Sample Category Title

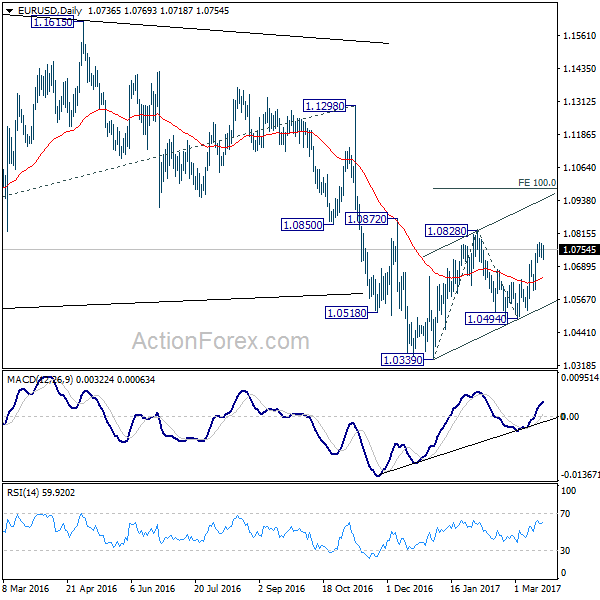

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0716; (P) 1.0747 (R1) 1.0769; More.....

EUR/USD lost some upside momentum with 4 hour MACD crossed below signal line. But with 1.0639 minor support intact, further rise is expected. Corrective rise from 1.0339 is still in progress and break of 1.0828 will target 100% projection of 1.0339 to 1.0828 from 1.0494 at 1.0983. Since such rise is viewed as a corrective move, we'd expect upside to be limited by 1.0983 to bring larger down trend resumption eventually. On the downside, break of 1.0639 minor support will turn bias back to the downside for 1.0494 support.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115.

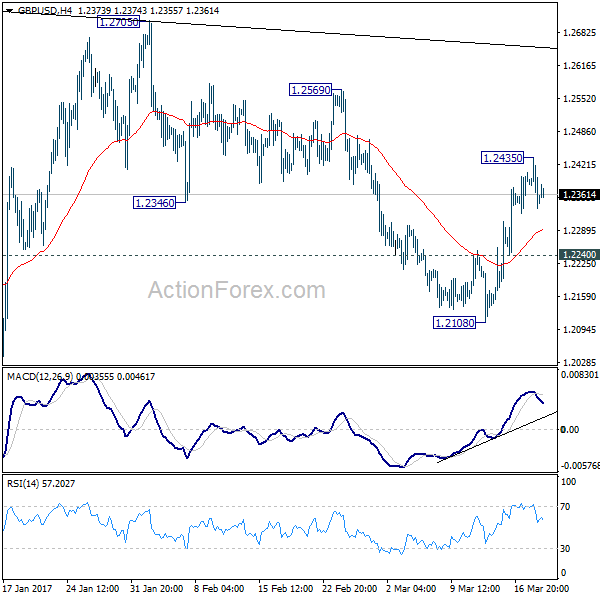

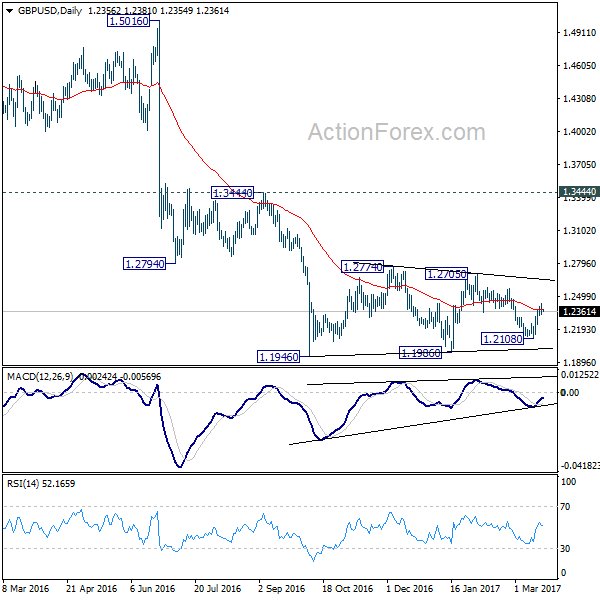

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2316; (P) 1.2375; (R1) 1.2417; More...

GBP/USD lost upside momentum after hitting 1.2435, with 4 hour MACD crossed below signal line. Intraday bias is turned neutral first. Price actions from 1.1946 are still seen as a consolidation pattern. Above 1.2435 will target 1.2705/74 resistance zone. But we'd expect strong resistance from 1.2705/2774 to limit upside. Meanwhile, break of 1.2240 minor support will turn bias back to the downside for 1.2108 support. Though, sustained break of 1.2774 will extend the rise towards 1.3444 key resistance level.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

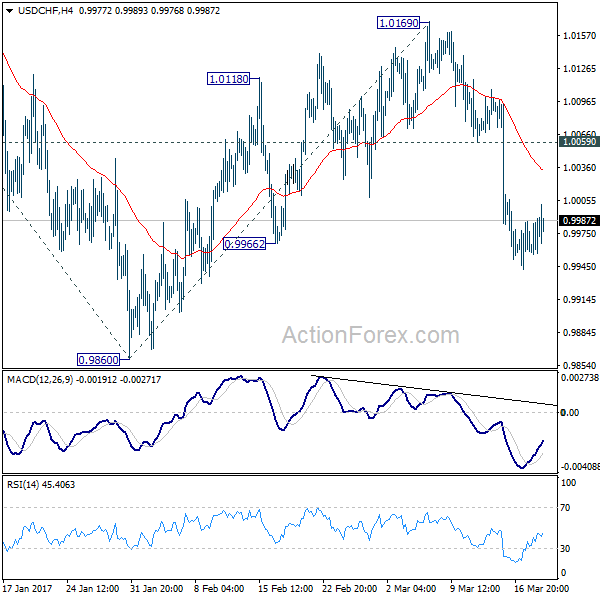

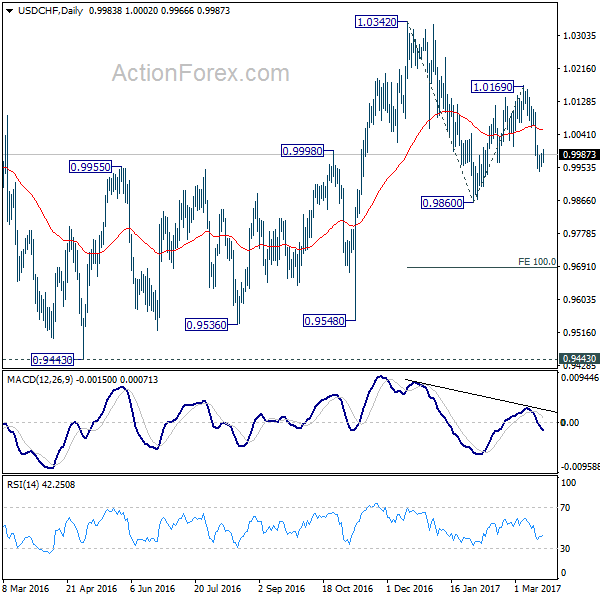

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9965; (P) 0.9978; (R1) 0.9998; More.....

USD/CHF lost some downside momentum with 4 hour MACD crossed above signal line. But with 1.0059 minor resistance intact, deeper fall is expected. We'd holding on to the view that recovery from 0.9860 has completed at 1.0169 and whole decline from 1.0342 is resuming. Break of 0.9860 will target 100% projection of 1.0342 to 0.9860 from 1.0169 at 0.9687. Nonetheless, on the upside, break of 1.0059 will turn bias back to the upside for 1.0169 resistance instead.

In the bigger picture, USD/CHF is staying in medium term sideway pattern between 0.9443/1.0342. In any case, decisive break of 1.0342 resistance is needed to confirm underlying strength. Otherwise, we'll stay neutral in the pair first. In case of another fall, we'd expect strong support from 0.9443/9548 support zone.

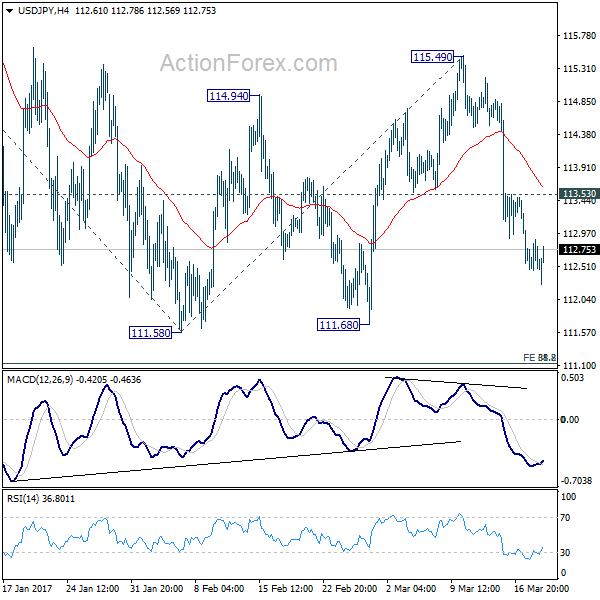

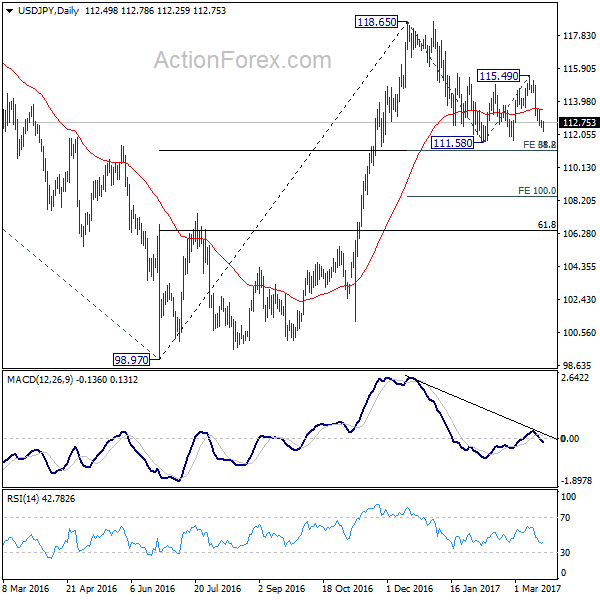

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.37; (P) 112.63; (R1) 112.82; More...

USD/JPY lost some downside momentum with 4 hour MACD crossed above signal line. But with 113.53 minor resistance intact, deeper decline is still expected. We're holding on to the view that consolidation pattern from 111.58 has completed with three waves up to 115.49. And decline from 118.65 is likely resuming. Further fall should be seen through 111.58 to 111.12/13 cluster support. This level represents 61.8% projection of 118.65 to 111.58 from 115.49 at 111.12 and 38.2% retracement of 98.97 to 118.65 at 111.13. At this point, we'd tentatively expect strong support from 111.12/13 cluster support to contain downside. On the upside, above 113.53 minor resistance will turn bias back to the upside for 115.49 resistance. However, sustained break of 111.12/13 will bring deeper decline to 100% projection of 118.65 to 111.58 from 115.49 at 108.42.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Nonetheless, sustained trading below 55 week EMA (now at 111.19) will extend the consolidation from 125.85 with another fall through 98.97 before completion.

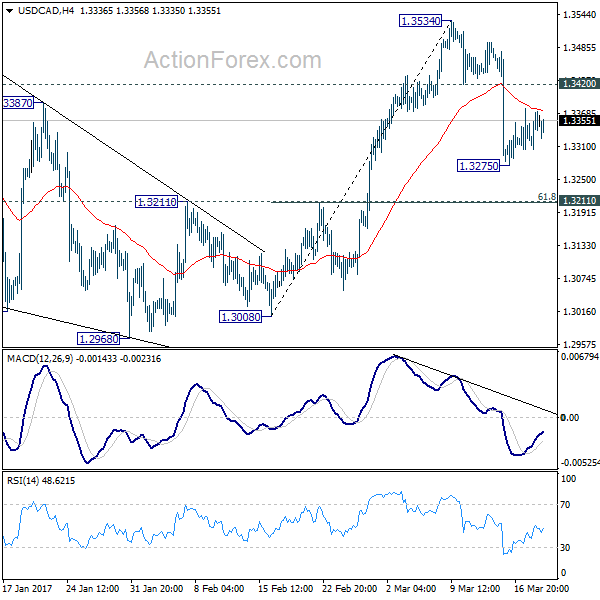

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3313; (P) 1.3343; (R1) 1.3382; More...

USD/CAD is staying in tight range above 1.3275 temporary low and intraday bias remains neutral first. Fall from 1.3534 might extend lower. But still, such decline is viewed as a correction pattern. Hence, we'd expect downside to be contained by 1.3211 cluster level (61.8% retracement of 1.3008 to 1.3534 at 1.3209) and bring rebound. On the upside, above 1.3420 minor resistance will indicate that the pull back is completed and turn bias back to the upside for 1.3534 resistance and then 1.3598. However, sustained break of 1.3211 will dampen this view and target 1.2968 key support level next.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. Break of 1.2968 wold at least bring at retest of 1.2460 low. However, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

Great Debate

Great French Debate

The first great French debate has the polls showing Macaron performing well and the markets were quick to react a.The EURO has recovered all its pre-debate risk off, bouncing pointedly higher with S&P equities in tow as risk appetite remains sturdy post debate

French debate poll by Elsie: most voters (29%) said Macron was the winner of the debate. Fillon and Le Pen were even with 11% of the votes, while Melenchon earned 20%.

Having held above the 1.0700 support, the Euro continues to reassert itself post-debate. With EURUSD traders gunning higher on the apparent pivot in ECB policy, in particular with the uber-doves like Visco flying to the hawks nest, it would suggest a test of the critical 1.0800 is in the offing with the market firmly in buy the dip mode.

RBA Minutes

All in all the minutes were upbeat despite some concerns over labour market slack, but the positive assessments of global affairs should balance out those issues. The problem for the Aussie is that the market is long and there was not enough meat in the minutes for dealers add to their positions. Overall, in the absence of domestic data, I suspect the long Aussie players will be looking for a continuation of the broader dollar weakness to cement their view and push above this huge .7750-75 resistance barriers.

Yen

Although USDJPY traded heavy early in the session, resilient risk appetite has underpinned today’s movements. I think the near-term outlook comes down to how aggressive the continuation of near term USD unwinds transpires, and at this stage, I suspect with latest pressure point, the French debate sidestepped, I suspect the USDJPY bulls took a sigh of relief while the near-term dollar bears quickly gave up the game. Back to the range I suspect. while the market pivots to the trade narrative and how near-term US administration policies will impact the global supply chain

Market Morning Briefing

STOCKS

Most equity indices are possibly in a sideways consolidation mode and may continue for some time. Broad range-bound movement is possible in the next couple of weeks.

Dow (20905.86, -0.04%) and Dax (12052.90, -0.35%) are almost stable without any major movement just now. As mentioned earlier, both could trade sideways for another couple of sessions before starting to move up. Dow has resistances coming up near 21200 and 21300 which if holds could possibly keep the index in sideways range for a longer time than expected. Dax may remain below 12156 for the next 2-sessions at least.

Nikkei (19469.62, -0.27%) is stuck within the support and resistance levels of 19200 and 19600 respectively and while that holds, we could expect the sideways consolidation to continue in the near term.

Shanghai (3255.80, +0.15%) is trading above 3200 and while that holds, medium term looks bullish towards 3300. Movement could be slow in the near term but eventually prices may move higher.

Nifty (9126.85, -0.36%) has been coming off in the last 2-sessions and could test support near 8990-9100 before again bouncing back towards 9200 and higher. Medium term looks bullish.

COMMODITIES

Gold (1228) is trading within the range of 1215-1245. Unless it will manage to close above 1240-45, it will be difficult for gold to move higher.

Silver (16.34) is trading slightly lower from its immediate resistance at 17.45 levels. The bias will remain bearish while it is trading below 17.45-50 levels.

Copper (2.64) was unable to close above its pivot at 2.66-70 of its recent trading range of 2.55-83. The chances of seeing 2.55 are much greater now.

Brent (51.87) and WTI (48.40) both are trading within their narrow ranges of 50-52 and 46-50. Considering the short term oversold sate, we may see some profit taking rally towards their respective resistances. The trend is still bearish in the near to medium term time frame thus any corrective bounce may face selling pressure at the higher levels. Brent-WTI ratio (2.23) may trade below 2.00 as it found resistance at 2.5 levels.

FOREX

Little movement is seen in the markets as expected. A more dovish than expected stance of the US Fed translates into a less wider than expected policy divergence between the Fed and the ECB, keeping the German-US interest rate differential higher and Dollar weaker.

Dollar Index (100.18) remains almost unchanged with the near term target remaining the same at 99.00 and resistance coming at 100.70-101.00.

Euro (1.0761) has been stuck in the narrow range of 1.07-1.08 for the last 4 sessions but it still remains to be seen if the resistance of 1.08 manages to push it down or not. Repeat - the current net short position of the speculators is the smallest since May’16, which may well turn out to be a contra-indicator for a top formation.

Dollar-Yen (112.70) is stable near our target/support of 112.00-111.70, little changed from the levels overnight. As discussed previously, only a break below 111.70 may open up much lower levels of 110.00 and even 108.50-00.

Pound (1.2362) is struggling in our resistance zone of 1.2430-40 just as expected and a failure to rise above 1.2440 soon may drag it down to 1.2300-1.2270 levels or lower.

Aussie (0.7710) has hit the resistance of 0.7750 last night but no buyers were found at the higher levels to continue the rise. We reiterate - this long term resistance area of 0.7750-0.7850 is a very significant make or break zone which, if overcome, may determine the path for the next few months but it remains to be seen if Aussie manages a break above 0.7750-0.7850 immediately or not.

Dollar Rupee (65.36) gained another 10 paisa in the last session but the range of 66.20-70 is expected to hold for the next few sessions.

INTEREST RATES

The US yields have fallen sharply contrary to our expectation of a pause. The 5yr (2%), 10YR (2.48%) and the 30Yr (3.09%) are 1-2bps lower and could come down towards 1.9%, 2.405 and 3.0% respectively in the near term before bouncing back from there.

The German-US 2yr (-2.08%) has broken above the immediate channel resistance and if it continues to move higher in the coming sessions, indicating a rise in Euro in the near term. But the German-US 10YR (-2.04%) is heading towards resistance above current levels and if some rejection is seen there, it could possibly limit the upside for Euro.

The US-Japan 10Yr yield spread (2.41%) may come down towards 2.35% giving some more scope for yen strength before a sharp bounce is seen.

Foreign Exchange Market Commentary

EUR/USD

Major pairs closed the day little changed, as a Japanese holiday and a light macroeconomic calendar kept investors in cautious mode. The dollar recovered from an early slide, underpinned by news that the Brexit has an official date: March 29th. Nevertheless, the greenback retains the week tone triggered last week by the US Fed, settling against the EUR at 1.0738. There were some minor releases in Europe, including wage growth, which increased in the last quarter of 2016 to 1.6% from a previous downwardly revised 1.4%, a sign that underlying price pressures are still weak in the region. Also, Germany released its February PPI data, which came in as expected, up 0.2% in February when compared to the previous month, and by 3.1% yearly basis, beating expectations of a 2.9% advance. In the US, Fed's Evans repeated what the market already knew that three hikes are possible for this year as policy makers are confident on inflation going up.

US President Trump is set to speak at a rally at the Kentucky Exposition Center, in Louisville at the beginning of the Asian session, but the macroeconomic calendar will remain scarce at both shores of the Atlantic on Tuesday.

From a technical point of view, the intraday movement seems barely corrective, as the price held above the immediate short term support at 1.0730, and the 4 hours chart shows that the price is a few pips above a bullish 20 SMA, although technical indicators head south within positive territory, with the Momentum about to cross its mid-line towards the downside. It would take a break below 1.0700 however, to confirm a downward move, while only beyond 1.0785, the pair will be able to regain its upward strength.

Support levels: 1.0730 1.0700 1.0660

Resistance levels: 1.0785 1.0820 1.0850

USD/JPY

The USD/JPY pair extended its multi-week decline by a few pips to 112.45 at the beginning of the week, ending the day not far above it and having topped for the day at 112.89. The Japanese yen appreciated as US Treasury yields kept falling this Monday, with the 10-year benchmark down to 2.48% from previous 2.50%. There are no news scheduled in Japan for the upcoming Asian session, which means that the pair will likely continue trading on sentiment. From a technical point of view, the risk remains towards the downside, as the price held well below its 100 and 200 SMAs both still horizontal far above the current level in the 4 hours chart, whilst the RSI indicator holds flat at oversold levels and the Momentum hovers back and forth below its 100 line. A downward acceleration below 112.50 should see the pair nearing the 112.00 level, where the pair has the 38.2% retracement of its late 2016 monthly rally, with scope to extend afterwards towards the 111.60 region, where the pair bottomed multiple times this year.

Support levels: 112.50 112.10 111.65

Resistance levels: 113.05 113.50 114.00

GBP/USD

The British Pound was the best performer this Monday, plunging from 1.2435 to 1.2334 following news indicating that the UK government will trigger the Brexit process next March 29, starting a two-year time frame to get a smooth deal that satisfies both parts. Following the announcement, EU Commission chief spokesman Margaritis Schinas said at a briefing in Brussels that the EU is ready to begin talks "immediately" and that they had a comprehensive plan in place. The GBP/USD pair settled for the day a couple of pips below 1.2345, a major Fibonacci support and February's low, while in the 4 hours chart, the price is also battling around a bullish 20 SMA and technical indicators have retreated sharply, with the Momentum indicator already within bearish territory and the RSI heading south around 54, all of which increases chances of a downward extension for the upcoming sessions. The UK will release multiple inflation figures this Tuesday, including PPI, CPI and retail price indexes for February, all of which will set the tone for the Pound probably for the next of the week.

Support levels: 1.2345 1.2300 1.2260

Resistance levels: 1.2425 1.2470 1.2510

GOLD

Gold prices edged higher this Monday, with spot settling at $1,234.12 a troy ounce, its highest settlement for this March. Prices for the commodity held firm, underpinned by a US Fed that's in no rush to raise rates and political uncertainty in the EU. A light macroeconomic calendar kept volumes low, but the commodity managed to recover above the 1,230.10 level, the 23.6% retracement of the December/February rally, now the immediate support. In the daily chart, the metal has also surpassed its 20 DMA, whilst technical indicators have extended their recoveries, now heading modestly higher within neutral territory. The 200 DMA stands at 1,249.25 a critical mid-term dynamic resistance as the indicator has rejected advances since early November 2016. Shorter term, and according to the 4 hours chart, the commodity has room to advance further, as the20 SMA has accelerated north below the current level, having already crossed above the 100 SMA and about to cross the 200 SMA, whilst the RSI indicator consolidates around 68 and the Momentum indicator turned flat above its 100 level, after correcting extreme overbought conditions.

Support levels: 1,230.10 1,223.15 1,212,90

Resistance levels: 1,242.50 1,249.25 1,255.60

WTI CRUDE

West Texas Intermediate crude oil futures settled at $48.92 a barrel after trading as low as 48.45, still pressure by concerns about rising US production. There were no major news affecting the oil market, although there were some comments from sources within the OPEC, about the possibility that the organization could extend its output cut to the second half of the year. The news also indicates that OPEC oil producers will be more willing to do so if non-OPEC countries remains part of the initiative. From a technical point of view, the daily chart shows that the US benchmark has made little progress over the past 24 hours, still contained by selling interest around the 200 DMA and with technical indicators having modestly corrected oversold conditions before turning back south. In the 4 hours chart, oil is trading below a modestly bullish 20 SMA, whilst technical indicators hold within negative territory, with no certain directional strength.

Support levels: 48.00 47.30 46.65

Resistance levels: 49.20 49.75 50.50

DJIA

US indexes closed the day little changed, with the Dow Jones Industrial Average down by 9 points, to 20,905.51, the S&P 4 points lower, to 2,373.47, and the Nasdaq Composite flat again at 5,901.53. Within the Dow, Caterpillar led advancers, adding 2.63%, followed by Nike that closed up 1.57% and Nike that added 1.0%. Hole Depot was the worst performer, closing 1.19% lower, followed by Visa that shed 1.10%. Financials and pharmaceutical equities also closed in the red, following the lead of their European counterparts. In the daily chart, the index remains stuck around a horizontal 20 SMA, while the Momentum indicator have turned flat right below its 100 level and the RSI indicator consolidates around 63. In the 4 hours chart, the index retains a neutral stance, hovering around horizontals 20 and 100 SMAs, and with technical indicators heading nowhere around their mid-lines.

Support levels: 20,890 20,852 20,817

Resistance levels: 20,925 20,978 21,015

FTSE 100

London shares´ market posted a modest gain this Monday, with the FTSE 100 recovering 4 points to settle at 7,429.81, in a lackluster start to the week. Royal Bank of Scotland was the worst performer, down 1,64%, followed by Hikma Pharmaceuticals that lost 1.57% after investment bank Merrill Lynch downgraded the stock to "neutral." Mining-related shares closed mixed, with Anglo American down 1.04%, but Randgold Resources adding 1.20% and Fresnillo 1.13%. From a technical point of view, the daily chart, shows that the benchmark maintains a neutral-to-bullish stance, as it holds near its recent record highs and above all of its moving averages in the daily chart, but with technical indicators still horizontal within positive territory. In the 4 hours chart, the 20 SMA maintains its bullish slope and offers a dynamic support at 7,400, whilst technical indicators have turned modestly lower, but remain within positive territory, with not enough directional strength to confirm a downward corrective move.

Support levels: 7,400 7,363 7,338

Resistance levels: 7,447 7,480 7,510

DAX

European equities closed mostly lower, with the German DAX shedding 42 points or 0.35% to settle at 12,052.90, weighed by a decline in automakers and banks. Deutsche Bank topped losers' list, down 3.54%, followed by Commerzbank that shed 2.39%. Volkswagen was also among the worst performer, losing 0.88%. E.ON, on the other hand, was the best performer for a second consecutive day, adding 1.03%, followed by SAP that gained 0.80%. The daily chart for the DAX shows that the index held above a bullish 20 SMA, while technical indicators lost upward strength, having turned flat within positive territory, indicating a limited downward potential, despite the absence of upward strength. In the shorter term, and according to the 4 hours chart, the index is struggling around a bullish 20 SMA whilst technical indicators have continuing easing within positive territory, but losing their bearish strength near their mid-lines, in line with the longer term perspective.

Support levels: 12,039 11,977 11,932

Resistance levels: 12,105 12,140 12,178

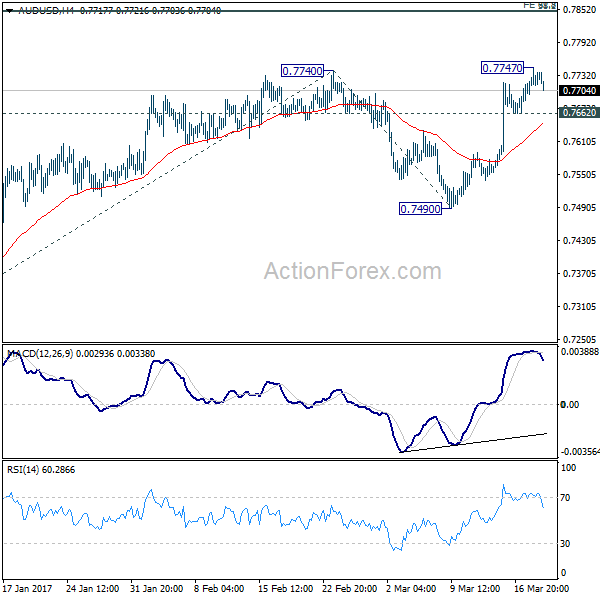

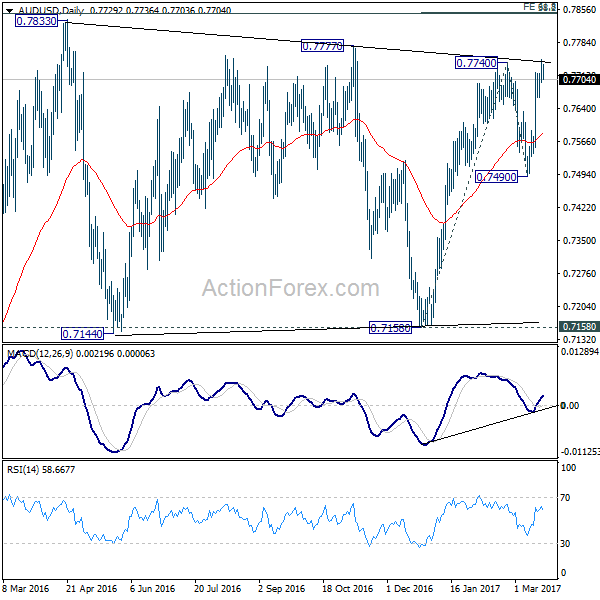

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7695; (P) 0.7721; (R1) 0.7755; More...

AUD/USD edged higher to 0.7747 but lost momentum since then, as seen in 4 hour MACD dragged below signal line. Further rise could be seen with 0.7662 minor support intact, through 0.7777 resistance. But at this point, we'd expect upside to be limited by 0.7849/50 cluster resistance to limit upside and bring reversal. That level represents 61.8% projection of 0.7158 to 0.7740 from 0.7490 at 0.7850 and key long term retracement level at 0.7849. On the downside, below 0.7662 minor support will turn bias to the downside for 0.7490 support first.

In the bigger picture, we're still treating price actions from 0.6826 low as a correction. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seek to 55 month EMA (now at 0.8169) and above.

Aussie Lost Momentum Despite Strong House Price, after RBA Minutes

Australian dollar's hit a four month high overnight but lost momentum after strong housing data and RBA minutes. RBA highlighted in the meeting minutes the risks from the heat-up housing markets. It noted that "data continued to suggest that there had been a build-up of risks associated with the housing market." And, "growth in household debt had been faster than that in household income."

Regarding the job markets, RBA said that "it was clear that spare capacity remained and there continued to be significant differences in labor market outcomes across the country." Also, "domestic wage pressures remained subdued and household income growth had been low, which, if it were to persist, would have implications for consumption growth and the risks posed by the level of household debt."

Also from Australia, house price index jumped 4.1% qoq in Q4, highest quarterly rise since 2015.

BoE Haldane: Low interest could have hurt productivity

In UK, BoE chief economist Andy Haldane said that low interest rates could have hurt productivity. He pointed out that the "total factor productivity" had its longest stagnation in history since the financial crisis. And low interest rates had kept unproductive "zombie" businesses alive. Meanwhile, he emphasized the importance of free trade and foreign direct investment to UK. He noted that "for a foreign-owned (company), it's twice as productive as domestically run firms. Higher exports, higher productivity - that screams from the data." And he hoped that "both of those features were preserved, ideally enhanced, in a post-Brexit world."

Talking about Brexit, UK Prime Minister Theresa May's spokesman James Slack said that Article 50 on Brexit will be triggered next Wednesday on March 29. And, UK representative to EU Tim Barrow has already informed European Council President Donald Tusk of the plan. Slack also noted that "after we trigger, the 27 will agree their guidelines for negotiations and the Commission's negotiating mandate." And, "President Tusk has said he expects an initial response within 48 hours. We want negotiations to start promptly."

Chicago Fed Evans: It could be three, two, or four hikes this year

In US, Chicago Fed President Charles Evans said Fed is on track for two more rate hike this year. Meanwhile, he maintained that a total of three hikes this year is "entirely possible". And, "as I gain more confidence in the outlook I could support three total this year. If inflation began to pick up, that would certainly solidify (that expectation). It could be three, it could be two, it could be four if things really pick up."

Minneapolis Federal Reserve President Neel Kashkari, the lone dissenter in last week's FOMC meeting when FOMC hiked interest rate, spoke again yesterday. He reiterated that "when the data do call for removing some monetary accommodation, my preference would be that we ... articulate a plan of exactly how and when we're going to roll off the balance sheet." And, "as we move forward, we allow the balance sheet to start running off. Then we can return to fed funds rate hikes when the data call for it." And in short, his preference is "the balance sheet should be the next move."

On the data front...

Elsewhere, UK inflation data will be the main focus in European session. Headline CPI is expected jump to 2.1% yoy in February and core CPI is expected to rise to 1.7% yoy. RPI, PPI, house price index, public sector net borrowing will also be released from UK. Swiss will release trade balance. Later in US session, Canada will release retail sales while US will release Q4 current account.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7695; (P) 0.7721; (R1) 0.7755; More...

AUD/USD edged higher to 0.7747 but lost momentum since then, as seen in 4 hour MACD dragged below signal line. Further rise could be seen with 0.7662 minor support intact, through 0.7777 resistance. But at this point, we'd expect upside to be limited by 0.7849/50 cluster resistance to limit upside and bring reversal. That level represents 61.8% projection of 0.7158 to 0.7740 from 0.7490 at 0.7850 and key long term retracement level at 0.7849. On the downside, below 0.7662 minor support will turn bias to the downside for 0.7490 support first.

In the bigger picture, we're still treating price actions from 0.6826 low as a correction. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seek to 55 month EMA (now at 0.8169) and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:30 | AUD | House Price Index Q/Q Q4 | 4.10% | 2.50% | 1.50% | |

| 0:30 | AUD | RBA Minutes | ||||

| 6:45 | CHF | SECO March 2017 Economic Forecasts | ||||

| 7:00 | CHF | Trade Balance (CHF) Feb | 3.85B | 4.73B | ||

| 9:30 | GBP | CPI M/M Feb | 0.50% | -0.50% | ||

| 9:30 | GBP | CPI Y/Y Feb | 2.10% | 1.80% | ||

| 9:30 | GBP | Core CPI Y/Y Feb | 1.70% | 1.60% | ||

| 9:30 | GBP | RPI M/M Feb | 0.80% | -0.60% | ||

| 9:30 | GBP | RPI Y/Y Feb | 2.90% | 2.60% | ||

| 9:30 | GBP | PPI Input M/M Feb | 0.10% | 1.70% | ||

| 9:30 | GBP | PPI Input Y/Y Feb | 20.10% | 20.50% | ||

| 9:30 | GBP | PPI Output M/M Feb | 0.30% | 0.60% | ||

| 9:30 | GBP | PPI Output Y/Y Feb | 3.70% | 3.50% | ||

| 9:30 | GBP | PPI Output Core M/M Feb | 0.20% | 0.50% | ||

| 9:30 | GBP | PPI Output Core Y/Y Feb | 2.50% | 2.40% | ||

| 9:30 | GBP | House Price Index Y/Y Jan | 6.30% | 7.20% | ||

| 9:30 | GBP | Public Sector Net Borrowing (GBP) Feb | 2.9B | -9.8B | ||

| 11:00 | GBP | CBI Trends Total Orders Mar | 5 | 8 | ||

| 12:30 | CAD | Retail Sales M/M Jan | 1.30% | -0.50% | ||

| 12:30 | CAD | Retail Sales Less Autos M/M Jan | 1.30% | -0.30% | ||

| 12:30 | USD | Current Account (USD) Q4 | -129B | 113B |