Sample Category Title

EUR/JPY Weekly Outlook

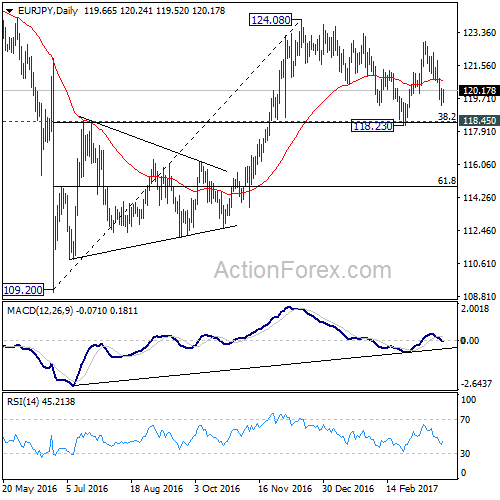

EUR/JPY's fall from 122.88 extended to as low as 119.31 last week before forming a temporary low there and recovered. Overall, there is no change in the view that price actions from 124.08 are developing into a consolidative pattern. While more sideway trading could be seen, an upside breakout is expected later to resume the larger rise from 109.20.

Intraday bias in EUR/JPY is neutral this week first. Below 119.31 will bring deeper fall. But we'd expect strong support from 118.45 key cluster support level (38.2% retracement of 109.20 to 124.08 at 118.39) to contain downside and bring rebound. On the upside, above 120.81 minor resistance will turn bias back to the upside for 124.08 high.

In the bigger picture, we're holding on to the view that medium term rise from 109.20 is still in progress. Focus is on 126.09 key resistance level. Sustained break will confirm completion of the whole decline from 149.76. And rise from 109.20 is of the same degree as the fall from 149.76. In such case, further rally would be seen to 104.04 resistance and possibly above before topping. Meanwhile, rejection from 126.09, or firm break of 118.45 cluster support, will likely extend the fall from 149.76 through 109.20 low.

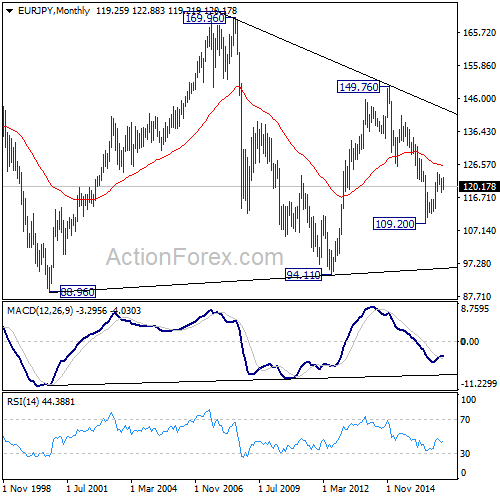

In the long term picture, medium term decline from 149.76 is seen as part of a long term sideway pattern from 88.96. Decisive break of 126.09 will indicate that such decline is completed and EUR/JPY has started another medium term rally already. Before that, deeper fall is mildly in favor towards 94.11 low. Overall, long term rang trading will continue.

EUR/GBP Weekly Outlook

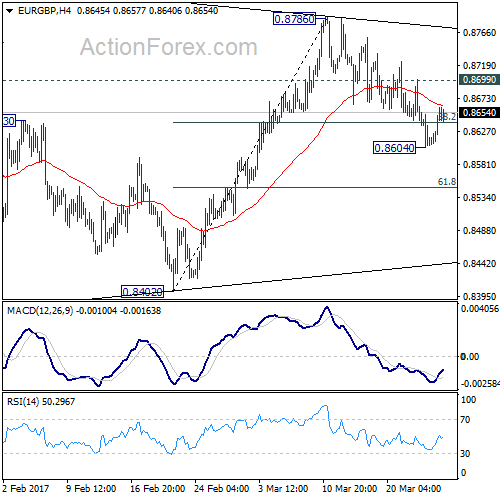

EUR/GBP's corrective fall extended to as low as 0.8604 last week and took out 38.2% retracement of 0.8402 to 0.8786 at 0.8639. The decline was deeper than expected but the cross quickly recovered after drawing support from 55 day EMA. The development mixed up the near term outlook a bit. But overall, there is no change in the view that price actions from 0.8303 are forming a corrective pattern, as the second leg of the correction from 0.9304. The question is what exact pattern it's turning out to be. Decline from 0.9304 is expected to resume later.

Initial bias in EUR/GBP stays neutral this week first. With 0.8699 minor resistance intact, deeper decline is mildly in favor. Below 0.8604 will target 61.8% of 0.8402 to 0.8786 at 0.8549 and possibly below. In that case, we'll look for support above to 0.8402 to bring another rebound before completing that correction from 0.8303. ON the upside, above 0.8699 will turn bias back to the upside for 0.8786. Break will target 61.8% retracement of 0.9304 to 0.8303 at 0.8922 to finish the pattern from 0.8303.

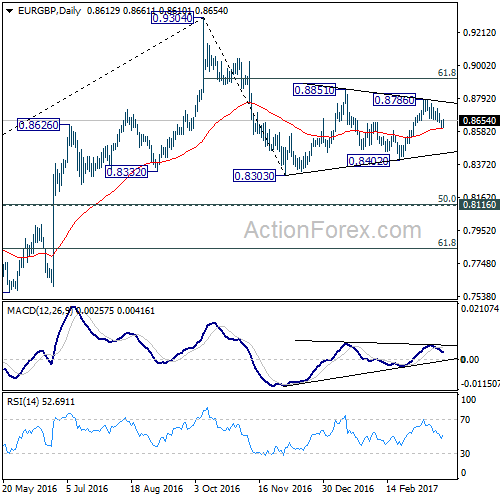

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. Deeper fall cannot be ruled out yet. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Overall, the corrective pattern would take some time to complete before long term up trend resumes at a later stage. Break of 0.9304 will pave the way to 0.9799 (2008 high).

In the long term picture, firstly, price action from 0.9799 is seen as a long term corrective pattern and should have completed at 0.6935. Secondly, rise from 0.6935 is likely resuming up trend from 0.5680 (2000 low). Thirdly, this is supported by the impulsive structure of the rise from 0.6935 to 0.9304. Hence, after the consolidation from 0.9304 completes, we'd expect another medium term up trend to target 0.9799 high and above.

EUR/AUD Weekly Outlook

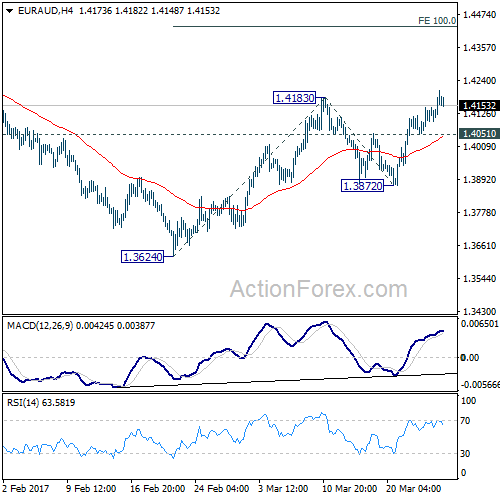

EUR/AUD's pull back was continued at 1.3872 last week. Subsequent rally and break of 1.4183 resistance indicates resumption hole rebound from 1.3624. The development also affirms our bullish view. That is, medium term trend is reversing after defending 1.3671 key support level, on on bullish convergence condition in daily MACD.

Initial bias in EUR/AUD is back on the upside this week. Further rally should now be seen to 100% projection of 1.3624 to 1.4183 from 1.3872 at 1.4431. Decisive break there will indicate upside acceleration and target 1.4721 key resistance next. On the downside, below 1.4051 minor support will turn focus back to 1.3872 support instead.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction could be completed after testing 1.3671 support. Break of 1.4721 cluster resistance (38.2% retracement of 1.6587 to 1.3624 at 1.4756) should confirm this case and target 61.8% retracement at 1.5455 and above. Overall, we'd expect the up trend from 1.1602 to resume later. However, sustained break of 1.3671 will invalidate our bullish view and would turn focus back to 1.1602 long term bottom.

In the longer term picture, the rise from 1.1602 long term bottom isn't over yet. We'll keep monitoring the development but there is prospect of extending the rise to 61.8% retracement of 2.1127 to 1.1602 at 1.7488 and above. However, sustained trading below 1.3671 should confirm trend reversal and target 1.1602 long term bottom again.

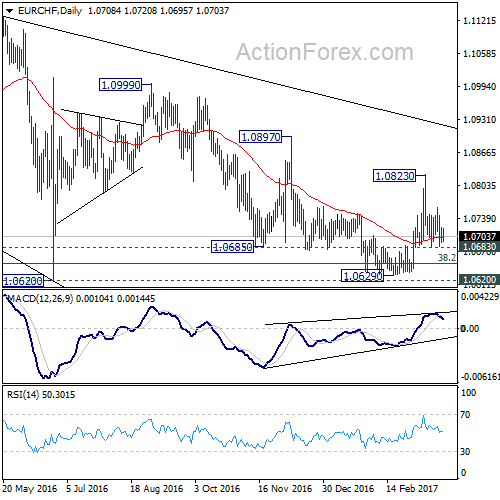

EUR/CHF Weekly Outlook

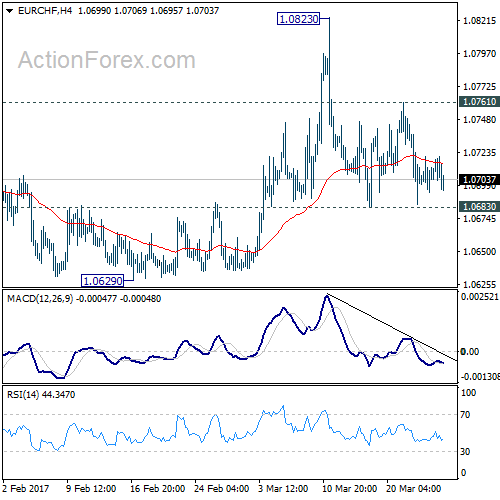

EUR/CHF stays in range of 1.0683/0823 last week and outlook is unchanged. With 1.0683 minor support intact, we'd slightly favoring the case of trend reversal on bullish convergence condition in daily MACD. But such view is dampened by prior rejection from the falling 55 week EMA.

Initial bias in EUR/CHF remains neutral this week first. Further rise is expected as long as 1.0683 minor support holds. Above 1.0761 minor resistance will turn bias to the upside for 1.0823 resistance first. Break will re-affirm the case of trend reversal and target 1.0897 resistance next. However, firm break of 1.0683 minor support will turn bias to the downside for 1.0620 key support level again.

In the bigger picture, the decline from 1.1198 is seen as a corrective move. Decisive break of 1.0897 resistance should confirm that it's completed. And in that case, larger up trend is resuming for another high above 1.1198. Meanwhile, sustained trading below 38.2% retracement of 0.9771 to 1.1198 at 1.0653 will target 50% retracement at 1.0485.

Summary 3/27 – 3/31

Monday, Mar 27, 2017

[php_everywhere] [/php_everywhere]

Tuesday, Mar 28, 2017

[php_everywhere] [/php_everywhere]

Wednesday, Mar 29, 2017

[php_everywhere] [/php_everywhere]

Thursday, Mar 30, 2017

[php_everywhere] [/php_everywhere]

Friday, Mar 31, 2017

[php_everywhere] [/php_everywhere].

Weekly Market Outlook – Buy The Dip In EM Risk

FX Markets - Buy The Dip In EM Risk

After almost three months of an uninterrupted surge, emerging market currencies have finally taken a breather. In three months the ZAR has gained an impressive 12.20%, with MXN and KRW not far behind. In fact, among the liquid EM currencies, only the ARS, PHP and TRY saw losses against the USD. Last week's pullback in stocks spilled into rates and FX, raising questions on the sustainability of the current bullish view on risk appetite.

We suspect that this run is not over yet based on two key factors:

1) The Fed's policy path continues to be discounted with expectations for a June rate hike now below 60% probability. The FOMC's March communications were decidedly dovish. Also, Friday's CPI and durable goods orders ex transportation both disappointed, highlighting the fact that US investor optimism was based predominately on sentiment indicators rather than hard data (which as been unimpressive). In addition, Trump's failure to force through the Obamacare repeal bill indicates the challenge he faces in policy execution. This inability specifically threatens the administration's pro-growth agenda, which could accelerate the US economic outlook and position more hikes in play. We suspect that risk is skewed towards a less steep Fed policy path, but it's critical to highlight that the steady improvement in EM currencies means less sensitivity to US rates adjustment. A dovish Fed will further support EM risk taking.

2) EM growth is highly dependent on global trade, which President Trump has potentially endangered. Trump's protectionist trade policy was on display in the administration's first 30 day with the rejection of the TransPacific Partnership (TPP).

But other than some random, disorganised Twitter rants, his "America first" protectionism is more image then trade policy.

In our view, Trump's ability to create meaningful trade barriers such as punitive import tariffs has been discounted. We can just about hear Trump's words when discussing trade or FX policy "nobody knew that *insert policy here* could be so complicated." As with healthcare, just about everyone in the financial markets knows how complicated and non-mechanical these issues are. With the fear of excessive protectionism fading, EM currencies should continue to find buyers.

Economics - RBNZ Hopes The Market Will Collaborate

The New Zealand dollar, like most commodity currencies, has performed relatively poorly during the month of March as it failed to attract investors' attention in spite of the broad based USD weakness. On the other hand, its close neighbour the Australian dollar has had strong momentum over the same period. This divergence could be explained by the surprising switch in forward guidance of the Reserve Bank of New Zealand that delayed any tightening move back in early February. The last RBNZ meeting, which was held last week, was of the same stripe. Graeme Wheeler did not change his view on the overvaluation of the Kiwi, instead repeating the need for a weaker Kiwi "to achieve more balanced growth". He also allayed fears concerning rising inflationary pressure, arguing that the spike was temporary, stemming from a temporary rise in commodity prices.

Overall, the tone of the statement suggests that the RBNZ is ready to tolerate higher inflation in order to allow for a weaker Kiwi. This may be a good decision especially as core inflation has picked up at a slower pace than headline inflation. However, we are having a hard time believing that the market will collaborate. Indeed, the RBNZ has often struggled to drive the market the way it wanted. The sharp drop in US sovereign yields will force investors to switch in yield seeking mode. Moreover, Kiwi and Aussie rates have started to move in opposite direction last week with the Kiwi 2- year sovereign yields reversing momentum to reach 2.16% on Friday, while its Aussie counterpart slid to 1.75%. We favour long NZD positions, especially against the Australian dollar. NZD/USD has room for appreciation, even though the risk-off sentiment will limit risk appetite. AUD/NZD has already fallen 1.4% since mid-March and is now heading towards the next key support area at around 1.0755 (Fibo 38.2% on January-March rally).

Economics - SNB Releases Its Annual Report

In the latest annual report from the SNB, we have learned that the Swiss central bank bought around CHF67 billion in foreign currencies in order to defend the franc. Comparatively, this is lower than in 2015, when the floor was removed. Interventions amounted then at CHF86.1 billion.

The SNB still sees the franc as "significantly overvalued" and so the negative interest rate policy is more relevant than ever. The Swiss economy relies on the exports. Hence it is normal to consider medium and long-term risk valuation. For now, the central bank is sticking to its wait-and-see approach.

Europe's political uncertainties are weighing heavily on the EURCHF and we believe that bearish pressure shows no signs of easing. In terms of Swiss data, inflation has never been so high in the last five years at 0.6% y/ y and the unemployment rate remains moderate at 3.6%. Exports are a little more concerning with two consecutive declines in January and February (respectively -4% and -2.2%). In the short and medium-term, the Swiss Franc should remain below 1.0800 and the SNB is likely to intervene to avoid extreme strengthening.

What is certain is that the SNB is monitoring any development from the ECB which massive QEs keep running. We also believe that the ECB is likely to soon enter a tightening cycle - to reduce monetary policy divergence with the US - which in turn will definitely benefit the Swiss economy.

Currency-wise, it seems obvious that the Swiss National Bank is likely to increase currency intervention to defend the franc this year. Since the start of this year, the pace of intervention seems to have accelerated. In January total deposits were standing at CHF530 billion. Three months later, the deposits lies at CHF 557.2 billion. On top of that when looking at the price action of the EURCHF, selling pressures are way too important around 1.0800 and makes these interventions almost useless.

Themes Trading - Gold & Metal Miners

The sudden collapse in commodity prices in 2014 sent mining stocks into free fall. In the long term, however, precious metals - and gold in particular - are the perennial go-to sources of protection against inflation and economic downturns, something investors should be looking out for. The gold market is dynamic, and there are compelling reasons why gold producers could rally. Consumer demand remains solid, with around 2,500 tons of gold mined worldwide every year. Over the long haul, gold as a commodity has appreciated by more than 287% over the past 15 years; by comparison, the S&P 500 has gained less than 44% over the same period. In a period of central bank policy shifts, it is reasonable to envisage a rebound in metal prices - something mining stocks will benefit from. Gold miners are a good way to tap into the benefits of precious metals without paying storage costs.

Gold & Metal Miners theme can now be trading in an easy to execute Strategic Certificate.

The Weekly Bottom Line

HIGHLIGHTS OF THE WEEK

United States

- Stock markets inched lower this week as odds increase that the promise of regulatory reforms and tax cuts will be delayed.

- Normally falling stocks, dollar, oil, and Treasury yields would suggest concern about the health of the U.S. economy. However, the data this week remained supportive of an expansion in the U.S. and global economies in the first half of this year.

- Later today the U.S. congress will vote on a bill to amend the Affordable Care Act (ACA) that is likely to have market implications. If the bill passes, it moves onto the Senate, but if today's vote fails, future amendments to the ACA could be in doubt.

Canada

- The big-ticket economic attention-grabber this week was the federal government's 2017 budget. The budget was largely a stay-the-course type, with the federal government accepting larger deficits over the medium-term to push its spending agenda along.

- Budget aside, the economic data this week highlighted that the economy may outperform near-term expectations, with retail sales roaring back from a disappointing December reading. Motor vehicle and parts remain the biggest driver of retail spending, highlighting that consumer confidence remains strong in Canada. Having said that, inflation readings were soft, suggesting the Bank of Canada isn't likely to move anytime soon.

UNITED STATES - MARKETS TAKE A BREATHER

There was little in the way of data and news this week to move markets. Nevertheless, stock markets inched lower, as it became increasingly apparent that the promise of regulatory reforms and tax cuts is likely to be delayed beyond the summer. Despite the rate hike by the Federal Reserve last week, U.S. Treasuries rallied, with the 10-yr Treasury yield briefly dipping below 2.4% - roughly the going rate in play prior to the Fed jawboning the market in late February. Coinciding with these market moves has been a decline in oil prices and a weaker trade-weighted U.S. dollar.

Normally falling stocks, dollar, oil, and Treasury yields would suggest concern about the health of the U.S. economy. However, this is unlikely the reason behind the market moves this week. In fact, on a year-to-date basis, the S&P 500 is up 5%, and the 10-yr yield is less than 10 basis points from where it was at the end of last year, and about 50 basis points higher than when it was before the November election. Moreover, although oil prices have dipped below $US 50 per barrel, the recent weakness has more to do with rising supply than declining demand.

The only outlier is the trade-weighted dollar, which has dropped by about 2.5-3.5% since the start of the year, depending on which measure is used. But this too is not necessarily a result of a more negative outlook for the U.S. economy, but rather a reflection of stronger global economic growth. For example, growth in Europe is expected to be well in excess of its trend pace again in 2017 for the third consecutive year, and suggests that the next step for the ECB is likely to tighten rather than ease monetary policy. Strong economic activity by its trading partners should support demand for U.S. produced goods and services, although we still are of the view that net trade is likely to be a small drag on U.S. economic activity this year.

The admittedly sparse data this week is broadly consistent with this view. Preliminary survey data for March released this morning suggests that the Eurozone economy likely expanded at a slightly faster pace than in previous months. Conversely, according to the same survey data the U.S. economy likely saw growth slow a touch in March. Moreover, U.S. existing home sales in February dropped 3.7% m/m to 5.48 million units (annualized). Some payback was expected in existing home sales after an unexpectedly strong showing in January despite rising mortgage rates. Although sales declined, home prices rose 7.7% on a yearon- year basis, up from 6.4% y/y growth in the prior month. Home price growth was once again driven by a lack of inventory. While our outlook for the economic fundamentals driving the housing market remains optimistic, a persistent lack of supply could reduce affordability and act as a material headwind to the housing market.

In an environment of elevated policy uncertainty, every data point and every word uttered by policymakers seems to matter more to markets. Later today the U.S. congress will vote on a bill to amend the Affordable Care Act (ACA) that is likely to have market implications. If the bill passes, it moves onto the Senate. However, if today's vote fails, President Trump has threatened to leave the ACA unchanged, and in so doing reneging on one of his core campaign promises to repeal and replace it.

CANADA - MIND THE BUDGET GAP

'Tis the season for budgets, and the most anticipated one of them all (the federal Budget) was tabled on Wednesday of this week. The federal government is projecting larger deficits over the medium-term to push its spending agenda along.

The federal government embarked on a pretty aggressive spending plan last year and estimates of the medium-term deficit have been creeping up since. That deficit is expected to reach $28.5 billion in fiscal year (FY) 2017-18, or 1.3% of GDP and is now projected to be between $5 and $7 billion dollars higher per year over the medium-term than expected in Budget 2016. In fact, the government anticipates to still be running a deficit of $18 billion (0.8% of GDP) by 2021.

In large part, the higher deficit projections reflect more cautious economic assumptions. Still, the government opted not to introduce major revenue generating measures to help fill the gap. There were a few small items, such as raising taxes on alcohol and cigarettes, removing the public transit tax credit and applying the GST to Uber rides, but nothing that will substantially move the needle on revenues. Rather, the federal government added a few more investment dollars to its spending plan for hot-topic issues such as parental leave, affordable housing and skills and innovation. Funding for most of the new initiatives introduced in this budget however, has been shuffled out of prior planned projects and will only add a cumulative $4.8 billion to the deficit between fiscal years 2016-17 and 2020-21.

The course of action in this week's wait-and-see budget may be appropriate. The Canadian economy may prove a bit stronger in the near-term than what has been baked into this budget, which could give just a bit of a nudge to near-term revenues. This week's retail sales report was yet another sign that the Canadian economy is gathering considerable momentum in 2017. Retail sales were up 2.4% in January, the sharpest monthly gain in almost seven years. More importantly, motor vehicle and parts (+3.8% m/m) drove the gain, highlighting that Canadians are feeling confident in their future employment prospects. TD Economics is forecasting nominal GDP growth of 4.7% in 2017, compared to the federal government's more cautious estimate of just 4.1%. At the same time, the timing might not be right for restrictive fiscal policy given the extensive risks facing Canada and the global economy.

One of the key risks remains in the government's longterm interest rate outlook. This week's soft consumer price report showed that all of the Bank of Canada's measures of inflation are running below the 2% target, underscoring the view that the central bank will remain on hold at least until next year. However, TD Economics believes that ongoing Federal Reserve hikes could pull up the 10-year Government of Canada bond yield by 30 to 40 basis points in 2017 and 2018 above the Budget 2017 assumptions.

Still, while deficits remain on the horizon, the debt-to- GDP ratio is not expected to breach 30% over the forecast plan. This is quite low from a historical perspective, at half the peak reached in the late 1990's, leaving some fiscal room to work down the deficit only gradually.