Sample Category Title

Trade Idea : USD/JPY – Sell at 111.30

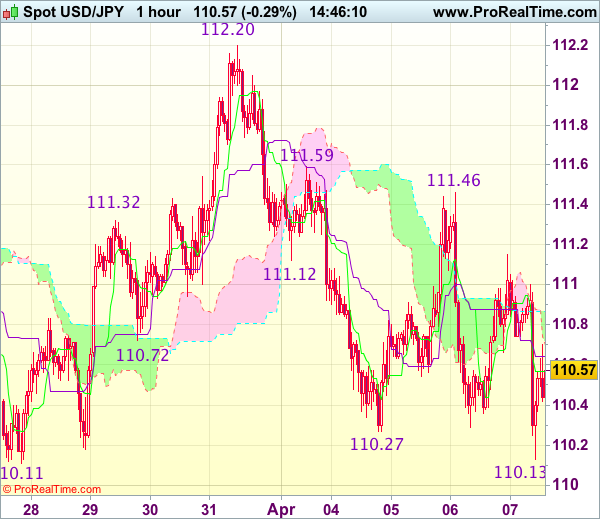

USD/JPY - 110.56

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 110.57

Kijun-Sen level : 110.64

Ichimoku cloud top : 110.87

Ichimoku cloud bottom : 110.70

Original strategy :

Sell at 111.30, Target: 110.30, Stop: 111.65

Position : -

Target : -

Stop : -

New strategy :

Sell at 111.30, Target: 110.30, Stop: 111.65

Position : -

Target : -

Stop : -

Although the the greenback fell briefly to 110.13, as dollar has rebounded after holding above support at 110.11, suggesting further consolidation above this level would be seen and corrective bounce to 111.00 cannot be ruled out, however, reckon upside would be limited and resistance at 111.46 should remain intact, bring another decline later, below said support at 110.11-13 would confirm medium term decline has resumed for further subsequent fall to 109.80-85 (1.618 times projection of 112.20-111.12 measuring from 111.59) but price should hold above 109.50-55 (100% projection of 112.20-110.27 measuring from 111.46).

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 111.20-30 should limit upside. Only above 111.46 resistance would abort and prolong choppy trading, risk rebound to 111.59, then towards 111.90-00 later but price should falter well below said resistance at 112.20.

Could The AUD Be Readying To Test December’s Lows?

Key Points:

- Double top formation could see a large decline over the coming weeks.

- Parabolic SAR remains highly bearish.

- The neckline of the pattern is now very much in sight.

The Aussie Dollar seems to have finally shed its bullishness and is now making a beeline for a crucial level of indication which might result in a substantial slide over the coming weeks. Specifically, if it breaks through the 0.7490 level, a developing chart pattern will likely be confirmed which should result in a decline back to the December lows.

More specifically, over the past 3 months we have seen what is now clearly a double top pattern form up. This structure has largely respected the overarching bearish trend line and, now that the AUD has closed below the 100 day EMA, this bearish sentiment should come back with a vengeance. As a result, the neckline of the double top is now firmly in sight which could mean further loses are now on the way.

Such a return of long-term bearishness would mirror the consensus being reached by a number of technical instruments. Namely, the parabolic SAR is steeply bearish and in practically no danger of having its bias inverted within the next few weeks. Similarly, the EMA bias is indicating that losses should extend moving ahead, especially now that the pair is below the 100 day average. Finally, we can also look to the MACD oscillator for some guidance as the recent signal line crossover would typically indicate that a downtrend is still firmly in place.

All things considered, we expect to see the neckline around the 0.7490 handle to not only be challenged but also be broken within a week or so. When this happens, selling pressure could mount significantly which may not truly abate until the AUDUSD moves all the way back to the 0.7158 mark. Downside risk should be capped around this level given that it has been a very robust support for the pair over the past year or so. However, we could also have some difficulty with the 0.7325 level which has also proven to be a solid zone of support as well.

Ultimately, this forecast may run into a bit of interference if the Australian and US fundamentals continue to post mixed results. However, given the widely held expectations of successive US rate hikes and the broadly bearish technical bias, is not too much of a stretch to envision a return to the lows seen only a few month ago. As a result, keep an eye on the neckline as over the coming sessions as it could be the first key support to yield in a rather impressive trance of losses.

Oil And Gold Are Moving Higher

Market movers today

The key market focus today is on the US military strike in Syria and the US non-farm payroll report from March due to be released in the US.

The US labour market has been in good shape over the past two months and we expect this trend to cont inue. We estimate a total of 160,000 new jobs were created in March but highlight that risks are skewed to the upside as the ADP labour report from Wednesday suggested weather condit ions had less of a negat ive effect on job growth than we have pencilled in. We est imate the average hourly earnings increased 0.2% m/m, which would mean an increase of 2.7% y/y. We furthermore est imate the unemployment rate remained at 4.7% aft er last mont h's decrease.

In the UK, the NIESR GDP est imate for March is due – the indicator is usually a good predictor of actual GDP growth.

German industrial production is due to be released on Friday. Following the weak factory orders in January, we estimate indust rial product ion for February will show a drop of 2.5%.

In the Scandis, focus will be on indust rial product ion in Norway and Denmark.

Selected market news

The US has launched a military strike in Syria after accusing Assad's regime of the gas at tack earlier this week that killed many civilians. Donald Trump confirmed the at tacks from his Florida Club – current ly the locat ion of the Chinese President Jinping's visit – stat ing that it is in t he ‘vital national security interest of the United States to prevent and deter the spread and use of deadly chemical weapons'. The attack targeted the air base from which the gas at tack presumably originated. Prior to the at tack, Russian officials stated that at tacks would have ‘negat ive consequences'.

Safe havens such as US Treasuries, JPY and CHF have rallied on the first military act ion of the young Trump presidency. Also, gold and oil are moving higher this morning on the back of the rise in geopolit ical risk, as the at tacks suggest a different approach from the Trump administ rat ion than that under Obama.

Yesterday, the Czech National Bank (CNB) abandoned the EUR/CZK floor in an ext raordinary monetary policy meet ing, as the condit ions for a sustainable fulfilment of the inflation target were met and there is no need to keep monetary condit ions as relaxed as before anymore, according to the CNB . The exchange rate is now free to move according to supply and demand in the market (‘managed float '). The CNB also confirmed it stands ready to mit igate any excessive exchange rate fluctuations, without ment ioning any specific levels. Governor Jiří Rusnok indicated at the later press conference that t he CNB's tolerance for volatility will be quite large.

Market Update – Asian Session: US Launches Missile Strike On Syrian Airbase Deemed Responsible For Chemical Attack

US launches missile strike on Syrian airbase deemed responsible for chemical attack

US Session Highlights

(US) INITIAL JOBLESS CLAIMS: 234K V 250KE; CONTINUING CLAIMS: 2.03M V 2.03ME

(US) House Intel Chief Nunes: to temporarily step down from committee's Russia investigation; says charges filed against him with Office of Congressional Ethics are entirely false and politically motivated

(US) House Freedom Chair Caucus Meadows (R-NC): majority of Freedom Caucus members will vote for healthcare bill if earlier White House offers are included in the legislation

(US) White House economic adviser Cohn reportedly tells lawmakers Trump administration remains open to a new Glass-Steagall law - press

US markets on close: Dow +0.1%, S&P500 +0.2%, Nasdaq +0.3%

Best Sector in S&P500: Energy

Worst Sector in S&P500: Telecom

Biggest gainers: LB +11.0%; STZ +6.4%; KSS +5.6%

Biggest losers: INCY -2.1%; FAST -1.5%; AMZN -1.2%

At the close: VIX 12.4 (-0.5pts); Treasuries: 2-yr 1.22% (-1bps), 10-yr 2.34% (-1bps), 30-yr 2.99% (-2bps)

US movers afterhours

HYGS: Awarded funding to build two hydrogen fueling stations fo Greater Toronto Area (GTA); +6.3% afterhours

RYI: Guides Q1 higher Rev y/y; guides Q1 adj EBITDA $53-55M v $37M y/y; +5.7% afterhours

OCLR: To join S&P SmallCap 600 index; +4.4% afterhours

WDFC: Reports Q2 $0.87 v $0.90e, R$96.5M v $99.8Me; affirms FY17 $3.64-3.71 v $3.65e, Cuts R$390-395M v $387Me; -4.2% afterhours

NPTN: CFO Ray Wallin to depart; effective May 15th; -2.2% afterhours

RT: Reports Q3 -$0.06 (adj) v +$0.03 y/y, R$225.7M v $271.5M y/y; Names James F. Hyatt as new CEO effective immediately; -9.3% afterhours

Politics

(US) Bipartisan group of senators including Sen Warren (D-MA) and Sen McCain (R-AZ) introduce 21st Century Glass Steagall legislation - press

(US) President Trump to nominate exec Derek Kan as Under Sec of Policy at DOT - press

Key economic data

(JP) JAPAN FEB LABOR CASH EARNINGS Y/Y: 0.4% V 0.5%E ; REAL EARNINGS (EX-INFLATION) Y/Y: 0.0% V 0.0% PRIOR

(AU) AUSTRALIA MAR AIG PERFORMANCE OF CONSTRUCTION INDEX: 51.2 V 53.1 PRIOR; 2nd straight expansion

(PE) PERU CENTRAL BANK (BRCP) LEAVES REFERENCE RATE UNCHANGED AT 4.25%; AS EXPECTED

Asia Session Notable Observations, Speakers and Press

Asian equity markets are mixed though risk is decidedly on the defensive as simmering geopolitical jitters are burning hotter. Two days after a chemical weapons attack against a Syria rebel stronghold by the Assad regime, President Trump ordered a missile strike against an air base from which the chemical attack was apparently staged. Nearly 60 Raytheon missiles were launched by two Navy destroyers that also took precaution not to hit any Russian assets that were present near the targeted airfield. Pentagon official said Russian military was informed where and when the Syria strike was coming, though State Sec Tillerson took a more critical tone of Moscow, noting that "Russia was either complicit or incompetent in carrying out its 2013 commitment in Syria". Tillerson added that US did not seek an approval from Moscow despite its explicit support for the Assad regime. Initial Congressional response has thus far been positive even though President Trump did not seek Congressional approval before authorizing the strike.

Markets reacted with sharply accentuated risk-off flows - US Treasuries spiked as the yield on the 10-yr fell to a 4-month low below 2.29%, Gold prices rose nearly $20 above 1,270, June S&P500 e-minis fell nearly 20 handles below 2,338 before consolidating the drop around 2,345, and WTI crude rose $1 above $52 even though Syria is not a major crude supplier with worries over Assad ally Iran taking a position against US action. Initial response from Russian officials has also been predictably cool, with one govt official stating that US-Russia cooperation may be in jeopardy. FX markets were also active in what is typically a less volatile session ahead of the non-farm payrolls - USD/JPY fell nearly 100pips to ¥110, AUD/USD fell 25pips below 0.7520, and USD/CHF fell 40pips to 1.0030.

High-profile initial dinner meeting between US Pres Trump and China Pres Xi in Florida has taken a back seat to the Syria escalation. Trump only stated that the two leaders "had a long discussion already, and so far I have gotten nothing, absolutely nothing, but we have developed a friendship."

In notable corporate news, Samsung Electronics put out its preliminary Q1 results beating expectations at Op profit KRW9.9T v KRW9.2Te, Rev KRW50T v KRW49.5Te, though the stock was down slightly in early going. Toshiba remained volatile, rising after today's local press report that Hon Hai submitted a bid near ¥3T for chip unit.

China

(CN) US Pres Trump: US to have a "very, very great relationship" with China in long term - financial press

(CN) Morgan Stanley: China growth and inflation will probably start to roll over in coming quarters due to high base and shift in policy; Expect only gradual moderation rather than sharp slowdown - Chinese press

(CN) China and South Korea to discuss North Korea nuclear issues - financial press

Japan

(JP) Japan Fin Min Aso: US-Japan dialogue agenda not limited to trade and FX

Australia/New Zealand

(AU) Australia govt reportedly has finished a scoping study for a potential free trade agreement with the EU

Korea

(KR) Japan said to extend its unilateral sanctions on North Korea by 2 years - press

Samsung Electronics: Reports prelim Q1 Op profit KRW9.9T v KRW9.2Te, Rev KRW50T v KRW49.5Te

Asian Equity Indices/Futures (23:00ET)

Nikkei -0.1%, Hang Seng -0.7%, Shanghai Composite +0.1%, ASX200 -0.1%, Kospi -0.4%

Equity Futures: S&P500 -0.3%; Nasdaq -0.3%, Dax -0.4%, FTSE100 -0.2%

FX ranges/Commodities/Fixed Income (23:00ET)

EUR 1.0635-1.0660; JPY 110.10-111.00; AUD 0.7515-0.7545; NZD 0.6960-0.6975

June Gold +1.0% at 1,265/oz; May Crude Oil +1.9% at $52.65/brl; May Copper +0.2% at $2.66/lb

iShares Silver Trust ETF daily holdings fall to 10,208 tonnes from 10,237 tonnes prior; 6th straight decline, lowest since Mar 2016

(CN) PBOC SETS YUAN MID POINT AT 6.8949 V 6.8930 PRIOR

(CN) PBoC skips open market operations for 10th straight session; Drains net CNY100B this week v drained CNY290B prior

(AU) Australia MoF (AOFM) sells A$600M in 2.0% 2021 Bonds; avg yield: 2.0635%; bid-to-cover: 6.12x

(US) US based stock funds see $11.9B outflow (largest outflow since Dec) in week ended Apr 5th v $1.8B inflow in prior week - Lipper

Asia equities notable movers

Australia

HLO.AU Helloworld +6.1% (raises guidance)

AGL.AU AGL Energy +2.7% (UBS upgrades)

ALL.AU Aristocrat +1.1% (Ord Minnett raises PT)

S32.AU South32 -2.7% (Morgans Financial downgrades)

JBH.AU JB Hi-Fi -1.4% (Deutsche Bank comment)

MET.NZ Metlifecare -4.0% (Infratil sells stake)

EHE.AU Estia Health -5.2% (update on Sentinel portfolio management)

Japan

8354.JP Fukuoka Financial +2.4% (Credit Suisse upgrades)

6502.JP Toshiba Corporation +2.0% (Hon Hai offer)

8174.JPNippon Gas Co +5.2% (JPMorgan initiates)

7735.JPScreen Holdings Co -3.0% (Macquarie downgrades)

2659.JPSan-A Co -3.7% (annual result)

3382.JPSeven & I Holdings +4.4% (annual result)

7013.JPIHI Corp +4.0% (Jefferies initiates)

2337.JPIchigo Group Holdings +3.5% (March result)

South Korea

005930.KR Samsung Electronics -0.7% (prelim Q1 result)

139480.KR E-Mart +4.4% (monthly sales)

Hong Kong

1317.HK China Maple Leaf Educational Systems +1.7% (H1 guidance)

960.HK Longfor Properties +1.2% (Mar result)

1030.HK Future Land Development Holdings +2.6% (Mar result)

1910.HK Samsonite +0.9% (acquisition)

1157.HK Zoomlion Heavy Industry Science and Technology +2.2% (Q1 guidance)

China

600489.CN Zhongjin Gold Co +5.7%, 601899.CN Zijin Mining +3.8%

Australia’s Construction Sector Slows In March

For the 24 hours to 23:00 GMT, the AUD declined 0.41% against the USD and closed at 0.7540.

LME Copper prices rose 1.1% or $62.0/MT to $5870.5/MT. Aluminium prices declined 0.3% or $6.0/MT to $1956.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7521, with the AUD trading 0.25% lower against the USD from yesterday's close.

Overnight data showed that Australia's AIG performance of construction index dropped to a level of 51.2 in March, compared to a level of 53.1 in the previous month.

The pair is expected to find support at 0.7500, and a fall through could take it to the next support level of 0.7480. The pair is expected to find its first resistance at 0.7554, and a rise through could take it to the next resistance level of 0.7588.

Going ahead, investors will look forward to Australia's unemployment rate, consumer inflation expectations, NAB business confidence and Westpac consumer confidence, all scheduled to release next week.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Stimulus Efforts Still Needed In The Euro-Zone: ECB’s Draghi

For the 24 hours to 23:00 GMT, the EUR declined 0.23% against the USD and closed at 1.0643, after the European Central Bank (ECB) Chief, Mario Draghi, stated that it was too soon to wind down the central bank's stimulus program, even though the Euro-zone economy is strengthening and added that there was scant evidence that inflation was approaching the central bank's target.

Separately, minutes from the ECB's March meeting showed that committee members broadly agreed that a substantial degree of stimulus is still needed.

On the data front, Germany's seasonally adjusted factory orders rebounded 3.4% on a monthly basis in February, driven by strong domestic demand, compared to a revised fall of 6.8% in the previous month, while market participants expected a gain of 4.0%. Moreover, activity in the nation's construction sector accelerated at the fastest pace in over a year, with the PMI advancing to a level of 56.4 in March, following a reading of 54.1 in the prior month.

The greenback gained ground against a basket of currencies, lifted by the release of upbeat US jobless claims data.

The US initial jobless claims fell more-than-expected to a level of 234.0K in the week ended 01 April 2017, hitting its lowest level in nearly two-years and pointing to a further tightening in the nation's labour market. Initial jobless claims had recorded a revised reading of 259.0K in the prior week, compared to market expectations of a fall to a level of 250.0K.

Meanwhile, investors remained nervous amid caution over an impending summit between US President, Donald Trump and Chinese President, Xi Jinping.

In the Asian session, at GMT0300, the pair is trading at 1.0644, with the EUR trading marginally higher against the USD from yesterday's close.

The pair is expected to find support at 1.0621, and a fall through could take it to the next support level of 1.0597. The pair is expected to find its first resistance at 1.0674, and a rise through could take it to the next resistance level of 1.0703.

Trading trend in the Euro today is expected to be determined by the release of Germany's industrial production and trade balance figures, both for February, slated to release in a few hours. Moreover, the US non-farm payrolls and unemployment rate data, both for March, scheduled to release later in the day, will garner a significant amount of market attention.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Pound Trading Flat In The Asian Session, Ahead Of A Slew Of Economic Releases In Britain

For the 24 hours to 23:00 GMT, the GBP declined 0.17% against the USD and closed at 1.2465.

In the Asian session, at GMT0300, the pair is trading at 1.2465, with the GBP trading flat against the USD from yesterday’s close.

The pair is expected to find support at 1.2441, and a fall through could take it to the next support level of 1.2416. The pair is expected to find its first resistance at 1.2497, and a rise through could take it to the next resistance level of 1.2528.

Ahead in the day, all eyes will be on UK’s trade balance, manufacturing as well as industrial production data, all for February and the NIESR GDP estimate for the three months to March. Also, a speech by the Bank of England Governor, Mark Carney, will attract investor attention.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Japan’s Consumer Confidence Hits Highest Level Since September 2013 In March

For the 24 hours to 23:00 GMT, the USD rose 0.31% against the JPY and closed at 110.84.

In economic news, Japan's consumer confidence index jumped to a level of 43.9 in March, surging to its highest level in more than three years. Markets expected the index to advance to a level of 43.4, after recording a revised reading of 43.2 in the previous month.

In the Asian session, at GMT0300, the pair is trading at 110.38, with the USD trading 0.42% lower against the JPY from yesterday's close.

The pair is expected to find support at 109.95, and a fall through could take it to the next support level of 109.52. The pair is expected to find its first resistance at 110.97, and a rise through could take it to the next resistance level of 111.56.

Next week, Japan's trade balance, Eco-watchers survey, flash machine tool orders and final industrial production data, will be on investor's radar.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Swiss Consumer Price Inflation Advanced As Expected In March

For the 24 hours to 23:00 GMT, the USD rose 0.13% against the CHF and closed at 1.0052.

Macroeconomic data revealed that Switzerland’s consumer price index (CPI) rose 0.2% MoM in March, meeting market expectations. The CPI had climbed 0.5% in the previous month. Meanwhile, on an annual basis, the CPI surprisingly remained steady at 0.6% in March.

In the Asian session, at GMT0300, the pair is trading at 1.0046, with the USD trading 0.06% lower against the CHF from yesterday’s close.

The pair is expected to find support at 1.0024, and a fall through could take it to the next support level of 1.0003. The pair is expected to find its first resistance at 1.0067, and a rise through could take it to the next resistance level of 1.0089.

Going ahead, market participants focus on Switzerland’s unemployment rate for March, due to release in a few hours, to gauge strength in the nation’s labour market.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Canada’s Building Permits Surprisingly Declined In February

For the 24 hours to 23:00 GMT, the USD declined 0.1% against the CAD and closed at 1.3416.

On the economic front, Canada's building permits unexpectedly dropped 2.5% on a monthly basis in February, confounding market expectations for a rise of 1.3%. In the previous month, building permits had recorded a revised rise of 5.8%.

In the Asian session, at GMT0300, the pair is trading at 1.3400, with the USD trading 0.12% lower against the CAD from yesterday's close.

The pair is expected to find support at 1.3379, and a fall through could take it to the next support level of 1.3359. The pair is expected to find its first resistance at 1.3435, and a rise through could take it to the next resistance level of 1.3471.

Going ahead, traders would keep a close watch on Canada's unemployment rate for March, scheduled to release later in the day.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.