Sample Category Title

GBP/USD Risks Falling Back Under 1.25

'While GBP managed to make a 'fresh high' of 1.2532, the up-move is lacking in momentum. That said, the undertone is generally positive and GBP could continue to edge higher towards 1.2550.' – UOB Group (based on FXStreet)

Pair's Outlook

Thursday was a relatively productive day for the British Pound, as it successfully stabilised above the 1.25 mark. However, downside risks are now higher, due to this major level being a tough psychological resistance, which tends to trigger U-turns lately, despite being crossed to the upside. As a result, the Cable could be seen undergoing a bearish correction today, with the monthly PP being a solid obstacle where support might be found. A much sharper decline is also possible, in which case the 55 and the 100-day SMAs are to limit the losses circa 1.24. Nevertheless, the GBP/USD is expected to continue recovering until the 1.27 handle is reached within the next month.

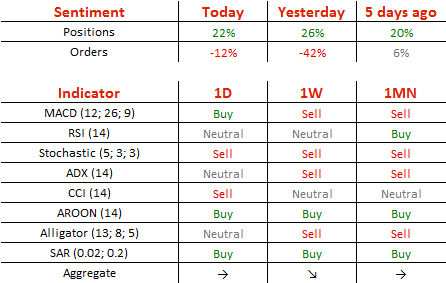

Traders' Sentiment

Traders' sentiment remains bullish, but now at 61% (previously 63%). The number of orders to sell the Sterling slid from 71 to 56%.

USD/JPY Attempts To Reverse Polarity

'U.S. yields are higher and it's not hard for dollar/yen to attract bids. It is often overlooked but the dollar continues to enjoy underlying support from widening U.S.-Japanese interest rate spreads.' – State Street Bank and Trust (based on Reuters)

Pair's Outlook

The US Dollar slid against the Japanese Yen again yesterday, failing to find support at the 111.00 major level, which was expected to trigger a rebound. Nevertheless, the USD/JPY pair has the opportunity to reverse momentum today and being recovering from its nearly 400 pips slump over the last eight days. Despite the possible rally, gains are likely to be very limited, with the 111.60 mark expected to be the ceiling. On the other hand, if US President Trump manages to broker a deal concerning the new healthcare system today, the Greenback will have the potential to even retake the weekly S1 at 111.78.

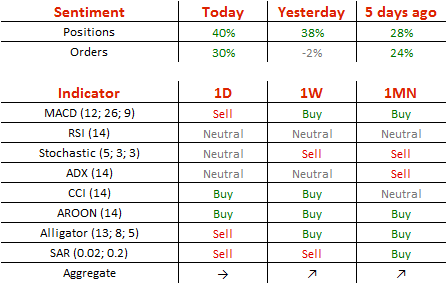

Traders' Sentiment

There are 70% of traders holding long positions today, compared to 69% on Thursday. Meanwhile, there are 65% of pending orders to purchase the Buck, up from 49% yesterday.

Gold Fluctuates Near 1,245 Mark

'If the (healthcare) vote is to pass the reforms, gold could face pressure. But, if it encounters problems, we might chase a previous high at around $1,260.' – Reuters

Pair's Outlook

The yellow metal traders are expecting the fundamentally important vote on US healthcare, which will reveal, whether Donald Trump can get legislation passed. Due to that reason the bullion bounced around the 1,245 mark on Friday morning. From a technical perspective the commodity price is squeezed in between the weekly R1 at 1,242.38 and the 50.00% Fibonacci retracement level at 1,248.96, which is enforced by the long term downward trend line at 1,250.12. Due to this trend line it can be assumed that the legislative bill will not be passed. However, it might as well be easily broken, and market participants should stay vigilant.

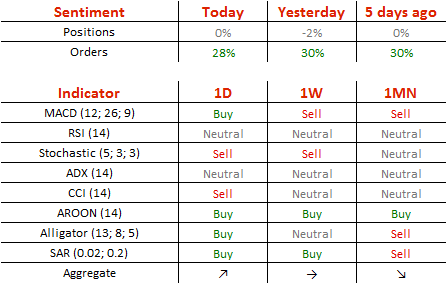

Traders' Sentiment

Trader open positions are once more neutral on the metal. However, 64% of orders are set to buy the bullion.

AUDUSD – Pullback May Pause At Daily Cloud Top

The Aussie holds in red for the fourth straight day and probed below strong supports at 0.7623/18 (top of ascending daily cloud / sideways-moving daily Kijun-sen).Dips were so far contained by 4-hr cloud base at 0.7604.

Firm break here would generate stronger bearish signal for deeper correction of 0.7489/0.7747 upleg, as the pair is on track for strong bearish weekly close.

Daily studies are moving into bearish mode and together with negative near-term technicals maintain downside risk.

However, the price may show hesitation at these supports as slow stochastic is reversing on 4-hr chart and entering oversold territory on daily.

While strong near-term bearish sentiment persists, we expect limited upside action, with focus still at lower targets at 0.7588 (Fibo 61.8% of 0.7489/0.7747) and more significant 0.7543 (200SMA / weekly cloud top).

Return above broken 10SMA (0.7653) would ease immediate bearish pressure, while sustained break above 0.7700 barrier is needed to confirm reversal.

Res: 0.7640, 0.7653, 0.7682, 0.7700

Sup: 0.7604, 0.7588, 0.7543, 0.7506

USDJPY – Weekly Cloud Top Delays Bears

The pair moved higher on Friday after hitting fresh low at 110.61 the day before, so far unable to firmly break into thick weekly cloud that counteract broader bears (USDJPY left 8 consecutive bearish daily candles on steep descend from 115.49).

Bounce is seen as corrective ahead of fresh extension lower that eyes psychological 110.00 support, however, correction may extend as bullish signal is generating on daily chart slow stochastic reversal from oversold territory.

In addition, today’s close above weekly cloud top (111.36) would generate another bullish signal.

Solid barriers lay at 111.60 (former base) and (111.97 (broken Fibo 38.2% of larger 101.17/118.65 ascend), where upticks should be ideally capped.

Otherwise, extended correction could be anticipated on break above 111.97 and 112.47 (Fibo 38.2% of 115.49/110.61 downleg).

Res: 111.36, 111.60, 111.97, 112.47

Sup: 110.84, 110.61, 110.25, 110.00

Forex Technical Analysis

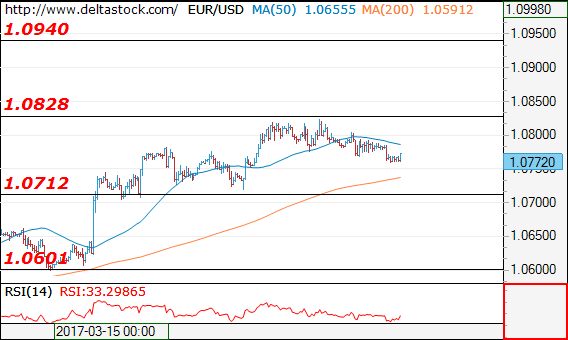

EUR/USD

Current level - 10772

The outlook remains positive, for a break through 1.0828, towards 1.0940 resistance mark. Crucial on the downside is 1.0712 low.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.0828 | 1.0870 | 1.0712 | 1.0600 |

| 1.0870 | 1.0945 | 1.0600 | 1.0490 |

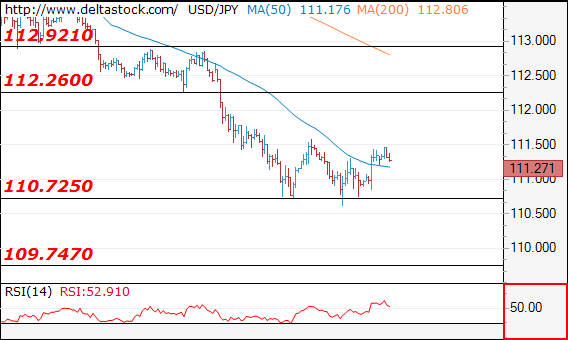

USD/JPY

Current level - 111.27

The rebound above 110.70 is corrective and the overall outlook remains bearish, for a slide towards 109.75 target area. Key resistance lies at 112.26.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 112.26 | 113.50 | 110.72 | 109.75 |

| 112.90 | 115.65 | 109.75 | 107.80 |

GBP/USD

Current level - 1.2487

The overall outlook is bullish, for a tight test of 1.2570 and even 1.2620. Initial support lies at 1.2425 and crucial on the senior frames is 1.2335

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2570 | 1.2570 | 1.2425 | 1.2107 |

| 1.2620 | 1.2705 | 1.2335 | 1.1984 |

GBPUSD – Hourly Cloud Holds Dips For Now, Overall Picture Is Bullish

Cable pulled back from Thursday's fresh one-month high at 1.2529, with dips being so far contained by thick hourly Ichimoku cloud (spanned between 1.2479/26).

Strong overall bullish stance was boosted by Thursday's close above 1.2476 (Fibo 61.8% of 1.2704/1.2107 downleg), keeping targets at 1.2563/69 (Fibo 76.4% of 1.2704/1.2107 / 24 Feb high) in near-term focus.

Overbought slow stochastic on daily chart suggests that correction may extend, but no firmer bearish signal seen so far.

Broken 100SMA (1.2412) and top of daily cloud (1.2404) mark strong supports which are expected to contain extended dips.

Res: 1.2518, 1.2529, 1.2568, 1.2580

Sup: 1.2472, 1.2426, 1.2412, 1.2404

EURUSD – Daily Tenkan-Sen To Hold Corrective Dips Before Bulls Resume

The Euro extends pullback from 1.0823 high on Friday and seen poised for further easing, as reversed slow stochastic on daily chart shows plenty of room downside.

The move is seen as correction ahead of fresh push higher as underlying trend remains bullish and the pair being on track for the fourth consecutive bullish weekly close.

Dips should be ideally contained above 1.0711 (daily Tenkan-sen, also near Fibo 38.2% of 1.0493/1.0823 upleg at 1.0697) to keep bullish structure intact.

Regain of 1.0827 target (02 Feb high / Fibo 38.2% of larger 1.1614/1.0339, May 2016 / Jan 2017 descend) would signal possible attack at 200SMA (currently at 1.0881).

Additional support is seen on weekly close above the neckline of asymmetric inverse H&S pattern on daily chart (1.0778) which was dented but without firm break higher so far.

Alternatively, break below 1.0700 handle would risk deeper correction and unmask daily Kijun-sen / daily cloud top at 1.0658/45.

Today's focus is on vote on US healthcare plan that was postponed from Thursday.

Res: 1.0803, 1.0827, 1.0881, 1.0950

Sup: 1.0759, 1.0711, 1.0697, 1.0658

Healthcare Vote To Decide On Next USD Move

Sunrise Market Commentary

- Rates: Vote on healthcare bill crucial for sentiment

We expect both eco data and Fed governors to be overshadowed by the vote on the new healthcare bill. Failure to push the bill through could signal problems ahead for his economic agenda and might falter markets' faith in the reflation trade. In that case, the US 10-yr yield might test 2.3% support. The reaction in case of a 'yes-vote' will probably be smaller. - Currencies: Healthcare vote to decide on next USD move

Yesterday, the dollar traded indecisively as uncertainty on the US healthcare vote weighed. An approval of the bill might trigger a relief rally of equities and of the dollar. However, we assume that more positive US news is needed to change the fortunes for the dollar in a sustainable way.

The Sunrise Headlines

- US stocks closed ended flat, as the vote on a bill to roll back Obamacare was delayed to today. Overnight, Asian risk sentiment is more positive as the Freedom Caucus said they would discuss an 'improved' bill proposal.

- Trump warned Republicans to pass a new healthcare bill or risk being stuck with Obamacare. The outcome of the vote is on a knife-edge having fractured his party and turned into a test of his ability to deliver on the rest of his agenda.

- BoJ Governor Kuroda said there is "no reason" to withdraw the bank's massive monetary stimulus now, or raise its bond yield targets, as inflation remains far from its 2% goal.

- Dallas Fed Kaplan said the central bank should roll off both MBS and Treasury holdings when it begins to let its balance sheet shrink. Kaplan also said that the median expectation for 3 rate increases in 2017 is a reasonable baseline.

- SF Fed Williams expects 3 or 4 times hikes this year. He would like to see a fed-funds rate that is 'half way' to its eventual resting level before beginning to wind down the balance sheet. That will probably be late this year.

- Growth at Japanese manufacturers softened to a three-month low in March as output and new orders increased at a slower rate. The preliminary PMI dropped to 52.6 last month, down from February's reading of 53.3

- Today's eco calendar contains EMU PMI data and US durable goods orders. Fed governors Evans, Bullard, Dudley and Williams are scheduled to speak.

Currencies: Healthcare Vote To Decide On Next USD Move

Healthcare vote to decide on next USD move

On Thursday, USD indecisiveness prevailed as markets waited whether the Trump administration would be able to pass a first vote to repeal Obamacare. USD/JPY traded with a slight negative bias and closed the session at 110.94 (from 111.16). EUR/USD finished the session at 1.0783 (from 1.0797). So, the dollar continued to hold up better against the euro than against the yen, with EUR/USD staying away from the key 1.0829/1.0874 resistance.

Overnight, markets see a rising chance that the changes to the healthcare Bill will get enough support from the House Freedom Caucus to pass the House vote. This supports risky assets (equities) in Asia.. USD/JPY is off yesterday's lows and trades again round 111.50. EUR/USD (1.0765/70 area) is also drifting cautiously south. The dollar rebound is supported a slight rise of US yields. Of course, the Trumpcare is no done thing yet.

The eco calendar contains two interesting reports. In EMU, PMI business confidence is expected slightly softer (55.8 in March from 56. After recent regional sentiment data, we put the risks for the EMU PMI on the downside of expectations. However, confidence remains at a healthy level. The US durable orders are expected to have risen 1.3% M/M, following a 2% M/M rise in January. We support the consensus view and have no arguments to deviate, but the report is very volatile in nature.

In a day-to-day perspective, the eco data (potentially softer EMU PMI and decent US durables) might be intrinsically USD supportive. However, the focus will be on the vote on Trump-care. An approval (most ‘likely' scenario?) might trigger a short-term relief rally in equities and the dollar. However, this rebound likely won't go far. The bumpy road ahead of the vote suggests more difficulties when other key issues (taxes etc) will be brought to Congress. So, more other USD positive news is needed to really call an end to the recent period of USD softness. A failure to pass the bill is USD negative with probably a confirmation of the downside break in USD/JPY. In that scenario, EUR/USD might go for a test of the 1.0829/74 area. A break is possible, but far from sure. We still doubt that the EUR/USD has really big upside potential if sentiment on risk were to turn outright negative

In a longer term perspective, we don't change our USD-constructive bias based on the eco fundamentals. However, this doesn't tell anything on the short-term momentum dynamics.

EUR/USD: topside blocked if Trump-care is to be approved?

EUR/GBP

Sterling extends gradual comeback, for now

Sterling remained well bid yesterday and EUR/GBP traded with a slightly negative bias going into the publication of the UK retail sales. The ONS February retail sales (1.4% M/M and 3.7% Y/Y) were stronger than expected. Sterling rallied further and EUR/GBP dropped to the low 0.86 area. Cable jumped to the 1.25+ area. However, the sterling rally ran into resistance even as the CBI retail data (published at noon) also suggested decent retail activity in March. Sterling is currently apparently more sensitive to (better than expected) price data, rather than activity data. EUR/GBP closed the session at 0.8612. Cable finished the day at 1.2521.

Overnight, BoE Vlieghe in a press article said that higher inflation didn't mean a rate increase. He wants evidence on strong wage growth before considering voting for a rate hike. Sterling is losing a few ticks this morning. Later today, only the BBA loans for Home Purchases are scheduled for release. Last week, sterling found a better bid after the early March decline. Some time ago, EUR/GBP cleared 0.8592 resistance, improving the MT technical picture. However, this week's (substantially) higher than expected UK inflation probably put a decent floor for sterling short-term. We changed our short-term bias on EUR/GBP from positive to neutral. Some further consolidation in the 0.85/0.88 area might be on the cards. Longer term, Brexit complications remain a potential negative for sterling, but this issue isn't in the spotlights right now. We are not convinced that the BoE will raise rates anytime soon, even not after this months' higher inflation data.

EUR/GBP: sterling remains well bid after higher UK inflation earlier this week

AUDUSD Showing First Signs Of A Completed Complex Correction, More Weakness In View

Aussie is currently making a sharp decline from around the 0.7749 level, where a possible top for wave C) of E may have been found. This sharp decline is a confirmation that the previous five wave rise within wave C) is completed and that a minimum three wave reversal may now be in the cards. At the moment we see price sharply declining into wave 3, that may extend its weakness towards the 0.7539 region.

AUDUSD, 4H