Sample Category Title

AUDUSD on Front Foot

The pair is on front foot in early Wednesday's trading and eyeing 0.7600 barrier, after previous day's weakness was contained by rising 55SMA at 0.7538.

This keeps strong support zone between 0.7532 and 0.7502, defined by 200 / 100 SMA's, out of rech or now.

Rising daily cloud continues to underpin (cloud top lies at 0.7527 today), with bullish signal generated on break above daily Tenkan-sen (0.7560).

Recovery rally is testing pivot at 0.7584 (Fibo 38.2% of 0.7739/0.7489 downleg) break of which will open next trigger at 0.7514 (daily Kijun-sen).

Sustained break here is needed to signal higher low at 0.7489 and open way for further retracement of 0.7739/0.7489 correction.

Res: 0.7600; 0.7614; 0.7643; 0.7700

Sup: 0.7560; 0.7545; 0.7532; 0.7494

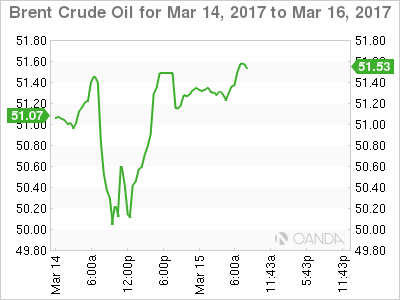

Oil Price off 3-Month Low; Weekly Inventories in Focus

Oil price bounced to $48.85 per barrel on Wednesday and hit the highest level since last Friday, after spiking to three-month low at $47.08 on Tuesday.

Rally was backed by surprise fall in US inventories in API report, released on Tuesday.

Double-Doji in past two days, with Tuesday's candle with very long tail, signal strong indecision and downside rejection after the price fell below $50 per barrel last week.

Investors are eyeing today's release of EIA crude inventories, which is showing forecast for 3.3 million barrels build in the week behind us, well below previous week's shock on 8.2 million barrels build.

Two long-tailed candles are underpinning, however, the price needs clear break above initial barrier at $48.71 (200SMA) to generate stronger signal for retest of breakpoint at $50.00 (daily cloud base / near Fibo 38.2% of $55.01/$47.08 fall).

Initial reversal signal is generating as daily RSI/slow stochastic are emerging from oversold territory.

Alternative scenario sees repeated close below 200SMA as signal of extended consolidation before broader bears resume.

Res: 48.71; 50.00; 50.70; 51.05

Sup: 48.31; 47.90; 47.08; 45.27

DAX – Steady as Markets Eye Dutch Vote, Fed Meeting

The DAX Index continues to hug the 12,000 level this week. In the Wednesday session, the DAX is at 11,989.50. On the release front, Eurozone Employment Change edged up to 0.3%, above the forecast of 0.2%. In the US, today's highlight is the Federal Reserve policy meeting, with the central bank widely expected to raise the benchmark rate a quarter-point, from 0.50% to 0.75%. On Thursday, the eurozone releases Final CPI, with the markets expecting the index to improve to 2.0%.

German numbers were a mixed bag on Tuesday. There was further indication that inflation continues to improve, as Final CPI rebounded with a gain of 0.6%, compared to a 0.6% decline a month earlier. The well-respected ZEW Economic Sentiment report improved to 1.28, although the markets had expected a stronger reading. Eurozone ZEW Economic Sentiment climbed to 25.6, its strongest gain since December 2015.

The eurozone continues to post improved inflation and growth data, and this has led to calls in some quarters for the ECB to tighten monetary policy. The ECB has kept the benchmark rate at a flat 0.0%, and its asset-purchase program does not expire until December. Will ECB President Mario Draghi taper the monthly purchases or at least signal such an intent? Draghi is doing his best to perform a complicated balancing act. A stronger economy would favor tighter policy, but he does not want ECB to become entangled in heated political contests in Europe. Dutch voters are having their say on Wednesday, while France holds elections in April, followed by Germany in September.

More job numbers out of the US, more good news for the economy. Nonfarm payrolls sparkled in February, as the indicator jumped to 235 thousand, easily beating the estimate of 196 thousand. The excellent NFP report makes it a virtual certainty that the Fed will raise rates by a quarter-point on Wednesday. Although a rate hike has been priced in by the markets at 93%, there have been disappointments in the past, so a rate move will likely give the dollar a boost against its major rivals, such as the euro. The solid job numbers also give President Trump a much-needed boost. Trump is under pressure to present an economic agenda, but the markets won't mind giving him some additional breathing room with the economy performing well.

Fed to Walk the Talk

Wednesday March 15: Five things the markets are talking about

Volatility is rising this week, with the VIX stateside jumping the most in four-weeks yesterday.

In Europe, elections remain a wild card for investors. Today's vote in the Netherlands will deliver a reading on the state of "populism" in the region as races in France and Germany begin to heat up.

In the U.S, investors have the Fed rate decision and economic projections to contend with (2pm EDT). The 100% implied probability means that, similar to Draghi's press conference last week, the tone of chair Yellen's press conference and forward guidance will decide if today decisions are a snooze fest or whether the 'mighty' USD and bond yields pivot away to higher or lower levels.

Down-under, there is the Aussie jobs report and the Bank of Japan (BoJ) rate announcement to open the Australasian sessions.

1. Global stocks mark time, wait for Fed decision

After a strong start to the week, Asian share prices consolidated in the overnight session, preferring to seek guidance from today's Fed rate announcement.

In Japan, the Nikkei share average (-0.2%) was dragged down by a firmer yen (¥114.60) along with the broader Topix (-0.2%).

In Hong Kong with investors also focusing on today's Fed dot-plot, the Hang Sang was on the back foot, retreating -0.2%. Sector performance were mixed, with energy shares leading the decline as lower oil prices dragged down the sector, while property stocks continued to outperform.

In China, stocks were roughly flat, with investors awaiting cues for direction as they closely monitored Premier Li Keqiang's press conference at the end of China's annual parliamentary meeting.

In Europe, equity indices are trading higher as market participants await results of today's Dutch election as well as the Fed's policy decision. Banking stocks are leading the gains on the Eurostoxx, while energy, commodity and mining stocks are trading higher on the FTSE 100.

U.S stocks are set to open in the black (+0.2%).

Indices: Stoxx50 +0.4% at 3,411, FTSE +0.3% at 7,378, DAX +0.1% at 12,004, CAC-40 +0.2% at 4,985, IBEX-35 +0.7% at 9,970, FTSE MIB +0.7% at 19,667, SMI +0.2% at 8,680, S&P 500 Futures +0.2%

2. Oil prices jump after surprise U.S. stock draw, gold higher

Oil prices have rebounded from yesterday's three-month lows after U.S industry data last night showed a surprise drawdown in crude stockpiles.

Ahead of the U.S open, Brent futures are up +71c, or +1.4%, at +$51.63, after settling down -43c at +$50.92 on Tuesday, their lowest close since November. U.S. West Texas Intermediate crude is trading up +81c, or +1.7%, at +$48.53 a barrel - the contract fell for a seventh consecutive session yesterday, its longest losing streak in 14- months.

API data yesterday revealed that U.S. crude stocks fell by -531k barrels last week. Market expectations were looking for an increase of +3.7m barrels. If the drawdown is confirmed today by the DoE it would be the first after nine consecutive builds.

Oil started the week under pressure after OPEC reported a rise in global crude stocks and a surprise output jump from its biggest member, Saudi Arabia.

Note: OPEC's monthly report indicated that oil stocks in industrialized nations rose in January to +278m barrels above the five-year average, with U.S. shale and other non-OPEC supply gaining.

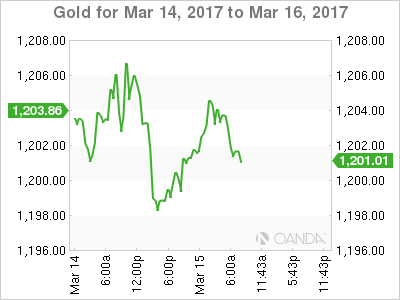

Gold prices (+0.4% to +$1,203.31 per ounce) have edged up this morning on safe-haven buying due to uncertainty over the outcome of today's Dutch elections.

Also, the market is waiting for clues on the pace of U.S interest rate hikes this year. With an immediate rate increase by the Fed as a done deal, the market is focusing on what message the Fed chair Yellen will deliver.

Note: In December, the Fed forecast three-rate rises this year.

3. Fed Hike 100% priced in

The argument for a +25bps hike by the Fed was bolstered yesterday, by a stronger-than-expected U.S PPI headline print (+0.3% vs. +0.1% m/m). Fed funds have priced in +100% probability for a hike today. Expect the market to be focusing on any hints of a change in the number of increases the Fed foresees this year in its dot-plot survey (in December the consensus was for three-rate hikes).

Ahead of the open, the yield on U.S 10's fell -1bps to +2.59%, after slipping -3bps on Tuesday. The equivalent Aussie rate was little changed at +2.92%.

This evening, the Bank of Japan (BoJ) is expected to keep its rates and yield-curve policy unchanged in its policy decision. On Thursday, the Bank of England (BoE), Swiss National Bank and Bank Indonesia are also expected to stand pat with their own policy decisions.

4. Dollar consolidates ahead of FOMC

It's not a surprise to see the mighty dollar lose some traction ahead of today's expected Fed rate hike.

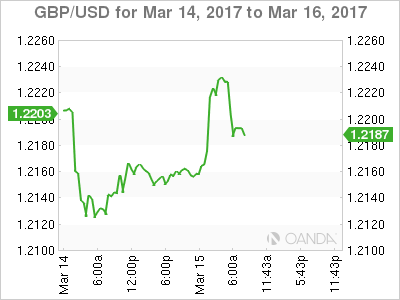

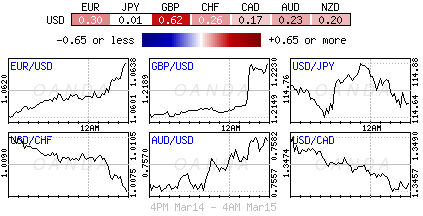

The pound (£1.2193) has trimmed some of its overnight gains after data showed U.K wage inflation slowed sharply (see below). The pair had managed to move off yesterday's seven-week low to print a one-week high earlier this morning (£1.2231). EUR/GBP trades at €0.8711, compared with around €0.8698 beforehand, still leaving the pound around +0.2% firmer on the day.

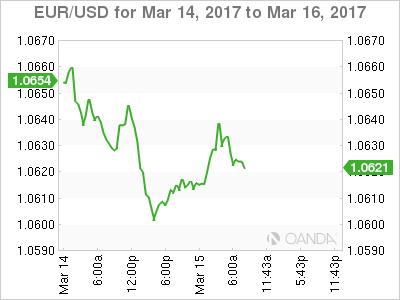

The EUR is slightly higher outright in quiet trade (€1.0630), while USD/JPY is steady in the mid-¥114 neighborhood.

5. U.K unemployment rate hits four decade low

Data this morning revealed that U.K unemployment rate fell to a forty-year low in the three-months through January, while wage growth after inflation slowed sharply. This may suggest that U.K citizens maybe facing a living standard squeeze despite the robust labor market.

Unemployment in the November-January period fell by -0.1% to +4.7% - employment rose by +92k. The market was expecting no change.

Note: Rising inflation is beginning eat into "real" wage growth, a sign that consumers may rein in spending, potentially causing the economy to slow in the months ahead. Adjusted for inflation, regular wages grew by only +0.8% in the three-months through January, the slowest pace of growth in three-years.

This morning's data should dissuade the BoE from adjusting policy any time soon. Fixed income dealers expect no change to the BoE's benchmark rate tomorrow, currently at +0.25%.

Traders Cautious Ahead Of Fed Decision

- US futures boosted by commodities but caution remains;

- Is sudden hawkish stance a sign that Fed now sees four hikes this year?

- Oil rebounds as inventories fall and Saudi's reaffirm commitment to market stability;

- Dutch election could be the canary in the mine ahead of the French election;

- Sterling volatile as Sturgeon runs into referendum difficulties and jobs data highlights weaker wage growth.

Ahead of today's highly anticipated FOMC decision, US equity markets are expected to open a little higher with the rally in commodities seen supporting the indices while overall caution is likely to remain.

It's quite clear that investors have been gearing up to today's decision from the US Federal Reserve ever since the blackout period began a little over a week ago. Market expectations have been raised dramatically ahead of the meeting by a coordinated onslaught of hawkish commentary from policy makers, to the point that a rate hike is now around 94% priced in. The upside on the hike itself therefore looks very limited which means we're relying on the dot plot and Janet Yellen if we're going to see much of a strengthening in the US dollar or Treasury yields.

I do wonder whether the sudden coordination from policy makers was driven by the belief that four rate hikes will be needed this year, an outcome that is only around 22% priced in at the moment. A rate hike now and another in June would certainly leave the door open to four increases and stop the Fed falling behind the curve if the US economy does respond strongly to either Trumps stimulus plans – should they be enacted this year – or the prospect of them. If the dot plot points to four hikes then I think the dollar may have further to run, if not then we could be perfectly in buy the rumour sell the fact territory.

It's not just the Fed decision that people are focused on today, although a quick look at the markets would suggest it is the dominant event for investors. Commodities are performing very well so far today, with oil in particular buoyed by Tuesday's surprised inventory drawdown, as reported by API, and Saudi Arabia's commitment to oil market stability. The commitment came after the OPEC report showed Saudi output actually increased in February although this was brushed off as being for storage purposes. An extension of the output deal between OPEC and non-OPEC members remains in doubt but the inventory numbers and Saudi energy ministry comments have afforded oil the opportunity to stabilise. It's been quite an aggressive sell-off in oil since the start of last week and a correction is good for the market. The fact that this came as Brent crude closed in on the psychologically significant $50 is no real surprise.

There'll also be a close eye on the Netherlands over the next 24 hours, as the country heads to the polls and we get an idea of just how strong the populist vote has engulfed the eurozone after years of problems. The Dutch election is effectively the canary in the mine for investors as, while Geert Wilders – the eurosceptic far right leader – has led many polls, the fragmented nature of the Dutch parliament combined with the inability of Wilders to find any parties to join a coalition, makes it very unlikely that he will rule. That said, the trend of polls underestimating the populist vote – as we saw last year in the UK Brexit referendum and US Presidential election – would favour Wilders and should we see similar results today, it would cause great concern ahead of the French election over the next couple of months as Marine Le Pen actually stands a realistic chance of winning.

It's been a bit of a rollercoaster ride this morning for the UK, with the pound initially boosted by Nicola Sturgeons acknowledgement that Scotland would probably not seek to join the EU right away in the event of a vote for independence, instead suggesting they could follow a Norway-type model. This came as a number of polls suggested Scots would once again vote to remain, just as they did a couple of years ago. This would be a crushing defeat for Sturgeon and the SNP and it would appear a sudden change of tactics will be necessary if they're going to avoid the same outcome as before. The pound did take a hit today after UK jobs data showed that while the unemployment situation still looks good, wage growth is slowing which, coming at a time when inflation is headed in the other direction, doesn't bode well for the UK's consumer driven economy.

EUR/USD Levels To Watch Prior To FED

The US Federal Reserve Bank ('the Fed'), has battled to ignite inflation since the GFC and up until now it has raised rates less frequently than the markets have expected, however, this approach may soon change. Today, the Fed is almost universally expected to raise its benchmark interest rates following strong NFP, full employment and an uptick in inflation. The forecast is that the FED will hike the rates by 0.25 % and the event will be volatile as the FED hike might have already been priced in. We need to watch important camarilla levels and POC zones.

Traders should focus on POC and 2 possible breakout points. The major range of the pair is 1.0720-1.0495. As EUR/USD has been sold on rallies as I have shown on Session Recap webinar and Pre-NFP coverage, the current POC 1.0660-75 is still valid for short on rallies (H5, ATR top, X cross) towards 1.0570 - Daily camarilla L4 support. Breakout of L4 should target L5 and Weekly L5 camarilla levels 1.0545 and 1.0495. The only exception to the upside could be the break of 1.0720 towards 1.0765 and that could happen if the FED doesn't hike the rate today which would be a big surprise.

NZDUSD Intraday Look

NZDUSD is looking bearish still, with current bounce being a wave four that may see slightly higher price up to 0.7000 psychological level before market resumes downward move to around 0.6840.

NZDUSD, 1H

GOLD Bearish Pause, SILVER Consolidating, Crude Oil Selling Pressures Diminish Around $48.

GOLD (in USD) Bearish pause.

Gold's weakness is definitely on since the metal reached resistance given at 1263 (27/02/2017 high). Expected to reach support at 1177 (11/01/2017 low). For the time being, the metal is pausing around $1200.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

SILVER (in USD) Consolidating.

Silver's selling pressures are important. Hourly support is given at 16.63 (27/01/2016 low). Expected to see continued bearish pressures.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

Crude Oil (in USD) Selling pressures diminish around $48.

Crude oil's bearish pressures continues. The commodity has been unable to mount a serious challenge to 55.24 (03/01/2017 high) resistance. Strong support given at 49.61 (08/12/2016) has been broken. Expected to see deeper selling pressures.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 24.82 (13/11/2002) while resistance can now be found at 55.24 (03/01/2017 high).

EUR/CHF Continued Bearish Pressures, EUR/JPY Continued Increase, EUR/GBP Weakening.

EUR/CHF Continued bearish pressures.

EUR/CHF's renewed bearish pressures continues to increase. The medium-term pattern suggests us to see continued bearish pressures towards key support that can be found at 1.0623 (24/06/2016 low). Temporary surges seem the new normal for the CHF.

In the longer term, the technical structure is mixed. Resistance can be found at 1.1200 (04/02/2015 high). Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

EUR/JPY Continued increase.

EUR/JPY's demand has rejuvenated. Hourly resistance at 121.34 (10/02/2017 high) has been broken. Strong resistance is given at a distance at 123.31 (27/01/2017 high). Expected to show further increase.

In the longer term, the technical structure validates a medium-term succession of lower highs and lower lows. As a result, the resistance at 149.78 (08/12/2014 high) has likely marked the end of the rise that started in July 2012. Strong support at 94.12 (24/07/2012 low) looks nonetheless far away.

EUR/GBP Weakening.

EUR/GBP is pushing lower. Selling pressures increase around 0.8800. Key resistance is given at 0.8854 (15/01/2017 high). The road is wideopen for further weakness as there is no close support.

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level.

USD/CHF Approaching Uptrend Channel, USD/CAD Sideways Price Action, AUD/USD Short-Term Demand Is Fading

USD/CHF Approaching uptrend channel.

USD/CHF is still riding within uptrend channel and is on its way to monitor support implied by lower bound of the uptrend channel. Key resistance is given at a distance at 1.0344 (15/12/2016 high). Hourly support is given at 1.0075 (13/03/2017 low). Expected to consolidate.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/CAD Sideways price action.

USD/CAD's bullish pressures are definitely on after breaking key resistance at 1.3353 (20/01/2017 high). Yet, as long as this resistance was not broken (20/01/2017 high), bullishness was limited. Expected to see further upside potential for the pair.

In the longer term, there is a golden cross with the 50 dma crossing the 200 dma indicating further upside pressures. Strong resistance is given at 1.4690 (22/01/2016 high). Long-term support can be found at 1.2461 (16/03/2015 low).

AUD/USD Short-term demand is fading.

AUD/USD's technical structure is still negative. The road is wide-open for further weakness towards support given at 0.7494 (19/01/2017 low). Key resistance is given at 0.7778 (08/11/2016 high) while hourly resistance is given at 0.7592 (13/03/2017 high).

In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.