Sample Category Title

Australian Dollar Eyes GDP

The Australian dollar is drifting on Tuesday. In the North American session, AUD/USD is trading at 0.6461, down 0.20% on the day at the time of writing.

Australia’s GDP expected to improve in Q3

Australia’s economy is expected to improve in the third quarter, with a market estimate of 0.4% q/q. This follows a disappointing gain of 0.2% in Q2, the weakest growth in five quarters, as household spending declined. On a yearly basis, GDP is expected to tick up to 1.1% compared to 1% in the second quarter.

The Australian economy continues to groan under the weight of high interest rates, which the Reserve Bank of Australia implemented in order to tame high inflation. Now that inflation has come down, there is pressure on the RBA to respond with lower rates. The RBA has become an outlier as most major central bank are in the middle of an easing cycle.

RBA Governor Bullock has remained hawkish, reiterating that underlying inflation is too high for the RBA’s liking and that a rate hike is not off the table. Headline inflation has fallen to 2.1%, well within the RBA’s target bank of 2%-3%, but the RBA remains concerned about underlying inflation, which accelerated in October to 3.5%, up from 3.2% a month earlier.

The market isn’t buying the warning of higher rates and expects the next rate move to be a cut sometime in mid-2025. That means that consumers will have to grapple with high rates for months, barring an unexpected fall in underlying inflation.

In the US, Federal Reserve Governor Christopher Waller said on Monday that he is leaning toward a cut in December but could change his mind if inflation surprised on the upside. The US releases November CPI one week prior to the rate announcement and the release will be a key factor as to whether the Fed cuts or maintains interest rates.

AUD/USD Technical

- AUD/USD tested resistance at 0.6478 earlier. Next, there is resistance at 0.6514

- 0.6441 and 0.6405 are the next support levels

CHFJPY: Price Outlook Following CPI Data

The Swiss Franc faces challenges as the Swiss National Bank (SNB) is now expected to cut interest rates by 50 basis points after recent inflation data showed continued weakness. In November, Swiss inflation remained flat at -0.1% month-on-month, the same as in October, while the annual rate rose slightly to 0.7%, still below expectations of 0.8%. This low inflation allows the SNB to lower interest rates further to support the economy.

Experts believe that Switzerland's economy is underperforming, with sluggish growth in its export sector and low capacity utilization. Economists like Dr. Karsten Junius from Bank J. Safra Sarasin suggest that the SNB must cut rates decisively to counter these economic pressures. The bank predicts a 50 basis point rate cut in December, followed by two more in 2025 to bring rates to 0%.

Although negative interest rates are not currently on the table, SNB President Schlegel has warned they can't be ruled out. Economists also suggest the SNB intervene in foreign exchange markets to weaken the Swiss Franc and prevent further deflation if needed. The Franc is struggling against major global currencies amid a challenging economic backdrop.

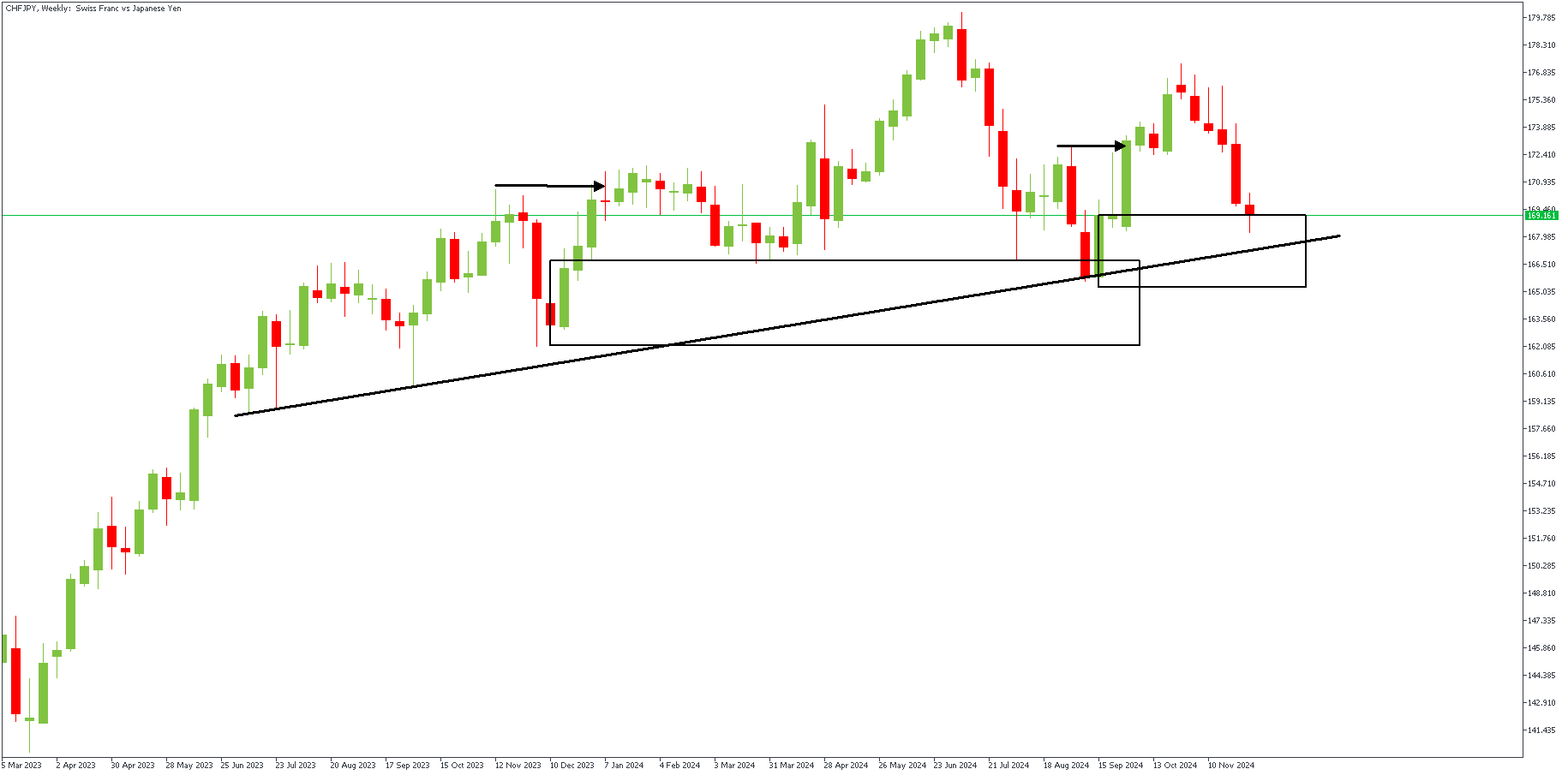

CHFJPY – W1 Timeframe

The weekly timeframe chart of CHFJPY shows a clear trendline support that the price is reaching. In addition, there is also a drop-base-rally demand zone that falls right within the 76% Fibonacci retracement region and aligns perfectly with the trendline support. Based on this, a long-term bullish sentiment can be established; however, let's confirm this further on the daily timeframe.

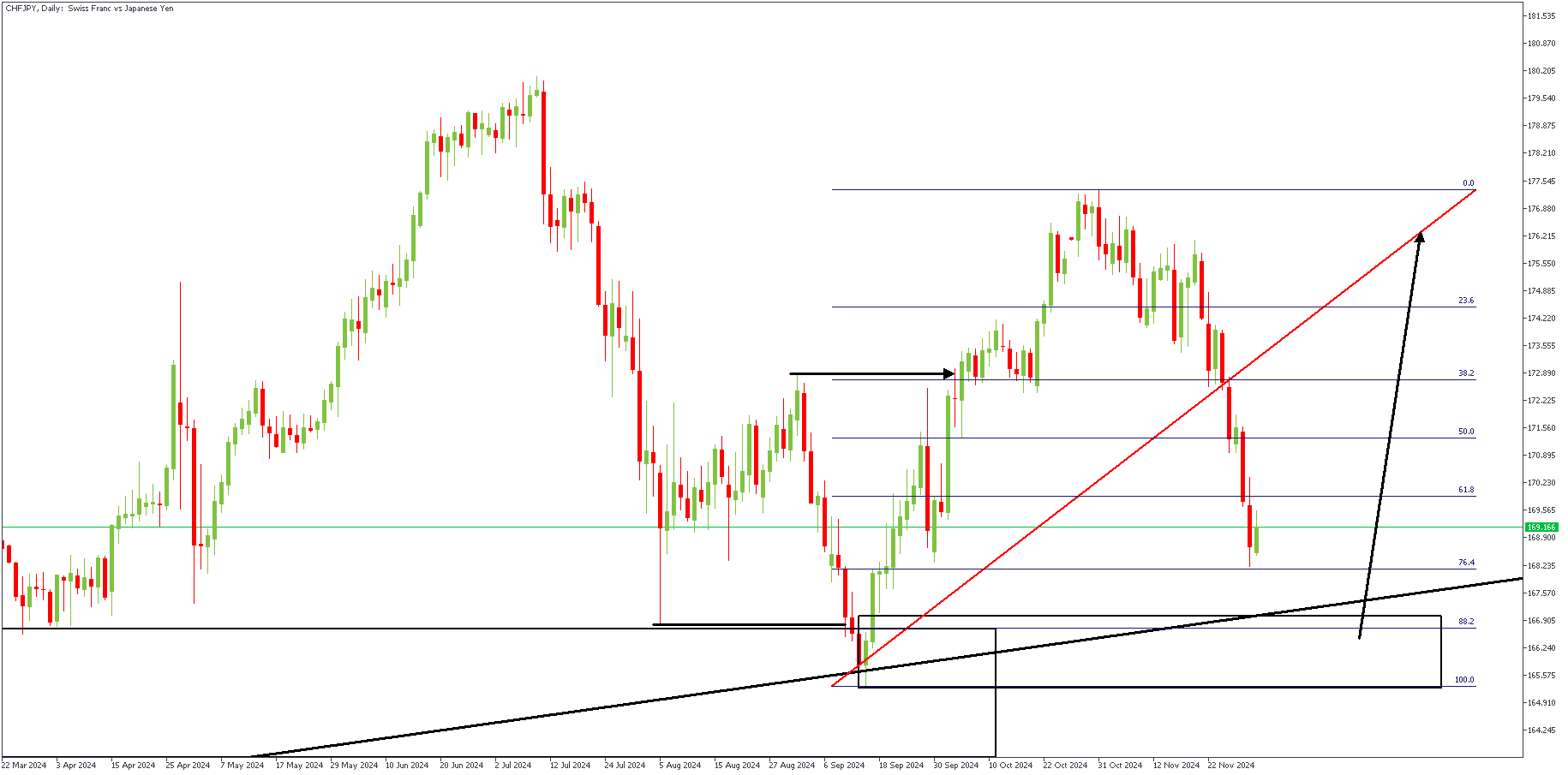

D1 Timeframe

On the daily timeframe chart, we see an SBR (Swing-Break-Retest) pattern being formed, with the demand zone falling right on top of the 88% Fibonacci retracement level. This seems a clear indication of a likely reaction from the highlighted demand and a possible entry for the bulls.

Analyst's Expectations:

- Direction: Bullish

- Target: 176.801

- Invalidation: 164.709

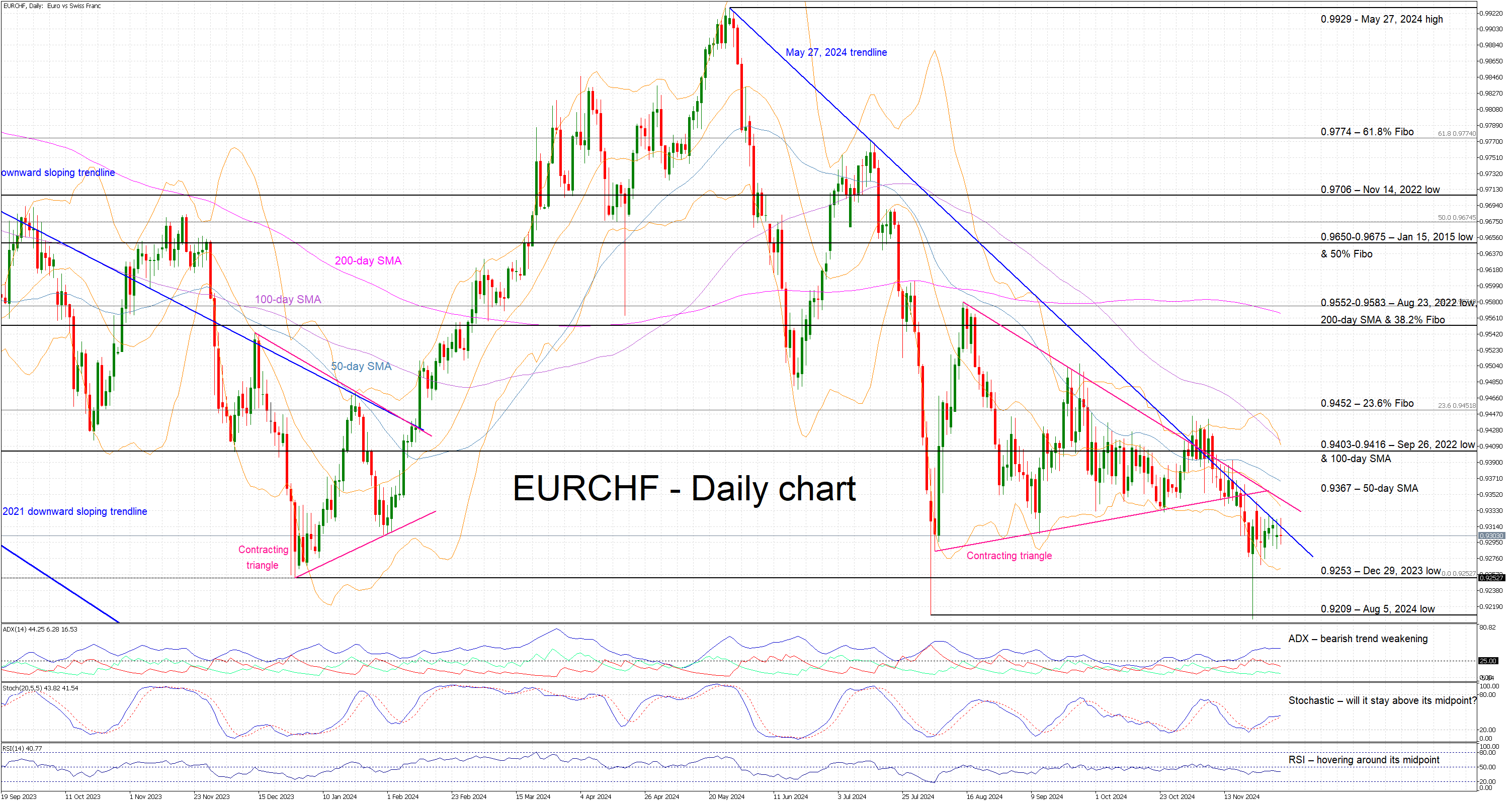

EURCHF Bulls Troubled by a Key Trendline

- EURCHF trades in a rather tight range

- The medium-term bearish trend remains valid

- Momentum indicators support the bearish trend

EURCHF is trading sideways today, testing once again the resistance set by the May 27, 2024 downward slopping trendline. EURCHF quickly rebounded from the November 22 low of 0.9204, but the bulls have failed to record another sizeable upleg. As a result, this pair has been trading in a very tight range over the past few sessions, despite the eurozone newsflow being extremely negative, both in terms of economic data and political developments.

This reduced volatility is reflected in the momentum indicators. In more detail, the Average Directional Movement Index (ADX) is moving sideways above its midpoint, and thus pointing to a weakening bearish trend in EURCHF. Additionally, the RSI continues to aimlessly hover below its midpoint, showing little appetite for a more forceful move lower. More importantly, the stochastic oscillator is preparing to test the support set by its moving average (MA). A bounce higher could reveal a buildup of bullish pressure in EURCHF, while a downwards break could open the door to another downleg in EURCHF.

If the bears remain confident, they could try to keep EURCHF below the May 27, 2024 trendline and then gradually push it towards the December 29, 2023 low at 0.9253. If successful, they could have the chance to retest the support set by the August 5, 2024 low at 0.9209 and record a new all-time low.

On the flip side, the bulls are craving a decent rally with the first obstacle being the May 27, 2024 trendline. If they manage to overcome both this trendline and the 50-day simple moving average (SMA) positioned at 0.9367, the next strong resistance could come at the 0.9430-0.9416 area. This region is populated by the 100-day SMA and the September 26, 2022 low, and a move above it could validate the bullish breakout.

To sum up, despite the negative eurozone newsflow, EURCHF bulls remain confident about staging an upleg, provided they manage to overcome a key trendline.

Sunset Market Commentary

Markets

A typical in-between trading day ahead of major eco releases and central bank speeches got shaken up by news coming from South Korea. SK president Yoon declared an emergency martial law during a televised address. Yoon of the conservative People Power Party accuses the opposition – which is in control of the 300-member parliament since 2022 – of paralyzing the government with impeachment moves and sympathizing with North Korea. Yoon vowed to “eradicate pro-North Korean forces and protect the constitutional order.” The surprise decision came amid a near-constant political standoff with the opposition, amongst others over next year’s budget bill. It’s the first time a president declared martial law since the military dictatorship ended in the late 1980s. As South Korean politics take a turn for the worse, so does the currency. USD/KRW surges to 1422, nearing the post-pandemic and 13-yr highs of <1450. US Treasuries reversed earlier minor losses. Safe haven flows push yields between 0.7-2.9 bps lower, the front outperforming. Gold eked out some gains as well as the news broke out, rising to $2653/ounce. Bunds underperform Treasuries, holding on to most of the earlier losses. Yields rise between 0.6 and 3.7 bps, underperforming against swap as well. The dust settled for now for French OATs ahead of tomorrow’s vote on a motion of no confidence. French yields lose a few bps at all tenors but the short-term ones. Spreads vs Bunds and swap ease as well after hitting new 12-year highs yesterday. There are only little traces of the breaking news on currency markets outside SK. The Swiss franc rose marginally. With EUR/CHF at key levels around 0.93, markets are wary to push the CHF even further and provoke the Swiss National Bank into interventions. Yen gains are a bit bigger, especially against an overall weakish US dollar. USD/JPY drops to 148.8. US equity futures turned red with the tech-heavy Nasdaq leading the way down. Calm already returned by the cash open though, with major indices more or less trading flat.

News & Views

Swiss headline inflation declined 0.1% M/M, slightly raising the Y/Y measure from 0.6% to 0.7%, the Swiss Statistical Office reported. Core inflation (ex fresh and seasonal products and energy & fuel) was unchanged on the month. The Y/Y figure also rose slightly to 0.9% from 0.8%. The 0.1% decrease compared with the previous month is due to several factors including lower prices for hotels and international package holidays. Prices also decreased for new cars and fruiting vegetables. Housing rentals and air transport recorded a price increase. The Swiss National Bank sees price stability as inflation holding with the 0.0%-2.0% target range. Markets after today’s CPI release see a sightly higher chance on a 50 bps rate cut at next week’s meeting compared to 25 bps cut as was the case at the previous three meetings (policy rate currently 1.0%). Poor growth domestically and at some of its major trading partners, inflation holding in the lower part of the SNB target range and a strong franc recently caused the SNB head Martin Schlegel not to exclude the use of negative interest rates and FX interventions if necessary to maintain price stability. The Swiss Franc didn’t react much today with EUR/CHF holding near 0.93.

Turkish Statistical Office data showed that inflation in the country declined less than hope for in November. Monthly headline inflation rose 2.24% M/M and 47.09% Y/Y (was 2.88% M/M and 48.58 Y/Y in October) but consensus expected a more pronounced decline to 46.6%. Core inflation showed a similar dynamics easing from 47.75% to 47.13%. Food and non-alcoholic beverages showed the biggest rise (5.1% M/M). In its November 28 policy statement, the central bank (CBRT) guided that ‘The tight monetary stance will be maintained until a significant and sustained decline in the underlying trend of monthly inflation is observed, and inflation expectations converge to the projected forecast range. Accordingly, the level of the policy rate will be determined in a way to ensure the tightness required by the projected disinflation path, taking into account both realized and expected inflation.’ This was seen as potentially opening the door for a December rate cut in case of an ongoing favourable inflation developments. However as food prices, which are basically out of reach of monetary policy, are the main driver for the ‘upward’ surprise, the debate on a guarded rate cut at the December 26 policy meeting probably remains open. The lira today declined slightly further against the dollar trading at a record low USD/TRY 34.75.

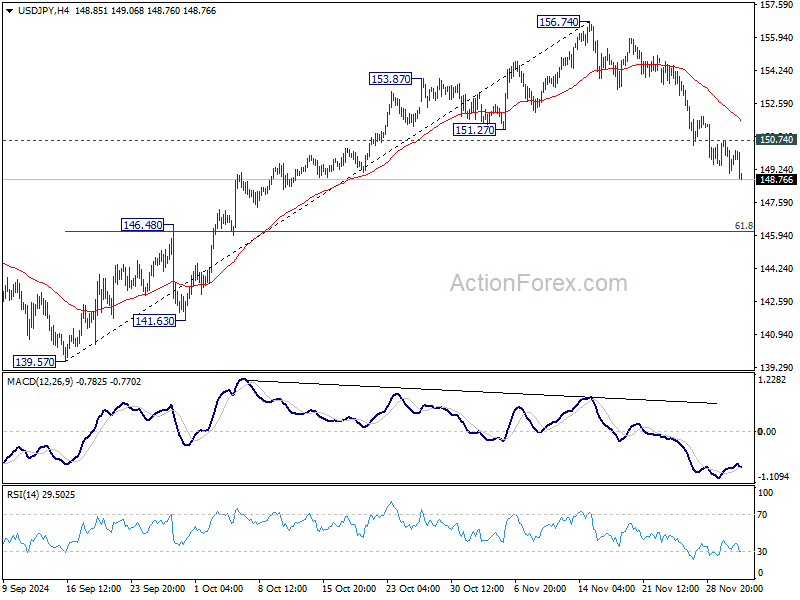

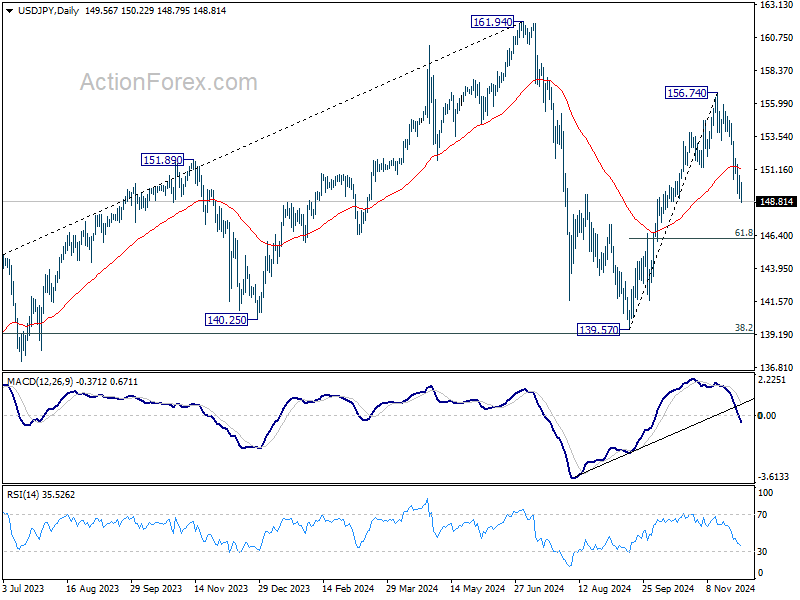

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.86; (P) 149.81; (R1) 150.53; More...

Intraday bias in USD/JPY stays on the downside as fall from 156.74 continues today. Current development suggests that whole rise from 139.57 could have finished at 156.74 already. Deeper fall should be seen to 61.8% retracement of 139.57 to 156.74 at 146.12 next. On the upside, above 150.74 minor resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0448; (P) 1.0511; (R1) 1.0560; More...

Range trading continues in EUR/USD and intraday bias remains neutral. Outlook stays bearish with 1.0609 resistance intact. On the downside, break of 1.0330 will resume the fall from 1.1213. Also, sustained trading below 1.0404 key fibonacci level will carry larger bearish implication. Nevertheless, firm break of 1.0609 will confirm short term bottoming, and turn bias back to the upside for 1.0760 support turned resistance first.

In the bigger picture, immediate focus is now on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2599; (P) 1.2671; (R1) 1.2724; More...

Intraday bias in GBP/USD remains neutral for the moment. While another rise cannot be ruled out, outlook will stay bearish as long as 55 D EMA (now at 1.2858) holds. Below 1.2615 minor support will turn intraday bias back to the downside for retesting 1.2486. Break there will resume whole fall from 1.3433.

In the bigger picture, a medium term top should be in place at 1.3433, and price actions from there are correcting whole up trend from 1.0351 (2022 low). Deeper decline is now expected as long as 55 D EMA (now at 1.2867) holds, to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

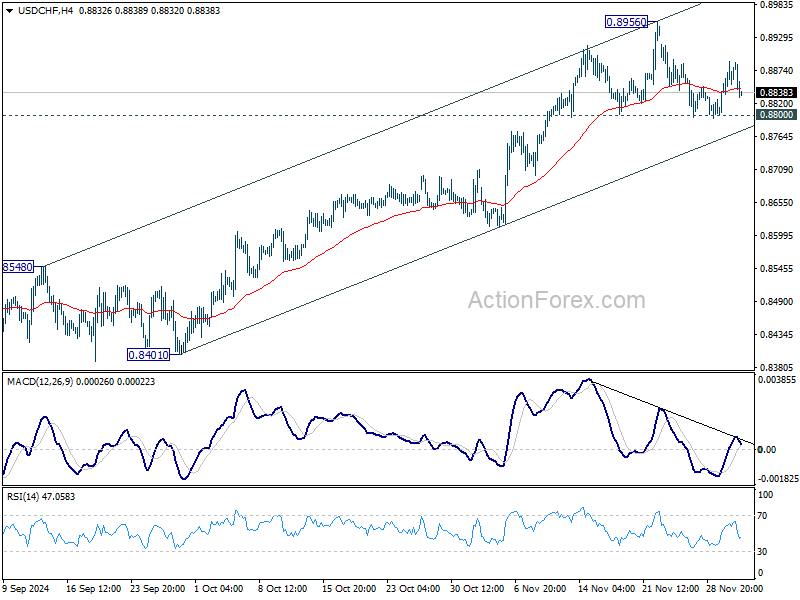

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8814; (P) 0.8852; (R1) 0.8903; More…

USD/CHF dips notably today but stays in established range below 0.8956. Intraday bias remains neutral at this point. With 0.8800 support intact, further rally is still in favor. On the upside, break of 0.8956 will resume the rally from 0.8374, and target 0.9223 key resistance next. However, firm break of 0.8800 will confirm short term topping and turn bias back to the downside for 55 D EMA (now at 0.8731).

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

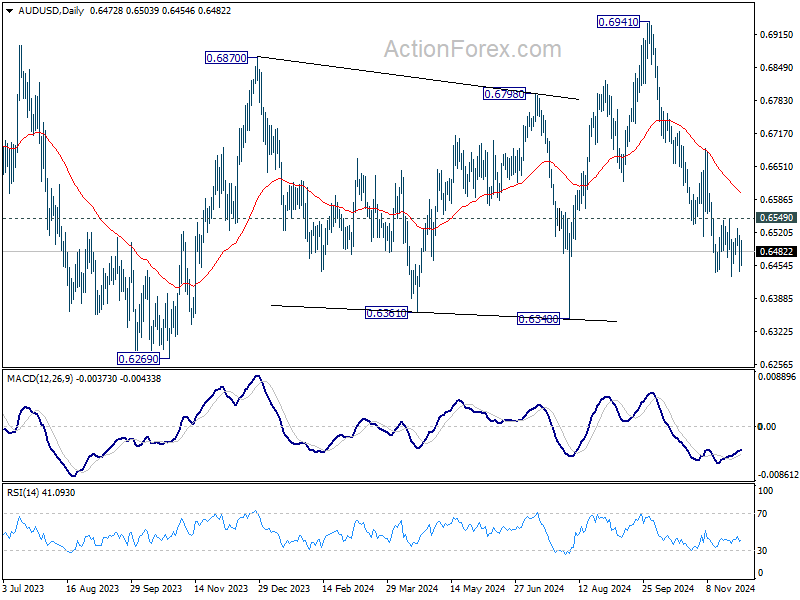

Swiss Franc Rises on Inflation Stabilization, Aussie Eyes GDP Data

Swiss Franc strengthened broadly after inflation data for November indicated a modest uptick, stabilizing after months of decline. Although the annual CPI reading missed market expectations, the stabilization reduces immediate pressure on SNB to implement a significant 50bps rate cut at its upcoming policy meeting this month.

However, uncertainty still lingers as SNB faces the challenge of balancing its decision against ECB's rate cut on the same day. A 50bps cut from ECB could drive upward pressure on the Franc, heightening deflationary risks for Switzerland and complicating SNB’s policy considerations.

Meanwhile, Dollar and Yen, which have led currency markets this week, are retracing some gains. Traders are awaiting US JOLTs job openings data later today for potential short-term volatility. However, the focus remains on Friday’s non-farm payrolls report, a high-stakes release that could set the tone for broader market movements across stocks, bonds, and currencies.

For the week so far, Yen is now the strongest performer, trailed closely by Dollar and and then Loonie. Sterling has displaced Euro as weakest currency, with Kiwi following in third-worst position. Swiss Franc and Aussie are holding middle positions.

Australia’s Q3 GDP report in the upcoming Asia session will be a focal point for the market. Growth is expected to accelerate to 0.5% qoq. A robust reading could bolster the case for RBA to hold off on rate cuts, supporting the Aussie in the process.

Technically, AUD/USD is staying in consolidations above 0.6433. Near term outlook remains bearish with 0.6549 resistance intact. Firm break of 0.6433 will resume the whole decline from 0.6941 to 0.6438 support next. However, firm break of 0.6549 will confirm short term bottoming, and bring stronger rebound back to 55 D EMA (now at 0.6597) and possibly above.

In Europe, at the time of writing, FTSE is up 0.89%. DAX is up 0.29%. CAC is up 0.53%. UK 10-year yield is down -0.0118 at 4.204. Germany 10-year yield is up 0.0009 at 2.037. Earlier in Asia, Nikkei rose 1.91%. Hong Kong HSI rose 1.00%. China Shanghai SSE rose 0.44%. Singapore Strait Times rose 0.93%. Japan 10-year JGB yield rose 0.0036 to 1.081.

ECB’s Cipollone: US tariffs likely to weaken both Eurozone growth and inflation

ECB Executive Board Member Piero Cipollone highlighted the potential economic implications of US tariffs on the Eurozone, emphasizing their dual impact on growth and inflation.

Cipollone noted that tariffs would weaken the Eurozone economy by reducing consumption, thereby lowering pressure on prices.

He pointed out that Chinese producers, excluded from the US market, might redirect their goods to Europe, potentially offering them at discounted prices.

On energy, Cipollone pointed out that while oil imports could become more expensive due to a stronger Dollar, US policies aimed at supporting domestic energy production could increase supply, offsetting price pressures.

"All this put together makes me think that we will have a reduction in growth but also a reduction in inflation," Cipollone concluded.

Swiss CPI stabilizes in Nov, but remains subdued at 0.7% yoy

Switzerland’s inflation data for November showed CPI falling -0.1% mom, matching expectations and mirroring October’s pace. Core CPI, which excludes volatile items like fresh and seasonal products, energy, and fuel, was flat on a monthly basis. Price movements showed domestic products falling -0.1% mom, while imported product prices dropped -0.4% mom.

On an annual basis, CPI edged up slightly from 0.6% yoy to 0.7% yoy, stabilizing after a downward trend since May, but falling short of market expectations of 0.8% yoy. Core CPI also rose modestly from 0.8% yoy to 0.9% yoy. Domestic product prices saw a slight decline from 1.8% yoy to 1.7% yoy, while imported product prices recovered somewhat, rising from -3.1% yoy to -2.3% yoy.

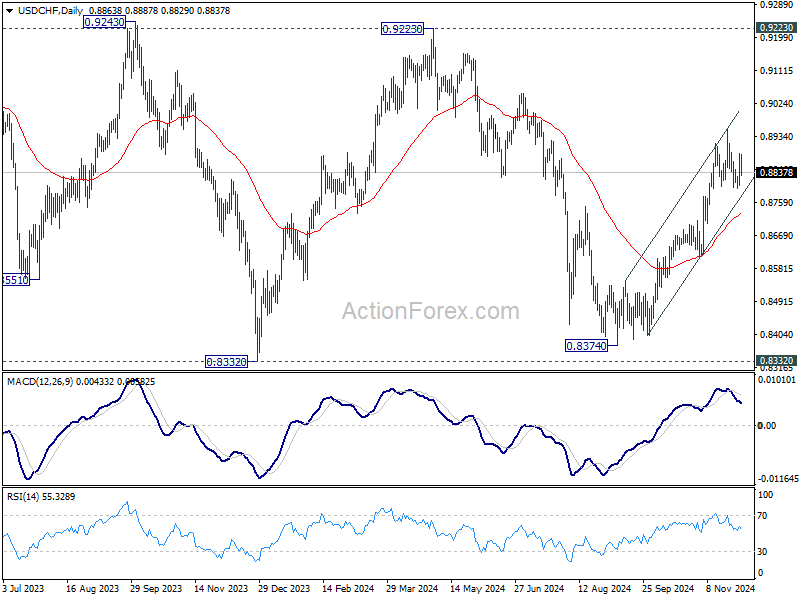

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8814; (P) 0.8852; (R1) 0.8903; More…

USD/CHF dips notably today but stays in established range below 0.8956. Intraday bias remains neutral at this point. With 0.8800 support intact, further rally is still in favor. On the upside, break of 0.8956 will resume the rally from 0.8374, and target 0.9223 key resistance next. However, firm break of 0.8800 will confirm short term topping and turn bias back to the downside for 55 D EMA (now at 0.8731).

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

OPEC+ Meeting in Focus: Will Oil Production Cuts Continue Through March 2025?

- Oil prices are currently stable, but OPEC+ is likely to extend oil output cuts into Q1 2025 due to weaker global demand.

- China’s oil demand may have peaked due to a decline in transport fuel demand and the rise of electric vehicles.

- Upcoming API and EIA oil inventory data releases will provide insights into U.S. crude supply levels and influence oil prices.

Oil prices are holding steady near the $72.35 support level, staying in a 6-day period of little movement. OPEC+ meets on Thursday, and there’s a higher chance they will extend their oil output cuts to Q1 2025.

OPEC + to Consider Oil Cut Rollover

OPEC+, which produces about half of the world’s oil, has been planning to slowly increase production until 2025. But weaker global demand and more oil being produced outside the group have created challenges and pushed prices down.

One source told Reuters that the group will likely extend output cuts into the first quarter, though all sources chose to stay anonymous.

Oil prices have remained pressurized for large parts of this year with support arriving as a result of geopolitical concerns rather than demand optimism.

OPEC+ is limiting oil production by 5.86 million barrels a day, which is about 5.7% of global demand, as part of steps agreed on since 2022 to keep the market stable. They had planned a small increase of 180,000 barrels a day in January, but this plan has been delayed because oil prices have dropped.

The question is how much longer will this go on given that the Oil demand outlook for 2025 does not look that appealing at present. With the US likely to increase output under a Trump Presidency, 2025 looks as if it will be an intriguing one.

Has Chinese Oil Demand Peaked?

According to an IEA China Researcher, Oil product demand excluding petrochemical feedstocks peaked in 2023. Crude imports are also projected to peak next year as concerns have grown this year largely on the back of poor performance by the real estate sector.

Another reason cited is that a decline in transport fuel demand may add to oil demand woes. There is concern that these developments could end the country’s decade-long run as the dominant driver of expanding oil consumption globally.

The growing adoption of EV vehicles in China has also accelerated the concerns and is likely to lead to demand plateauing next year. The rise in EV adoption has led to a situation where the petrochemical sector will be the main sector to underpin demand moving forward.

All in all consensus appears to be growing that Chinese crude imports have or will peak in the next year or so. Although Jet Fuel demand is expected to rise it is not enough to offset the declines in other areas.

Crude Oil Net Imports in MLN T (China)

Source: LSEG

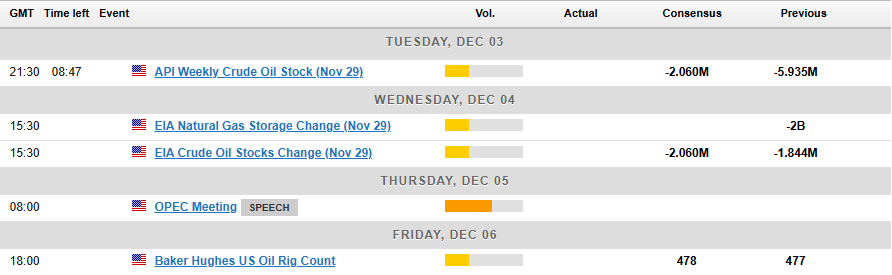

Oil Inventory Data Ahead

The upcoming API and EIA oil inventory data releases on December 3 and 4, will provide critical insights into U.S. crude supply levels, helping traders and analysts gauge the balance between supply and demand.

If the data reveals a larger-than-expected inventory build, it may signal weaker demand or oversupply, likely putting downward pressure on oil prices. Conversely, a substantial draw in inventories could highlight tighter supply conditions and potentially trigger a price rally.

Either way the bigger question on my mind is whether either move will be sustainable.

Technical Analysis

From a technical perspective, Oil has been rangebound for the last six trading days as bulls try to push price toward the recent swing high at 75.00.

At the time of writing Oil is up around 1.44% on the day and this could in part be down to rumors around a 3 month extension by OPEC + to production cuts. However, this delay was largely expected and unless we get a daily candle close above the 73.00 handle there is still a possibility of intraday pullback.

This is just based on recent history with Crude prices testing the 73.00 handle over the last two trading days being met by significant bearish pressure. Will today prove to be different?

Immediate resistance rests around the 75.00 handle before the 76.35 resistance zone comes into focus where we also have the 100-day MA.

Alternatively, a push lower from current prices will have to navigate support around the 72.38 handle, before the 71.00 handle becomes an area of focus.

Brent Crude Oil Daily Chart, December 3, 2024

Source: TradingView (click to enlarge)

Support

- 72.38

- 71.00

- 70.00 (key area of confluence)

Resistance

- 75.00

- 76.35

- 76.83