Sample Category Title

Forex Technical Analysis

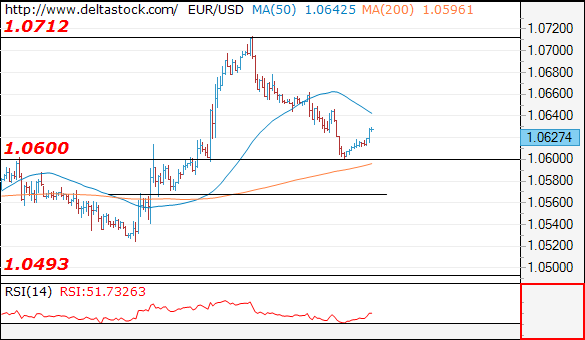

EUR/USD

Current level - 10627

The slide from 1.0712 is complete and the intraday bias is slightly positive above 1.0600, with a risk of a tight test at 1.0660 resistance. My outlook on the senior frames is bearish below 1.0660, for a break through 1.0600, towards 1.0450. Crucial on the upside is 1.0712 high.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.0660 | 1.0710 | 1.0600 | 1.0450 |

| 1.0710 | 1.0870 | 1.0493 | 1.0350 |

USD/JPY

Current level - 114.72

My outlook here is bullish above 114.50, for an upswing towards 115.70. Crucial on the downside is 114.10 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 114.95 | 118.65 | 114.10 | 114.10 |

| 115.65 | 120.00 | 114.10 | 113.37 |

GBP/USD

Current level - 1.2219

The recent reversal at 1.2107 signals a positive bias, for a violation of 1.2250, towards 1.2300 area. Key intraday support lies at 1.2170.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2250 | 1.2570 | 1.2170 | 1.2080 |

| 1.2300 | 1.2705 | 1.2000 | 1.1984 |

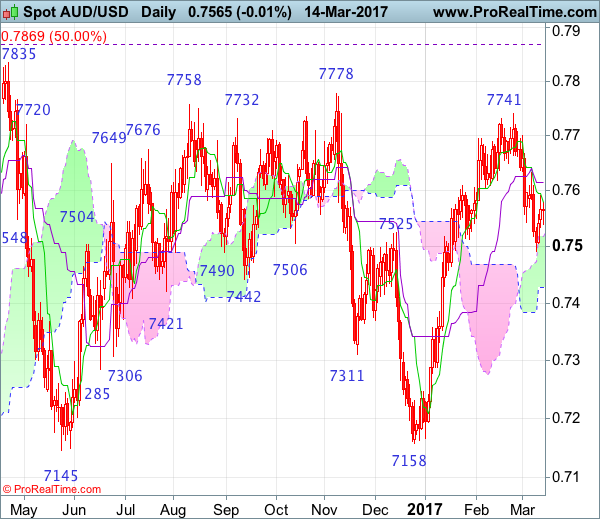

AUD/USD Candlesticks and Ichimoku Analysis

Weekly

- Last Candlesticks pattern: Shooting star

- Time of formation: 5 Sep 2016

- Trend bias: Down

Daily

- Last Candlesticks pattern: Shooting star

- Time of formation: 8 Sep 2016

- Trend bias: Down

Although aussie slipped again last week and fell to as low as 0.7491, as the pair found good support there and has rebounded, retaining our bullishness and consolidation with upside bias is seen for further gain to the Kijun-Sen (now at 0.7616), then test of resistance at 0.7633, however, a daily close above latter level is needed to signal low is formed, bring a stronger rebound to 0.7665-70. Looking ahead, only above 0.7700 would signal the pullback from 0.7741 has ended, bring retest of this level, break there would confirm recent upmove has resumed and extend gain to previous chart resistance at 0.7778, above there would retain bullishness and confirm early erratic upmove from 0.6827 (2016 low) has resumed for retest of 0.7835 (2016 high) first.

On the downside, expect pullback to be limited to 0.7540 and bring such a rebound. Below said support at 0.7491 would extend the fall from 0.7741 top for retracement of recent upmove towards the lower Kumo (now at 0.7427). Only a daily close below the lower Kumo would shift risk to the downside and signal recent rise has ended, bring weakness to 0.7390-00 and possibly towards 0.7350 but reckon 0.7300-10 would remain intact, bring rebound later.

Recommendation: Hold long entered at 0.7515 for 0.7715 with stop below 0.7490.

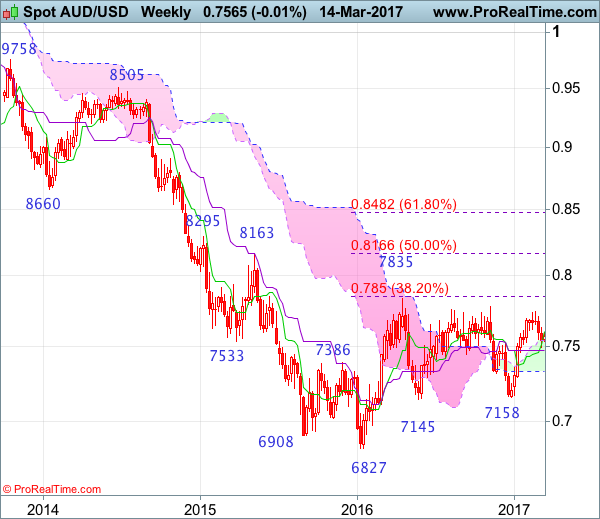

On the weekly chart, although aussie’s retreat from 0.7741 has kept price under near term pressure and further consolidation below said resistance would be seen, reckon downside would be limited to last week’s low at 0.7491 and bring rebound later, above 0.7630-35 would bring test of 0.7700 but break of said resistance at 0.7741 is needed to extend the rebound from 0.7158 towards resistance at 0.7778, however, as broad outlook remains consolidative, reckon upside would be limited and price should falter below 2016 high at 0.7835. Looking ahead, only above this level would suggest an upside break of recent established broad range has occurred, bring further subsequent rise towards 0.7900.

On the downside, assize’s downside is likely to be limited to the upper Kumo (now at 0.7540) and bring another rebound. Below said support at 0.7491 would risk test of the Kijun-Sen (now at 0.7468) but break there is needed to signal top is formed, bring weakness to 0.7400, break there would add credence to this view, bring subsequent fall to the lower Kumo (now at 0.7331), a drop below 0.7285-90 support would indicate the rebound from 0.7158 has ended and bring further decline to 0.7200-10, then towards strong support area at 0.7145-58.

German Investor Confidence Improves Less Than Expected In March

'[The fact that confidence] only shows a slight upward movement is a reflection of the current uncertainty surrounding future economic development. With regard to the economic situation in Germany, no clear conclusion can be drawn from the most recent economic signals'. - Achim Wambach, ZEW

Investor sentiment in the Euro zone's largest economy, Germany, improved markedly in March but less than analysts expected, a report released on Tuesday showed. The Mannheim-based Centre for European Economic Research (ZEW) said its German Economic Sentiment Index came in at 12.8 points for March, slightly up from the preceding month's 10.4. However, market analysts anticipated a bigger increase to 13.2 during the reported period. Data also showed the Current Conditions Index climbed to 77.3 from 76.4 points seen in February, falling behind analysts' expectations for a rise to 78.0. The ZEW President Professor Archim Wambach highlighted that risks surrounding the upcoming federal elections and the future of US foreign policy remained high, and, therefore, it was not possible to provide a clear view on the current state of the German economy. In the meantime, the Euro zone ZEW Indicator of Economic Sentiment advanced to 25.6 points in March from the prior month's 17.1, surpassing forecasts for a reading of 19.3. Furthermore, the indicator for the current economic situation in the region came in at 7.4 in March, up from February's 2.8. Any reading above the 0.0-point level reflects general investor optimism. The Euro fell against other major currencies shortly after the release.

New Zealand Reports Better-Than-Expected Current Account Deficit

'New Zealand earned $2.0 billion from investment overseas, $129 million more than in the September quarter. A large portion of this extra income was reinvested back into the overseas subsidiaries, instead of being paid out as dividends'. - Daria Kwon, Statistics New Zealand

New Zealand's current account deficit dropped markedly during the last quarter of 2016 amid stronger tourism and higher reinsurance flows into New Zealand, following the November earthquake, official figures revealed on Tuesday. Statistics New Zealand reported the country's current account deficit fell to NZ$2.34 billion in the Q4 of 2016, surpassing analysts' expectations for a NZ$2.43 billion deficit. Meanwhile, the preceding quarter's gap of NZ$4.89 billion was revised up to NZ$5.03 billion. On an annual basis, the country's deficit came in at NZ$7.112, accounting for 2.7% of GDP, following 3% in the Q3 of 2016. Analysts expected the deficit to account for 2.8% of GDP. Data also showed that the number of tourists coming to New Zealand and the amount of money they spend rose markedly. Thus, service spending climbed to a $1.2 billion surplus, $174 million up from the prior quarter. Moreover, Statistics New Zealand said that overseas reinsurance claims, submitted after the November 7.8 magnitude earthquake hit the town of Kaikoura, also boosted fund flows in the country. Analysts suggest that the better-than-expected current account deficit would be highly welcomed by the Reserve Bank of New Zealand that holds a meeting next week. However, markets do not expect the Central bank to raise its key interest rate at the upcoming meeting.

USDJPY Is Holding Within Daily Cloud Ahead Of FOMC

Tuesday's trading ended in red after repeated failure to sustain break above daily cloud. Near-term price action is holding within the cloud in directionless mode and awaiting Fed for stronger signals.

Daily Tenkan-sen that contained Tuesday's easing at 114.51, offers solid support, as Tenkan-sen / Kijun-sen lines are in bullish setup and maintain positive bias.

Daily cloud is thickening and continues to underpin, with final close above it, needed to signal stronger upside action towards next target at 115.91 (Fibo 61.8% of 118.59/111.57descend).

Conversely, increased downside risk could be expected on break below daily cloud base (114.27), while extension below daily Tenkan-sen (113.55) will signal reversal.

Res: 114.99, 115.18, 115.49, 115.91

Sup: 114.51, 114.27, 114.00, 113.55

Cable – Bounce Above 10SMA Eases Immediate Downside Pressure But Overall Bears Remain In Play

Cable bounced to 1.2250 zone on Wednesday and reversed Tuesday's losses that hit fresh multi-week low at 1.2107. Again, dips were short-lived and another failure to close below 1.2155 (Fibo 76.4%) pivot, signals strong hesitation of larger bears. However, overall picture is bearish and favors further downside, with eventual firm break below 1.2155 seen as a trigger. Meantime, today's recovery rally that improved near-term studies and probed above initial barrier at 1.2206 (falling 10SMA) signals extended consolidation. Close above 10SMA would give initial signal of basing and possible stronger correction of steep fall from 1.2538 to 1.2107. Firm break above next pivot at 1.2300 is needed to confirm scenario. UK jobs data are in immediate focus, ahead of FOMC, which is expected to give clearer direction signals.

Res: 1.2254, 1.2283, 1.2300, 1.2345

Sup: 1.2206, 1.2177, 1.2153, 1.2107

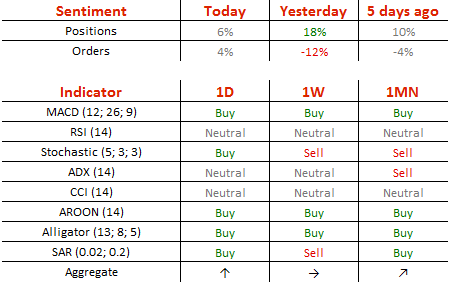

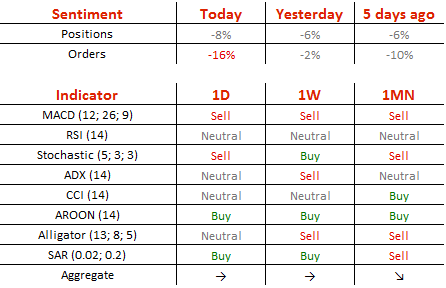

EUR/USD Near 1.06 Mark On Wednesday

'The exchange rate is more or less the result of the monetary policies and the different cyclical positions on both sides of the Atlantic.' – Jens Weidmann, Bundesbank (based on Bloomberg)

Pair's Outlook

On Wednesday morning the common European currency was squeezed in by two simple moving averages against the US Dollar just above the 1.06 level. The 20-day SMA was providing support from the downside at 1.0604 level, and the 55-day SMA was putting up resistance to the currency exchange rate at 1.0621 level. It is most likely that the support level will be passed and the rate will continue lower to the first weekly support level, which is located at the 1.0566 mark. Such a move would be consistent with the Federal Reserve announcing a rate hike later in the day.

Traders' Sentiment

SWFX trader sentiment remains bearish, as 54% of all open positions remain short. Meanwhile, 58% of trader set up orders are set to sell the Euro.

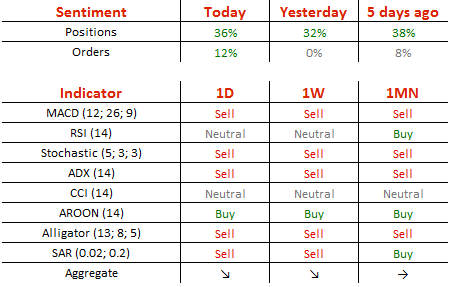

GBP/USD In Limbo Around 1.22 Ahead Of Fed Minutes

'The fact that the GBP now appears cheap is insufficient to sustain a credible recovery by the currency at this stage. We recommend selling sterling on any temporary rally triggered by a shift in market focus. We maintain our target for EUR/GBP close to 0.90 and GBP/USD well below 1.20 in Q3.' – SEB Bank (based on PoundSterlingLive)

Pair's Outlook

The GBP/USD pair was close to touching the 1.21 mark on Tuesday, the lowest level in two months; however, it was able to stabilise above the 1.2150 mark. A sharp rebound was registered earlier today, but the cause of it is USD weakness rather than GBP strength, with US Treasury yields weighing on the US currency. A lot can change after Fed's Minutes are released, which is the main market driver today. First of all, the Cable risks falling under 1.21, should the Fed deliver on a rate hike and provide insight concerning future ones this year. On the other hand, any disappointment would help the Pound regain some ground, with the 1.23 easily seen retaken.

Traders' Sentiment

Bullish traders' sentiment grew stronger, as now 68% of all open positions are long. The share of buy orders edged up from 50 to 56%.

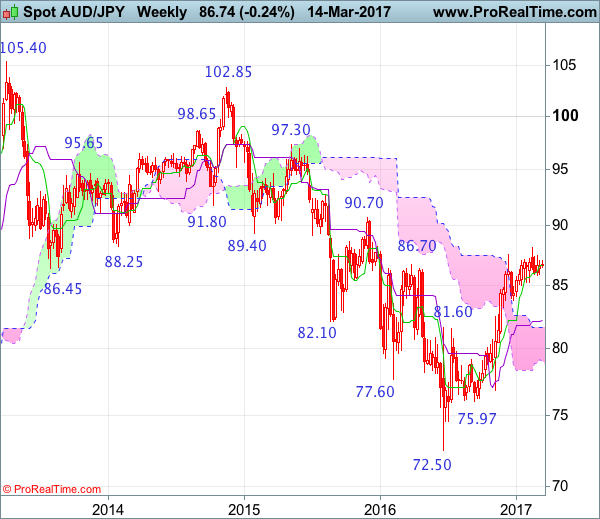

AUD/JPY Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting star

• Time of formation: 12 Dec 2016

• Trend bias: Down

Daily

• Last Candlesticks pattern: Shooting star

• Time of formation: 1 Nov 2016

• Trend bias: Up

Despite falling to 85.85 last week, as aussie found support there again and has rebounded, suggesting further consolidation above this level would be seen an recovery to 87.45-50 cannot be ruled out, however, reckon upside would be limited to 87.75 and price should falter below resistance at 88.15, bring retreat later. A break above said resistance at 88.15 would signal the erratic rise from 72.50 low has resumed for retracement of early downtrend to 89.00,, however, overbought condition should prevent sharp move beyond psychological resistance at 90.00, risk from there is seen for a retreat to take place later.

On the downside, expect pullback to be limited to 86.45-50 and price should stay well above said support at 85.85 and bring another bounce later. Only a break of said support at 85.85 would signal another leg of decline from 88.15 is underway for further fall to 85.50 and possibly towards support at 85.20, a drop below this level would provide confirmation that top has been made, bring retracement of recent upmove to 85.00, then towards 84.50-55 but support at 83.75 should remain intact and bring rebound later.

Recommendation: Would stand aside for this week.

On the weekly chart, aussie has remained confined within near term narrow range, suggesting further sideways trading would be seen and upside bias remains for recent corrective upmove from 72.50 low to resume after consolidation, break of 88.15 resistance would confirm this view and bring retracement of early downtrend to 88.50 and then 89.00-10 but reckon upside would be limited to psychological resistance at 90.00 and previous resistance at 90.70 should remain intact, risk from there is seen for a retreat to take place later.

On the downside, although initial pullback to the Tenkan-Sen (now at 86.60) cannot be ruled out, reckon downside would be limited to support at 85.85 and bring another rise. A weekly close below 85.85 would defer and bring weakness to 85.00-10, however, reckon downside would be limited to 84.10-15 and price should stay above 83.75 support. Only below indicated support at 83.75 would suggest a temporary top has been formed at 88.15 and bring test of previous support at 83.20, break there would add credence to this view, then retracement of recent rise would take place, bring further fall to 82.50 and possibly towards the Kijun-Sen (now at 82.18) which is likely to hold on first testing.

USD/JPY: Downside Risks Persist

'I think the dollar might have trouble above the 115 level today, with Japanese exporters still seeking to sell above it ahead of the end of the Japanese fiscal year this month.' – Kaneo Ogino, Global-info Co. (based on Reuters)

Pair's Outlook

Strong PPI was insufficient to cause any substantial volatility on Tuesday, but the USD/JPY pair still remained relatively unchanged for the third consecutive day. Some signs suggest the US Dollar is to strengthen again, such as the technical indicators—they are giving strong bullish signals. A possible rate hike today also suggests the Buck could post gains, however, that implies the ascending channel pattern is likely to be broken to the upside. From the technical perspective a plunge would be more probable, as that would preserve the pattern and an eventual retest of the up-trend circa 113.00, where the USD could receive sufficient momentum to pierce the two-year down-trend.

Traders' Sentiment

There are 53% of traders holding long positions (previously 59%), while only 52% of all pending orders are to acquire the Greenback.