Sample Category Title

Trade Idea Update: USD/CHF – Stand aside

USD/CHF - 1.0093

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the greenback retreated after meeting resistance at 1.0109 and mild downside bias is seen for test of 1.0060 support, however, break there is needed to signal the fall from 1.0171 top has resumed and extend weakness to 1.0035-40 but support at 1.0009 should remain intact, risk from there has increased for a rebound to take place later.

On the upside, above said resistance at 1.0109 would bring rebound to 1.0120 but break of resistance at 1.0142 is needed to signal low is formed and suggest the fall from 1.0171 has ended, bring another rise towards this level later. As near term outlook is still mixed, would be prudent to stand aside in the meantime.

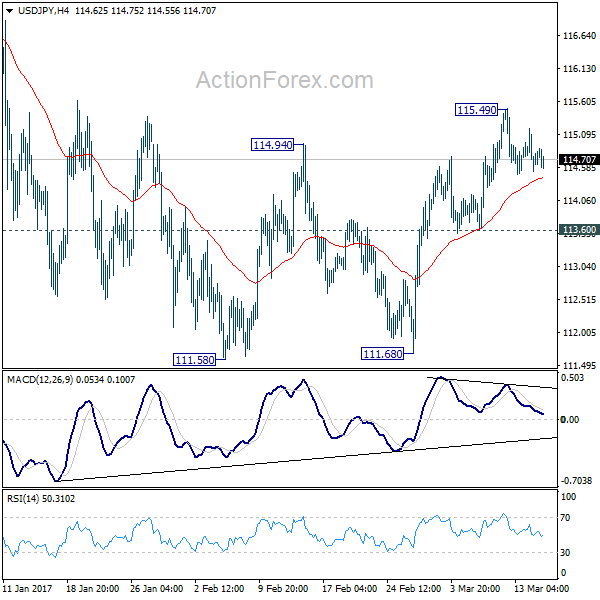

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 114.44; (P) 114.81; (R1) 115.12; More...

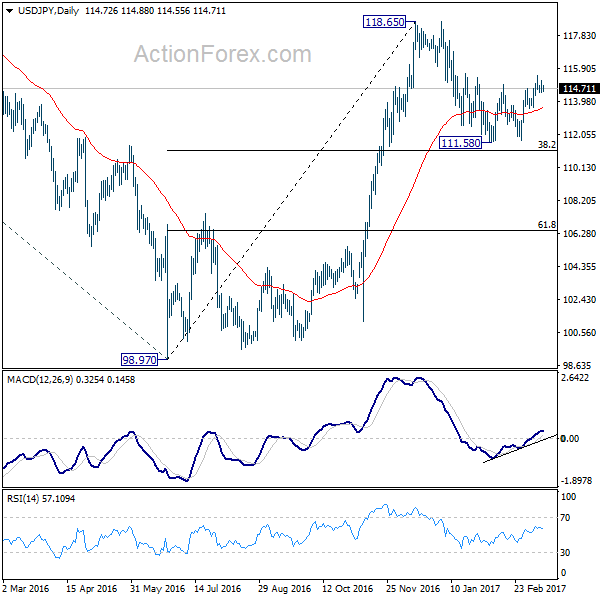

Intraday bias in USD/JPY remains neutral as the consolidation from 115.49 temporary top extends. Deeper retreat cannot be ruled out. But we'd expect strong support above 113.60 to contain downside and bring rise resumption. As noted before, corrective decline from 118.65 should have completed with a a double bottom pattern (111.58, 111.68). Above 115.49 should turn bias to the upside and pave the way for a test on 118.65. Decisive break there will extend whole rise from 98.97 and target 125.85 high next. On the downside, however, break of 113.60 will invalidate our view and turn bias back to the downside for 111.58/68 support zone instead.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Rejection from 125.85 and below will extend the consolidation with another falling leg before up trend resumption.

Trade Idea Update: GBP/USD – Buy at 1.2140

GBP/USD - 1.2202

Original strategy :

Buy at 1.2140, Target: 1.2250, Stop: 1.2105

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2140, Target: 1.2250, Stop: 1.2105

Position : -

Target : -

Stop : -

Although cable resumed recent decline and extend weakness to 1.2109 yesterday, the subsequent rebound suggests low is possibly formed there and consolidation with upside bias is seen for gain to 1.2260-65, above there would add credence to this view, bring retracement of recent decline to 1.2290-95 (50% Fibonacci retracement of 1.2479-1.2109), however, resistance at 1.2301 should limit upside and price should falter below 1.2335-40 (61.8% Fibonacci retracement), bring another decline later.

In view of this, we are looking to buy cable on dips as 1.2135-40 should limit downside. Only below said support at 1.2109 would extend recent decline to 1.2090, however, loss of downward momentum should prevent sharp fall below 1.2070 and reckon 1.2040-50 would hold from here, sterling may stage another rebound from there later.

Yen Listless Ahead of Fed, BoJ Rate Announcements

USD/JPY is almost unchanged in the Wednesday session. Currently, the pair is trading at 114.70. On the release front, Japanese Revised Industrial Production declined 0.4%, above expectations. In the US, there were no surprises from key consumer reports, as retail sales and CPI posted small gains in February. Today's highlight is the Federal Reserve policy meeting, with the central bank widely expected to raise the benchmark rate a quarter-point, from 0.50% to 0.75%. On Thursday, the US publishes a host of key indicators, led by unemployment claims.

The Bank of Japan will set its interest rate shortly after the Federal Reserve makes its announcement. Unlike the Fed meeting, the BoJ meeting will likely be a non-event, with the BoJ expected to hold pat and maintain rates at -0.10%. If, as expected, the Fed does raise rates, monetary divergence will widen and the yen could lose more ground against the US dollar. The Japanese economy has showed improvement, recording four consecutive quarters of growth. Still, analysts are not expecting the BoJ to make any changes to its ultra-loose monetary policy, as inflation levels remain well below the BoJ's target of around 2.0%.

With the markets expecting a quarter-point rate hike on Wednesday, will the currency markets react to a Fed move? Although a rate hike has been priced in by the markets at 93%, there have been disappointments in the past, so a rate move could boost the dollar at the expense of gold. Strong US employment numbers in February have reinforced market speculation that the Fed will raise rates for the first time this year. Nonfarm payrolls sparkled in February, as the indicator jumped to 235 thousand, easily beating the estimate of 196 thousand. Wage growth climbed 2.6% compared to February 2016, while the participation rate edged up to 63.0%, up from 62.9%. These solid job numbers have also provided President Trump with a much-needed boost. Trump is under pressure to present an economic agenda, but the markets won't mind giving him some additional breathing room, with the economy performing so well.

Trade Idea Update: EUR/USD – Stand aside

EUR/USD - 1.0613

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the single currency slipped to as low as 1.0600, as euro found good support there and has rebounded again, suggesting consolidation above this level would be seen and gain to 1.0660-65 cannot be ruled out, however, break there is needed to signal low is formed, bring further gain to 1.0680-85 but price should falter below this week’s high at 1.0714.

On the downside, below said support at 1.0600 would signal top has been formed at 1.0714 and downside risk remains for the fall from there to bring retracement of recent rise to 1.0570-75, then 1.0550 but reckon downside would be limited and support at 1.0525 should remain intact. As near term outlook is mixed, would be prudent to stand aside in the meantime.

Trade Idea Update: USD/JPY – Stand aside

USD/JPY - 114.66

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As the greenback met renewed selling interest at 115.20 yesterday and slipped again, retaining our view that further consolidation below last week’s high at 115.51 is in store and risk of another fall to 114.48 support cannot be ruled out, however, reckon downside would be limited to 114.26 support and as this move is viewed as retracement of recent upmove, reckon downside would be limited to 114.00-05 (38.2% Fibonacci retracement of 111.69-115.51) and price should stay well above strong support at 113.56-61), bring rebound later.

In view of this, would be prudent to stand aside for now. A firm break above 115.20 would suggest low is formed, bring a stronger rebound but still reckon said resistance at 115.51 would cap upside. Only break there would revive bullishness and extend recent upmove to previous resistance at 115.62, then towards 115.90-00.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2100; (P) 1.2161; (R1) 1.2213; More...

GBP/USD formed a temporary low again at 1.2108 and recovered. Intraday bias is turned neutral for another round of consolidation. But still, outlook stays bearish as long as 1.2346 support turned resistance holds. As noted before, consolidation pattern from 1.1946 is completed at 1.2705 is resuming larger down trend. Below 1.2108 will target a test on 1.1946/86 support zone. Break of 1.1946 will confirm our bearish view.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

Dollar Mildly Lower ahead of FOMC, Sterling Rebounds on Job Data

Dollar weakens mildly again as markets are awaiting FOMC rate decision, economic projections and press conference. Headline CPI rose 0.1% mom, 2.7% yoy in February, up from 2.5% yoy and beat expectation of 2.6% yoy. Core CPI rose 0.2% mom mom, 2.2% yoy, down from 2.3% yoy but met expectation of 2.2% yoy. Retail sales rose 0.1% in February, above expectation of -0.1%. Ex-auto sales rose 0.2% , above expectation of -0.1%. Empire state manufacturing index dropped to 16.4 in March, down from 18.7 but beat expectation of 15.0. The data are mixed to positive but markets paid little attention to them.

Fed to upgrade economic projections

Fed is widely expected to hike federal funds rate by 25bps to 0.75-1.00%. The rate hike itself is well priced in. Thus the focus will be largely on three things, the FOMC statement, new economic projection, and Fed chair Janet Yellen's press conference. Markets are looking through today's hike and are eager to get the hints on what Fed would do next. The table below showed FOMC's median projections back in December.

Federal funds rate are projected to be at 1.4% by the end of 2017, 2.1% by the end of 2018. They equivalent to 3 rate hikes in total for this year and 2-3 hikes next year. Any upward revision to the numbers will imply a faster path. In particular, some analysts are anticipating a meaningful revision to 2018's projections to reflect a firmer chance of 3 hikes. Meanwhile, the markets will also look closely to the revisions to economic projections, with focuses on the core PCE number for this year and next.

More on FOMC:

- Upcoming Rate Hikes And 2018 Median Dot Plot In Focus

- FOMC Preview - It's All in the Dots

- Fed Expected to Raise US Interest Rates

- FOMC Preview: Fed to Maintain Signal of Three Hikes this Year

Sterling rebounds as unemployment rate hit 4 decade low

Sterling recovers notably today after stronger than expected job data. ILO unemployment rate dropped to 4.7% in January, better than expectation of being unchanged at 4.8%. Also, that's the lowest level in more than four decades since mid-1975. Employment rose 92k, and hit the highest level on record. However, was growth was disappointing as average weekly earnings rose 2.2% 3moy slowed from 2.6% 3moy and missed expectation of 2.4% 3moy. Meanwhile, claimant counts dropped -11.3k in February versus expectation of 3.2k rise. Claimant count rate was unchanged at 2.1%.

Strength in the Pound is relatively limited though as markets await FOMC rate decision today and then BoE rate decision tomorrow. At the mean time, traders are still awaiting UK prime minister Theresa May to finally trigger the Article 50 to kick start Brexit negotiation with EU.

Dutch voters heading to election

The Dutch election held today is generally seen as a first gauge of spread of populism into Europe, ahead of elections in France and Germany. There have been voices from right-wing parties in the core of EU calling for anti-EU referendum. Meanwhile, the exact result of the election in the Netherland could be less important than the implications. The fractured political environment will certainly produce no majority in the parliament. And as many as five parties are possibly needed to form a coalition. Also from Europe, Swiss PPI dropped -0.2% mom rose 1.3% yoy in February. Eurozone employment rose 0.3% qoq in Q4.

BoJ watched in Asian session

BoJ monetary policy decisions will be the focus in the coming Asian session. The central bank is widely expected to keep interest rate unchanged at -0.1%. Also, it will maintain the Yield Curve Control framework to guide 10 year yield to around zero. With the YCC, BoJ will likely keep the pace of asset purchase at JPY 80T per annum. The announcement could end as a non-event.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2100; (P) 1.2161; (R1) 1.2213; More...

GBP/USD formed a temporary low again at 1.2108 and recovered. Intraday bias is turned neutral for another round of consolidation. But still, outlook stays bearish as long as 1.2346 support turned resistance holds. As noted before, consolidation pattern from 1.1946 is completed at 1.2705 is resuming larger down trend. Below 1.2108 will target a test on 1.1946/86 support zone. Break of 1.1946 will confirm our bearish view.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Current Account Balance (NZD) Q4 | -2.3B | -2.43B | -4.89B | -5.03B |

| 23:30 | AUD | Westpac Consumer Confidence Mar | 0.10% | 2.30% | ||

| 04:30 | JPY | Industrial Production M/M Jan F | -0.40% | -0.80% | -0.80% | |

| 08:15 | CHF | Producer & Import Prices M/M Feb | -0.20% | 0.40% | 0.40% | |

| 08:15 | CHF | Producer & Import Prices Y/Y Feb | 1.30% | 0.80% | ||

| 09:30 | GBP | Jobless Claims Change Feb | -11.3K | 3.2K | -42.4K | -41.4K |

| 09:30 | GBP | Claimant Count Rate Feb | 2.10% | 2.10% | ||

| 09:30 | GBP | ILO Unemployment Rate (3M) Jan | 4.70% | 4.80% | 4.80% | |

| 09:30 | GBP | Average Weekly Earnings 3M/Y Jan | 2.20% | 2.40% | 2.60% | |

| 10:00 | EUR | Eurozone Employment Q/Q Q4 | 0.30% | 0.20% | 0.20% | |

| 12:30 | USD | Empire State Manufacturing Index Mar | 16.4 | 15 | 18.7 | |

| 12:30 | USD | CPI M/M Feb | 0.10% | 0.00% | 0.60% | |

| 12:30 | USD | CPI Y/Y Feb | 2.70% | 2.60% | 2.50% | |

| 12:30 | USD | CPI Core M/M Feb | 0.20% | 0.20% | 0.30% | |

| 12:30 | USD | CPI Core Y/Y Feb | 2.20% | 2.20% | 2.30% | |

| 12:30 | USD | Advance Retail Sales Feb | 0.10% | -0.10% | 0.40% | 0.60% |

| 12:30 | USD | Retail Sales Less Autos Feb | 0.20% | -0.10% | 0.80% | 1.20% |

| 14:00 | USD | NAHB Housing Market Index Mar | 65 | 65 | ||

| 14:00 | USD | Business Inventories Jan | 0.30% | 0.40% | ||

| 14:30 | USD | Crude Oil Inventories | 3.3M | 8.2M | ||

| 18:00 | USD | FOMC Rate Decision | 1.00% | 0.75% |

Canadian Dollar Quiet Ahead of Fed, US Consumer Data

USD/CAD is almost unchanged in the Wednesday session. Currently, the pair is trading at 1.3450. On the release front, it's a very busy day in the US. Retail sales and CPI indicators are expected to soften in February. Today's highlight is the Federal Reserve policy meeting, with the central bank widely expected to raise the benchmark rate a quarter-point, from 0.50% to 0.75%. There are no Canadian events on the schedule. On Thursday, the US publishes a host of key indicators, led by unemployment claims.

With the markets expecting a quarter-point rate hike on Wednesday, will the currency markets react to a Fed move? Although a rate hike has been priced in by the markets at 93%, there have been disappointments in the past, so a rate move could boost the dollar at the expense of gold. Strong US employment numbers in February have reinforced market speculation that the Fed will raise rates for the first time this year. Nonfarm payrolls sparkled in February, as the indicator jumped to 235 thousand, easily beating the estimate of 196 thousand. Wage growth climbed 2.6% compared to February 2016, while the participation rate edged up to 63.0%, up from 62.9%. These solid job numbers have also provided President Trump with a much-needed boost. Trump is under pressure to present an economic agenda, but the markets won't mind giving him some additional breathing room, with the economy performing so well.

Market Awaits Looming Fed Rate Hike

- Markets bide time ahead of Fed; expected to raise rates

- Netherlands begin voting in election testing anti-establishment mood

- UK Jan wage data misses expectations and below month ago levels

Overnight:

Asia:

- China Premier Li stated that ties between China and US keep moving forward and was optimistic about ties. One-China policy was foundation of China-US relations. Trade war with China would hurt US companies and did not wish for such a scenario. 6.5% GDP target was not low and not easy to meet. China faced "relatively large " employment pressure this year as the number of college graduates would hit record high of 7.95M

Europe:

- EU officials said to consider June 20th meeting to authorize Brexit talks. Considering forcing UK to wait until June for formal terms of Brexit to begin, reducing the time PM May has to negotiate a deal

- Scottish First Min Sturgeon (SNP): Might attempt to join European Free Trade Association (EFTA) instead of staying in EU after vote for independence

- YouGov Times survey showed 57% of Scotland voters want to stay in the UK; 43% want to be independent

- ECB's Nouy (SSM chief): Greece bank situation had noticeably and substantially improved in last two years but NPLs remained a major challenge

- France presidential candidate Fillon reportedly placed under formal investigation over diversion of public finances in relation to jobs for family members investigation (as suspected)

Energy:

- Weekly API Oil Inventories: Crude: -0.5M v +11.6M prior (first draw in 3 weeks)

Economic data

- (FR) France Feb Final CPI EU Harmonized M/M: 0.2% v 0.1%e; Y/Y: 1.4% v 1.4%e, CPI Ex-Tobacco Index: 100.5 v 100.5e

- (CH) Swiss Feb Producer & Import Prices M/M: -0.2% v 0.4%e; Y/Y: 1.3% v 1.8%e

- (IS) Iceland Central Bank (Sedabanki) left its 7-Day Term Deposit Rate at 5.00%

- (UK) Feb Jobless Claims Change: -11.3K v -41.4K prior; Claimant Count Rate: 2.1% v 2.2% prior

- (UK) Jan Average Weekly Earnings 3M/Y: 2.2% v 2.4%e; Weekly Earnings (ex Bonus) 3M/Y: 2.3% v 2.5%e

- (UK) Jan ILO Unemployment Rate 3M/3M: 4.7% v 4.8%e

**Fixed Income Issuance:

- (IN) India sold total INR100B vs. INR100B indicated in 3-month and 12-month Bills

- (DK) Denmark sold total DKK1.26B in 3-month and 6-month Bills

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

**Index snapshot (as of 09:40 GMT)**

Indices [Stoxx50 +0.4% at 3,411, FTSE +0.3% at 7,378, DAX +0.1% at 12,004, CAC-40 +0.2% at 4,985, IBEX-35 +0.7% at 9,970, FTSE MIB +0.7% at 19,667, SMI +0.2% at 8,680, S&P 500 Futures +0.2%]

Market Focal Points/Key Themes: European equity indices are trading higher as market participants await results of the Dutch election as well as the Fed's policy decision due later today; Banking stocks generally higher across the board with the peripheral lender weighted FTSE MIB and IBEX outperforming as a result; Energy, commodity and mining stocks also trading higher as copper and oil prices trade higher intraday; shares of Hikma Pharmaceuticals leading the gains in the FTSE 100 after releasing its FY16 results.

Upcoming scheduled US earnings (pre-market) include Concordia Healthcare, Siteone Landscape Supply, Titan International, and Verso Corp.

Equities (as of 09:30 GMT)

- Consumer Discretionary: [Dufry DUFN.CH +2.6% (FY16 results), Hennes & Mauritz HMB.SE -4.8% (Feb sales), Inditex ITX.ES -1.2% (FY16 results), Robert Walters RWA.UK +3.8% (FY16 results)]

- Consumer Staples: [Sixt SIX2.DE -0.5% (FY16 results)]

- Financials: [Munich Re MUV2.DE -1.6% (outlook, share buyback)]

- Healthcare: [Hikma Pharmaceuticals HIK.UK +7.4% (FY16 results)]

- Industrials: [BASF BAS.DE +0.4% (raises prices globally for antioxidants & light stabilizers by 10%), Polymetal POLY.UK +0.9% (FY16 results)]

- Technology: [Tecan Group TECN.CH -6.9% (FY16 results)]

- Utilities: [Ascopiave ASC.IT +2.0% (FY16 results), E.On EOAN.DE -2.8% (FY16 results, cuts workforce)]

Speakers

- ECB's Praet(Belgium) reiterated Council view that needed to build sufficient confidence that inflation will converge to medium-term target

- UK Brexit Min Davis stated that was expecting Queens approval on Article 50 law (royal assent) on Thursday, Mar 16th. Govt had not done any economic assessment of impact of NOT reaching a Brexit agreement. Could be upside to no deal with EU; not as frightening as people think

- EU's Tusk reiterated view that Euro Area economy is improving. Carefully preparing for Brexit negotiations; would try to keep EU and UK close after Brexit

- EU's Juncker: Unemployment was falling but region was not out of the economic crisis just yet

- Iceland Central Bank stated that it was too early to predict impact of the end of capital controls. To continue to mitigate short-term volatility (**Note: lifter capital controls earlier this week after 8 years)

- BOE Shadow MPC: BoE should prepare the ground for a possible rate hike in the minutes of their next meeting

- Denmark Central Bank raised its 2017 and 2018 GDP growth forecasts

- IEA Mar Monthly Report maintained its 2017 global oil demand growth forecast at 1.4M bpd. Opec production was higher in Feb from 32.06M to 32.0M; compliance of 91% v 90% m/m. OECD oil inventories at 3.03B barrels, +48M barrels (1st rise in six months). It noted that oil market needed time to re-balance as January inventories rise

Currencies

- USD was softer ahead of Fed rate decision where expectations are for another 25bps hike.

- The GBP/USD saw some pre-European action as the pair popped up to test above 1.2250 level. Pair moved off 7-week lows to hit a 1-week high. Dealers saw no news for the move other than buy-stops being elected. One excuse was a report by the Shadow MPC that the BoE should prepare the ground for a possible rate hike in the minutes of their next meeting (tomorrow).

- EUR/USD slightly higher in quiet trade at 1.0630 while USD/JPY was steady in the mid-114 neighborhood.

**Fixed Income:

- Bund futures trade at 159.79 up 24 ticks continuing to bounce from 158.73 lows made yesterday with 2s10s flattening on better demand for longer dated bonds. Continued upside targets 160.20 followed by 160.66. Support lies at yesterday low at 158.73 followed by 158.40.

- Gilt futures trade at 126.39 up 13 ticks trading near highs supported by weaker Avg weekly earnings data out of the UK.. Support moves to 125.75 then 125.57 with further weakness eyeing 125.24. Resistance remains at 126.38 then 126.87 followed by 127.35. Short Sterling futures trade virtually flat across the strp with Jun17Jun18 spread remaining at 17/18bp.

- Wednesday liquidity report showed Tuesday's excess liquidity rose to €1.373T a rise of €2B from €1.371T prior. Use of the marginal lending facility rose to €976M from €620M prior.

- Corporate issuance after a strong start to the week issuance grinding to a halt yesterday as issuers remain sidelined ahead of the FOMC rate meeting this evening. Today is expected to remain quiet ahead of the Fed decision.

Looking Ahead

- (CO) Colombia Feb Consumer Confidence Index: -26.0e v -30.2 prior

- OPEC workshop in Vienna

- 05:50 (EU) ECB allotment in 7-day USD Liquidity Tender at fixed % vs. $915M prior (recd 2 bids)

- 06:00 (EU) Euro Zone Q4 Employment Q/Q: No est v 0.2% prior; Y/Y: No est v 1.2% prior

- 06:00 (ZA) South Africa Q1 Business Confidence: No est v 38 prior

- 06:00 (IT) Italy Feb Final CPI (Including Tobacco) M/M: No est v 0.3% prelim; Y/Y: No est v 1.5% prelim

- 06:00 (IT) Italy Feb Final CPI EU Harmonized M/M: No est v 0.2% prelim; Y/Y: No est v 1.5% prelim, CPI FOI Index Ex Tobacco: No est v 100.6 prior

- 06:00 (EU) Daily Euribor Fixing

- 06:00 (GR) Greece Debt Agency (PDMA) to sell €1.0B in 13-Week Bills

- 06:00 (SE) Sweden to sell Bills - 06:00 (ZA) South Africa announces details of next bond auction (held on Tuesdays)

- 06:30 (DE) Germany to sell €1.0B in 2.5% Aug 2046 Bunds

- 06:30 (PT) Portugal Debt Agency (IGCP) to sell €1.0-1.5B in 6-month and 12-month Bills

- 07:00 (US) MBA Mortgage Applications w/e Mar 10th: No est v 3.3% prior

- 07:00 (BR) Brazil Mar FGV Inflation IGP-10 M/M: 0.2%e v 0.1% prior

- 07:00 (ZA) South Africa Jan Retail Sales M/M: +0.2%e v -2.3% prior; Y/Y: 1.1%e v 0.9% prior

- 07:00 (IE) Ireland Feb CPI M/M: No est -0.5% prior; Y/Y: No est v 0.3% prior

- 07:00 (IE) Ireland Feb CPI EU Harmonized M/M: +0.5%e -0.5% prior; Y/Y: 0.4%e v 0.2% prior

- 07:00 (RU) Russia to sell combined RUB45B in 2022 and 2033 OFZ bonds

- 07:45 (US) Daily Libor Fixing

- 08:00 (UK) PM May weekly question time in House of Commons

- 08:00 (FI) Finland govt responds to no-confidence motions

- 08:30 (US) Mar Empire Manufacturing: 15.0e v 18.7 prior

- 08:30 (US) Feb CPI M/M: 0.0%e v 0.6% prior; Y/Y: 2.7%e v 2.5% prior

- 08:30 (US) CPI Ex Food and Energy M/M: 0.2%e v 0.3% prior; Y/Y: 2.2%e v 2.3% prior

- 08:30 (US) Feb CPI Index NSA: 243.416e v 242.839 prior; CPI Core Index SA: 251.155e v 250.783 prior

- 08:30 (US) Feb Advance Retail Sales M/M: 0.1%e v 0.4% prior; Retail Sales Ex Auto M/M: 0.1%e v 0.8% prior, Retail Sales Ex Auto and Gas: 0.2%e v 0.7% prior, Retail Sales Control Group: 0.2%e v 0.4% prior

- 08:30 (US) Feb Real Avg Weekly Earnings Y/Y: No est v -0.5% prior (revised from -0.6%), Real Avg Hourly Earning Y/Y: No est v 0.1% prior (revised from 0.0%)

- 09:00 (US) The Federal Open Market Committee (FOMC) begins final day of policy meeting

- 09:00 (HU) Hungary Central Bank (NBH) Feb Minutes

- 09:00 (PL) Poland Feb CPI Core M/M: 0.1%e v 0.1% prior; Y/Y: 0.4%e v 0.0% prior

- 09:00 (CA) Canada Feb Existing Home Sales M/M: No est v -1.3% prior

- 09:15 (UK) Baltic Dry Bulk Index - 09:45 (IT) ECB's Visco in Milan

- 10:00 (US) Mar NAHB Housing Market Index: 65e v 65 prior

- 10:00 (US) Jan Business Inventories: 0.3%e v 0.4% prior

- 10:00 (BE) Belgium Jan Trade Balance: No est v €0.1B prior

- 10:30 (US) Weekly DOE Crude Oil Inventories

- 10:50 (UK) BoE conducts reverse Gilt auction (7-15 years)

- 11:00 (PE) Peru Feb Unemployment Rate: 7.5%e v 7.2% prior

- 11:00 (PE) Peru Jan Economic Activity Index (Monthly GDP) Y/Y: 4.5%e v 3.2% prior (revised from 3.3%)

- 12:00 (NG) Nigeria to sell 2021, 2027 and 2036 Bonds

- 12:30 (IL) Israel Feb CPI M/M: -0.2%e v -0.2% prior; Y/Y: 0.2%e v 0.1% prior

- 14:00 (US) FOMC Interest Rate Decision: Expected to Raise Fed Funds Target Range to 0.75-1.00%

- 16:00 (US) Jan Total Net TIC Flows: No est v -$42.8B prior; Net Long-term TIC Flows: No est v -$12.9B prior