Sample Category Title

New Altcoin Leaders Emerge as Bitcoin Stalls Below $100K

Market Picture

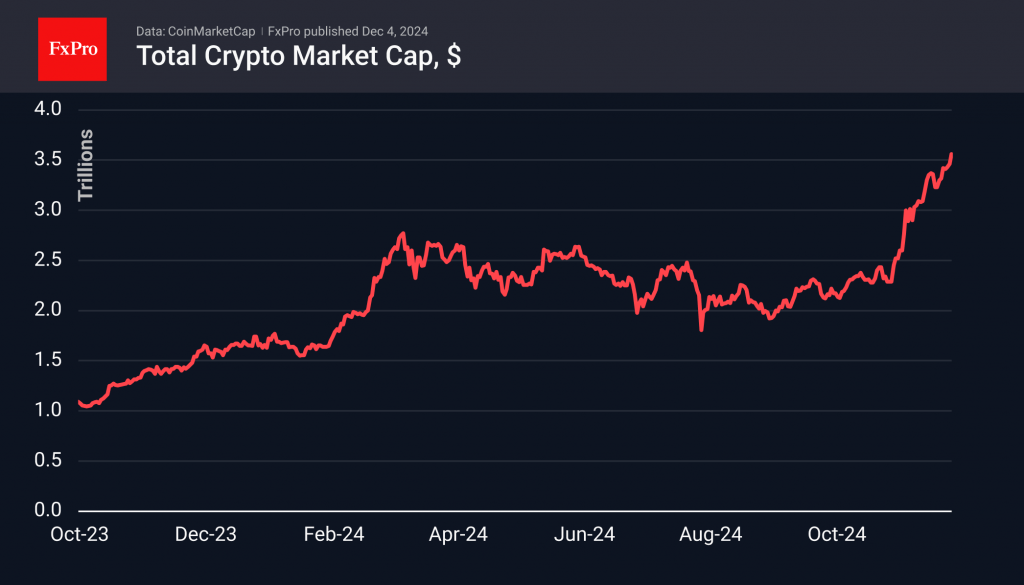

The crypto market has grown by 2.6% in the last 24 hours, reaching a new record of $3.56 trillion. Altcoins are still driving the growth, but this time, the momentum comes from different players. Among the top performers over the past day were Tron (+67%) and BNB (+18%). The Altcoin Season Index reached 89 amid a near doubling of altcoin capitalisation over the past month, four times faster than Bitcoin’s gains.

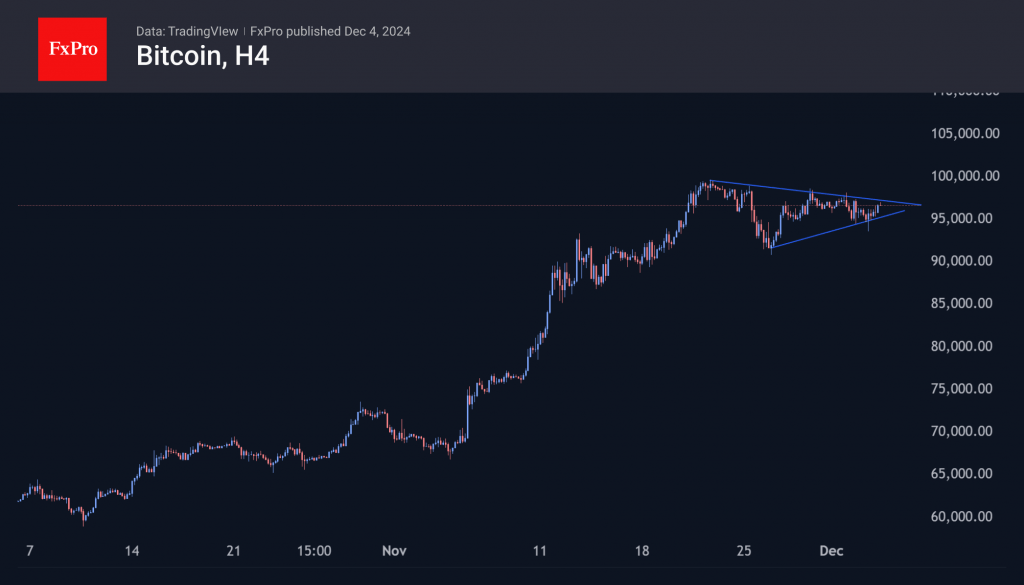

The first cryptocurrency is up 1.4% in 24 hours, hovering just below $97,000. On Tuesday, events in South Korea caused a brief dip to $93K, which attracted additional buying. Bitcoin’s rise seems like a logical trend amid political uncertainty in rich countries, including France and Germany. Technically, bitcoin remains in a consolidation mode as the price sits in the $92-100K range.

On Tuesday, Tron soared. A dramatic acceleration of growth occurred with the renewal of historical highs at $0.23. Liquidation of short positions brought the price closer to $0.45 before stabilising at $0.39. A continuation of the bull run makes $0.60 the next potential target.

News Background

Another recalculation showed that the first cryptocurrency’s mining difficulty increased by 1.59%, reaching a high of 103.9 T. The average hash rate for the period since the last value change was 832.7 EH/s.

BTC growth will be volatile due to the profit taken by holders and BTC ETF dynamics. At the end of last week, clients withdrew $457 million from Bitcoin funds, while long-term investors reduced their balances by 508,990 BTC.

According to Bitfinex, the number of coins held by speculators approached a cyclical high of 3,282,000 BTC. The number of coins held by long-term investors fell to 12.45 million BTC, the lowest since July 2022, IntoTheBlock calculated.

Arkham Intelligence noted that US authorities sent 10,000 BTC (~$963 million) related to Silk Road to Coinbase. QCP Capital attributes the current bitcoin correction to these reports.

BoE’s Bailey reiterates gradual approach to rate cuts

In an interview with the Financial Times, BoE Governor Andrew Bailey acknowledged that while inflation had recently dropped to target levels, there remains “a distance to travel” in managing price stability. He noted that inflation might temporarily exceed target levels again ahead.

Bailey addressed market expectations for four rate cuts next year, emphasizing that BoE's projections are "conditioned on market rates" and highlighting the word "gradual" in their approach.

On the impact of Donald Trump’s return to the White House and the associated rise in tariffs, Bailey described the effects as "not straightforward at all."

He explained that such policies could move traded prices but are also contingent on reactions from other countries and exchange rate adjustments, adding further uncertainty to the inflation outlook.

EURAUD Surges Higher

- EURAUD trades aggressively higher today

- The upleg has paused at two key SMAs

- Momentum indicators are mostly bullish

EURAUD is recording a sizeable upleg today following the weak Australian GDP print for the third quarter of 2024 that somewhat opened the door to an RBA cut in early 2025. The rally has paused at the 100- and 200-day simple moving averages (SMAs), with euro bulls recovering a good chunk of their recent losses in fewer than 10 sessions. The overall trend remains negative though, supported by the political shenanigans in the eurozone.

Meanwhile, the momentum indicators are mostly bullish. The RSI has climbed once again above its midpoint, and it appears eager for a move higher. More importantly, the stochastic oscillator is edging higher, towards its overbought territory, and building a good gap from its moving average. Only the Average Directional Movement Index (ADX) is ignoring the currently bullish move, as it continues to point to a trendless market.

Should the bulls remain thirsty, they could try to push EURAUD above the 100- and 200-day SMAs and towards the 23.6% Fibonacci retracement level of the August 26, 2022 – April 26, 2023 uptrend at 1.6406. If successful, the door could then be wide open to retest the August 24, 2015 high at 1.6583.

On the other hand, the bears are probably keen on retaking market control. Their first task is probably to keep EURAUD below the 1.6363-1.6375 area, and then gradually push it lower towards the 1.6256-1.6250 region. It would be a strong win for the bears if they managed to quickly erase today’s price action, giving them the opportunity to stage a new selloff towards 1.6000.

To sum up, EURAUD is trading higher today, but the bulls need to overcome some key resistance levels for the current rally to have legs.

Australian Dollar Hits Four-Month Low Amid Weak GDP Data

The Australian dollar fell to a four-month low of 0.6450 against the US dollar on Wednesday, following disappointing GDP data that heightened expectations for potential interest rate cuts by the Reserve Bank of Australia (RBA).

The latest GDP figures revealed that Australia’s economy expanded by only 0.3% quarter-over-quarter in Q3, falling short of the anticipated 0.4% growth. Year-on-year, the growth rate was just 0.8%, significantly below the expected 1.0%. These figures have raised concerns on trading floors about the possible onset of a recession.

Despite the weak GDP report, expectations for the RBA’s upcoming December meeting remain unchanged. The consensus is that the central bank will hold rates steady while continuing to assess economic conditions. However, market sentiment regarding the medium-term monetary policy has shifted slightly, with a 30% likelihood of an RBA rate cut by February. Investors are increasingly betting on the possibility of adjustments by May.

Externally, the Australian dollar is facing additional pressure from a stronger US dollar, which continues to attract investors seeking safe-haven assets amid global economic uncertainties.

Technical analysis of AUD/USD

H4 chart: the AUD/USD pair has reached the target of its recent decline at 0.6490 and is now forming a growth structure towards 0.6480. A broad consolidation range may develop around this level. If the price breaks above this range, a rise to 0.6555 is anticipated. This bullish scenario is supported by the MACD indicator, with its signal line below zero but poised for an upward movement.

H1 chart: the market has nearly reached the primary target of the decline at 0.6490 and is expected to initiate a growth structure to 0.6485. A narrow consolidation range may form, and a breakout above this range could lead to an ascent towards 0.6555, followed by a potential retracement to 0.6480. Once this level is reached, another upward wave towards 0.6700 may be possible. The Stochastic oscillator supports this analysis, with its signal line currently below 20 but expected to climb sharply towards 80, indicating potential for upward momentum.

Eurozone PPI rises 0.4% mom in Oct led by rising energy costs

Eurozone PPI increased by 0.4% mom in October, aligning with market expectations. On an annual basis, PPI fell by -3.2% yoy, the anticipated -3.3% decline, reflecting mixed dynamics across sectors.

In Eurozone, Energy prices surged by 1.4% mom, driving the monthly increase, while intermediate goods prices slipped by -0.1% mom. Capital goods prices were unchanged, while durable consumer goods rose by 0.3% mom and non-durable consumer goods by 0.2% mom.

Across the EU, PPI also rose by 0.4% mom, while the annual figure showed a decline of -3.0% yoy. Among Member States, Estonia and Italy led the monthly increases with a 1.0% rise, followed by France (+0.9%) and Sweden (+0.8%). Conversely, Bulgaria experienced the sharpest decline at -2.9%, followed by Slovakia (-2.0%) and Romania (-1.5%).

UK PMI services finalized at 50.8, growth stalls amid rising costs and gloomy outlook

UK services sector showed signs of slowing in November, with final PMI Services reading dropping to 50.8 from October’s 52.0, marking the weakest level in 13 months. Composite PMI similarly declined to 50.5 from 51.8, barely holding above the threshold for expansion.

Tim Moore, Economics Director at S&P Global Market Intelligence, remarked that service providers saw activity "close to stalling". Businesses faced weaker sales pipelines, postponed projects, and heightened caution among clients, all of which curtailed growth.

Additionally, the anticipation of higher employer National Insurance contributions weighed on hiring decisions, with workforce numbers shrinking for the second consecutive month. Many firms cited margin pressures as a reason for not replacing departing staff.

Inflationary pressures intensified, with salary costs driving input price increases at the fastest pace since April. This, coupled with worries about policies outlined in the Autumn Budget, led to a "considerable reduction" in business optimism.

Eurozone PMI composite finalized at 10-month low as stagflation concerns loom

Eurozone’s final PMI Services reading fell to 49.5 from October’s 51.6, marking a 10-month low. Composite PMI followed suit, dipping to 48.3 from 50.0, also the lowest in 10 months, indicating that the region’s private sector is contracting.

Among major economies, Ireland stood out as a bright spot with its Composite PMI hitting a 30-month high at 55.2. Conversely, Germany and France—the bloc's economic heavyweights—reported Composite PMI levels of 47.2 and 45.9, respectively,.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, described Eurozone’s predicament as a case of "stagflation," a challenging scenario for central bankers.

"The economy started shrinking while the PMI price components went up for the second month in a row," he noted. Inflation pressures remain high, driven largely by the services sector, and the weaker Euro adds to concerns about rising import costs in the coming months.

ECB finds itself in a precarious position ahead of its December 12 policy meeting. While the sluggish economy could benefit from monetary easing, inflationary pressures, exacerbated by substantial wage growth in Q3, limit its room to maneuver.

De la Rubia expects ECB to avoid aggressive action, likely opting for a cautious 25bps rate cut.

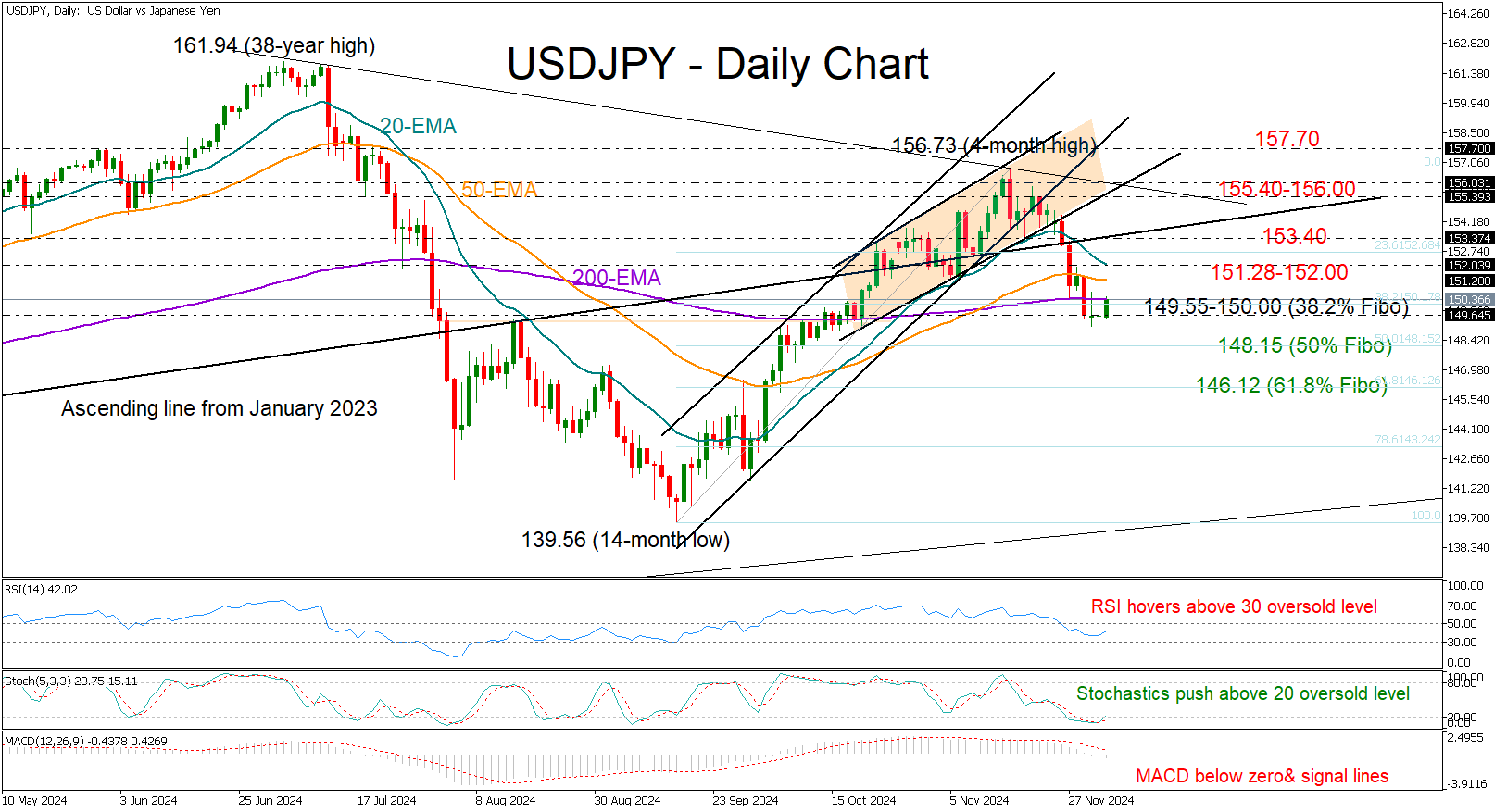

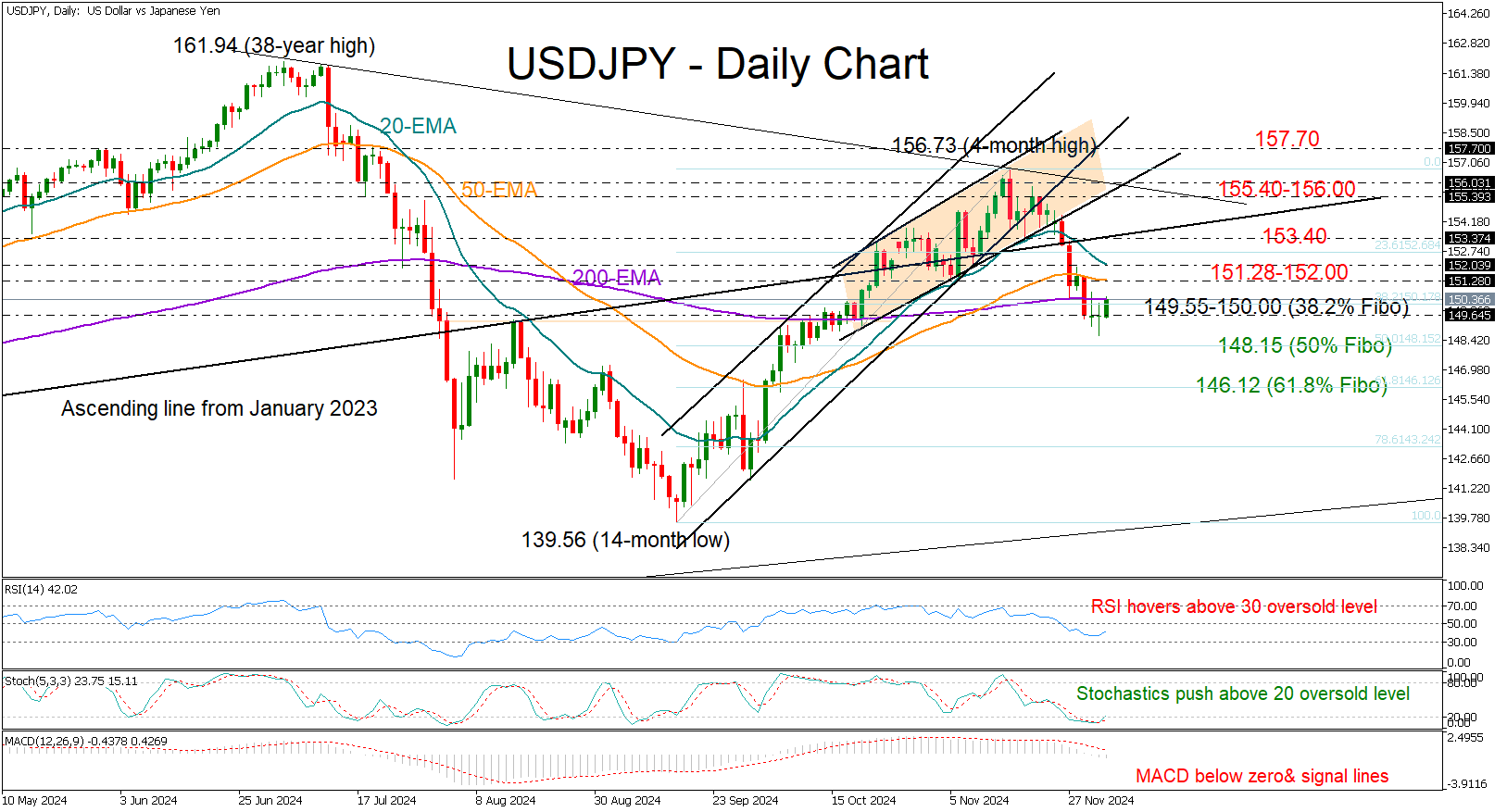

USDJPY Fights for a Close Above 150

- USDJPY stuck within 149.55-150.00 area

- Short-term risk is skewed to the downside

- ADP Jobs data, ISM non-mfg PMI on the agenda

USDJPY is pushing again for a close above the 150.00 number and the 200-day exponential moving average (EMA) after closing around the 149.55 base for the third consecutive trading day on Tuesday.

There is no sufficient evidence that the market is oversold. Although the stochastic is set for an upturn above 20, the RSI has yet to reach its 30 oversold level and the MACD is in downward move within negative area. Hence, traders might need stronger increases before boosting their exposure in the market.

A sustainable move above 150.00 and beyond the 20- and 50-day EMAs at 151.28 and 152.00 respectively could see a test near the 153.40 barrier. The bulls must breach the latter to advance toward the 156.00 resistance.

However, should the bears successfully claim the 149.55 floor, the 50% Fibonacci retracement of the previous uptrend could come first into play at 148.15. A step lower could squeeze the price straight to the 61.8% Fibonacci mark of 146.12.

In a nutshell, USDJPY continues to face a bearish bias below 150.00. In the event of an upside breakout, downside risks may not evaporate until the price runs sustainably beyond 153.40, while an extension above 156.00 would put the price back on an uptrend.

WTI Crude Oil Rises Towards Downtrend Line

- WTI crude oil meets 70.00 level

- Remains in trading range in short-term

- Broader outlook is still bearish

WTI crude oil prices have seen a notable bullish reaction during yesterday's session, almost testing the medium-term descending trend line near 70.40. The commodity has battled several times with the diagonal line over the last month, but it is still holding within a sideways channel since October 14.

If the price has a successful upside attempt beyond the 50-day simple moving average (SMA) at 70.75, then it may test the upper boundary of the range at 72.95. Even higher, the market would fight with the 200-day SMA at 76.65.

On the other hand, a potential decline could send traders toward the previous low of 67.00, ahead of the 17-month trough of 65.70. A move below this area would endorse the longer-term bearish outlook.

The technical oscillators are confirming the upside move, with the MACD extending its positive momentum above its trigger line and the stochastic heading toward the overbought area.

All in all, WTI crude oil needs a sustained bullish boost to exit from the consolidation area in the near term, and the broader bearish outlook is still in place.

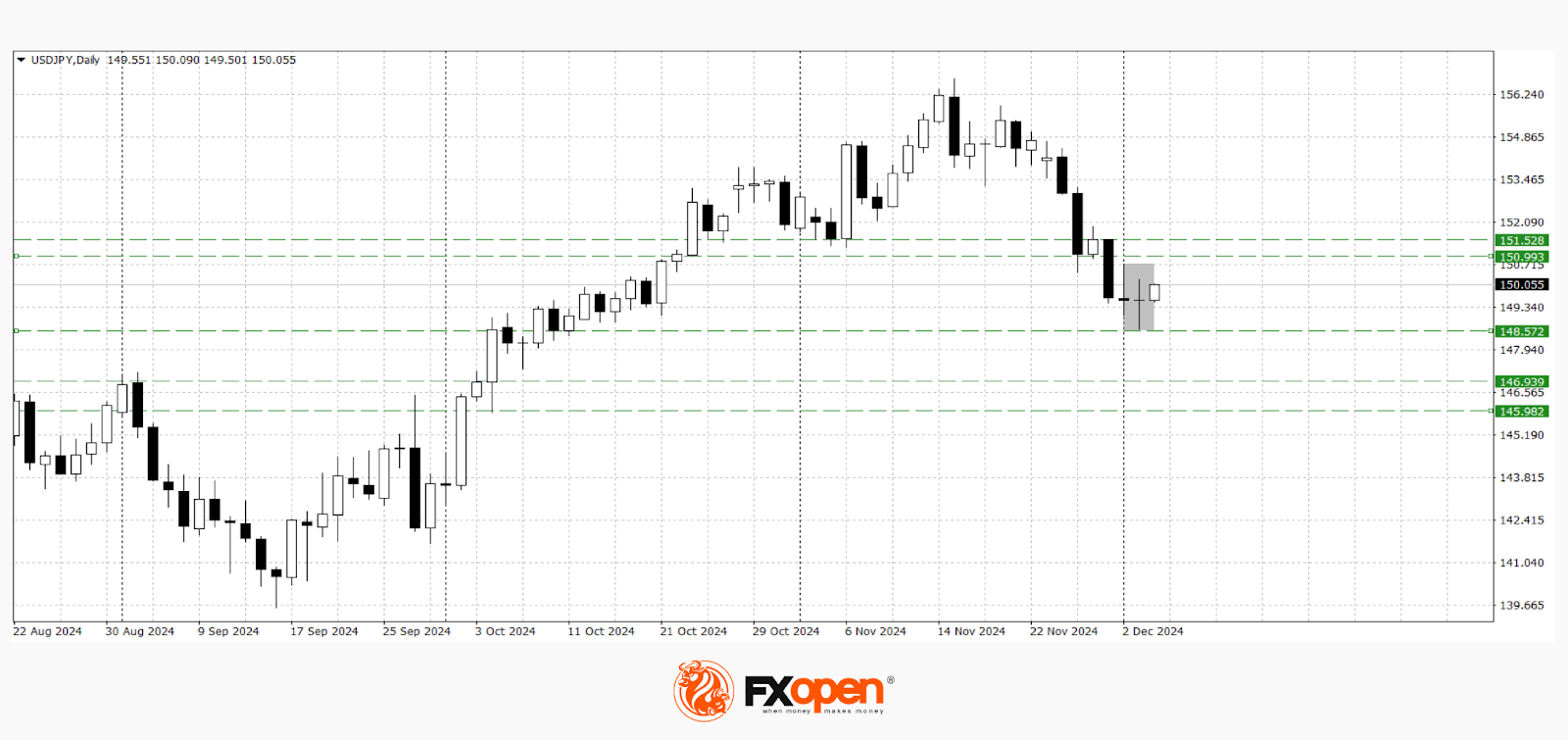

Yen Strengthens on Rate Hike Expectations; Euro Tests Recent Lows

USD/JPY

Over the past week, the USD/JPY pair dropped by approximately 500 pips. As anticipated, sellers tested the critical 150.00–149.00 range. This level may serve as the starting point for an upward corrective rebound.

The sharp decline in USD/JPY is likely tied to recent comments from the Bank of Japan’s Governor, Kazuo Ueda, hinting at a potential rate hike soon. He noted that "economic data is progressing as planned." Following Tokyo's inflation data showing an uptick and increased business investments, experts now predict the BoJ may raise rates by 0.5% at its December meeting.

Technical analysis suggests USD/JPY may begin an upward correction after its sharp fall, as a reversal "doji" candlestick pattern has formed on the daily timeframe.

If the 149.00–148.60 range holds as support, the pair could strengthen towards 151.50–151.00. However, a break below yesterday’s low may resume the downtrend towards 147.00–146.00.

Key upcoming events for USD/JPY in the next trading sessions include:

- 16:15 (GMT +3): ADP Non-Farm Employment Change (US)

- 17:45 (GMT +3): US Services PMI

- 18:00 (GMT +3): ISM Non-Manufacturing PMI (US)

EUR/USD

The euro remains under pressure. In addition to the threat of US-imposed trade tariffs, concerns over the French government have emerged. A political crisis could result in the government’s resignation, exerting further downward pressure on EUR/USD.

Currently trading near 1.0500, the pair may see an upward correction towards 1.0700–1.0600 if buyers manage to push it above the 1.0600–1.0540 zone. However, another rejection at 1.0540 could lead to fresh lows around 1.0340.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.