Sample Category Title

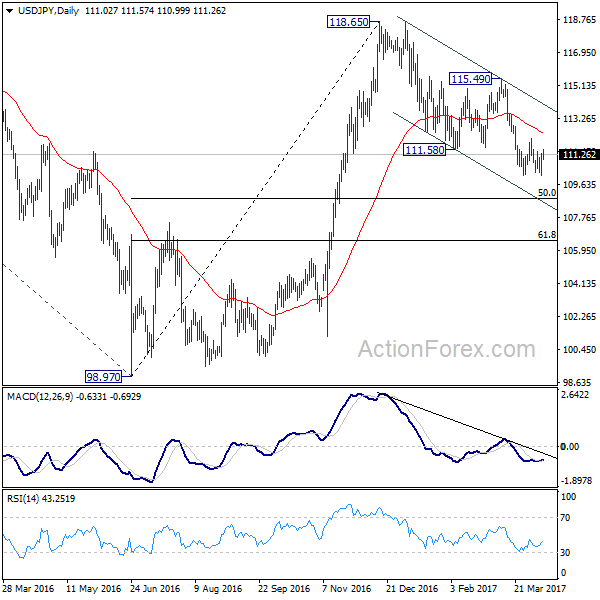

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.29; (P) 110.83; (R1) 111.57; More....

USD/JPY is bounded in range of 110.10/112.19 and intraday bias remains neutral first. The pair is staying in the near term falling channel and the correction from 118.65 could extend lower. Below 110.10 will turn intraday bias to the downside for 50% retracement of 98.97 to 118.65 at 108.81. On the upside, however, break of 112.19 resistance will indicate short term reversal and turn bias back to the upside for 115.49 resistance.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Nonetheless, sustained trading below 55 week EMA (now at 111.15) will extend the consolidation from 125.85 with another fall through 98.97 before completion.

EUR/USD Bullish Divergence at Strong Support

The EUR/USD has formed a bullish divergence at the confluence - POC. The POC 1.0535-60 (historical buyers, M L3, W L3, W L4, bullish divergence) is at the strong support indicated by camarilla pivot points. If 1.0500 stays strong the POC could reject the price towards 1.0618, 1.0650 and 1.0700. Have in mind that these are counter trend movements and the trend is still bearish. However due to a potential reversal at POC, the pair could reject towards above mentioned levels.

Canada: Home Construction Surges in March

Canadian housing starts surged more than 50k to 254k annualized units in March, or nearly 50k above expectations and the highest number in nearly a decade. The strong March number sent the 6-month moving average higher to 211k – the fastest pace since 2012.

Most of the uptick was related to the highly volatile multifamily units, which were 37k higher on the month. Single-family construction was largely flat, rising a mere 2k in March.

Looking across the country, the gains were broad based. British Columbia accounted for most of the March uptick, rising 17k to 44.7k, while Quebec (+12k to 53k) and the Prairies (up nearly 9k to 45.1k) were not far behind. Ontario also saw 5k more units being constructed, with the March tally at 88.8k. Atlantic Canada was the lone underperformer, down by 3k to 3.8k on weakness in Nova Scotia and Newfoundland & Labrador.

Toronto and Vancouver, the two most closely watched housing markets, saw the largest gains, up 17k (to 53k) and 12k (to 30k), respectively.

Key Implications

Despite some anticipated give back following two unusually warm months, March surprised to the upside, with builders breaking ground on the highest number of properties since 2007. This was particularly true on the multi-family segment, which accounted for most of the monthly gain.

The strength was particularly pronounced in Toronto and Vanouver, which have been the two hottest markets in recent quarters – despite some pullback in luxury segment sales in the latter market in recent months. The supply response in Toronto is particularly welcome, given the white hot pace of price growth and dearth of inventory on the market. The completion of these units should help take some steam out of Toronto's home price growth, although this won't happen overnight and is likely a story for next year and beyond.

The gains in the Prairies, while above expectations, corroborate a turning point for the region's economies, which are slowly recovering from a two-year recession, particularly in Alberta and Saskatchewan, while the weakness in Atlantic Provinces, while partly-weather related, appears in line with slowing population and economic growth across this region.

All in all, this was a great report, but the lofty number is unlikely to last into the coming months as the effects of the warm winter likely manifest in a slower pace of homebuilding during spring and summer months. This is especially the case given the likely slowdown in the volatile multifamily segment, which should come back down to earth in the coming months. Ultimately, we expect starts will settle just below 200k during the remainder of the year.

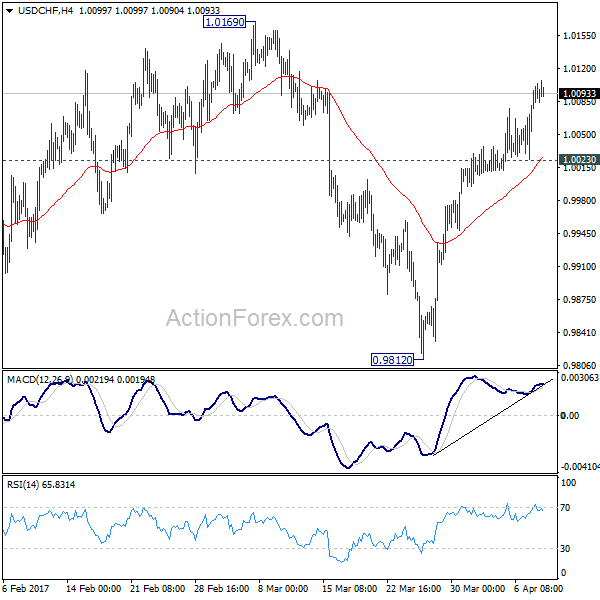

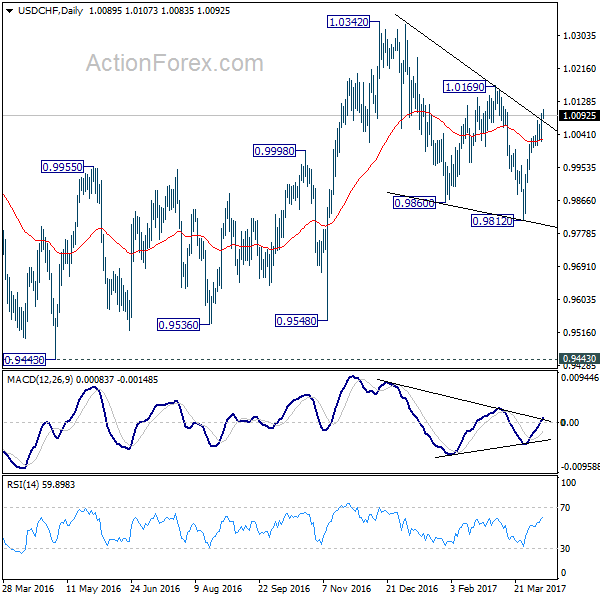

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.0043; (P) 1.0069; (R1) 1.0117; More.....

Intraday bias in USD/CHF remains on the upside as the rise from 0.9812 is still in progress. As noted before, corrective fall from 1.0342 should have finished with three waves down to 0.9812. Further rise should now be seen to 1.0169 resistance first . Decisive break there will confirm this bullish case and target 1.0342 key resistance next. On the downside, below 1.0023 minor support will turn bias neutral and bring consolidations before staging another rally.

In the bigger picture, we're still maintain that firm break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the cross. However, the corrective nature of the fall from 1.0342 to 0.9812 is starting to give the medium term outlook a bullish favor. Hence, in stead of looking for topping signal around 1.0342, we'd now pay closer attention to upside acceleration as USD/CHF approaches this level again.

Euro Lower on French Election News, Canadian Dollar Lifted by Oil Price

The Japanese Yen is trading as the weakest major currency today as it's paring back this month's gain. Canadian Dollar is so far the strongest one for the day as supported by strength in oil price. Dollar attempted to extend Friday's rally earlier today but no follow through buying in seen yet. Meanwhile, Euro is weighed down mildly by news on French presidential election. Overall, trading activity is quite subdued today as traders are probably starting preparing for holiday and long weekend ahead.

French election becomes a four-way match

In France, support for far left Jean-Luc Melenchon and conservative Francois Fillon jumped recently. That makes the presidential election in April and May a four-way match together with far right Marine Le Pen and centrist Emmanuel Macron. The latest Kantar Sofres poll published on Sunday showed that Macron and Le Pen tied for first with 24% support, Melenchon at 18% and Fillon at 17%. For the moment, anti-Euro Le Pen and pro-Euro Macron are still the favorites to enter into the run-off in May. And in that case, Macron is the favorite to win. However, the odds of Le Pen winning could jump if Fillon or Melenchon run the run-off with her. And, in that case, Frexit risk will also surge.

Released from Eurozone, Sentix investor confidence rose to 23.9 in April, up from 20.7, above expectation of 23.9.

BoJ concerned of Trump's trade policies

BoJ Governor Haruhiko Kuroda said at a quarterly meeting of regional branch managers that Japan's economy "continues to recover moderately as a trend". And he's optimistic that it would "turn into a moderate expansion". Meanwhile, he also reiterated his pledge to maintain ultra loose monetary policy until the 2% inflation target is hit. A report of the meeting noted that business plains could be affected by uncertainties over US President Donald Trump's trade balance. In particular, the reported noted a postponement of a metal product plant in Mexico even though there was no change in the investment plan in Japan. Also, there were growing concerns that US trade policies could affect exports and overseas production.

Released in Asian session, Japan economy watcher sentiment dropped to 47.4 in March. Current account surplus widened to JPY 2.12T in February. From Australia, home loans dropped -0.5% in February.

CAD strengthens as oil extends rally

Bank of Canada rate decision on Wednesday will be a major focus this week. BoC is widely expected to keep interest rate unchanged at 0.50%. The tone of the statement could remain slightly dovish in spite of improvements in economic data. Nonetheless, Canadian Dollar will likely follow more on oil prices as WTI crude oil could be heading back to 55.24 resistance due to geopolitical tensions. In addition, Libya's Sharara field halted production just one week after re-opening. Meanwhile, Russia Energy Minister Alexander Novak was reported saying that he's considering an extension of the OPEC-led production cuts by another six-month.

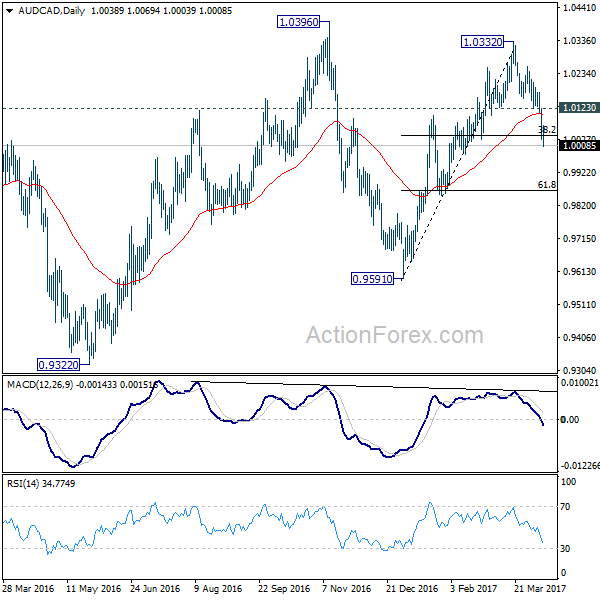

AUD/CAD to head lower to 0.9874 fibonacci level.

Canadian Dollar continues to enjoy much strength against Australian Dollar. As we mentioned back in the Daily Report on April 3, 1.0332 was confirmed to be a top and rise from 0.9591 is finished. The cross dropped through 38.2% retracement of 0.9591 to 1.0332 at 1.0049 as expected. And there is no sign of bottoming yet. Outlook in AUD/CAD will remains bearish as long as 1.0123 resistance holds. Current fall should extend to 61.8% retracement at 0.9874 and below. But overall, the cross is bounded in long term consolidation pattern start at 1.0784 (2012 high). And it stayed in range between 0.9148/1.0784 for more than five years. We're not seeing any clear long term trend yet.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.0043; (P) 1.0069; (R1) 1.0117; More.....

Intraday bias in USD/CHF remains on the upside as the rise from 0.9812 is still in progress. As noted before, corrective fall from 1.0342 should have finished with three waves down to 0.9812. Further rise should now be seen to 1.0169 resistance first . Decisive break there will confirm this bullish case and target 1.0342 key resistance next. On the downside, below 1.0023 minor support will turn bias neutral and bring consolidations before staging another rally.

In the bigger picture, we're still maintain that firm break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the cross. However, the corrective nature of the fall from 1.0342 to 0.9812 is starting to give the medium term outlook a bullish favor. Hence, in stead of looking for topping signal around 1.0342, we'd now pay closer attention to upside acceleration as USD/CHF approaches this level again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Current Account (JPY) Feb | 2.21T | 1.79T | 1.26T | |

| 01:30 | AUD | Home Loans Feb | -0.50% | 0.00% | 0.50% | 0.40% |

| 05:00 | JPY | Eco Watchers Survey Current Mar | 47.4 | 49.8 | 48.6 | |

| 08:30 | EUR | Eurozone Sentix Investor Confidence Apr | 23.9 | 21 | 20.7 | |

| 12:15 | CAD | Housing Starts Mar | 254K | 215.5k | 210.2k | 214K |

| 14:00 | USD | Labor Market Conditions Index Change Mar | 1.3 |

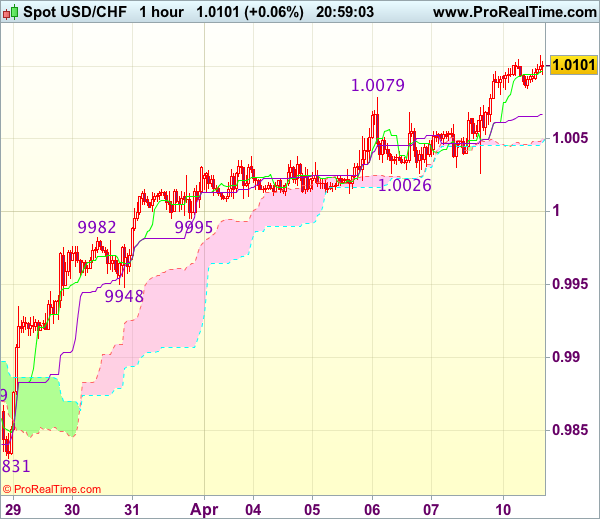

Trade Idea Update: USD/CHF – Buy at 1.0030

USD/CHF - 1.0094

Original strategy :

Buy at 1.0030, Target: 1.0130, Stop: 0.9995

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0030, Target: 1.0130, Stop: 0.9995

Position : -

Target : -

Stop : -

The greenback has maintained a firm undertone after Friday’s rally, adding credence to our bullish view that recent upmove from 0.9813 is still in progress and upside bias remains for this move to extend further gain to previous resistance at 1.0109, then towards 1.0140-45, however, loss of upward momentum should prevent sharp move beyond another previous resistance at 1.0171, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy dollar on pullback as support at 1.0026 should limit downside. Below minor support at 0.9995 would defer and suggest top is possibly formed, risk correction to 0.9960 but support at 0.9948 should hold from here.

Trade Idea Update: GBP/USD – Sell at 1.2450

GBP/USD - 1.2404

Original strategy :

Sell at 1.2450, Target: 1.2350, Stop: 1.2485

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.2450, Target: 1.2350, Stop: 1.2485

Position : -

Target : -

Stop : -

As the British pound found good support around 1.2365-66 and has recovered, suggesting consolidation above this level would be seen an above the Kijun-Sen (now at 1.2418) would bring recovery towards 1.2450-55 before prospect of another decline, below said support at 1.2365-66 would extend recent decline from 1.2616 to 1.2350, then towards 1.2325-30 but near term oversold condition should limit downside and reckon 1.2300 would hold from here.

In view of this, would not chase this fall here and would be prudent to sell cable on recovery as 1.2450-60 should limit upside. Above the upper Kumo (now at 1.2469) would defer and suggest low is formed instead, risk test of resistance at 1.2506 first, break there would confirm, then a stronger rebound to 1.2525-30 would follow.

Trade Idea Update: EUR/USD – Sell at 1.0635

EUR/USD - 1.0586

Original strategy :

Sell at 1.0635, Target: 1.0535, Stop: 1.0670

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0635, Target: 1.0535, Stop: 1.0670

Position : -

Target : -

Stop : -

The single currency ran into renewed selling interest at 1.0667 on Friday (after NFP) and has dropped again, the breach o indicated support at 1.0600 adds credence to our bearish view that the decline from 1.0906 is still in progress and may extend further weakness towards 1.0550-55 (50% projection of 1.0906-1.0635 measuring from 1.0689), then 1.0525-30, however, near term oversold condition should prevent sharp fall below 1.0500, risk from there is seen for a rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 1.0635 (previous support now resistance) should limit upside. Only a firm break above said resistance at 1.0667 would abort and suggest low is formed instead, risk a stronger rebound to 1.0689, then 1.0702.

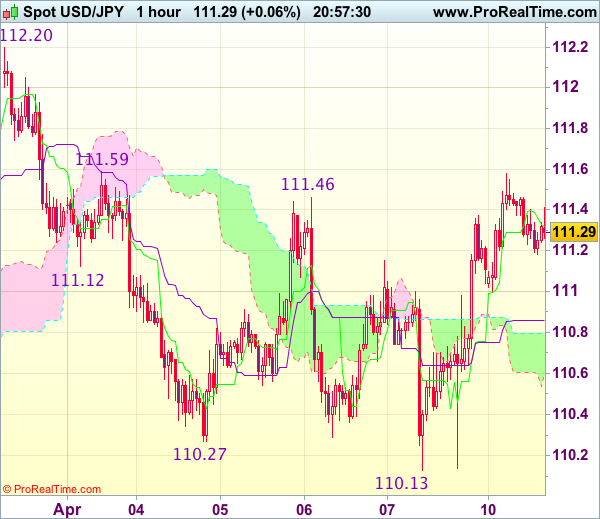

Trade Idea Update: USD/JPY – Buy at 110.90

USD/JPY - 111.27

Original strategy :

Buy at 110.90, Target: 111.90, Stop: 110.55

Position : -

Target : -

Stop : -

New strategy :

Buy at 110.90, Target: 111.90, Stop: 110.55

Position : -

Target : -

Stop : -

Although the greenback fell to as low as 110.13 late last week, as dollar has staged a strong rebound after holding above indicated support at 110.11, retaining our view that further consolidation above this level would be seen and mild upside bias is for test of 111.59 resistance, a break there would signal the fall from 112.20 has ended, then a stronger rebound to 111.90-00 would follow but said resistance at 112.20 should hold and choppy trading within 110.11-112.20 would continue.

In view of this, we are looking to buy dollar on dips but one should exit on such rebound. Below the lower Kumo (now at 110.60) would signal an intra-day top is formed instead, risk weakness to 110.40 but only break of said support at 110.11-13 would confirm medium term decline has resumed for further subsequent fall to 109.80-85 (1.618 times projection of 112.20-111.12 measuring from 111.59) but price should hold above 109.50-55 (100% projection of 112.20-110.27 measuring from 111.46).

Geopolitical Risks Leave Markets on Edge

Global stocks were mixed during trading on Monday, with participants adopting a defensive stance after the heightened geopolitical risks weighed heavily on sentiment. Asian shares simply struggled for direction amid the cautious trading mood and the noticeable anxiety has limited gains in Europe. With the lingering sense of caution creating a lacklustre trading atmosphere, Wall Street may struggle to find the momentum needed to venture higher this afternoon. Stock markets could come under renewed selling pressure, as geopolitical risks are compounded with the messy mixture of political uncertainty, Brexit woes and Trump developments.

Dollar Index breaks above 101.00

The Dollar Index breached above the 101.00 resistance level on Friday, after markets received March's mixed US jobs report positively. Although the dismal NFP figure of 98k initially sparked some jitters, this was swiftly countered by the unexpected decline in unemployment rates that dropped to their lowest levels in almost 10 years at 4.5%. The upside seen in the Dollar was complimented by hawkish comments from the Fed's Dudley, which bolstered speculation of more rate hikes this year. Whilst the geopolitical risks and renewed expectations of further rate hikes may support the Dollar bulls, the ongoing concerns over Trump's ability to move forward with tax reforms could create some headwinds and limit gains down the line.

Sterling slides below 1.2400

Sterling was exposed to steep losses last week, following the unexpected drop in the British manufacturing output which reignited concerns over the health of the UK economy as it prepares to depart from the EU. A resurgent Dollar from the mixed NFP report fuelled the downside and provided a foundation for bears to drag prices below the 1.2400 level. With the bias towards Sterling firmly bearish amid the ongoing Brexit uncertainty, further downside may be expected with any technical bounces seen an opportunity for sellers to attack prices lower. From a technical standpoint, bears need a solid daily close below 1.2370 which could open a path lower towards 1.2300.

Currency spotlight - EURUSD

The growing uncertainty ahead of the upcoming French presidential elections has haunted investor attraction towards the Euro. Markets are still weighing the possibility of Eurosceptic Marine Le Pen winning the elections and the jitters have translated to downside further shocks for the Euro. With the Dollar back in fashion amid the speculations of higher US rates, the EURUSD remains under intense selling pressure. From a technical viewpoint, the EURUSD fulfils the prerequisites of a bearish trend on the daily charts as there have been consistently lower highs and lower lows. The solid breakdown below 1.0600 could encourage a further decline back towards 1.0500.

Commodity spotlight - Gold

The explosive combination of Dollar strength and risk aversion left Gold chaotic on Friday, with prices eventually concluding the week below $1260. While the metal remains supported in the medium to longer-term amid the geopolitical tensions and political risks across the globe, the renewed rate hike expectations could enforce downside pressures in the short term. Gold's trajectory on the daily charts remains tilted to the upside, with bulls in firm control above the $1240 higher low. From a technical standpoint, a solid daily close above $1260 is needed for any further upside. In an alternative scenario, a breakdown below $1240 may open a path back towards the $1225 support.