Sample Category Title

GBP/USD Wedge Resistance Tapped

We spoke yesterday about the GBP/USD wedge that saw price coiling up nicely, and I couldn't go past featuring the continued price action to end the week.

First up, let's take a look at what we said yesterday:

Zooming into any of the intraday charts, you can see that price is coiling into a wedge pattern:

GBP/USD 4 Hourly:

Seeing as though price is right smack bang in the middle of the daily range, the direction on which to trade this pattern isn't clear. Do you view it as a continuation pattern because price has rallied off support and this is merely a pause before a further push higher, or do you take the view that it is simply a turn as we get closer to the top of the range?

Yesterday's price action goes some way toward answering the question:

GBP/USD 4 Hourly:

As you can see, price shot up, tapped the upper trend line of the wedge and was rejected back down.

Zoom into an even lower time frame chart and you can see just how violent the rejection was.

China-US Meeting And US Jobs In The Spotlight

Dollar higher ahead of NFP

The US dollar is higher against most majors currency pairs before the China-US summit and the release of the US employment report. Chinese President Xi Jinping has landed in Florida to meet with US counterpart Donald Trump to hold bilateral talks where trade and North Korea will be on the agenda. The two day meeting is sure to bring some market direction with the other driver being the US jobs report.

The U.S. non farm payrolls (NFP) will be released on April 7, at 8:30 am EDT (12:30 GMT). The forecast calls for a print of over 170,000 new jobs added to the US economy even after an impressive 235,000 announced last month. Although the headline number has shown consistent growth market watchers will be focusing on the average hourly earning for signs of higher pay leading to higher spending form US consumers. Analysts anticipate the hourly earning to gain 0.2 percent and allow the Fed to be patient on rates.

US employment has been the strongest pillar of the economic recovery and has kept pace with the US Federal Reserve two rate hikes in December (2015 and 2016) and the 25 basis point interest rate rise in March with the promise of more coming this year if the economy grows as expected. The Trump administration has struggled to recapture the optimism of the post election victory when the pro-growth policies were announced, but so far have not been delivered. Minutes from the March FOMC meeting showed internal debate on inflation and growth that could make the central bank rethink their hawkish view on the number of rate hikes this year.

The EUR/USD lost 0.06 in the last 24 hours. The single currency is trading at 1.0642 as political risk is one of many factors dragging it downwards. French elections anxiety has been dampened after the latest televised debate, but situations in Italy and elections later in the year in Germany have not painted an encouraging scenario for European unity.

Mario Draghi said on Thursday that the policies of the European Central Bank (ECB) remain appropriate and even despite positive signs of recovery it is too soon to talk about reducing stimulus. This means that the divergence between the Fed and the ECB will only grow as the Fed slowly but surely continues on a tightening path while the ECB is still unsure when it will abandon its expansionary policies. The German central bank governor does not agree in full with the ECB and would rather see and end to stimulus sooner rather than later.

The price of energy gained 1.33 percent during the Thursday trading session. West Texas is trading at $51.50 in a week that has seen the price of crude rising despite a larger than expected buildup of inventories in the US. Oil started the week barely above $50 and broke under that price level as inventory data started to be published hinting that despite all the effort from the Organization of the Petroleum Exporting Countries (OPEC) to stabilize prices. US crude inventories showed a buildup of 1.6 million barrels last week when the market had forecasted a drawdown of 100,000.

Fundamentals don’t fully explain the move as there is ample evidence of oversupply in the market, yet the price is still rising even as there are more US producers waiting to ramp up production. Asian markets that have been limited by the OPEC cut, have turned to US oil which reduces the overall negative impact of increased US crude. China has surpassed Canada as the main destination of US oil.

A disruption in Canadian supplies after the shutdown of the Syncrude oilseeds facility in Alberta has also helped WTI march higher.

The USD/CAD gained 0.186 percent in the last 24 hours. The pair is trading at 1.3408 ahead of employment data for both the US and Canada. The private payroll report published on Wednesday in the US has boosted optimism around the NFP to be published on Friday. The ADP had two massive data points back to back that have analysts improving their forecast for the NFP that is coming of a 235,000 jobs added and is now expected to deliver above 170,000. Canadian job gains are anticipated to be around 5,700 after a strong 15,300 last month. The data for both will go out at the same time with the market focusing on the US data before digesting the Canadian employment report.

The Canadian dollar has not fully taken advantage of the rise in oil prices as investors are anxious about macro events around the globe. The meeting between Presidents Trump and Xi in Florida could have far reaching implications for trade ahead of any Nafta renegotiation talks with Canada and Mexico. Risks are offsetting the rise in commodities with analysts also expecting the Bank of Canada (BoC) to remain in the sidelines as the U.S. Federal Reserve slowly hikes rates and as evidenced by the minutes released this week start trimming their balance sheet.

Market events to watch this week:

Wednesday, April 5

4:30am GBP Services PMI

8:15am USD ADP Non-Farm Employment Change

10:00am USD ISM Non-Manufacturing PMI

10:30am USD Crude Oil Inventories

2:00pm USD FOMC Meeting Minutes

Thursday, April 6

7:30 am EUR ECB Meeting Minutes

8:30am USD Unemployment Claims

Friday, April 7

4:30am GBP Manufacturing Production m/m

8:30am CAD Employment Change

8:30am USD Average Hourly Earnings m/m

8:30am USD Non-Farm Employment Change

British Pound Steady as US Jobless Claims Sparkles

GBP/USD is showing little movement in the Thursday session. In North American trade, GBP/USD is trading at 1.2480. On the release front, there are no major British indicators. In the US, unemployment claims dropped sharply to 234 thousand, easily beating the forecast of 251 thousand. On Friday, the UK publishes Manufacturing Production. Across the pond, US job numbers will be in focus, with the release of three key indicators – Nonfarm Employment Change, Average Hourly Earnings and the unemployment rate.

Although the Bank of England proved to be overly pessimistic about the Brexit vote back in June, policymakers continue to sound the alarm about the negative impact that Brexit will have on the British economy. On Wednesday, Gertjan Vlieghe, a member of the BoE Monetary Policy Committee, warned that that consumer spending in the UK was weakening and the situation was likely to worsen. Vlieghe weighed in on the discussion over monetary policy, as he cautioned the BoE against raising interest rates. The BoE, which has adapted a neutral stance towards a rate move, is not expected to raise rates before 2018, and lengthy Brexit negotiations could delay a rate hike even further. Although inflation levels have moved higher, wage growth and consumer spending remain soft, so there isn't much pressure on the BoE to raise rates in the near future.

The Federal Reserve released the minutes of its March policy meeting on Wednesday. At that meeting, the Fed raised rates a quarter-point to 0.75%, but the dovish rate statement disappointed the markets, triggering broad losses for the US dollar. In the minutes, policymakers noted upside risk to the US economy, but remained divided on whether inflation will rise to the Fed target of 2.0%. Most policymakers were in favor of taking steps to trim the $4.5 trillion balance, which has ballooned since the Fed implemented its aggressive quantitative easing program back in 2008. So what's next for the Fed? According to the CME's Fed Watch, the odds of a rate hike at the May meeting are just 5 percent, while the likelihood of a rate hike in June stand at 63 percent. Fed policymakers appear divided on how many more times the Fed will press the rate trigger. Last week, FOMC member Eric Rosengren called for three more hikes, saying the Fed should raise rates in June, September and December. Rosengren said that employment and inflation levels were close to the Fed's targets, and that three additional hikes were needed in order to prevent the US economy from overheating. However, a majority of FOMC members are in favor of just two more hikes this year.

Elliott Wave Analysis: S&P500 Intraday View

S&P500 is making an intra-day rally from around the 2340 mark, where support may have been found for a flat correction. Ideally we will now see a five wave movement to the upside follow and hopefully a breach above the 2378 level.

S&P500, 1H

Japanese Yen Dips as US Jobless Claims Dives

USD/JPY has posted gains in the Thursday session, as the pair trades just below the 111 level in the North American session. On the release front, Japanese Consumer Confidence improved to 43.9, above the forecast of 43.5 points. In the US, unemployment claims dropped to 234 thousand, its lowest level in five weeks. On Friday, US job numbers will be in focus, with the release of three key indicators – Nonfarm Employment Change, Average Hourly Earnings and the unemployment rate.

The Japanese consumer remains pessimistic about the economy, as the latest consumer confidence survey came in at 43.9 points for March. Although this reading improved over the February release of 43.1, a release below the 50-point level points to pessimism. There are some bright points in the economy, as manufacturing and export numbers are pointing higher. At the same time, domestic consumption remains soft and inflation levels remain well below the BoJ's target of 2.0% percent. The BoJ's preferred inflation indicator, BoJ Core CPI, remains weak and dipped to 0.1 percent. With inflation at low levels, the Bank of Japan is in no rush to tighten monetary policy.

There were no surprises from the minutes of the Fed March policy meeting. At that meeting, the Fed raised rates a quarter-point to 0.75%, but the dovish rate statement disappointed the markets, triggering broad losses for the US dollar. In the minutes, policymakers noted upside risk to the US economy, but remained divided on whether inflation will rise to the Fed target of 2.0%. Most policymakers were in favor of taking steps to trim the $4.5 trillion balance, which has ballooned since the Fed implemented its aggressive quantitative easing program back in 2008. So what's next for the Fed? According to the CME's Fed Watch, the odds of a rate hike at the May meeting are just 5 percent, while the likelihood of a rate hike in June stand at 63 percent. Fed policymakers appear divided on how many more times the Fed will press the rate trigger. Last week, FOMC member Eric Rosengren called for three more hikes, saying the Fed should raise rates in June, September and December. Rosengren said that employment and inflation levels were close to the Fed's targets, and that three additional hikes were needed in order to prevent the US economy from overheating. However, a majority of FOMC members are in favor of just two more hikes this year.

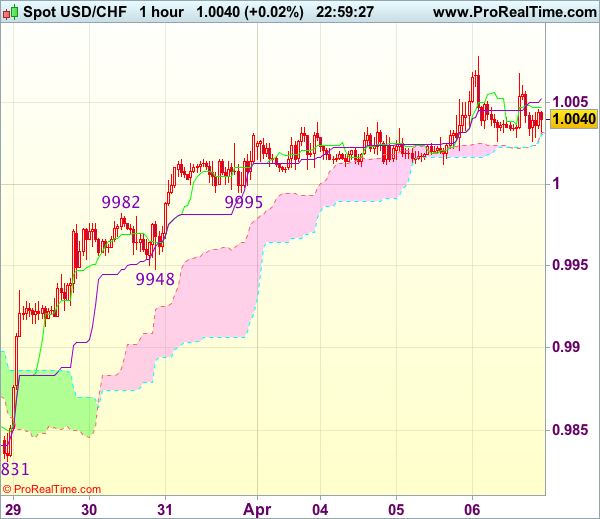

Trade Idea Wrap-up: USD/CHF – Buy at 0.9950

USD/CHF - 1.0042

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.0047

Kijun-Sen level : 1.0053

Ichimoku cloud top : 1.0032

Ichimoku cloud bottom : 1.0031

Original strategy :

Buy at 0.9950, Target: 1.0050, Stop: 0.9915

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9950, Target: 1.0050, Stop: 0.9915

Position : -

Target : -

Stop : -

As the greenback has maintained a firm undertone after last week’s rally above 1.0003 resistance, suggesting recent rise from last week’s low at 0.9813 is still in progress and bullishness remains for this move to 1.0080, then towards previous resistance at 1.0109, however, loss of upward momentum should prevent sharp move beyond latter level and reckon 1.0140-50 would hold, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy dollar on pullback as support at 0.9948 should limit downside. Below 0.9925-30 would abort and signal top is formed instead, bring correction to 0.9905-10 but reckon previous resistance at 0.9869 would hold from here.

Trade Idea Wrap-up: GBP/USD – Stand aside

GBP/USD - 1.2492

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2478

Kijun-Sen level : 1.2478

Ichimoku cloud top : 1.2475

Ichimoku cloud bottom : 1.2459

Original strategy :

Sold at 1.2465, stopped at 1.2500

Position : - Short at 1.2465

Target : -

Stop : - 1.2500

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As the British pound has rebounded again finding support at 1.2450, dampening our bearishness and further choppy trading is in store, hence upside risk remains for recovery to 1.2520-25, however, as broad outlook remains consolidative, reckon upside would be limited and price should falter below resistance at 1.2559, bring retreat later.

As near term outlook has turned mixed, would be prudent to stand aside in the meantime. Below said support at 1.2450 would revive bearishness and bring weakness to said support at 1.2419, break there would bring test of 1.2400 but below there is needed to add credence to our view that the rebound from 1.2377 has ended at 1.2559, bring further fall towards support at 1.2377.

USD Stabilizes after Soft Post-Minutes Market Reaction

Headlines

US equities opened marginally higher after yesterday's correction as some Fed governors considered valuations as quite high. European equities are trading with gains of up to 0.5% after reversing opening losses.

"Before making any alterations to the components of our stance -- interest rates, asset purchases and forward guidance --we still need to build sufficient confidence that inflation will indeed converge to our aim over a medium-term horizon, and will remain there even in less supportive monetary policy conditions," ECB Draghi said.

India's monetary policy committee has decided to hold the central bank's key policy rate steady at 6.25%, saying the economy appears to be on course to meet its inflation target (4%). The RBI did narrow the interest rate corridor by hiking the reverse repo rate to 6% in order to help manage the weighted average call rate.

The Czech crown surged almost 1.5% to its highest level against the euro since November 2013, after the country's central bank scrapped the EUR/CZK 27.00 cap on the currency it had in place for 3-1/2 years. EUR/CZK currently trades around 26.70.

Filings for US unemployment benefits declined to a five-week low, highlighting a resilient job market, a Labor Department report showed. Weekly jobless claims declined from 259k to 234k (vs 250k expected).

The ECB's inner circle faced a push from heads of member states' monetary authorities to drop the doom and gloom from its rhetoric and present a much more optimistic outlook on the eurozone's economic prospects at its policy vote last month, Minutes showed.

It would make sense, if the US economy continues to grow, for the Federal Reserve to begin trimming its $4.5 trillion balance sheet towards the end of this year, unwinding extraordinary stimulus deployed during the crisis, SF Fed Williams said.

Rates

Core bonds remain resilient

Global core bonds moved according to script until European noon. Equity and oil prices gradually rose, pulling Bunds and US Treasuries somewhat lower. ECB's Draghi urged that it's too early to speculate on an ECB exit as the central bank needs sufficient confidence that inflation converges to their aim. Apart from some minor losses for the euro, markets ignored his comments. During US trading, core bonds again showed their recent resilience. They changed direction even if intraday trends on stock and commodity markets were extended. On top, US weekly jobless claims unexpectedly declined towards the cycle low and ECB Minutes showed that divergence inside the ECB is larger than president Draghi indicated this morning. They eventually decided to keep forward guidance unchanged as changing it could backfire on markets. A retro perspective interpretation? SF Fed governors Williams confirmed that the Fed could start winding down its balance sheet towards the end of the year.

At the time of writing, the German yield curve marginally bull flattens with yield changes ranging between flat (2-yr) and -1.4 bps (30-yr). Changes on the US yield curve are less than 1 bp. On intra-EMU bond markets, 10-yr yield spread changes versus Germany range between -3 bps (Ireland) and +2 bps (Spain/Greece).

The French debt agency successfully launched a new 10-yr OAT (€4.91B 1% May2027) and tapped the on the run 15-yr OAT (€3.1B 1.5% May2031) for a combined €8B, the maximum amount on offer. The auction bid cover (1.98) improved from previous auctions this year and was more in line with average. The Spanish treasury taps the on the run 3-yr Bono €1.86B (1.4% Jan2020), 10- yr Obligacion (€1.27B 1.5% Apr2027) and off the run Obligacion (€0.79B 4.7% Jul 2041). The total amount sold (€3.92B) was near the middle of the eyed €3.5- 4.5B with a neutral auction bid cover of 1.64.

Currencies

USD stabilizes after soft post-Minutes market reaction

The dollar stabilized against the euro and the yen today after yesterday's soft market reaction to the March FOMC Minutes. EUR/USD dropped briefly on soft Draghi comments early in European dealings, but the pair soon returned to waitand- see modus ahead of tomorrow's US payrolls (1.0660 area). USD/JPY rebounded of the Asian lows as equities reversed a poor open (110.75 area).

Overnight, WS's risk off sentiment also affected Asian markets. Most indices showed losses of 0.5%/1.0%, with China outperforming and Japan underperforming. USD/JPY retested this week's lows (110.30 area), but no break occurred. EUR/USD held in the upper half of the 1.06 big figure.

Early in European dealings, ECB Draghi reiterated that it is too early to change the ECB's policy guidance as the ECB president sees no sufficient evidence to materially alter the inflation outlook. The euro tumbled as the Draghi headlines hit the screens. EUR/USD filled bids in the 1.0630 area. However, most of the move was almost immediately reversed. Draghi's assessment didn't bring much news and the reaction on the interest rate markets was non-existent. Later in the session, the Minutes of the March ECB meeting also maintained a soft tone. However, they weren't able to remove investors' feeling that the debate on a change in the ECB's assessment still persists within the governing council. EUR/USD settled in well-known territory in the 1.0650/75 area. USD/JPY gradually rebounded as equities reversed opening losses.

After a few weeks of higher than expected jobless claims, the indicator was again better than expected (weekly claims of 234 000 from 259 000). The dollar hardly reacted just one day before the key US payrolls report. Even so, the dollar stayed away from the recent lows, despite yesterday's soft market reaction to the March Fed Minutes. EUR/USD trades currently in the 1.0660 area. USD/JPY is trading near 100.80. USD traders are counting down to tomorrow's US payrolls.

At its extraordinary monetary policy meeting today, the CNB Bank Board decided to end the CNB's exchange rate commitment (EUR/CZK 27.00 floor). The CNB stands ready to use its instruments to mitigate potential excessive exchange rate fluctuations if needed. EUR/CZK currently trades around 26.60

Sterling: no UK specific news to guide trading

There were no important eco data in the UK today. So, sterling trading was driven by non-UK factors and technical considerations. EUR/GBP also spiked briefly lower on the Draghi headlines early in European trading. The pair dropped to the 0.8510/15 area. However, as was the case for EUR/USD, the decline was almost immediately reversed. From there, EUR/GBP didn't go anywhere, holding a very tight range in the mid 0.85 area. sterling is trading marginally softer against the dollar as the US currency is regaining slightly ground after yesterday's setback. Cable is trading in the 1.2465 area.

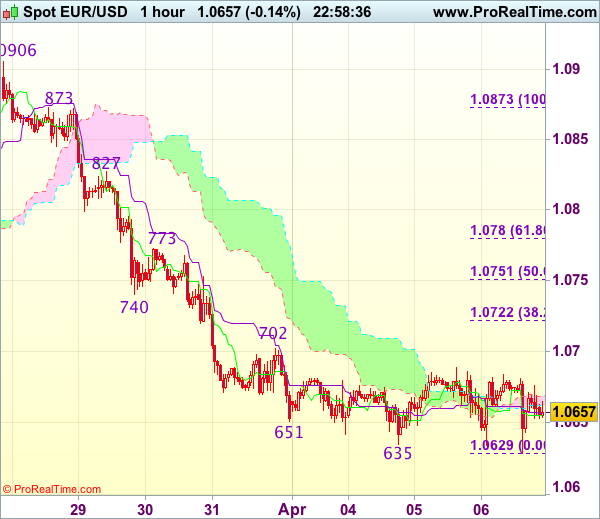

Trade Idea Wrap-up: EUR/USD – Sell at 1.0725

EUR/USD - 1.0659

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.0655

Kijun-Sen level : 1.0657

Ichimoku cloud top : 1.0670

Ichimoku cloud bottom : 1.0662

Original strategy :

Sell at 1.0725, Target: 1.0610, Stop: 1.0760

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0725, Target: 1.0610, Stop: 1.0760

Position : -

Target : -

Stop : -

As the single currency has remained under pressure after recent selloff, bearishness remains for the decline from 1.0906 to extend further weakness to 1.0620, then test of previous chart support at 1.0600, however, a sustained breach below the latter level is needed to retain downside bias for subsequent selloff to 1.0570-75 first.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 1.0720-30 should limit upside. Only a firm break above resistance at 1.0773 would suggest low is formed instead, bring a stronger rebound to 1.0800 but resistance at 1.0827 should remain intact.

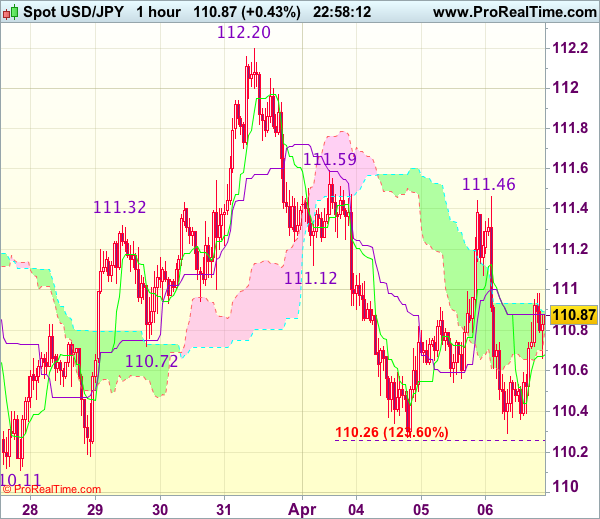

Trade Idea Wrap-up: USD/JPY – Sell at 111.30

USD/JPY - 110.93

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 110.69

Kijun-Sen level : 110.88

Ichimoku cloud top : 110.93

Ichimoku cloud bottom : 110.89

Original strategy :

Sell at 111.10, Target: 110.10, Stop: 111.45

Position : -

Target : -

Stop : -

New strategy :

Sell at 111.30, Target: 110.30, Stop: 111.65

Position : -

Target : -

Stop : -

As the greenback has rebounded after holding above support at 110.27 (this week’s low), retaining our view that further consolidation would be seen and initial recovery to 111.20-30 cannot be ruled out, however, reckon resistance at 111.46 would cap upside and bring another decline later. Below said support at 110.27 would extend the fall from 112.20 to last week’s low at 110.11 but break there is needed to retain downside bias and confirm medium term decline has resumed for further subsequent fall to 109.80-85 (1.618 times projection of 112.20-111.12 measuring from 111.59) which is likely to hold on first testing.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 111.00-10 should limit upside. Only above 111.46 resistance would abort and prolong choppy trading, risk rebound to 111.59, then towards 111.90-00 later but price should falter well below said resistance at 112.20.