Sample Category Title

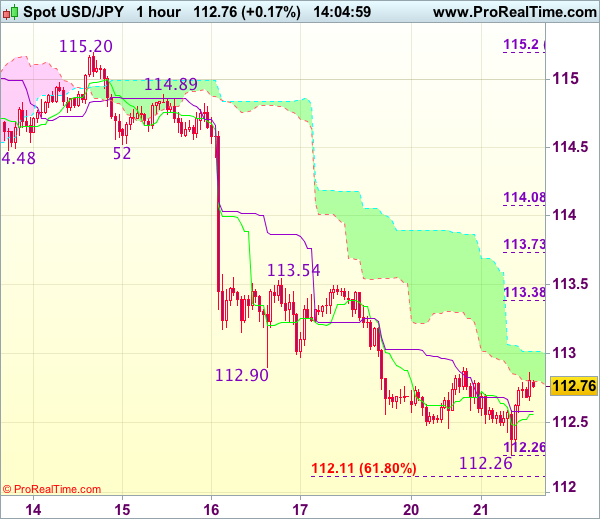

Trade Idea : USD/JPY – Buy at 112.55

USD/JPY - 112.75

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 112.56

Kijun-Sen level : 112.58

Ichimoku cloud top : 113.01

Ichimoku cloud bottom : 112.80

Original strategy :

Sell at 113.50, Target: 112.40, Stop: 113.85

Position : -

Target : -

Stop : -

New strategy :

Buy at 112.55, Target: 113.55, Stop: 112.20

Position : -

Target : -

Stop : -

Although the greenback fell briefly to 112.26, the subsequent rebound suggests consolidation above this level would be seen and gain to 113.00-05 is likely, above there would suggests low is possibly formed, bring a stronger rebound to 113.35-40 (38.2% Fibonacci retracement of 115.20-112.26), however, break of resistance at 113.54 is needed to provide confirmation, bring further subsequent gain to 113.70-75 (50% Fibonacci retracement).

In view of this, we are looking to buy dollar on dips but one must exit on such rebound. Below said support at 112.26 would risk one more fall to 112.10-15 (61.8% projection of 115.20-112.90 measuring from 113.54) but loss of downward momentum should prevent sharp fall below previous support at 111.69, risk remains for a rebound to take place later.

European Open Briefing

Global Markets:

- Asian stock markets: Nikkei down 0.35 %, Shanghai Composite gained 0.20 %, Hang Seng rose 0.40 %, ASX 200 lost 0.10 %

- Commodities: Gold at $1228 (-0.45 %), Silver at $17.36 (-0.45 %), WTI Oil at $49.10 (+0.40 %), Brent Oil at $51.90 (+0.50 %)

- Rates: US 10-year yield at 2.48, UK 10-year yield at 1.24, German 10-year yield at 0.44

News & Data:

- Australia ANZ Roy Morgan Weekly Consumer Confidence Index Mar 20: 112.0 (Prior 113.1)

- Australia House Price Index QoQ Q4: 4.1% (Prior 1.50%)

- Australia House Price Index YoY Q4:7.7% (Prior 3.50%)

- PBoC Fixes USDCNY Reference Rate At 6.9071 (Prev 6.8998)

RBA Meeting Minutes:

- Judged steady policy consistent with growth and inflation targets

- A rising AUD would complicate economic transition

- Recent data suggested a 'build-up of risks' in the housing market

- Home prices strong and rising briskly in Sydney and Melbourne

- Home investment borrowing had picked up, debt rising faster than household incomes

- Slow growth in incomes could restrain consumption given high debt levels

- Soft GDP wage measure suggests very little labour cost pressure in economy

- Wages growth, underlying inflation expected to rise only gradually

- Still difficult to assess momentum in labour market

Markets Update:

The Australian Dollar declined overnight as the RBA meeting minutes were considered rather dovish. Recent economic data out of Australia was weak too, especially the latest jobs market numbers. AUD/USD fell from 0.7735 to a low of 0.77. The pair found solid support there and bounced back to 0.7710, where it consolidated into the Sydney session close. Key support is now seen at 0.7650/60, while resistance lies at 0.7740, followed by 0.7780.

USD/JPY came under pressure in the early Asian session, falling to 112.25. However, the pair caught a bid later and recovered to 112.80. Resistance is noted at 113.00, and decent selling interest lies around 113.50.

The Pound was sold yesterday, following the news that Brexit will officially start next week. However, that was already expected and the downside momentum quickly waned. GBP/UD consolidated in a 1.2355-80 range in Asia. The focus now lies on the upcoming inflation data, which be released today at 09:30 GMT. The market is expecting an increase in the CPI numbers, from -0.5 % in January to +0.5 % in February.

Upcoming Events:

- 09:30 GMT – UK CPI

- 10:00 GMT – BoE Governor Carney speaks

- 10:00 GMT – FOMC Member Dudley speaks

- 12:30 GMT – US Current Account

- 12:30 GMT – Canadian Retail Sales

- 16:00 GMT – FOMC Member George speaks

- 22:00 GMT – FOMC Member Mester speaks

- 23:50 GMT – Japanese Trade Balance

- 23:50 GMT – BoJ Meeting Minutes

AUD/USD: RBA Concerned About House Prices And Highly Indebted Households

For the 24 hours to 23:00 GMT, the AUD rose 0.08% against the USD and closed at 0.7726.

On the data front, Australia's CB leading indicator advanced by 0.4% in January, compared to a drop of 0.1% in the preceding month.

LME Copper prices rose 0.03% or $2.0/MT to $5891.0/MT. Aluminium prices rose 0.4% or $7.0/MT to $1908.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7709, with the AUD trading 0.22% lower against the USD from yesterday's close.

According to minutes of the Reserve Bank of Australia's (RBA) March meeting, board members expect to see Australian consumer prices continue to rise, albeit at a gradual pace. Further, the central bank warned of risks from rapidly climbing nation's house prices and an acceleration of domestic household debt.

In other economic news, Australia's house price index advanced 4.1% on a quarterly basis in 4Q 2016, more than market expectations for a rise of 2.5%. The index had climbed 1.5% in the previous quarter.

The pair is expected to find support at 0.7688, and a fall through could take it to the next support level of 0.7668. The pair is expected to find its first resistance at 0.7738, and a rise through could take it to the next resistance level of 0.7768.

Going ahead, Australia's Westpac leading index for February, set to release overnight, will be on investor's radar.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

EUR/USD: Germany’s Producer Price Inflation Accelerates At Its Fastest Pace Since November 2011 In February

For the 24 hours to 23:00 GMT, the EUR declined 0.25% against the USD and closed at 1.0733.

On the data front, Germany's producer price index rose 3.1% on an annual basis in February, notching its highest level in over five years, amid a surge in energy prices. However, the index fell short of market expectations of a rise of 3.2%, while following a gain of 2.4% in the previous month.

Separately, according to the Bundesbank monthly report, the German economy has continued to expand and will do so in the foreseeable future, on the back of robust industrial output.

In the US, the Chicago Federal Reserve (Fed) President, Charles Evans, reiterated the Fed's view that two more interest rate hikes this year are likely and added that the central bank will possibly wait at least until June to decide on the next interest rate hike. Nevertheless, he also added that four rate rises this year isn't totally out of the realm of possibility, if the economy “really” picks up and inflation tops the Fed's 2.0% target.

On the data front, the US Chicago Fed national activity index advanced to a level of 0.34 in February, compared to a revised reading of -0.02 in the previous month, whereas investors had envisaged the index to climb to a level of 0.03.

In the Asian session, at GMT0400, the pair is trading at 1.0755, with the EUR trading 0.2% higher against the USD from yesterday's close.

The pair is expected to find support at 1.0722, and a fall through could take it to the next support level of 1.0690. The pair is expected to find its first resistance at 1.0782, and a rise through could take it to the next resistance level of 1.0810.

Amid no economic releases across the Euro-zone today, market participants will closely monitor comments from a host of Fed officials, scheduled later in the day.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

GBP/USD: Britain Will Trigger Formal Brexit Process On 29 March

For the 24 hours to 23:00 GMT, the GBP declined 0.22% against the USD and closed at 1.2358, after the British Government announced that Prime Minister, Theresa May, will launch UK's separation proceedings with the European Union on 29 March 2017.

In the Asian session, at GMT0400, the pair is trading at 1.2365, with the GBP trading 0.06% higher against the USD from yesterday's close.

The pair is expected to find support at 1.2320, and a fall through could take it to the next support level of 1.2276. The pair is expected to find its first resistance at 1.2422, and a rise through could take it to the next resistance level of 1.2480.

Going ahead, investors will look forward to UK's crucial inflation figures for February, slated to release in a few hours and is expected to breach the Bank of England's 2.0% target. Moreover, UK's public sector net borrowing data for February will be closely monitored by investors.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

USD/JPY: Japanese Yen Trading Lower In The Morning Session

For the 24 hours to 23:00 GMT, the USD slightly declined against the JPY and closed at 112.52.

In the Asian session, at GMT0400, the pair is trading at 112.72, with the USD trading 0.18% higher against the JPY from yesterday’s close.

The pair is expected to find support at 112.36, and a fall through could take it to the next support level of 111.99. The pair is expected to find its first resistance at 112.99, and a rise through could take it to the next resistance level of 113.25.

Looking ahead, market participants will eye minutes of the Bank of Japan’s (BoJ) recent monetary policy meeting along with Japan’s adjusted merchandise trade balance for February, due to release overnight.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

USD/CHF: Swiss Franc Trading A Tad Higher, Ahead Of Switzerland’s Trade Balance Data

For the 24 hours to 23:00 GMT, the USD rose 0.3% against the CHF and closed at 0.9988.

In economic news, Switzerland's total sight deposits advanced to a level of CHF557.2 billion in the week ended 17 March, from CHF555.4 billion in the previous week.

In the Asian session, at GMT0400, the pair is trading at 0.9987, with the USD trading marginally lower against the CHF from yesterday's close.

The pair is expected to find support at 0.9959, and a fall through could take it to the next support level of 0.9932. The pair is expected to find its first resistance at 1.0008, and a rise through could take it to the next resistance level of 1.0030.

Going ahead, traders would keep a close watch on Switzerland's trade balance for February and the SECO economic forecast report, slated to release in a while.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

USD/CAD: Loonie Trading On A Weaker Footing, Ahead Of Canada’s Retail Sales Data

For the 24 hours to 23:00 GMT, the USD rose 0.13% against the CAD and closed at 1.3339.

In the Asian session, at GMT0400, the pair is trading at 1.3351, with the USD trading 0.09% higher against the CAD from yesterday's close.

The pair is expected to find support at 1.3311, and a fall through could take it to the next support level of 1.3272. The pair is expected to find its first resistance at 1.3381, and a rise through could take it to the next resistance level of 1.3412.

Ahead in the day, investors will look forward to Canada's retail sales data for January.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

RBA Minutes Highlighted Concerns over Household Debts, Rising Housing Bubble

At the RBA minutes for the March meeting, policymakers raised concerns over the increasing levels of household debts which would be exacerbated by rising unemployment and falling consumption. The members also noted there had been a "buildup of risks associated with the housing market". While the central bank has been paying close attention to the housing market, including prices, supply, rents, debts and supervisory markets, the reference of "a buildup of risks" was non-existent in the March meeting statement and the February minutes. On the economic growth outlook, RBA acknowledged that the domestic economy continued to move away from mining investment while terms of trade increased in recent months. Moreover, the members expected that inflation would continue to rise, albeit gradually. Policymakers reiterated that economic growth would be supported by low interest rates.

The RBA has turned more vigilant over the housing market bubble. The minutes suggested that "there had been a build-up of risks associated with the housing market". It added that "in the eastern capital cities, a considerable additional supply of apartments was scheduled to come on stream over the next few years". Moreover, "growth in rents had been the slowest for two decades. Borrowing for housing by investors had picked up over recent months and growth in household debt had been faster than that in household income. Supervisory measures had contributed to some strengthening of lending standards". Indeed, Treasurer Scott Morrison warned yesterday that "there remain pressures that have built up again over the last few months". He and the chief corporate regulator have indicated that measures to further crack down property investor loans would be implemented. According to Morrison, "Australia has a very high proportion of interest only loans and these are issues that have been the topic of discussion".

The RBA highlighted that "spare capacity remained and there continued to be significant differences in labour market outcomes across the country". Moroever, "domestic wage pressures remained subdued and household income growth had been low, which, if it were to persist, would have implications for consumption growth and the risks posed by the level of household debt". In the longer term, the members expected spare capacity to "decline slowly" while wage growth and underlying inflation would "rise, but only gradually".

Regarding the stance to leave the cash rate unchanged at 1.5%, the minutes noted "the board judged that holding the stance of policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time".

Obvious is Scary

The pound fell Monday after reports that Theresa May has set March 29 as the day to trigger Article 50. The New Zealand dollar was the top performer while GBP lagged. Japan is back from holiday but the Asia-Pacific calendar remains light. We also take a look at the first French Presidential debate.

As we wrote about yesterday, the net cable short position is at the most extreme levels on record. Presumably, those are bets on a decline after Article 50. What's also notable is that in the past two weeks, the net short has nearly doubled. In that time cable has edged higher and that leaves many traders underwater.

The trade is so obviously setting up for a short squeeze that it scares us, making us think we've missed something. Goldman Sachs is out with some research saying specs tend to be right about the direction of GBP but we struggle to see it this time. There should be nothing surprising about Article 50; not only in financial markets but also on Main St. Or maybe we're overthinking it.

In any case, what we're sure of is that if a short squeeze starts after Article 50, it will get very violent, very quickly.

Turning to politics, an instant poll from Elabe showed that Macron was the most-convincing, followed by Melenchon with Le Pen tied for third. Those types of surveys tend to be flakey and with a large portion of the French electorate remains undecided though and the polls in the coming days will be market moving.

The exchanges on immigration and culture were the most heated but one of the things that was striking was how populist rhetoric is growing more refined in Europe and globally. An example was Le Pen shifting to promoting sovereignty in a move that echoed 'America First'. She said she wasn't running to be Merkel's Vice-Chancellor. That's the kind of talk that will increasingly strike a chord in a Eurozone where growth is unbalanced.