Sample Category Title

China’s Caixin PMI services falls to 51.5, manufacturing boosts composite index to 52.3

China’s Caixin PMI Services dropped to 51.5 in November from 52.0, missing market expectations of 52.5, reflecting a slowdown in the sector’s expansion. However, PMI Composite rose to 52.3 from 51.9, supported by improvements in manufacturing.

Wang Zhe, Senior Economist at Caixin Insight Group, highlighted the challenges facing the economy. He noted that while the downturn appears to be "bottoming out," the recovery requires "further consolidation." Persistent contraction in employment underscores that the impact of economic stimulus has yet to translate into labor market gains, with businesses hesitant to expand their workforce.

Wang also stressed the importance of monitoring the "consistency and effectiveness" of additional stimulus measures. The economy continues to face "structural and cyclical pressures," compounded by the risk of "continued accumulation of external uncertainties," necessitating "sufficient policy buffers."

Japan’s PMI services shows renewed growth, composite activity marginally improves

Japan’s services sector returned to growth in November, with PMI Services index finalized at 50.5, up from 49.7 in October. Composite PMI, which combines manufacturing and services activity, edged up to 50.1 from 49.6, signaling a modest overall improvement in private-sector activity.

Usamah Bhatti, Economist at S&P Global Market Intelligence, noted that the services sector experienced a "renewed upswing" as improved demand and stronger client confidence supported output and sustained new business growth. The sector’s near-term outlook appears favorable, with growth in outstanding business reaching its highest level in eight months, and optimism about the 12-month outlook remaining robust.

While the services sector drove the overall stabilization, the manufacturing sector continued to lag, with a slight contraction in production. Input cost pressures persisted across industries, contributing to higher prices for goods and services. However, businesses expressed optimism that inflationary and global uncertainties would subside, paving the way for a stronger rebound in Japan’s private sector.

ECB’s Holzmann: Modest rate cut possible next week, not more

Austrian ECB Governing Council member Robert Holzmann indicated in an interview with Austria's Oberösterreichische Nachrichten newspaper that a rate cut at next week's meeting is possible, but ruled out a significant reduction.

He stated that while the likelihood of a reduction "isn't zero," the cut would be "moderate, not very strong," as current data do not strongly support such a move.

Holzmann mentioned that a 25bps cut is "conceivable," but emphasized "not more" than that. Though, no decision has been made and it will depend on the "final data we receive."

He acknowledged that inflation developments have been moving in the "right direction," but recent "deviations to the upside" have emerged.

Additionally, he expressed concern over a "row of challenges" facing the economy, highlighting that the geopolitical environment suggests price increases are "more likely than unlikely." Contributing factors include rising oil and energy prices and potential impacts from policies under President-elect Donald Trump.

Fed officials signal neutral policy path but keep December decision open

Several Fed officials shared their views overnight but avoided giving specific guidance on what to expect at the December 18 FOMC rate decision. The tone of their remarks highlighted confidence in recent economic progress while maintaining a cautious stance on future rate adjustments.

Fed Governor Adriana Kugler characterized the US economy as being in a "good position" following significant strides toward maximum employment and price stability. She acknowledged that the labor market remains solid and inflation is steadily moving toward 2% target, albeit with "some bumps along the way."

Kugler emphasized that Fed is moving policy toward a "more neutral setting" while remaining vigilant for risks or supply shocks that could reverse progress.

San Francisco Fed President Mary Daly reiterated the importance of recalibrating policy but left the timing of adjustments undecided. "Whether it will be in December or sometime later, that's a question we'll have a chance to debate and discuss in our next meeting," she said.

Chicago Fed President Austan Goolsbee shared a more forward-looking perspective, suggesting that "over the next year it feels to me like rates come down a fair amount" from current levels. However, he acknowledged the importance of meeting regularly to reassess economic conditions as they evolve.

First Impressions: Australian National Accounts, September Quarter 2024

The Australian economy grew by a sluggish 0.3% in the September quarter, with increased government spending driving all of the gain. Private demand (spending by consumers and businesses) flatlined with household consumption and new business investment surprising to the downside, both holding flat over the quarter.

The Australian economy grew by a sluggish 0.3% in the September quarter, with increased government spending driving all of the gain. Private demand (spending by consumers and businesses) flatlined with household consumption and new business investment surprising to the downside, both holding flat over the quarter. The outcome was softer than Westpac’s forecast of 0.6%qtr and the market forecast of 0.5%qtr.

The main takeaway from the September update however is that an expected tentative recovery in private demand has not formed. The RBA did flag that a flat quarter for consumption was likely. However, the weakness of annual growth in spending and continued pressures on household disposable income – even with tax cuts flowing – points to a weaker underlying picture.

In another sign of the weaker underlying picture, average (non-farm) earnings per hour moderated to grow 1.3% in six-month annualised terms, down from 2.3%yr in the June quarter and well below the pre pandemic average of 1.8%.

In year ended terms, the economy grew 0.8% in the September quarter – the slowest annual rate since the early 1990s recession outside of the pandemic. This was considerably softer than Westpac’s forecast of 1.2%yr and the 1.1%yr increase expected by the market.

Total new spending by governments continues to grow strongly and is now at a record share of the economy (27.5% of GDP from the previous peak of 26.9% of GDP last quarter). New public investment increased 6.1%, off the back of a spike in defence-related spending and increased investment in infrastructure. Public consumption continued to grow at a solid pace (1.4%qtr and 4.7%yr), as cost-of-living measures announced in recent budgets kicked in from 1 July.

New private demand grew 0.1%qtr to be 0.7% higher over the year to Q3. This was slightly higher than the flat quarterly outcome recorded in Q2. With population running at a brisk 2¼%yr, new private demand on a per capita basis continues to go backwards.

The consumer sector continues to be sick, recording a flat outcome over the quarter to be just 0.4% higher in annual terms. This suggests that per capita consumption has fallen by almost 2.0% over the past year.

Actual consumption is estimated to have been around 0.3ppts higher in the quarter, as governments used rebates and other cost of living measures to pick up the tab for certain consumption items such as electricity, public transport, cheaper car rego etc.

The benefits of costs of living measures, including the stage 3 tax cuts, were largely saved, with the household savings ratio increasing to 3.2% in the September quarter.

New business investment declined 0.2%qtr in the September quarter to be 1.5% higher in annual terms. Non-dwelling construction unexpectedly fell in the quarter, in part due to larger transfers to the public sector. Machinery and equipment continued to increase, up 0.6%qtr to be 0.7% lower in annual terms. CAPEX data showed the industries at the forefront of the underlying structural changes impacting the economy (such as investment in clean energy and renewables) continue to invest, which is being offset by businesses at the coalface of the consumer led slowdown.

Net exports and inventories were as expected. Net exports contributed 0.1 ppts to growth in GDP in the September quarter, on the back of a positive contribution from the net goods balance. Inventories detracted 0.3 ppts from growth in the September quarter, with the private sector running down its stock of inventories for a second consecutive quarter.

Cost pressures continue to moderate as the impact of the larger than average 2022-23 minimum and award wage increase roll out of annual calculations. Average (non-farm) earnings per hour moderated to 3.2%yr, from 6.5%yr in the June quarter. Not only was there a step down, but the pace of the decline is gathering speed with average (non-farm) earnings per hour up just 1.3%yr in six-month annualised terms, down from 2.3%yr in the June quarter and well below the pre pandemic average of 1.8%. This is leading to a moderation in unit labour costs (a key measure of domestic cost pressures). ULCs are now running at 3.9%yr, a touch above the outcomes recorded over 2019 when underlying inflation was below the target band.

Elliott Wave View: USDJPY Impulsive Decline Favors More Downside

Short Term Elliott Wave structure in USDJPY suggests that rally to 156.76 ended wave X. This completed correction against cycle from 7.3.2024 high. Pair has now turned lower. Structure of the decline from 156.76 is unfolding as 5 waves impulsive Elliott Wave structure. Down from 156.76 high, wave (i) ended at 155.14 and wave (ii) ended at 155.78. Wave (iii) lower ended at 153.85 and wave (iv) rally ended at 154.74. Final leg wave (v) ended at 153.83 which completed wave ((i)). Corrective rally in wave ((ii)) ended at 155.88 as expanded flat.

Pair has resumed lower in wave ((iii)). Down from wave ((ii)), wave (i) ended at 153.54 and wave (ii) ended at 154.72. Wave (iii) lower ended at 149.52 and wave (iv) ended at 150.53. Final leg wave (v) ended at 149.46 which completed wave ((iii)) in higher degree. Rally in wave ((iv)) ended at 150.74. Expect pair to extend lower 1 more leg to end wave ((v)). This should complete wave 1 in higher degree. Afterwards, it should rally in wave 2 to correct cycle from 11.15.2024 high before turning lower again. Near term, as far as pivot at 156.76 high stays intact, expect rally to fail in 3, 7, 11 swing for further downside.

USDJPY 60 Minutes Elliott Wave Chart

USDJPY Elliott Wave Video

https://www.youtube.com/watch?v=jsMMeXW82LA

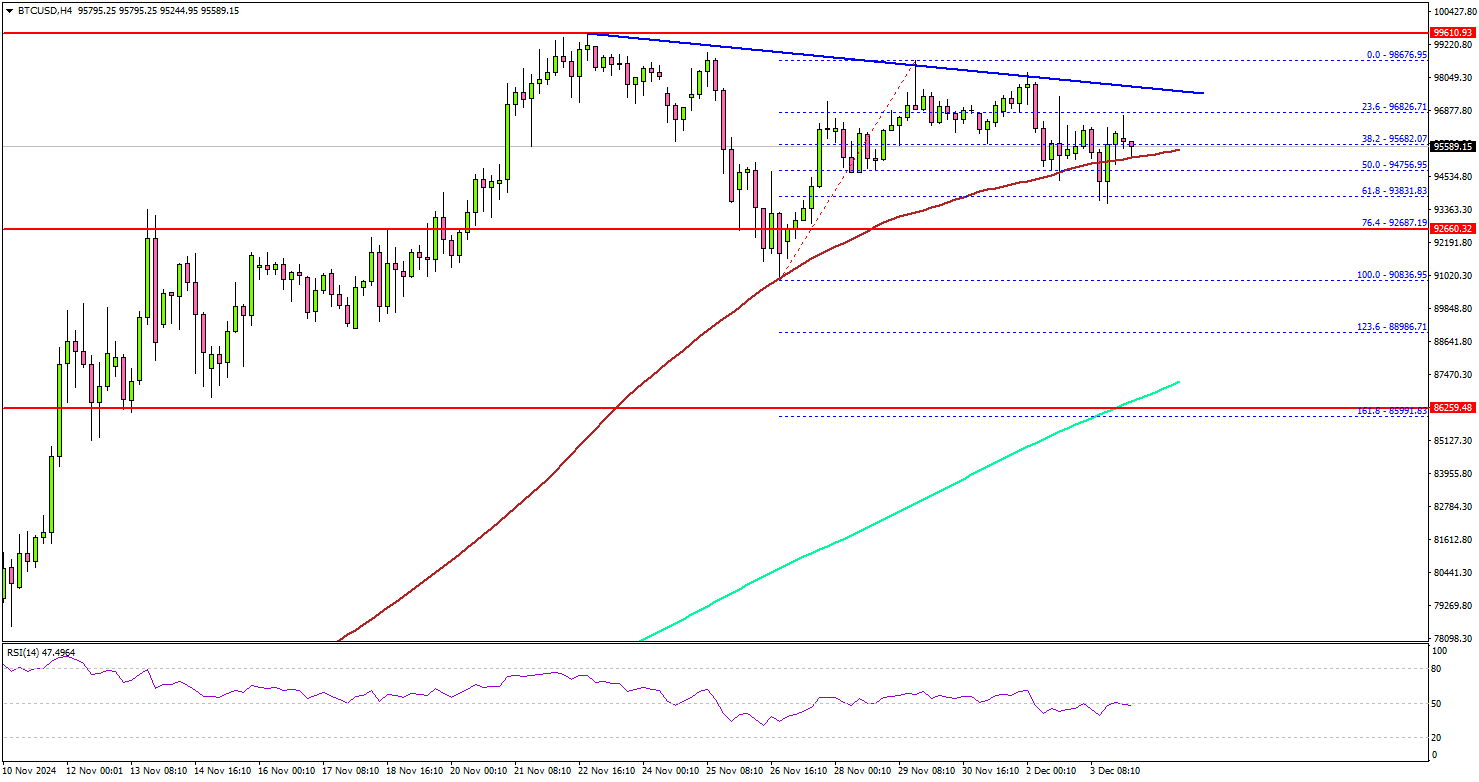

Bitcoin Uphill Climb: Can The King of Crypto Break Through?

Key Highlights

- Bitcoin price started a consolidation phase below the $100,000 zone.

- A connecting bearish trend line is forming with resistance at $97,500 on the 4-hour chart.

- Ethereum price seems to be facing hurdles near the $3,750 zone.

- XRP extended its surge toward $2.85 before correcting some points.

Bitcoin Price Technical Analysis

Bitcoin price made another attempt to gain pace above the $95,000 resistance zone. However, BTC/USD failed to settle above $98,000 and failed to test $100,000.

Looking at the 4-hour chart, the price started a downside correction from the $98,800 zone. There was a move below the $96,800 and $95,500 support levels. The price dipped below the 50% Fib retracement level of the upward move from the $90,836 swing low to the $98,676 high.

Immediate support is near the $92,650 level. It is near the 76.4% Fib retracement level of the upward move from the $90,836 swing low to the $98,676 high.

The next key support sits at $90,800. A downside break below $90,800 might send Bitcoin toward the $88,000 support. Any more losses might send the price toward the $85,000 support zone.

On the upside, the price could face resistance near the $96,500 level. There is also a connecting bearish trend line forming with resistance at $97,500 on the same chart. The next key resistance is $97,200.

The main hurdle is now near $98,000. A successful close above $98,000 might start another steady increase. In the stated case, the price may perhaps rise toward the $100,000 milestone level.

Looking at XRP, the bulls pumped the price above the $2.50 and $2.70 levels before the bears took a stand near the $2.85 zone.

Today’s Economic Releases

- US ISM Services Index for Nov 2024 – Forecast 55.5, versus 56.0 previous.

- US Factory Orders for Oct 2024 (MoM) - Forecast +0.2%, versus -0.5% previous.

Year Ahead – What Does 2025 Hold for US Dollar and Japanese Yen?

- US dollar set for bullish start to new year as Fed rate cut bets pared

- Yen bears make a comeback, but will they reign in 2025?

- Fed and BoJ policy expectations diverge after Trump’s re-election

‘Trump trade’ reinforces dollar bulls

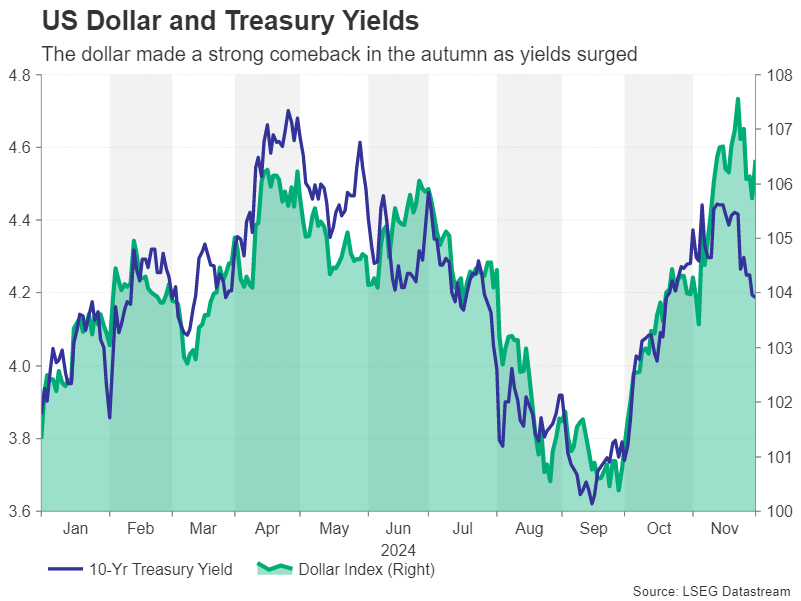

The Federal Reserve finally cut interest rates in September, but far from falling, the US dollar embarked on a fresh rally as policymakers dashed hopes of aggressive policy easing. As we head into 2025, there can be no denying about the dollar’s superiority. The greenback is not only being supported by a resilient US economy and persistent price pressures, but also by expectations that the incoming Trump administration will enact polices that will further boost growth and inflation.

Donald Trump’s historic victory in the 2024 presidential election is shaping up to be the defining narrative for financial markets in 2025. But as the dollar and assets such as US equities and cryptocurrencies cheer the prospect of a Republican-controlled Congress, Trump’s return to the White house isn’t being celebrated by everyone.

Leaving aside the risk to countries that will probably be at the receiving end of Trump’s trade tirade, his election pledges, which are deemed to be inflationary, could cause a major headache for the Fed. Expectations that big tax cuts and tariff hikes will fuel inflation have already pushed Treasury yields to multi-month highs, powering the dollar’s rally.

How inflationary will Trump’s policies be?

The question for the 2025 outlook is how quickly the Republicans will be able to push through their tax agenda and how readily will Trump resort to imposing higher tariffs as he begins trade negotiations with America’s major trading partners like the European Union, Mexico and China?

But it’s not just about the timing. With a budget deficit running at more than 6% of GDP and a ballooning national debt, the Republicans could slash spending to pay for their tax giveaways, offsetting some of the boost to the economy from lower taxes.

When it comes to tariffs, it’s yet unclear how far the new Trump administration will go in slapping higher levies on imports, particularly on Chinese goods, which could be in excess of 60%. Trump has a tendency of using scaremongering as a negotiating tactic.

Hence, for the dollar, it’s all about how much has already been priced in and how much that’s yet to be factored in by investors. Any signs that Trump’s election promises will be watered down are likely to be negative for the US dollar during 2025. Similarly, should there be any delays by the newly elected lawmakers in preparing and agreeing to Trump’s legislative agenda, a dollar pullback is a strong possibility.

However, if the Republicans move swiftly with tax cuts and Trump shows his unwillingness to compromise on trade, the dollar will be well positioned to climb towards its 2022 highs when the Fed was hiking rates aggressively.

The Fed’s inflation dilemma

Although the Fed’s tightening days are over and borrowing costs are now falling, the inflation battle is not won and policymakers are wary about lowering rates too quickly. The Fed’s unexpectedly hawkish stance is underscoring the greenback’s bullish outlook. The main concern is that inflation appears to be settling closer to 2.5% instead of the Fed’s 2.0% target.

If this is the case even before Trump has taken office, there’s a real risk that the Fed will not be able to deliver many rate cuts in 2025, while a rate hike cannot be completely ruled out.

Geopolitical risks

Away from domestic politics and Fed policy, the risks to inflation are somewhat tilted to the upside. Assuming there is no nuclear fallout in the meantime, a Trump presidency will probably push for a ceasefire agreement between Ukraine and Russia. However, Trump is likely to take a more hard-line stance against Iran. This risks triggering a wider conflict in the Middle East, especially if it involves tougher sanctions on Iranian oil, or allowing Israel to strike Iran’s oil facilities.

A fresh oil price shock is hardly what the Fed needs when it’s still struggling to tame inflation. As the world’s reserve currency, the dollar also stands to gain directly from risk-off episodes.

Summing up, although there’s not a lot on the horizon that can trigger a massive dollar selloff, its ability to continue marching higher hinges on the actual size of Trump’s tax cuts and tariff increases that will eventually be approved.

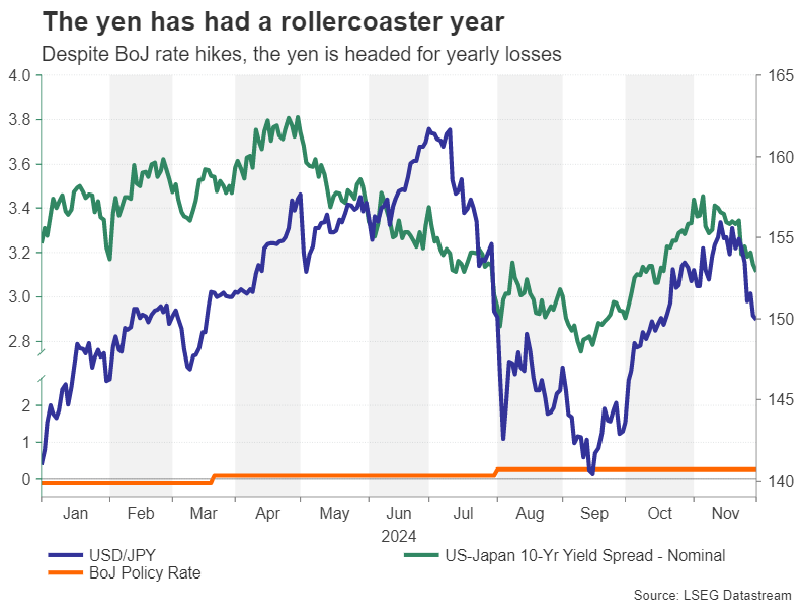

Yen’s rollercoaster ride

So where does all this leave the yen? The Japanese currency staged a dramatic recovery over the summer from levels last seen in 1986. The bullish reversal was driven by a combination of policy pivots by the Bank of Japan and the Fed, as well as direct intervention in the currency markets by Japanese officials.

However, the Bank of Japan’s hawkish surprises soon turned to caution and uncertainty about the pace of subsequent rate hikes has been weighing on the yen. But that’s not to say that the yen can’t restore its bullish posture in 2025.

BoJ has one eye on wages

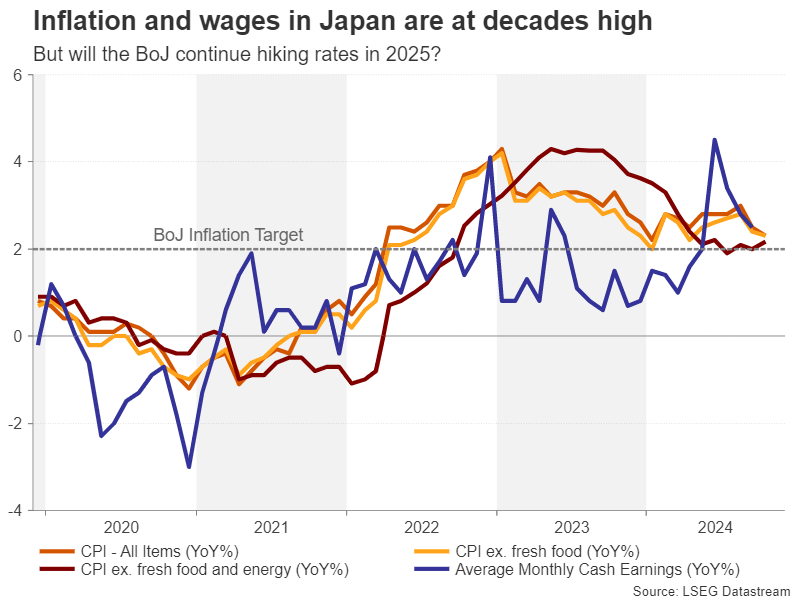

Although inflation in Japan has fallen to around 2.0%, policymakers see upside risks to the outlook from wage pressures as well as higher import costs from the weaker yen and increases in commodity prices. The BoJ is hopeful that next year’s spring wage negotiations will lead to another round of strong pay deals.

The country’s biggest trade union is aiming for wage increases of at least 5.0%. Such an outcome could pave the way for the BoJ to hike rates to 1.0% by the end of 2025.

Yield differentials matter

However, even if borrowing costs do rise to 1.0% or higher, yield differentials with the US might not necessarily narrow much if the Fed finds itself with very limited scope to trim its rates. Hence, whilst the BoJ may catch some investors off guard with its determination to normalize monetary policy, any yen rebound will depend as much on Fed policy as on domestic policy.

Still, with uncertainty hanging over the global economic outlook due to the elevated geopolitical tensions and Trump back at the White House, safe haven flows could also be the yen’s saviour in 2025.

USD/JPY Technical Analysis: Is a Short-Term Pullback Imminent Despite USD/JPYs Slide?

- USD/JPY continues its decline, with a fresh low around 148.797.

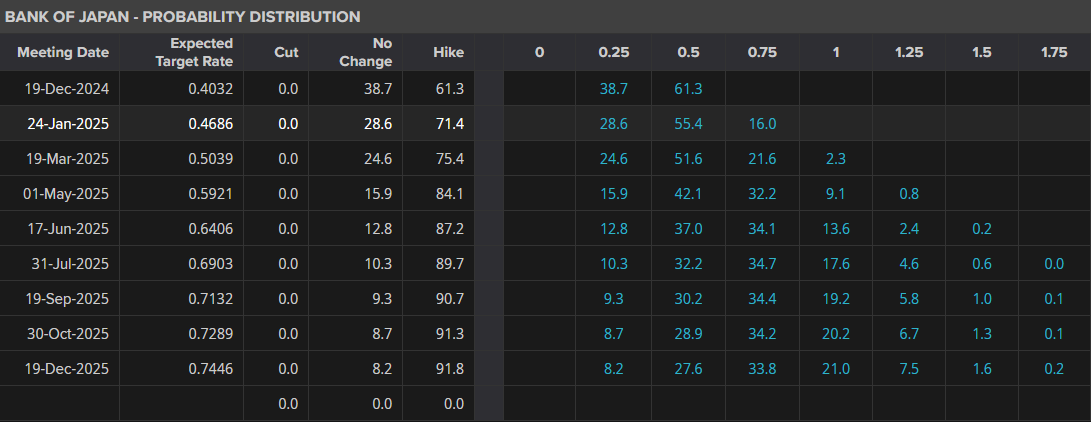

- Bank of Japan (BoJ) Governor Ueda’s hawkish rhetoric suggests a potential rate hike sooner than later.

- Technical analysis indicates a potential short-term pullback towards 150.00, despite the overall downward trend.

USD/JPY has continued its decline today having displayed some resilience with a brief pullback in part of the Asian and early European sessions. This optimism has since dissipated with the pair printing a fresh low around the 148.797 handle.

The technical picture for the Yen has been an intriguing one with the possibility of a break or bounce of the psychological 150.00 handle discussed last week Key levels were laid out in the article titled USD/JPY Price Outlook – Yen Extends Gains as Key Confluence Level Approaches, which has since played out pretty much as expected.

USD/JPY Technical Analysis: Is a Short-Term Pullback Imminent Despite USD/JPYs Slide?

There has long been a push for the BoJ to normalise policy and something which current Governor Ueda was brought in for. However, the Governor has been resolute since taking office that he will only act when he is happy with wage growth data in Japan. The Governor had been adamant that wage growth needed to outpace inflation before significant rate hikes.

Recent data including CPI and PPI are on the right track. The most important for Governor Ueda has been wage growth which has been rising as well with Prime Minister Ishiba and unions pushing for a 5-6% pay hike in next year’s wage talks. Governor Ueda meanwhile over the weekend continued his hawkish rhetoric that the BoJ is likely to hike rates sooner than later.

Immediate risks to the USD/JPY come from US jobs data this week. The data will have an impact on the probability of a December rate hike and thus needs to be monitored.

Probabilities of a BoJ Rate Hike

Source: LSEG

Technical Analysis USD/JPY

From a technical standpoint, USD/JPY is currently trading below the 100-day MA but a daily candle close below the MA will be key. There are concerns that a potential short-term pullback toward 150.00 may materialize.

The last two days have proven that bullish interest remains with a push higher on both days before selling pressure prevailed. Could this be a warning that a short-term pullback may be incoming?

The RSI remains above the oversold region as well which will give sellers another vote of confidence. However, a daily candle close above the 100-day MA might give sellers a brief pause and potentially wait for a pullback before getting involved.

What could work in favor of USD/JPY is seasonality. The US Dollar is historically poor in December as market participants usually pivot to more riskier assets like US equities. There is also the possibility of portfolio rebalancing ahead of 2025.

USD/JPY Chart, December 3, 2024

Source: TradingView (click to enlarge)

Support

- 148.96

- 147.95

- 146.37

Resistance

- 150.00

- 150.87

- 151.98