Sample Category Title

Copper: Very Early Stages Of A New Downwards Trend

The first movement downwards from the high on the 13th of February to the low of the 23rd of February was choppy and overlapping and came on overall declining volume. The market fell of its own weight.

The bounce up to the 1st of March came with some increase in volume. The volume profile looks slightly bullish up to this point, but not strongly.

The fall to the last low on the 9th of March came with increasing volume. This looks clearly bearish.

The next bounce to the high of the 20th of March came with clearly declining volume. This looks like a counter trend movement within a new downwards trend.

ADX has not yet indicated a downwards trend. It is below 15 although it is rising slightly today and the -DX line is above the +DX line.

Contracting Bollinger Bands and declining ATR suggest the market is not yet trending.

The most bearish part of this chart is the recent volume profile. Other indicators suggest caution for short positions.

Copper may be in the very early stages of a new downwards trend. The green trend line goes back to August 2011 and has recently provided resistance. A!er price breached the lower edge of the lilac line, it then turned up to find resistance at that line for a typical throwback. The gold channel is a base channel about minor waves 1 and 2. The upper edge has provided resistance for another second wave correction. The lower edge may now be providing some support. If this Elliott wave count is correct, then Copper should break below support at the lower edge of this channel. It may then turn upwards for a test of resistance before moving down and away.

Market Morning Briefing

STOCKS

Almost all indices have fallen and could continue to trade lower or remain sideways for the week.

Both Dow (20668.01, -1.14%) and Dax (11962.13, -0.75%) are off from yesterday’s levels.

Dow has fallen from resistance levels as indicated in the 3-day candles and the weekly line charts and while this holds, Dow could be bearish in the near term. A break below immediate daily support on 20600 could lead to a fall towards 20500-20300 levels. Note price action near 20600.

Dax has also negated the immediate support near 12000 and has resolved on the downside, opening up chances of a fall towards 11700 levels in the near term.

Nikkei (19065.37, -2.01%) has fallen in line with the fall in Dollar-Yen. The broad 19600-18600 region has again come into focus and the sideways consolidation since Dec’16 is continuing to remain for now. Note the 21-week MA near 18950 could possible act as an immediate support which if breaks could open up levels of 18800.

Shanghai (3236.52, -0.77%) could test lower levels of 3200. A break below is not preferred just now. Some sideways consolidation in the 3200-3250 region is possible for now.

Nifty (9121.50, -0.06%) has possibly begun its first sharp correction after the recent rally in the past 2-months. An initial fall towards 9000-8990 levels could be expected as mentioned yesterday.

COMMODITIES

Overnight weakness in Dollar index (99.65) has helped Gold (1245) to trade above its pivot at 1241. It may have resistance at 1250. A close above that could open up 1272-78 levels.

Silver (17.53) is also trading above its pivot of 17.45 .Immediate resistance poised at 18.00 level.

Copper (2.58) was unable to close above its pivot at 2.70-72 of its recent trading range of 2.55-83 and fell in line with our expectation. It may find support at 2.57 levels in near term but a close below that could open up 2.55 and 2.49 as well.

Brent (50.54) and WTI (47.34) both have fallen but still trading within their respective ranges of 50-52 and 47-49 with a bearish bias. We have US crude oil inventory data at 8.00 pm IST. An increase of 1.9M barrel (as expected) or higher in weekly inventory could open up the lower band of their trading channels.

FOREX

Uncertainty over the passing of Republican pro-growth policies through US congress has unsettled the Dollar and the focus now is on the Republican attempt to pass a health-care bill tomorrow, 23rd March.

Dollar Index (99.85) has broken below 100.00 in line with our expectation as it gets gradually closer to our target of 99.00. The narrow band of 99.00-98.50 is a very significant support zone which may be tested in the coming days

Euro (1.0794) has tested the upper end of the near term range of 1.07-1.08 on relief from French election debate in which the centrist candidate seems to have got a lead over the far rightist Le Pen. The German-US 10Yr rate differential (-1.96%) is just breaking above a major resistance around -2.00% (check Interest Rates) but Euro is yet to rally above the resistance of 1.0830-50. Though the upside possibilities must be considered more now, we prefer t wait and watch till a clean break above 1.0850 is seen.

Dollar-Yen (111.59) is trading below 112.00-111.70, which is a call for 110.00 and even 108.50-00 as targets in the coming days. Near term upside may be limited to 113.00.

Contrary to expectations, Pound (1.2465) jumped above the resistance of 1.2440 on the back of a stronger than expected inflation at 2.3% for Feb’17, breaking through the BOE target of 2% for the first time in 3 years. Now if Pound manages to sustain above 1.25 levels for a session or two, the rise may extend all the way to 1.2650-1.2700.

Aussie (0.7660) has been pushed lower hard by the long term resistance 0.7750-0.7850, which has been aided by the weakness in the base metals like Copper too (Check Commodities section). While the downside is open now, the chances of sideways trading in the band of 0.7600-0.7750 for a few sessions can’t be rule out yet.

Dollar Rupee (65.29) is trading at 65.51 in the NDF now, slightly above the immediate intraday resistance of 65.45 which may take it higher to the near term resistance of 65.60-70. The support of 65.20 is expected to hold for the week.

INTEREST RATES

The US yields continue to fall. The 5yr (1.94%), 10YR (2.41%) and the 30Yr (3.03%) have fallen in line with our expectation and this could possibly continue for 1-2 sessions before we may expect a bounce back to higher levels.

The US 10-5yr (0.47%) could test 0.45% before rising from there.

The 5Yr (-0.15%) and the 10Yr (0.06%) Japan yields have moved down and could test support just below current levels while the 30YR (0.84%) is almost stable near current levels.

The German yields have moved up followed by some weakness in the US Dollar while the Euro gained. There is some more room on the upside which could be tested in the next couple of sessions before a dip is seen.

The German-US 2YR (-2.01%) and the 10Yr (-1.96%) have shot up breaking the immediate resistances confirming a sharp rise in Euro in the near term. Refer to FOREX section above for specific view on Euro. The yield spreads could rise for another 1-2 sessions before pausing.

The US-Japan 10YR (2.35%) has come down as expected and could test immediate support just below current levels. If that produces an immediate bounce, further yen strength could be limited. In case, the yield spread breaks below the immediate support, it could indicate a sharp fall in dollar-Yen to continue in the near term. We need to keep a close watch on this.

The US-UK 10YR (-1.16%) has also risen sharply and is heading towards resistance near -1.03%. Till then the pound has enough scope of rising on the upside.

AUD/USD: Australia’s Westpac Leading Index Dropped In February

For the 24 hours to 23:00 GMT, the AUD declined 0.6% against the USD and closed at 0.7680.

On the data front, China's leading economic index rose 1.2% in February. In the prior month, the index had advanced 1.1%.

LME Copper prices declined 2.1% or $125.5/MT to $5765.5/MT. Aluminium prices rose 0.5% or $10.0/MT to $1918.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7660, with the AUD trading 0.26% lower against the USD from yesterday's close.

Overnight data indicated that Australia's Westpac leading index dropped 0.07% on a monthly basis in February. In the prior month, the Westpac leading index had advanced 0.03%.

The pair is expected to find support at 0.7622, and a fall through could take it to the next support level of 0.7583. The pair is expected to find its first resistance at 0.7724, and a rise through could take it to the next resistance level of 0.7787.

With no economic releases in Australia today, investor sentiment would be governed by global macroeconomic factors.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

EUR/USD: Euro Trading Between Its MA’s In The Asian Session

For the 24 hours to 23:00 GMT, the EUR rose 0.73% against the USD and closed at 1.0811, after a strong debate performance from French centrist Presidential candidate, Emmanuel Macron, thus cementing his position as the front-runner in the election race.

In the US, the Cleveland Federal Reserve (Fed) President, Loretta Mester, expects the US central bank to hike interest rates more than three times this year.

In the Asian session, at GMT0400, the pair is trading at 1.0792, with the EUR trading 0.18% lower against the USD from yesterday's close.

The pair is expected to find support at 1.0756, and a fall through could take it to the next support level of 1.0719. The pair is expected to find its first resistance at 1.0824, and a rise through could take it to the next resistance level of 1.0855.

Going ahead, investors will look forward to the Euro-zone's current account data for January, slated to release in a few hours. Additionally, traders would eye the US existing home sales for February and the house price index for January, slated to release later in the day.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

GBP/USD: Britain’s Annual Inflation Surpassed The Bank Of England’s 2.0% Target In February

For the 24 hours to 23:00 GMT, the GBP rose 0.96% against the USD and closed at 1.2477, after data showed that British annual inflation advanced at the fastest pace in more than three years in February, breaching the Bank of England's 2.0% target.

UK's consumer price index (CPI) jumped 2.3% YoY in February, accelerating to its highest level since September 2013 amid a sharp drop in the pound and rising food and fuel prices, thus piling pressure on the Bank of England to raise interest rates sooner than estimated. The CPI had registered an advance of 1.8% in the prior month, while markets anticipated for it to rise 2.1%. On the other hand, the nation's public sector net borrowing posted a less-than-expected deficit of £1.1 billion in February, as compared to a revised surplus of £11.7 billion in the previous month, whereas investors had envisaged for a deficit of £2.8 billion.

In the Asian session, at GMT0400, the pair is trading at 1.2474, with the GBP trading slightly lower against the USD from yesterday's close.

The pair is expected to find support at 1.2377, and a fall through could take it to the next support level of 1.2279. The pair is expected to find its first resistance at 1.2533, and a rise through could take it to the next resistance level of 1.2591.

In absence of any economic releases in the UK today, investors will focus on global macroeconomic events for further direction.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

USD/JPY: Officials Highlight Financial Market Risk: BoJ Minutes

For the 24 hours to 23:00 GMT, the USD declined 0.92% against the JPY and closed at 111.49.

In the Asian session, at GMT0400, the pair is trading at 111.65, with the USD trading 0.14% higher against the JPY from yesterday's close.

Minutes of the Bank of Japan's (BoJ) January monetary policy meeting showed that board members rejected suggestions that the central bank should raise its 10-year government bond yield target in the future to match expected gains in treasury yields. Members held the view that Japan's inflation and growth will accelerate in the foreseeable future, but it remains a difficult task due to concerns about greater uncertainty in global financial markets.

In economic news, Japan's adjusted merchandise trade surplus widened to a level of ¥680.3 billion in February, hitting its highest level since April 2010, compared to a revised trade surplus of ¥204.0 billion in the prior month. Markets were expecting the nation's trade surplus to expand to a level of ¥550.8 billion.

Additionally, the nation's exports grew the most in more than two years, after it climbed 11.3% YoY in February, surpassing market expectations for an advance of 10.1%, as demand from China and other regions of Asia jumped. Exports had advanced 1.3% in the prior month. Meanwhile, the nation's imports recorded a less-than-expected rise of 1.2% on an annual basis in February, against market consensus for a gain of 1.3% and after recording a rise of 8.5% in the previous month.

Early morning data showed that the nation's all industry activity index unexpectedly increased 0.1% in January, defying market expectations for a flat reading. In the prior month, the index had recorded a revised drop of 0.2%.

The pair is expected to find support at 111.09, and a fall through could take it to the next support level of 110.52. The pair is expected to find its first resistance at 112.54, and a rise through could take it to the next resistance level of 113.42.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

USD/CHF: Switzerland’s Trade Surplus Narrowed In February

For the 24 hours to 23:00 GMT, the USD declined 0.57% against the CHF and closed at 0.9931.

Macroeconomic data indicated that Switzerland's trade surplus narrowed to CHF3.11 billion in February, following a revised surplus of CHF4.83 billion in the prior month.

Separately, the State Secretariat for Economic Affairs (SECO) in its latest forecast, lowered Switzerland's economic growth outlook to 1.6% in 2017, down from the forecast of 1.8% it projected in December, while leaving the growth forecast for 2018 unchanged at 1.9%.

In the Asian session, at GMT0400, the pair is trading at 0.9943, with the USD trading 0.12% higher against the CHF from yesterday's close.

The pair is expected to find support at 0.9912, and a fall through could take it to the next support level of 0.9881. The pair is expected to find its first resistance at 0.9982, and a rise through could take it to the next resistance level of 1.0021.

Going ahead, traders would focus on Swiss National Bank's quarterly bulletin report, slated to release later in the day.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

USD/CAD: Canada’s Retail Sales Posted Its Largest Gain In Almost 7 Years In January

For the 24 hours to 23:00 GMT, the USD rose 0.1% against the CAD and closed at 1.3352.

On the economic front, retail sales in Canada rebounded more-than-anticipated by 2.2% in January, accelerating at its strongest pace in nearly seven years, suggesting that the economy is gaining momentum. Meanwhile markets expected for an advance of 1.5%, following a revised drop of 0.4% in the previous month.

In the Asian session, at GMT0400, the pair is trading at 1.3375, with the USD trading 0.17% higher against the CAD from yesterday's close.

The pair is expected to find support at 1.3296, and a fall through could take it to the next support level of 1.3217. The pair is expected to find its first resistance at 1.342, and a rise through could take it to the next resistance level of 1.3465.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

US Dollar Fails To Reverse Bearish Trend

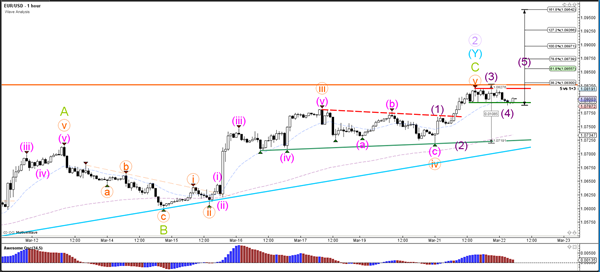

Currency pair EUR/USD

The US Dollar is struggling to show any signs of strength as the EUR/USD keeps pushing higher and higher in a bullish trend channel (red/blue lines). A push above the horizontal resistance (orange) invalidates the wave 2 (purple), which seems likely at the moment when considering deep bullish retracement.

The EUR/USD broke the resistance trend line (dotted red) of the contracting. A break above the resistance could see price move higher within a wave 5 (purple) towards the Fibonacci targets of wave 5 vs 1+3.

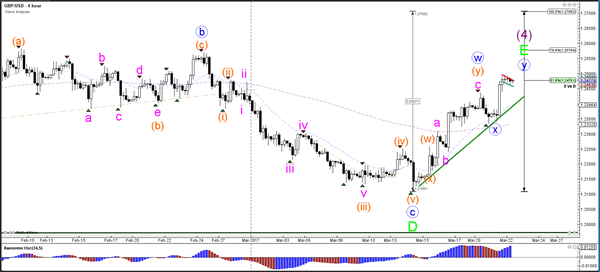

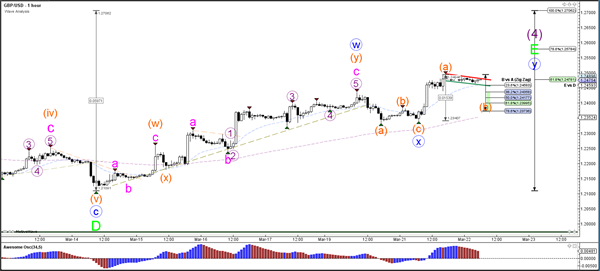

Currency pair GBP/USD

After bouncing at the wave X (blue), the GBP/USD has reached the 61.8% Fibonacci level at 1.25 of a wave E (green) triangle formation. A bullish breakout could see the GBP/USD continue towards the 78.6% Fibonacci resistance level.

The GBP/USD completed the ABC zigzag (orange) within wave X (blue). A retracement could see price challenge and potentially bounce at the Fibonacci levels wave B vs A.

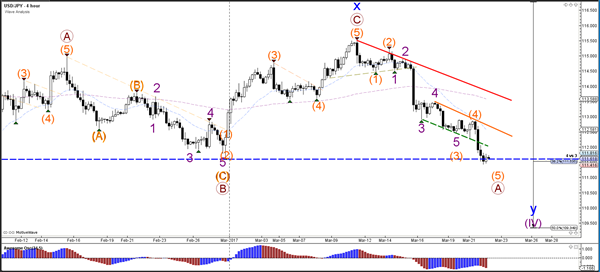

Currency pair USD/JPY

The USD/JPY broke below the bottom (dotted blue) which has changed the wave structure compared to yesterday. The wave 1-2 has been replaced by an ABC (brown) zigzag within wave X (blue). The bearish correction could see a fall from the 383.2% Fibonacci level towards the 50% Fib.

The USD/JPY could be building a 5 wave (purple/orange) within a larger wave A (brown).

European Open Briefing

Global Markets:

- Asian stock markets: Nikkei down 1.90 %, Shanghai Composite fell 0.75 %, Hang Seng declined 1.30 %, ASX 200 lost 1.55 %

- Commodities: Gold at $1245 (-0.10 %), Silver at $17.54 (-0.25 %), WTI Oil at $48.10 (-0.30 %), Brent Oil at $50.80 (-0.35 %)

- Rates: US 10 year yield at 2.42, UK 10 year yield at 1.26, German 10 year yield at 0.46

News & Data:

- Australia Westpac Leading Index (MoM) Feb: -0.07% (prior 0.03%)

- Japan Trade Balance (Feb): 813bln (Est 822bln) (Prior -1,087bln)

- Japan Exports (YoY): 11.3 % (Est 10.6 %) (Prior 1.3 %)

- Japan Imports (YoY): 1.2 % (Est 0.6 %) (Prior 8.5 %)

- Japan All Industry Activity (MoM) Jan: 0.1% (Est 0.00%) (Prior -0.2% rev)

- PBoC Fixes USDCNY Reference Rate At 6.8889 (Prev 6.9071)

Markets Update:

Most of the Asian stock indices declined overnight. Sentiment turned negative in yesterday's US trading session, as investors are starting to doubt that US President Donald Trump will be able to pass his planned tax reform. The S&P 500 finished the trading day with a loss greater than 1 percent. Overnight, the Nikkei lost almost 2 percent on the day, while the Australian ASX 200 fell around 1.50 percent.

The Dollar remains under pressure as well. EUR/USD broke above 1.08 yesterday, and while it failed to clear resistance at 1.0825, a breakout seems imminent. Meanwhile, GBP/USD broke above trendline resistance and is approaching 1.25.

Only the commodity currencies failed to benefit from the Dollar weakness. The Australian and New Zealand Dollar fell as the decrease in risk appetite weighed on the currencies. AUD/USD declined from 0.7750 to 0.7650, while NZD/USD dropped from 0.7090 to 0.7015.

Upcoming Events:

- 09:00 GMT – Euro Zone Current Account

- 13:00 GMT – US House Price Index

- 14:00 GMT – US Existing Home Sales

- 14:30 GMT – US Crude Oil Inventories

- 20:00 GMT – RBNZ Rate Decision

- 20:00 GMT – RBNZ Rate Statement