Sample Category Title

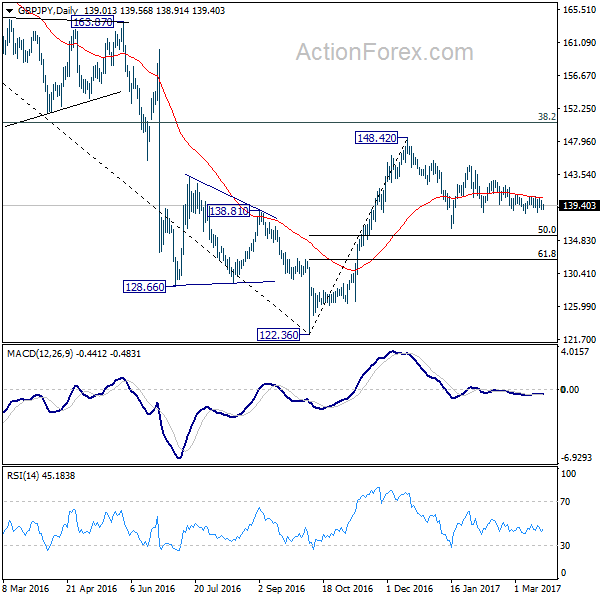

GBP/JPY Daily Outlook

Daily Pivots: (S1) 138.60; (P) 139.37; (R1) 139.84; More...

GBP/JPY is still staying in tight range above 138.53 support and intraday bias stays neutral. Price actions from 148.42 are forming a consolidation pattern. And there is no clear sign of completion yet. On the downside, break of 138.53 support would trigger bring deeper fall to 136.44 support and possibly below. We'd expect strong support from 50% retracement of 122.36 to 148.42 at 135.39 to contain downside and bring rebound. On the upside, break of 142.79 resistance will turn bias to the upside and send GBP/JPY through 144.77 resistance.

In the bigger picture, price actions from 122.36 medium term bottom are still seen as a corrective pattern. Main focus is on 38.2% retracement of 195.86 to 122.36 at 150.42. Rejection from there will turn the cross into medium term sideway pattern. Or, sustained break of 50% retracement of 122.36 to 148.42 at 135.39 will turn outlook bearish for a test on 122.36 low. Though, sustained break of 150.42 will extend the rebound towards 61.8% retracement of 195.86 to 122.36 at 167.78.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0705; (P) 1.0725; (R1) 1.0745; More...

EUR/CHF recovers today but stays in range below 1.0823. Intraday bias remains neutral for the moment. On the upside, break of 1.0823 resistance will re-affirm the case of trend reversal. And intraday bias will be turned back tot he upside for 1.0897 resistance for confirmation. However, break of 1.0683 minor support will turn bias to the downside for 1.0620 key support level again.

In the bigger picture, the decline from 1.1198 is seen as a corrective move. Decisive break of 1.0897 resistance should confirm that it's completed. And in that case, larger up trend is resuming for another high above 1.1198. Meanwhile, sustained trading below 38.2% retracement of 0.9771 to 1.1198 at 1.0653 will target 50% retracement at 1.0485.

Asian Market Update: RBA Minutes Balance Rising Property Prices And Slower Wage Growth

RBA minutes balance rising property prices and slower wage growth

Asia Mid-Session Market Update: RBA minutes balance rising property prices and slower wage growth; Strong performance by Macron in France debates lifts EUR

US Session Highlights

(US) Fed's Kashkari (dove, dissenting vote): job market showing more signs of slack and we are still short on inflation; The economy is growing more slowly than we would like - CNBC interview

(US) Fed's Evans (dove, voter): Three rate hikes in 2017 is possible; could be more or less - Fox Business interview

(US) Fed's Harker (hawk, FOMC voter): Would not rule out more than three rate hikes this year; all meetings are live for rate decisions; Would like to get well north of 1% rates before halting bond reinvestments, maybe close to 1.5% - CNBC interview

(US) House Intel Chair Nunes: there was not a wiretap of Trump Tower; it is possible there was other surveillance against Trump and his aides - hearings on Russia interference in elections

(US) FBI Director Comey: confirms that FBI is investigating Russian govt efforts to interfere in election, including potential links between Trump campaign and Russia - press

US markets on close: Dow flat, S&P500 -0.2%, Nasdaq flat

Best Sector in S&P500: Materials

Worst Sector in S&P500: Financials

Biggest gainers: CF +3.8%, NVDA +3.2%, CAT +2.7%, BHI +2.5%, IFF +2.5%

Biggest losers: KSS -4.8%, FSLR -4.7%, M -3.8%, JWN -3.1%, GPS -2.7%

At the close: VIX 11.3 (+0.1 pts); Treasuries: 2-yr 1.30% (flat), 10-yr 2.47% (-3bps), 30-yr 3.09% (-2bps)

US movers afterhours

FSM: Announces possible delay in filing its annual financial results; -2.5% afterhours

GEL: Offering 4M Common Units (3.4% of outstanding); -5.7% afterhours

Politics

(FR) France Elabe poll: Macron was most convincing in presidential debate; Melenchon 2nd; Le Pen and Fillon tied for 3rd

(US) Pres Trump: Preparing executive order to put coal miners back to work; Working to remove regulations in auto industry

Asia Key economic data:

(AU) AUSTRALIA Q4 HOUSE PRICE INDEX Q/Q: 4.1% (biggest increase in 5 years) V 2.5%E; Y/Y: 7.7% V 6.3%E

(AU) Australia ANZ Roy Morgan Weekly Consumer Confidence Index: 112.0 v 113.1 prior

(NZ) NEW ZEALAND FEB CREDIT CARD SPENDING M/M: -1.4% V 0.4% PRIOR; Y/Y: 5.3% V 7.1% PRIOR

(NZ) New Zealand Feb Net Migration: 6.0K v 6.4K prior (6-month low)

Asia Session Notable Observations, Speakers and Press

Asian equity markets traded mixed and mostly in narrow ranges, tracking another flattish day on Wall St. Bullish sentiment has been tempered by uncertainty regarding Pres Trump's pro-business tax agenda as the cabinet continues to wrestle with Congressional inquiry into Russia election ties as well as negotiation on Obamacare repeal legislation that needs to get passed before tax reform can begin. Modest safehaven bid of US Treasuries continued on Monday as yield curve flattened and financials struggled.

In Asian hours, futures are pointing to more optimism attributed to initial response from Elabe poll in France that showed Macron as the most credible candidate in today's debate, potentially defusing concerns of a populist revolt propelling Le Pen to a surprise victory in May. EUR/USD bounced on the poll release, rising some 50pips to 1.0770, while USD/JPY reversed some of the early pressure to rise over 40pips above 112.70.

Outside of the political risks, the absence of meaningful economic data has otherwise contributed to a fairly lackluster session. Release of RBA March meeting minutes produced a brief ripple in AUD with an initial 10pips rise to session highs of 0.7735 followed by steady retreat to 0.77 handle. RBA expanded on its statement with growing concern over home prices, improved global conditions, and forecast commodity prices to remain firm for longer than expected. On the other hand however, RBA was more downbeat about sustained momentum in wage inflation following latest disappointing labor data, while also maintaining focus on uncertainty in policies of China and US. Traders will look ahead to tomorrow's speech from RBA's Debelle for any more clarity, though analyst consensus of a neutral RBA over the near term is likely to be maintained.

China

(CN) China Ministry of Commerce (MOFCOM) and National Development Reform Commission (NDRC) may announce rules this year restricting outbound investment

(CN) China Vice Foreign Minister Zheng Zeguang: Premier Li's upcoming visit to Australia and New Zealand will send a positive message to the world that the nations are bundled with free trade

Japan

(JP) Japan Chief Cabinet Sec Suga: Japan to actively engaged in macro and FX talks at G-20

(JP) Japan said to mull shortening period between auction and issuance of some JGB's - financial press

Australia/New Zealand

(AU) RBC: Today's RBA minutes erred more on the hawkish side - SMH

(NZ) NZ Institute of Economic Research (NZIER) shadow board: RBNZ should keep interest rates at 1.75% with a tightening bias

Korea

(KR) South Korea Acting President Hwang Need to closely monitor financial markets - press

Asian Equity Indices/Futures (00:30ET)

Nikkei -0.3%, Hang Seng +0.2%, Shanghai Composite +0.2%, ASX200 -0.1%, Kospi +1.0%

Equity Futures: S&P500 +0.2%; Nasdaq +0.2%; Dax +0.2%; FTSE100 +0.2%

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.0720-1.0770; JPY 112.30-112.80; AUD 0.7700-0.7740; NZD 0.7040-0.7065

Apr Gold -0.5% at $1,228/oz; May Crude Oil +0.4% at $49.11/brl; May Copper -1.0% at $2.63/lb

SPDR Gold Trust ETF daily holdings fall 3.8 tonnes to 830.3 tonnes; 3rd straight decline

iShares Silver Trust ETF daily holdings rise to 10,342 tonnes from 10,303 tonnes prior

(CN) PBOC SETS YUAN MID POINT AT 6.9071 V 6.8998 PRIOR; weakest Yuan setting since Mar 15th; 3rd straight weaker setting

(CN) PBOC to inject combined CNY80B v CNY100B prior in 7,14, and 28-day reverse repos

(KR) South Korea MoF sells 10-yr pre-issuance Govt bond at 2.2%

Asia equities/Notables/movers by sector

Consumer discretionary: 1107.HK Modern Land China -10.0% (FY16 result); HVN.AU Harvey Norman +3.3% (denies speculation about ASIC review of reporting); TGA.AU Thorn Group -7.5% (guidance)

Consumer staples: 1432.HK China Shengmu Organic Milk -3.8% (FY16 result)

Financials: 1528.HK Red Star Macalline Group -6.6% (FY16 result); 1238.HK Powerlong Real Estate Holdings +5.5% (FY16 result); SPO.AU Spotless Group +48.6% (bid by Downer)

Industrials: 3836.HK China Harmony Auto Holding -7.5% (guidance); AZJ.AU Aurizon -0.9% (UBS cuts rating); 6448.JP Brother Industries +4.2% (Goldman Sachs raises rating)

Technology: 698.HK Tongda Group Holdings -3.1% (FY16 result); 1357.HK Meitu -10.3% (regulator requests trading records); 6502.JP Toshiba Corporation +3.2% (Westinghouse Electric bankruptcy consideration)

Materials: 2068.HK China Aluminum International Engineering Corp +14.2% (FY16 result); 5423.JP Tokyo Steel Mfg -4.9% (maintains steel prices); NHC.AU New Hope Corporation +4.9% (H1 result)

Energy: 2386.HK Sinopec Engineering Group Co +4.7% (JPMorgan raises rating)

Healthcare: VRT.AU Virtus Health -3.7% (Morning star cuts rating); BKL.AU Blackmores +13.4% (China has indefinitely delayed new cross-border e-commerce laws)

Telecom: TPM.AU TPG Telecom +5.6% (affirms guidance)

The Donald Trump And Angela Merkel Meeting

Market movers today

In the US, we are due to get preliminary University of Michigan consumer confidence data (one of the soft economic indicators) for March today.

The Donald Trump and Angela Merkel meeting, initially scheduled for this Monday but postponed due to the blizzard in the north eastern part of the US, is set to take place at the White House today. This will be the first meeting between the German Chancellor and the new American President. Likely topics on the agenda are the future of the transatlantic alliance but also funding for NATO and relations with Russia.

In the euro area, S&P is scheduled to update its rating and outlook on Portugal, Finland, Austria and Cypress, while Moody's will be reviewing Estonia.

In Denmark, the Association of Danish Mortgage Banks is due to release its housing market statistics for Q4 16.

Selected market news

Different camps of the Governing Council within the ECB seem to be forming, both when it comes to how the 'normalisation' of monetary policy should start and regarding when it is time to embark on a clearer adjustment to the forward guidance. Overnight Ewald Nowotny (Hawk) was quoted in a Handelsblaat interview as saying that the 'deposit rate could rise before [the] main rate', while Peter Praet said during a speech in Brussels that 'inflation dynamics haven't yet become self-sustained'. It will be interesting to see how this 'gorge' continues to develop.

Donald Trump's first budget outline was presented yesterday. As expected, it had heavy emphasis on infrastructure spending without further detail and an increased defence budget, which he plans to fund with deep cuts to diplomatic and foreign aid programmes. Also, the Environmental Protection Agency is set to see its budget cut by 31%. The full 2018 budget is due to be released later this spring and it will include 'our specific mandatory and tax proposals, as well as a full fiscal path'.

Yesterday's Norges Bank meeting did not bring any surprises, as the sight deposit rate was left unchanged at 0.50% and the Board maintained the 'neutral bias' introduced in September. The rate path was revised 'postponing' the expectation of when the first rate hike will occur and stating 'the key policy rate will most likely remain at today's level in the period ahead'.

The Bank of England meeting did not surprise much either, as it made no policy changes and reiterated its neutral stance by repeating it could move 'in either direction'. However, the meeting was not completely uneventful, as Kristin Forbes (a known hawk) voted for a March hike and the statement disclosed that 'some members noted that it would take relatively little further upside news…for them to consider that a more immediate reduction in policy support might be warranted'.

The overnight session was very quiet, with the Asian equity indices seeing marginal gains and losses, no big FX moves and slightly higher yields of Japanese government bonds.

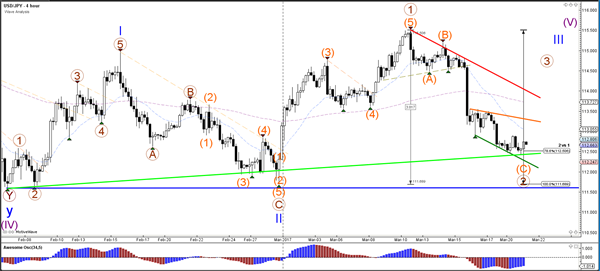

USDJPY Elliott Wave View: Ending Impulse

Short term Elliott Wave view in USDJPY suggests that rally to 115.48 on 3/10 ended Intermediate wave (X). Decline from there is unfolding as a zigzag Elliott wave structure in which the first leg wave A is subdivided in 5 impulsive waves. Down from 3/10 high, Minute wave ((i)) ended at 114.46, Minute wave ((ii)) ended at 115.195, Minute wave ((iii)) ended at 112.88 and Minute wave ((iv)) ended at 113.56. Cycle from 3/10 high is mature and Primary wave A has enough extension to be called complete, but more downside towards 111.56 – 111.95 area can’t be ruled out to complete Primary wave A. Afterwards, pair should bounce in Primary wave B in 3, 7, or 11 swing to correct cycle from 3/10 high before the decline resumes. A break above proposed Minutte wave (iv) at 112.9 may be an early indication that Primary wave A has ended.

USDJPY 1 Hour Chart

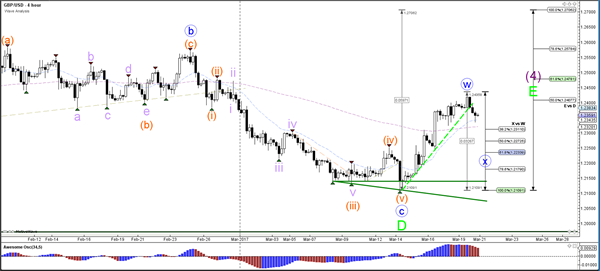

GBP/USD Bearish ABC Zigzag Within Wave-E Triangle

Currency pair GBP/USD

The GBP/USD turned at the 50% Fibonacci level of wave E (green) but a larger bullish correction via a WXY (blue) seems likely at this point. The Fibonacci levels of wave X (blue) could therefore be bouncing spots.

The GBP/USD seems to have completed a 5th wave (purple) and is now building a bearish correction via an ABC (orange) zigzag.

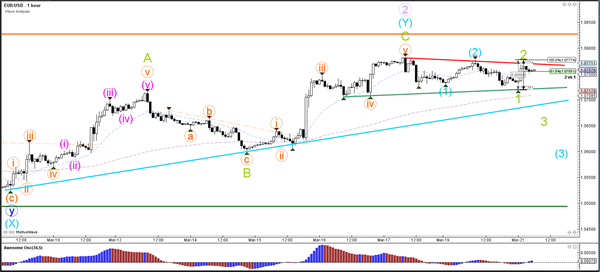

Currency pair EUR/USD

The EUR/USD is building a contracting triangle (green/orange lines) at the 78.6% Fibonacci resistance level of wave 2 (purple). A potential break above the 100% level invalidates the current wave 1-2 (purple) structure but a breakout below support (green/blue) could see a new downtrend emerge.

The EUR/USD could be building a second pullback with waves 1-2 (blue/green). A break above the 100% level invalidates the bearish reversal and could see price retest 1.08 and the resistance top (orange).

Currency pair USD/JPY

The USD/JPY is building a pullback and could bounce at the 78.6% Fibonacci retracement level of wave 2 (brown). A break below the 100% Fibonacci level invalidates wave 2 (blue/brown).

The USD/JPY might be starting its bullish turn via a wave 1-2 (orange) if price stays above the 100% level and manages to break above resistance (orange/red).

Daily Technical Outlook And Review

A note on lower timeframe confirming price action...

Waiting for lower timeframe confirmation is our main tool to confirm strength within higher timeframe zones, and has really been the key to our trading success. It takes a little time to understand the subtle nuances, however, as each trade is never the same, but once you master the rhythm so to speak, you will be saved from countless unnecessary losing trades. The following is a list of what we look for:

- A break/retest of supply or demand dependent on which way you're trading.

- A trendline break/retest.

- Buying/selling tails ... essentially we look for a cluster of very obvious spikes off of lower timeframe support and resistance levels within the higher timeframe zone.

- Candlestick patterns. We tend to only stick with pin bars and engulfing bars as these have proven to be the most effective.

EUR/USD

Shortly after the open, EUR bulls rose up and took charge, lifting the major to a high of 1.0777 going into the London open. This is where things began to turn sour for the bulls. The pair fell from here, broke Friday's low at 1.0727 and clipped the H4 trendline support extended from the high 1.0679. Although a buy from this angle is tempting, given that the approach to this line was in the form of a symmetrical H4 AB=CD bullish pattern, we'd still prefer to see price connect with the H4 demand sitting just below it at 1.0705-1.0723 before considering a position here.

Over on the weekly chart, the candles are seen hovering just ahead of a weekly resistance level pegged at 1.0819, shadowed closely by the 2016 yearly opening base line drawn from 1.0873. Looking down to the daily chart, nevertheless, we can see that the unit came into contact with a daily bearish AB=CD (black arrows) 127.2% Fib ext. at 1.0770 on Friday. As you can probably see though, there's not much room left for the bears to stretch their legs from here owing to the daily support area positioned just below at 1.0714-1.0683.

Our suggestions: In view of the current H4 demand area being seen around the top edge of the aforementioned daily support area, and room seen to advance north on the weekly chart, there's still a healthy chance of a bounce being seen from the H4 base.

However, as we mentioned in Monday's report, it is obviously down to the individual trader as to whether or not this zone requires additional price confirmation. For us personally, we believe it's best to wait for a reasonably sized H4 bullish rotation candle to take shape before a long trade is executed for the simple reason that we do not favor being stopped out on a fakeout down to the nearby 1.07 handle.

Data points to consider: FOMC member Dudley speaks at 10am GMT.

Levels to watch/live orders:

- Buys: 1.0705-1.0723 ([waiting for a reasonably sized H4 bull candle to form is advised before pulling the trigger] stop loss: ideally beyond the confirming candle).

- Sells: Flat (stop loss: N/A).

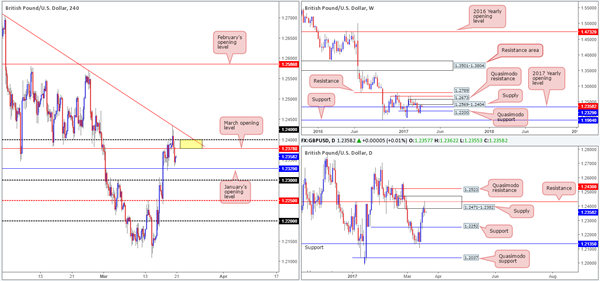

GBP/USD

In recent sessions, H4 price briefly whipsawed through the 1.24 handle and tagged in offers around a nearby H4 trendline resistance stretched from a high of 1.2706. From here, cable dove lower and ended the day on its back foot; closing just ahead of January's opening base line drawn from 1.2329. Yesterday's bearish assault likely has something to do with the fact that both the weekly and daily charts show this market to be trading from supply (weekly supply: 1.2569-1.2404/daily supply: 1.2471-1.2382).

Should the H4 candles retest the 1.24/1.2378 neighborhood today (psychological handle/March opening level – yellow zone) before testing January's open level, our desk has noted that they would be interested in shorting from here.

Our suggestions: Assuming that the above comes to fruition, and we see rejection printed from the H4 sell zone, a short trade will be initiated, targeting 1.2329 followed closely by the 1.23 handle.

Data points to consider: UK inflation data at 9.30am. FOMC member Dudley speaks at 10am GMT.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 1.24/1.2378 (stop loss: ideally placed beyond the rejection wick).

AUD/USD

Trade update: stopped out at 0.7742 on the short taken from 0.7732).

Beginning with a look at the weekly chart this morning, weekly action is currently seen testing a weekly trendline resistance taken from the high 0.7835, which is positioned nearby the underside of a weekly supply penciled in at 0.7849-0.7752. Turning our attention to the daily chart, the Aussie gravitated north from the daily support area at 0.7699-0.7656 yesterday and shook hands with a daily Quasimodo resistance level drawn in at 0.7734.

Jumping across to the H4 chart, we can see that upside is presently capped by a H4 Quasimodo resistance level pegged at 0.7732. However, with the close-at-hand H4 support area lurking at 0.7720-0.7706 (seen positioned directly above the current daily support area), the bears equally have little room to stretch their legs!

Our suggestions: While weekly, daily and H4 charts do indicate that bearish structure is in play, we cannot justify a short at this time. It would just be too risky given that there is not only a H4 support area sitting nearby, but just beneath this there's also a daily support area (see above). Therefore, opting to stand on the sidelines here may very well be the better path to take today.

Data points to consider: Australian monetary policy meeting minutes at 12.30am. FOMC member Dudley speaks at 10am GMT.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

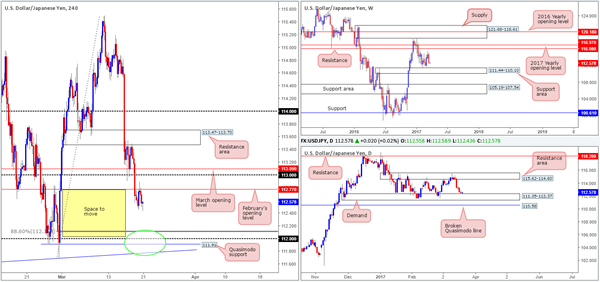

USD/JPY

February's opening level at 112.77 managed to elbow its way into the spotlight as a resistance during the early hours of yesterday's London morning segment. Our reason for not choosing to take part in selling from this line was simply due to the daily demand zone lurking within touching distance at 111.35-112.37.

As can be seen from the daily chart this morning, daily price is in fact now trading close by the top edge of the above said daily demand. Be that as it may, we do not plan on buying from here. Instead we have our eye on the 112 handle (green circle). There are a number of technical aspects that support a buy from this angle:

The H4 88.6 retracement value seen at 112.11.

The H4 Quasimodo support at 111.91.

A H4 trendline support taken from the low 111.59.

All of the above is positioned within the current daily demand, which happens to be located around the top edge of a weekly support area at 111.44-110.10.

Our suggestions: Given the above points, a long from 112 is far more appealing to us. Nevertheless, seeing as how the H4 buy zone (111.75/112.11) is rather large, a reasonably sized H4 bullish candle is required to be seen before we pull the trigger. This will not only show buyer intent but it will also help in avoiding any aggressive fakeout seen through our pre-determined zone.

Data points to consider: FOMC member Dudley speaks at 10am GMT.

Levels to watch/live orders:

- Buys: 111.75/112.11 ([waiting for a reasonably sized H4 bull candle to form is advised before pulling the trigger] stop loss: ideally beyond the confirming candle).

- Sells: Flat (stop loss: N/A).

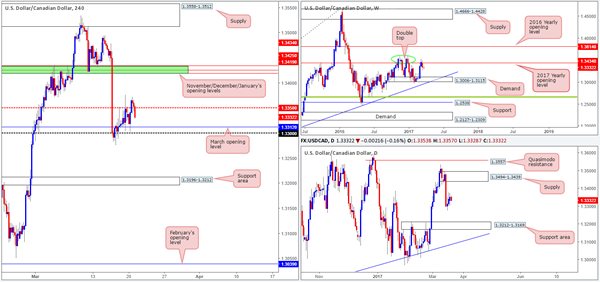

USD/CAD

Working our way from the top this morning, we can see that weekly action sold off. Price whipsawed through the 2017 yearly opening level at 1.3434 and came so very close to tapping the weekly double-top formation seen around the 1.3588 region (green circle). The next downside area to have an eyeball from here is the weekly demand pegged at 1.3006-1.3115. The story on the daily chart, however, shows that price is loitering mid-range between a daily supply seen at 1.3494-1.3439 and a daily support area at 1.3212-1.3169.

Looking over to the H4 candles, price looks to be on course to cross swords with March's opening level at 1.3312, following a rather deep fakeout above the H4 mid-way resistance level at 1.3350. Would we consider a buy from 1.3312? Although this number is bolstered by a nearby psychological handle at 1.33, we would still probably not buy from here. Our reason for why simply comes down to there being no higher-timeframe convergence.

Our suggestions: With the above points in mind, we feel that even though a bounce MAY be seen from the 1.33 region today, it's just not worth the risk, in our opinion. As a result, we will be placing this pair on the back burner today and revisiting it going into tomorrow's open.

Data points to consider: FOMC member Dudley speaks at 10am. Canadian core retail sales at 12.30pm GMT.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

USD/CHF

Recent action shows that the Swissy extended Friday's bounce from the H4 demand at 0.9929-0.9963 up to parity (1.0000), which, as you can see, is currently proving to be a stable line of resistance. Given the velocity of the rebound from 1.0000, could further selling be seen? While it's possible the market may continue to pump lower, we would advise caution here! Not only is there a daily demand base currently in play right now at 0.9929-0.9975 (houses the current H4 demand), there's also a weekly trendline support intersecting with this zone! Therefore, the bears certainly have their work cut out for them if they intend on pushing this market lower.

Our suggestions: Owing to the above, our team has absolutely no interest in selling today. Instead, we're actually looking at buying from the H4 Quasimodo support at 0.9951 that's lodged within the aforementioned H4 demand. Usually, we'd look to place stops below the apex of the Quasimodo formation, but given where it's positioned, we feel stops would be best placed beyond the H4 demand base at 0.9927.

Data points to consider: FOMC member Dudley speaks at 10am GMT

Levels to watch/live orders:

- Buys: 0.9951 (stop loss: 0.9927).

- Sells: Flat (stop loss: N/A).

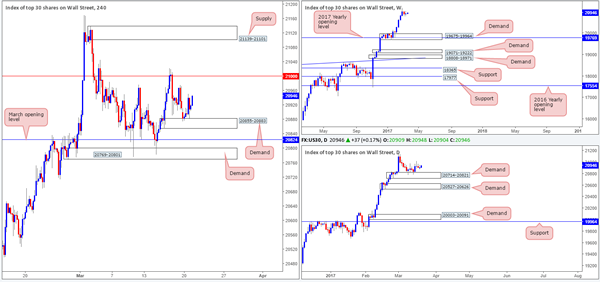

DOW 30

US equities bounced nicely from the H4 demand base fixed at 20855-20883 during the course of yesterday's sessions. Assuming that the bulls remain in control here, the next area of interest can be seen at the 21000 mark: a level that capped upside beautifully on Thursday. With the daily demand zone at 20714-20821 currently holding ground, and the weekly chart showing absolutely no weekly resistance ahead, we feel further buying is likely going to transpire today/this week.

Our suggestions: However, before our team can become buyers, we will need to see the H4 candles engulf the 21000 mark. In the event that this comes to fruition, and the H4 candles retest 21000 as support, we will look to buy the rejection candle off this number and target the H4 supply seen overhead at 21139-21101.

Data points to consider: FOMC member Dudley speaks at 10am GMT.

Levels to watch/live orders:

- Buys: Watch for price to engulf 21000 and then look to trade any retest seen thereafter (stop loss: dependent on the rejection candle, but ideally beyond the rejection candle's tail).

- Sells: Flat (stop loss: N/A).

GOLD

As can be seen from the H4 chart this morning, bullion is heavily selling off and has brought the unit to within touching distance of the H4 support area drawn from 1227.5-1223.9. While it is true that price bounced beautifully from this H4 zone on Thursday last week, it might be worth noting that the daily candles are currently housed within a daily resistance area at 1232.9-1224.5. Therefore, although history could repeat itself here, we would not feel comfortable buying from this barrier today.

Our suggestions: Should price engulf the current H4 support zone on the other hand, then we feel taking a short on any retest to the underside of this zone is attractive (assuming a reasonably sized H4 bear candle is seen following the retest), since the next area of support does not come into view until we connect with February's opening base line at 1211.5.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Watch for price to engulf the H4 support area at 1227.5-1223.9 and then look to trade any retest seen thereafter (stop loss: dependent on the rejection candle, but ideally beyond the rejection candle's wick).

Trade Idea : USD/CHF – Sell at 1.0020

USD/CHF - 0.9980

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9985

Kijun-Sen level : 0.9980

Ichimoku cloud top : 0.9975

Ichimoku cloud bottom : 0.9969

Original strategy :

Sell at 1.0020, Target: 0.9920, Stop: 1.0055

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0020, Target: 0.9920, Stop: 1.0055

Position : -

Target : -

Stop : -

As the greenback recovered after finding support at 0.9942 on Friday, suggesting consolidation above this level would be seen and corrective bounce to 1.0005-10 (38.2% Fibonacci retracement of 1.0109-0.9942) cannot be ruled out, however, reckon upside would be limited to 1.0025 (50% Fibonacci retracement) and bring another decline later. Below said support at 0.9942 would extend recent decline from 1.0171 to 0.9920-25 but loss of near term downward momentum should prevent sharp fall below 0.9900 and reckon 0.9870-75 would hold from here.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 1.0020-25 should limit upside and bring another decline. Only above previous support at 1.0060 (now resistance) would abort and signal low is formed instead, risk rebound to 1.0090-95 first.

Trade Idea : GBP/USD – Buy at 1.2300

GBP/USD - 1.2345

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2362

Kijun-Sen level : 1.2386

Ichimoku cloud top : 1.2375

Ichimoku cloud bottom : 1.2323

Original strategy :

Buy at 1.2310, Target: 1.2435, Stop: 1.2275

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2300, Target: 1.2435, Stop: 1.2265

Position : -

Target : -

Stop : -

Cable’s retreat after yesterday’s brief rise to 1.2436 suggests consolidation below this level would be seen and pullback to support at 1.2335 cannot be ruled out, however, reckon downside would be limited to 1.2310 (previous resistance now support) and bring another rise later, above said resistance at 1.2436 would extend recent upmove from 1.2109 (this month’s low) to 1.2450 but loss of near term momentum should prevent sharp move beyond previous resistance at 1.2479, risk from there has increased for a retreat to take place later.

In view of this, would not chase this move from here and we are looking to buy cable on pullback as said previous resistance at 1.2310 should limit downside and bring another rise. Below 1.2270-75 (50% Fibonacci retracement of 1.2109-1.2436) would defer and suggest top is possibly formed, risk correction to 1.2241 support.

Trade Idea : EUR/USD – Buy at 1.0700

EUR/USD - 1.0763

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.0745

Kijun-Sen level : 1.0748

Ichimoku cloud top : 1.0752

Ichimoku cloud bottom : 1.0744

Original strategy :

Buy at 1.0700, Target: 1.0800, Stop: 1.0665

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0700, Target: 1.0800, Stop: 1.0665

Position : -

Target : -

Stop : -

As the single currency has continued trading with a firm undertone after last week’s rally, suggesting recent erratic upmove from 1.0493 low is still in progress and may extend further gain towards previous chart resistance at 1.0829, however, loss of near term upward momentum should prevent sharp move beyond 1.0850-60 and price should falter well below 1.0890-00, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and we are looking to buy euro on subsequent pullback as 1.0706 support should limit downside and bring another rise later. Below 1.0675-80 would defer and suggest top is possibly formed, risk weakness to 1.0640 (previous resistance now support) but still reckon indicated support at 1.0600 would remain intact.