Sample Category Title

Trade Idea: EUR/GBP – Buy at 0.8620

EUR/GBP - 0.8681

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term down

Original strategy :

Buy at 0.8620, Target: 0.8750, Stop: 0.8580

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.8620, Target: 0.8750, Stop: 0.8580

Position : -

Target : -

Stop : -

The single currency has remained under near term downward pressure, retaining our view that further consolidation below resistance at 0.8788 would be seen and initial downside risk remains for pullback to 0.8645-48 (38.2% Fibonacci retracement of 0.8422-0.8788), however, reckon downside would be limited to 0.8615-20 and bring another rise later, break of 0.8760 would suggest the pullback from 0.8788 has ended, bring retest of this level, above there would extend the rise from 0.8403 low to 0.8800 but loss of upward momentum should prevent sharp move beyond 0.8825-30 and price should falter well below 0.8850.

In view of this, we are looking to buy euro on subsequent pullback as 0.8615-20 should limit downside. Below 0.8605 (50% Fibonacci retracement of 0.8422-0.8788) would defer and suggest top is possibly formed, risk test of 0.8560-65 (61.8% Fibonacci retracement) but support at 0.8547 should remain intact.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

DAX – Steady Despite Soft German Inflation Report

The DAX Index has edged higher in the Monday session. Currently, the DAX is at 12,055.65. On the release front, it's a quiet start to the week in the eurozone. German CPI slipped to 0.2%, well off the forecast of 0.7%. We'll also hear from German Buba President Jens Weidmann.

Last week's Dutch election was good news for backers of the EU. There had been fears that the far right-wing Freedom Party of Geert Wilders would make substantial gains. Wilders is a fierce critic of the EU and pledged to hold a referendum on the Netherland's membership in the EU (with the catchy slogan "Nexit"). Dutch Prime Minister Mark Rutte won the election handily, bringing a sigh of relief from governments in Western Europe. Still, Wilders commands the second largest party in the country and his party will be a major player on the Dutch political scene. Next stop is France, which goes to the polls in April. Polls have far rightist Marine Le Pen and centrist Emmanuel Macron and running neck-and-neck in the first round of the presidential election on April 23. Still, Macron is expected to win in the second-round vote in May.

As widely expected, Federal Reserve raised rates by a quarter-point last week. However, the US dollar responded with broad losses. Why the negative response? Firstly, there was disappointment in the markets with the Fed policy statement, which was more dovish than expected. The rate move was priced in at over 90 percent, and there had been speculation that a red-hot US economy would propel the Fed to accelerate its pace of monetary tightening, with possibly four rate hikes this year. Instead, Fed Chair Janet Yellen reiterated that further rate hikes would be "gradual" and the Fed made no changes to its "dot plot", with a projection for three rate hikes in 2017. As well, the US dollar may have lost ground due to traders and investors acting on "buy on rumor, sell on fact". What's next for Janet Yellen & Co? Analysts don't expect another rate move in May, while a hike in June is currently priced in at 50%. The markets will be looking for clues about the Fed's monetary plans. A host of FOMC members will be speaking this weak, highlighted by Janet Yellen's speech on Thursday at an event in Washington. The market will be looking for clues regarding monetary policy. In the past, Fed policymakers have presented conflicting positions, and if the market senses divisions within the Fed, the US dollar could lose ground.

Trade Idea: USD/CAD – Stand aside

USD/CAD - 1.3354

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term up

New strategy :

Stand aside

Position: -

Target: -

Stop:-

Although the greenback found support at 1.3276 late last week and consolidation above this level would be seen initially, reckon upside would be limited to 1.3390-00 and price should falter below previous support at 1.3421 (now resistance), bring another decline later, below said support at 1.3276 would add credence to our bearish view that top has been made at 1.3535 and extend the fall from there for retracement of recent upmove to 1.3235-40 (61.8% Fibonacci retracement of 1.3056-1.3535) but reckon previous resistance at 1.3210 would hold.

In view of this, would be prudent to stand aside in the meantime. Above previous support at 1.3421 (now resistance) would suggest low is formed, bring a stronger rebound to 1.3450 and possibly test of resistance at 1.3479, however, only break of 1.3495 resistance would indicate the pullback from 1.3535 has ended and bring retest of this level later.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

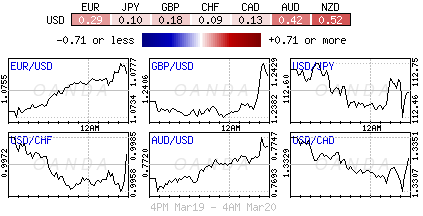

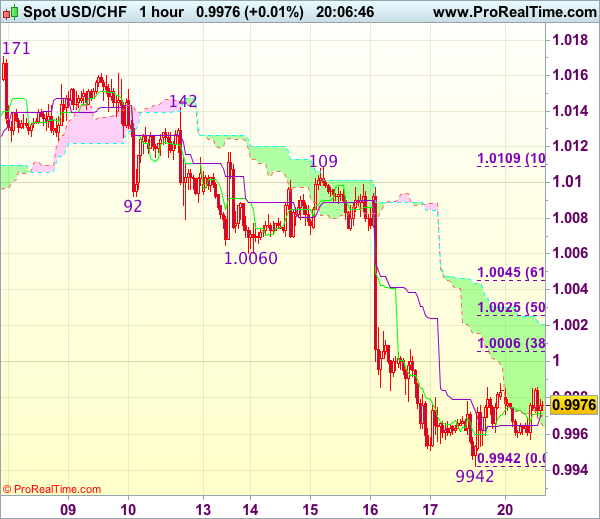

Trade Idea Update: USD/CHF – Sell at 1.0020

USD/CHF - 0.9975

Original strategy :

Sell at 1.0020, Target: 0.9920, Stop: 1.0055

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0020, Target: 0.9920, Stop: 1.0055

Position : -

Target : -

Stop : -

As the greenback has rebounded after finding support at 0.9942 on Friday, suggesting consolidation above this level would be seen and corrective bounce to 1.0005-10 (38.2% Fibonacci retracement of 1.0109-0.9942) cannot be ruled out, however, reckon upside would be limited to 1.0025 (50% Fibonacci retracement) and bring another decline later. Below said support at 0.9942 would extend recent decline from 1.0171 to 0.9920-25 but loss of near term downward momentum should prevent sharp fall below 0.9900 and reckon 0.9870-75 would hold from here.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 1.0025 (current level of the upper Kumo) should limit upside and bring another decline. Only above previous support at 1.0060 (now resistance) would abort and signal low is formed instead, risk rebound to 1.0090-95 first.

Trade Idea Update: GBP/USD – Buy at 1.2310

GBP/USD - 1.2378

Original strategy :

Buy at 1.2325, Target: 1.2445, Stop: 1.2290

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2310, Target: 1.2435, Stop: 1.2275

Position : -

Target : -

Stop : -

As cable has retreated after intra-day brief rise to 1.2436, suggesting consolidation below this level would be seen and pullback to support at 1.2335 cannot be ruled out, however, reckon downside would be limited to 1.2310 (previous resistance now support) and bring another rise later, above said resistance at 1.2436 would extend recent upmove from 1.2109 (this month’s low) to 1.2450 but loss of near term momentum should prevent sharp move beyond previous resistance at 1.2479, risk from there has increased for a retreat to take place later.

In view of this, would not chase this move from here and we are looking to buy cable on pullback as said previous resistance at 1.2310 should limit downside and bring another rise. Below 1.2270-75 (50% Fibonacci retracement of 1.2109-1.2436) would defer and suggest top is possibly formed, risk correction to 1.2241 support.

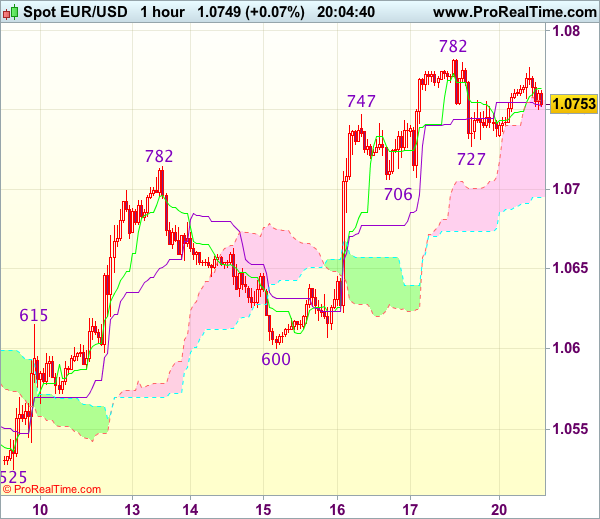

Trade Idea Update: EUR/USD – Buy at 1.0700

EUR/USD - 1.0745

Original strategy :

Buy at 1.0710, Target: 1.0810, Stop: 1.0675

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0700, Target: 1.0800, Stop: 1.0665

Position : -

Target : -

Stop : -

As the single currency has maintained a firm undertone after last week’s rally, suggesting recent erratic upmove from 1.0493 low is still in progress and may extend further gain towards previous chart resistance at 1.0829, however, loss of near term upward momentum should prevent sharp move beyond 1.0850-60 and price should falter well below 1.0890-00, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and we are looking to buy euro on subsequent pullback as 1.0706 support should limit downside and bring another rise later. Below 1.0675-80 would defer and suggest top is possibly formed, risk weakness to 1.0640 (previous resistance now support) but still reckon indicated support at 1.0600 would remain intact.

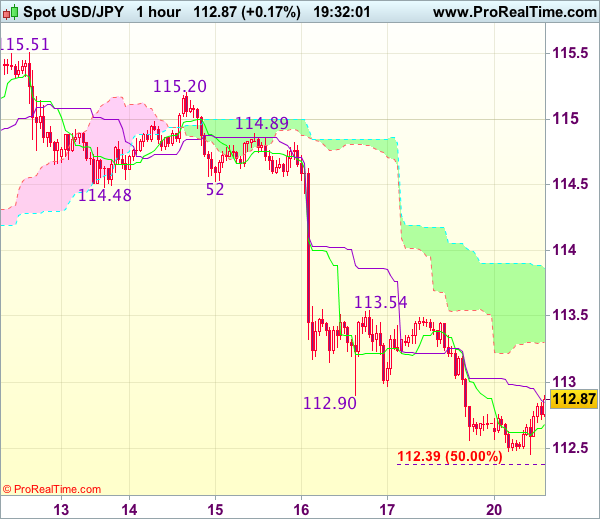

Trade Idea Update: USD/JPY – Sell at 113.50

USD/JPY - 112.86

Original strategy :

Sell at 113.50, Target: 112.40, Stop: 113.85

Position : -

Target : -

Stop : -

New strategy :

Sell at 113.50, Target: 112.40, Stop: 113.85

Position : -

Target : -

Stop : -

As the greenback has recovered after marginal fall to 112.46, suggesting minor consolidation above this level would be seen and corrective bounce to the lower Kumo (now at 113.25) cannot be ruled out, however, reckon 113.51-54 (38.2% Fibonacci retracement of 115.20-112.46 and previous resistance) would limit upside and bring another decline later. Below said support at 112.46 would extend weakness to 112.35-39 (50% projection of 115.20-112.90 measuring from 113.54), then 112.10-15 (61.8% projection) but loss of downward momentum should prevent sharp fall below previous support at 111.69, risk from there has increased for a rebound to take place later.

In view of this, would not chase this fall here and would be prudent to sell dollar on subsequent recovery as said resistance at 113.54 should limit upside, bring another decline later. Only above the upper Kumo (now at 113.90) would abort and signal low is formed instead, bring rebound to 114.20-25 later.

GBPUSD: Bullish, Targeting Further Upside Pressure

GBPUSD: The pair remains on the offensive leaving risk higher in the days ahead. Support lies at the 1.2350 level where a break will turn attention to the 1.2300 level. Further down, support lies at the 1.2250 level. Below here will set the stage for more weakness towards the 1.2200 level. Conversely, resistance stands at the 1.2450 levels with a turn above here allowing more strength to build up towards the 1.2500 level. Further out, resistance resides at the 1.2550 level followed by the 1.2600 level. On the whole, GBPUSD continues to face upside pressure.

Speeches from Trump and Central Bankers Key Today

- Central bank speeches eyed as Fed, BoE and ECB turn more hawkish;

- Oil lower as US rigs rise again last week to 631, highest since September 2015;

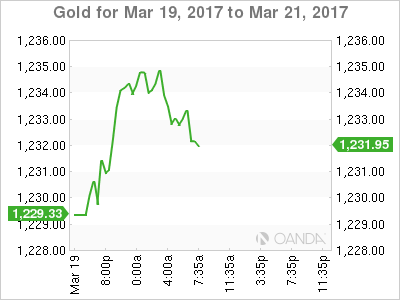

- Gold spurred on by weaker dollar but rally may be running out of steam.

US futures are pointing to a marginally lower open on Monday, as traders eye tonight's speech from Donald Trump as well as a few other from policy makers from the Federal Reserve, Bank of England and ECB.

It's looking a little quiet on the economic data side today but speeches from policy makers from three major central banks and the President of the US should keep things interesting. All three central banks have been erring on the hawkish side recently, with the Fed raising interest rates last week, one BoE policy maker dissenting on leaving rates unchanged – preferring instead to hike – and the ECB having recently cut its asset purchases and suggested it could raise rates before it ends QE.

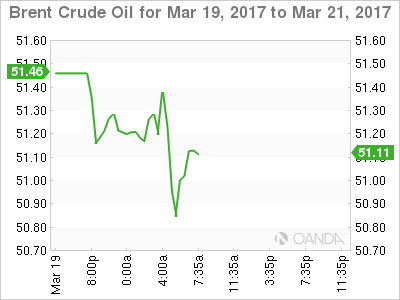

Oil is trading down around 1% today after oil rig data from Baker Hughes on Friday reported another increase, this time of 14 bringing the total to 631. The US shale industry has been quick to respond to last year's rebound in oil prices which was largely driven by an agreement between OPEC and some non-OPEC producers to cut output.

While producers remain confident that the measures taken and high level of compliance will bring the market into balance, price action would suggest traders are not buying it. The resurgence in US shale is overshadowing the efforts of other producers for now and while US stockpiles continue to build, the cuts still far outweigh the gains in the US. Still, an extension to the cuts may be necessary before the market will rebalance, which may be easier said than done as that would involve conceding further market share to the US.

Gold is currently trading higher again on the day but the rally appears to be losing some steam. While the gains since the start of the year were being spurred on by growing political risks, with the gains in February having coincided with a rally in the dollar which is unusual, the recent moves appear to be being driven purely by the softness we've seen in the greenback since last week's rate hike. To the downside, Gold could face a test around $1,220, with $1,200 below being a potentially important level. To the upside, $1,236-1,237 should be an interesting test of resistance.

EUR to Focus on French Presidential Debate

Monday March 20: Five things the markets are talking about

Market volatility remains low across markets from equities to currencies and fixed-income as dealers and investors attempt to evaluate how sustainable the hopeful global economic recovery is.

Investor focus turns away from last week's central bank statements to U.S policy or Trumponomics. The White House is heading for a busy week, with anticipated House health care legislation coming to the floor and the Senate starting hearings on a Supreme Court nominee (Gorsuch).

Currently, the 'mighty' U.S. dollar is heading for its longest losing streak since last Novembers U.S Presidential election, while most major equity indexes falter near their all-time high, while treasury yields trade atop of the recent lows.

On the weekend, the G20 official communiqué upheld their commitment against competitive "devaluation," but also omitted language on promoting free trade (see below).

On the data front, investors this week will be kept busy by Euro and Japanese flash PMI's. In the U.K, price data and retail sales will be released for February. Minutes of the BoJ's January meeting and the RBA's March meeting will be published, while the RBNZ will announce its monetary policy decision.

1. Global stocks see mixed results

Last week was the best week since January for global equities.

However overnight, it was a mixed performance. Equities have retreated in Europe, Australia and New Zealand. Japan's stock market was closed for a holiday, while indexes rose in emerging markets.

The MSCI's broadest index of Asia-Pacific shares ex-Japan added +0.3%. In Hong Kong, the Hang Seng climbed +0.7%, while Chinese shares were mixed with the CSI 300 down -0.1%, while the Shanghai Composite added +0.1%. Down-under, Aussie shares closed down -0.36%.

Elsewhere, the MSCI's emerging markets index added +0.4% to hit its highest level in more than two-years.

In Europe, equity indices are trading lower as market participants digest the weekends G20 communiqué. Banking stocks are putting pressure on the Eurostoxx while energy; commodity and mining stocks trade lower in the FTSE 100.

U.S stocks are set to open in the red (-0.2%).

Indices: Stoxx50 -0.2% at 3,436, FTSE -0.2% at 7,411, DAX -0.3% at 12,055, CAC-40 -0.4% at 5,011, IBEX-35 -0.3% at 10,215, FTSE MIB -0.3% at 20,016, SMI flat at 8,698, S&P 500 Futures -0.2%

2. Higher U.S oil production offsetting OPEC's supply cuts

Crude oil prices start the week on the back foot, pressured by rising U.S drilling activity and steady supplies from OPEC countries despite last November's agreement of production cuts.

Ahead of the U.S open, Brent crude futures are down -34c, or -0.66%, at +$51.42 per barrel. U.S West Texas Intermediate (WTI or light crude) has slipped -48c, or -0.98%, to +$48.30 a barrel.

Friday's date from Baker Hughes showed that U.S drillers added +14 oil rigs in the week to March 17, bringing the total count up to +631, the most in 18-months, extending a recovery that is expected to boost U.S shale production by the most in six-months in April.

Gold prices have edged up (up +0.2% to +$1,231.05 per ounce) as the 'mighty' dollar stays on the defensive after last week's "less hawkish" tone from the Fed, despite the rate hike. Yellen's cautious guidance has the market pricing in almost no chance of another rate rise in May, but rises to 50-50 for June.

Note: Markets are bracing for a packed week of Fed messaging - this week there are nine different U.S policy makers set to speak, including Chair Janet Yellen on Thursday.

3. U.S Treasury yields lower, ECB futures tightening

Currently, to many the possibility of the ECB raising interest rates before its QE program ends is a "tail risk." However, its not stopping the market from pricing in the possibility of incremental "small" hikes.

Looking at the Euro curve, FI dealers are pricing in some tightening pressures to the ECB's deposit rate (-0.4%) over the next 18-months. Dealers see a +10 bps rise by January 2018, a +15 bps rise by May 18 and a +20 bps rise by August 2018. To many, this would still be considered a "dovish" hike.

Elsewhere, U.S 10-year Treasuries are little changed at +2.50% after falling -4 bps on Friday. The yield on Aussie 10's have dropped -3 bps to +2.82%.

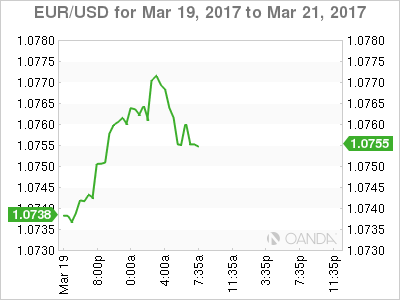

4. EUR to focus on French Presidential Debate

The EUR and GBP have both benefitted from a weaker dollar after the G-20 statement dropped a pledge to promote free trade, reviving concerns about U.S. policy causing disruption to trade. The dollar is also continuing its weakness from a "less hawkish" message from the Fed.

EUR/USD is up +0.2% at €1.0767, while GBP/USD has rallied to a three-week high £1.2436. USD/JPY has dropped to trade atop a three-week low around ¥112.47.

Note: EUR's gains may be limited as market focus shifts to today's French Presidential TV debate. Any narrowing of centrist candidate Macron's lead after the debate could indeed instigate fresh EUR selling.

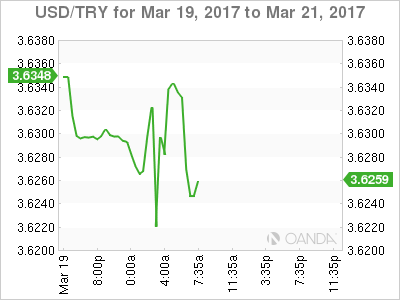

Elsewhere, the KRW (+1.1% to $1,116) trades at a five month high outright amid continued appetite for the currency as the political picture becomes somewhat clearer. TRY ($3.6338) is recovering some of the falls prompted by Moody's downgrading Turkey's sovereign rating outlook to negative from stable late Friday.

5. G20's communiqué

The weekends post-meeting communiqué retained language on avoiding currency manipulation - previously aimed chiefly at Japan and China - but it omitted a call for 'free trade.' This may be considered a win for the U.S as it opens the door to more overt efforts by the Trump administration to shift the balance of its international relationships.

U.S Treasury Sec Mnuchin: U.S wants free, but fair and balanced trade. NAFTA would have to be reviewed, some WTO rules needed to be better enforced and older agreements may have to be renegotiated.

German Fin Min Schaeuble: G20 communiqué was adopted unanimously. G20 trade discussions were complicated; there was broad consensus that 'open trade' is necessary to strengthen global growth.

Bundesbank President Weidmann: Meeting was marked by intense struggle for a common position, still much to discuss on trade. Agreed now is the time to implement structural reforms.

Japan Fin Min Aso: No one at the meeting remarked that they were against free trade and confirmed importance of free trade despite language in communiqué.

China Fin Min Xiao Jie: Unwaveringly supports free trade and investment, opposes protectionism.

IMF's Lagarde: Global cooperation and pursuing the right policies can help achieve "strong, sustained, balanced, and inclusive growth, while the wrong ones could stop the new momentum in its tracks."