Sample Category Title

Weekly Focus: UK Finally Filing for Divorce

Market movers ahead

- Comments from the last FOMC meeting indicated that the Fed will be willing to let inflation slightly overshoot the 2% target. Thus, we expect the PCE core inflation figures on Friday to attract special interest. We expect an increase of 0.2% m/m, implying 1.7% y/y.

- In the euro area, we are due to get HICP inflation figures for March. We believe headline inflation will decline to 1.6%, partly as the energy price inflation support starts to wear off. We also look for a small increase in the German IFO expectations, as other surveys still indicate optimism in the business economy.

- In the UK, we look for the Article 50 trigger on Wednesday and the EU's Brexit guidelines, which should be published within 48 hours of Article 50 being triggered.

Global macro and market themes

- We see an increasing risk of a market correction.

- We see less support for risk sentiment, as we are close to a peak in global PMIs and the risk of Donald Trump disappointing the markets is increasing.

- Monetary policy is set to stay accommodative in both the US and Europe.

- Changes to US economic policy are likely to come later and be smaller than previously expected.

- In our view, the risk of US military conflict with North Korea is rising.

Canadian Inflation Little Changed at 2% in February

- The year-over-year rate of headline CPI inflation edged down to 2.0% from 2.1% in January. The reading fell slightly short of market expectations for an unchanged 2.1% rate but inflation continues to track above the Bank's Q1/17 forecast of 1.8%.

- The rate of energy price inflation was little changed at 12% as the drop in energy prices in February (including gasoline -5%) was similar to the dip seen a year ago.

- Food prices were 2.3% lower than a year ago when exchange-rate-driven increases in some food prices were most intense. This continues the most significant period of food price deflation in more than two decades, though base effects should see the pace of decline softening going forward.

- Excluding food and energy, consumer prices were up 2.0% year-over-year after January's rate (2.2%) was the fastest since 2007.

- The Bank of Canada's three new core measures averaged 1.6% in February for a fourth consecutive month (after rounding). CPI-Common, remaining at its lowest level in two decades (1.3%), is somewhat out of sync with the other two measures which are closer to their longer-run averages.

Our Take:

After an upside surprise on inflation in January, today's report was a bit more ho-hum as the annual rates of headline inflation and major components (food, energy, and core) were all little changed in February. All items CPI is tracking above the Bank of Canada's latest forecast but that largely reflects transitory factors (namely energy prices) that the Bank said they were "looking through" in March's policy statement. Meanwhile, their new core measures, all of which remained below 2%, will likely continue to be cited as evidence of excess capacity in the economy. There has been some evidence of firming in other core measures - ex food and energy inflation is running at 2% and prices for services ex shelter, a gauge of domestic price pressure, have picked up in the last two months. That said, today's report fits with the Bank's narrative on slack in the economy, and given heightened uncertainty regarding US policy, we doubt their neutral tone will change much at April's meeting despite the solid run of data we've seen in recent months.

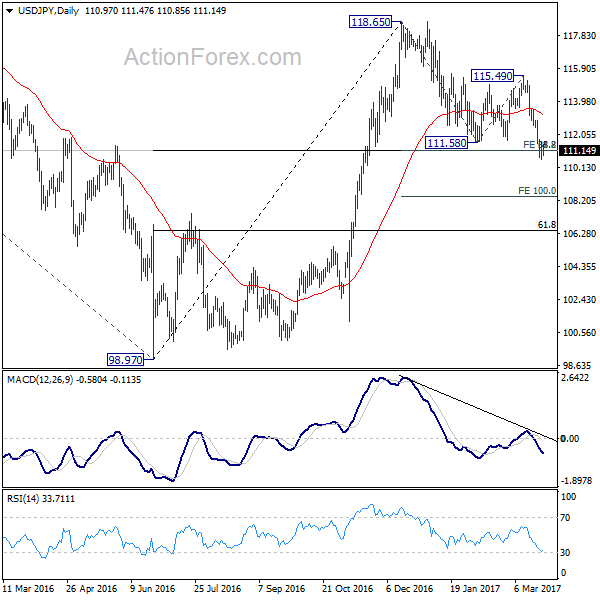

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.50; (P) 111.03; (R1) 111.45; More...

Intraday bias in USD/JPY stays neutral as it continues to struggle around 111.12/13 support. At this point, we're still favoring the case for strong support around 111.12/13 to bring rebound. This level represents 61.8% projection of 118.65 to 111.58 from 115.49 at 111.12 and 38.2% retracement of 98.97 to 118.65 at 111.13. Break of 112.86 resistance will indicates completion of the correction from 118.65. In such case, intraday bias will be turned back to the upside for 115.49 resistance and above. However, sustained trading below 111.12/13 will pave the way to 100% projection at 108.42 next.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Nonetheless, sustained trading below 55 week EMA (now at 111.12) will extend the consolidation from 125.85 with another fall through 98.97 before completion.

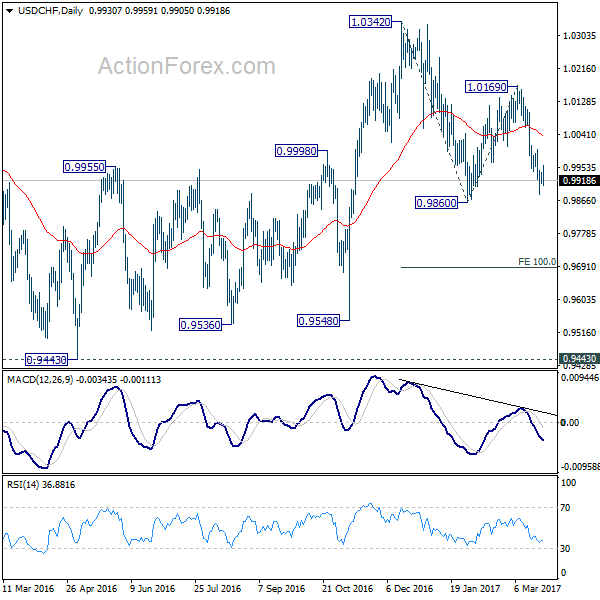

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9915; (P) 0.9928; (R1) 0.9946; More.....

Intraday bias in USD/CHF remains neutral for consolidation above 0.9881 temporary low. Deeper decline is in favor as long as 1.0002 minor resistance holds. Break of 0.9860 near term support will extend the whole fall from 1.0342 towards 100% projection of 1.0342 to 0.9860 from 1.0169 at 0.9687. However, break of 1.0002 will argue that fall from 1.0169 is finished and will turn bias back to the upside for this resistance instead.

In the bigger picture, USD/CHF is staying in medium term sideway pattern between 0.9443/1.0342. In any case, decisive break of 1.0342 resistance is needed to confirm underlying strength. Otherwise, we'll stay neutral in the pair first. In case of another fall, we'd expect strong support from 0.9443/9548 support zone.

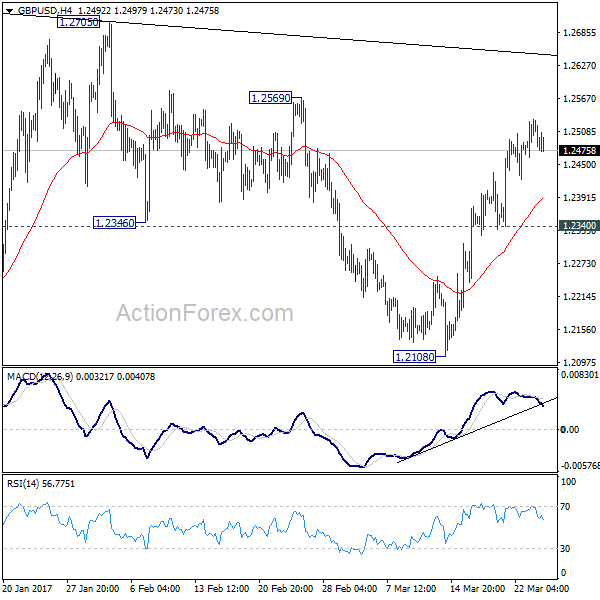

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2478; (P) 1.2505; (R1) 1.2547; More...

GBP/USD continues to lose upside momentum as seen in 4 hour MACD. But at this point, further rise is still expected with 1.2340 minor resistance holds. Above 1.2569 will target 1.2705/74 resistance zone. Price actions from 1.1946 are seen as a consolidation pattern. Hence, we'd expect strong resistance from 1.2705/2774 to limit upside and bring down trend resumption. On the downside, break of 1.2340 support will turn bias back to the downside for 1.2108 support. Though, sustained break of 1.2774 will extend the rise towards 1.3444 key resistance level.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

Canada: Inflation Edges Down, Core Measures Still Soft

Canadian consumer prices rose 2.0 % (year-on-year) in February, decelerating from 2.1% in January. Prices were up 0.2% month-on-month (on par with consensus). On a seasonally adjusted basis, prices fell an estimated 0.2% month-on-month.

Once again energy was the main source of price pressures. Despite a 0.8% decline on a month-on-month basis, relative to a year ago, transportation costs were up 6.6% on the month, up from 6.3% in January.

Partially offsetting higher energy prices, food prices continue to decline. Food prices were down 2.3% year-on-year in February (from 2.1% previously), mainly due to falling prices for fresh vegetables, which were down 14%.

Core inflation measures remained benign: CPI-common and CPI-median were both unchanged at 1.3% and 1.9% respectively, while CPI-trim edged down to 1.6% (from 1.7% previously). All core measures are year-on-year.

Key Implications

Not much to report here in terms of inflation in Canada. Headline inflation looks likely to remain close to 2.0% over the next several months, and with energy prices relatively stable, is likely to decelerate modestly through the second half of this year.

Market expectations for rate hikes from the Bank of Canada have moved up in recent months, following rate hikes in the United States. However, with soft inflation and messaging from Bank of Canada officials that the Canadian economy remains in excess supply, investors may be over pricing the chance of a rate hike. Consistent with gradual absorption of economic slack, we do not expect the central bank to step off the sidelines until well into 2018.

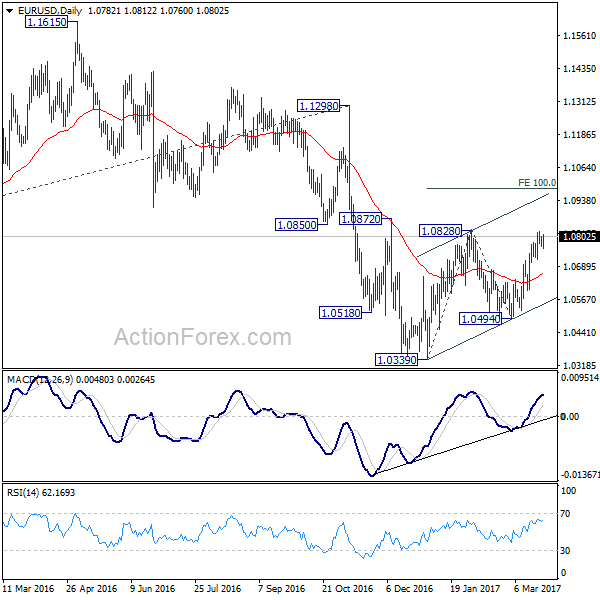

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0766; (P) 1.0785 (R1) 1.0804; More.....

Intraday bias in EUR/USD remains neutral as consolidation from 1.0824 temporary top continues. Further rise remains in favor as long as 1.0718 minor support holds. Break of 1.0828 resistance will extend the rise from 1.0339 to 100% projection of 1.0339 to 1.0828 from 1.0494 at 1.0983. However, as rise from 1.0339 is seen as a corrective move. We'd expect upside to be limited by 1.0983 to complete the correction. On the downside, break of 1.0718 minor support will turn bias to the downside for 1.0494 support first.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to resume later. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115.

Euro Lifted by PMIs, Dollar Recovered as Health Care Vote Awaited

Euro trades broadly higher today as lifted by solid PMI data. Meanwhile, the greenback also follows even though markets are facing uncertainty on health care vote in House. US president Donald Trump has issued his ultimatum to House Republicans that if the American Health Care Act is not passed today, he will move on to other priorities and leave Obamacare alone. The vote is seen as an important litmus test on Trump's ability to push through his initiatives. Released in US session, US durable goods orders jumped 1.7% in February versus expectation of 1.2%. But ex-transport orders rose 0.5% only. From Canada, headline CPI slowed to 2.0% yoy in February, below expectation of 2.1% yoy. CPI core common came in at 1.9% yoy, median at 1.9% yoy, trimmed at 1.6% yoy.

Eurozone PMI composite hit near six year high

Eurozone PMI manufacturing rose to 56.2 in March, up from 55.4 and beat expectation of 55.3. Eurozone PMI services rose to 56.5, up from 55.5 and beat expectation of 55.3. PMI composite rose to 56.7, hitting the highest level in six years since April 2011. Markit noted that "the acceleration in growth towards the end of the quarter, as well as improving trends in new business and an increased appetite to hire, suggest that strong growth momentum will be sustained into the second quarter."

Germany PMI manufacturing rose to 58.3, up from 56.8, beat expectation of 56.5. German PMI services rose to 55.6, up from 54.4 and beat expectation of 54.5. France PMI manufacturing rose to 53.4, up from 52.2 and beat expectation of 52.4. France PMI services rose to 58.5, up from 56.4, beat expectation of 56.1. Also from Europe, UK BBA mortgage approvals dropped to 42.6k in February.

ECB chief economist Peter Praet said that policy makers are "more confident on growth". However, "economic outlook is still conditional on maintaining a substantial degree of monetary accommodation. Talks about exit are premature." Praet also said that the forward guidance has served the central bank well. Meanwhile, he noted that "Brexit is regrettable and harmful, but it is also an opportunity for the banking union."

Japan manufacturing PMI missed expectations

Japan PMI manufacturing dropped to 52.6 in March, down from 53.3 and missed expectation of 53.5. Markit noted that "although signaling a slower rate of expansion during March, the latest PMI data again point to a Japanese manufacturing economy expanding at a decent clip." And, "new order books remain in solid growth territory, with gains seemingly supported by the weaker yen." Nonetheless, "this comes at the cost of ongoing marked rises in purchase costs: input price inflation remained close to a two-year high in March."

New Zealand trade deficit narrowed to NZD -18m in February but missed expectation of NZD 160m surplus. For the 12 months through February, trade deficit was at NZD 3.794b, the worst figure in nearly nine years.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0766; (P) 1.0785 (R1) 1.0804; More.....

Intraday bias in EUR/USD remains neutral as consolidation from 1.0824 temporary top continues. Further rise remains in favor as long as 1.0718 minor support holds. Break of 1.0828 resistance will extend the rise from 1.0339 to 100% projection of 1.0339 to 1.0828 from 1.0494 at 1.0983. However, as rise from 1.0339 is seen as a corrective move. We'd expect upside to be limited by 1.0983 to complete the correction. On the downside, break of 1.0718 minor support will turn bias to the downside for 1.0494 support first.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to resume later. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Feb | -18M | 160M | -285M | -257M |

| 21:45 | NZD | Exports (New Zealand dollars) Feb | 4.01b | 4.20b | 3.91b | |

| 00:30 | JPY | PMI Manufacturing Mar P | 52.6 | 53.5 | 53.3 | |

| 08:00 | EUR | France Manufacturing PMI Mar P | 53.4 | 52.4 | 52.2 | |

| 08:00 | EUR | France Services PMI Mar P | 58.5 | 56.1 | 56.4 | |

| 08:30 | EUR | Germany Manufacturing PMI Mar P | 58.3 | 56.5 | 56.8 | |

| 08:30 | EUR | Germany Services PMI Mar P | 55.6 | 54.5 | 54.4 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Mar P | 56.2 | 55.3 | 55.4 | |

| 09:00 | EUR | Eurozone Services PMI Mar P | 56.5 | 55.3 | 55.5 | |

| 09:30 | GBP | BBA Mortgage Approvals Feb | 42.6K | 44.9K | 44.7K | 44.1K |

| 12:30 | CAD | CPI M/M Feb | 0.20% | 0.20% | 0.90% | |

| 12:30 | CAD | CPI Y/Y Feb | 2.00% | 2.10% | 2.10% | |

| 12:30 | CAD | CPI Core - Common Y/Y Feb | 1.90% | 1.30% | ||

| 12:30 | CAD | CPI Core - Median Y/Y Feb | 1.90% | 1.90% | ||

| 12:30 | CAD | CPI Core - Trim Y/Y Feb | 1.60% | 1.70% | ||

| 12:30 | USD | Durable Goods Orders Feb P | 1.70% | 1.20% | 2.00% | |

| 12:30 | USD | Durables Ex Transportation Feb P | 0.50% | 0.70% | 0.00% |

Markets Tense ahead of Delayed Healthcare Vote

The mounting anticipation ahead of the delayed healthcare vote later today has created an unnatural calm across the financial markets with investors adopting a cautious approach. Asian shares concluded mostly mixed during early trading on Friday amid the subdued trading mood with the loss of appetite for risk limiting gains in Europe. Wall Street could come under pressure with participants on standby ahead of a critical healthcare bill that will assess Trump's administration's ability to push through legislations. While Trump has threatened that without a vote to the healthcare bill he will move on to other agenda's, markets may interpret a potential failure today as something that could create some headwinds for the pending tax reforms and infrastructure spending.

Gold awaits healthcare vote

The renewed protectionism concerns and Trump jitters have triggered risk aversion this week consequently attracting investors to safe-haven assets. In times of unease, Gold remains a trader's best friend and such was displayed on Thursday when the metal punched above $1253. Although prices have edged slightly lower on Friday amid a stabilizing Dollar, bulls remain somewhat in control on the daily charts above $1225. Much attention will be directed towards the pending healthcare vote this evening which could create further uncertainty if the bill is rejected. With the growing threat of a rejection of the healthcare bill raising doubts over Trump's ability to move forward with the pro-growth policies, the uncertainty should redirect participants to Gold. From a technical standpoint, bulls need a solid break back above $1250 for a further incline higher towards $1260.

Commodity spotlight - WTI Crude

WTI Crude found itself slightly supported on Friday following reports of Saudi Arabia's production to the United States falling which offered a slight window for bulls to attack. Despite this new development, the oil markets remain under pressure as fears heighten over the global glut. Sentiment remains firmly bearish towards oil with further downside expected as the fading confidence over the effectiveness of OPEC's output cut encourages bears to install renewed rounds of selling. While speculations have heightened over OPEC extending the supply cuts by another six months, questions may be raised if such may stabilize the oil markets especially when factoring the resurgence of U.S Shale. From a technical standpoint, WTI remains heavily pressured on the daily charts. Bears remain in firm control below $50 with the next level of interest at $47.

Currency spotlight - EURUSD

The EURUSD has bounced back in style this month as the receding political risks in Europe rekindled appetite for the single currency. Technical traders will be paying very close attention to how prices react to the 1.0800 resistance with a breakout encouraging a further incline higher towards 1.0850. If economic data from Europe continues to display signs of stability and the Dollar weakens further, then the EURUSD could be poised for further upside in the short to medium term.

European Major PMI Manufacturing Data Beats Expectations to 6-Year Highs

Notes/Observations

- US healthcare vote back on; Trump said to have issued an ultimatum to leave Obamacare in place unless they pass new healthcare bill; political risk weighing on market participation

- Major European Manufacturing PMI extend further into expansion territory to multi-year highs

Overnight:

Asia:

- Japan Mar Preliminary Manufacturing PMI registers its 7th month of expansion (52.6 v 53.3 prior)

- BOJ chief Kuroda says "no reason" to withdraw stimulus now

Europe:-

- BOE Vlieghe stated that higher inflation did not mean any interest rate hike. Needed to see evidence of strong wage growth before considering voting for a rate rise

Americas:

- Fed's Kaplan (moderate, voter): 3 rate hike this year is reasonable baseline; could be faster or slow but not looking for a pause in hikes now

- Fed's Kashkari (dove, dissenting vote): - We're coming up short on our inflation mandate; Fed has powerful tools if inflation rises too fast

Energy:

- State Dept to approve Keystone pipeline permit Friday

Summary of Trump Healthcare Bill:

- Vote has been postponed to Friday morning (no set time)

- White House and GOP leadership said to have presented a 'final offer' on healthcare bill to the Freedom Caucus to either accept or reject. Freedom Caucus yet to give formal answer to this offer. White House reportedly offered to remove essential benefits from plans on the individual market

- Trump said to have issued an ultimatum to House Republicans that he will leave Obamacare in place unless they pass new healthcare bill - financial press

- White House: Freedom Caucus discussion was positive; does not say deal reached; moderate members will come to white house for talks; Trump has not asked house speaker Ryan to delay healthcare vote; ultimately expects to have votes to pass healthcare bill; confident the bill will pass in the morning

- President Trump: the healthcare bill vote is going to be very close; we have a chance

- Freedom Caucus Chair Meadows: still hopeful will get agreement on health care bill; Freedom Caucus has made reasonable requests. still not enough votes to pass health bill; plans to reach out to moderate Republicans in House to try to reach agreement; optimistic common ground will be found with enough Senators to pass a bill

- House Republican Leader McCarthy: there are not enough votes currently to pass healthcare bill; will start debate on house floor on healthcare bill on Friday morning

- White House spokesman Spicer: Trump is looking forward to a vote on the healthcare bill; have seen the numbers rising for 'yes' votes

Economic Data

- (NL) Netherlands Q4 Final GDP Q/Q: 0.6% v 0.5%e; Y/Y: 2.5% v 2.3%e

- (FR) France Q4 Final GDP Q/Q: 0.4% v 0.4%e; Y/Y: 1.1% v 1.2%e

- (FR) France Mar Preliminary Manufacturing PMI (beat): 53.4 v 52.4e (6th month of expansion), Services PMI: 58.5 v 56.1e, Composite PMI: 57.6 v 55.8e

- (CZ) Czech Mar Business Confidence: 13.1 v 15.2 prior; Consumer Confidence: 6.3 v 5.8 prior

- (DE) Germany Mar Preliminary Manufacturing PMI (beat): 58.3 v 56.5e (28th month of expansion and highest since Apr 2011), Services PMI: 55.6 v 54.5e, Composite PMI: 57.0 v 56.0e

- (EU) Euro Zone Mar Preliminary Manufacturing PMI (beat): 56.2 v 55.3e (45th month of expansion and highest since Apr 2011), Services PMI: 56.5 v 55.3e, Composite PMI: 56,7 v 55.8e

- (UK) Feb BBA Loans for House Purchase (miss): 42.6K v 44.9Ke

- Fixed Income Issuance:

- (ZA) South Africa sold total ZAR650M vs. ZAR650M indicated in I/L 2029, 2033 and 2050 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Index snapshot (as of 09:20 GMT)

Indices [Stoxx50 -0.3% at 3,442, FTSE -0.1% at 7,336, DAX flat at 12,035, CAC-40 -0.3% at 5,017, IBEX-35 -0.4% at 10,288, FTSE MIB -0.2% at 20,134, SMI -0.2% at 8,613, S&P 500 Futures +0.2%]

Market Focal Points/Key Themes: European equity indices are trading lower in the morning session as market participants remain jittery ahead of the highly anticipated vote on US President Trump's healthcare bill; Banking stocks generally lower across the board; shares of Allianz the laggard in the Eurostoxx after receiving an analyst downgrade; Commodity and mining stocks trading higher in the FTSE 100 as copper prices consolidate around intraday highs; Oil stocks lower as oil prices consolidate near intraday lows.

Upcoming notable scheduled US earnings (pre-market) include Finish Line, and REX American Resources.

Equities (as of 09:15 GMT)

- Consumer Discretionary: [IG Design IGR.UK +9.3% (trading update)]

- Financials: [Credit Suisse CSGN.CH +0.8% (revises Q4 Net loss, annual report), Allianz ALV.DE -1.4% (analyst downgrade)]

- Healthcare: [Biotest BIO.DE -8.8% (ImmunoGen has elected not to exercise its late stage co-development option for the US-Market with Biotest's antibody-drug conjugate (BT-062)), PureTech Health PRTC.UK +4.4% (Novartis licensing agreement)]

- Industrials: [FACC FACC.AT +0.1% (prelim FY16 results)]

- Technology: [Smiths Group SMIN.UK +3.9% (H1 results)]

Speakers

- ECB's Praet (Belgium, chief economist) reiterated view that Euro Area was doing better and that deflation risk was gone. Reiterated view that talks of exit from accommodative measures was premature as labor market had more slack than what jobs data showed. Italy's low growth showed acute structural problems and any return to ITL currency (Lira) for Italy would not solve the country's problem

- France Fin Min Sapin reiterated view that conditions were in place for budget deficit to GDP ratio to move below 3.0% in 2017

- Germany Fin Min Schauble reiterated view that pumping more money into Europe was the wrong message

- EU's Juncker reiterated view that UK Brexit bill will be around £50B

- EU's Dombrovskis reiterated EU Commission view that Italy needed to bring its debt level down; country needed to ensure 0.2% budget correction

- Italy Fin Min Padoan stated that its domestic economic and inflation situation was improving

- Sweden Central Bank (Riksbank) Business Survey: Industrial activity stronger than expected. Companies saw the coming six months economic activity would remain good, although there was some concern over political developments abroad

- Moody's affirmed New Zealand sovereign rating at AAA; outlook stable

Currencies

- FX price action and risk outlook hinging on President Trump looming healthcare vote. Political risk weighing on participation as time was running out to get votes for the Republican plan to repeal and replace "Obamacare"

- EUR/USD was back above 1.08 level aided by the major European Manufacturing PMI as it extended further into expansion territory to multi-year highs

- GBP/USD was slightly lower in quiet trade hovering below the 1.25 level.

- USD/JPY moved off Thursday's low to stay above the 111 level in the session.

Fixed Income:

- Bund futures trade at 159.98 down 4 ticks retracing the bulk of the earlier losses with stronger preliminary PMI data out of Europe coming ahead of estimates with the highest reading recorded since April 2011. Resistance remains at 160.45 followed by 160.66. Support moves to 159.41 then contract low of 158.73.

- Gilt futures trade at 126.36 down 4 ticks, off the 126.05 session low, with weakness in Equities pushing futures higher during the session. Support moves to 125.80 followed by 125.47. Resistance moves to 126.85 then 127.35 followed by 127.89. Short Sterling futures trade flat to 1bp with Jun17Jun18 spread widening to 23/23.5Bp.

- Friday's liquidity report showed Thursday's excess liquidity rose to €1.336B a rise of €7B from €1.329T prior. Use of the marginal lending facility rise to €283M from €232M prior.

- Corporate issuance saw no deals priced with weekly issuance at $20.8B at the low end of analysts estimates.

For the week ending Mar 22nd Lipper US fund flows reported IG net inflows $5.2B bringing YTD inflows to €35.1B, High Yield Bonds saw inflows of $736M bringing YTD outflows to €5.69B.

Looking Ahead

- (US) House of Representatives vote on Healthcare Bill (no set time)

- 06:00 (EU) Daily Euribor Fixing

- 06:00 (FR) France Debt Agency (AFT) announces upcoming Bill/Oat auctions

- 06:30 (RU) Russia Central Bank (CBR) Interest Rate Decision: Expected to leave Key 7-Day Auction Rate unchanged at 10.00%

- 07:00 (UK) DMO to sell combined £2.0B in 1-month, 3-month and 6-month bills (£0.5B, £0.5B and £1.0B respectively)

- 07:30 (IS) Iceland cancels Bonds

- 07:30 (IN) India Weekly Forex Reserves

- 07:45 (US) Daily Libor Fixing

- 08:00 (CL) Chile Feb PPI M/M: No est v 0.9% prior

- 08:00 (US) Fed's Evans speaks at Community Development Event

- 08:00 Russia Central Bank (CBR) Gov Nabiullina to hold post rate decision press conference

- 08:30 (US) Feb Preliminary Durable Goods Orders: 1.3%e v 2.0% prior; Durables Ex-Transportation: 0.6%e v 0.0% prior; Capital Goods Orders (Non-defense ex aircraft): +0.5%e v -0.1% prior, Capital Goods Shipments (non-defense/ex-aircraft): +0.3%e v -0.4 prior; Ex-Defense: No est v 1.5% prior

- 08:30 (CA) Canada Feb CPI M/M: 0.2%e v 0.9% prior; Y/Y: 2.1%e v 2.1% prior; Consumer Price Index: No est v 129.5 prior

- 08:30 (CA) Canada Feb CPI Common Core Y/Y: No est v 1.3% prior; CPI Medium Core Y/Y: No est v 1.9% prior; CPI Trim Core Y/Y: No est v 1.7% prior

- 08:30 (US) Fed's Bullard to speak to Economic Club of Memphis

- 09:00 (ES) Spain Debt Agency (Tesoro) announces upcoming bond issuance

- 09:15 (UK) Baltic Dry Bulk Index

- 09:30 (BR) Brazil Feb Current Account: $0.0Be v -$5.1B prior; Foreign Direct Investment (FDI): $4.8Be v $11.5B prior

- 09:45 (US) Mar Preliminary Markit Manufacturing PMI: 54.7e 54.2 prior

- 10:00 (MX) Mexico Jan Retail Sales M/M: -0.6%e v -1.4% prior; Y/Y: 5.1%e v 9.0% prior

- 11:00 (EU) Potential European sovereign ratings after the close

- (CY) Cyprus Sovereign Debt to Be Rated by Moody's

- (DK) Denmark Sovereign Debt to be rated by Moody's

- (SA) Saudi Arabia Sovereign Debt to be rated by Moody's

- (LU) Luxembourg Sovereign Debt to be rated by DBRS

- 13:00 (FR) France Feb Net Change in Jobseekers: -10.0Ke v +0.8K prior; Total Jobseekers: 3.457Me v 3.468M prior

- 13:00 (US) Weekly Baker Hughes Rig Count data

- 13:00 (IT) Pope Francis meets EU Leaders before Rome Summit

- 15:00 (CO) Colombia Jan Economic Activity Index Y/Y: 0.6%e v 1.0% prior

- 15:00 (CO) Colombia Central Bank Interest Rate Decision: Expected to cut Overnight Lending Rate by 25bps to 7.00%