M/M: No est v -0.2% prior

16:30 (US) Weekly API Oil Inventories

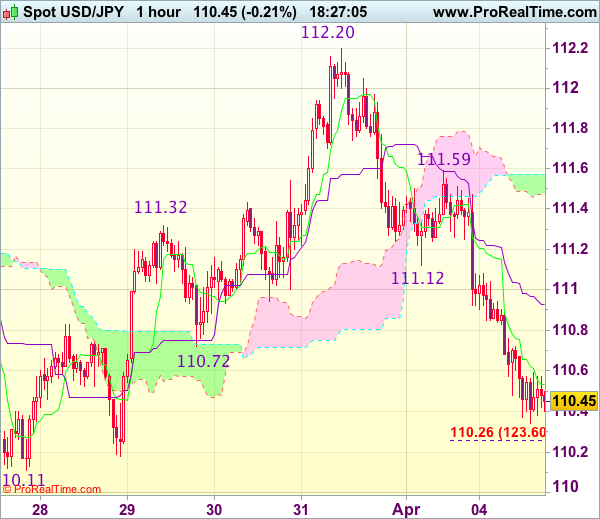

Trade Idea Update: USD/JPY – Sell at 110.95

USD/JPY - 110.45

Original strategy :

Sell at 110.95, Target: 109.95, Stop: 111.30

Position : -

Target : -

Stop : -

New strategy :

Sell at 110.95, Target: 109.95, Stop: 111.30

Position : -

Target : -

Stop : -

As the greenback has dropped again after meeting renewed selling interest at 111.59 yesterday, adding credence to our view that top ha been formed at 112.20 and bearishness remains for the selloff from there to extend weakness to 110.11 support, however, break there is needed to retain downside bias and confirm medium term decline has resumed for further subsequent fall to 109.80-85 (1.618 times projection of 112.20-111.12 measuring from 111.59) which is likely to hold on first testing.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 110.90-95 should limit upside. Above previous support at 111.12 (now resistance) would defer but only break of resistance at 111.59 would abort and signal the fall from 112.20 has ended instead.

Technical Outlook: US Crude – Correction Cracks $50.00 Support, Risks Dips To $49.39

WTI oil extends pullback from recovery highs at $50.82, following repeated upside rejection of recovery rally that was capped by daily Kijun-sen line. The price is in red for the second day and fresh extension lower cracked psychological $50.00 support on Tuesday. The move is so far seen as correction on strongly overbought slow stochastic on daily chart, which is attempting to generate stronger bearish signal on reversal. Correction could extend to $49.39 (Fibo 38.2% of $47.07/$50.82 upleg), before fresh attempts higher. Technicals studies are in mixed mode and without clear direction, however, recent break above $50.00 pivot was positive signal for further recovery. Limited dips are required to keep bullish scenario in play for fresh attempts towards next targets at $51.03/20 (50% of $55.01/$47.06/100SMA). Alternatively, increased downside pressure could be expected on loss of $49.39 support, while extension below $48.95 (daily Tenkan-sen) would signal reversal.

Res: 50.33, 50.73, 50.83, 51.03

Sup: 48.87, 49.39, 48.95, 48.50