Sample Category Title

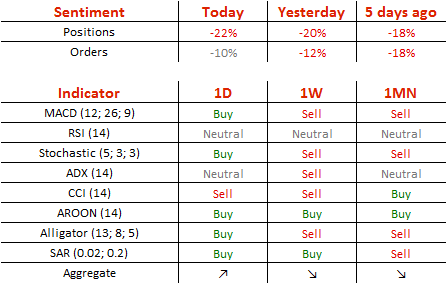

EUR/USD Stops At 1.08 Mark

'The only thing holding global fund managers back from Europe is Marine Le Pen.' – Wayne Gordon, UBS (based on Bloomberg)

Pair's Outlook

During the early hours of Wednesday's trading session the common European currency against the Greenback fluctuated just below the weekly R1, which is located at the 1.0814 level. The weekly resistance is strengthened also by the 38.20% Fibonacci retracement level at 1.0826. The currency pair surged on Tuesday and gained almost 0.7%. Due to that factor it can be assumed that this is a minor consolidation of positions before the surge continues. It is possible that the rate retreats back down to the monthly R1 at 1.0772 before it attempts to break the before mentioned resistance levels.

Traders' Sentiment

SWFX sentiment remains bearish, as 61% of open positions are short on Wednesday. Moreover, 55% of trader set up orders are to sell the Euro.

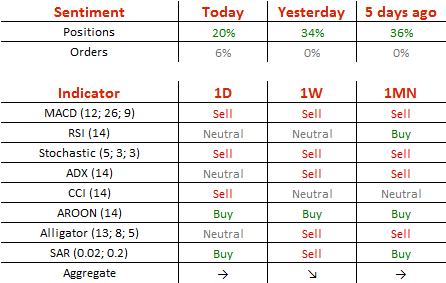

GBP/USD Sets Eye On 1.25

'It's probably going to take some sort of meaningful change in expectations around monetary or fiscal policy to revive the dollar and set it back on a strengthening trend.' – Erik Nelson, Wells Fargo (based on Reuters)

Pair's Outlook

The strong UK inflation data yesterday helped the British currency to strengthen further against the US Dollar, ultimately causing the nine-month down-trend to be pierced. Trade even managed to close above the monthly pivot point, but that does not necessarily mean that support will be sufficient for another leg up. In case bulls retain the upper hand, the pair could easily overcome the 1.25 major level, with the main target shifting to 1.2672, namely the 23.60% Fibo. However, technical indicators remain mixed, thus, the Cable still risks undergoing a corrective decline, but with the 1.24 mark expected to be intact.

Traders' Sentiment

There are 60% of traders being long the Sterling today, compared to 67% on Tuesday. At the same time, 53% of all pending orders are to acquire the Pound (up from 50% yesterday).

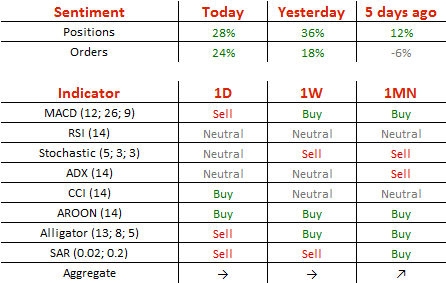

USD/JPY To Fall For The Seventh Day In A Row

'Unlike the dollar and treasuries, the 'Trump trade' still had an impact on equities. But if such impact on equities is to fade, it would weigh on dollar/yen. The dollar will also suffer against other currencies as U.S. yields would decline.' – Barclays (based on Reuters)

Pair's Outlook

Risk-aversion was driving the markets yesterday, causing the USD/JPY pair to drop for the sixth consecutive day. The Buck dropped 85 pips, which was just sufficient to close below the 11.75 psychological support, not to mention the breach of the ascending channel pattern. The US Dollar is now likely to keep edging lower, with the nearest support being around 111.30, formed by the lower Bollinger band and the monthly S1. However, according to the RSI indicator, the Greenback is poised to make a U-turn soon, with today expected to be the last day of a nearly 400-pip slump.

Traders' Sentiment

Although not as strong as yesterday, but market sentiment remains bullish at 64% (previously 68%). Meanwhile, the share of purchase orders inched higher, namely from 59 to 62%.

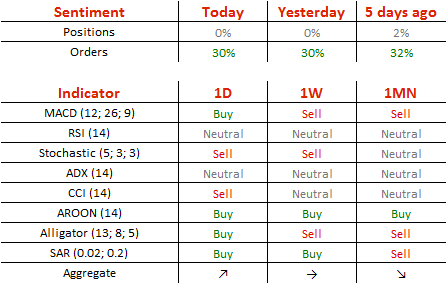

Gold Trades Near 1,245 Level

'Gold will likely continue to rally going into Wednesday's session as Tuesday's U.S. stock market selloff was significant and will likely have a knock-on effect on international equity markets over the next 24 hours.' – Edward Meir, INTL FCStone (based on Reuters)

Pair's Outlook

The yellow metal began Wednesday's trading above the weekly R1 at 1,242.38, which began to provide support by the end of Tuesday's trading. The commodity price is squeezed in between the mentioned weekly R1 and the 50.00% Fibonacci retracement level, which is located at the 1,248.96 level. Due to the persisting bullish sentiment in the markets it can be assumed that the metal will surge, which means that it would pass the retracement level and move in to the next resistance. Above the 50.00% Fibo the closest resistance is the weekly R2 at 1,256.24 and the 200-day simple moving average at the 1,258.57 level.

Traders' Sentiment

Trader open positions are neutral on Wednesday. Meanwhile, 65% of trader set up orders are set to buy the metal.

Cable – Bulls Cracked 1.2500, Fibo 76.4% Barrier At 1.2563 In Focus

Cable generated fresh bullish signal after Tuesday's strong rally that closed well above daily cloud and today's probe above psychological 1.2500 barrier. Near-term focus is turning towards next objective at 1.2563/68 (Fibo 76.4% of 1.2704/1.2107/24 Feb high), however, the pair is showing hesitation at 1.2476 pivot (Fibo 61.8% retracement), as fresh bulls cracked barrier, but require daily close above it, to confirm continuation. Meantime, overbought slow stochastic, but so far without reversal signal, suggests extended consolidation. Broken 100SMA (currently at 1.2412) is expected to contain and keep intact a cluster of supports that lies below. Only return below daily cloud (spanned between 1.2356 and 1.2404) would sideline near-term bulls.

Res: 1.2504, 1.2521, 1.2568, 1.2580

Sup: 1.2462, 1.2412, 1.2404, 1.2382

EURUSD Approaches Initial Target At 1.0827, Extension Towards 200SMA At 1.0886 Seen On Break

The Euro is holding steady and consolidating in1.0800 zone in early Wednesday's trading, after strong rally on Tuesday peaked at 1.0818 and closed above 1.0800 handle. Strong bullish sentiment is in play and favor final push towards initial target at 1.0827 (02 Feb high/Fibo 38.2% of larger 1.1614/1.0339, May 2016/Jan 2017 descend). Break of the latter is expected to trigger fresh acceleration towards next target at 1.0886 (falling 200SMA). Tuesday's long bullish candle and multiple bull-crosses of daily MA's continue to underpin near-term action, however, overbought slow stochastic warns of extended consolidation before bulls resume. Rising 5SMA marks immediate support at 1.0769, ahead of higher base/10SMA at 1.0720/10 zone, which should ideally contain downticks.

Res: 1.0818; 1.0827; 1.0886; 1.0931

Sup: 1.0787; 1.0769; 1.0719; 1.0708

Dollar Tests Key Support As Reflation Trade Falters

Sunrise Market Commentary

- Rates: Core bonds profit as (US) equity markets and oil prices took a hit

US equities corrected more than 1% lower yesterday with main indices closing below the neckline of a minor double top formation, suggesting that the down-leg isn't over yet. Simultaneously, oil prices took a hit. Especially US Treasuries profited from a safe haven bid. Today's eco calendar is empty, suggesting more (risk) sentiment-driven trading. - Currencies: Dollar tests key support as reflation trade falters

A risk-off correction triggered a further decline in US yields and pushed the dollar to key support levels. Especially USD/JPY is vulnerable if the risk-off trade continues. EUR/USD nears 1.0829/74 resistance. However, the EUR/USD rally might slow as we don't expect the US/German interest rate differential to widen further in case of a real risk-off move.

The Sunrise Headlines

- US equities were heavily hit by profit taking after Nasdaq hit new all-time highs amid belief that Trump's pro-growth policies won't sail through Congress. Banks led the rout as US Treasury yields fell, while the dollar continued its retreat. Asian equities follow WS down the drain this morning.

- Centrist Macron's bid for power in France gathered pace when he won support from a junior minister in the Socialist government while the interior minister resigned amid scandal in a new twist to the topsy-turvy presidential campaign.

- BoJ board members rejected suggestions the central bank should raise its 10-yr government bond yield target to match expected gains in Treasury yields, Minutes of their January monetary policy meeting showed

- Cleveland Fed Mester said she's built 'a bit more' than 3 interest rate increases into her forecast and expects the US to expand at a faster rate than the 2% target this year. Voting member Dallas Fed Kaplan pencils in 3 hikes.

- Portugal extended the maturities on state loans to its bank resolution fund by nearly three decades to 2046 to avoid imposing extra costs on a fragile banking sector as the state looks set to sell rescued bank Novo Banco at a loss to be borne by banks.

- Banks in London that relocate operations to the euro zone after Brexit are likely to be spared a lengthy entry test by regulators, making it easier for them to shift, according to two officials with knowledge of the matter.

- Today's eco calendar remains extremely thin with only US existing home sales. After European trading, the Reserve Bank of New Zealand is expected to hold its policy rate unchanged at 1.75%.

Currencies: Dollar Tests Key Support As Reflation Trade Falters

Key USD support area under heavy strain

On Tuesday, the euro initially profited as polls showed a receding chance of a Le Pen victory in the French Presidential election. Later, dollar softness returned as investors took profit on ‘the US reflation trade'. Equities fell prey to intraday profit taking and interest rate differentials between the US and Europe/Germany narrowed further., both for shorter (2yr) and longer (10 yr) maturities. The trade-weighted dollar dropped below the psychological barrier of 100. USD/JPY tested the 111.60 supported and close the session at 111.71. EUR/USD finally stabilized in the low 1.08 area and close the session at 1.0811. The first resistance at 1.0829 came within reach but was left intact for now.

Overnight, Asian equities joined the risk-off correction from the US, with Japanese equities hit the hardest as USD/JPY is testing the key 111.60/36 support area. The correction on the reflation trade also weighs on industrial commodities and commodity related assets (despite the decline of the dollar). The Aussie dollar is losing ground against an overall weak dollar. AUD/USD off the recent highs north of 0.77 and trades currently in the 0.7660 area. EUR/USD is holding within near the recent highs (1.0810).

Today, the only economic data release of importance is the February US Existing Home sales. The market expects a 5.56M annual rate of sales, down 2.4% M/M from January, which was the highest level in about 10 years. We put the risks for the outcome on the downside of consensus. Aside from the data, we keep an eye on the comments from central bankers on the recent developments.

In day-to-day perspective, the key question is whether the correction on the reflation trade continues. We assume that, after this first shock, some market nervousness might persist, especially as long as there is no concrete, additional news on US (fiscal) policy. Last week, US bond sentiment was already positive after the Fed policy decision. This decline in US yields might have some further to go and weigh on the dollar. USD/JPY looks most vulnerable. A sustained break of the 111.36/60 support might have consequences for the overall USD sentiment. Over the previous days, the big change was the sharp narrowing of the USGerman 2- and 10-year yield spread. If markets were to move to a more protracted risk-off correction, the decline of US and German yields might again be more in line.

Interest rate differentials shouldn't narrow that much further. In an overall risk-off context, EUR/USD might remain rather well bid but we don't see a strong case for a big outperformance of the euro against the dollar. So, a test of the 1.0829/74 resistance is very well possible, but the EUR/USD rebound might slow from here. Even so, in a day-to-day perspective, there is no reason to try the catch the falling (USD) knife already now. In a longer term perspective, we don't change our USD-constructive bias based on the eco fundamentals. However, this doesn't tell anything on the short-term momentum/trading dynamics

EUR/USD holding near the key 1.0829/74 resistance

EUR/GBP

Higher UK inflation puts a solid floor for sterling

The euro initially rallied yesterday as polls showed that Macron took the lead in the (1st round of the) presidential race. EUR/GBP filled offers in the 0.8725 area. However, mid-morning, the focus turned to the UK inflation. CPI inflation jumped to 2.3% Y/Y, well above the BoE's inflation target. Core inflation (2.0% Y/Y) was also well above consensus. Last week, some BoE members warned that they considered a rate hike if inflation (or growth) accelerates. UK yields and sterling jumped higher. EUR/GBP dropped to the 0.8655 area. Later in the session, EUR/USD and cable basically traded in line as a risk-off correction started on US stock markets. EUR/GBP closed the session at 0.8663 (from 0.8690). Cable finished the day at 1.2478 from 1.2358, mirroring both sterling strength and US weakness.

Today, there are no important eco data in the UK. So, sterling trading will be driven by overall market trends/risk sentiment. Of late, a risk-off context often hurt sterling more than the euro. However, with markets pondering the chances on a UK rate hike after yesterday's high UK inflation data, the balance between the euro and sterling might remain in place as long as there are no new (negative) headlines on Brexit.

Last week, the sterling decline took a breather. Some time ago, EUR/GBP cleared 0.8592 resistance, improving the MT technical picture. However, yesterday's (substantially) higher than expected UK inflation probably put a decent floor for sterling short-term. We change our short-term bias on EUR/GBP from positive to neutral. Some further consolidation in the 0.85/0.88 area might be on the cards. Longer term, Brexit complications remain a potential negative for sterling, but this issue isn't in the spotlights right now.

EUR/GBP: Higher than expected UK inflation puts a floor for sterling

USDCAD Trading At The Start Of A Big Bearish Impulse

USDCAD made a nice and sharp reversal lower into final wave 5 of 1) yesterday. Today's rally is the beginning of a corrective wave 2), with first leg A in the making. The ideal reversal zone for the undergoing wave 2) is around the 50.0 or 61.8 Fibonacci ratio, from where bears may again push price lower.

USDCAD, 4H

Asian Market Update: Trump Rally Skids Off Track As Health Care Bill Faces Stiff Opposition Ahead Of Thursday House...

Trump rally skids off track as Health Care bill faces stiff opposition ahead of Thursday House vote

US Session Highlights

(US) Mar Philadelphia Fed Non-Manufacturing General Business Conditions: 35.4 v 29.3 prior

(US) Fed's Dudley (dove, FOMC voter): rules must make sure risk of big bank failure is really low - Q&A with reporters

(US) President Trump: asked whether he can get health care bill votes, "I think so"

(US) Rep Peter King (R-NY): does not know if health care bill has the votes to pass the House

(US) House Speaker Ryan (R-WI): a lot of Freedom Caucus members are supporting Trump healthcare bill

(US) 25 Freedom Caucus members are now 'hard no's' on the healthcare bill (GOP can only lose 21 Republican votes and still get the bill passed); unless the bill is dramatically changed by Wed night, the Freedom Caucus may issue a formal statement of opposition and House leaders may have to consider delaying the vote that is scheduled for Thursday - CNBC's Harwood

US markets on close: Dow -1.1%, S&P500 -1.2%, Nasdaq -1.8%

Best Sector in S&P500: Utilities

Worst Sector in S&P500: Financials

Biggest gainers: CMG +2.8%, DUK +1.9%, PPL +1.8%, D +1.8%, XEL +1.8%

Biggest losers: KEY -6.5%, HBAN -6.1%, CMA -6.1%, BAC -5.8%, TDG -5.5%

At the close: VIX 12.5 (+1.1 pts); Treasuries: 2-yr 1.26% (-4bps), 10-yr 2.44% (-4bps), 30-yr 3.05% (-4bps)

US movers afterhours

DLTH: Reports Q4 $0.43 (adj) v $0.33e, R$174.7M v $163Me; Guides initial FY17 GAAP EPS $0.66-0.71, net sales $455-465M v $445Me, Adj EBITDA $47-49.5M v $41.2M y/y; +20.7% afterhours

ACHN: USPTO grants composition of matter patent for small molecule complement alternative pathway Factor D inhibitors; +3.9% afterhours

SLW: Reports Q4 $0.19 v $0.17e, R$258M v $253Me; raises dividend 16.7% to $0.07 (implied yield 1.05%); +3.4% afterhours

FDX: Reports Q3 $2.35 v $2.63e, R$15.0B v $15.0Be; Cuts FY17 capex (incl TNT Express) $5.3B (prior $5.6B); CEO: expect an excellent Q4; +2.1% afterhours

NKE: Reports Q3 $0.68 v $0.52e, R$8.43B v $8.45Be; Q3 Worldwide Futures orders -1% v +3.4%e; -3.7% afterhours

Politics

(US) Pres Trump: Thursday's vote on healthcare legislation is crucial for Republican party - press

(US) US Chamber of Commerce: supports Republican healthcare bill - letter to lawmakers

(US) White House: Pres Trump plans to attend the NATO summit on May 25th - press

Asia Key economic data:

(JP) JAPAN FEB TRADE BALANCE: ¥813B (10-month high) V ¥807BE; ADJ TRADE BALANCE: ¥680B (7-year high) V ¥551BE

(AU) AUSTRALIA FEB WESTPAC LEADING INDEX M/M: -0.1% V 0.0% PRIOR

(AU) AUSTRALIA FEB SKILLED VACANCIES M/M: 0.1% V 0.6% PRIOR

Asia Session Notable Observations, Speakers and Press

Asian equity markets are down significantly, tracking the biggest loss of the year on Wall St where political risk has become increasingly amplified. US indices closed near the lows on late US session report that 25 members of Congressional Republican "Freedom Caucus" are united with a "hard no" position on Trump/Ryan version of Obamacare repeal/replace, which in turn puts into question the viability of White House plans for fiscal stimulus and tax reform. President Trump is making last ditch efforts to negotiate a deal, but also warned that dissenters risk

losing their Congressional seats in the midterms. Treasuries were bid higher across the curve and low-beta Utilities rallied, while Financials and Materials took the most direct hit.

Nikkei225 is the worst performing index in Asia, with added headwinds from overall decline in USD boosting JPY, as Financials is also the worst segment in Japan. Australia is also underperforming as miners slump on lower iron ore prices. In FX, USD/JPY fell below 111.50 for the first time since last November, and AUD's decline to 0.7650 was a 1-week low. NZD/USD was rangebound ahead of tomorrow's RBNZ decision after a brief rally in US hours on increasing dairy auction prices.

Economic data centered around Japan, where Feb Trade Balance recovered from last month's multi-month lows. Exports spiked to a 2-year high 11.3% v 10.1%e, as shipments to Asia and China grew over 20% and US exports recovered from last month's loss with a flat print. BOJ Minutes from Jan meeting maintained view that economy is in moderate recovery trend, though most members agreed price momentum is not yet firm and inflation expectations remain in weakening phase. Recall that meeting preceded the latest BOJ statement when the medium-term outlook for inflation was improved.

China

(CN) Chinese press op-ed speculates economy may face more downward pressure in H2; Govt should increase efforts to stabilize growth

(CN) According to a PBoC survey in Q1, 52% of China urban households believe housing prices are "unacceptably high" - Chinese press

Japan

(JP) BOJ Member Funo: Vintal for BOJ to continue with powerful easing; Must be mindful of downside risks to price outlook; Price momentum is still insufficient

(JP) According to Recruit Jobs, average part time wages in Japan's Tokyo, Nagoya and Osaka metropolitan areas rose 2.3% y/y amid tighter labor market - Nikkei

(JP) Japan Finance Ministry said to seek larger JGB bids from primary dealers in effort to avoid risk of undersubscription - Nikkei

Australia/New Zealand

(AU) Australia Trade Min Ciobo: Relationship with China is very strong

(NZ) Westpac: RBNZ statement tone tomorrow may be balanced and policy outlook expected to remain unchanged, leaving markets "roughly unmoved" - press

(NZ) ANZ economist: Prices for New Zealand commodities are holding up better than expected, as highlighted by positive dairy auction overnight - NZ press

Korea

(KR) North Korea may have launched several missiles today; South Korea military says the launches were not successful - Japan press

Asian Equity Indices/Futures (00:30ET)

Nikkei -2.0%, Hang Seng -1.4%, Shanghai Composite -0.7%, ASX200 -1.6%, Kospi -0.6%

Equity Futures: S&P500 -0.3%; Nasdaq -0.2%; Dax -0.2%; FTSE100 -0.2%

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.0790-1.0820; JPY 111.45-111.80; AUD 0.7650-0.7690; NZD 0.7015-0.7045

Apr Gold -0.1% at $1,245/oz; May Crude Oil -0.2% at $48.13/brl; May Copper -0.3% at $2.60/lb

(US) Weekly API Oil Inventories: Crude: +4.5M v -0.5M prior (7th build in the past 9 weeks)

SPDR Gold Trust ETF daily holdings rise 4.1 tonnes to 834.4 tonnes; First rise since Mar 15th

(CN) PBOC SETS YUAN MID POINT AT 6.8889 V 6.9071 PRIOR; first stronger setting in 4 sessions

(CN) PBOC to inject combined CNY90B v CNY80B prior in 7,14, and 28-day reverse repos

(CN) China MoF sells 3-yr upsized bonds; avg yield 3.0289% v 2.91%e; bid-to-cover ratio 1.69x

(JP) Japan MoF sells ¥500B in 0.4% 40-year JGB bonds, bid to cover: 2.95x v 2.99x prior

(AU) Australia MoF (AOFM) sells A$800M in 2.25% 2028 Bonds; avg yield: 2.8595%; bid-to-cover: 2.19x-

(KR) South Korea sells KRW300B in 50-yr govt bonds at 2.225%

Asia equities / Notables / movers by sector

Consumer staples: 168.HK Tsingtao Brewery Co -3.4% (profit warning); FCG.NZ Fonterra -0.5% (H1 result)

Financials: 1628.HK Yuzhou Properties -1.5% (FY16 result); 81.HK China Overseas Grand Oceans Group -3.4% (FY16 result); 7164.JP Zenkoku Hosho Co +7.6% (raises guidance); PMV.AU Premier Investments +4.6% (Deutsche Bank raises rating)

Industrials: 1038.HK Cheung Kong Infrastructure -1.2% (FY16 result); NUF.AU Nufarm +3.1% (H1 result)

Technology: 1070.HK TCL Multimedia Technology Holdings -0.8% (FY16 result)

Materials: FMG.AU Fortescue -5.3%, BHP.AU BHP Billiton -2.6%, RIO.AU Rio Tinto -2.5% (iron ore declines); EVN.AU Evolution Mining +0.9%, SBM.AU St Barbara +2.6%, NCM.AU Newcrest Mining +2.0% (gold price rises)

Energy: 6.HK Power Assets Holdings -1.4% (FY16 result); 2688.HK ENN Energy Holdings -1.9% (FY16 result)

Telecom: TPM.AU TPG Telecom -2.3% (Credit Suisse cuts rating)

Utilities: 902.HK Huaneng Power International -6.1% (FY16 result)

Oil Prices Broke Above 52USD/Bbl On Tuesday

Market movers today

We have a light data calendar today, with no big market movers in the US, euro area or UK.

Later today, the Reserve Bank of New Zealand will announce its policy rate decision, but we do not expect any changes and project the central bank to leave its cash rate at 1.75%.

In the Scandies, Danish retail sales data and the Norwegian Labour Force Survey for January are published. See the next page.

Selected market news

Asian equity markets were deep in the red this morning after Wall Street had its worst session since the US election, with the S&P 500 tumbling by 1.2% yesterday. The reason was growing concerns that the Trump growth policies will not be implemented as easily as expected, leading investors to abandon risky assets in favour of safe havens such as gold and govies.

EUR/USD climbed above 1.08 yesterday and French stocks and bonds rallied, as centrist Emmanuel Macron's chances of winning the French presidency seemed to have risen after his strong performance in the first TV debate on Monday. The backing of his campaign of a junior minister in the Socialist government – the first to do so – and the resignation of the French interior minister amid another ‘fake work' corruption scandal, seems to have boost his chances further. Whereas market concerns over a Marine Le Pen win might have somewhat abated, the focus could again soon return to Italy. A poll showed support for the Five Star movement (M5S) rising to 32.3%, its highest ever reading, whereas the ruling Democratic Party (PD) saw its popularity drop to 26.8%, due to internal feuds and divisions, with a left-wing faction of the party breaking away and forming a new party on their own (Democratic and Progressive Movement). Currently, the Paolo Gentiloni government is still working on drawing up a new electoral law with some form of proportional representation that might reward a stable majority to any party or coalition winning 40% of the vote. Although M5S so far has ruled out forming any coalitions with other parties, the traditional centre-right and centre-left alliance currently also falls short of the 40% threshold, leaving a high degree of uncertainty about who will head any future government. The current parliament is scheduled to carry on until May 2018, but a number of political leaders, including Matteo Renzi, are pressing for an early election already in September.

Yesterday, we also saw UK inflation surprising on the upside, rising to 2.3% in February. While inflation is now above the Bank of England's 2% inflation target, it does not change our view that the central bank will stay on hold for a longer period of time and refrain from rate increases at a time of high political uncertainty with the upcoming triggering of Article 50 on 29 March. Donald Tusk announced yesterday that there will be a special ‘Brexit' European Council meeting on 29 April, to agree and finalise the negotiation guidelines and official ‘Brexit' negotiations with the UK could then start sometime in May.

Oil prices broke above 52USD/bbl on Tuesday, helped by expectations that OPEC would extend its output cut beyond June. However, prices slipped again in later trading as concerns about persistently high crude inventories resurfaced. Today's release of US crude oil inventory levels will therefore be watched closely by the market.